India Pet Food Market Size, Share, Trends and Forecast by Pet Type, Product Type, Pricing Type, Ingredient Type, Distribution Channel, and Region, 2026-2034

India Pet Food Market Size, Share, Trends & Forecast (2026-2034)

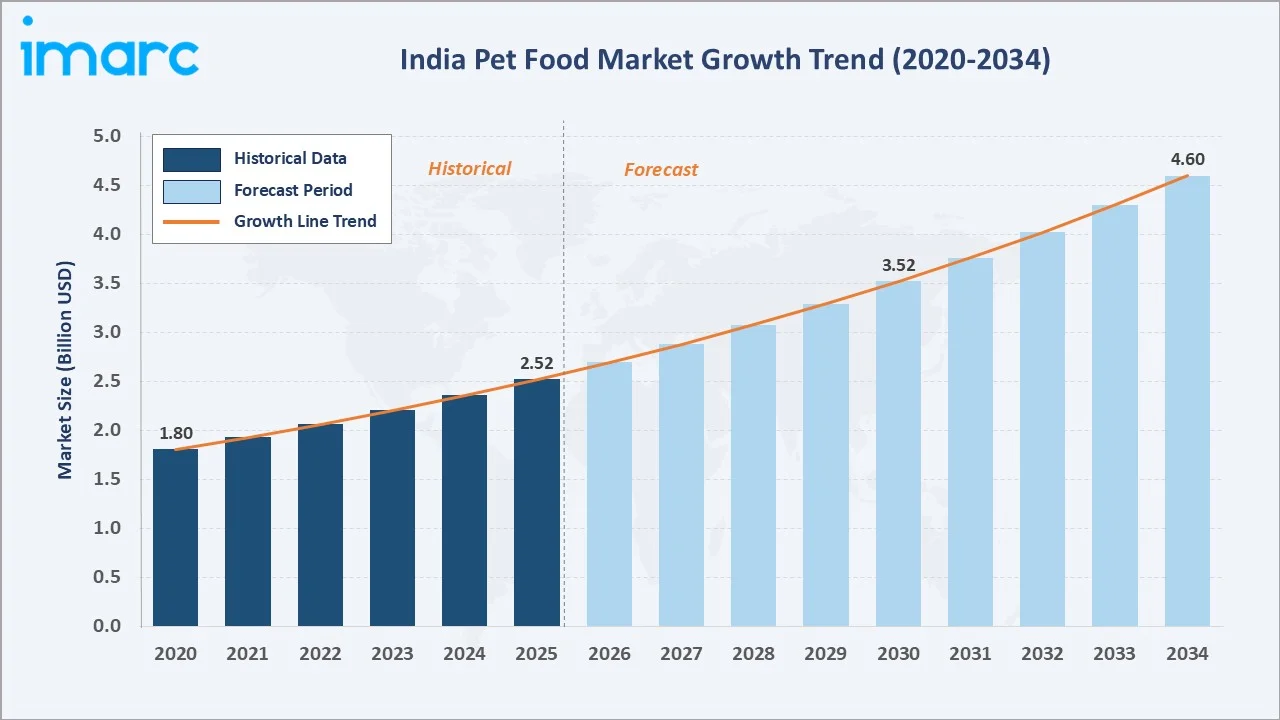

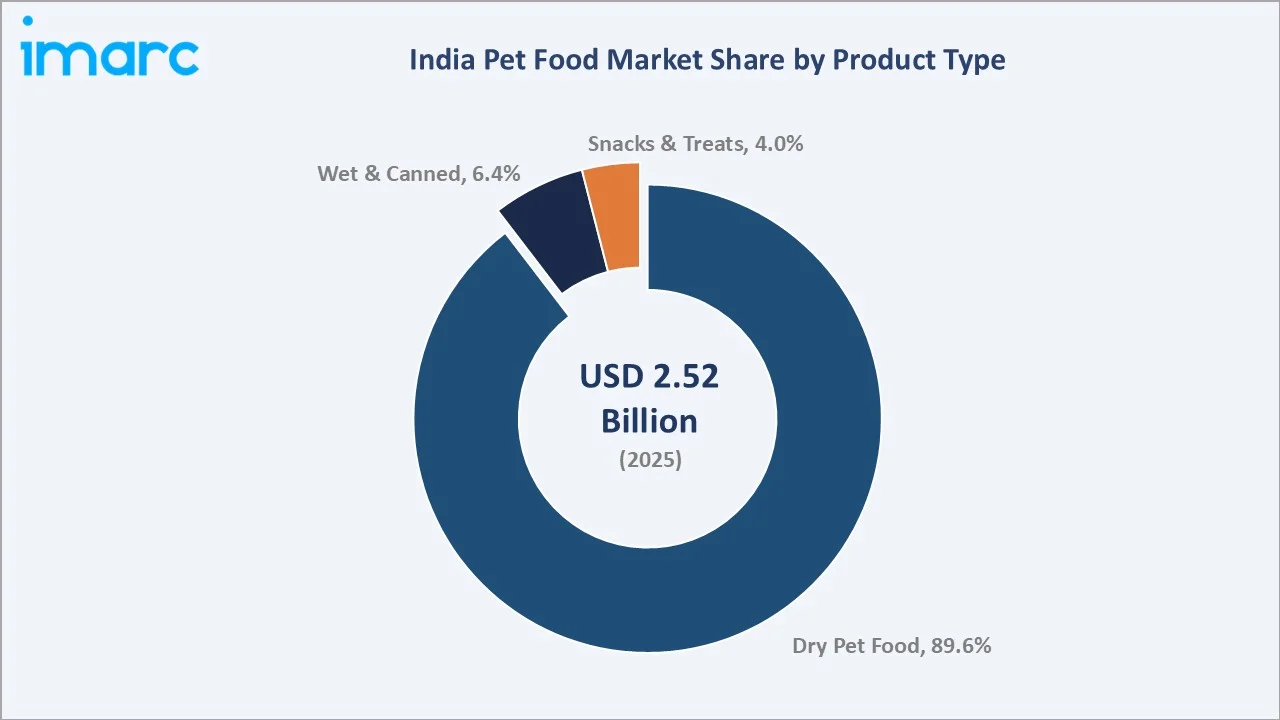

The India pet food market reached USD 2.52 Billion in 2025 and is projected to reach USD 4.60 Billion by 2034, growing at a CAGR of 6.91% during 2026-2034. Rising pet humanization, rapid urban pet ownership expansion, growing awareness of scientifically formulated nutrition, and the proliferation of e-commerce pet retail platforms are the primary growth catalysts driving sustained market expansion across India's diverse geography.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.52 Billion |

