India Power Electronics Market Size, Share, Trends and Forecast by Device, Material, Application, Voltage, End Use Industry, and Region, 2026-2034

India Power Electronics Market Summary:

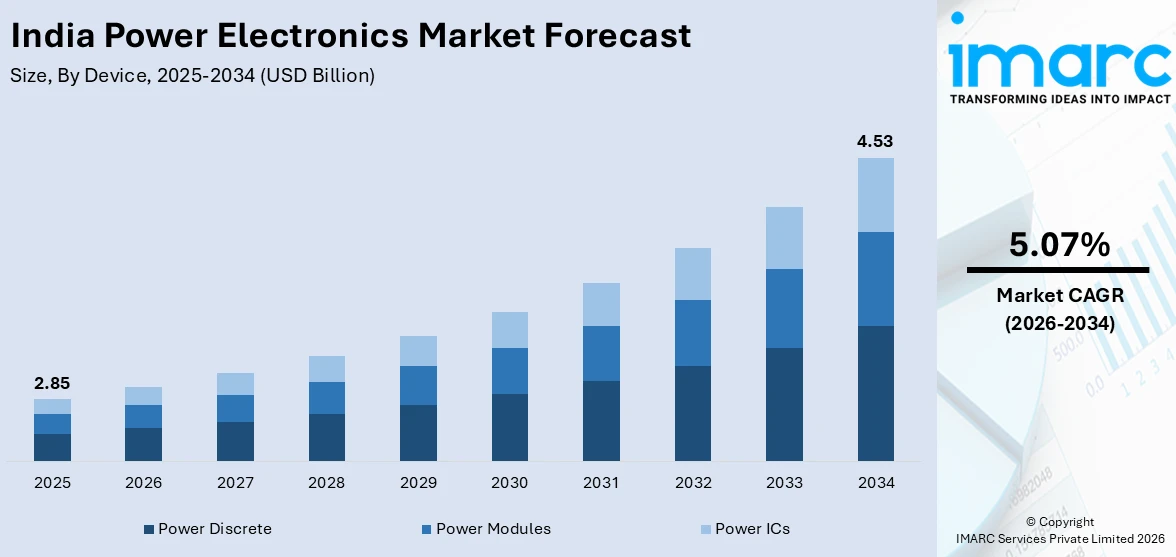

The India power electronics market size was valued at USD 2.85 Billion in 2025 and is projected to reach USD 4.53 Billion by 2034, growing at a compound annual growth rate of 5.07% from 2026-2034.

The market is driven by the rapid expansion of renewable energy infrastructure, accelerating electric vehicle adoption, and growing industrial automation across key manufacturing sectors. Rising demand for energy-efficient systems, expanding grid modernization efforts, and government-backed semiconductor development programs are reinforcing long-term growth momentum. Increasing consumer electronics penetration, proliferation of smart devices, and widening power management applications are collectively elevating India's prominence in the global India power electronics market share.

Key Takeaways and Insights:

- By Device: Power discrete dominates the market with a share of 50.0% in 2025, driven by the widespread use of discrete switching and rectification devices across consumer, industrial, and automotive power applications.

- By Material: Silicon leads the market with a share of 85.0% in 2025, owing to established manufacturing infrastructure, cost competitiveness, and broad compatibility with consumer electronics and general-purpose industrial applications.

