India Power Market Size, Share, Trends and Forecast by Power Source, End User, and Region, 2026-2034

India Power Market Summary:

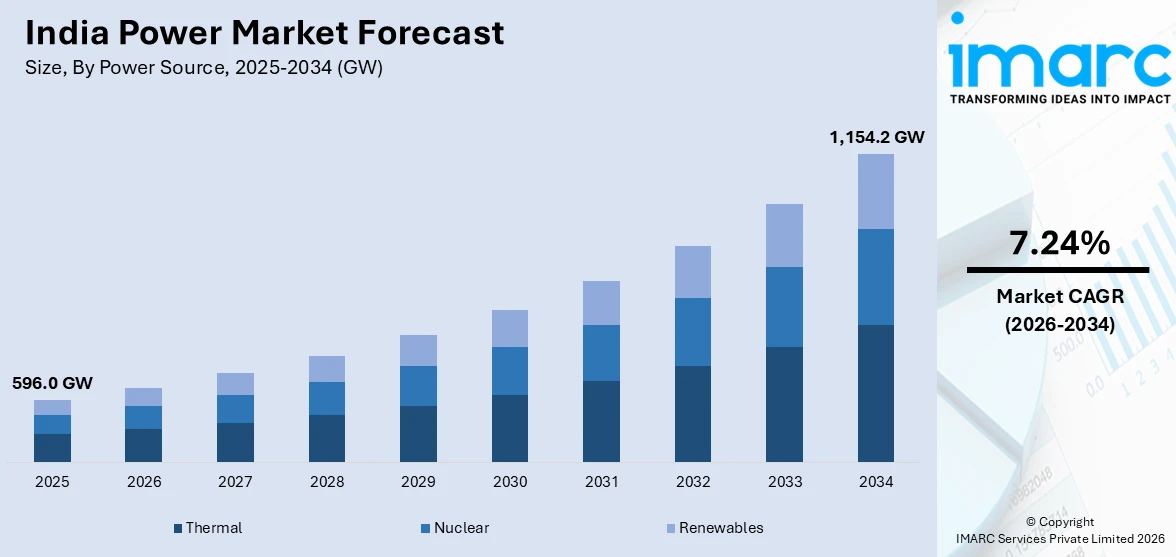

The India power market size reached 596.0 GW in 2025 and is projected to reach 1,154.2 GW by 2034, growing at a compound annual growth rate of 7.24% from 2026-2034.

The India power market is experiencing notable growth, driven by the increasing electricity demand from rapid industrialization, urbanization, and rising per capita usage. Accelerated renewable energy deployment, supportive government policies targeting non-fossil fuel capacity expansion, and large-scale infrastructure modernization are reshaping the energy landscape. The growing investments in transmission networks, energy storage systems, and grid digitalization are enhancing supply reliability and operational efficiency, thus contributing to the India power market share.

Key Takeaways and Insights:

- By Power Source: Thermal dominates the market with a share of 54.6% in 2025, driven by India’s extensive coal reserves, established generation infrastructure, and critical role in providing baseload electricity to meet the country’s rapidly growing energy requirements.

