India Plastic Pipes Market Size, Share, Trends and Forecast by Type, Diameter, End Use, and Region, 2026-2034

India Plastic Pipes Market Summary:

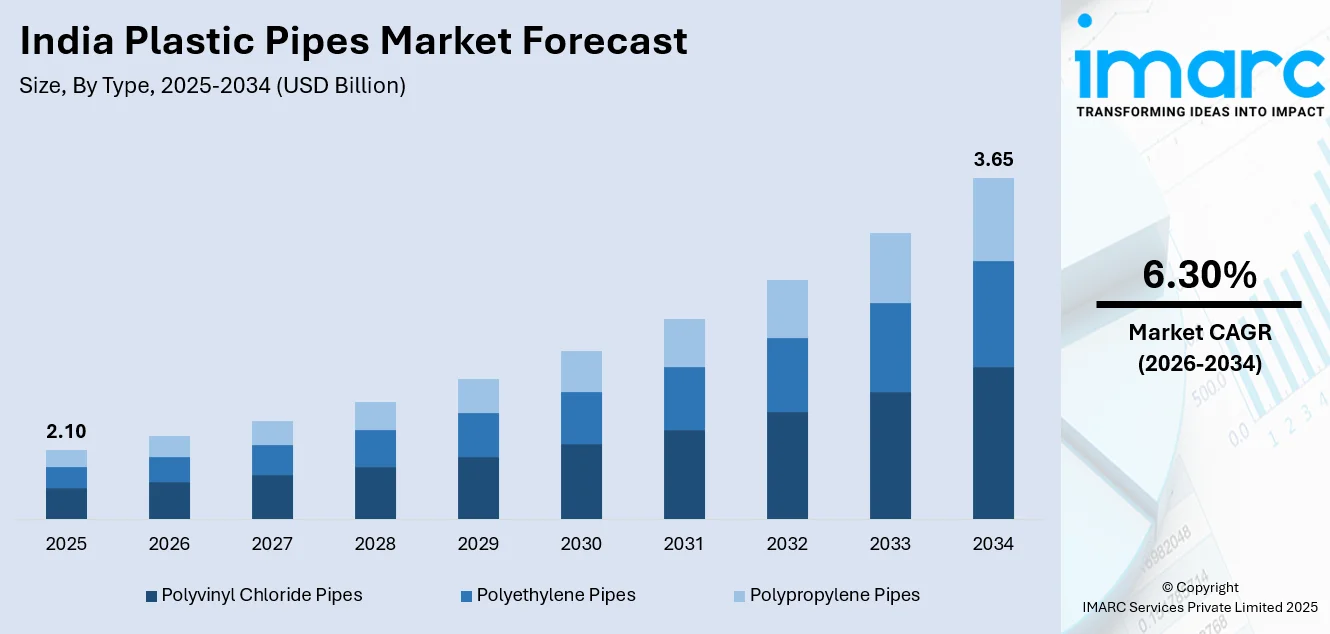

The India plastic pipes market size was valued at USD 2.10 Billion in 2025 and is projected to reach USD 3.65 Billion by 2034, growing at a compound annual growth rate of 6.30% from 2026-2034.

The market is primarily driven by supportive government initiatives including the Jal Jeevan Mission and Smart Cities Mission, which are creating substantial demand for plastic piping solutions in water supply and urban infrastructure projects. The expanding agricultural sector, with increasing adoption of micro-irrigation systems, continues to fuel demand for durable and cost-effective piping solutions. Additionally, the booming real estate sector across tier-2 and tier-3 cities, coupled with the ongoing replacement of aging galvanized iron pipes with modern plastic alternatives, is strengthening the India plastic pipes market share.

Key Takeaways and Insights:

- By Type: Polyvinyl chloride Pipes dominate the market with a share of 55% in 2025, owing to their adaptability, affordability, and resistance to corrosion. Their extensive use spans irrigation, plumbing, and drainage applications across both residential and agricultural sectors, making them a preferred choice for a wide range of piping needs.

- By Diameter: <50mm leads the market with a share of 28% in 2025, driven by their extensive use in residential plumbing applications, drip irrigation systems, and small-scale water distribution networks.

