India Plant Based Protein Market Size, Share, Trends and Forecast by Source, Type, Nature, Application, and Region, 2026-2034

India Plant Based Protein Market Size, Share, Trends & Forecast (2026-2034)

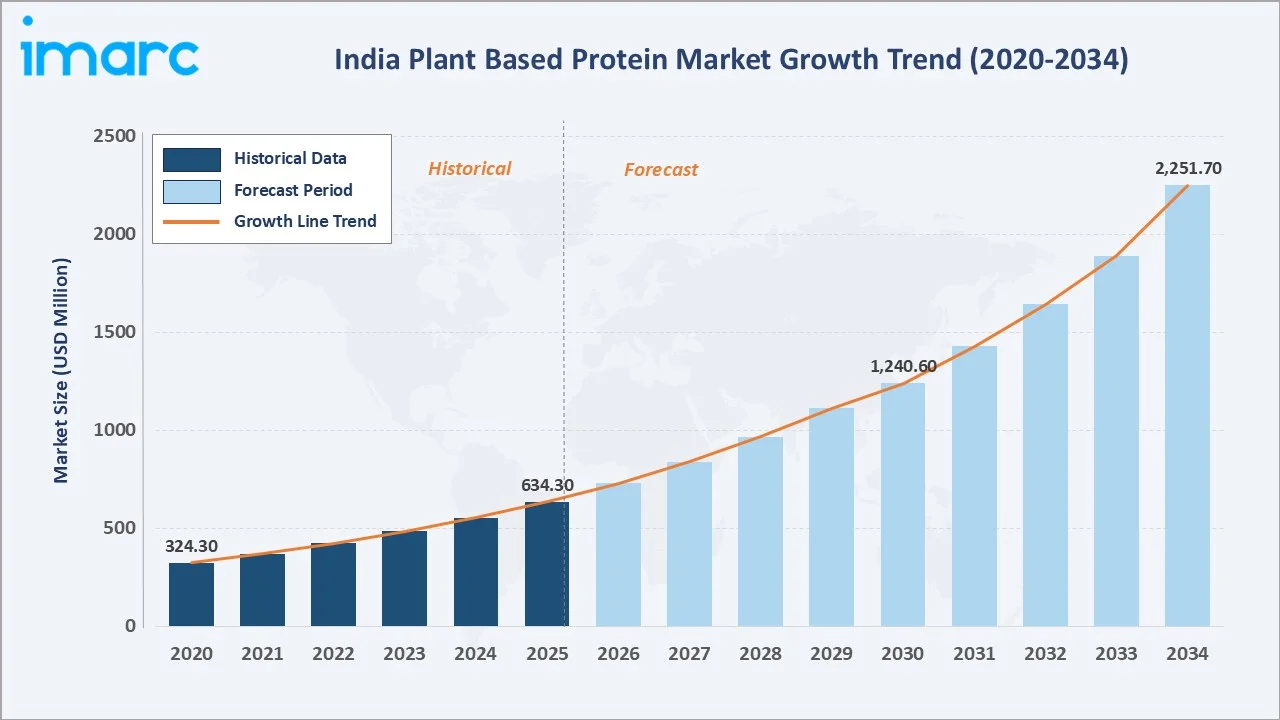

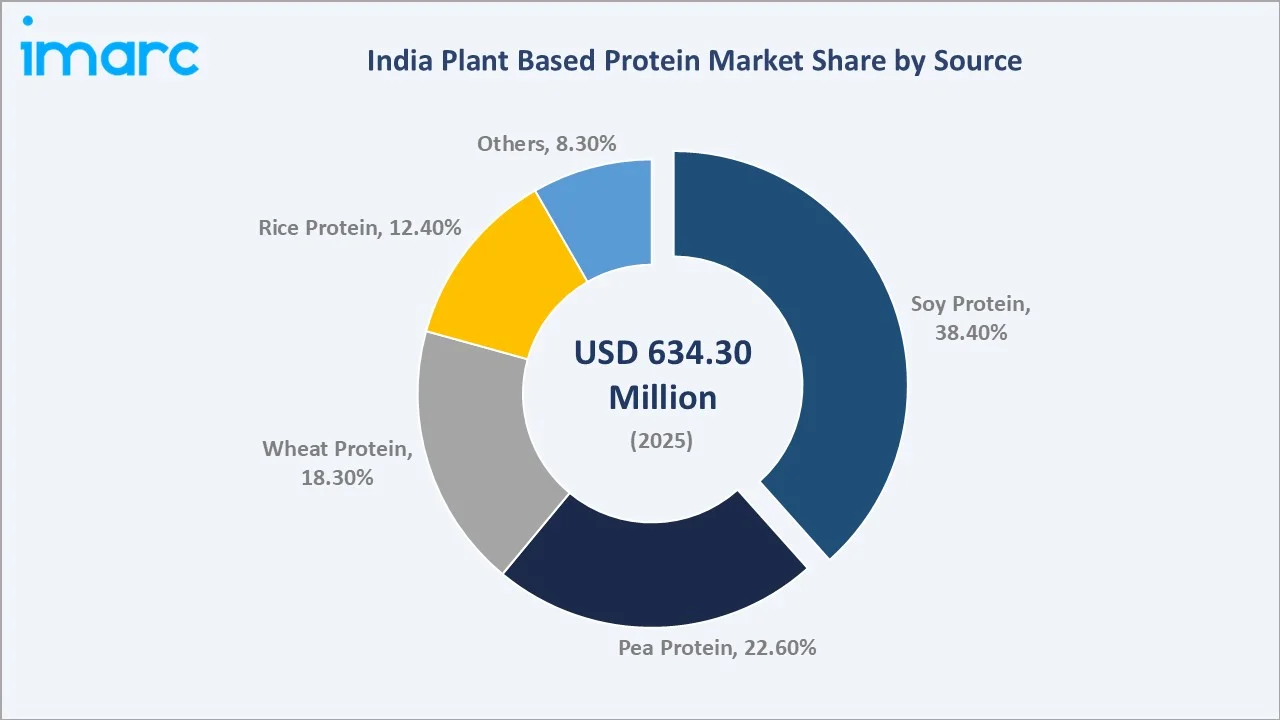

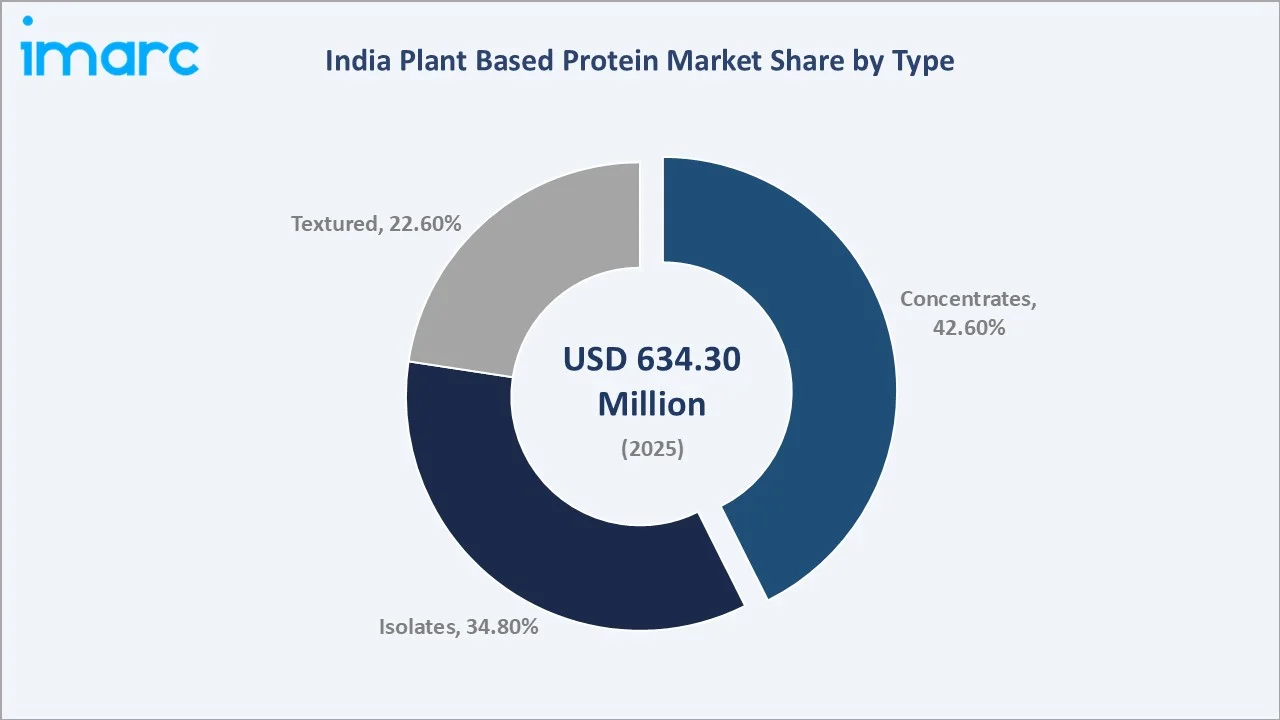

The India plant based protein market size reached USD 634.3 Million in 2025 and is projected to reach USD 2,251.7 Million by 2034, exhibiting a CAGR of 14.36% during 2026-2034. The market is propelled by India's rapidly expanding vegetarian and flexitarian population, rising health-consciousness among urban consumers, surging demand for sustainable protein alternatives, growing fitness culture, and increasing penetration of plant-based protein products across food and beverage, health supplement, and pharmaceutical applications.

