India PropTech Market Size, Share, Trends, and Forecast by Solution, Application, Deployment, End User, and Region, 2026-2034

India PropTech Market Size, Share, Trends & Forecast (2026-2034)

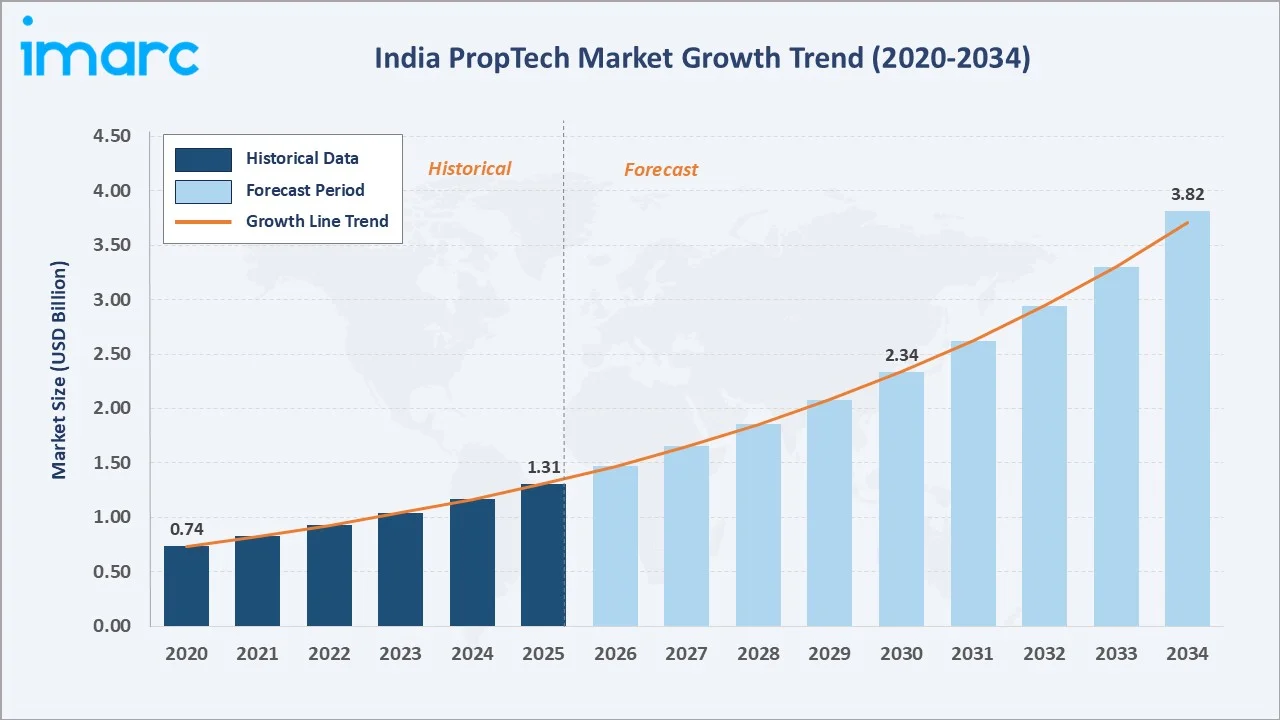

The India proptech market size increased from USD 1.31 Billion in 2025 to USD 1.47 Billion in 2026 and is projected to reach USD 3.82 Billion by 2034, growing at a CAGR of 12.26% during 2026-2034. India's real estate sector is undergoing a structural digital transformation, driven by AI-enabled property platforms, blockchain-linked transactions, smart property management, and increasing VC funding.