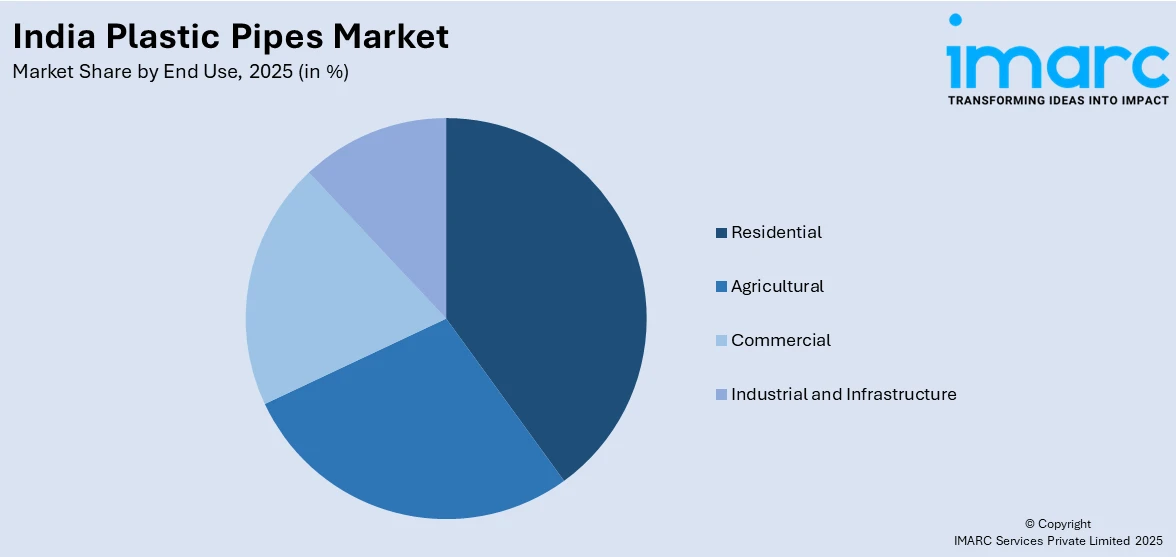

- By End Use: Residential represents the largest segment with a market share of 34% in 2025, supported by robust housing construction activity, urban development projects, and the ongoing transition from metal to plastic plumbing systems.

- By Region: North India dominates the market with a share of 32% in 2025, driven by intensive urbanization, infrastructure development, and significant government investment in water supply and sanitation projects.

- Key Players: The India plastic pipes market exhibits moderate competitive intensity, with established domestic manufacturers competing alongside multinational corporations. The market is witnessing consolidation as leading players expand their product portfolios through strategic acquisitions and capacity additions across diverse geographic regions.

To get more information on this market Request Sample

The Indian plastic pipes market is witnessing strong growth, supported by major government initiatives and ongoing infrastructure development programs. Expanding rural water supply and irrigation projects are generating steady demand for reliable and durable piping solutions. Compared to global benchmarks, per-capita consumption of pipes in India remains relatively low, highlighting considerable growth opportunities. Technological advancements, such as UV-resistant polymers, antimicrobial coatings, and cross-linked polyethylene (PEX) innovations, are enhancing product performance and longevity. In addition, increased government support for irrigation and water management programs is reinforcing market expansion, encouraging manufacturers to scale up production and adopt modern materials. These combined factors, rising infrastructure investment, technological progress, and policy backing, are positioning India’s plastic pipes industry for sustained growth across residential, agricultural, and commercial applications.

India Plastic Pipes Market Trends:

Government-Driven Infrastructure Development

The Indian government’s large-scale infrastructure programs are driving strong growth in the plastic pipes market. Initiatives like the Jal Jeevan Mission and the Smart Cities Mission are expanding access to a reliable water supply and modernizing urban water networks. Extensive pipeline networks, often monitored through advanced SCADA systems, are being installed to improve efficiency and service delivery. These developments are creating steady demand for durable PVC and HDPE pipes, as both rural and urban projects require reliable, long-lasting piping solutions for water distribution and drainage systems.