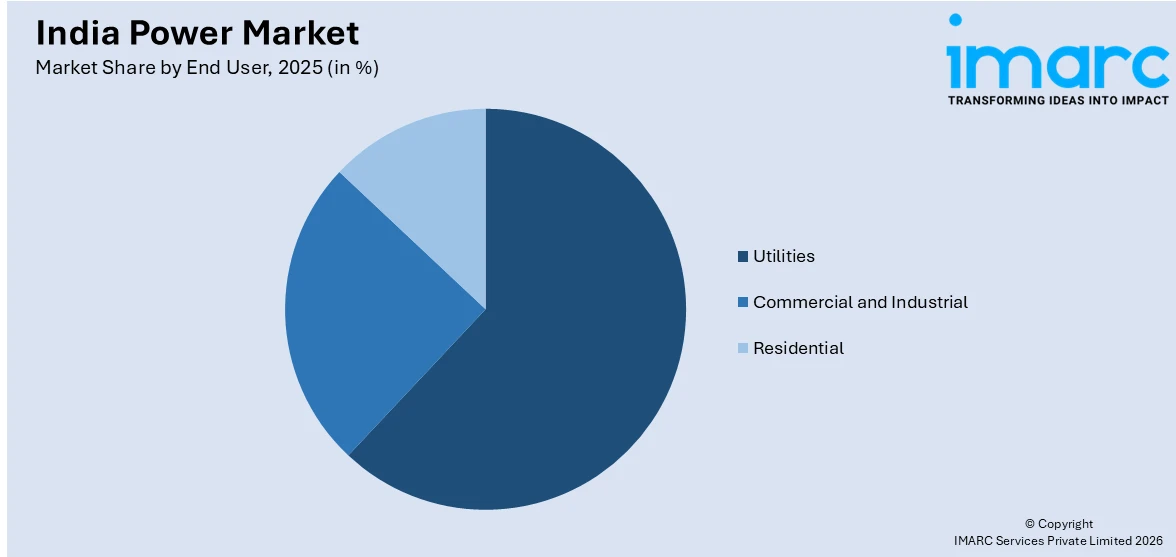

- By End User: Utilities represent the largest segment with a market share of 62.3% in 2025, reflecting the dominance of state-owned distribution companies and central generating stations in managing bulk power procurement, transmission, and distribution across India’s vast electricity network.

- By Region: West India dominates the market with a share of 31.4% in 2025, supported by Gujarat’s substantial thermal and renewable capacity, Maharashtra’s industrial electricity demand, and the region’s advanced grid infrastructure enabling large-scale power generation.

- Key Players: The India power market features intense competition among large state-owned utilities, central generating companies, and private sector conglomerates, with players diversifying across thermal, renewable, nuclear, and hybrid energy portfolios to strengthen their market positioning.

To get more information on this market Request Sample

The India power market is being driven by rising electricity demand from rapid urbanization, industrial expansion, and the growing infrastructure needs across transport, housing, and commercial sectors. Strong government focus on capacity addition, grid modernization, and renewable integration is supporting long term sector growth. Thermal power continues to remain critical for baseload stability and peak demand management, alongside increasing investments in solar, wind, and hybrid projects. As of February 13, 2026, India has 39,545 MW of thermal power projects under construction, including 4,845 MW of stressed projects, with plans to meet a future thermal capacity requirement of 307,000 MW by 2034–35 and add 97,000 MW of coal-based capacity. In addition, technological upgrades, such as smart grids, digital utility platforms, and energy storage, are improving efficiency, while foreign investment and private sector participation are strengthening financing, competition, and innovation across the market.

India Power Market Trends:

Technological Advancements in Power Generation

Technological innovation is playing a major role in improving power generation efficiency in India through smart grids, energy storage systems, and the digitalization of power plants. These advancements reduce operational costs, enhance resource utilization, and support more reliable electricity production. In 2025, the Ministry of Power announced the launch of the India Energy Stack (IES), a national digital infrastructure initiative designed to enable real time data sharing, smart utility operations, and better user access, with a 12 month pilot testing the Utility Intelligence Platform for improved grid efficiency. Continued progress in combined cycle plants and hybrid renewable systems is making generation more adaptable and cost effective.

Foreign Investments and Private Sector Participation

Foreign investment and private sector participation are propelling the growth of India power market by providing capital, technology, and operational expertise. Liberalized policies and eased foreign direct investment (FDI) norms are attracting international and domestic investors across generation, transmission, and distribution segments. According to IBEF, the power sector accounted for about 2.7% of total FDI inflows through June 2025, with cumulative inflows of INR 1,21,734.99 Crore, while the non-conventional energy segment alone received INR 1,69,772.12 Crore between April 2000 and June 2025. These investments are supporting new capacity additions, renewable deployment, grid upgrades, and competitive market development nationwide.

Integration of Smart Grids and Grid Modernization

Smart grids are strengthening India’s power infrastructure by enabling real time monitoring, improved demand response, and efficient distribution management. These systems enhance grid resilience, reduce outages, and facilitate the integration of decentralized renewable energy sources, supporting a more reliable electricity network. In 2025, Vodafone Idea announced plans to deploy 12 million smart meters across India over three years under the National Smart Grid Mission, with the meters managed through its IoT Smart Central platform to reduce losses and improve efficiency. The growing automation of grid operations is expected to meet rising electricity demand while advancing sustainability and operational performance nationwide.

Market Outlook 2026-2034:

The India power market is poised for notable growth throughout the forecast period, driven by rising electricity demand and diversifying energy sources. The market size was estimated at 596.0 GW in 2025 and is expected to reach 1,154.2 GW by 2034, reflecting a compound annual growth rate of 7.24% over the forecast period 2026-2034. Massive investments in renewable energy infrastructure, thermal capacity augmentation, nuclear power development, and transmission network expansion are expected to fuel capacity growth while improving grid reliability and energy accessibility across all user segments.

India Power Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Power Source |

Thermal |

54.6% |

|

End User |

Utilities |

62.3% |

|

Region |

West India |

31.4% |

Power Source Insights:

- Thermal

- Nuclear

- Renewables

Thermal dominates with a market share of 54.6% of the total India power market in 2025.