Market Snapshot

|

Metric |

Value |

|

Base Year Market Size (2025) |

USD 1.31 Billion |

| Market Size (2026) | USD 1.47 Billion |

|

Forecast Market Size (2034) |

USD 3.82 Billion |

|

CAGR (2026-2034) |

12.26% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

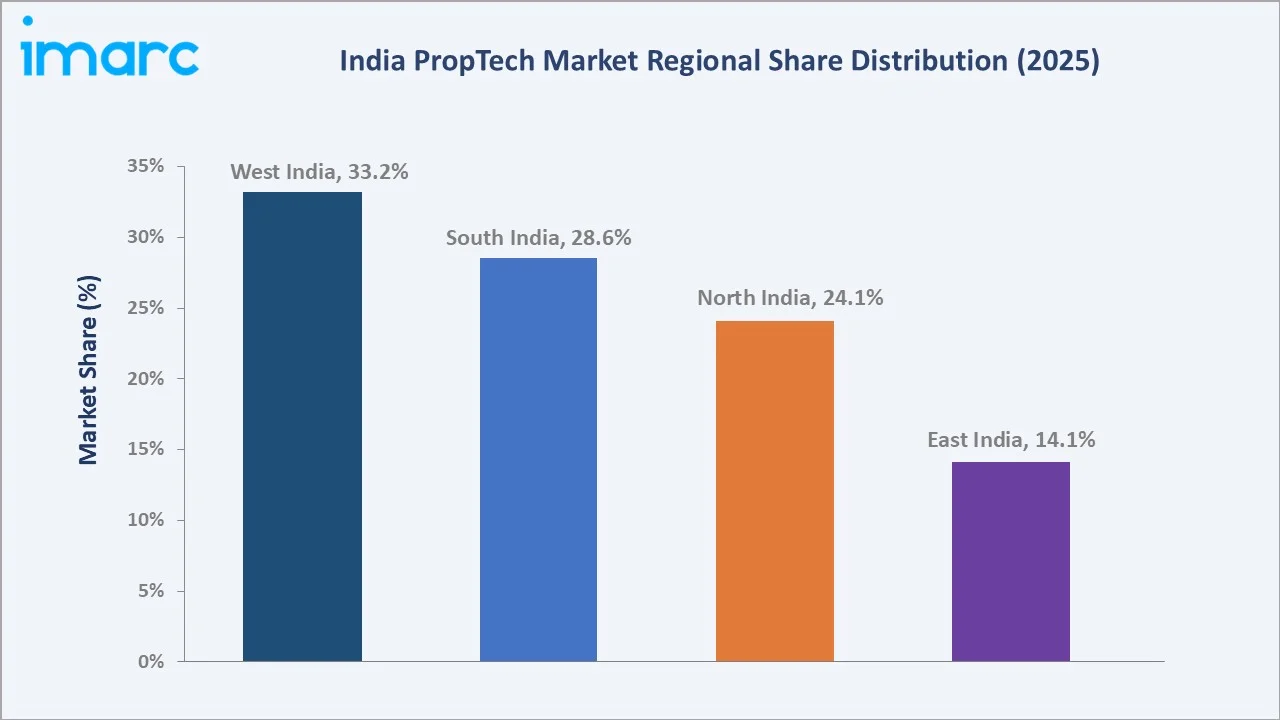

Largest Region |

West India (33.2% share, 2025) |

|

Fastest Growing Segment |

Cloud Deployment |

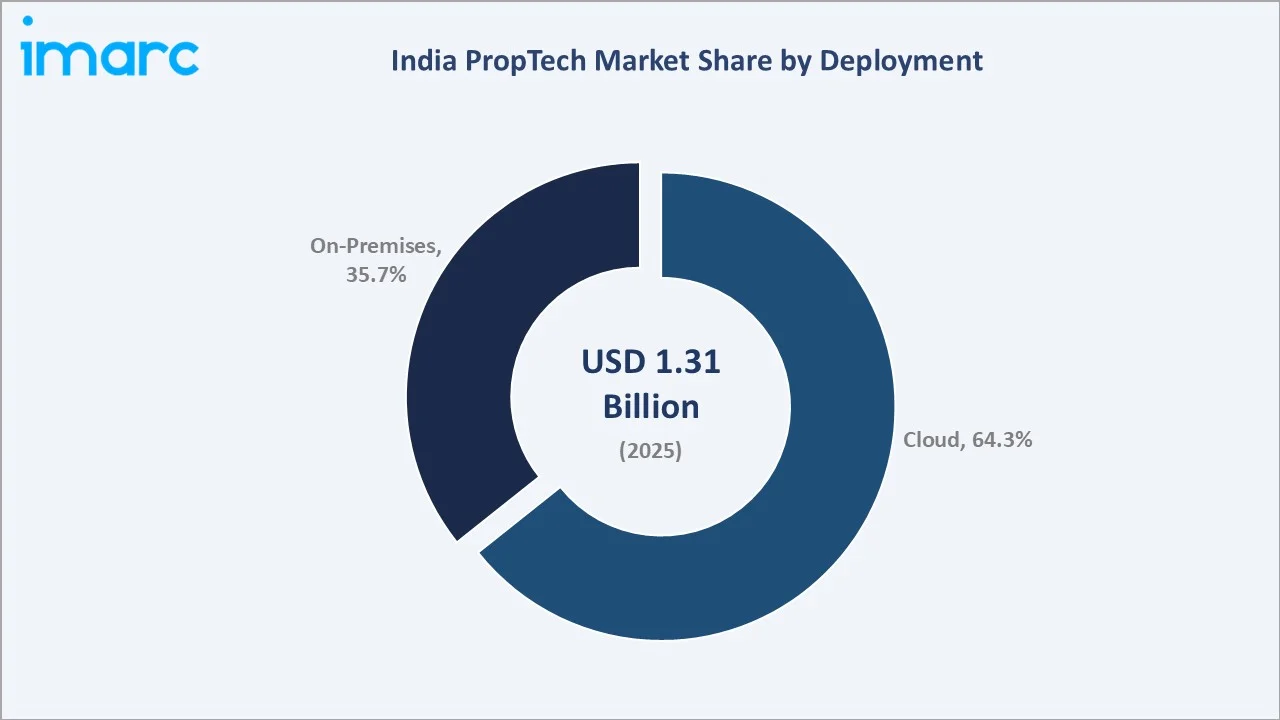

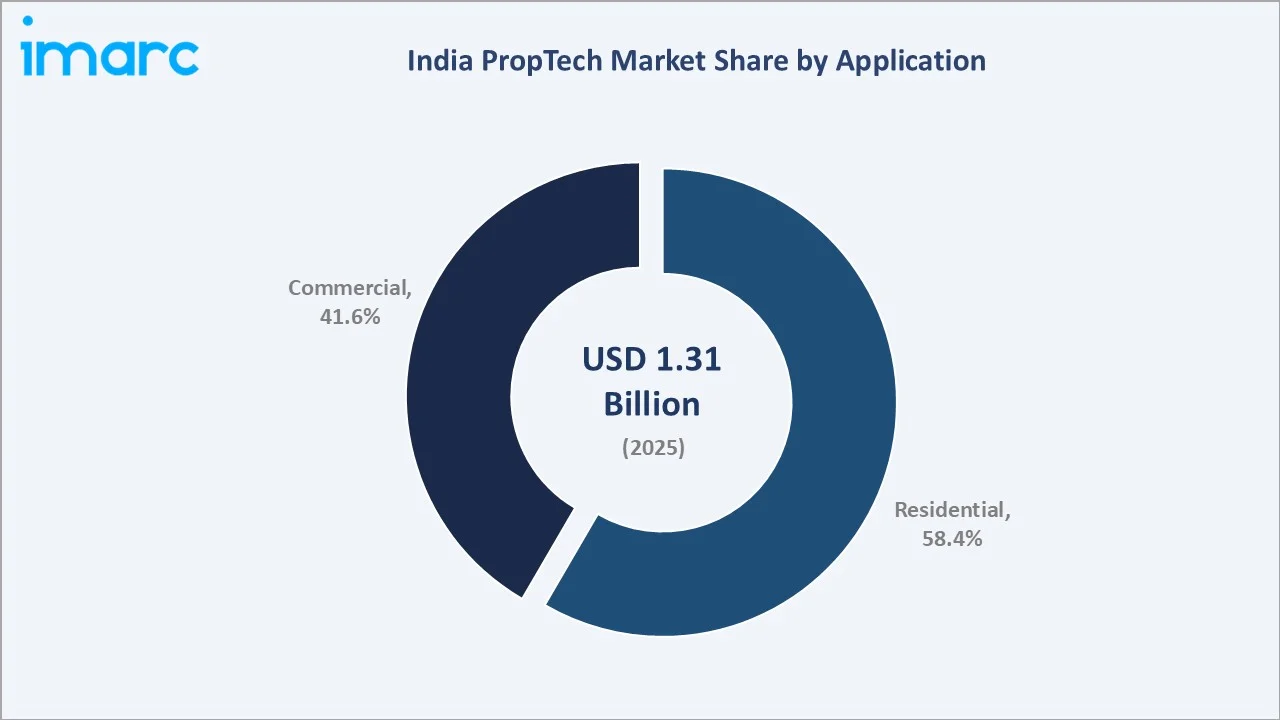

West India dominates, holding a 33.2% market share in 2025, driven by Mumbai's commercial real estate hub and Pune's technology corridor. Cloud deployment accounts for 64.3% of the market, while the residential segment leads applications with a 58.4% share. Rising urbanization, government Smart Cities initiatives, and growing smartphone penetration are accelerating proptech adoption across residential and commercial segments.

