India Plasma Fractionation Market Size, Share, Trends and Forecast by Product, Sector, Application, End User, and Region, 2026-2034

India Plasma Fractionation Market Summary:

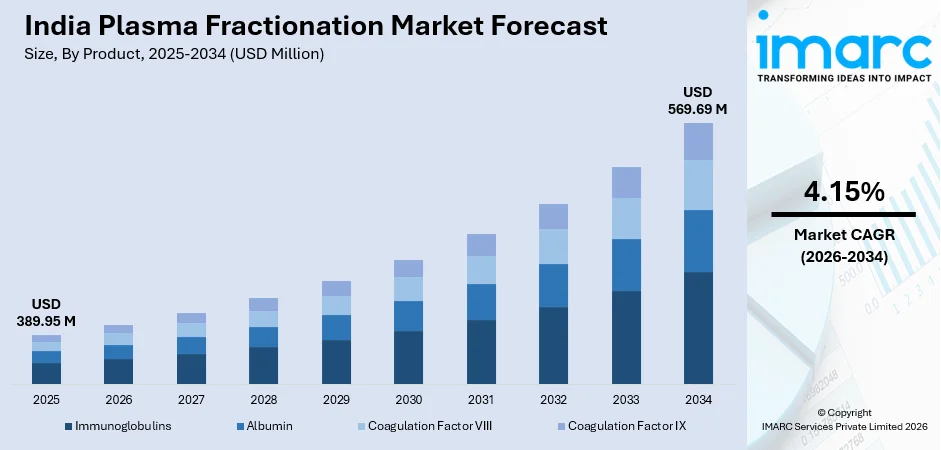

The India plasma fractionation market size was valued at USD 389.95 Million in 2025 and is projected to reach USD 569.69 Million by 2034, growing at a compound annual growth rate of 4.15% from 2026-2034.

The India plasma fractionation market is propelled by the rising prevalence of immunodeficiency disorders, autoimmune diseases, and bleeding conditions, driving sustained demand for plasma-derived therapeutic products. Growing healthcare awareness, expanding hospital infrastructure, and supportive government policies underpinning plasma collection are further accelerating market development. Increasing adoption of plasma-derived therapies across clinical specialties, coupled with the emergence of domestic manufacturing capabilities, continues to strengthen the market share.

Key Takeaways and Insights:

- By Product: Immunoglobulins dominate the market with a share of 46.3% in 2025, owing to their essential therapeutic role in managing primary and secondary immunodeficiency disorders, autoimmune diseases, and neurological conditions. The growing disease burden and expanding clinical applications continue to drive adoption across diverse healthcare settings.

- By Sector: Private sector represents the leading segment with a share of 75.0% in 2025, driven by stronger investment capacity, advanced healthcare infrastructure, and superior procurement networks that enable private hospitals to consistently source and administer specialized plasma-derived therapies.

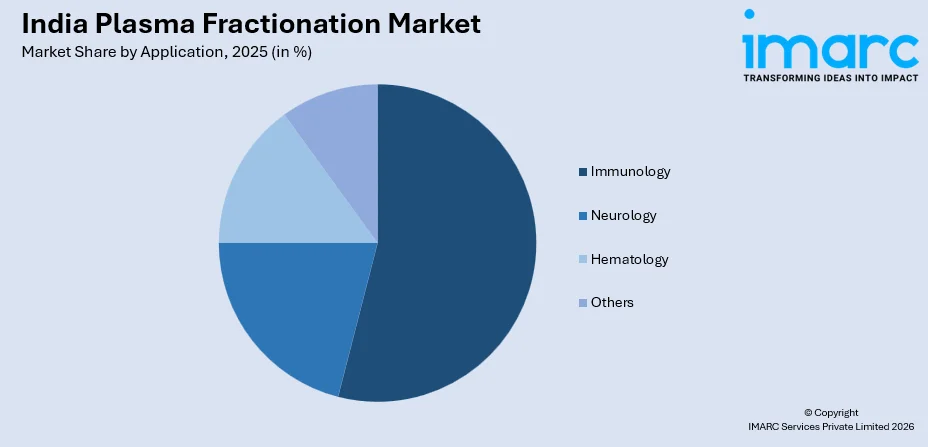

- By Application: Immunology leads the market with a share of 53.9% in 2025. This dominance is driven by the elevated burden of primary immunodeficiency disorders and autoimmune conditions, alongside deepening clinical awareness of the efficacy of plasma-derived immunoglobulin therapies across immunological specialties in India.

