India Peptide Synthesis Market Size, Share, Trends and Forecast by Product, Technology, Application, End Use, and Region, 2026-2034

India Peptide Synthesis Market Summary:

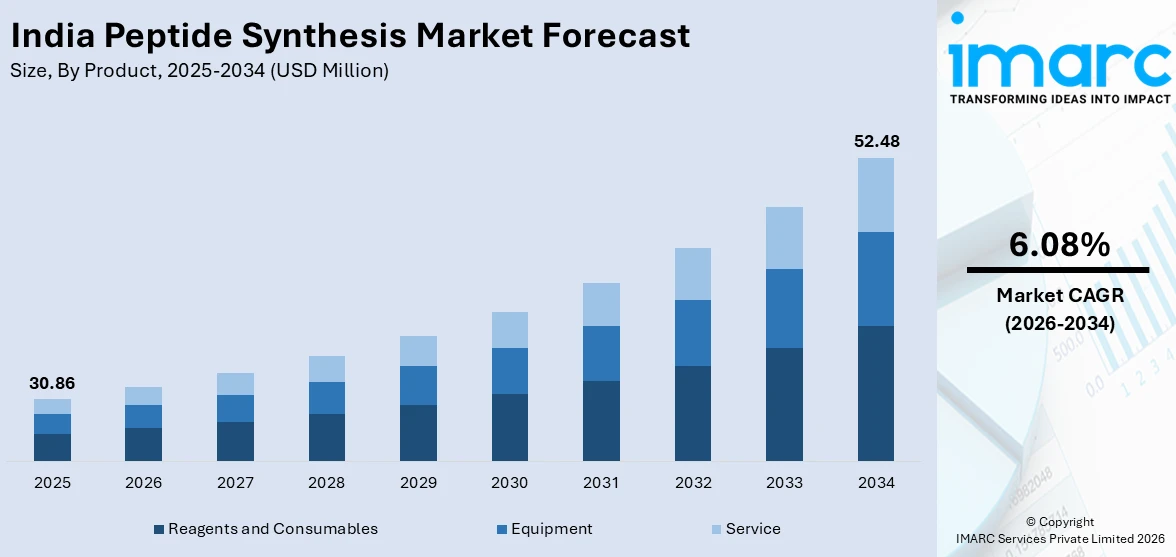

The India peptide synthesis market size reached USD 30.86 Million in 2025. The market is projected to reach USD 52.48 Million by 2034, growing at a CAGR of 6.08% during 2026-2034. The market is driven by government support through the Production-Linked Incentive scheme, strengthening domestic API manufacturing infrastructure, rapid expansion of CRDMO capabilities with state-of-the-art peptide synthesis facilities, and rising demand for complex peptide therapeutics, including GLP-1 receptor agonists for diabetes and obesity treatment. These factors are collectively expanding the India peptide synthesis market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Market Size in 2025 | USD 30.86 Million |