To get more information on this market, Request Sample

India's proptech market is positioned for robust expansion through 2034, underpinned by sustained real estate transaction volumes, state-led digital transformation, and the rapid integration of AI and cloud-based technology models. Key platforms are moving beyond property listings toward enterprise-grade AI SaaS, IoT-enabled smart buildings, and blockchain-based transaction systems that collectively drive deeper market penetration.

Executive Summary

The India proptech market is expanding at an accelerating pace, underpinned by the convergence of digital real estate solutions, government Smart Cities investments, and robust VC-backed startup activity. The market grew from USD 1.31 Billion in 2025 to USD 1.47 Billion in 2026 and is forecast to reach USD 3.82 Billion by 2034, growing at a CAGR of 12.26%. This growth trajectory reflects broad-based digital adoption across India's USD 300+ Billion real estate sector, spanning property search, transaction management, facility operations, and investment platforms.

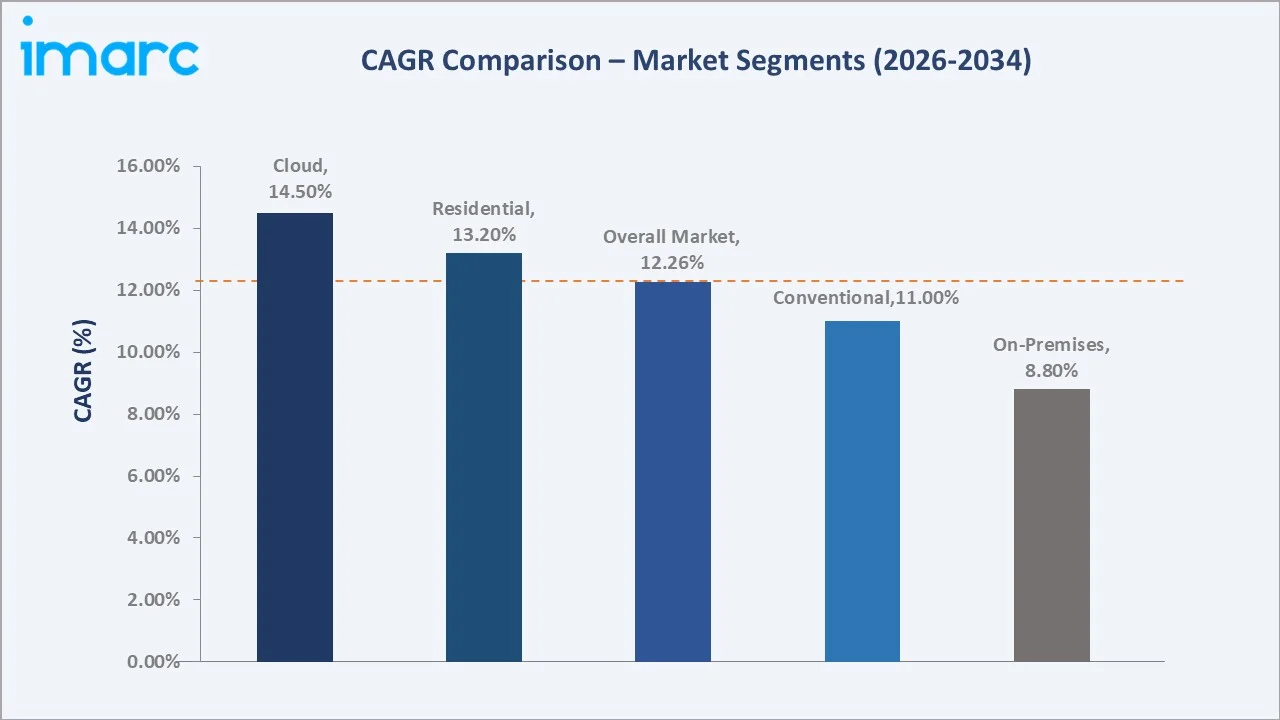

Cloud deployment dominates with a 64.3% share in 2025, driven by scalable SaaS platforms offered by leading proptech players, including NoBroker, MagicBricks, and Housing.com. The residential segment commands 58.4% of application revenue, fueled by a housing demand wave across Tier-1 and Tier-2 cities. West India leads regionally at 33.2%, anchored by Mumbai's commercial density and Pune's expanding tech-real estate ecosystem.

Key growth drivers include rising urbanization, 806 million internet users at the start of 2025, and the government's Digital India Land Records Modernization Programme (DILRMP), which has integrated over 87% of Sub-Registrar Offices with digital land record systems. Market leaders, including NoBroker Technologies Solutions Pvt. Ltd., Info Edge India Ltd, Times Internet, REA Group Ltd., and Square Yards Group, are scaling AI-driven tools to enhance property discovery, transaction efficiency, and broker productivity across 200+ cities.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Deployment) |

Cloud – 64.3% share (2025) |

|

Fastest Growing Segment (Deployment) |

Cloud – ~14.5% CAGR (2026-2034) |

|

Largest Application |

Residential – 58.4% share (2025) |

|

Leading Region |

West India – 33.2% share (2025) |

|

Top Companies |

NoBroker Technologies Solutions Pvt. Ltd., Info Edge India Ltd, Times Internet, REA Group Ltd., and Square Yards Group |

Key Analytical Observations Supporting the Above Data:

- Cloud deployment accounts for 64.3% of India's proptech market in 2025. Cloud's dominance reflects scalable SaaS adoption by brokers, property managers, and real estate developers seeking cost-efficient platforms without on-premises infrastructure investment.

- The residential segment represents 58.4% of application revenue in 2025, driven by post-pandemic housing demand, rising aspirational home ownership among millennials, and digital-first property search behavior across urban India.

- West India's 33.2% share reflects Mumbai's status as India's largest commercial real estate market, alongside Pune, Ahmedabad, and Surat, contributing to rapid residential proptech adoption and strong investor activity in the region.

- On-premises deployment retains a 35.7% share, primarily among large enterprise real estate developers and institutional asset managers requiring data security, compliance control, and integrated legacy system connectivity.

- According to Entrackr, Indian proptech startups raised over USD 550 million across 32 deals in 2025, reflecting sustained investor confidence in platforms deploying AI, computer vision, and blockchain to disrupt traditional property transaction workflows.