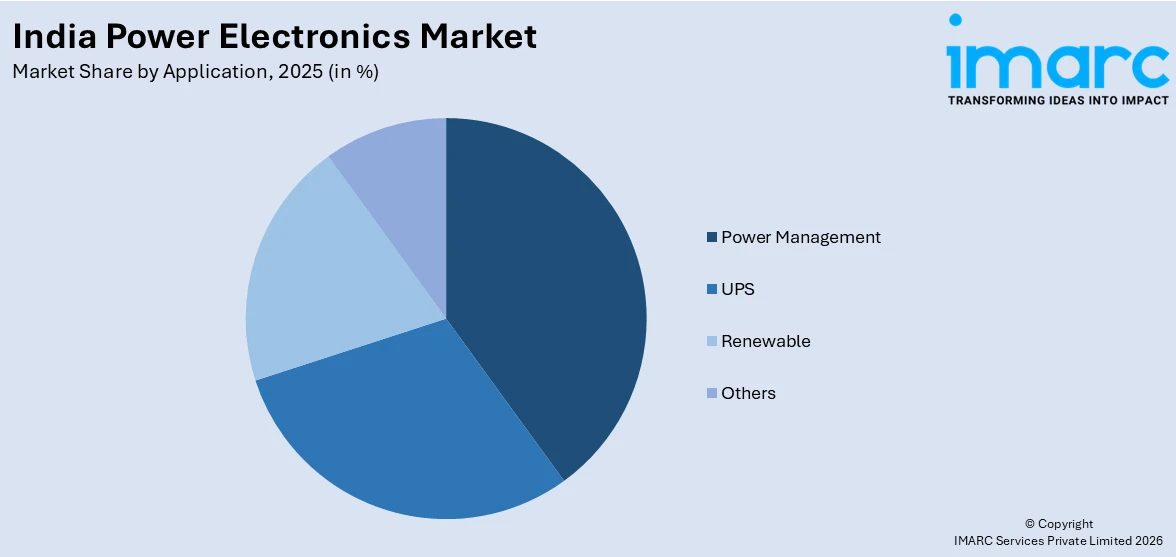

- By Application: Power management represents the largest segment with a market share of 35.5% in 2025, driven by demand across smartphones, data centers, industrial controls, and embedded electronics requiring stable and efficient power delivery.

- By Voltage: Low voltage dominates the market with a share of 60.0% in 2025, owing to high demand for compact consumer electronics, portable devices, and low-power industrial equipment driving segment leadership.

- By End Use Industry: Consumer electronics leads the market with a share of 35.0% in 2025, driven surging smartphone penetration, rising appliance upgrades, and growing adoption of connected and smart electronic devices.

- By Region: West and Central India leads the market with a share of 29.5% in 2025, owing to dominant industrial base, thriving electronics manufacturing activity, and strong semiconductor investment inflows.

- Key Players: The India power electronics market features a competitive mix of domestic and multinational manufacturers competing across device, module, and integrated circuit categories through technological differentiation, cost optimization, and strategic product portfolio expansion across industrial, automotive, and consumer end-use applications.

To get more information on this market Request Sample

The India power electronics market is propelled by a convergence of structural and policy-driven forces reshaping the country's energy, mobility, and industrial landscape. The rapid scaling of renewable energy capacity has created sustained demand for inverters, converters, and grid integration components across solar and wind installations. As per sources, GoodWe marked a decade in the Indian solar market and announced that cumulative inverter shipments in the country have crossed 6 GW underscoring rising deployment of power electronics in renewable projects. Simultaneously, the accelerating transition toward electric vehicles and charging infrastructure is driving adoption of advanced power modules and battery management components. Government programs promoting semiconductor manufacturing are catalyzing domestic production capabilities at scale. The expansion of telecommunications, smart grid infrastructure, and data centers is further intensifying demand for efficient and reliable power solutions.

India Power Electronics Market Trends:

Growing Adoption of Wide Bandgap Semiconductors in Power Systems

Wide bandgap materials such as silicon carbide and gallium nitride are progressively replacing conventional silicon in high-performance power applications across India. These advanced materials deliver superior thermal stability, higher switching frequencies, and significantly reduced power losses, making them ideal for electric vehicle inverters, renewable energy systems, and industrial motor drives. In April 2025, Polymatech Electronics announced the foundation of India’s first dedicated gallium nitride (GaN) semiconductor chip plant in Nava Raipur, Chhattisgarh, a ₹1,143 crore project supported by state incentives to increase GaN chip manufacturing for rising frequency and high efficiency applications. Growing awareness of their efficiency advantages is encouraging design engineers across automotive and energy sectors to adopt these materials in next-generation power systems.