| Market Forecast in 2034 | USD 52.48 Million |

| Market Growth Rate (2026-2034) | 6.08% |

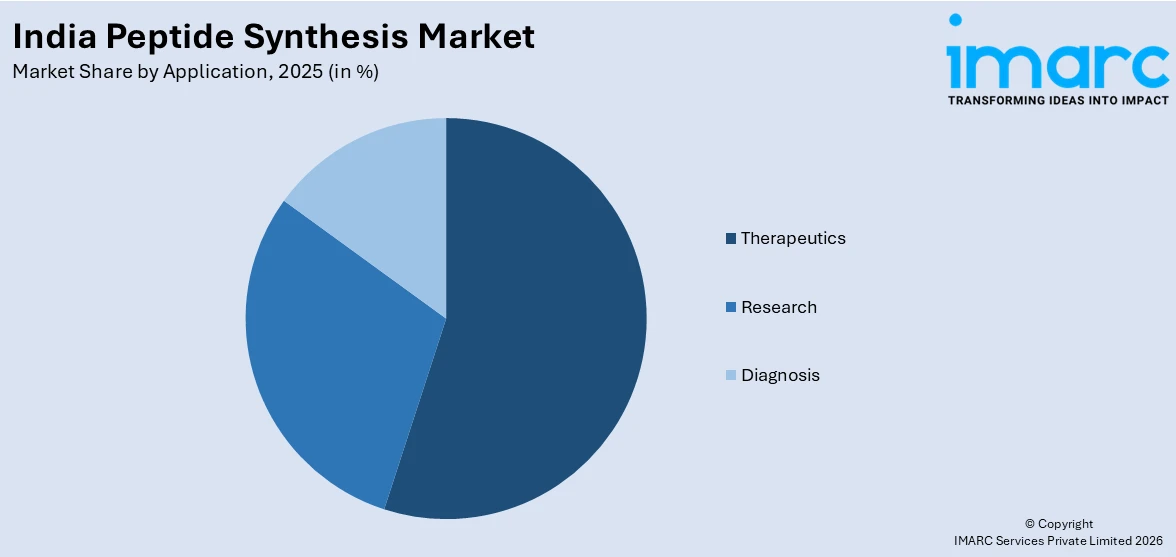

| Key Segments | Product (Reagents and Consumables (Resins, Amino Acids, Coupling Reagents, Dyes and Fluorescent Labeling Reagents, Others), Equipment (Peptide Synthesizers, Chromatography Equipment, Lyophilizers, Others), Service), Technology (Liquid Phase Peptide Synthesis (LPPS), Solid Phase Peptide Synthesis (SPPS), Hybrid Technology), Application (Therapeutics (Cancer, Metabolic, Cardiovascular Disorder, Infectious Diseases, CNS, Gastrointestinal Disorders (GIT), Pain, Respiratory, Dermatology, Renal Disorders, Others), Research, Diagnosis), End Use (Pharmaceutical and Biotechnology Companies, CDMOs and CROs, Academic and Research Institutes), and Region (North India, South India, East India, West India) |

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

India Peptide Synthesis Market Outlook (2026-2034):

The India peptide synthesis market is poised for robust growth, underpinned by strategic government initiatives reducing import dependence, expanding CRDMO infrastructure with advanced automation and robotics, and the global surge in peptide-based therapeutic development. Increasing investments in specialized peptide research centers, strategic acquisitions bringing international expertise to Indian shores, and the growing adoption of artificial intelligence in peptide drug discovery will further accelerate market expansion. Additionally, India's cost-competitive manufacturing capabilities, skilled scientific workforce, and regulatory alignment with global standards position the country as an attractive destination for peptide synthesis outsourcing throughout the forecast period.

To get more information on this market Request Sample

Impact of AI:

Artificial intelligence is transforming peptide drug discovery by enabling rapid identification of therapeutic candidates through computational modeling and machine learning algorithms. AI-powered platforms accelerate the screening of vast peptide sequence libraries in silico, predict bioactivity and toxicity profiles, and optimize synthesis parameters, significantly reducing development timelines and costs. As these technologies mature, AI integration in peptide synthesis is expected to enhance India's competitive advantage by improving process efficiency, enabling novel peptide design, and facilitating faster clinical translation of peptide-based therapeutics.

Market Dynamics:

Key Market Trends & Growth Drivers:

Government-Led Production-Linked Incentive Scheme Strengthening Domestic API Infrastructure