Thermal holds the biggest market share owing to its established infrastructure base and dependable large scale generation capacity. Coal based plants account for the majority of installed capacity, supplying consistent electricity to meet baseload demand across industrial and urban centers. India’s domestic coal availability and extensive network of thermal stations enable steady output throughout the year. Thermal power also offers grid stability, supporting fluctuations from renewable sources, such as solar and wind. Many existing transmission systems are designed around thermal generation hubs, reinforcing their operational importance. This long-standing dominance continues to anchor the country’s overall electricity supply structure.

Thermal power remains dominant because it can deliver continuous generation regardless of weather conditions, making it crucial during peak demand periods. Industrial clusters, railways, and large commercial establishments depend on uninterrupted supply that thermal plants reliably provide. Existing long term coal linkages and power purchase agreements ensure predictable production levels. Government efforts to modernize older plants with improved efficiency technologies further extend their operational life. Reflecting this priority, in 2025 Prime Minister Narendra Modi launched thermal power projects in Kanpur worth over Rs 47,000 crore, including the 660 MW Panki and Ghatampur expansions, adding 3,081 MW to Uttar Pradesh’s capacity.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Utilities

- Commercial and Industrial

- Residential

Utilities lead with a market share of 62.3% of the total India power market in 2025.

Utilities represent the largest segment due to their central role in electricity generation, transmission, and distribution across the country. State owned and private utility companies account for the largest share of power procurement and usage, supplying electricity to residential, commercial, and industrial segments. Rapid urbanization, rising household electrification, and expansion of smart city projects continue to increase the demand handled by utilities. Government schemes supporting around-the-clock power access and grid strengthening are further boosting utility driven utilization. Utilities also manage large scale infrastructure, such as substations and transmission corridors, making them the most significant end user category in the market.

Utilities also dominate because they are the primary buyers of power generation capacity, including thermal, hydro, and renewable sources. With India’s growing focus on renewable integration, utilities are investing heavily in solar parks, wind farms, and hybrid projects to meet clean energy targets. Long term power purchase agreements and regulated tariff structures provide stable demand and predictable revenue streams. Upgrades in distribution networks, smart metering, and reduction of transmission losses are increasing operational efficiency. Additionally, rising peak load requirements from metros, railways, and urban commercial centers are largely serviced through utility networks.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 31.4% share of the total India power market in 2025.

West India leads the market driven by its strong industrial base, high electricity usage, and advanced infrastructure across states, such as Maharashtra and Gujarat. Major manufacturing hubs, petrochemical complexes, and commercial centers in Mumbai, Pune, Surat, and Ahmedabad generate sustained power demand throughout the year. The region has also attracted large scale investments in transmission networks and capacity expansion, ensuring reliable supply to industries and urban households. Rapid urbanization and rising residential utilization further strengthen the market growth. Presence of leading private utilities and proactive state policies continue to support generation, distribution efficiency, and overall power sector development across West India.

West India also benefits from significant renewable energy deployment, particularly solar and wind projects in Gujarat, Rajasthan’s western belt, and coastal Maharashtra. Strong grid connectivity and industrial off take agreements are accelerating clean power adoption and supporting capacity expansion. In 2025, Ingka Investments, the investment arm of Ingka Group (IKEA), launched its first renewable energy project in India, a 210 MWp solar installation in Bikaner, Rajasthan, expected to generate 380 GWh annually. Ports, logistics corridors, data centers, metro rail projects, and commercial real estate growth further reinforce rising regional electricity demand.

Market Dynamics:

Growth Drivers:

Why is the India Power Market Growing?

Rapid Urbanization and Industrialization

India's rapid urbanization and industrialization are impelling the growth in the power market, as the demand for energy rises across residential, commercial, and industrial sectors. With urban areas expanding and industrial activities intensifying, there is an increase in the need for a reliable and uninterrupted electricity supply. The development of infrastructure, such as smart cities and industrial zones, requires enhanced energy capacity to support residential needs, manufacturing, transportation, and services. According to World Bank data, India’s urban population accounted for approximately 36.87% of the total population in 2024. This increasing rate of urbanization is driving investments into generation, transmission, and distribution systems, further propelling the growth of the Indian power market.