- By End User: Hospitals and clinics prevail the market with a share of 85.3% in 2025, underpinned by their central role in administering plasma-derived therapeutics across acute, chronic, and critical care settings, serving as the primary point of plasma therapy delivery throughout the country.

- By Region: West and Central India comprises the largest region with a 32.0% share in 2025, driven by the concentration of advanced healthcare facilities, a robust pharmaceutical manufacturing ecosystem, and elevated per capita healthcare expenditure in states, such as Maharashtra and Gujarat.

- Key Players: Key players drive the India plasma fractionation market by expanding domestic manufacturing capacity, diversifying plasma-derived product portfolios, and forging strategic partnerships with hospitals and government health agencies. Their investments in regulatory compliance, technological upgradation, and distribution network enhancement strengthen product accessibility across Indian healthcare settings.

To get more information on this market Request Sample

The India plasma fractionation market is witnessing consistent growth underpinned by the convergence of epidemiological, technological, and policy-level factors. The rising burden of chronic and rare diseases, including primary immunodeficiency disorders, hemophilia, and autoimmune conditions, has catalyzed demand for plasma-derived therapies, such as immunoglobulins, albumin, and coagulation factors across multiple clinical specialties. As per the Hemophilia and Health Collective of North (HHCN), India ranked second globally for hemophilia cases in 2024, with around 1,36,000 individuals affected by hemophilia A. Expanding healthcare infrastructure, growing physician awareness, and progressive government initiatives are strengthening India’s domestic plasma supply chain and reducing dependence on imported plasma fractions. Hospitals and clinical research institutions are at the forefront of plasma therapy adoption, particularly in critical care and surgical settings, serving as the primary drivers of product consumption.

India Plasma Fractionation Market Trends:

Expansion of Domestic Plasma Collection Infrastructure

The India plasma fractionation market is being shaped by the progressive expansion of plasma collection infrastructure across the country. The growing number of licensed blood banks and plasma collection centers is improving the availability of recovered plasma for fractionation, addressing longstanding raw material constraints. India’s National Plasma Policy mandates mobilization of surplus plasma from blood banks for fractionation purposes, fostering a more organized supply ecosystem. This expansion is particularly evident in metropolitan regions, where improved logistics and growing voluntary donor populations are steadily enhancing the availability of high-quality plasma for therapeutic manufacturing.

Technological Advancements in Plasma Fractionation Processes

The India plasma fractionation market is benefiting from the adoption of advanced separation technologies, including high-performance chromatography and depth filtration techniques, which are enhancing both the purity and yield of plasma-derived therapeutic proteins. Modern fractionation facilities are incorporating automated processing systems that reduce human error and ensure compliance with Good Manufacturing Practice standards. The introduction of in-process viral inactivation technologies has improved the safety profile of plasma-derived products, reinforcing clinician and patient confidence. These technological advances collectively enable manufacturers to produce a broader range of high-quality plasma products from the same volume of raw plasma.

Growing Clinical Adoption Across Diverse Medical Specialties

A growing culture of evidence-based practice is driving the adoption of plasma-derived therapies across diverse medical specialties in India. Physicians in immunology, hematology, neurology, and critical care are increasingly prescribing immunoglobulins, albumin, and coagulation factors based on expanding clinical guidelines. Continuing medical education programs are raising awareness of plasma-derived treatment options among specialists and general practitioners, improving patient access to life-saving therapies. The broader availability of specialized diagnostic tools is enabling earlier identification of conditions that benefit from plasma-derived treatment protocols, driving deeper market penetration.

Market Outlook 2026-2034:

The India plasma fractionation market is poised for steady and sustained expansion throughout the forecast period, driven by evolving epidemiological patterns, progressive healthcare policies, and growing domestic manufacturing capabilities. The deepening integration of plasma-derived products across critical care, immunology, and hematology settings underscores the market’s long-term clinical relevance. The market generated a revenue of USD 389.95 Million in 2025 and is projected to reach a revenue of USD 569.69 Million by 2034, growing at a compound annual growth rate of 4.15% from 2026-2034. As healthcare coverage expands across tier-2 and tier-3 cities, demand for plasma-derived therapies is expected to grow substantially, supported by rising physician awareness, improved diagnostic infrastructure, and increasing patient access to specialty care.