|

Forecast Market Size (2034) |

USD 4.60 Billion |

|

CAGR (2026-2034) |

6.91% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

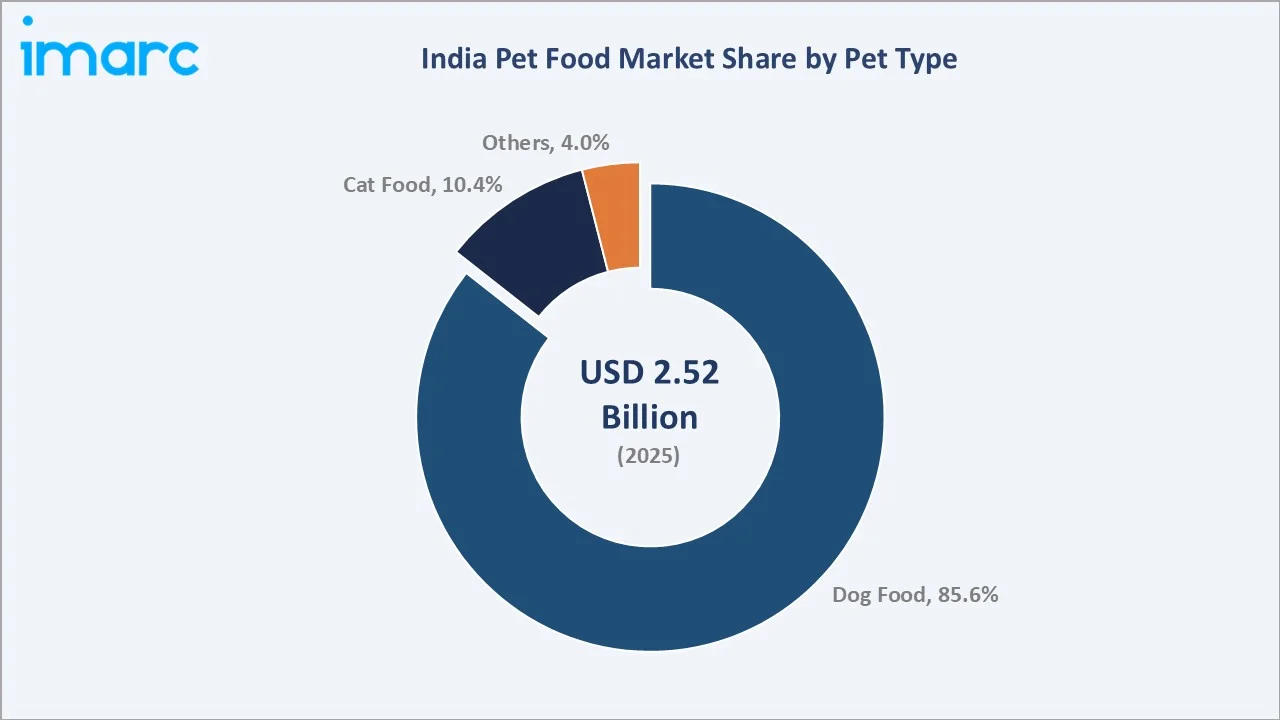

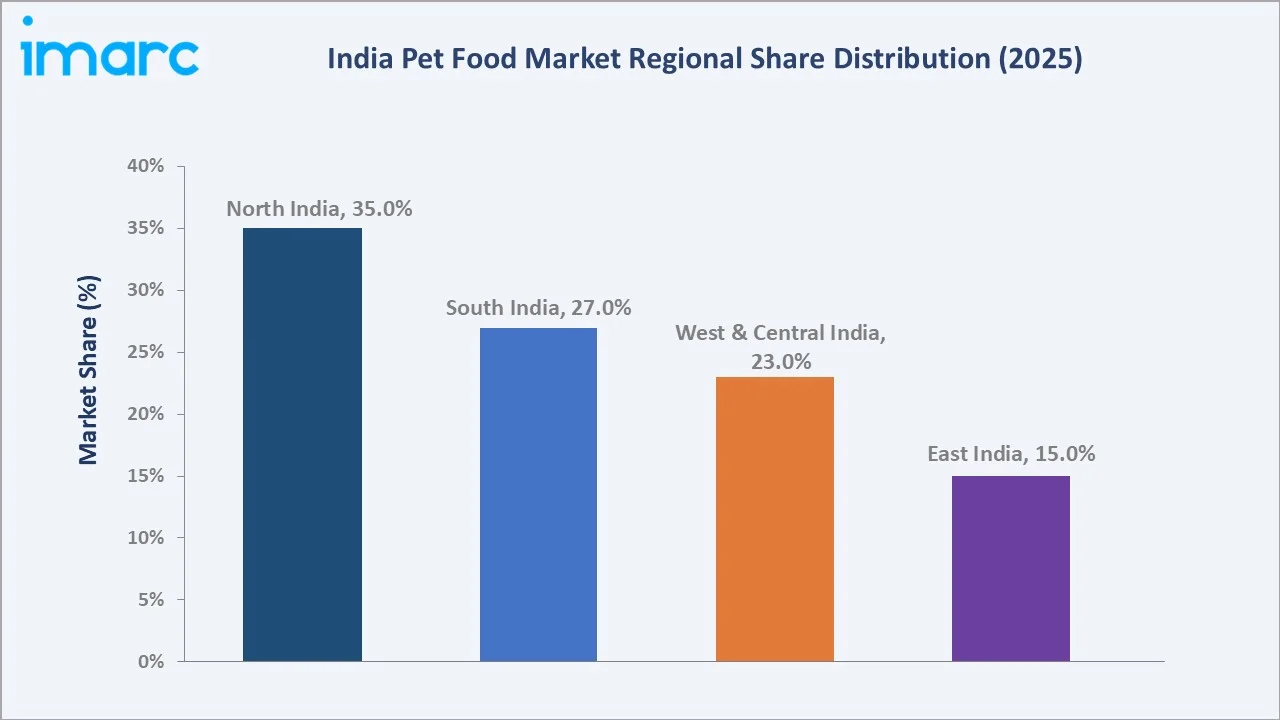

North India leads regionally with a 35.0% market share in 2025, anchored by Delhi-NCR's premium pet ownership concentration. Dog food dominates at 85.6%, reflecting India's overwhelming preference for canine companions. Dry pet food commands an 89.6% share, driven by convenience, shelf stability, and cost efficiency across all pet owner segments.

To get more information on this market, Request Sample

India's pet food market demonstrates consistent compounding growth from USD 1.80 Billion in 2020 to USD 2.52 Billion in 2025, underpinned by three structural forces: the post-COVID surge in pet adoption, the premiumization of pet nutrition driven by millennial and Gen-Z pet owners, and India's expanding organized pet retail infrastructure crossing 5,000+ dedicated pet stores.

Executive Summary

India's pet food market is expanding at a steady 6.91% CAGR, supported by rising disposable incomes, a deepening pet humanization culture, and the rapid scaling of e-commerce pet nutrition platforms. The market grew from USD 1.80 Billion in 2020 to USD 2.52 Billion in 2025 and is forecast to reach USD 4.60 Billion by 2034, adding USD 2.08 Billion in incremental value over the forecast period.

Dog food retains the dominant pet type share at 85.6% in 2025, as India's estimated 31–37 million pet dogs represent the largest pet cohort nationally. Cat food at 10.4% is the fastest-growing pet type as urban apartment living accelerates cat adoption. Dry pet food commands 89.6% of the product type segment, reflecting its price competitiveness versus wet alternatives and the dominant kibble purchasing behavior across Tier-1 and Tier-2 cities.