India’s Production-Linked Incentive (PLI) scheme represents a strategic effort to reduce dependence on pharmaceutical imports and strengthen domestic manufacturing capabilities. Launched in 2020 with an initial allocation of around INR 6,940 crore (USD 850 million) for key bulk drugs, it is part of the broader InNR 15,000 crore PLI program for the pharmaceutical sector. The scheme provides performance-linked financial incentives to manufacturers based on incremental domestic sales of selected pharmaceutical products over six years, targeting critical bulk drugs, active pharmaceutical ingredients (APIs), and intermediates where import dependence—particularly on China—was highest. By March 2025, the initiative had enabled large-scale domestic production of 38 essential APIs, including Penicillin G, Clavulanic Acid, Atorvastatin, and Metformin, covering roughly 67% of previously highly imported APIs. Complementary measures include approvals for bulk drug parks in Himachal Pradesh, Gujarat, and Andhra Pradesh with a budget of INR 3,000 crore to develop shared infrastructure, and raising the foreign direct investment limit to 100% for Greenfield projects. These coordinated policies create a favorable environment for peptide synthesis companies, offering financial support during capital-intensive setup phases and enabling investments in advanced equipment, clean rooms, and quality control systems, positioning India as a growing hub for complex molecule manufacturing. This government support is accelerating the India peptide synthesis market growth by reducing barriers to entry, encouraging innovation in synthesis technologies, and positioning Indian manufacturers to capture growing global demand for peptide-based therapeutics, particularly in the lucrative anti-diabetic and anti-obesity segments.

Rapid Expansion of CRDMO and CDMO Capabilities with Advanced Peptide Synthesis Infrastructure

The Indian pharmaceutical sector is rapidly evolving, with companies increasingly investing in Contract Research, Development, and Manufacturing Organization (CRDMO) capacities focused on peptide synthesis. This reflects a strategic move toward high-value, complex therapeutics that offer premium pricing and superior margins compared to traditional small-molecule APIs. Leading firms are establishing advanced peptide research and manufacturing centers equipped with automation, robotics, high-throughput platforms, and sophisticated liquid-handling systems, enhancing precision, scalability, and efficiency. In April 2025, Sai Life Sciences inaugurated a dedicated Peptide Research Center in Hyderabad, providing comprehensive support for peptide synthesis, discovery, and complex modalities, streamlining drug discovery timelines and improving success rates. Building on this, the company broke ground in October 2025 on a 100,000-square-foot CMC Process R&D Center, featuring specialized peptide and oligo labs, 140 process chemistry fume hoods, a 25,000-square-foot analytical lab, and NCE formulation capabilities, doubling existing process R&D capacity. These investments highlight peptides’ growing appeal across oncology, metabolic, cardiovascular, and infectious disease therapeutics due to their specificity, biocompatibility, and lower off-target risk. Strategic acquisitions and technology transfers further accelerate India’s CRDMO capabilities, positioning the country as a globally competitive, cost-effective hub for high-quality peptide manufacturing.

Surging Global Demand for Peptide Therapeutics Driving Market Opportunities

The global pharmaceutical market is experiencing a surge in peptide-based therapeutics, presenting significant opportunities for India’s peptide synthesis industry. Peptides, short chains of amino acids, have gained prominence due to their diverse biological activities, including antimicrobial, antitumor, and hormonal signaling functions. The diabetes and obesity segment has emerged as a key growth driver, with GLP-1 receptor agonists such as semaglutide and tirzepatide achieving blockbuster status, fueling strong demand for peptide manufacturing capabilities. In April 2025, Granules India acquired Switzerland-based Senn Chemicals AG for CHF 20 million (INR 192.5 crore), gaining expertise in both liquid-phase and solid-phase peptide synthesis and access to an established international customer base. Collaborative development efforts are already underway, focusing on GLP-1 receptor agonists and expanding to a broader pipeline of peptide APIs. Peptides’ therapeutic potential extends to oncology, where they function as targeted drug delivery agents, cardiovascular treatments through modulation of complex signaling pathways, and antimicrobial applications addressing rising antibiotic resistance. With over 80 globally approved peptide therapeutics and more than 630 ongoing clinical trials since 2015, demand for peptide synthesis spans early research to commercial manufacturing. India’s technical expertise, cost advantages, and growing CRDMO infrastructure position domestic manufacturers to capture a significant share of this expanding global market.