Expansion of Domestic Semiconductor Manufacturing Ecosystem

India's power electronics landscape is undergoing a structural transformation as government-backed semiconductor ecosystem initiatives gain momentum across multiple states. The establishment of silicon fabrication units, compound semiconductor facilities, and advanced assembly and testing infrastructure is progressively reducing reliance on imported components. In February 2026, India’s Prime Minister inaugurated the ₹22,516 crores Semiconductor Assembly, Test, Marking & Packaging (ATMP) facility of the US-based company Micron Technology in Sanand, Gujarat, and the commercial production of memory chips has begun. State-level policies offering capital support and infrastructure incentives are attracting both domestic and international players to establish manufacturing operations in India.

Smart Grid and Energy Management Applications Driving Demand

India's large-scale grid modernization effort is creating sustained and design-led demand for power electronic devices used in smart metering, energy management, and demand response systems. The national program targeting widespread deployment of prepaid meters is generating high-volume requirements for microcontrollers, power supplies, and communication modules requiring compact and efficient power electronics. In July 2025, REC Power Development and Consultancy Limited (RECPDCL) signed contracts to deploy 33.26 lakh prepaid smart meters across Gujarat under Phase II of the Revamped Distribution Sector Scheme (RDSS), highlighting strong grid‑level adoption of advanced metering infrastructure. This transformation is strengthening the domestic power electronics ecosystem and enabling manufacturers to develop integrated, system-level capabilities.

Market Outlook 2026-2034:

The India power electronics market is poised for steady and sustained growth over the coming years, supported by intensifying investments in renewable energy, electric mobility, semiconductor manufacturing, and smart infrastructure development. Widening application scope across consumer electronics, industrial automation, and telecommunications, combined with government-backed production initiatives and a maturing domestic supply chain, will reinforce revenue momentum. Progressive adoption of advanced power semiconductor materials and integrated module technologies will further accelerate market development and deepen India's position within the global power electronics landscape. The market generated a revenue of USD 2.85 Billion in 2025 and is projected to reach a revenue of USD 4.53 Billion by 2034, growing at a compound annual growth rate of 5.07% from 2026-2034.

India Power Electronics Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Device |

Power Discrete |

50.0% |

|

Material |

Silicon |

85.0% |

|

Application |

Power Management |

35.5% |

|

Voltage |

Low Voltage |

60.0% |

|

End Use Industry |

Consumer Electronics |

35.0% |

|

Region |

West and Central India |

29.5% |

Device Insights:

- Power Discrete

- Diode

- Transistors

- Thyristor

- Power Modules

- Intelligent Power Module

- Power Integrated Module

- Power ICs

- Power Management Integrated Circuit

- Application-Specific Integrated Circuit

Power discrete dominates with a market share of 50.0% of the total India power electronics market in 2025.

Power discrete form the foundational layer of India's power electronics market, encompassing transistors, diodes, thyristors, and rectifiers that enable switching, amplification, and voltage regulation across virtually all electronic systems. Their widespread adoption across consumer electronics, industrial machinery, automotive platforms, and power supply units ensures consistently high and recurring demand. In August 2025, the Union Government approved four semiconductor projects in Punjab including facilities focused on high‑power discrete semiconductor manufacturing such as MOSFETs, IGBTs, and Schottky diodes, under the India Semiconductor Mission, signaling targeted support for discrete power device production.

Manufacturers are progressively developing higher-voltage and higher-current power discrete variants to serve the growing requirements of renewable energy systems and electric vehicle applications. Advancements in packaging technology and gate engineering are improving switching performance and reducing on-state losses, extending the relevance of power discrete devices even as integrated module adoption rises. Their cost advantages, design flexibility, and broad compatibility with existing circuit architectures continue to make them the preferred choice for engineers across industrial, consumer, and automotive design segments throughout India.

Material Insights:

- Silicon

- Sapphire

- Silicon Carbide

- Gallium Nitride

- Others

Silicon leads with a share of 85.0% of the total India power electronics market in 2025.