North India leads regionally at 35.0%, while South India (27.0%) benefits from the Bengaluru-Hyderabad tech corridor pet ownership boom. Key players, including Mars, Incorporated, Nestlé S.A., Colgate-Palmolive Company, IB Group, and Farmina Pet Foods, are scaling premium and mid-tier portfolios to capture India's diverse demand spectrum.

Key Market Insights

|

Insight |

Data |

|

Largest Pet Type |

Dog Food – 85.6% share (2025) |

|

Fastest Growing Pet Type |

Cat Food – ~8.2% CAGR (2026-2034) |

|

Largest Product Type |

Dry Pet Food – 89.6% share (2025) |

|

Fastest Growing Product Type |

Snacks and Treats – ~9.2% CAGR (2026-2034) |

|

Leading Region |

North India – 35.0% share (2025) |

|

Top Companies |

Mars, Incorporated, Nestlé S.A., Colgate-Palmolive Company, IB Group, Farmina Pet Foods |

Key Analytical Observations Supporting the Above Data:

- Dog Food at 85.6% (2025) dominates owing to India's estimated 31–37 million pet dog population. The canine segment benefits from deep brand loyalty to Pedigree and Royal Canin, vet-driven prescription diet recommendations, and the expanding mid-premium kibble segment targeting nutrition-aware pet owners in urban India.

- Dry pet food at 89.6% (2025) reflects the affordability advantage over wet and canned alternatives, with 1 kg packs retailing at INR 300–900 across modern trade and e-commerce. Kibble's ambient storage compatibility with Indian household conditions reinforces its structural dominance through 2034.