Key Market Challenges:

Complex Regulatory Compliance and Stringent Quality Control Requirements

Peptide synthesis is subject to exceptionally strict regulatory oversight from agencies such as the US FDA, EMA, and India’s CDSCO, posing major compliance challenges that increase operational costs and extend development timelines. Establishing robust quality control protocols for peptide APIs requires extensive testing, including impurity profiling, amino acid analysis, moisture and microbiological testing, and high-molecular-weight impurity detection. Each manufacturing step must be precisely characterized to minimize batch-to-batch variation, as peptide synthesis is highly sensitive to process parameters like temperature, pH, and reaction efficiency. Regulatory authorities have intensified scrutiny of starting materials, resins, amino acids, coupling reagents, solvents, requiring full documentation and validation at every stage. Incomplete chemical reactions and side-chain protection steps often generate closely related impurities, demanding advanced analytical methods to detect and quantify even trace levels. Maintaining impurity levels below 0.1% is technically difficult and financially burdensome, particularly for complex long-chain peptides. Achieving Good Manufacturing Practice compliance necessitates heavy investment in cleanroom infrastructure, validated analytical equipment, trained personnel, and continuous audits. Recent US FDA warning letters to Indian facilities highlight persistent data-integrity and contamination issues, while new GMP deadlines and ICH Q12 implementation further elevate compliance costs and may trigger industry consolidation.

Persistent Import Dependence for Critical Raw Materials and Supply Chain Vulnerabilities

Despite India’s dominant position as a global generic medicine supplier, its peptide synthesis segment remains heavily dependent on imported raw materials. The country continues to rely on China for most active pharmaceutical ingredients and peptide starting materials, including specialized amino acids, protected derivatives, resins, and high-purity coupling reagents. This dependence exposes manufacturers to severe supply chain vulnerabilities, as seen during the COVID-19 pandemic when disruptions led to global drug shortages. Price volatility in fermentation inputs and intermediates also threatens profitability, compressing margins amid rising material costs. Quality and consistency of imported materials are critical, as minor variations can significantly affect peptide purity and yield. Moreover, limited global suppliers of specialized reagents create bottlenecks and weaken Indian firms’ negotiating positions. Supply chain risks further extend to compliance issues, logistics delays, and cold-chain requirements for temperature-sensitive reagents. While government initiatives like the Production Linked Incentive scheme and bulk drug parks aim to promote domestic manufacturing of key intermediates, achieving full backward integration will require sustained investment and technological capability development. Until then, Indian peptide manufacturers remain vulnerable to supply disruptions, price fluctuations, and quality inconsistencies across international supply networks.

Shortage of Specialized Skilled Workforce and Technical Expertise Gaps

The peptide synthesis industry in India faces a severe shortage of specialized professionals skilled in complex organic chemistry, peptide coupling reactions, chromatographic purification, and analytical characterization. Manufacturing peptides demands precise control at every synthesis stage, from amino acid coupling to deprotection and purification, requiring deep understanding of reaction dynamics and experience with automated synthesizers and chromatographic systems. However, the current talent pool lacks sufficient expertise, particularly in analytical quality control, an area flagged by the National Skill Development Corporation as critically understaffed. This shortage contributes to regulatory non-compliance, as evidenced by US FDA warnings citing data-integrity and contamination lapses often linked to inadequate operator training. Analytical characterization of peptides, involving HPLC, mass spectrometry, NMR, and peptide mapping, requires operators with advanced technical proficiency and regulatory awareness. The gap between academic education and industry requirements remains wide, forcing companies to invest heavily in on-the-job training, slowing scale-up and diverting skilled staff to mentoring roles. Competition for limited expertise inflates labor costs, eroding India’s traditional cost advantage in pharmaceutical manufacturing. Building a sustainable peptide ecosystem will require systematic curriculum upgrades, hands-on training programs, and stronger academia-industry collaboration.

India Peptide Synthesis Market Report Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India peptide synthesis market, along with forecasts at the country and regional levels for 2026-2034. The market has been categorized based on product, technology, application, and end use.

Analysis by Product:

- Reagents and Consumables

- Resins

- Amino Acids

- Coupling Reagents

- Dyes and Fluorescent Labeling Reagents

- Others

- Equipment

- Peptide Synthesizers

- Chromatography Equipment

- Lyophilizers

- Others

- Service

The report has provided a detailed breakup and analysis of the market based on the product. This includes reagents and consumables (resins, amino acids, coupling reagents, dyes and fluorescent labeling reagents, and others), equipment (peptide synthesizers, chromatography equipment, lyophilizers, and others), and service.