Technological Advancements and Product Diversification

Manufacturers are expanding their product offerings with advanced polymer-based materials for enhanced performance. Innovations include UV-resistant polymers for agricultural applications, antimicrobial pipes for potable water systems, and CPVC pipes for hot water plumbing. For instance, in October 2024, DCW Limited announced USD 16.8 million investment to expand CPVC production capacity from 20,000 to 50,000 metric tons. The integration of IoT technology in PVC pipes enables real-time monitoring, reducing maintenance costs and enhancing system efficiency across infrastructure applications.

Rising Adoption in Agricultural Irrigation

The agricultural sector is increasingly adopting plastic pipes to support efficient irrigation systems. Micro-irrigation and drip irrigation techniques, which rely on small-diameter plastic pipes, are becoming more prevalent, driven by government initiatives and subsidies that help farmers offset installation costs. These measures encourage wider implementation of modern water-saving practices across farms. Continued policy support and increased funding for irrigation programs aim to expand coverage, improve water-use efficiency, and enhance crop productivity, reinforcing the role of plastic piping solutions as a critical component of modern agricultural infrastructure.

Market Outlook 2026-2034:

The Indian plastic pipes market is poised for robust growth, fueled by ongoing investments in infrastructure, rapid urbanization, and modernization in the agricultural sector. Rising demand for efficient water management systems and advanced plumbing solutions is encouraging manufacturers to scale up domestic production capacities. At the same time, technological innovations in pipe materials, such as CPVC and uPVC, are improving product performance, durability, and versatility. These factors collectively strengthen market competitiveness, enabling companies to meet the evolving needs of residential, commercial, and agricultural applications across the country. The market generated a revenue of USD 2.10 Billion in 2025 and is projected to reach a revenue of USD 3.65 Billion by 2034, growing at a compound annual growth rate of 6.30% from 2026-2034.

India Plastic Pipes Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Polyvinyl Chloride Pipes |

55% |

|

Diameter |

<50mm |

28% |

|

End Use |

Residential |

34% |

|

Region |

North India |

32% |

Type Insights:

- Polyvinyl Chloride Pipes

- Polyethylene Pipes

- Polypropylene Pipes

Polyvinyl chloride pipes dominates with a market share of 55% of the total India plastic pipes market in 2025.

PVC pipes continue to dominate the India market due to their exceptional versatility, cost-effectiveness, and proven performance across diverse applications. These pipes offer superior resistance to corrosion, chemicals, and abrasion, making them ideal for both underground and above-ground installations. The segment benefits from widespread adoption in agricultural irrigation, where uPVC pipes are preferred for their lightweight construction, pressure resistance, and ease of installation. For instance, in March 2023, Finolex Industries expanded production with a new PVC fittings plant in Pune, investing INR 100 crore to meet growing market demand.

The PVC segment is bolstered by advancements in technology, such as CPVC pipes for hot water systems and uPVC pipes for sewage management. uPVC, unlike traditional PVC, is free of plasticizers, making it more rigid and resistant to UV exposure and weathering. Continued replacement of aging galvanized iron pipes in existing buildings supports steady demand, while domestic manufacturers are expanding production capacity to meet the growing requirements of the market.

Diameter Insights:

- <50mm

- 50-100mm

- 100-200mm

- 200-400mm

- 400-700mm

- >700mm

<50mm leads the market with a share of 28% of the total India plastic pipes market in 2025.

Small diameter pipes under 50mm dominate the market driven by their extensive application in residential plumbing, drip irrigation systems, and last-mile water distribution networks. These pipes are essential components in micro-irrigation installations, which have covered over 95 lakh hectares under the PMKSY scheme through December 2024. The lightweight construction and easy installation characteristics make them ideal for both rural and urban applications, particularly in projects requiring flexibility and maneuverability in confined spaces.

The segment benefits from the Jal Jeevan Mission's focus on providing individual household tap connections, requiring extensive small-diameter piping networks. In April 2025, the Union Cabinet sanctioned INR 1,600 crore for the M-CADWM sub-scheme under PMKSY, facilitating direct water delivery to farm gates through underground pressurised piped systems for landholdings up to 1 hectare, further driving demand for small diameter pipes.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Agricultural

- Commercial

- Industrial and Infrastructure

Residential exhibits clear dominance with a 34% share of the total India plastic pipes market in 2025.

The residential segment dominates the plastic pipe market, supported by strong housing construction and the gradual shift from conventional metal pipes to modern plastic alternatives. Growing urbanization and evolving middle-class preferences are driving demand for advanced plumbing solutions in new homes. The segment is further strengthened by the increasing adoption of CPVC pipes, valued for their thermal stability and ease of installation. Manufacturers are also expanding capacity with new facilities to meet the rising residential demand.

The residential sector has demonstrated resilience with sustained demand from the replacement of aging GI pipes, which have an average lifespan of 20-25 years and are prone to corrosion. Despite cyclical fluctuations in real estate launches, PVC and CPVC pipe sales have remained strong due to this replacement demand. Tier-2 and tier-3 cities are emerging as growth centers, with manufacturers expanding their distribution networks to capture this expanding residential construction activity.

Regional Insights:

- North India

- South India

- East India

- West India

North India represents the largest share with 32% of the total India plastic pipes market in 2025.

North India leads the plastic pipe market, fueled by rapid urbanization, extensive infrastructure development, and strong government initiatives in water supply and sanitation projects. High population density and growing construction activity in key urban centers further support market growth. For example, in March 2025, Prince Pipes and Fittings inaugurated its eighth manufacturing facility in Begusarai, Bihar, reflecting a strategic push to strengthen its presence in the northern market and cater to increasing urban demand for piping solutions.

The region’s thriving agricultural sector also contributes significantly to market expansion, generating strong demand for irrigation and farm-level piping systems. Investments in modern irrigation practices and rural water delivery projects drive adoption of plastic pipes, making North India a key growth hub. The combination of urban infrastructure projects and agricultural requirements positions the region as a critical market for manufacturers looking to capitalize on rising water management and construction-related piping needs.

Market Dynamics:

Growth Drivers:

Why is the India Plastic Pipes Market Growing?

Government Infrastructure Initiatives Driving Unprecedented Demand

The Indian government's transformative infrastructure programs are creating sustained demand for plastic piping solutions. For instance, by February 1, 2025, the Jal Jeevan Mission had expanded tap water access to an additional 12.20 crore rural households, raising overall coverage to more than 15.44 crore homes across India. This translates to nearly four-fifths of the rural population now having household water connections. Launched on August 15, 2019, by Prime Minister Narendra Modi, the mission has progressed sharply from its initial stage, when only about 3.23 crore rural households had access to tap water. This mission involves massive pipeline networks for water supply and distribution across rural India. The Smart Cities Mission has completed over 7,500 projects valued at INR 1.51 lakh crore. The project also includes an extensive network of water pipelines that are continuously supervised through SCADA-based monitoring systems to ensure efficient operation and real-time control. These government initiatives provide long-term visibility for sustained market growth.

Expanding Agricultural Irrigation Sector

The agricultural sector accounts for approximately 40% of total plastic pipe consumption in India, with significant growth potential as only half of India's farmland is currently irrigated. The Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) provides financial assistance covering 55% of micro-irrigation costs for small farmers and 45% for others. Between FY16 and FY25, INR 21,968 crore was allocated for the Per Drop More Crop component, covering 95.58 lakh hectares with micro-irrigation systems. Budgetary support for the Pradhan Mantri Krishi Sinchayee Yojana was strengthened to enhance irrigation infrastructure and water management initiatives. In parallel, additional approvals were granted to expand piped water delivery systems directly to agricultural fields under the M-CADWM program, reinforcing efforts to improve farm-level water access and boost irrigation efficiency across rural areas.

Rapid Urbanization and Real Estate Development

India's rapid urbanization and expanding middle class are driving demand for modern plumbing and piping solutions across residential, commercial, and industrial construction. By 2036, India’s towns and cities are projected to house around 600 million people, accounting for 40% of the total population, up from 31% in 2011. Urban areas are also expected to drive economic growth, contributing nearly 70% of the country’s GDP, underscoring the growing significance of cities as centers of population and economic activity. The country's per-capita pipe consumption remains significantly lower than the global average and major economies like the US, Europe, and China, indicating substantial headroom for growth. The plastic pipe market is expected to see strong expansion, driven by a healthy housing cycle that continues to stimulate demand for piping solutions across residential construction and related infrastructure segments. Tier-2 and tier-3 cities are emerging as significant growth centers, with manufacturers expanding distribution networks. Modern plastic pipes are replacing aging galvanized iron pipes due to their lower costs, easier installation, and longer lifespan, maintaining demand even during real estate slowdowns.