Silicon remains the commanding material in India's power electronics market, underpinned by its well-established manufacturing infrastructure, broad process maturity, and strong cost competitiveness relative to emerging semiconductor materials. Traditional silicon-based devices continue to serve the vast majority of consumer electronics, industrial automation, and general power supply applications where extreme performance thresholds are not a primary design requirement. The widespread availability of silicon processing equipment, a trained engineering workforce, and mature domestic and global supply chains collectively reinforce its dominant position across commodity and mid-range power device categories throughout India.

Incremental advancements in silicon device architecture continue to expand performance boundaries, enabling silicon-based power components to remain competitive in a growing range of industrial and residential power management applications. Its compatibility with established fabrication processes and deep ecosystem integration makes silicon the default material choice for high-volume, cost-sensitive power electronics designs. As India scales domestic semiconductor manufacturing, silicon-based fabrication infrastructure forms the primary foundation upon which the country's broader power device production capabilities are being built and progressively expanded.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Power Management

- UPS

- Renewable

- Others

Power management exhibits a clear dominance with a 35.5% share of the total India power electronics market in 2025.

Power management represents the largest application segment in India's power electronics market, encompassing voltage regulators, DC-DC converters, battery charging circuits, and power delivery architectures embedded across a wide spectrum of consumer, industrial, and telecommunications systems. The rapid proliferation of smartphones, tablets, wearables, and connected devices is generating sustained demand for advanced power management integrated circuits capable of maximizing energy efficiency and minimizing thermal losses within increasingly compact device form factors. In December 2025, Cyient Semiconductors signed an agreement to acquire a majority stake in Kinetic Technologies for up to USD 93 Mn, expanding India’s power management IC capabilities across data centers, EVs, and industrial applications.

The growing complexity of modern electronic systems is driving demand for intelligent power management solutions capable of dynamic load regulation, adaptive voltage scaling, and real-time power monitoring. Industrial control systems, embedded computing platforms, and smart infrastructure applications are increasingly relying on precision power management components to ensure operational stability and energy optimization. As India's electronics design ecosystem matures, local engineering teams are placing greater emphasis on power management architecture at the system design stage, further entrenching the segment's leadership position across a broadening range of domestic application categories.

Voltage Insights:

- Low Voltage

- Medium Voltage

- High Voltage

Low voltage leads with a market share of 60.0% of the total India power electronics market in 2025.

Low voltage dominates India's market, reflecting the enormous volume of consumer electronics, portable devices, embedded systems, and low-power industrial controls that collectively constitute the core of domestic demand. Applications spanning smartphone charging circuits, laptop adapters, home appliance controls, and LED driver systems represent the highest-volume category for power semiconductor devices, driven by India's rapidly expanding consumer base and rising household electronics penetration. The growth of India's consumer electronics manufacturing sector, supported by government production incentive programs, has further strengthened the domestic supply base for low-voltage power devices across multiple product categories.

The continued expansion of smart home appliances, personal electronics, and connected IoT devices is expected to sustain low-voltage segment leadership throughout the forecast period. Miniaturization trends and rising energy efficiency requirements are encouraging design engineers to adopt increasingly sophisticated low-voltage power solutions capable of delivering higher performance within tighter power budgets. As India's electronics manufacturing ecosystem deepens and domestic design capabilities advance, low-voltage power devices will continue to represent the highest-volume deployment category, anchoring overall market demand and shaping procurement patterns across the domestic power electronics supply chain.

End Use Industry Insights:

- Automotive

- Military and Aerospace

- Energy and Power

- IT and Telecommunication

- Consumer Electronics

- Others

Consumer electronics dominates with a market share of 35.0% of the total India power electronics market in 2025.

Consumer electronics remains the largest end-use industry for power electronics in India, driven by sustained growth in smartphone adoption, expanding household appliance penetration, and the rapid proliferation of connected and smart electronic devices across urban and semi-urban markets. As per sources, India’s 5G smartphone shipments accounted for 89% of total shipments, reflecting strong consumer demand for next‑generation connected devices that embed advanced power management components. India's position as one of the world's fastest-growing consumer electronics markets ensures a consistently high and recurring volume of power management components, battery charging circuits, display driver power supplies, and low-voltage switching devices.