India Plasma Fractionation Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Immunoglobulins |

46.3% |

|

Sector |

Private Sector |

75.0% |

|

Application |

Immunology |

53.9% |

|

End User |

Hospitals and Clinics |

85.3% |

|

Region |

West and Central India |

32.0% |

Product Insights:

- Immunoglobulins

- Albumin

- Coagulation Factor VIII

- Coagulation Factor IX

Immunoglobulins dominate with a market share of 46.3% of the total India plasma fractionation market in 2025.

Immunoglobulins represent the most widely utilized class of plasma-derived therapeutics in India. Their wide range of therapeutic applications includes autoimmune diseases, primary and secondary immunodeficiency disorders, and neurological ailments, such as chronic inflammatory demyelinating polyneuropathy and Guillain-Barré syndrome. Immunoglobulin-based treatments are gaining demand in hospitals and specialty clinics due to the rising diagnosis rates of immune-related illnesses. Physician confidence in prescribing these medicines for a variety of complicated immune-mediated illnesses has also been bolstered by their recognized safety profile and demonstrated clinical efficacy.

In addition to treating immunodeficiency, immunoglobulins are being used more frequently in clinical specialties for diseases, such as myasthenia gravis, Kawasaki illness, and idiopathic thrombocytopenic purpura, which reflects growing therapeutic indications. Rising physician knowledge of the effectiveness of intravenous immunoglobulin therapy, better insurance coverage, and easier access to healthcare in urban and semi-urban areas assist this segment. Over the course of the projection period, the segment's market leadership is anticipated to be further sustained by the use of subcutaneous immunoglobulin formulations, which provide patients with better convenience and improved tolerability when compared to intravenous options.

Sector Insights:

- Private Sector

- Public Sector

Private sector leads with a share of 75.0% of the total India plasma fractionation market in 2025.

The private sector commands a decisive majority of the India plasma fractionation market, driven by superior investment capacity, advanced clinical infrastructure, and strong procurement networks. Private hospitals and clinics actively source plasma-derived products, including albumin, immunoglobulins, and coagulation factors, to meet the demands of critical care, surgical, and chronic disease management. The presence of well-established multi-specialty hospital chains further strengthens the sector’s ability to deliver advanced plasma-based therapies efficiently.

The private sector’s dominance is further reinforced by the willingness of private healthcare institutions to invest in specialized plasma therapies, particularly for rare disease management and complex surgical procedures. Private pharmaceutical companies and fractionators have accelerated capacity expansion and technological upgradation, enabling higher product yields and improved compliance with international quality and safety standards. This competitive environment within the private sector fosters innovation and diversification of plasma-derived product portfolios, ultimately improving the overall availability and quality of therapies across India’s diverse healthcare landscape.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Neurology

- Immunology

- Hematology

- Others

Immunology exhibits a clear dominance with a 53.9% share of the total India plasma fractionation market in 2025.

Immunology represents the most prominent application segment within the India plasma fractionation market, anchored by the high prevalence of primary and secondary immunodeficiency disorders across the population. The administration of intravenous immunoglobulin therapies forms the cornerstone of treatment for conditions, ranging from common variable immunodeficiency to autoimmune diseases, such as systemic lupus erythematosus and immune thrombocytopenic purpura. Rising diagnosis rates of immune-related disorders are further strengthening the demand for immunoglobulin-based treatments.

Beyond primary immunodeficiency, the immunology segment gains from the increasing acceptance of plasma-derived treatments for autoimmune diseases, where immunoglobulins are utilized to inhibit inflammatory cascades and modify aberrant immune responses. Evidence-based plasma therapy is being adopted by India's fast growing specialist immunology and rheumatology community, and early referral and treatment initiation rates are being improved by raising general practitioner understanding. The segment's long-term expansion is being aided by the increased accessibility of diagnostic technologies for immune system disorders, which makes it possible to identify individuals who benefit from continued immunoglobulin therapy in early stages.

End User Insights:

- Hospitals and Clinics

- Clinical Research Laboratories

- Academic Institutes

Hospitals and clinics represent the leading segment with a 85.3% share of the total India plasma fractionation market in 2025.