India PropTech Market Overview

Proptech (Property Technology) encompasses technology-driven solutions that transform how real estate is researched, transacted, managed, and invested. India's proptech ecosystem spans property listing portals, AI-powered search and valuation tools, digital transaction management, smart building platforms, facility management software, and fractional investment platforms. The market supports buyers, renters, sellers, developers, brokers, institutional investors, and property managers.

Macroeconomic catalysts include India's urban population projected to reach 600 million by 2031, real estate contributing approximately 5-6% to GDP, and 3.21 crore have been sanctioned and 2.67 crore completed under the Pradhan Mantri Awas Yojana-Gramin (PMAY-G). Real estate's digital transformation is also supported by RERA (Real Estate Regulatory Authority) compliance requirements that mandate transparency in project data, payment timelines, and grievance redressal, creating structural demand for proptech compliance tools.

Market Dynamics

To evaluate market opportunities, Request Sample

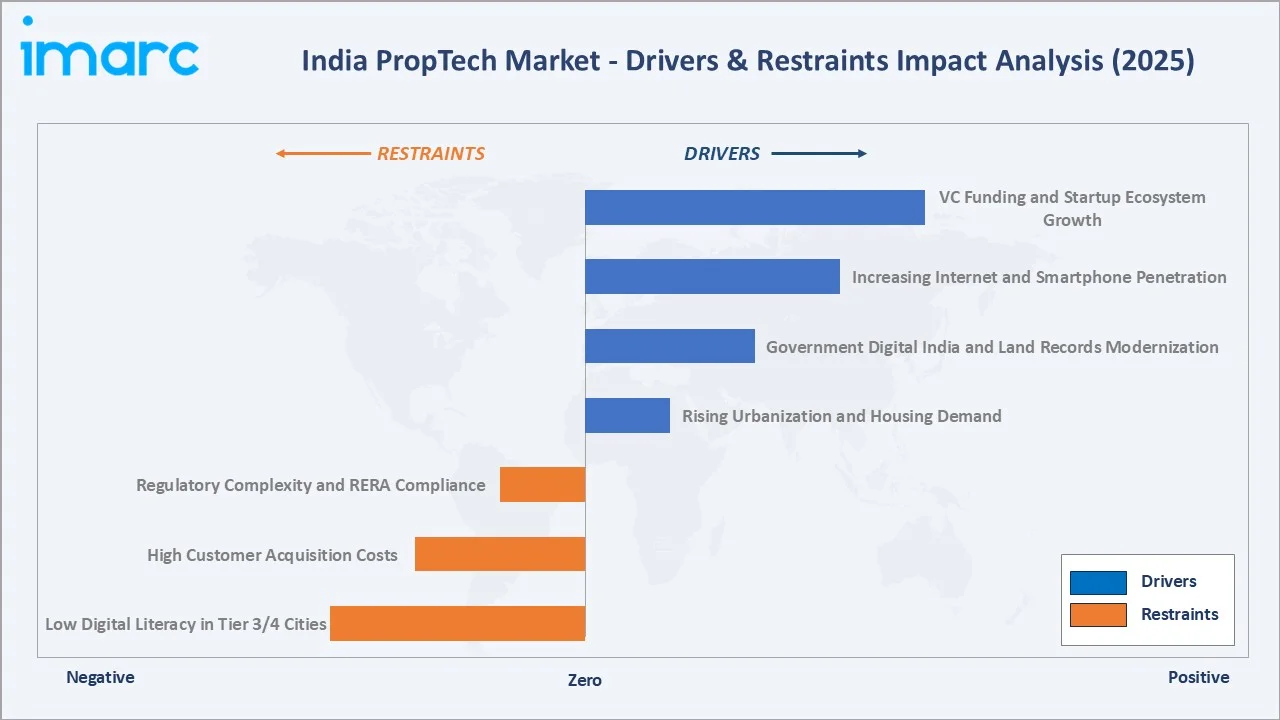

Market Drivers

- Rising Urbanization and Housing Demand: The Economic Survey noted that, according to World Bank estimates, India’s urban population is expected to reach 600 million by 2036, requiring efficient property search, transaction, and management solutions. About 94% of the 8,067 projects under the Smart Cities Mission have been completed, with investments totaling ₹1.64 lakh crore, directly stimulating proptech adoption in 100+ designated cities.

- Government Digital India and Land Records Modernization: The Digital India Land Records Modernization Programme (DILRMP) has integrated over 87% of Sub-Registrar Offices with digital systems by October 2024. As residents in 19 states can now download digitally signed, legally valid land records from home, this has created the data infrastructure underpinning proptech valuation, title verification, and transaction tools.

- Increasing Internet and Smartphone Penetration: India reached 806 million internet users in 2025, with 75%+ accessing real estate platforms via smartphones. Mobile-first proptech platforms such as NoBroker and Housing.com have leveraged this access to scale user bases to 40+ million registered users each, democratizing property search beyond metro geographies.

- VC Funding and Startup Ecosystem Growth: In 2025, the proptech sector raised over USD 550 million in total funding, driven by key players such as Square Yards. In 2025, Aurum PropTech's acquisition of PropTiger for INR 86.45 crore exemplifies ongoing consolidation that creates integrated proptech platforms with broader capabilities.

Market Restraints

- Low Digital Literacy in Tier 3/4 Cities: In 2025, India’s rural population accounts for 63.13% of the total 1.463 billion population, which lacks the digital literacy required to independently navigate proptech platforms, limiting market penetration to Tier-1 and select Tier-2 cities.

- High Customer Acquisition Costs: Property transactions are infrequent lifecycle events, creating persistently high customer acquisition costs (CAC) for proptech platforms. NoBroker and 99acres spend USD 30–60 per acquired user, requiring subscription and ancillary service revenue to achieve positive unit economics, particularly in competitive metro markets.

- Regulatory Complexity and RERA Compliance: Diverging RERA implementations across 34+ state and union territory Real Estate Regulatory Authorities create compliance complexity for platforms operating nationally. Integration requirements for project registration data, payment disclosures, and grievance systems add technical overhead and increase operational costs by 12–18% for cross-state proptech operators.

Market Opportunities

- AI-Powered Property Valuation and Analytics: Platforms integrating satellite imagery, transaction registries, and demographic data for automated valuation models (AVMs) are attracting institutional real estate funds and mortgage lenders seeking faster, more accurate underwriting support.