The transition toward energy-efficient appliance designs, guided by government efficiency rating standards, is progressively driving demand for higher-performance power conversion components within air conditioners, washing machines, refrigerators, and other household electronics. The growing adoption of premium smartphones with fast-charging capabilities and sophisticated power delivery architectures is further elevating the performance requirements placed on power electronics components. As domestic electronics manufacturing scales and product categories diversify, the consumer electronics end-use segment will remain the primary volume driver for power semiconductor demand throughout India.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India dominates with a market share of 29.5% of the total India power electronics market in 2025.

West and Central India leads the regional power electronics landscape, driven by a strong concentration of industrial manufacturing, thriving electronics assembly operations, and well-developed commercial infrastructure across its key states. The region benefits from mature industrial corridors, strong port connectivity facilitating component imports, and a growing ecosystem of electronics manufacturing service providers capable of serving both domestic and export-oriented production requirements. State-level semiconductor and electronics policies offering capital support, infrastructure incentives, and streamlined regulatory processes have attracted sustained inflows of domestic and multinational investment into the region's power electronics supply chain.

The region's competitive advantage is further reinforced by its proximity to large end-user markets across consumer electronics, automotive manufacturing, and industrial equipment segments concentrated in the western industrial belt. A deepening base of semiconductor assembly, testing, and packaging facilities is progressively enhancing local value addition and reducing dependence on imported components. As government-backed manufacturing initiatives continue to gain momentum, West and Central India is expected to consolidate its regional leadership position, attracting further investment across the power electronics design, manufacturing, and distribution value chain.

.jpeg)

Market Dynamics:

Growth Drivers:

Why is the India Power Electronics Market Growing?

Rising Electric Vehicle Penetration Across Domestic Mobility Segments

India's accelerating transition toward electric mobility is generating sustained demand for power electronics components across traction inverters, onboard chargers, battery management systems, and DC-DC converters. Growing adoption of electric two-wheelers and three-wheelers in urban and semi-urban markets is creating high-volume requirements for compact, cost-efficient power modules tailored to domestic mobility patterns. According to reports, India sold 11,49,334 electric two‑wheelers and 1,59,235 units electric three‑wheelers under the PM E‑DRIVE scheme, reinforcing IGF‑backed growth in EV power electronics components. Government policies encompassing emission standards, vehicle electrification targets, and charging infrastructure development programs are structurally reinforcing demand across the entire power electronics supply chain serving India's automotive sector.

Expanding Industrial Automation and Manufacturing Modernization

India's manufacturing sector is undergoing progressive modernization, with rising adoption of variable frequency drives, programmable logic controllers, robotic systems, and precision motion control equipment that rely heavily on advanced power electronics for efficient energy conversion and motor management. Government initiatives promoting industrial upgrading, smart factory implementation, and domestic production across strategic sectors are accelerating automation investment. In March 2026, Maharashtra inaugurated the ₹700 cr XSIO Advanced Industrial & Manufacturing Park near Nagpur, integrating AI‑driven infrastructure to support advanced manufacturing and automation technologies. This structural shift is creating broad-based demand for power modules, gate driver circuits, and high-reliability discrete devices capable of operating within demanding industrial environments across diverse manufacturing verticals.

Growing Demand from Telecommunications and Digital Infrastructure

The rapid expansion of telecommunications infrastructure, including next-generation network deployment and base station densification, is creating significant demand for power electronics components used in rectifiers, power conversion units, and backup power systems. In 2025, India deployed over 508,000 5G base transceiver stations (BTS), reflecting accelerated rollout of next-generation mobile networks that rely on efficient power electronics for uninterrupted operation. Simultaneously, the proliferation of data centers supporting cloud computing, digital services, and enterprise workloads is intensifying requirements for highly efficient rack-level power distribution and server power delivery architectures. This convergence of telecom and digital infrastructure growth is establishing telecommunications as a structurally important and consistently expanding end-use segment for India's power electronics market.