- North India's 35.0% (2025) regional share is supported by high pet adoption across Delhi NCR, Chandigarh, Jaipur, Lucknow, and other urban centers. Rising disposable incomes, growing awareness of balanced pet nutrition, and the shift from homemade meals to packaged dry food, wet food, treats, and functional diets are driving demand.

- Snacks and Treats at ~9.2% CAGR are the fastest-growing product type, driven by the human-to-pet treat-giving behavior and rising e-commerce discovery of functional treats addressing joint health, dental care, and coat nutrition, particularly for the growing senior dog population in urban India.

- The overall market's 6.91% CAGR through 2034 is underpinned by India's pet food market penetration rate of 10-20% of all pet-owning households, creating a substantial conversion opportunity as disposable income growth and brand awareness drive a shift from home-cooked to commercial pet nutrition.

India Pet Food Market Overview

Pet food encompasses dry food (kibble), wet and canned food, and snacks and treats formulated to meet the complete nutritional requirements of companion animals, including dogs, cats, and others. India's market spans mass-market dry kibble, premium and super-premium grain-free formulations, veterinary prescription diets, and functional treats, distributed through 5,000+ pet specialty stores, veterinary clinics, modern trade, and India's rapidly growing e-commerce pet category, exceeding INR 2,000 crore annually.

India's pet food market has undergone a fundamental transformation since Pedigree's entry in the 1990s, with approximately 600,000 pets adopted in 2023, including the majority of first-time pet owners, leading to first-time buyers of commercial pet nutrition. The FSSAI regulations and subsequent amendments are driving formulation standardization, quality certification investment, and import tariff structuring that collectively shape the competitive landscape through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

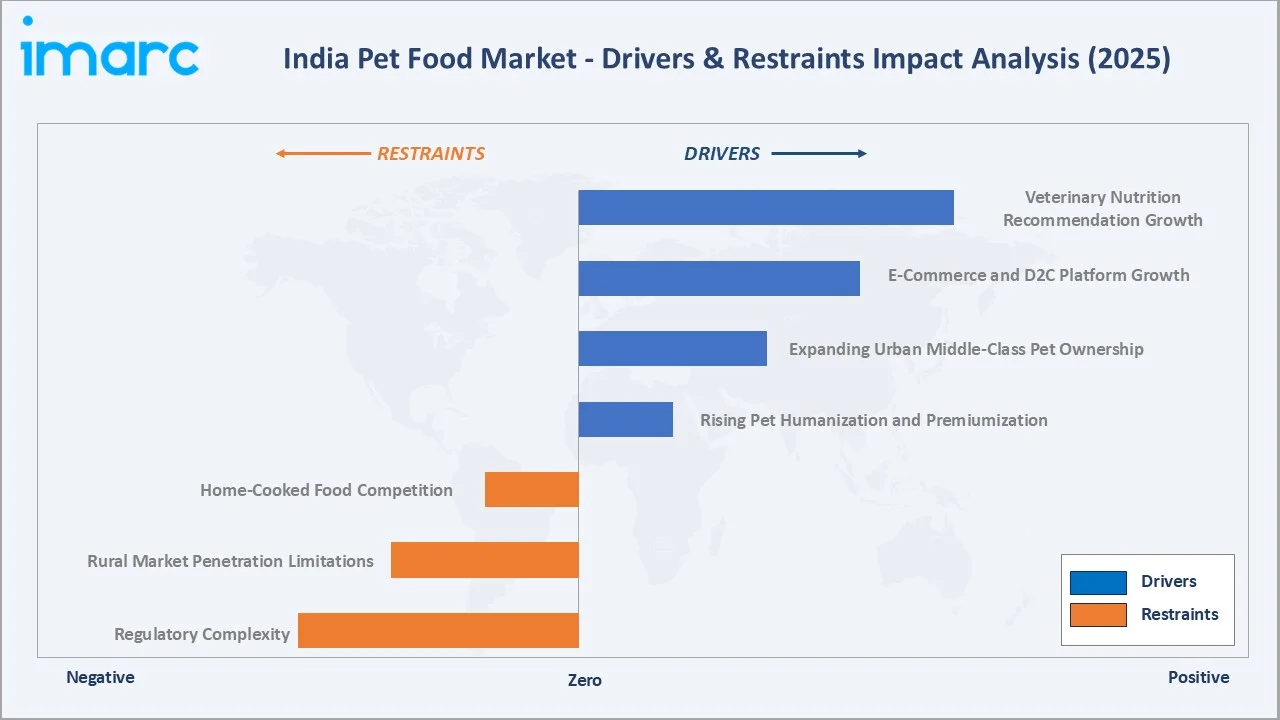

Market Drivers

- Rising Pet Humanization and Premiumization: India's urban pet owners increasingly treat pets as family members, driving demand for human-grade ingredient formulations, grain-free diets, and breed-specific nutrition. The Indian pet care market crossed USD 3.6 Billion in 2024, with pet food representing the largest category.

- Expanding Urban Middle-Class Pet Ownership: The World Bank projects that by 2036, India’s urban population will reach 600 million, representing 40% of the country’s total population. This will lead to first-generation urban households adopting pets at an accelerating rate. Social media communities, including Indian Pet Parents and YouTube pet care channels, are normalizing commercial pet food over home-cooked meals among new pet owners.

- E-Commerce and D2C Platform Growth: Online pet food sales are expected to grow at approximately 40%+ CAGR between 2026 and 2034. Moreover, Heads Up For Tails is targeting a 10% share of the Indian pet care market by FY25 and aims to grow into an INR 500 crore brand by 2026. Subscription-based pet food delivery is extending repeat purchase frequency.

- Veterinary Nutrition Recommendation Growth: India's 87,000 registered veterinarians increasingly recommend prescription diets and therapeutic nutrition for diabetes, kidney disease, obesity, and allergies. Hill's Science Diet and Royal Canin's Veterinary range benefit from vet-channel dominance that creates durable brand loyalty beyond the initial prescription period.

Market Restraints

- Home-Cooked Food Competition: An estimated 60–70% of India's pet-owning households still feed home-cooked rice, meat, and vegetables as primary nutrition. Cultural preference for fresh, home-prepared food represents the primary conversion barrier for commercial pet food brands, requiring sustained nutritional education investment.

- Rural Market Penetration Limitations: Organized pet food retail infrastructure is concentrated in Tier-1 and Tier-2 cities. India's 6.65 lakh rural villages have near-zero organized pet food penetration, with awareness and distribution gaps limiting addressable market expansion to urban geographies.

- Regulatory Complexity: FSSAI pet food regulations, ongoing BIS certification requirements, and state-level veterinary drug licensing for prescription diets create compliance costs that disproportionately burden domestic small and medium manufacturers, slowing innovation in the functional and therapeutic nutrition segments.

Market Opportunities

- Cat Food Premiumization: India's cat population is growing at 15%+ annually as urban apartment living drives cat adoption. Cat food at 10.4% of the market remains underpenetrated relative to global benchmarks, representing a USD 400+ Million expansion opportunity by 2034.

- Functional and Therapeutic Nutrition: India's aging pet population is creating demand for joint health, cognitive support, and weight management formulations. Hill's Prescription Diet and Royal Canin Veterinary are scaling India-specific therapeutic ranges for the growing chronic disease management segment.

Market Challenges

- Price Sensitivity and Mass-Market Margin Pressure: Government institutional channels procure at L1 pricing, compressing margins for mass-market brands. Price-elastic Tier-2 and Tier-3 consumers remain sensitive to premium price differentials, limiting mid-tier product adoption velocity.

- Cold-Chain Infrastructure for Wet Food: Wet and canned pet food requires refrigerated distribution, which is limited outside major metros. Without cold-chain expansion, the wet and canned pet food segment (6.4%) will remain constrained to urban modern trade channels despite international benchmarks showing 20–30% wet food penetration.

Emerging Market Trends

1. Super-Premium and Functional Pet Food Adoption

Health and wellness are becoming key drivers in premium pet food, with owners increasingly seeking products featuring functional, health-related claims like 'natural' and 'high protein,' with ingredients that mirror human nutrition trends. This shift toward nutrition‑focused formulations reflects pet owners’ desire for foods that support preventive care and overall well‑being.

2. Indian Pet Food Startup Secures Funding for Growth

India’s pet food startup Zoomies has raised around INR 50 million (about USD 550,000) in pre‑seed funding to scale its clean‑label, direct‑to‑consumer pet food brand and expand its product offerings for cats and dogs. The investment will support broader market reach, stronger supply chains, and increased distribution as the company taps into growing trust and demand for transparent, high‑quality pet nutrition in India.

3. Cat Food Market Acceleration

In April 2026, Royal Canin, a subsidiary brand of Mars, Incorporated, introduced Fussy Cat, a dry food in India formulated with high protein (≈40%) and enhanced palatability to address selective eating behavior in cats. The product aims to support digestive tolerance and healthy weight while ensuring balanced nutrition for picky eaters and is available via pet stores, online platforms, and veterinary clinics.

4. Veterinary Channel and Prescription Diet Expansion

In January 2024, Hill’s Pet Nutrition announced a range of new and upgraded Prescription Diet products designed to support specific health needs in cats and dogs, such as low‑fat, hydrolyzed, urinary, and digestive formulas, using science‑based taste and gut‑health technologies. Vet-recommended nutrition now accounts for 28% of premium segment purchases, anchoring brand loyalty that persists beyond the initial prescription cycle.