Market Restraints:

What Challenges is the India Plastic Pipes Market Facing?

Raw Material Price Volatility

PVC and CPVC resins form a major share of plastic pipe manufacturing costs and are derived from petrochemicals, making prices highly volatile. Fluctuations in crude oil markets lead to frequent resin price swings, creating margin pressure for manufacturers. Sudden price corrections often result in inventory losses and cautious distributor behavior, which together disrupt sales volumes and profitability across the value chain.

Import Competition and Trade Challenges

India’s plastic pipes industry relies heavily on imported polymer resins, exposing it to global trade dynamics and geopolitical risks. Weak demand in major producing countries has intensified the inflow of low-priced PVC into India, heightening competitive pressure. Delays in trade protection measures and regulatory rollbacks have further increased exposure to cheaper imports, impacting domestic producers’ pricing power and capacity utilization.

Environmental Regulations and Compliance Requirements

Tighter environmental regulations governing plastic usage and waste management are reshaping industry operations in India. Manufacturers are required to adopt responsible recycling, disposal, and sustainability practices, which demand additional capital and operational adjustments. These compliance costs can strain profitability and disproportionately affect smaller players, potentially accelerating industry consolidation as larger firms are better positioned to absorb regulatory expenses.

Competitive Landscape:

The India plastic pipes market exhibits moderate competitive intensity, with established domestic manufacturers competing alongside international players across price segments. The organized sector has gained market share as leading players leverage established supplier relationships, extensive distribution networks, and brand recognition to navigate volatile market conditions. The market is witnessing consolidation through strategic acquisitions and capacity expansions as major players strengthen their positions. Competition is intensifying due to low entry barriers, with price wars emerging as larger players seek to maintain market share. Technological innovation in product development and manufacturing processes has become a key differentiator, with players investing in advanced materials and sustainable production methods to meet evolving customer requirements.

Recent Developments:

- March 2025: Supreme Industries signed a memorandum of understanding to acquire Wavin Industries' pipes and fittings business for USD 30 million (approximately INR 262 crores). Wavin India, part of the Orbia Group, manufactures a range of piping systems under the 'Wavin' brand within the country. This acquisition reflects Supreme Industries’ strategic move to expand its footprint in the Indian piping solutions market.

- March 2025: Ashirvad Pipes announced approximately Rs 400 crore investment in two new greenfield manufacturing facilities in Chennai and Hyderabad by FY2027, targeting the South Indian market.

- June 2024: Rollepaal established an exclusive agreement with Sintex, a subsidiary of Welspun World conglomerate, providing RBlue extrusion lines for PVCO pipes to increase efficiency in producing high-quality pipes for potable water applications.

India Plastic Pipes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Polyvinyl Chloride Pipes, Polyethylene Pipes, Polypropylene Pipes |

| Diameters Covered | <50mm, 50-100mm, 100-200mm, 200-400mm, 400-700mm, >700mm |

| End Uses Covered | Residential, Agricultural, Commercial, Industrial and Infrastructure |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India plastic pipes market size was valued at USD 2.10 Billion in 2025.

The India plastic pipes market is expected to grow at a compound annual growth rate of 6.30% from 2026-2034 to reach USD 3.65 Billion by 2034.

Polyvinyl chloride pipes dominated with 55% market share in 2025, driven by their versatility, cost-effectiveness, corrosion resistance, and widespread adoption across agricultural irrigation, plumbing, and drainage applications in both residential and commercial sectors.

Key factors driving the India plastic pipes market include supportive government initiatives like Jal Jeevan Mission and Smart Cities Mission, expanding agricultural irrigation through PMKSY, rapid urbanization, booming real estate sector, and the ongoing replacement of aging galvanized iron pipes with modern plastic alternatives.

Major challenges include volatile raw material prices particularly PVC resin linked to crude oil fluctuations, import competition from countries like China, compliance with environmental regulations under Plastic Waste Management Rules 2022, and intensifying competition from unorganized sector players.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)