- Fractional Ownership and Real Estate Tokenization: A recent report by property consulting firm JLL projects that India’s fractional ownership market will grow more than 10-fold, surpassing $5 billion by 2030. SEBI's Small and Medium REITs (SM-REITs) regulatory framework (2024) has created a compliant structure for fractional commercial real estate investment, expanding proptech’s reach to retail investors.

- Smart Building and IoT Integration: As of 2024, green-certified office space in India totaled approximately 503 million sq ft, accounting for 66% of the total Grade A inventory across the top six cities. It represents a substantial addressable market for IoT-enabled building management, energy optimization, and predictive maintenance platforms.

Market Challenges

- Platform Monetization and Profitability: Despite strong user growth, most Indian proptech platforms operate at significant losses. NoBroker reported INR 803 Crore operating revenue in FY2023 but continued to burn capital on expansion. The transition from brokerage disruption to sustainable subscription and SaaS revenue models remains the sector's primary structural challenge.

- Data Privacy and Cybersecurity Risks: Proptech platforms aggregate sensitive financial, identity, and location data from millions of users, creating cybersecurity exposure. The Digital Personal Data Protection Act (DPDPA) 2023 imposes penalties of up to INR 250 Crore for data breaches, compelling platforms to invest significantly in data security infrastructure.

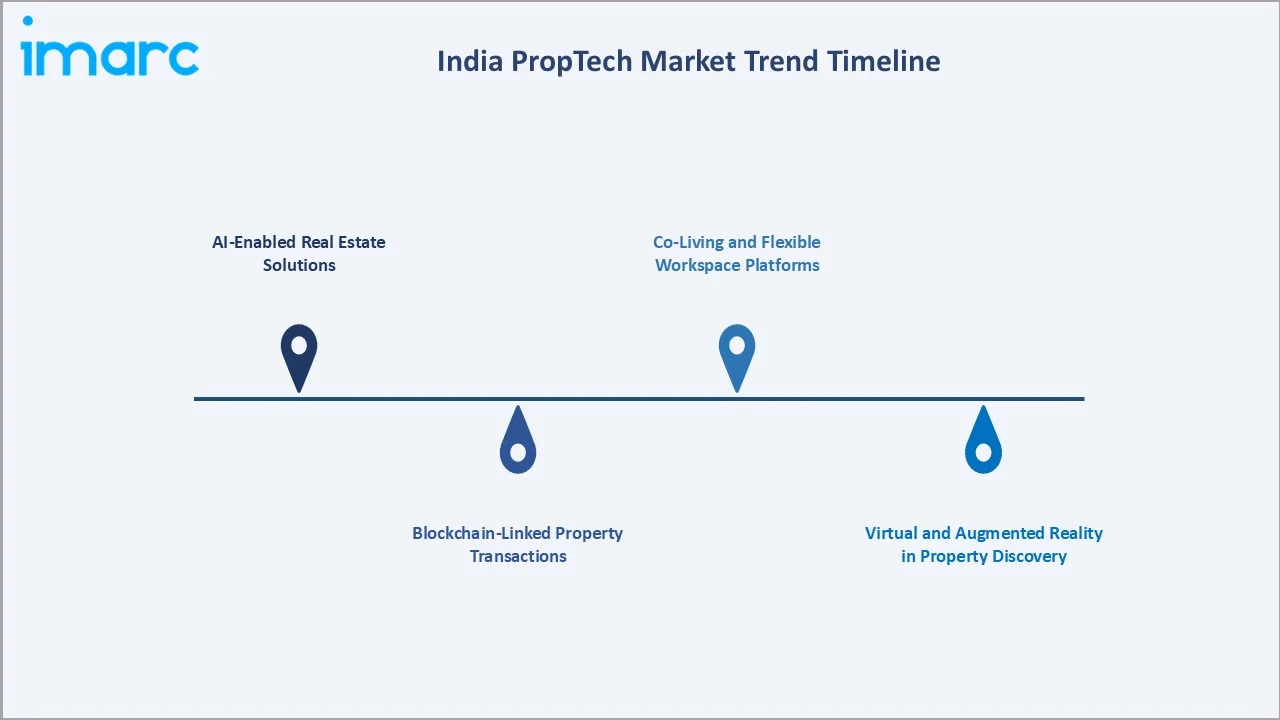

Emerging Market Trends

1. AI-Enabled Real Estate Solutions

AI integration has moved from experimentation to operational deployment across India's proptech ecosystem. In 2025, MagicBricks scaled its READPRO AI-powered CRM to over 85,000 active broker licences across 200+ cities. NoBroker launched ConvoZen.AI, a cloud-based conversational intelligence platform automating voice and non-voice customer interactions. These deployments signal a shift from listing portals toward AI SaaS platforms commanding enterprise-level pricing.

2. Blockchain-Linked Property Transactions

Blockchain-based property registration and escrow solutions are gaining traction, particularly in Maharashtra and Telangana, which have piloted digital land record integration with DLT frameworks. In July 2023, PropVR, the 3D visualization division of Square Yards, was recognized as an authorized partner for Unreal Engine to develop Digital Twin and Interactive 3D solutions for the real estate industry.

3. Virtual and Augmented Reality in Property Discovery

In January 2025, Housing.com enhanced real estate visualization with next‑gen 3D, AR, and VR technologies, making property browsing more immersive and interactive for buyers. The platform’s innovations aim to help users better understand space, layout, and design, improving decision‑making and engagement in property search experiences.

4. Co-Living and Flexible Workspace Platforms

Bengaluru-based Colive currently operates 15,000 beds. Co-working proptech enablers, including platforms managing flexible workspace transactions, have grown alongside India's startup ecosystem.