Analysis by Technology:

- Liquid Phase Peptide Synthesis (LPPS)

- Solid Phase Peptide Synthesis (SPPS)

- Hybrid Technology

A detailed breakup and analysis of the market based on the technology have also been provided in the report. This includes liquid phase peptide synthesis (LPPS), solid phase peptide synthesis (SPPS), and hybrid technology.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Therapeutics

- Cancer

- Metabolic

- Cardiovascular Disorder

- Infectious Diseases

- CNS

- Gastrointestinal Disorders (GIT)

- Pain

- Respiratory

- Dermatology

- Renal Disorders

- Others

- Research

- Diagnosis

The report has provided a detailed breakup and analysis of the market based on the application. This includes therapeutics (cancer, metabolic, cardiovascular disorder, infectious diseases, CNS, gastrointestinal disorders (GIT), pain, respiratory, dermatology, renal disorders, and others), research, and diagnosis.

Analysis by End Use:

- Pharmaceutical and Biotechnology Companies

- CDMOs and CROs

- Academic and Research Institutes

A detailed breakup and analysis of the market based on the end use have also been provided in the report. This includes pharmaceutical and biotechnology companies, CDMOs and CROs, and academic and research institutes.

Analysis by Region:

- North India

- South India

- East India

- West India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The India peptide synthesis market exhibits a moderately competitive landscape characterized by a mix of established domestic pharmaceutical companies expanding into peptide synthesis, specialized contract research and manufacturing organizations focusing exclusively on peptides, and international peptide manufacturers establishing or expanding Indian operations. Competition primarily revolves around technical capabilities in complex peptide synthesis, quality and regulatory compliance track records, production scale and capacity, turnaround times for development and manufacturing, and pricing competitiveness. Key players are increasingly pursuing vertical integration strategies to control critical aspects of the value chain from raw material sourcing through final purification and analytical testing. The market is witnessing consolidation through strategic acquisitions as domestic companies seek to rapidly acquire peptide synthesis expertise and international companies aim to establish cost-competitive manufacturing footprints in India. Differentiation strategies emphasize specialized capabilities in challenging peptide sequences, proprietary technologies for difficult couplings or purifications, experience with specific therapeutic classes, and established relationships with innovator pharmaceutical companies.

India Peptide Synthesis Industry Latest Developments:

- October 2025: PolyPeptide Group announced a significant capacity expansion investment at its Ambernath facility in India, transforming it into a larger and more diversified site. This expansion represents part of PolyPeptide's strategic growth initiative to strengthen its global peptide manufacturing network and meet increasing demand for peptide-based therapeutics. The Ambernath facility operates as one of PolyPeptide's six GMP-certified facilities globally, serving clients across pharmaceutical, cosmetics, and theragnostic industries.

India Peptide Synthesis Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Technologies Covered | Liquid Phase Peptide Synthesis (LPPS), Solid Phase Peptide Synthesis (SPPS), Hybrid Technology |

| Applications Covered |

|

| End Uses Covered | Pharmaceutical and Biotechnology Companies, CDMOs and CROs, Academic and Research Institutes |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India peptide synthesis market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India peptide synthesis market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India peptide synthesis industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Peptide Synthesis Market Report

The India peptide synthesis market reached a value of USD 30.86 Million in 2025.

The market is projected to grow at a CAGR of 6.08% during 2026-2034, reaching USD 52.48 Million by 2034.

Key growth drivers include government PLI scheme incentives, CRDMO infrastructure expansion, rising demand for GLP-1 receptor agonist therapeutics, and cost-competitive domestic manufacturing capabilities.

The report covers segmentation by product, technology, application, end use, and region. Each segment includes detailed market size and forecast analysis.

Key trends include AI-assisted peptide drug discovery, strategic international acquisitions, expanded automation in synthesis facilities, and rising oncology and metabolic therapeutic pipeline activity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)