Market Snapshot

|

Metric |

Value |

|

Market Size in 2025 |

USD 634.3 Million |

|

Market Forecast in 2034 |

USD 2,251.7 Million |

|

CAGR (2026-2034) |

14.36% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Source Segment |

Soy Protein – 38.4% (2025) |

|

Largest Type Segment |

Concentrates – 42.6% (2025) |

|

Leading Region |

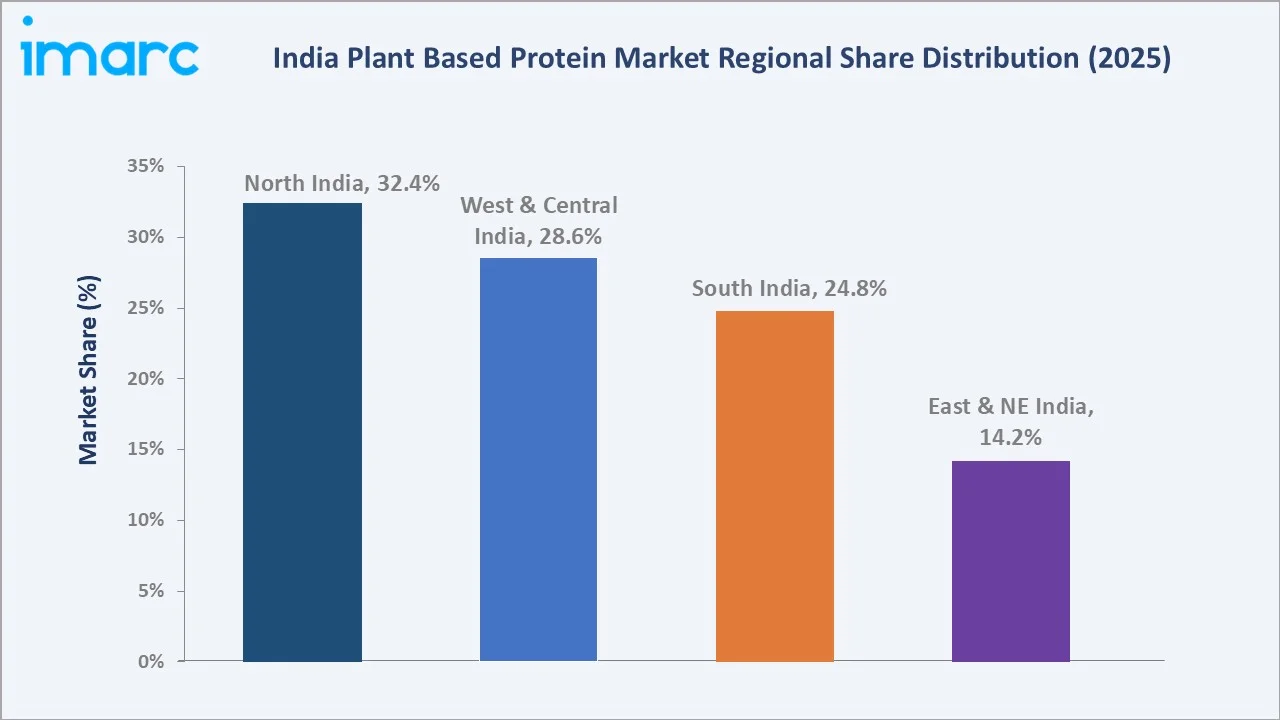

North India – 32.4% (2025) |

|

Fastest Growing Segment |

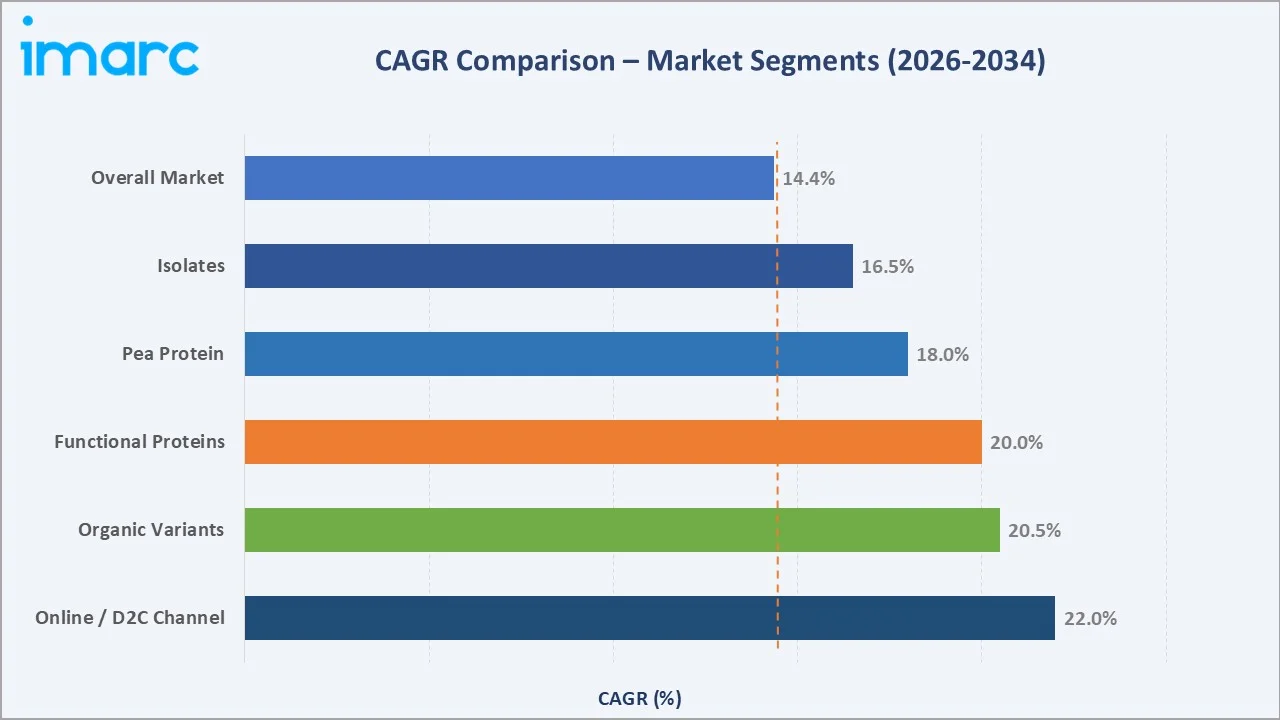

Pea Protein – est. CAGR ~18% (2026-2034) |

North India leads the India plant based protein market with a 32.4% share in 2025. Soy protein is the dominant source at 38.4%, while concentrates command the largest type segment at 42.6%. Pea protein, at 22.6%, emerges as the fastest-growing source driven by clean-label demand and superior amino acid profiles.