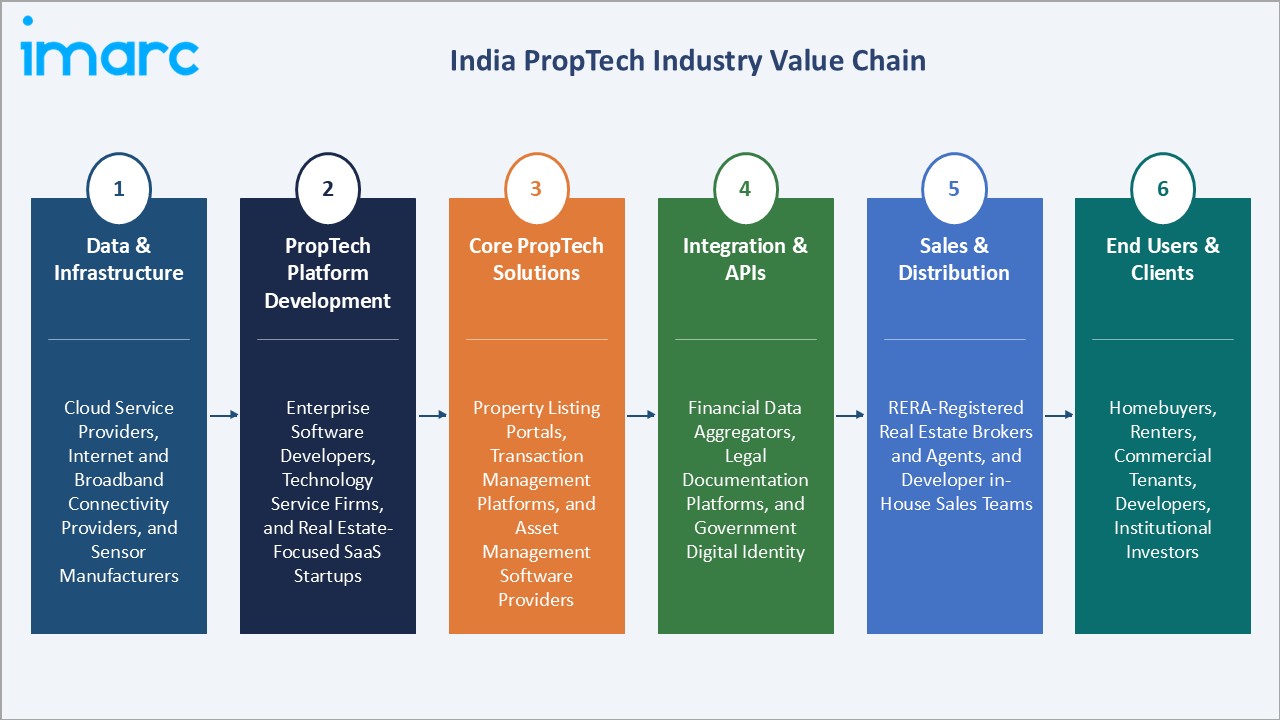

Industry Value Chain Analysis

India's proptech value chain spans digital infrastructure provision through end-user deployment, with specialized operators at each stage enabling increasingly seamless property transactions and management.

|

Stage |

Key Players / Examples |

|

Data & Infrastructure |

Cloud service providers, internet and broadband connectivity providers, and sensor manufacturers |

|

PropTech Platform Development |

Enterprise software developers, technology service firms, and real estate-focused SaaS startups |

|

Core PropTech Solutions |

Property listing portals, transaction management platforms, and asset management software providers |

|

Integration & APIs |

Financial data aggregators, legal documentation platforms, and government digital identity |

|

Sales & Distribution |

RERA-registered real estate brokers and agents, and developer in-house sales teams |

|

End Users & Clients |

Homebuyers, renters, commercial tenants, developers, institutional investors |

Technology Landscape in the India PropTech Industry

Artificial Intelligence and Machine Learning

AI is the defining technology of India's proptech evolution, powering recommendation engines, automated valuation models (AVMs), lead scoring, and conversational bots. NoBroker launched CallZen AI, an AI‑powered contact center intelligence platform designed to help businesses automate conversations, improve lead engagement, and enhance customer support efficiency.

Cloud SaaS and Mobile-First Platforms

Over 64.3% of the market is cloud-deployed in 2025, enabling platforms to scale rapidly across Tier-2 and Tier-3 cities without physical infrastructure. Mobile applications account for 70%+ of proptech user sessions in India, with platforms such as NoBroker, Housing.com, and 99acres maintaining 4.0+ star ratings on Android and iOS app stores with 10 million+ installs each.

Blockchain and Smart Contracts

Blockchain adoption in Indian proptech is accelerating, particularly in land title verification, rental escrow, and fractional ownership tokenization. The Government of India's DILRMP programme, exploring DLT-based land records in select states by 2026, is expected to create a regulatory-compliant framework for blockchain proptech. Proptech startups offering tokenized commercial real estate investment are targeting SEBI's SM-REIT framework to operate compliantly.

IoT and Smart Building Technology

IoT-enabled building management systems (BMS) are being deployed across India's Grade-A commercial and premium residential segments. Smart building investments by DLF, Embassy REIT, and Mindspace REIT are creating demand for integrated proptech platforms managing energy consumption, visitor management, and predictive maintenance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Residential |

58.4% |

2025 |

|

Deployment |

Cloud |

64.3% |

2025 |

|

Solution |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

West India |

33.2% |

2025 |

By Deployment

Cloud deployment dominates with a 64.3% share in 2025. Cloud's dominance reflects the SaaS model adoption by property platforms, enabling rapid feature deployment, mobile accessibility, and scalable user management without on-premises infrastructure costs. Cloud proptech solutions offer 40–60% lower total cost of ownership versus on-premises deployments for mid-market real estate firms.

To access detailed market analysis, Request Sample

On-premises deployment retains a 35.7% share, primarily used by large enterprise real estate developers, institutional asset managers, and government-affiliated housing agencies requiring stringent data sovereignty, compliance with state government IT security policies, and deep integration with legacy ERP and property management systems.

By Application

The residential segment commands a 58.4% application share in 2025. Demand is driven by India's urbanization wave, with 10+ million new urban households forming annually, a rising middle-class aspiring to home ownership, and digital-native millennials who prefer online-first property search and transaction workflows.

Commercial proptech represents 41.6% of the market, encompassing office leasing platforms, retail property management tools, warehouse and logistics RE tech, and flexible workspace management solutions. Commercial proptech is growing at approximately 11.0% CAGR, driven by increasing demand for smart building management and enterprise-grade property analytics platforms adopted by REITs and institutional landlords.

Regional Market Insights

West India's market leadership (33.2%, 2025) reflects the concentration of India's most valuable commercial real estate in Mumbai's BKC, Lower Parel, and Worli districts, complemented by Pune's expanding IT park ecosystem, driving both residential and commercial proptech adoption. Gujarat's GIFT City is also emerging as a proptech-friendly zone with digital-first regulatory infrastructure.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

33.2% |

Dominant commercial real estate activity, expanding technology and IT corridors, and the presence of special economic zones |

|

South India |

28.6% |

Rapidly growing technology-real estate nexus, dual-city urban expansion, and rising manufacturing and industrial real estate demand |

|

North India |

24.1% |

High-density commercial and luxury residential markets, concentration of proptech startups, and venture capital activity |

|

East India |

14.1% |

Recovering residential demand, smart city infrastructure development, and emerging technology parks |

South India at 28.6% represents India's most innovation-driven proptech geography. Bengaluru is home to 40+ proptech startups leveraging the city's deep technology talent pool, while Hyderabad's accelerating data center and tech park development is generating new commercial proptech demand.

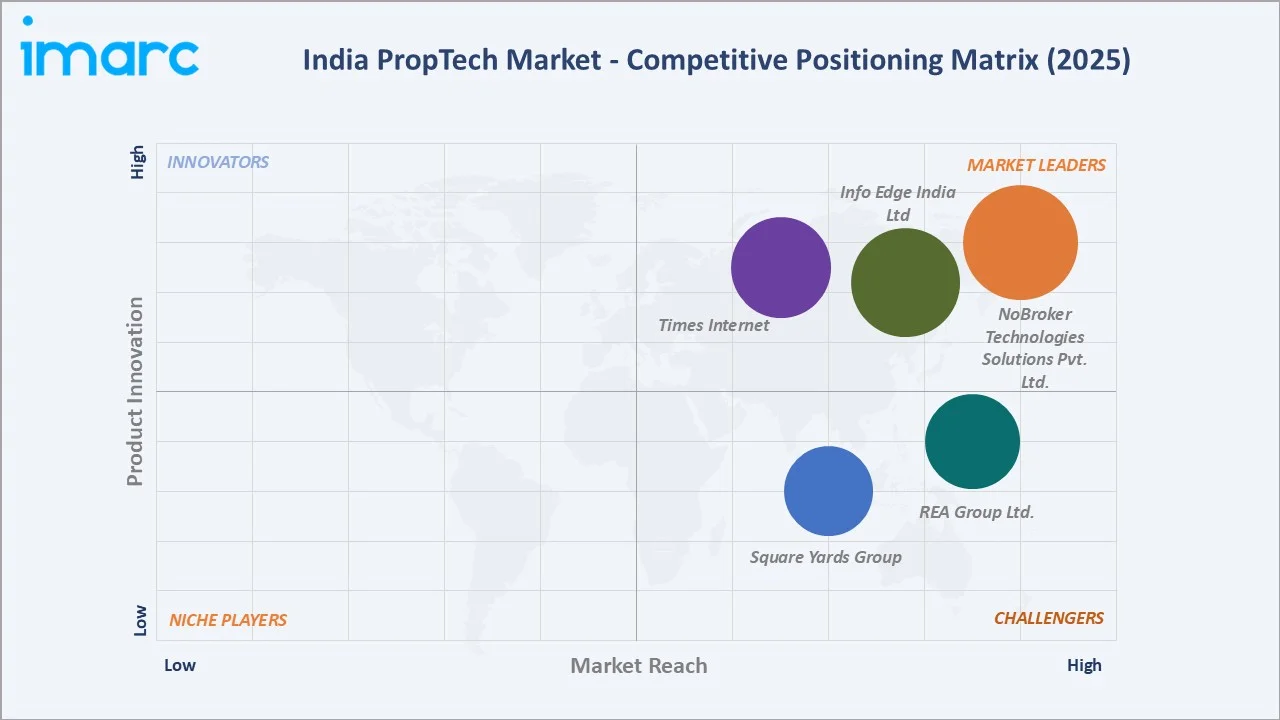

Competitive Landscape

The India proptech market is highly fragmented, with the top five platforms including NoBroker Technologies Solutions Pvt. Ltd., Info Edge India Ltd, Times Internet, REA Group Ltd., and Square Yards Group, collectively holding approximately 45–50% of total market revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

NoBroker Technologies Solutions Pvt. Ltd. |

NoBroker |

Market Leader |

Broker-free property transactions; AI-driven CRM; 10M+ users |

|

Info Edge India Ltd |

99acres |

Market Leader |

Property listings; RE media; strong developer-broker network |

|

Times Internet |

MagicBricks |

Market Leader |

AI CRM (READPRO); 85,000+ broker licences; 60M+ monthly users |

|

REA Group Ltd. |

Housing.com |

Strong Challenger |

Full-stack advisory; AR/VR tours; mortgage facilitation |

|

Square Yards Group |

PropVR, Square Connect, Azuro |

Strong Challenger |

End-to-end RE services; digital twins; global market linkage |

A large base of 500+ proptech startups across property search, transaction tech, smart buildings, co-living, and fractional investment ensures ongoing competitive intensity. The market is experiencing consolidation via M&A, with Aurum PropTech's acquisition of PropTiger in 2025 as the most notable recent transaction.

Key Company Profiles

NoBroker Technologies Solutions Pvt. Ltd.

NoBroker Technologies Solutions Pvt. Ltd., headquartered in Bengaluru, is India's first and largest broker-free real estate platform, connecting verified property owners directly with tenants and buyers. Founded in 2014, NoBroker has over 10 million registered users across 11 major cities.

- Product Portfolio: Broker-free rentals and sales, NoBroker Shield (rental protection), NobrokerHood (society management app), CallZen AI, home services.

- Recent Developments: In FY24, NoBroker saw its operating revenue grow ~32% to about INR 803 crore and narrowed its net loss by 19%.

- Strategic Focus: Platform monetization through subscription services; enterprise B2B SaaS expansion; AI-first product development roadmap.

Times Internet

Times Internet’s MagicBricks is a leading property portal serving over 60 million monthly users. Its READPRO AI-powered CRM platform has emerged as India's leading broker productivity tool, with 85,000+ active licenses across 200+ cities as of 2025.

- Product Portfolio: Property listings, READPRO AI CRM, MagicHomes (new developments guide), EMI calculator, property valuation tool, site visit product.

- Recent Developments: In March 2026, Magicbricks signed a one-year Memorandum of Understanding (MoU) with the National Real Estate Development Council (NAREDCO) to promote data-driven research, policy discussions, and knowledge sharing within India’s real estate sector.

- Strategic Focus: CRM SaaS monetization; broker ecosystem digitalization; Tier-2 city market expansion.

Square Yards Group

Square Yards Group, headquartered in Gurugram, is a global proptech company providing end-to-end real estate services across India and international markets, including the UAE, Canada, and Australia. The company reported operational profitability in FY2024-25, a key milestone among Indian proptech platforms.

- Product Portfolio: Property discovery, virtual site visits, mortgage assistance, legal documentation, 3D digital city twins, secondary market transactions.

- Recent Developments: In May 2026, Square Yards crossed INR 2,000 crore in revenue in FY26 and reported a 3.7× increase in EBITDA driven by strong growth across its ecosystem of real estate and proptech businesses.