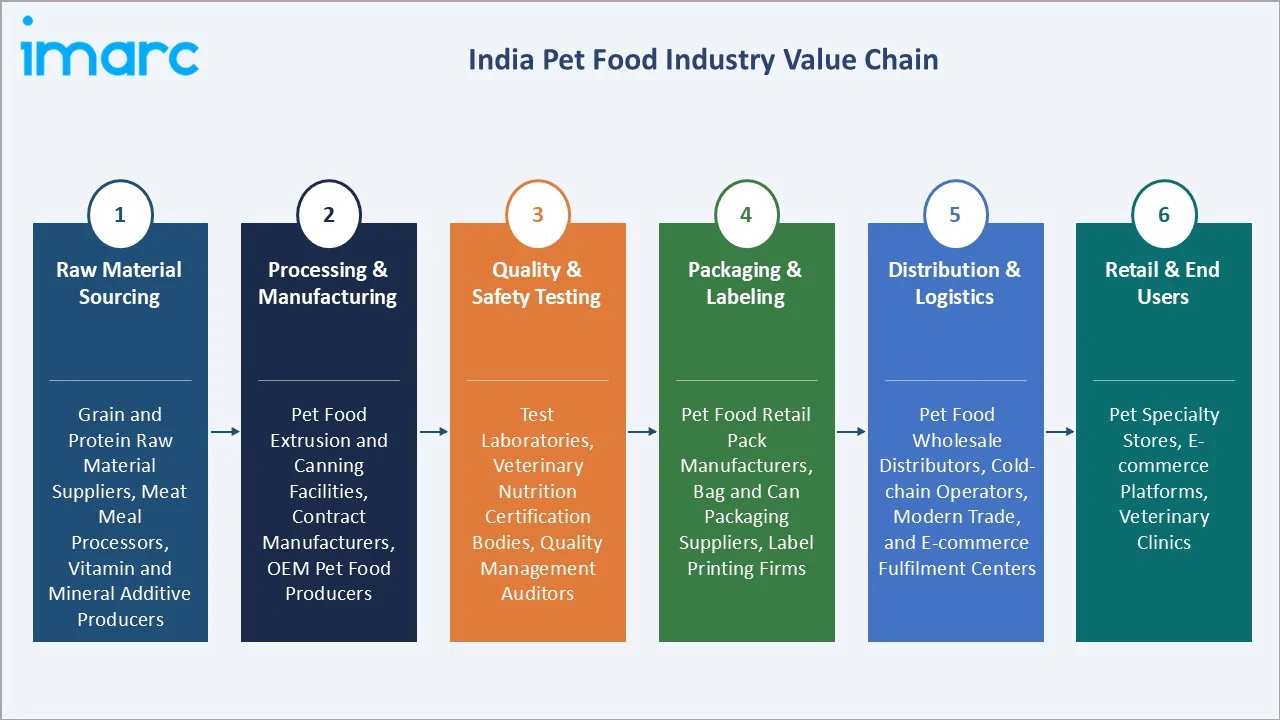

Industry Value Chain Analysis

India's pet food value chain spans raw material procurement through retail delivery, with each stage managed by specialized manufacturers, importers, distributors, and retail platforms whose integration defines product quality, pricing, and market reach.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Grain and protein raw material suppliers, meat meal processors, vitamin and mineral additive producers |

|

Processing & Manufacturing |

Pet food extrusion and canning facilities, contract manufacturers, OEM pet food producers |

|

Quality & Safety Testing |

Test laboratories, veterinary nutrition certification bodies, quality management auditors |

|

Packaging & Labeling |

Pet food retail pack manufacturers, bag and can packaging suppliers, label printing firms |

|

Distribution & Logistics |

Pet food wholesale distributors, cold-chain operators, modern trade, and e-commerce fulfilment centers |

|

Retail & End Users |

Pet specialty stores, e-commerce platforms, veterinary clinics |

Technology Landscape in the India Pet Food Industry

Advanced Extrusion and Formulation Technology

High-moisture extrusion and twin-screw extrusion technology enable the production of grain-free, high-meat kibble with 40%+ protein content at commercially viable costs. Mars Petcare's facility and Drools' plant operate European-standard extrusion lines producing breed-specific kibble geometries and textured soft-dry formats that differentiate India's premium segment from commodity bulk dry food.

Precision Nutrition and AI-Driven Formulation

Global pet food companies are deploying AI-driven formulation platforms to develop India-specific recipes addressing local protein sources and Indian dog breed nutritional requirements. Hill's Pet Nutrition's nutrigenomics research program is developing breed-specific formulations for Indian breeds, including Indian Pariah dogs, targeting the growing segment of breed-aware pet owners.

E-Commerce Personalization and Subscription Technology

Online orders for pet care products in India grew by 95% in FY25 compared with FY24, driven by rising demand for pet food, preventive care, accessories, and specialized health‑oriented items. Brand websites saw even stronger growth, with prepaid orders jumping about 300% year‑on‑year, as pet parenting expands into tier‑2 and tier‑3 cities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Pet Type |

Dog Food |

85.6% |

2025 |

|

Product Type |

Dry Pet Food |

89.6% |

2025 |

|

Pricing Type |

Mass Products |

70.0% |

2025 |

|

Ingredient Type |

Animal-Derived |

80.0% |

2025 |

|

Distribution Channel |

Specialty Stores |

50.0% |

2025 |

|

Region |

North India |

35.0% |

2025 |

By Pet Type

Dog food commands an 85.6% share in 2025, driven by India's estimated 31–37 million pet dogs representing the dominant companion animal population. The dog food segment benefits from three decades of branded nutrition awareness, with Pedigree and Royal Canin achieving near-universal brand recognition among urban dog owners.

To access detailed market analysis, Request Sample

Cat food at 10.4% is the fastest-growing pet type at ~8.2% CAGR, as India's cat population expands rapidly across urban apartments, where dogs face space and housing society restrictions. Others (4.0%) encompass fish food, bird feed, and small animal nutrition, a nascent but growing segment as exotic pet ownership trends emerge among younger urban demographics.

By Product Type

Dry pet food dominates at 89.6% in 2025, reflecting unique market characteristics: kibble's ambient storage compatibility with Indian climate conditions, its strong price-to-nutrition value proposition, and the preference of first-time pet owners for easy, mess-free feeding.

Wet and canned pet food at 6.4% is constrained by cold-chain limitations and higher unit economics (INR 45–120 per serving versus INR 15–35 for equivalent dry food calories). Snacks and treats at 4.0% represent the fastest-growing product type at ~9.2% CAGR, driven by the explosive growth of functional dental chews, freeze-dried meat treats, and joint-health supplements positioned at the treat-gifting behavior of India's urban pet parents.

Regional Market Insights

North India's market leadership (35.0%, 2025) is anchored by Delhi-NCR's unparalleled concentration of premium pet stores, veterinary specialists, and organized pet grooming infrastructure. North India drives outsized demand for premium and therapeutic nutrition, sustaining higher average selling prices relative to other regions.

South India at 27.0% (2025) is the fastest-growing region, with Bengaluru and Hyderabad's tech-sector workforce driving premium pet food adoption at rates exceeding national averages. West & Central India at 23.0% benefits from Mumbai's high pet ownership density and Maharashtra's organized retail infrastructure. East India at 15.0% represents the largest under-penetrated opportunity, with Kolkata's growing middle class increasingly adopting commercial pet nutrition.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

35.0% |

Highest urban pet ownership density, Delhi-NCR premium pet product demand, large modern retail, e-commerce penetration |

|

South India |

27.0% |

Tech-corridor pet ownership growth, strong vet ecosystem, rising awareness of branded nutrition, millennial-driven pet humanization trend |

|

West & Central India |

23.0% |

Mumbai-Pune metro pet adoption surge, Maharashtra modern trade network, Gujarat growing pet specialty retail, rising organized sector pet care spends |

|

East India |

15.0% |

Expanding urban middle-class pet ownership, growing e-commerce penetration, increasing brand awareness in Tier-2 cities, rising disposable incomes |

Competitive Landscape

India's pet food market exhibits moderate concentration, with Mars, Incorporated, Nestlé S.A., and Colgate-Palmolive Company collectively holding approximately 55–65% of organized market revenue in 2025.

|

Company Name |

Brand/Products |

Market Position |

Core Strength |

|

Mars, Incorporated |

Pedigree, Whiskas, Sheba, Cesar, Iams, Royal Canin |

Market Leader |

Broadest brand portfolio; largest distribution network; MNC-backed R&D and vet nutrition expertise across all pet categories |

|

Nestlé S.A. |

Felix, Purina Friskies, Purina ProPlan |

Market Leader |

Premium and science-backed formulations; strong modern trade presence; nutrition research depth; growing e-commerce channel |

|

Colgate-Palmolive Company |

Hill's Science Diet, Hill's Prescription Diet |

Strong Challenger |

Vet-channel dominance; therapeutic prescription diet leadership; strong trust among veterinarians across urban India |

|

IB Group |

Drools Focus, Drools Daily Nutrition, Drools Optium, Drools Ultium, Canine Creek, Cat/Dog Treats, Drools Cat Dry Food, Drools Kitten Dry Food, Creamy Treats, among others |

Strong Challenger |

Largest Indian-origin brand; cost-competitive with premium positioning; strong D2C and e-commerce scaling across Tier 1-2 cities |

|

Farmina Pet Foods |

Farmina Vet Life, N&D Quinoa, N&D Prime, N&D Pumpkin, N&D Ancestral Grain |

Challenger |

Super-premium natural ingredient positioning; Italian heritage; growing adoption among health-conscious urban pet owners |

Domestic brands led by IB Group are capturing 20–25% of mid-tier volumes through aggressive pricing and India-specific e-commerce distribution strategies.

Key Company Profiles

Mars, Incorporated

Mars, Incorporated is the market leader in India's pet food sector, operating across mass, mid-premium, and super-premium segments. Mars India offers dry dog food at scale for the domestic and export market.

- Product Portfolio: Pedigree (dry & wet food for dogs, puppy food, dog treats), Whiskas, Sheba, Cesar, Iams, and Royal Canin (puppy food, adult dog food, senior dog food, kitten food, adult cat food, senior cat food).

- Recent Developments: In July 2025, Mars, Incorporated rolled out its “Feed Them Like Cats and Dogs” campaign for Pedigree and Whiskas, aiming to educate pet owners about the different nutritional needs of dogs and cats and encouraging a shift from emotional to informed feeding.

- Strategic Focus: Expansion of Royal Canin vet-channel distribution to clinics; Pedigree e-commerce scaling.

IB Group

IB Group’s subsidiary Drools Pet Food is one of India's largest domestically-owned pet food brands, achieving significant scale through cost-competitive formulations, aggressive D2C investment, and a distribution network.

- Product Portfolio: Drools Focus, Drools Daily Nutrition, Drools Optium, Drools Ultium, Canine Creek, Cat/Dog Treats, Drools Cat Dry Food, Drools Kitten Dry Food, Creamy Treats, among others.

- Recent Developments: In April 2026, Drools Pet Food announced an INR 180 crore investment and a strategic partnership with Tetra Pak to launch fresh pet food in Tetra Recart aseptic packaging, making it shelf‑stable without refrigeration and redefining pet nutrition formats in India.

- Strategic Focus: Premium kibble portfolio expansion; South and East India distribution deepening; cat food category build-out for the rapidly growing feline segment.

Market Concentration Analysis

India's pet food market exhibits moderate concentration in 2025, with Mars, Incorporated, Nestlé S.A., and Colgate-Palmolive Company holding approximately 55–65% of organized market revenue. The mid-tier segment is primarily contested by domestic players IB Group, while the super-premium segment sees increasing competition from imported European brands.