Government Policies and Initiatives

The Indian government’s policies and initiatives play a significant role in shaping the power market. Various programs and efforts towards renewable energy capacity expansion are contributing to a rise in energy demand. Policies promoting affordable electricity access, along with the focus on sustainable energy, are contributing to the diversification of the country’s energy mix. In 2026, the Ministry of Power introduced the Draft National Electricity Policy 2026, which outlines ambitious goals for sustainable energy. The policy targets 2,000 kWh per capita electricity usage by 2030 and aims to align with India’s climate commitments, marking a significant shift from the previous policy established in 2005. These efforts highlight the government’s commitment to transforming the power sector while ensuring a greener, more reliable energy future for the nation.

Renewable Energy Adoption

The growing focus on renewable energy adoption is driving the Indian power market's transformation. With an increasing shift towards clean energy sources like solar, wind, and hydroelectric power, the renewable energy segment is becoming an essential component of the energy mix. The government’s ambitious targets to increase renewable energy capacity contribute to the expansion of solar and wind farms, enabling India to reduce its dependence on fossil fuels. For instance, in 2026, India launched Phases 3 and 4 of the Green Energy Corridor to integrate 150 GW of renewable energy into the national grid. This initiative supports India's goal of achieving 500 GW of non-fossil fuel power by 2030. The expansion aims to enhance grid capacity and stability amid growing renewable generation.

Market Restraints:

What Challenges the India Power Market is Facing?

Financial Distress of Distribution Companies Constraining Sector Viability

India's power distribution companies are grappling with significant financial difficulties, with substantial losses and mounting dues to generators. This financial strain hinders their procurement capacity, delays payments, and restricts investment in network upgrades. As a result, these challenges create a bottleneck that disrupts the efficiency and growth of the entire power value chain, affecting overall system reliability and long-term sustainability.

Transmission Infrastructure Gaps Limiting Renewable Energy Integration

India's transmission network expansion is not keeping up with the rapid growth of renewable energy capacity, leading to integration challenges. The shortfall in the commissioning of new transmission lines impedes the efficient transfer of renewable power from resource-rich areas to demand centers. This gap in infrastructure limits the country's ability to fully harness renewable energy potential, affecting the overall efficiency of the power sector.

Grid Flexibility Constraints Amid Rapidly Changing Generation Mix

The growing share of variable renewable energy sources is challenging grid management, as coal-fired power plants have limited flexibility in adjusting output during peak solar generation. The lack of sufficient energy storage and shifting demand patterns further complicate the situation. To address these challenges, significant investments in flexible generation capacity and advanced grid management systems are essential to maintain grid stability and ensure a reliable energy supply.

Competitive Landscape:

The India power market exhibits highly competitive intensity characterized by the coexistence of large central public sector undertakings, state-owned generating companies, and major private conglomerates competing across thermal, renewable, nuclear, and hybrid energy segments. Strategic investments in capacity expansion, technology diversification across ultra-supercritical thermal plants and utility-scale solar and wind projects, and vertical integration across generation, transmission, and distribution functions define competitive positioning. Increasing FDI, rising private sector participation, and evolving regulatory frameworks are intensifying market competition while driving innovation in energy storage, grid modernization, and clean energy solutions.

Recent Developments:

- September 2025: Adani Green commissioned 408.1 MW of renewable energy projects in Khavda, Gujarat, raising its operational capacity to 16,486.1 MW. The company aimed for a 17 GW milestone, with future projects set for continued growth. These projects were operationalized following relevant clearances.

- August 2025: India launched the first 660 MW unit of the Ghatampur Thermal Power Project in Kanpur Nagar, Uttar Pradesh. The project, costing INR 21,780.94 Crore, included three supercritical units, with the remaining two units expected by FY 2025-2026. The power purchase agreements cover supply to Uttar Pradesh and Assam.

India Power Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

GW |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Power Sources Covered |

Thermal, Nuclear, Renewables |

|

End Users Covered |

Utilities, Commercial and Industrial, Residential |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Power Market Report

The India power market reached a volume of 596.0 GW in 2025.

The India power market is expected to grow at a compound annual growth rate of 7.24% from 2026-2034 to reach 1,154.2 GW by 2034.

Thermal dominates the India power market with a share of 54.6% in 2025, driven by extensive coal reserves and a well-established infrastructure of coal, gas, and lignite-fired power stations.

Key factors driving the India power market include the rising adoption of smart grids that enable real time monitoring, efficient distribution, and renewable integration. In 2025, Vodafone Idea announced deployment of 12 million smart meters under the National Smart Grid Mission to reduce losses and improve efficiency nationwide.

Major challenges include persistent financial distress of distribution companies, transmission infrastructure gaps limiting renewable energy integration, grid flexibility constraints amid a rapidly changing generation mix, coal dependency concerns, and supply chain bottlenecks in critical energy equipment manufacturing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade