India Precious Metals Market Size, Share, Trends and Forecast by Metal Type, Application, and Region, 2026-2034

India Precious Metals Market Summary:

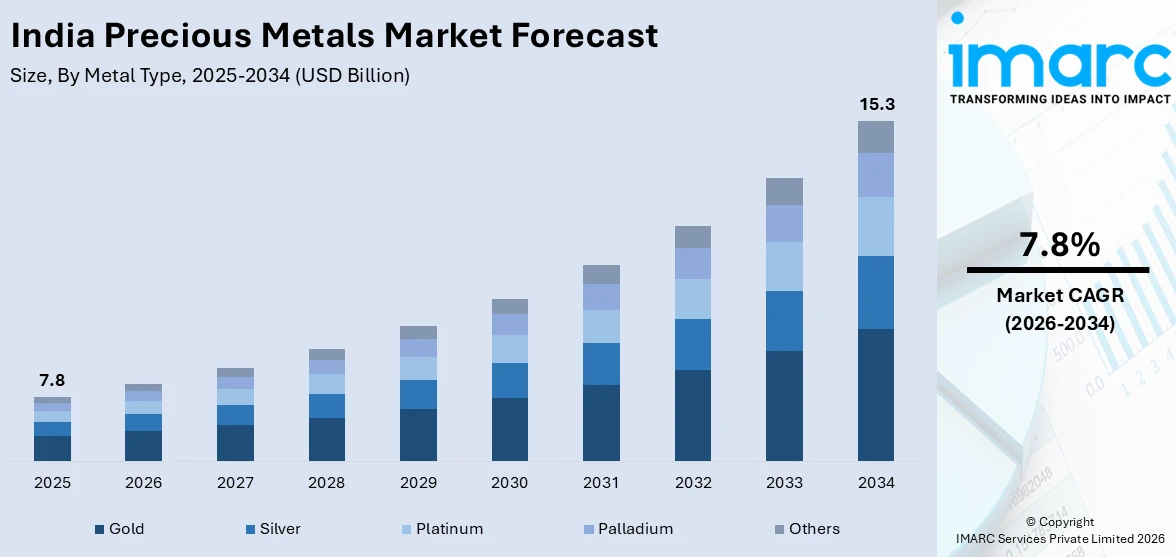

The India precious metals market size was valued at USD 7.8 Billion in 2025 and is projected to reach USD 15.3 Billion by 2034, growing at a compound annual growth rate of 7.8% from 2026-2034.

The India precious metals market is expanding as rising affluence among the growing middle class, deep-rooted cultural traditions surrounding gold and silver, and increasing consumer demand for investment-grade assets drive sustained growth. Favorable government policies, including reduced import duties and streamlined hallmarking standards, are strengthening formal trade channels and boosting consumer confidence. Advancements in refining technologies, expanding organized retail networks, and the growing adoption of digital gold and exchange-traded fund platforms are further broadening market participation and reshaping the market share.

Key Takeaways and Insights:

- By Metal Type: Gold dominates the market with a share of 70% in 2025, owing to its deep cultural significance across Indian weddings and festivals, strong safe-haven investment appeal, and widespread acceptance as a store of wealth among both urban and rural consumers.

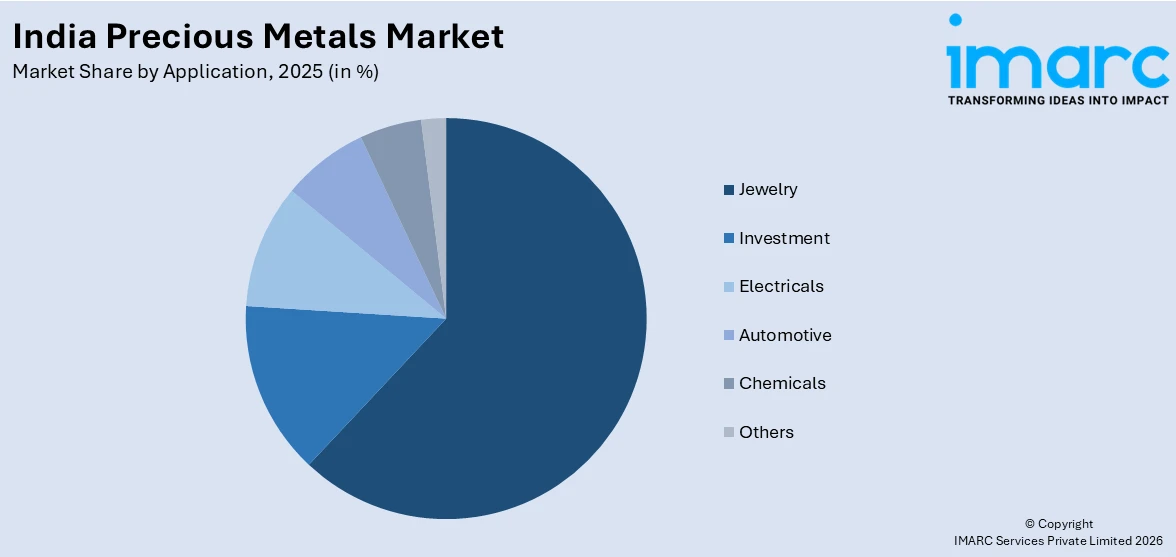

- By Application: Jewelry leads the market with a share of 62% in 2025. This dominance is driven by the enduring tradition of gold and silver adornment during weddings, religious ceremonies, and festive occasions, supported by rising disposable incomes and expanding organized retail presence.

- Key Players: Key players drive the India precious metals market by expanding retail footprints, investing in advanced manufacturing and refining capabilities, launching innovative product lines, and strengthening omnichannel distribution. Their focus on hallmarking compliance, customer trust, and strategic partnerships enhances market penetration and accelerates adoption across diverse consumer segments.

To get more information on this market Request Sample

The India precious metals market is experiencing robust expansion, driven by a convergence of cultural, economic, and policy-related factors. India's deep cultural affinity for gold and silver, particularly during weddings and religious festivals, ensures sustained baseline demand across both rural and urban populations. The expanding middle class with growing disposable incomes is increasingly turning to precious metals as reliable stores of value and portfolio diversifiers. Government initiatives, including the reduction of gold import duties from 15% to 6% in the Union Budget 2024, have significantly lowered acquisition costs and encouraged formal trade channels. The rapid adoption of digital gold platforms and exchange-traded funds is broadening market access to younger demographics. Furthermore, the expanding use of silver in solar photovoltaic manufacturing and electronics is adding an industrial dimension to traditional consumption patterns, strengthening the overall market trajectory.

India Precious Metals Market Trends:

Rising Adoption of Digital Gold and Exchange-Traded Fund Platforms

Indian investors are increasingly embracing digital gold and gold exchange-traded funds as convenient and cost-effective alternatives to physical ownership. These platforms enable fractional purchases and seamless trading, attracting younger demographics and first-time investors. The total assets managed (AUM) by gold ETFs in India exceeded INR 1 Trillion, as of October 2025, with gold ETF portfolios increasing from 7.83 Lakh in October 2020 to more than 95 Lakh in October 2025, underscoring the structural shift toward digitized precious metals investment.

Expanding Industrial Applications of Silver in Renewable Energy

Silver consumption is being increasingly propelled by its critical role in solar photovoltaic cell manufacturing, electronics, and electric vehicle (EV) components. As India accelerates its renewable energy transition, with installed solar capacity crossing 100 gigawatts in January 2025, the demand for silver paste and conductive materials is rising sharply. Additionally, government-led initiatives promoting domestic solar manufacturing and grid-scale renewable projects are further strengthening silver demand. Moreover, the increasing deployment of high-efficiency solar modules, which require greater silver content per cell, is intensifying material demand. This trend underscores silver’s growing strategic importance in supporting India’s clean energy and electrification goals.

Shift Towards Organized and Branded Jewelry Retail

The India precious metals market is witnessing an accelerating transition from unorganized to organized retail, with branded jewelers gaining market share through enhanced transparency, hallmarking compliance, and omnichannel strategies. Consumers increasingly favor trusted brands offering certified products with buyback guarantees. This shift is further supported by rising financial literacy and awareness around purity standards, making buyers more quality-conscious. Digital platforms, virtual try-ons, and online price transparency are also strengthening organized players’ reach beyond metro cities.

Market Outlook 2026-2034:

The India precious metals market is poised for sustained expansion over the forecast period, driven by deepening cultural demand, favorable policy frameworks, and expanding industrial applications. Rising affluence among the growing middle class, coupled with increasing adoption of gold and silver as investment vehicles, is expected to strengthen demand across both physical and financial channels. The government's supportive stance on import duties and hallmarking standards will continue to foster organized trade and consumer confidence. The market generated a revenue of USD 7.8 Billion in 2025 and is projected to reach a revenue of USD 15.3 Billion by 2034, growing at a compound annual growth rate of 7.8% from 2026-2034. Expanding use of silver in solar manufacturing, growing penetration of digital gold platforms, and the continued dominance of jewelry consumption will serve as key catalysts for long-term growth.

India Precious Metals Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Metal Type | Gold | 70% |

| Application | Jewelry | 62% |

Metal Type Insights:

- Gold

- Silver

- Platinum

- Palladium

- Others

Gold dominates with a market share of 70% of the total India precious metals market in 2025.