Hospitals and clinics serve as the cornerstone of plasma-derived therapy administration in India, managing a wide spectrum of patients requiring albumin, immunoglobulins, and coagulation factors across acute, chronic, and critical care settings. The integration of plasma therapies in intensive care units, surgical wards, and specialized hematology and immunology departments has significantly expanded their utilization. The presence of trained medical professionals and advanced monitoring facilities enables the safe administration of complex plasma-based treatments.

The sustained dominance of hospitals and clinics is further reinforced by their capacity to manage complex therapeutic protocols requiring trained clinical oversight, which is essential for plasma-derived product administration. With India’s ongoing healthcare infrastructure expansion, encompassing the establishment of new specialty hospitals and multi-specialty care centers across tier-2 and tier-3 cities, the geographic reach of plasma therapy delivery is progressively widening. Government schemes targeting healthcare coverage expansion and hospital bed additions are expected to increase the volume of plasma-derived product utilization across diverse clinical settings throughout the forecast period.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India comprises the largest region with a 32.0% share of the total India plasma fractionation market in 2025.

West and Central India stands as the leading regional market for plasma fractionation, anchored by the dense concentration of advanced healthcare facilities, pharmaceutical manufacturing hubs, and clinical research institutions in Maharashtra, Gujarat, and Madhya Pradesh. The region’s prominence reflects its strong biopharmaceutical industrial base and well-developed hospital networks. Several major metropolitan cities in this region host leading tertiary care hospitals and specialty treatment centers. Additionally, strong logistics and distribution infrastructure supports efficient supply and availability of plasma-derived therapies across healthcare institutions.

West and Central India’s dominant market position is further underpinned by higher per capita healthcare expenditure, a large urban patient population with greater access to specialist care, and a well-established network of private super-specialty hospitals that consistently procure plasma-derived products. The region’s pharmaceutical manufacturing ecosystem, particularly in Gujarat, also supports downstream fractionation activities, reinforcing both supply-side capabilities and demand-side strength throughout the forecast period. This integrated ecosystem further strengthens the region’s leadership in plasma-derived therapeutic distribution.

Market Dynamics:

Growth Drivers:

Why is the India Plasma Fractionation Market Growing?

Rising Prevalence of Immunodeficiency Disorders and Bleeding Conditions

India is experiencing a substantial and escalating burden of primary immunodeficiency disorders and inherited bleeding conditions, both of which require sustained management with plasma-derived therapies. Primary immunodeficiency disorders arise from genetic defects affecting immune system function and necessitate long-term immunoglobulin replacement therapy to prevent recurrent and potentially life-threatening infections. As diagnostic capabilities improve through enhanced laboratory infrastructure and growing clinical awareness, more patients across urban and rural India are being accurately identified and directed toward appropriate plasma-derived interventions. Simultaneously, secondary immunodeficiency conditions, driven by the increasing incidence of cancer treatments, organ transplantation, and the broader adoption of immunosuppressive regimens, have substantially expanded the patient population requiring immunoglobulin supplementation. The growing recognition of the efficacy of plasma-derived therapies in neurological conditions, such as Guillain-Barré syndrome and chronic inflammatory demyelinating polyneuropathy, is further widening clinical applications.

Supportive Government Policies and Healthcare Infrastructure Development

India’s government has implemented a series of progressive policy frameworks that directly support the growth of the plasma fractionation market. Through mandates on plasma mobilization from licensed blood banks and fractionation-focused initiatives, the government is systematically increasing the supply of raw plasma available to fractionators. Regulatory reforms have progressively streamlined the licensing and operational framework for plasma fractionation centers, encouraging both established pharmaceutical entities and specialized biopharmaceutical players to invest in and expand domestic fractionation capacity. Government procurement programs, particularly those targeting the treatment of hemophilia, immunodeficiency disorders, and critical care conditions, are creating stable demand channels that reduce commercial risk for domestic manufacturers. Healthcare infrastructure development under flagship government schemes is expanding hospital bed capacity, surgical volumes, and intensive care facilities, which directly increase the consumption of albumin, coagulation factors, and immunoglobulins. These policy-led developments are progressively attracting investment and fostering a more self-sufficient domestic plasma fractionation ecosystem in India.