To get more information on this market, Request Sample

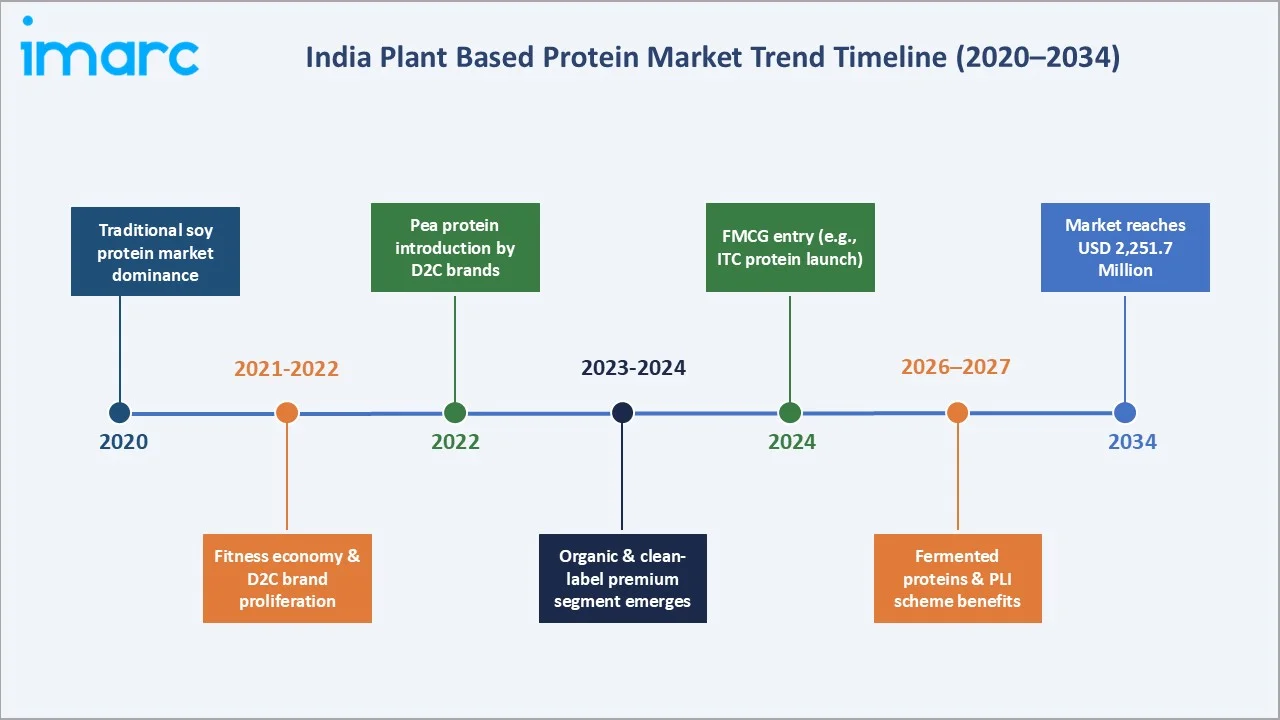

From USD 324.3 Million in 2020 to USD 634.3 Million in 2025 and a projected USD 2,251.7 Million by 2034, India's plant based protein market nearly triples in size over the forecast decade, reflecting one of the highest compound growth rates among Asian food ingredient markets.

Executive Summary

The India plant based protein market demonstrates exceptional growth momentum, underpinned by structural shifts in dietary preferences, expanding health consciousness, and surging demand for sustainable nutrition. Valued at USD 634.3 Million in 2025, the market is forecast to reach USD 2,251.7 Million by 2034 at a CAGR of 14.36%. This growth trajectory - nearly doubling every five years - reflects the convergence of India's vegetarian heritage, a burgeoning fitness economy, and a maturing functional food and supplement sector.

Soy protein dominates with a 38.4% source share in 2025, reflecting India's long-standing soy cultivation infrastructure and consumer familiarity. Pea protein at 22.6% emerges as the fastest-growing alternative, driven by allergen-free positioning and high digestibility scores. Concentrates lead the type segmentation at 42.6%, supported by cost efficiency and broad application versatility across food, beverage, and supplement manufacturing.

North India accounts for 32.4% of market revenues in 2025, anchored by high urbanization rates, established food manufacturing hubs, and strong fitness culture in metros like Delhi, Gurugram, and Chandigarh. South India at 24.8% and West and Central India at 28.6% represent high-growth zones driven by organized retail expansion and rising middle-class health expenditure. The India plant based protein market outlook through 2034 remains robustly positive.

Key Market Insights

|

Insight |

Data |

|

Largest Source Segment |

Soy Protein – 38.4% share (2025) |

|

Largest Type Segment |

Concentrates – 42.6% share (2025) |

|

Fastest Growing Source |

Pea Protein – est. CAGR ~18% (2026-2034) |

|

Fastest Growing Type |

Isolates – est. CAGR ~16.5% (2026-2034) |

|

Leading Region |

North India – 32.4% share (2025) |

|

Key Market Opportunity |

USD 1.6 Billion addressable by 2034 in health & fitness |

Key Analytical Observations Supporting the Above Data:

- Soy Protein commands 38.4% market share (2025), reflecting India's deep-rooted soy cultivation ecosystem, and widespread use across protein powders, meat analogues, and bakery fortification.

- Concentrates lead type segmentation at 42.6% share (2025), driven by their cost-effectiveness and 60-70% protein content range, making them the preferred choice for mainstream food and beverage manufacturers.

- North India's 32.4% revenue dominance is supported by high-density urban populations, established food-processing clusters in Punjab, Haryana, and Uttar Pradesh, and strong gym and sports nutrition consumption patterns.

- India's plant-based protein market in 2020 stood at USD 324.3 Million and nearly doubled to USD 634.3 Million by 2025- a 95.6% growth in just five years - underscoring the rapid pace of market adoption.

India Plant Based Protein Market Overview

The India plant based protein industry represents one of the fastest-expanding segments within the country's broader food ingredients and nutraceuticals ecosystem. Plant-based proteins encompass a diverse product spectrum - from soy, pea, wheat, and rice protein concentrates and isolates to texturized vegetable proteins (TVPs), protein blends, and novel crop-derived ingredients - collectively serving consumers and manufacturers across health supplements, functional foods, dairy alternatives, meat analogues, and pharmaceutical nutrition segments.

India's unique demographic and cultural landscape - home to approximately 500 million vegetarians and a growing flexitarian population - provides an exceptionally fertile foundation for plant-based protein adoption. The market's value chain spans oilseed and grain cultivation through industrial extraction, processing, formulation, and multi-channel distribution reaching both B2B manufacturers and B2C end consumers through e-commerce, modern retail, and pharmacy networks.

The India plant based protein market forecast through 2034 is shaped by macroeconomic tailwinds including rising per-capita income, expanded healthcare awareness post-COVID-19, and government initiatives promoting protein consumption through the Right to Protein campaign.

Market Dynamics

To evaluate market opportunities, Request Sample

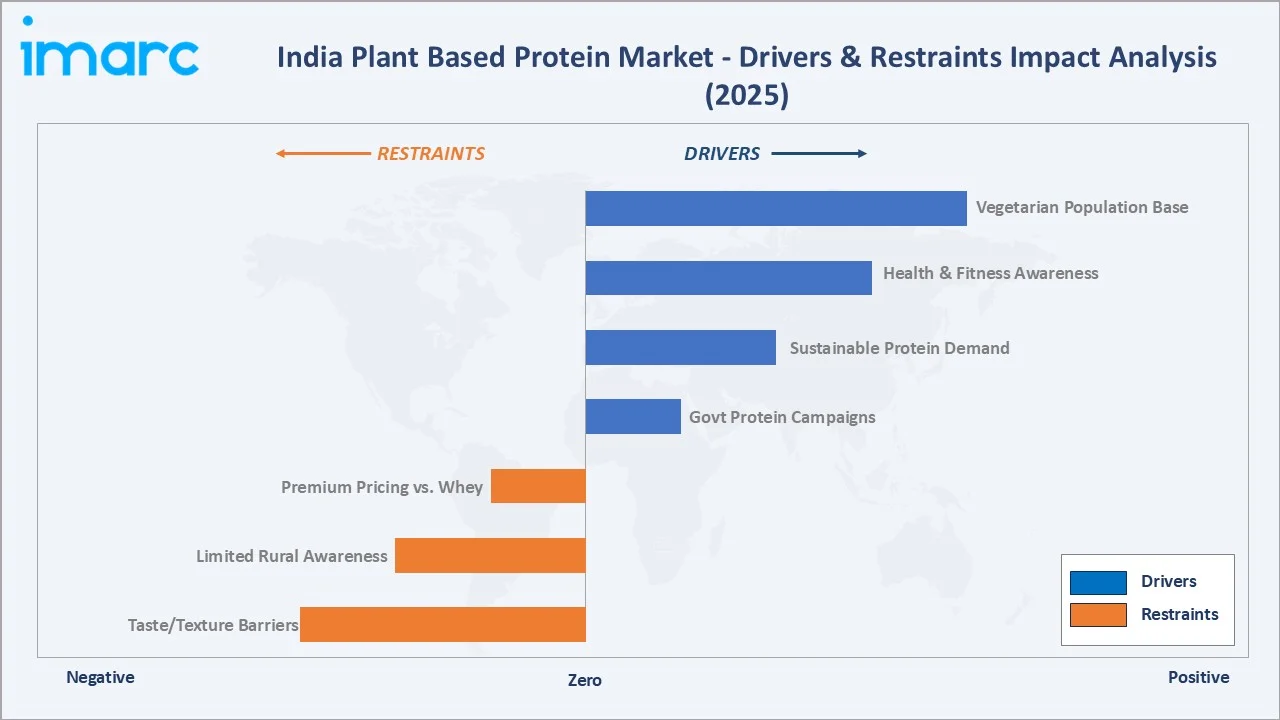

Market Drivers

- India's Large Vegetarian Population Base: India hosts an estimated 500 million vegetarians - the world's largest - creating an inherently high baseline demand for plant-derived protein ingredients across food and supplement categories.

- Rising Health and Fitness Awareness: Post-pandemic health consciousness has elevated protein literacy. An estimated 63% of urban Indian consumers now actively read nutritional labels, and gym memberships in Tier-1 and Tier-2 cities have grown at approximately 11% CAGR since 2021.

- Government Protein Awareness Campaigns: The Right to Protein initiative is expanding consumer awareness and driving adoption of protein-based products through widespread media and retail campaigns, increasing trial rates and encouraging repeat purchases across health-conscious segments.

Market Restraints

- Consumer Taste and Texture Perception Barriers: Taste perception remains a key barrier to plant protein adoption, with many non-vegan consumers citing it as a primary concern, thereby slowing mainstream penetration despite increasing awareness and availability.

- Higher Price Points vs. Conventional Protein Sources: Higher pricing of premium protein isolates compared to whey-based alternatives limits adoption, particularly in price-sensitive semi-urban and rural markets, thereby constraining broader market penetration despite growing health awareness.

Market Opportunities

- Functional Food and Beverage Fortification: India's packaged food sector, valued at approximately INR 10,180 billion in 2024, represents a high-volume, high-growth channel for plant protein ingredient incorporation across breakfast cereals, protein bars, dairy alternatives, and bakery products.

- Meat Analogue Market Expansion: The Indian plant-based meat market is estimated to grow at over 14.36% CAGR through 2030, creating direct demand pull for texturized plant proteins and high-quality protein isolates used in product formulation.

- E-commerce and D2C Channel Growth: India’s online health supplement market is witnessing strong growth, providing plant protein brands with cost-effective access to a vast and expanding base of internet-enabled consumers, thereby accelerating digital-driven adoption and market penetration.

Market Challenges

- Inconsistent Raw Material Quality and Supply: India’s soy and pea cultivation is impacted by monsoon dependency, leading to yield variability and supply fluctuations, which in turn affects raw material availability and pricing stability for plant protein manufacturers.

- Competition from Whey and Animal Protein: Established whey protein brands continue to exert strong competitive pressure due to lower pricing and superior taste perception, making it challenging for premium plant protein isolates to gain share within the sports nutrition segment.

Emerging Market Trends

The following trends are actively reshaping India's plant based protein market growth trajectory through 2034:

1. Rapid Expansion of Pea Protein Adoption

Pea protein is emerging as a mainstream protein source, driven by its hypoallergenic nature, high digestibility, and balanced amino acid profile, with strong growth supported by increasing adoption and new product launches by major FMCG companies in the Indian market.

2. Protein Fortification of Traditional Indian Foods

A uniquely Indian trend involves fortifying traditional staples such as atta, rice, snacks, and dairy alternatives with plant proteins, enabling companies to enhance nutritional value while leveraging consumer familiarity to drive adoption.

3. Clean Label and Organic Plant Protein Demand

The organic plant protein segment is witnessing strong growth, driven by rising demand for clean-label, non-GMO, and certified products, with organic variants commanding premium pricing due to perceived health benefits and higher quality standards among increasingly conscious consumers.

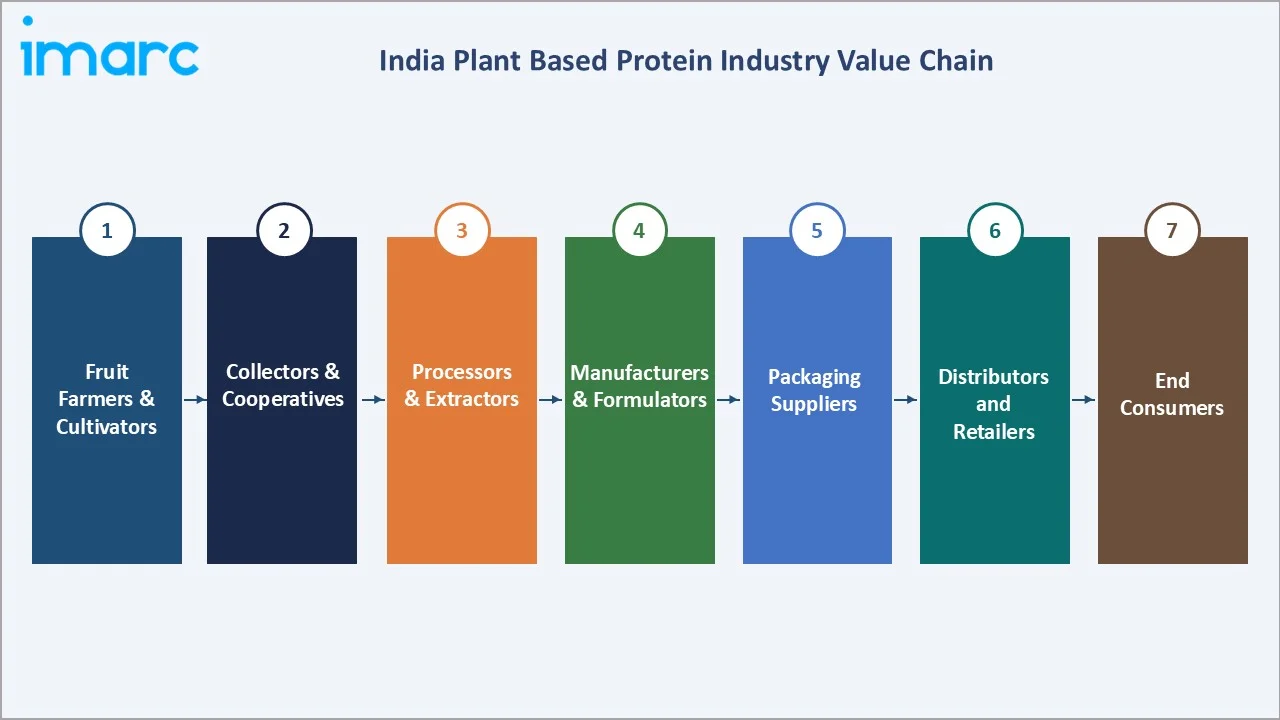

Industry Value Chain Analysis

The India plant based protein value chain spans eight interconnected stages from agricultural cultivation through extraction, processing, formulation, distribution, retail, and end-use.

|

Stage |

Key Players / Examples |

|

Raw Material Cultivation |

Soy farmers (MP, Maharashtra, Rajasthan); Pea growers (UP, Punjab); Wheat cultivators (Punjab, Haryana); Rice farmers (West Bengal, AP) |

|

Processing & Extraction |

Ruchi Soya Industries, Taj Agro Products; regional solvent extraction units; aqueous processing specialists |

|

Protein Manufacturing |

Marico, Emami Agrotech, Godrej Agrovet; contract manufacturers producing concentrates, isolates, and TVP for B2B supply chains |

|

Formulation & Blending |

D2C supplement brands; FMCG companies (ITC, Britannia); pharmaceutical nutrition companies (Abbott, Nestle Health Science) |

|

Packaging Suppliers |

Uflex, Huhtamaki India, EPL Limited; flexible packaging specialists for powder, sachet, and liquid protein formats |

|

Distributors |

FMCG distributors (HUL, Marico networks); cold-chain logistics for refrigerated analogues; e-commerce fulfillment (Amazon, Flipkart) |

|

Retailers |

BigBasket, Blinkit, Amazon India (online); D-Mart, Reliance Smart, Spencer's (modern trade); pharmacy chains (Apollo, MedPlus) |

|

End Consumers |

Health-conscious urban consumers; fitness professionals; vegetarian and vegan households; pharmaceutical and clinical nutrition users |

India’s plant protein market benefits from a strong domestic soybean production base alongside imports, ensuring stable raw material availability and supporting the growth of soy as a leading protein source across food and nutrition applications.

Technology Landscape in the India Plant Based Protein Industry

Solvent Extraction and Aqueous Processing

Traditional solvent (hexane-based) extraction remains the dominant processing method for soy protein concentrates in India. However, water-based aqueous extraction is gaining share due to clean-label advantages and elimination of residual solvent concerns.

High-Pressure and Enzymatic Processing

Enzymatic hydrolysis technology is being adopted by leading Indian processors to produce protein hydrolysates and improved solubility profiles. These high-value ingredients are finding application in sports nutrition, infant formula, and medical nutrition.

Extrusion Technology for Textured Proteins

High-moisture extrusion (HME) technology, capable of creating fibrous meat-like textures from plant proteins, is being deployed by Indian food manufacturers to scale plant-based meat analogue production.

Fermentation and Precision Biology

Precision fermentation using microbial chassis is emerging as the next frontier in Indian plant protein technology. Startups funded through BIRAC grants are developing fermented protein ingredients with superior amino acid profiles.

Market Segmentation Analysis

The India plant based protein market analysis is presented across two primary segmentation dimensions: By Source and By Type, for which complete data inputs are provided.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Source |

Soy Protein |

38.4% |

2025 |

|

Type |

Concentrates |

42.6% |

2025 |

|

Nature |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

North India |

32.4% |

2025 |

By Source

To access detailed market analysis, Request Sample

Soy Protein (38.4%, 2025): Soy protein leads the India plant based protein market share by source, driven by India's established soybean cultivation (approximately 12 million hectares under cultivation in 2024-25), low production costs, and versatile application across protein powders, TVPs, and food fortification. The segment's growth is tempered by GMO concerns among premium consumers.

By Type

Concentrates (42.6%, 2025): Protein concentrates dominate the India plant based protein market type segmentation, valued for their balance of cost efficiency and functional performance. With protein content ranging from 60-70%, concentrates serve mainstream food and beverage manufacturers, mass-market supplement brands, and animal feed applications - delivering broad market reach at accessible price points.