Gold maintains its commanding position in the India precious metals market, motivated by its unparalleled cultural importance in Indian customs, marriages, and religious rituals. For people of various income levels, the metal is a preferred means of preserving wealth as well as an ornamental asset. Strong consumer sentiment has kept demand momentum going, bolstered by positive revisions to customs duties and increasing rural affluence after successful monsoon seasons. Institutional confidence in gold as a strategic reserve asset was demonstrated by the Reserve Bank of India's acquisition of 73 Tons of gold in the first eleven months of 2024.

Gold's twin function as a socially meaningful asset and an investment instrument further contributes to its ongoing popularity in India. In addition to traditional physical purchases, customers are diversifying into gold exchange-traded funds, sovereign gold bonds, and digital gold platforms due to rising urbanization and increased financial knowledge. In order to take market share away from the unorganized sector, organized jewelers are growing their retail networks throughout smaller cities by utilizing hallmarking compliance and transparent pricing. The ongoing growth of gold lending services and recycling ecosystems is expanding market penetration and improving accessibility for larger consumer segments nationwide.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Jewelry

- Investment

- Electricals

- Automotive

- Chemicals

- Others

Jewelry leads with a share of 62% of the total India precious metals market in 2025.

Jewelry remains the predominant application for precious metals in India, driven by the nation's long-standing cultural customs of wearing gold and silver during religious events, festivals, and weddings. Bridal sets, necklaces, bangles, and earrings are in high demand throughout the months-long Indian wedding season. Consumers are gravitating towards organized retail channels due to rising disposable incomes and the aspirational attractiveness of branded jewelry. With an expenditure of almost INR 1,000 crore, Malabar Gold & Diamonds opened an integrated manufacturing facility in Hyderabad in July 2025 that can produce 4.7 Tons of gold jewelry annually.

The jewelry industry is profiting from changing consumer preferences, as younger generations look for new designs that combine classic workmanship with cutting-edge aesthetics. Customers in Generation Z and Millennials are increasingly drawn to personalized pieces, everyday wear collections, and lightweight jewelry selections. By reaching customers in tier-two and tier-three cities, jewelers are expanding their market reach and boosting volume growth, owing to the quick development of e-commerce and omnichannel retail methods. Mandatory hallmarking laws have also increased consumer trust in the purity of products, making organized branded jewelry more widely used and creating a more open marketplace nationwide.

Regional Insights:

- South India

- North India

- West and Central India

- East India

South India represents a significant consumption hub for precious metals, driven by the region's strong cultural affinity for gold jewelry, particularly in states like Kerala, Tamil Nadu, and Karnataka. Strong buying activity is maintained all year long, due to the existence of significant organized jewelers, strong demand associated to weddings, and a long-standing custom of giving gold as gifts during holidays like Onam and Pongal.

North India contributes substantially to the India precious metals market, supported by a dense population, a large concentration of wedding ceremonies, and robust spending power in Delhi-NCR and other urban areas. Both organized retail and traditional jewelry stores will continue to see demand due to the region's cultural emphasis on ornate bridal jewelry sets and festive gold purchases around Diwali and Dhanteras.

West and Central India serves as a vital market for precious metals, anchored by Mumbai's prominence as a major bullion trading center and Gujarat's leading role in diamond cutting and jewelry manufacturing. Rising urbanization across Maharashtra and Madhya Pradesh, coupled with increasing disposable incomes, is driving robust demand for both investment-grade bullion and jewelry products throughout the region.

East India is an emerging market for precious metals, with growing demand driven by increasing affluence and expanding organized retail presence in states, such as West Bengal, Odisha, and Jharkhand. The region's rich tradition of intricate gold jewelry designs and rising consumer preference for hallmarked products are supporting market growth and encouraging brand-driven purchases across urban and semi-urban areas.

Market Dynamics:

Growth Drivers:

Why is the India Precious Metals Market Growing?

Favorable Government Policies and Import Duty Reforms

The Indian government's progressive policy reforms are serving as a powerful catalyst for the precious metals market. Strategic interventions aimed at reducing trade barriers, formalizing bullion channels, and enhancing product transparency have collectively strengthened consumer confidence and market participation. Complementary measures, including the reduction of long-term capital gains holding periods on gold from 36 to 24 months, as per the Finance (No.2) Bill, 2024, and favorable taxation treatment for gold ETFs, have enhanced the investment appeal of precious metals across financial instruments. Mandatory hallmarking regulations continue to bolster product purity assurance, encouraging consumers to purchase through organized channels. These policy measures are collectively creating a more accessible, transparent, and competitive precious metals ecosystem that supports sustained demand growth across investment, jewelry, and industrial segments.

Rising Middle-Class Affluence and Cultural Demand Traditions

India's rapidly expanding middle class, supported by robust economic growth and rising household incomes, is fueling sustained demand for precious metals across both consumption and investment categories. Gold and silver hold deep cultural significance in Indian society, serving as essential elements of weddings, religious ceremonies, and festival celebrations. The Indian wedding season alone generates substantial precious metals demand, as bridal jewelry sets remain an indispensable component of marriage traditions across all regions and communities. According to the World Gold Council, India's overall gold demand reached 802.8 Tons in 2024, reflecting a 5% increase over 2023, driven by strong investment appetite and festive buying. Growing financial literacy and awareness about wealth preservation strategies are encouraging consumers to diversify their savings into gold bars, coins, and financial instruments. Rural demand, bolstered by favorable agricultural seasons and government income support programs, continues to provide a strong consumption base for the precious metals market.

Expanding Industrial Applications and Technological Integration

The growing industrial utilization of precious metals, particularly silver and platinum group metals, is adding a significant structural demand dimension beyond traditional consumption patterns. Silver's superior electrical and thermal conductivity makes it indispensable in solar photovoltaic cell manufacturing, electronics, EV components, and emerging data center infrastructure. As India accelerates its renewable energy ambitions, the demand for silver in solar panel production has intensified substantially. Platinum and palladium continue to find critical applications in automotive catalytic converters and chemical processing industries. The integration of precious metals into advanced electronics, medical devices, and hydrogen fuel cell technologies is diversifying demand sources and strengthening the market's long-term growth trajectory. This expanding industrial footprint is reducing demand cyclicality and making precious metals consumption in India more closely aligned with long-term trends in clean energy, advanced manufacturing, and high-tech industrial expansion.

Market Restraints:

What Challenges the India Precious Metals Market is Facing?

Price Volatility and Affordability Pressures

Significant fluctuations in international precious metals prices create uncertainty for both consumers and industry participants in India. Sharp price rallies, driven by geopolitical tensions and safe-haven demand, reduce affordability and suppress jewelry purchases, particularly among price-sensitive consumers in semi-urban and rural markets. At the same time, sudden price corrections disrupt inventory planning and margin stability for retailers and manufacturers, increasing overall market volatility.

Smuggling and Informal Trade Channels

Despite significant import duty reductions, smuggling and informal gold trade continue to pose challenges for the India precious metals market. Illicit channels undermine formal trade, reduce government revenue, and distort market pricing dynamics. Although the narrowing duty differential has reduced smuggling incentives, sophisticated networks and persistent demand for unaccounted gold sustain informal flows, particularly during high-demand festive periods. This ongoing challenge requires continued regulatory vigilance and enforcement measures to protect formal market integrity.

Supply Chain Dependencies and Import Reliance

India's near-total dependence on imports for its precious metals requirements exposes the market to external supply disruptions, currency fluctuations, and geopolitical risks. Domestic gold mining output remains negligible compared to consumption volumes, leaving the country vulnerable to changes in global supply dynamics and trade policies. Rising import bills, driven by elevated global prices, place pressure on the current account balance. Additionally, silver supply constraints from aging global mines and declining ore grades could impact industrial availability and pricing stability over the forecast period.

Competitive Landscape:

The India precious metals market features an increasingly competitive landscape as organized players continue to expand their presence and market influence. Established jewelers and bullion dealers are investing in manufacturing capabilities, retail network expansion, and digital platforms to capture growing consumer demand. Competition is driven by brand trust, hallmarking compliance, product innovation, and omnichannel distribution strategies. Players are differentiating through contemporary jewelry designs, transparent pricing policies, and loyalty programs to attract diverse consumer segments. Strategic partnerships, manufacturing investments, and regional expansion initiatives are enabling market participants to strengthen their competitive positioning and capitalize on the structural shift towards organized retail channels across the country.

India Precious Metals Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Metal Types Covered | Gold, Silver, Platinum, Palladium, Others |

| Applications Covered | Jewelry, Investment, Electricals, Automotive, Chemicals, Others |

| Regions Covered | South India, North India, West and Central India, South India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Precious Metals Market Report

The India precious metals market size was valued at USD 7.8 Billion in 2025.

The India precious metals market is expected to grow at a compound annual growth rate of 7.8% from 2026-2034 to reach USD 15.3 Billion by 2034.

Gold holding the largest revenue share of 70%, remains pivotal for India's precious metals consumption, driven by its deep cultural significance in weddings and festivals, strong investment appeal, and widespread acceptance as a trusted store of wealth among Indian consumers.

Key factors driving the India precious metals market include favorable government import duty reforms, rising middle-class affluence and cultural demand traditions, expanding industrial applications in solar and electronics, growing adoption of digital investment platforms, and strengthening organized retail presence.

Major challenges include significant price volatility affecting consumer affordability, persistent smuggling through informal trade channels, heavy import dependence creating supply vulnerabilities, currency fluctuation risks, and global supply chain constraints impacting silver availability for industrial applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)