Market consolidation is emerging through VC-backed D2C platforms: Heads Up For Tails reportedly closing in on USD 25 million in Series B funding (December 2025), and Supertails raised USD 15 Million in Series B, collectively channeling premium brand discovery and repeat purchase through digital-first pet care ecosystems that reduce dependence on traditional distributor networks.

Investment & Growth Opportunities

Fastest Growing Segments

Cat food (~8.2% CAGR), snacks and treats (~9.2% CAGR), wet and canned pet food (~8.5% CAGR), and super-premium dry food (~11% CAGR) represent the highest-return investment vectors through 2034. Together, these sub-categories address an incremental market of approximately USD 1.2 Billion by 2034, above 2025 spend levels, driven by cat adoption growth, functional treat premiumization, and the transition from home-cooked to commercial nutrition.

Emerging Market Expansion

Tier-2 cities, including Jaipur, Lucknow, Pune, Bhopal, and Coimbatore, collectively represent an under-penetrated INR 800 crore pet food opportunity by 2030, as first-generation urban pet owners in these markets begin adopting commercial nutrition. E-commerce penetration in Tier-2 cities, growing at approximately 55% annually, is enabling brand reach without retail infrastructure investment.

Venture and Institutional Investment Trends

- India's pet care sector attracted USD 100+ Million in venture capital in 2023–2025, with D2C platforms, veterinary telehealth, and premium pet nutrition startups receiving Series A–C rounds. Pet food represents 40–50% of total pet care VC deployment, reflecting investor confidence in category structural growth.

- Contract manufacturing capacity is creating OEM production opportunities for global brands seeking India-specific formulations without capex investment, reducing market entry barriers for international super-premium brands targeting urban consumers.

Future Market Outlook (2026-2034)

India's pet food market will expand from USD 2.52 Billion in 2025 to USD 4.60 Billion by 2034 at a 6.91% CAGR. Dog food will sustain volume dominance, but cat food's share will grow to 14–16% by 2034 as urban cat ownership normalizes. Dry food will remain dominant, but wet food and treats will grow structurally as cold-chain infrastructure expands and functional nutrition awareness deepens.

By 2034, AI-personalized nutrition platforms will serve 5+ million Indian pet owners with breed, age, and health-condition-specific feeding recommendations. India's position as a growing pet food export hub, leveraging domestic chicken and marine protein sources, will attract global brands to establish India-based manufacturing for Southeast Asian and Middle Eastern export markets, creating manufacturing investment that reinforces domestic competitive capacity.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including pet food brand managers, veterinary nutritionists, pet store operators, e-commerce category heads, and institutional investors across Delhi, Mumbai, Bengaluru, and Chennai.

Secondary Research

Secondary research covered FSSAI pet food regulatory documentation, APEDA export statistics, Pet Food Manufacturers' Association India reports, IMARC's pet care industry databases, venture capital transaction records, and industry publications, including PetAge India, ZooMark, and Petfood Industry Magazine.

Forecasting Models

Market size estimations used bottom-up forecasting incorporating pet population data, per-pet food expenditure benchmarks, distribution channel penetration rates, and company revenue disclosures. A CAGR of 6.91% reflects consensus validated against FSSAI registration trends and IMARC's primary expert panel through 2034.

India Pet Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Pet Types Covered | Dog Food, Cat Food, Others |

| Product Types Covered | Dry Pet Food, Wet and Canned Pet Food, Snacks and Treats |

| Pricing Types Covered | Mass Products, Premium Products |

| Ingredient Types Covered | Animal Derived, Plant Derived |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Others |

| Regions Covered | South India, North India, West and Central, East India |

| Companies Covered | Mars, Incorporated, Nestlé S.A., Colgate-Palmolive Company, IB Group, Farmina Pet Foods, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Pet Food Market Report

The market reached USD 2.52 Billion in 2025 and is forecast to reach USD 4.60 Billion by 2034 at a 6.91% CAGR.

Dog food leads at 85.6% in 2025, driven by India's 31–37 million pet dog population and three decades of branded nutrition awareness anchored by Pedigree and Royal Canin.

Dry pet food dominates at 89.6% in 2025, reflecting kibble's ambient storage advantages, price competitiveness, and the dominant purchasing behavior of first-time pet owners across India.

North India leads at 35.0% in 2025, anchored by Delhi-NCR's premium pet ownership concentration, high-density veterinary infrastructure, and the largest organized pet retail network in India.

Key players include Mars, Incorporated, Nestlé S.A., Colgate-Palmolive Company, IB Group, and Farmina Pet Foods, competing through product innovation, vet-channel relationships, and D2C e-commerce platforms.

Snacks and treats are the fastest-growing product type at ~9.2% CAGR, while Cat food is the fastest-growing pet type at ~8.2% CAGR, driven by urban cat adoption and functional treat premiumization.

Rising pet humanization, expanding urban middle-class pet ownership, e-commerce and D2C platform proliferation, veterinary nutrition recommendation growth, and the structural shift from home-cooked to commercial pet nutrition are the primary growth catalysts.

Home-cooked food competition, rural market penetration limitations, FSSAI regulatory compliance costs, cold-chain infrastructure gaps for wet pet food, and price sensitivity in mass-market segments are the primary challenges.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)