Regional Market Insights

North India's 32.4% market leadership in 2025 reflects the region's dense urban population, established food and supplement manufacturing clusters, and high-income consumer segments in Delhi-NCR driving premium product adoption.

|

Region |

Share (2025) |

Key Growth Drivers |

Major Players / Hubs |

|

North India |

32.4% |

High urbanization; fitness culture in NCR; food-processing clusters in Punjab, Haryana, UP |

Delhi-NCR supplement brands; Haryana dairy alternative manufacturers; UP soy processors |

|

West & Central India |

28.6% |

Maharashtra's strong FMCG ecosystem; MP's dominant soy cultivation; Mumbai's organized retail depth |

Mumbai/Pune FMCG brands; MP soy processors; Indore food manufacturing clusters |

|

South India |

24.8% |

Bangalore tech-sector wellness demand; strong pharmacy retail networks; growing vegan community in Chennai, Hyderabad |

Bangalore D2C brands; Hyderabad food-tech companies; Chennai nutraceutical processors |

|

East & NE India |

14.2% |

Rising Kolkata and Guwahati urban consumption; growing organized retail; strong rice protein raw material base |

Kolkata FMCG distributors; West Bengal rice protein processors; Assam emerging retail |

West and Central India's 28.6% share is anchored by Madhya Pradesh's dominance in Indian soy cultivation - the state produces approximately 45% of India's total soybean crop - creating a vertically integrated local supply chain advantage. South India at 24.8% is increasingly defined by the Bangalore technology sector's high-income wellness consumer base. East and Northeast India at 14.2% represents the highest-growth frontier, with organized retail penetration in Tier-2 cities beginning to drive plant protein adoption beyond early-adopter urban centers.

Competitive Landscape

The India plant based protein market is moderately fragmented at the branded consumer level, with a mix of established domestic FMCG conglomerates, dedicated plant protein companies, and international brands competing across ingredient and finished product categories.

|

Company Name |

Key Brand (s) |

Market Position |

Core Strength |

|

Ruchi Soya (Patanjali Foods) |

Nutrela |

Market Leader (Soy) |

Largest soy protein brand; vertically integrated soy processing; 1.2M+ retail touchpoints |

|

ITC Limited |

Aashirvaad |

Diversified Leader |

Strong brand equity; pan-India distribution; protein-fortified atta and health food products |

|

Marico Limited |

Saffola |

Health & Wellness Leader |

Urban consumer trust; expansion into protein-fortified snacks and D2C supplements |

|

Tata Consumer Products |

Tata Soulfull, 1mg |

Innovation Leader |

Grain-based protein fortification; digital-first health platform; nutraceutical portfolio |

|

GoodDot Enterprises |

GoodDot |

Plant Meat Pioneer |

India's leading plant-based meat brand; proprietary TVP formulations; strong D2C and QSR channels |

|

Vezlay Foods |

Vezlay |

Emerging Challenger |

Soy-based meat analogues; growing foodservice presence; modern trade distribution expansion |

|

Amway India |

Nutrilite |

International Premium Leader |

High-quality pea and soy protein supplements; strong direct-selling network in Tier-1 and Tier-2 cities |

|

Herbalife Nutrition |

Formula 1 |

Global Supplement Player |

Established direct network; plant protein shakes; strong gym and fitness community integration |

The competitive landscape is evolving rapidly, with established FMCG players acquiring or launching plant protein sub-brands while nimble D2C startups leverage digital channels to build targeted consumer communities. International players including ADM, Roquette, and Cargill are deepening India-specific ingredient distribution, intensifying competitive dynamics through 2034.

Key Company Profiles

Ruchi Soya Industries Limited (Patanjali Foods)

Ruchi Soya Industries, operating under the Patanjali Foods umbrella since the 2019 acquisition, is India's largest soy protein manufacturer and a dominant player in the plant-based protein market.

- Product Portfolio: Nutrela soy chunks (TVP), Nutrela Daily Protein, soy protein concentrates, soy flour, and de-oiled cake.

- Recent Developments: Ruchi Soya expanded its Nutrela protein portfolio with high-protein biscuits and fortified atta products targeting the mass-market nutrition segment.

- Strategic Focus: Mass-market distribution dominance through 4763 distributors and 5 lakh retail touch points; premiumization of Nutrela brand into isolate-grade supplements; expansion into modern trade and quick commerce channels.

ITC Limited

ITC Limited is one of India's largest diversified conglomerates with a strong and rapidly growing health and wellness platform, particularly through its Aashirvaad brand. ITC has systematically integrated plant protein fortification across its portfolio.

- Product Portfolio: Aashirvaad Atta, B Natural juices, Aashirvaad protein supplements, and a pipeline of functional food products with added plant protein across snack and bakery categories.

- Recent Developments: In 2025, ITC’s has launched “Aashirvaad Atta with High Protein” under its Aashirvaad brand. The product set to rival multigrain and high-fibre wheat flour options in the market.

- Strategic Focus: Leveraging ITC's unmatched distribution network to mainstream plant protein through trusted staples brands; investment in ingredient innovation through its agri-science capabilities.

Marico Limited

Marico Limited is a leading FMCG company with a strong and rapidly growing health and wellness platform, particularly through its Saffola brand.

- Product Portfolio: Saffola Protein Whey & Plant-Based Protein Blend, Saffola FITTIFY protein snacks, plant-based protein powder supplements, and high-protein oats.

- Recent Developments: In 2026, Marico strengthened its presence in the plant-based nutrition segment by acquiring a majority stake in digital-first brand Cosmix, highlighting rising FMCG interest in emerging health and protein-focused startups.

- Strategic Focus: Premiumization of Saffola into a comprehensive health platform; digital-first consumer acquisition through Saffola's app and e-commerce; geographic expansion of protein products into Tier-2 and Tier-3 cities through Marico's established distribution networks.

Market Concentration Analysis

The India plant based protein market exhibits moderate-to-low concentration at the branded consumer level. The top 5 players - Ruchi Soya (Patanjali Foods), ITC Limited, Marico Limited, Amway India, and GoodDot Enterprises collectively account for an estimated 35-42% of branded retail market revenues in 2025. However, significant revenues flow through unbranded ingredient supply chains and private-label products.

The market's fragmentation is driven by the diversity of applications - spanning bulk ingredient supply, mass-market TVP, premium sports nutrition, clinical nutrition, and plant-based meat - each attracting distinct competitive sets. B2B ingredient supply is relatively concentrated, with Ruchi Soya and a handful of regional soy processors controlling the majority of domestic concentrate and TVP manufacturing capacity.

Investment & Growth Opportunities

Fastest Growing Segments

Pea protein isolates, functional protein supplements (probiotic-enhanced and collagen-boosted plant proteins), and high-moisture extruded plant-based meat ingredients represent the three highest-growth investment vectors through 2034.

Emerging Market Expansion

Tier-2 and Tier-3 Indian cities - including Jaipur, Lucknow, Coimbatore, Surat, and Bhubaneswar - represent the most compelling geographic expansion opportunities. Quick commerce platforms are reducing distribution barriers significantly.

Strategic Investment Trends

- Indian venture capital firm Omnivore startups exceeded USD 150 Million cumulatively between 2021 and 2025, with plant protein ingredients and consumer brands attracting the majority of deal flow.

- Government PLI scheme for food processing enables plant protein manufacturers to access INR 9,207 Crore in production incentives contingent on incremental processing capacity investment.

Future Market Outlook (2026-2034)

The India plant based protein market is positioned for exceptional sustained growth through 2034, anchored by demographic tailwinds, functional innovation, and digital channel acceleration. From a base of USD 634.3 Million in 2025, the market is forecast to reach USD 2,251.7 Million by 2034.

The market's trajectory through 2034 will be shaped by several structural forces: the continued rise of India's fitness economy (estimated to reach USD 8 Billion by 2030); the maturation of plant-based meat analogues from niche to mainstream Indian restaurant and household products; regulatory evolution under FSSAI creating clearer quality standards; and the emergence of precision fermentation and enzymatic processing as cost-competitive production technologies.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 120 industry stakeholders conducted in 2024-2025, comprising plant protein ingredient manufacturers, FMCG brand managers, retail buyers, nutritionists, sports dietitians, food technologists, and consumers across North, South, West, and East India. Primary data was collected through online surveys, telephonic interviews, and in-person focus groups across key plant protein consumption markets.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, trade publications (Food Navigator India, Nutraceuticals World), FSSAI regulatory filings, modern retail scanner data, and consumer research databases. Industry association data from the FICCI Food Processing Committee and the Protein Foods and Nutrition Development Association of India (PFNDAI) were incorporated alongside APEDA export data and Ministry of Agriculture crop production reports.

Forecasting Models

Market size estimates and CAGR projections were derived through a combination of top-down and bottom-up forecasting models incorporating India's GDP growth trajectory (projected at 6.5-7.0% annually through 2030), per-capita protein consumption trends, organized retail expansion indices, and product category adoption curves benchmarked against analogous markets in China and Southeast Asia. Three-scenario analysis (base, optimistic, and conservative) was conducted to capture regulatory, competitive, and demand uncertainty.

India Plant Based Protein Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Soy Protein, Pea Protein, Wheat Protein, Rice Protein, Others |

| Types Covered | Concentrates, Isolates, Textured |

| Natures Covered | Conventional, Organic |

| Applications Covered | Health and Fitness, Food and Beverages, Pharmaceutical, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Ruchi Soya (Patanjali Foods), ITC Limited, Marico Limited, Tata Consumer Products, GoodDot Enterprises, Vezlay Foods, Amway India, Herbalife Nutrition, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India plant based protein market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India plant based protein market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India plant based protein industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Plant Based Protein Market Research Report and Industry Forecast Report

The India plant based protein market reached USD 634.3 Million in 2025 and is projected to reach USD 2,251.7 Million by 2034.

The market is expected to grow at a CAGR of 14.36% during 2026-2034, driven by rising health awareness, growing vegetarian population, product innovation, and expanding e-commerce penetration across India.

Soy protein leads with a 38.4% share in 2025, supported by India's established soybean cultivation across 12 million hectares, cost competitiveness, and versatility across food, supplement, and analogue applications.

Concentrates dominate with a 42.6% type segment share in 2025, valued for their cost efficiency and, making them suitable for mainstream food and supplement manufacturing applications.

North India leads with a 32.4% share in 2025, driven by high urbanization, strong fitness culture in Delhi-NCR, and established food and supplement manufacturing clusters in Punjab, Haryana, and Uttar Pradesh.

Key drivers include India's large vegetarian population base, rising health and fitness consciousness, government protein awareness campaigns, growing demand for sustainable protein alternatives, and rapid e-commerce channel expansion.

Leading companies include Ruchi Soya (Patanjali Foods), ITC Limited, Marico Limited, Tata Consumer Products, GoodDot Enterprises, Vezlay Foods, Amway India, and Herbalife Nutrition.

Pea protein is the fastest growing source segment, estimated at ~18% CAGR through 2034, fueled by its allergen-free status, high digestibility exceeding 85%, and growing clean-label and vegan consumer demand.

Key challenges include taste and texture perception barriers, premium pricing versus whey proteins, limited Tier-3 and rural market awareness, monsoon-driven raw material supply variability, and evolving FSSAI regulatory complexity.

The market is expected to reach USD 2,251.7 Million by 2034, driven by functional innovation, e-commerce expansion, plant-based meat growth, and increasing per-capita health expenditure across Indian consumers.

Key opportunities include pea protein isolate manufacturing, functional and fortified protein supplements plant-based meat ingredient supply, and export to Southeast Asia and Middle East markets.

Sustainability considerations are driving preference for plant-based proteins, as their lower environmental impact is attracting environmentally conscious urban consumers and supporting the shift away from animal-based protein sources.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)