Expansion of Domestic Manufacturing Capacity and Technological Upgradation

The India plasma fractionation market is undergoing a structural transformation, driven by the expansion of domestic manufacturing capacity and the adoption of advanced fractionation technologies. The establishment and scaling of private-sector plasma fractionation facilities is progressively addressing this supply gap, creating a more resilient and cost-competitive domestic supply chain. Advanced separation techniques, including high-performance liquid chromatography and membrane-based filtration, are enabling manufacturers to achieve higher purity levels, improved product yields, and a broader range of therapeutic proteins from a given volume of plasma. The integration of automated processing and real-time quality monitoring systems is reducing production variability and enhancing compliance with international regulatory standards, opening pathways for export and global market participation. Investments in viral safety and inactivation technologies are further improving the safety profile of domestically produced plasma-derived products, strengthening both clinician confidence and regulatory approval prospects.

Market Restraints:

What Challenges the India Plasma Fractionation Market is Facing?

Limited Domestic Plasma Collection and Supply Chain Constraints

The India plasma fractionation market faces a significant challenge due to inadequate domestic plasma collection relative to clinical demand, creating a structural supply gap that limits fractionation output. Only a fraction of collected blood undergoes component preparation and plasma mobilization for fractionation purposes, constraining the availability of high-quality source plasma. Issues, such as storage deterioration, contamination risks, and logistical inefficiencies, further reduce the effective plasma supply available to fractionators, perpetuating dependence on costly imports.

High Capital Requirements and Complex Regulatory Framework

Establishing a plasma fractionation facility requires substantial capital investment, along with a prolonged development timeline of several years before achieving operational readiness. The technical complexity of fractionation processes, combined with stringent Good Manufacturing Practice compliance requirements and multi-stage regulatory approvals from national authorities, creates significant entry barriers. Smaller companies and new market entrants face considerable financial and operational challenges in navigating these requirements, limiting the expansion of the domestic manufacturing base and potentially constraining competitive price discovery within the India plasma fractionation market.

Low Awareness and Diagnostic Gaps in Under-Served Regions

Despite overall market growth, significant gaps in clinical awareness and diagnostic infrastructure persist in rural and semi-urban regions of India, limiting the identification and treatment of conditions requiring plasma-derived therapies. Many patients with primary immunodeficiency disorders, bleeding conditions, and autoimmune diseases remain undiagnosed or receive delayed diagnoses, reducing demand realization for plasma-derived products. The uneven geographic distribution of specialist healthcare facilities further restricts patient access to immunoglobulin and coagulation factor therapies, creating inequality in treatment outcomes across different regions of the country.

Competitive Landscape:

The India plasma fractionation market operates within a relatively concentrated competitive environment, characterized by a small number of domestic manufacturers complemented by the presence of global plasma-derived therapy suppliers. Domestic players focus on developing diverse product portfolios encompassing albumin, immunoglobulins, and coagulation factors, while leveraging regulatory familiarity and established relationships with government health programs and private hospital networks to sustain their market positions. Strategic initiatives, such as capacity expansions, product launches, and distribution network development, are key competitive drivers among domestic participants. The competitive landscape is expected to intensify as more domestic manufacturers achieve commercial-scale operations, and as India’s import substitution drive attracts further private investment into the sector.

India Plasma Fractionation Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Immunoglobulins, Albumin, Coagulation Factor VIII, Coagulation Factor IX |

| Sectors Covered | Private Sector, Public Sector |

| Applications Covered | Neurology, Immunology, Hematology, Others |

| End Users Covered | Hospitals and Clinics, Clinical Research Laboratories, Academic Institutes |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Plasma Fractionation Market Research Report and Industry Forecast Report

The India plasma fractionation market size was valued at USD 389.95 Million in 2025.

The India plasma fractionation market is expected to grow at a compound annual growth rate of 4.15% from 2026-2034 to reach USD 569.69 Million by 2034.

Immunoglobulins dominated the market with a share of 46.3%, driven by the high prevalence of primary immunodeficiency disorders and autoimmune conditions in India, and their broad clinical applicability across immunology, neurology, and critical care specialties.

Key factors driving the India plasma fractionation market include the rising prevalence of immunodeficiency and bleeding disorders, supportive government policies, expanding domestic manufacturing capacity, and growing clinical adoption of plasma-derived therapies across immunology, hematology, and critical care specialties.

Major challenges include limited domestic plasma collection capacity, high capital requirements and complex regulatory frameworks for establishing fractionation facilities, inadequate diagnostic infrastructure in rural regions, and continued dependence on imports to meet clinical demand for certain specialized plasma-derived therapeutic products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)