Market Restraints:

What Challenges the India Power Electronics Market is Facing?

High Dependency on Imported Semiconductor Components

India's power electronics industry remains significantly dependent on imported semiconductor components, particularly advanced power devices and specialized integrated circuits with limited domestic production availability. This reliance exposes manufacturers to supply chain disruptions, currency fluctuation risks, and pricing volatility stemming from global geopolitical developments. While domestic manufacturing programs are progressively building local production capacity, achieving meaningful import substitution at commercial scale remains a gradual process that continues constraining cost competitiveness across the domestic power electronics supply chain.

Infrastructure Gaps Across Emerging Industrial Regions

Inconsistencies in power grid reliability, limited access to specialized testing facilities, and underdeveloped industrial infrastructure across emerging manufacturing zones create operational challenges for power electronics producers. These gaps increase product development timelines, raise compliance and certification costs, and complicate quality assurance processes. Manufacturers serving geographically dispersed domestic markets must account for variable infrastructure conditions when designing products, adding engineering complexity and constraining the pace of market expansion across underserved industrial regions.

Shortage of Specialized Power Electronics Engineering Talent

The power electronics sector demands engineers with deep expertise in semiconductor physics, thermal management, circuit design, and embedded systems, skill sets that remain insufficient relative to the sector's rapid growth requirements. While academic programs and government skilling initiatives are gradually expanding the talent pipeline, the gap between industry demand and qualified workforce availability persists. This shortfall slows innovation cycles, increases recruitment costs, and limits the domestic capacity to develop advanced power device solutions for emerging high-performance applications.

Competitive Landscape:

The India power electronics market is characterized by a dynamic competitive environment featuring both established multinational semiconductor manufacturers and growing domestic players across device, module, and integrated circuit categories. Global participants leverage advanced process technologies, extensive research and development investments, and broad product portfolios to maintain leadership across high-value application segments. Domestic manufacturers are increasingly competitive in consumer electronics, industrial power supply, and low-voltage device segments, benefiting from proximity to end-market customers and government incentive support. Strategic partnerships between global technology leaders and Indian manufacturing entities are accelerating technology transfer and local production capabilities. Competition is intensifying as semiconductor initiatives attract new entrants and expand the domestic supply base across the entire power electronics value chain.

Recent Developments:

- In December 2025, the PCIM Asia New Delhi Conference debuted, bringing together global experts and Indian authorities to showcase next-generation power electronics for electric mobility, renewable energy, smart grids, and data centers, fostering innovation, collaboration, and domestic talent development in India’s growing power electronics ecosystem.

India Power Electronics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Devices Covered |

|

| Materials Covered | Silicon, Sapphire, Silicon Carbide, Gallium Nitride, Others |

| Applications Covered | Power Management, UPS, Renewable, Others |

| Voltages Covered | Low Voltage, Medium Voltage, High Voltage |

| End Use Industries Covered | Automotive, Military and Aerospace, Energy and Power, IT and Telecommunication, Consumer Electronics, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Power Electronics Market Report

The India power electronics market size was valued at USD 2.85 Billion in 2025.

The India power electronics market is expected to grow at a compound annual growth rate of 5.07% from 2026-2034 to reach USD 4.53 Billion by 2034.

Power discrete held the largest share in the device segment in 2025, driven by widespread use of switching and rectification devices across consumer electronics, industrial equipment, and automotive power applications throughout India.

Key factors driving the India power electronics market include surging renewable energy investments, accelerating electric vehicle adoption, government semiconductor manufacturing initiatives, industrial automation expansion, grid modernization programs, and growing consumer electronics demand across urban and semi-urban markets.

Major challenges include high import dependency on advanced power semiconductors, infrastructure gaps in testing and production facilities, shortage of specialized engineering talent, complex regulatory compliance requirements, and supply chain vulnerabilities affecting component availability and overall manufacturing cost competitiveness.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)