- Strategic Focus: Profitability-led growth; secondary property market expansion; NRI and international investor acquisition.

Market Concentration Analysis

India's proptech market exhibits moderate-to-high fragmentation below the top five platforms. The top five players (NoBroker, 99acres, MagicBricks, Housing.com, and Square Yards) collectively hold approximately 45–50% of market revenue in 2025. Below this tier, 500+ startups serve niche segments including co-living, construction tech, smart buildings, fractional investment, and commercial property analytics.

M&A consolidation is accelerating with Aurum PropTech's acquisition of PropTiger (INR 86.45 Crore, 2025) and Info Edge's continued investment in 99acres, reflecting the market's maturation. Private equity interest is expanding beyond seed-stage into growth and late-stage proptech investments, with deal counts up 35% year-on-year in 2024–2025.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud proptech SaaS (estimated CAGR 14.5%), AI-driven property analytics (20%+ CAGR), smart building IoT (18.5% CAGR), and fractional ownership platforms (45% CAGR) represent the four highest-growth investment vectors through 2034. Together, these categories address a total addressable market of approximately USD 1.8 Billion by 2030 within India's combined domestic and international proptech market.

Emerging Market Expansion

Tier-2 and Tier-3 cities, including Jaipur, Indore, Lucknow, Kochi, and Coimbatore, collectively represent an incremental USD 600 Million proptech opportunity by 2034, as smartphone penetration deepens and local real estate formalizes. Proptech platforms entering these markets via asset-light digital-first strategies, vernacular language interfaces, and offline-to-online hybrid broker models are best positioned to capture first-mover advantages.

Venture and Institutional Investment Trends

- Key investment themes include AI property advisory, fractional ownership infrastructure, RegTech for RERA compliance, smart building management, and ConTech (construction technology) platforms addressing India's housing supply gap.

- SoftBank, Alpha Wave, WestBridge, and Tiger Global have committed over USD 1.5 Billion to Indian proptech between 2019 and 2025, with co-living, broker tech, and AI valuation platforms attracting the highest investment multiples.

- SEBI's SM-REIT framework (2024) has created a regulated investment structure enabling fractional real estate platforms to offer compliant, liquid investment products to retail investors, potentially unlocking USD 2+ Billion in new proptech capital.

Future Market Outlook (2026-2034)

The India proptech market is positioned for sustained, double-digit growth through 2034. From a base of USD 1.31 Billion in 2025 to USD 1.47 Billion in 2026, the market is projected to reach USD 3.82 Billion by 2034, representing total incremental value creation of USD 2.51 Billion at a CAGR of 12.26%. This growth will be driven by the deepening integration of AI, blockchain, IoT, and cloud technologies into India's USD 300+ Billion real estate sector.

Regulatory evolution will shape the competitive landscape: RERA's strengthening, the Digital Personal Data Protection Act's enforcement, and SEBI's SM-REIT regime will collectively raise compliance standards and favor well-capitalized platforms. Platforms that achieve regulatory alignment, operational profitability, and multi-city breadth by 2027 are positioned to capture disproportionate revenue growth as market consolidation reduces the competitive field.

Long-term, India's proptech trajectory is tied to three structural forces: urbanization adding 10+ million urban households annually, India's real estate sector targeting USD 1 Trillion contribution to GDP by 2030, and the government's continued investment in digital land records and smart city infrastructure. Proptech is transitioning from a listings-oriented industry toward a full-stack technology layer managing the entire lifecycle of property ownership, occupation, and investment across India.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews with over 120 industry stakeholders in 2024–2025, including proptech platform executives, real estate developers, institutional investors, RERA officials, and technology vendors across India, Singapore, and the UAE. Insights were used to validate market sizing, identify growth drivers, and triangulate segment-level revenue estimates.

Secondary Research

Secondary research encompassed company annual reports, SEBI filings, RERA registrations data, NHB and DPIIT databases, proptech industry reports (JLL, ANAROCK, CBRE), VC deal databases (Tracxn, Crunchbase), and trade publications. Over 180 secondary sources were reviewed and cross-validated to ensure analytical accuracy.

Forecasting Models

Market size estimations were derived using a combination of top-down and bottom-up forecasting approaches, incorporating real estate transaction volumes, Proptech user and revenue data from company disclosures, VC investment trends, and macroeconomic indicators. A base-case CAGR of 12.26% reflects consensus analyst estimates validated against reported platform revenue growth rates from FY2020 to FY2025.

India PropTech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solutions Covered | Business Intelligence, Facility Management, Portfolio Management, Real Estate Search, Asset Management, Enterprise Resource Planning, Others |

| Applications Covered |

|

| Deployments Covered | On-premises, Cloud |

| End Users Covered | Housing Associations, Real Estate Agents, Property Investors, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | NoBroker Technologies Solutions Pvt. Ltd., Info Edge India Ltd, Times Internet, REA Group Ltd., Square Yards Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India proptech market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India proptech market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India proptech industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India PropTech Market Report

The India proptech market size is estimated at USD 1.47 Billion in 2026 and is projected to reach USD 3.82 Billion by 2034.

The market is expected to grow at a CAGR of 12.26% during 2026-2034, driven by cloud adoption, AI integration, and rising real estate transaction digitalization.

West India leads with a 33.2% share in 2025, anchored by Mumbai's commercial real estate hub, Pune's IT corridor, and Gujarat's GIFT City digital infrastructure.

Cloud deployment dominates with a 64.3% share in 2025, driven by scalable SaaS platform adoption across brokers and property managers.

The residential segment holds a 58.4% share in 2025, fueled by urbanization, millennial home ownership demand, and digital property search behavior.

Key players include NoBroker Technologies Solutions Pvt. Ltd., Info Edge India Ltd, Times Internet, REA Group Ltd., and Square Yards Group.

AI powers recommendation engines, automated valuation models, AI CRM tools like READPRO and ConvoZen.AI, lead scoring, and conversational bots, directly improving broker productivity and platform conversion rates.

Key challenges include low digital literacy in Tier 3/4 cities, high customer acquisition costs, platform profitability, RERA compliance complexity, and data privacy regulation under the DPDPA 2023.

AI property analytics, cloud SaaS platforms, smart building IoT, fractional ownership, co-living management, and ConTech represent the highest-growth investment categories through 2034.

RERA's compliance mandates for project registration, payment timelines, and grievance redressal create structural demand for proptech compliance tools, driving adoption among developers and brokers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade