India PVC Pipes Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India PVC Pipes Market Size, Share, Trends & Forecast (2026-2034)

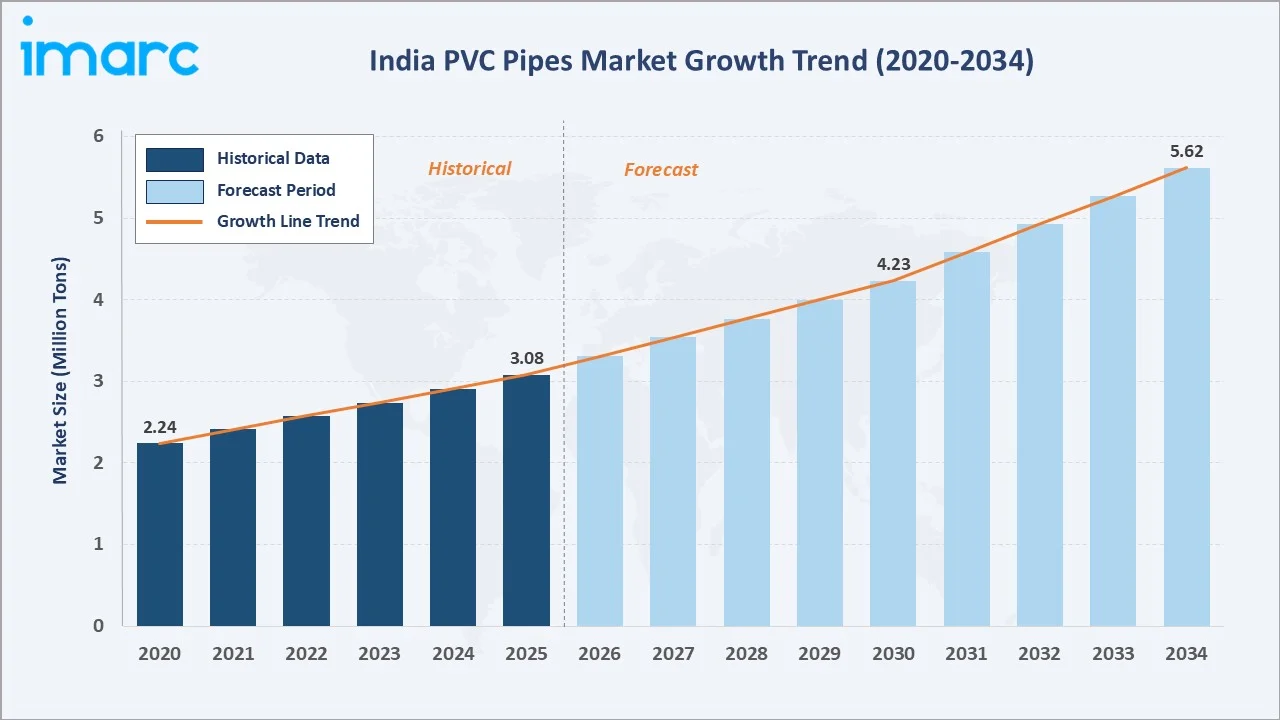

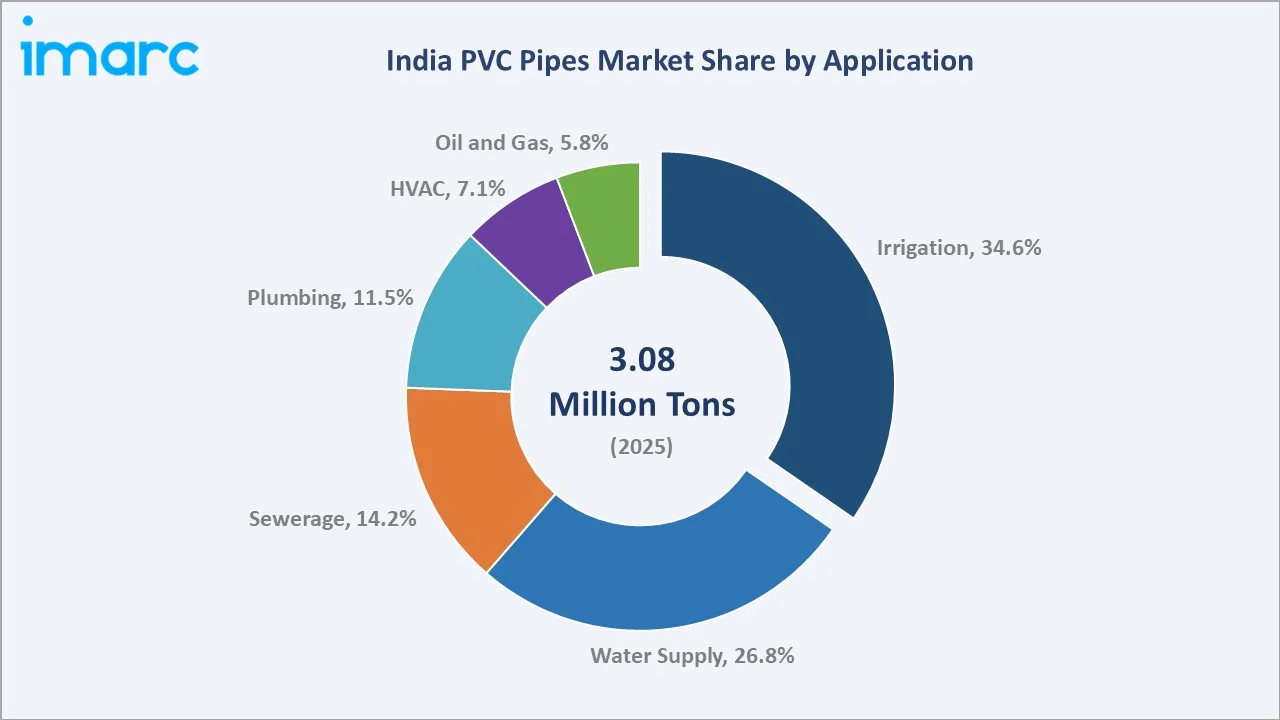

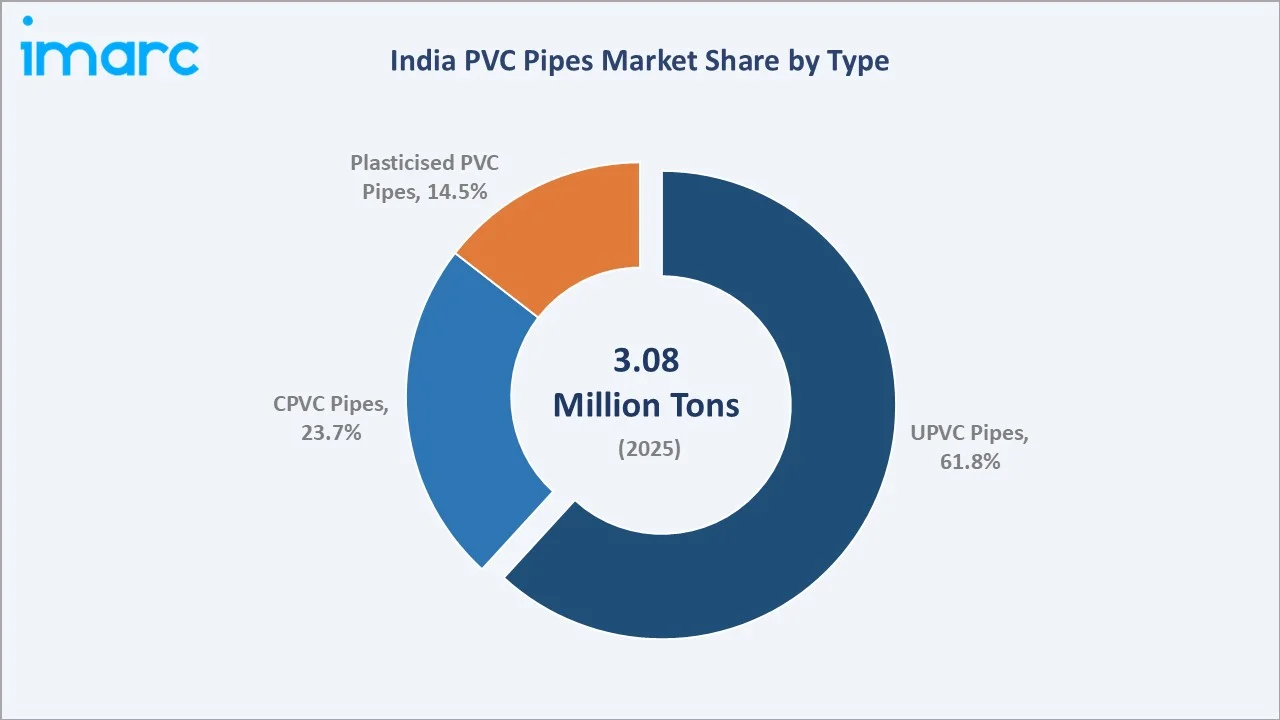

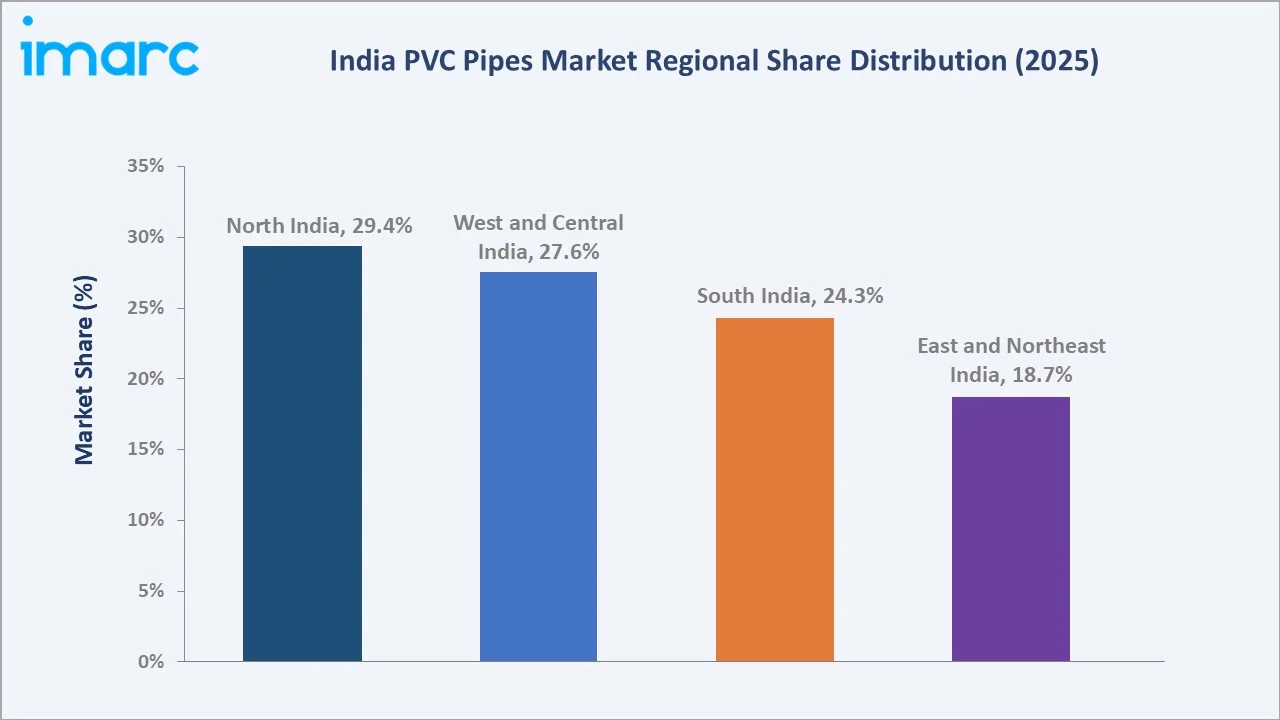

The India PVC pipes market size reached 3.08 Million Tons in 2025 and is projected to reach 5.62 Million Tons by 2034, exhibiting a CAGR of 6.59% during the forecast period 2026-2034. Rapid urbanization, large-scale government water infrastructure programs such as the Jal Jeevan Mission, expansion of micro-irrigation networks, and rising affordable housing construction are driving the India PVC pipes market growth. Irrigation applications lead at 34.6% share in 2025, while UPVC pipes account for 61.8% of total demand. North India dominates with 29.4% of national volume in 2025, supported by extensive agricultural plumbing and PMAY-led housing rollouts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

3.08 Million Tons |

|

Forecast Market Size (2034) |

5.62 Million Tons |

|

CAGR (2026-2034) |

6.59% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (29.4% share, 2025) |

|

Leading Type |

UPVC Pipes (61.8%, 2025) |

|

Leading Application |

Irrigation (34.6%, 2025) |

The India PVC pipes market growth trajectory from 2020 through 2034 reflects a steady historical expansion followed by a sharper forecast curve, anchored by accelerating government spending on water and sanitation infrastructure across rural and urban India.

To get more information on this market, Request Sample

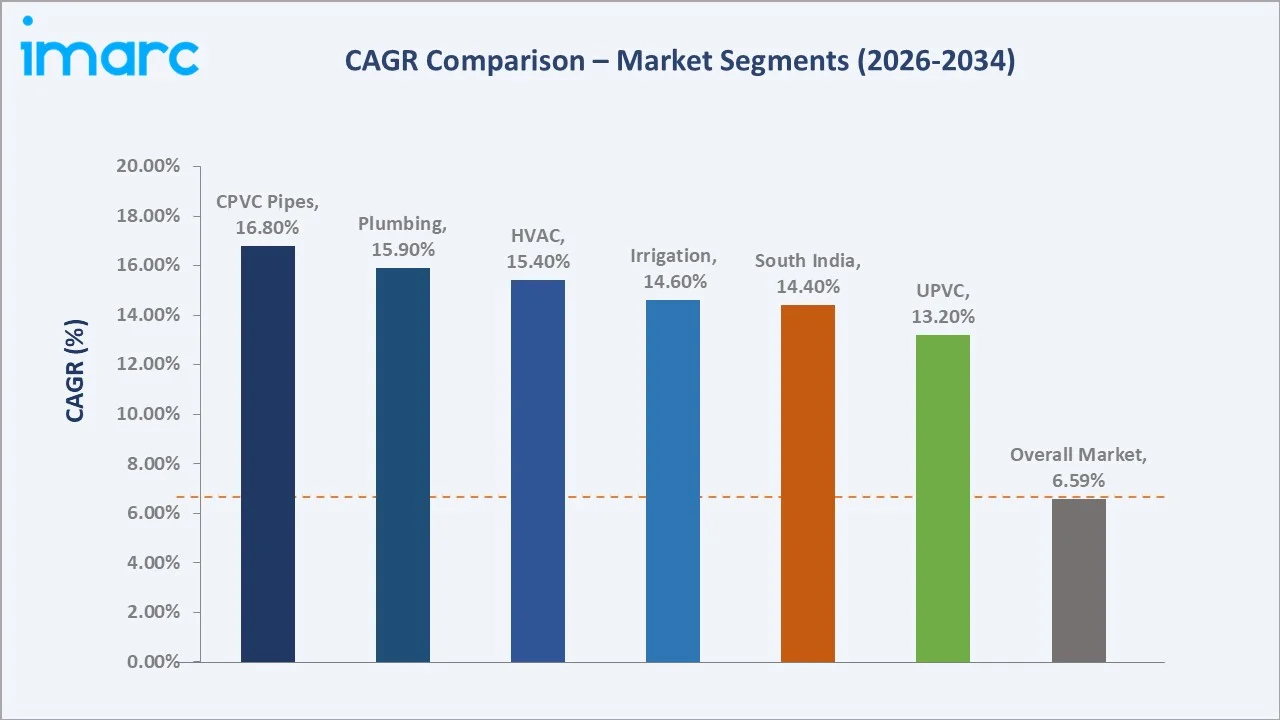

Segment-level CAGR comparisons highlight CPVC pipes and HVAC plus plumbing applications as the fastest-growing sub-segments within the India PVC pipes market forecast through 2034, outpacing the overall 6.59% market average.

Executive Summary

The India PVC pipes market is undergoing a structural transformation driven by mission-mode water infrastructure programs, agricultural modernization, and the rapid pace of residential construction. Valued at 3.08 Million Tons in 2025, the market is forecast to reach 5.62 Million Tons by 2034 at a CAGR of 6.59%. Volume growth is supported by tap-water connection targets under the Jal Jeevan Mission, which had reached over 78% of rural households by 2025.

Irrigation applications command a 34.6% share in 2025, propelled by drip and sprinkler adoption under the Pradhan Mantri Krishi Sinchayee Yojana. Water supply applications follow at 26.8%, reflecting urban distribution upgrades. UPVC pipes dominate with 61.8% of volume in 2025, while CPVC pipes are the fastest-growing type, projected to expand at roughly 16.8% CAGR through 2030 on the back of premium plumbing demand.

North India leads with a 29.4% share in 2025, while West and Central India hold 27.6% and South India accounts for 24.3%. The India PVC pipes market outlook remains highly positive as government capex, agricultural mechanization, and urbanization converge across all major regions through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Irrigation - 34.6% share (2025) |

|

Second Application |

Water Supply - 26.8% share (2025) |

|

Largest Type |

UPVC Pipes - 61.8% share (2025) |

|

Fastest Growing Type |

CPVC Pipes - ~16.8% CAGR (2025-2030) |

|

Leading Region |

North India - 29.4% volume share (2025) |

|

Top Companies |

Finolex Industries Ltd., Supreme Industries Ltd., Astral Limited, Prince Pipes & Fittings Ltd., APL Apollo. |

|

Market Opportunity |

Jal Jeevan Mission and PMAY-driven volume demand |

Key Analytical Observations Supporting the Data Above:

- Irrigation's 34.6% dominance in 2025 reflects accelerating micro-irrigation adoption, with India's drip and sprinkler coverage crossing 97 Lakh hectares as of 2025 under PMKSY.

- UPVC's 61.8% share is sustained by cost competitiveness for water supply and irrigation lines, where IS 4985-compliant UPVC remains the default specification across state water boards.

- CPVC's ~16.8% CAGR is driven by hot-water plumbing in mid-income housing, with India adding nearly 4.2 Crore urban housing units per year between 2022 and 2024 under PMAY-Urban.

- North India's 29.4% lead reflects high agricultural pipe consumption in Punjab, Haryana, Uttar Pradesh, and Rajasthan, plus large infrastructure pipelines in Delhi-NCR.

- Jal Jeevan Mission had achieved 15.4 crore tap connections by 2025, lifting rural PVC pipe demand by an estimated 18-22% annually through the program window.

- Top five players - Finolex, Supreme, Astral, Prince, and Apollo - collectively command an estimated 38-42% of organized market volume in 2025.

India PVC Pipes Market Overview

PVC pipes are rigid or semi-rigid polymer-based piping systems used to transport water, slurry, gases, and other fluids across agricultural, residential, commercial, and industrial settings. The Indian market includes a broad portfolio spanning UPVC, CPVC, and plasticized PVC variants, with diameters typically ranging from 12 mm in plumbing to over 600 mm in sewerage. These products are manufactured under BIS standards including IS 4985, IS 13592, IS 15778, and IS 7834.

The industry sits at the intersection of agricultural mechanization, urban water and sanitation upgrades, and real estate construction cycles. Macroeconomic tailwinds include central capex outlays of INR 11.11 lakh crore in FY2024-25, sustained PMAY rollouts, and the structural shift from galvanized iron to polymer plumbing across new builds. Volatile PVC resin imports from Northeast Asia create the principal cost pressure on the Indian supply base.

Market Dynamics

To evaluate market opportunities, Request Sample

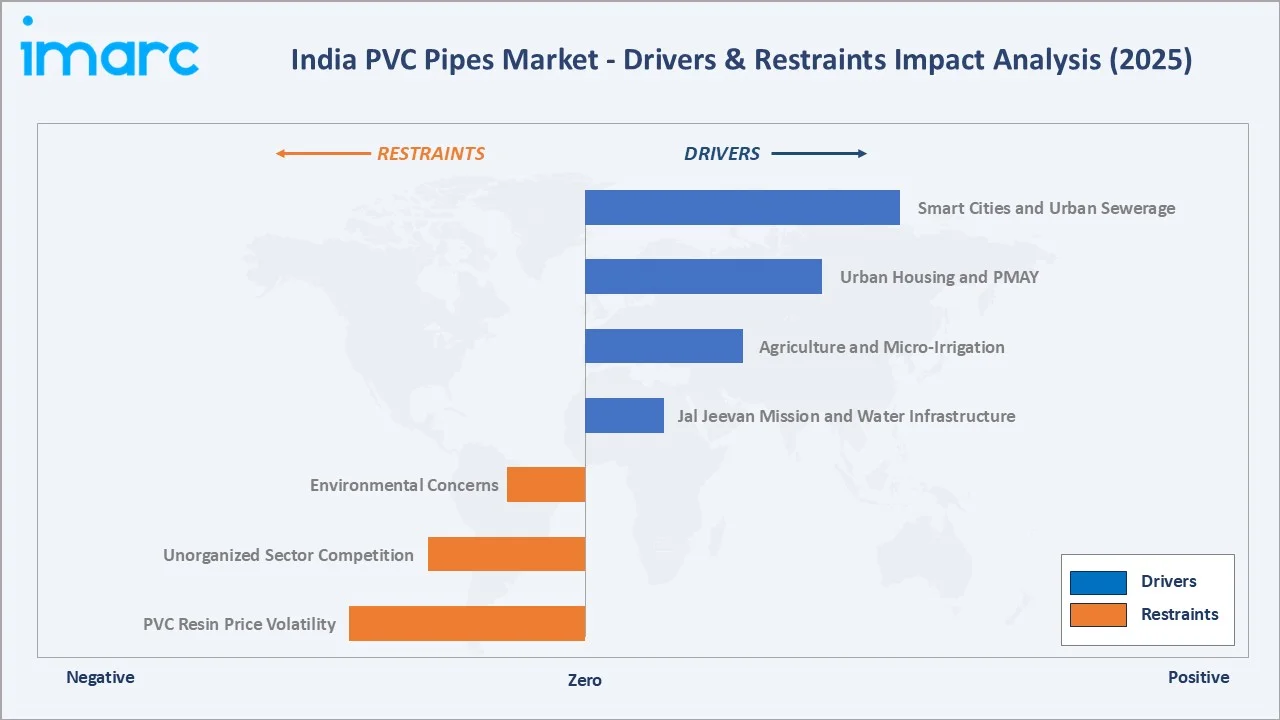

Market Drivers

- Jal Jeevan Mission and Water Infrastructure: The central government allocated INR 70,163 crore to the Department of Drinking Water and Sanitation in the 2024-25 Union Budget, fueling sustained PVC pipe procurement across rural water supply schemes.

- Agriculture and Micro-Irrigation: Under the PMKSY’s Per Drop More Crop component, India has brought over 7.5 million hectares under micro-irrigation since 2016, reflecting steady expansion of water-efficient farming practices, creating one of the largest sustained demand pools for UPVC and irrigation-grade fittings.

- Urban Housing and PMAY: Pradhan Mantri Awas Yojana (Urban) sanctioned over 1.18 crore houses since inception, with 89 lakh completed by early 2025, generating multi-year volume demand for plumbing-grade CPVC and UPVC systems.

- Smart Cities and Urban Sewerage: India’s urban transformation initiatives, including AMRUT 2.0, Smart Cities Mission, and Swachh Bharat Mission (Urban), together represent multi-lakh-crore investments in urban infrastructure and services, with sewerage and storm-water lines forming a key consumption segment for large-diameter PVC systems.

These four drivers operate concurrently rather than in isolation, which explains why analysts project sustained double-digit CAGR for the India PVC pipes market through 2034 even under conservative assumptions.

Market Restraints

- PVC Resin Price Volatility: India imports over 55% of its PVC resin demand. Asian contract prices for industrial alcohol and related chemicals have remained in the range of ~USD 300–430 per ton during 2023–2025, reflecting relatively stable supply-demand dynamics despite periodic volatility, directly compressing manufacturer margins.

- Unorganized Sector Competition: An estimated 35-40% of India's pipe volume continues to flow through unbranded and small-scale producers, intensifying price pressure for organized players in tier-3 and tier-4 markets.

- Environmental Concerns: Rising scrutiny on lead and phthalate stabilizers, plus tightening Central Pollution Control Board norms, is forcing reformulation costs on smaller producers.

Market Opportunities

- PVC-O and Premium Pipe Adoption: Molecularly oriented PVC pipes are emerging as a high-margin niche for water utilities, with early adopters in Maharashtra and Gujarat specifying PVC-O for trunk water mains.

- Recycled-Content Pipes: Brand owners are piloting closed-loop scrap recovery programs, opening a new ESG-aligned product tier as commercial real estate buyers begin specifying recycled content.

- Tier-3 and Tier-4 City Expansion: Smaller cities are expected to see a substantial increase in new urban dwellings over the coming years, driven by rapid urbanization and expanding housing demand, creating distribution-led growth opportunities for pan-India branded players.

Market Challenges

- BIS Lead-Free Compliance: Phased lead-free stabilizer mandates effective 2025-2027 are forcing alloy and additive transitions, raising input costs for smaller manufacturers without R&D scale.

- Counterfeit Branding: Spurious pipes mimicking established brands account for an estimated INR 4,000-5,000 crore in displaced sales annually, particularly in rural distribution.

- Logistics and Last-Mile Reach: Bulky pipe SKUs face transit damage and high freight intensity, limiting the economics of serving deep-rural micro-irrigation accounts beyond regional production hubs.

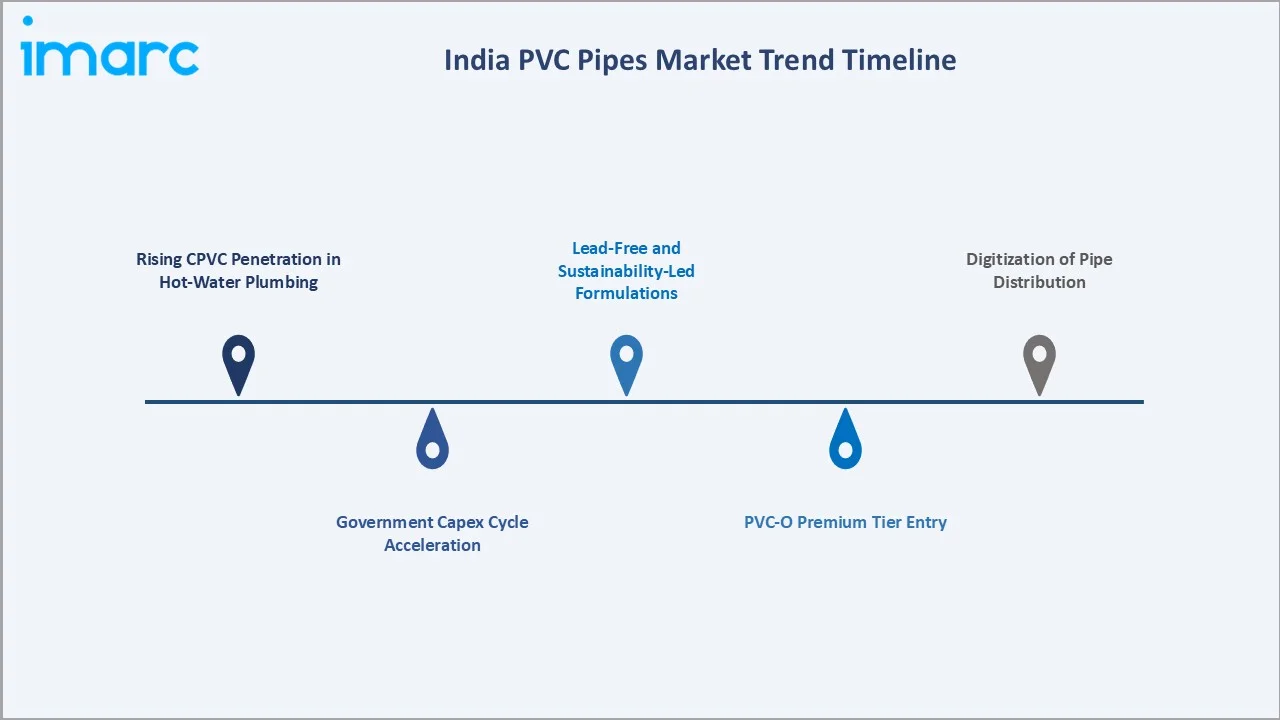

Emerging Market Trends

1. Rising CPVC Penetration in Hot-Water Plumbing

CPVC adoption is growing at roughly 16.8% CAGR through 2030 as developers shift from galvanized iron to corrosion-free polymer systems. Premium projects in metros are now specifying CPVC as a standard, while tier-2 cities are following with a one to two year lag.

2. Government Capex Cycle Acceleration

The Ministry of Jal Shakti has been allocated about ₹98,700 crore in FY2024–25, with the majority of spending directed toward drinking water and sanitation. A significant share of this allocation is focused on flagship programmes such as Jal Jeevan Mission. Pipe demand from JJM alone is estimated at 750-900 thousand tons of UPVC equivalent annually through the mission window, anchoring volume growth.

3. Lead-Free and Sustainability-Led Formulations

BIS amendments mandating phased phase-out of lead stabilizers are pushing organized manufacturers toward calcium-zinc and organic-tin systems. By 2027, lead-free PVC is expected to be the de facto standard across municipal tenders.

4. PVC-O Premium Tier Entry

Molecularly oriented PVC pipes deliver 30-40% higher pressure ratings at lower wall thickness. Indian utilities have begun trialing PVC-O for trunk mains, with Maharashtra Jeevan Pradhikaran among the early specifiers in 2024-2025.

5. Digitization of Pipe Distribution

B2B portals and dealer-app rollouts by Finolex, Astral, and Supreme are streamlining tier-3 and tier-4 reach. App-based ordering accounted for an estimated 14-18% of organized dealer transactions in 2025, up from under 5% in 2021.

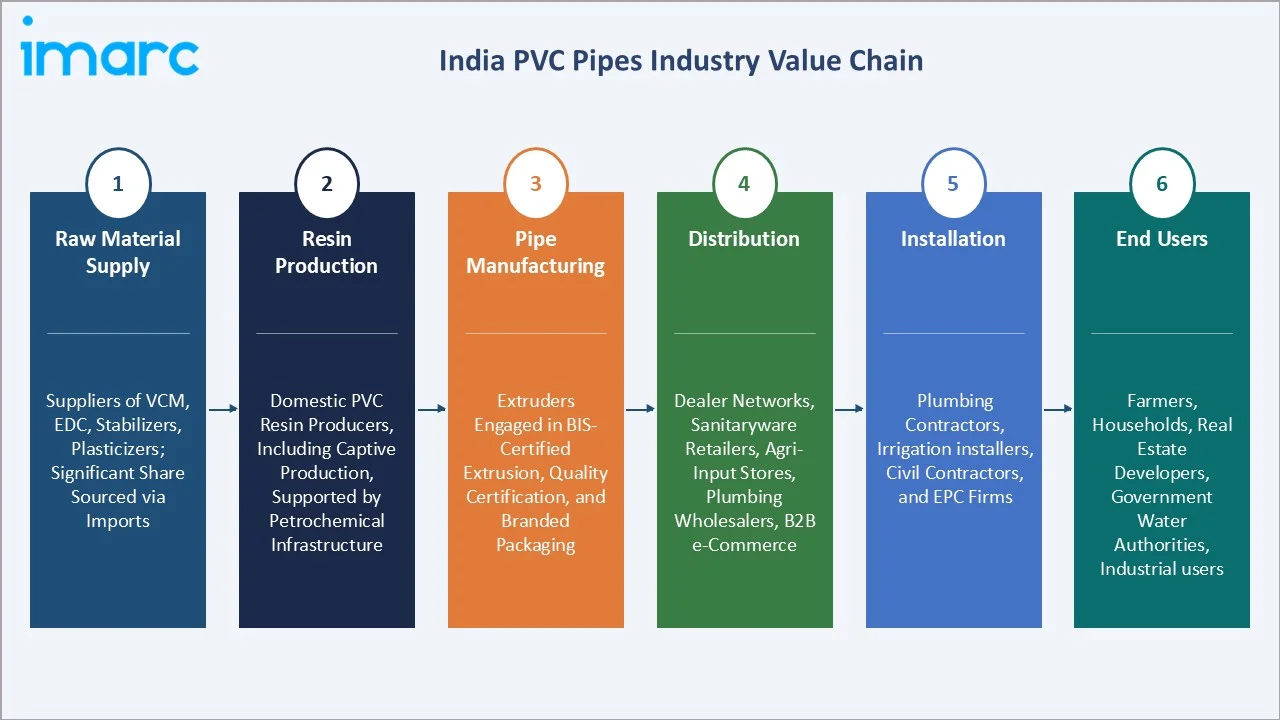

Industry Value Chain Analysis

The India PVC pipes value chain spans six integrated stages from raw material supply through end-user installation. Each stage carries distinct margin profiles and competitive dynamics relevant to the broader India PVC pipes market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Suppliers of vinyl chloride monomer (VCM), ethylene dichloride (EDC), stabilizers, plasticizers, and lubricants, with a significant share sourced through imports |

|

Resin Production |

Domestic producers manufacturing PVC resin, including captive production for downstream integration, supported by petrochemical infrastructure |

|

Pipe Manufacturing |

Pipe manufacturers engaged in extrusion, quality certification, and branded packaging for plumbing, irrigation, and infrastructure applications |

|

Distribution |

Extensive dealer networks, sanitaryware retailers, agricultural input stores, plumbing wholesalers, and B2B e-commerce platforms |

|

Installation |

Plumbing contractors, irrigation system installers, civil contractors, and EPC firms executing infrastructure and utility projects |

|

End Users |

Farmers, households, real estate developers, government water authorities, municipal bodies, and industrial users |

Pipe manufacturers capture the highest strategic value by integrating BIS-certified extrusion, brand equity, and a multi-tier dealer network. Distribution and last-mile installation are the key competitive moats, especially across rural and tier-3 territories where brand trust drives specification.

Technology Landscape in the PVC Pipes Industry

Resin and Stabilizer Innovation

Indian manufacturers are transitioning from lead-based stabilizers to calcium-zinc and organic-tin systems, in line with global REACH and EU norms. Calcium-zinc adoption crossed an estimated 60% of organized output by 2025 and is expected to be near-universal by 2027.

Materials Innovation - PVC-O and CPVC

Biaxially oriented PVC (PVC-O) and chlorinated PVC (CPVC) represent the technology frontier. PVC-O delivers up to 50% higher hydrostatic strength versus standard UPVC, while CPVC handles continuous service temperatures up to 93°C - making it the preferred polymer for hot-water plumbing in urban housing.

Smart Connectivity and Leak Detection

Sensor-embedded pipe systems for water utilities are at an early adoption stage. Pilots in Bengaluru, Pune, and Indore are integrating flow and pressure sensors at trunk-line level to support non-revenue water reduction, with a target of cutting NRW from 38% to under 20% by 2030.

Automation in Manufacturing

Leading players have invested in twin-screw extruders with inline laser micrometers and automated bagging, lifting line throughput by 25-35% versus a 2018 baseline. Industry 4.0 retrofits at Finolex and Astral plants now provide real-time defect detection and SKU-level OEE dashboards.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the India PVC pipes market, with forecasts at the national and regional levels from 2026 to 2034. The market has been segmented based on application and type.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Unplasticized PVC Pipes | 61.8% | 2025 |

| Application | Irrigation | 34.6% | 2025 |

| Region | North India | 29.4% | 2025 |

By Application

Irrigation leads the India PVC pipes market application with a 34.6% share in 2025. Demand is anchored by drip and sprinkler installations under PMKSY, with India's micro-irrigation coverage crossing 70 million hectares by 2024. Punjab, Maharashtra, and Andhra Pradesh remain the highest-consuming agricultural states for irrigation-grade UPVC pipes.

To access detailed market analysis, Request Sample

Water Supply applications account for 26.8%, anchored by Jal Jeevan Mission's tap connection rollouts and AMRUT 2.0 urban water upgrades. Sewerage holds 14.2%, supported by Swachh Bharat Mission Phase 2 and municipal sewer expansions. Plumbing represents 11.5%, where CPVC has emerged as the fastest-growing sub-segment within mid- and premium-housing projects.

HVAC applications hold 7.1% in 2025, with demand from commercial real estate cooling towers and chilled water lines. Oil and Gas accounts for 5.8%, primarily from city gas distribution networks where MDPE remains the default but PVC retains a role in non-pressure ancillary lines.

By Type

Unplasticized PVC (UPVC) is the dominant type at 61.8% share in 2025. Cost competitiveness, BIS standardization, and broad applicability across irrigation and water supply make UPVC the workhorse of the Indian market. State water utility tenders almost universally specify IS 4985-compliant UPVC pipes.

Chlorinated PVC (CPVC) holds 23.7% share and is the fastest-growing type at an estimated 16.8% CAGR through 2030. Hot-water plumbing in PMAY-Urban projects, premium residential builds, and HVAC chilled-water lines anchor demand. Brand-led adoption is highest in metros, while CPVC penetration in tier-3 cities is expanding rapidly as plumber awareness grows.

Plasticized PVC pipes account for 14.5% of volume in 2025. Flexible suction hoses, drainage applications, and low-pressure agricultural fittings are the principal use cases. Growth is moderate as rigid alternatives gain ground in most water-conveyance applications.

Regional Market Insights

|

Region |

Share (2025) and Key Growth Drivers |

|

North India |

29.4% - Punjab and Haryana agriculture, Delhi-NCR housing, JJM rollouts in UP and Rajasthan |

|

West and Central India |

27.6% - Maharashtra and Gujarat industrial demand, MP and Chhattisgarh JJM, Pune and Nagpur housing |

|

South India |

24.3% - Tamil Nadu and Andhra micro-irrigation, Bengaluru and Hyderabad commercial construction |

|

East and Northeast India |

18.7% - West Bengal and Bihar JJM acceleration, Northeast border infrastructure programs |

North India

North India commands 29.4% volume share in 2025. Punjab, Haryana, Uttar Pradesh, and Rajasthan together account for one of the densest agricultural pipe consumption belts in the country, with Punjab's micro-irrigation coverage exceeding 2.3 Million hectares by 2024. Delhi-NCR's residential pipeline and ongoing JJM rural connections sustain demand growth at slightly above the national CAGR.

West and Central India

West and Central India hold 27.6% share, anchored by Maharashtra, Gujarat, and Madhya Pradesh. Gujarat's agricultural belt and Maharashtra Jeevan Pradhikaran's water supply tenders form a stable demand base, while MP's JJM rollout has been one of the fastest among large states, with rural tap connections crossing 75% by 2024.

South India

South India accounts for 24.3% share, led by Tamil Nadu, Andhra Pradesh, Telangana, and Karnataka. The region combines strong micro-irrigation adoption in AP and TN with rapid commercial real estate construction in Bengaluru and Hyderabad. South India is also a leading hub for organized CPVC consumption, supported by Astral's Hyderabad manufacturing footprint.

East and Northeast India

East and Northeast India represent 18.7% volume share in 2025. JJM acceleration in Bihar and West Bengal is closing the historical demand gap, while infrastructure programs across the Northeast and Look-East corridor are creating fresh institutional pipeline opportunities. The region is forecast to show one of the higher growth rates over 2026-2030 from a smaller base.

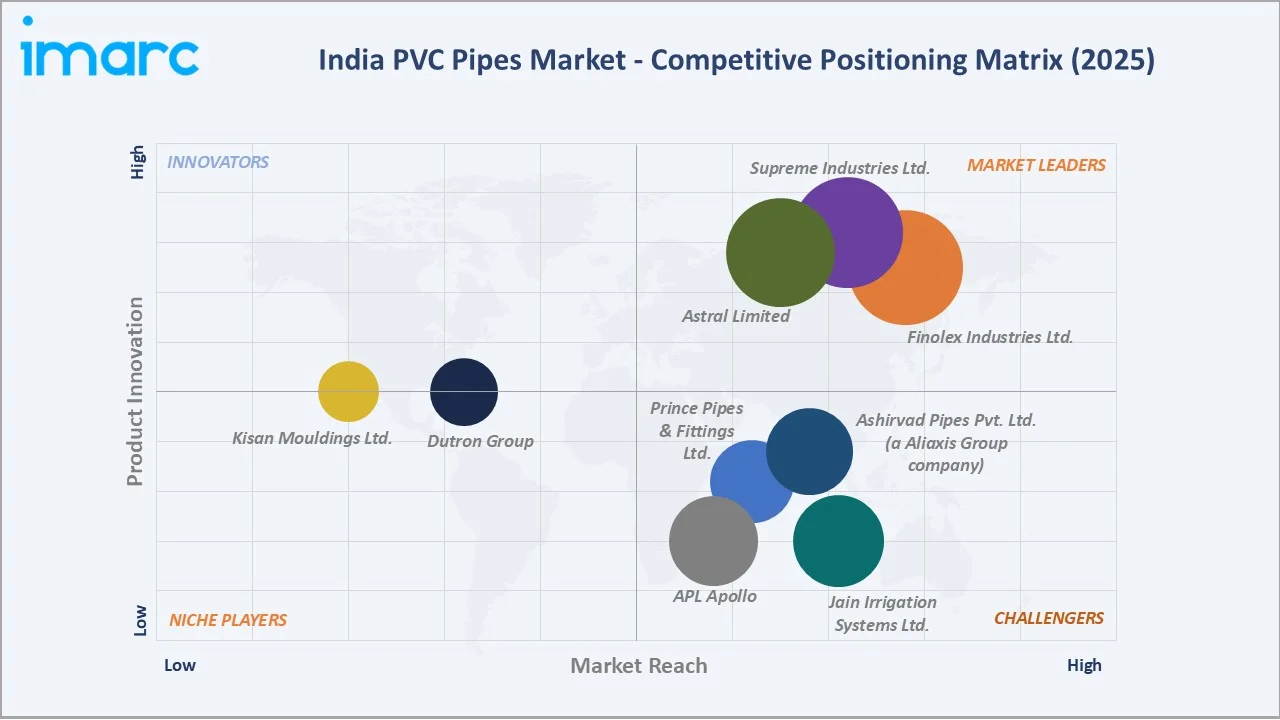

Competitive Landscape

|

Company Name |

Brand |

Market Position |

Core Strength |

|

Finolex Industries Ltd. |

Finolex Pipes |

Leader |

Captive PVC resin, agri-pipe leadership, pan-India dealer network |

|

Supreme Industries Ltd. |

Supreme Pipes |

Leader |

Broadest SKU range, premium plumbing, building products portfolio |

|

Astral Limited |

Astral Pipes |

Leader |

CPVC pioneer in India, premium plumbing, brand equity |

|

Prince Pipes & Fittings Ltd. |

Prince Pipes |

Challenger |

Lubrizol partnership, growing housing-segment penetration |

|

APL Apollo |

Apollo Pipes |

Challenger |

Cost-led North and West India presence, expanding capacity |

|

Ashirvad Pipes Pvt. Ltd. (a Aliaxis Group company) |

Ashirvad Pipes |

Challenger |

South India CPVC strength, Aliaxis backing, premium positioning |

|

Jain Irrigation Systems Ltd. |

Jain Irrigation Systems |

Challenger |

Micro-irrigation integration, agri-tech ecosystem |

|

Kisan Mouldings Ltd. |

Kisan Pipes |

Emerging |

Agri-irrigation focus, regional distribution depth |

|

Dutron Group |

Dutron Pipes |

Emerging |

Gujarat-led regional play, value segment focus |

The India PVC pipes competitive landscape is moderately fragmented. Pan-India organized brands compete with strong regional players and a long tail of unorganized producers. Leading players differentiate on BIS certification breadth, dealer reach, brand recall among plumbers and farmers, and increasingly on CPVC and premium-tier offerings.

Key Company Profiles

Finolex Industries Ltd.

Finolex Industries Ltd. is one of India's largest PVC pipe manufacturers and the only major fully integrated player with captive PVC resin capacity. Headquartered in Pune, Maharashtra, the company has been operating since 1981 and serves agriculture, plumbing, and infrastructure segments across the country.

- Product & Platform Portfolio: Finolex's portfolio includes UPVC agricultural pipes, CPVC plumbing systems under the Finolex CPVC range, SWR drainage pipes, column pipes for borewells, and a broad fittings catalogue. Annual pipe capacity exceeds 4 lakh tons across plants in Maharashtra and Gujarat.

- Recent Developments: Finolex Industries expanded its production capacity by adding 50,000 tonnes, taking its total installed capacity to around 5.2 lakh tonnes. The expansion was executed in phases across recent quarters, reflecting the company’s strategy to align capacity with expected industry growth.

- Strategic Focus: The company is focused on backward-integration advantages, deeper rural dealer reach, and expanding its CPVC plumbing share in tier-2 and tier-3 cities through brand campaigns and plumber-loyalty programs.

Supreme Industries Ltd.

Supreme Industries Ltd. is one of India's largest plastic processors with one of the broadest pipe portfolios in the market. Founded in 1942 and headquartered in Mumbai, the company spans plastic piping, packaging, industrial, and consumer products.

- Product & Platform Portfolio: Supreme's pipes portfolio covers UPVC, CPVC, HDPE, PPR, and composite pipes, with applications across plumbing, sewerage, fire-fighting, irrigation, and gas. The company operates over 25 manufacturing plants and serves more than 4,000 dealers nationally.

- Recent Developments: In FY2025, Supreme Industries announced a significant capital expenditure plan, committing over ₹1,100 crore toward capacity expansion and strategic growth initiatives. The investment includes the acquisition of Wavin India’s building and infrastructure business, strengthening its position in the piping segment.

- Strategic Focus: Supreme is targeting premium-tier growth in CPVC and PVC-O while maintaining its volume leadership in standard UPVC. Geographic expansion in eastern India and increasing the share of value-added fittings remain priority initiatives.

Astral Limited

Astral Limited, headquartered in Ahmedabad, Gujarat, is the largest CPVC pipe manufacturer in India and a leading premium plumbing brand. The company was founded in 1996 and operates a Lubrizol licensing partnership for CPVC compounds.

- Product & Platform Portfolio: Astral's portfolio spans CPVC plumbing, UPVC plumbing, SWR drainage, column pipes, agricultural pipes, and adhesives via its Resinova business. The company operates pipe manufacturing facilities in Gujarat, Tamil Nadu, Odisha, and Uttar Pradesh.

- Recent Developments: In 2025, Astral Limited strengthened its manufacturing footprint by commencing commercial production at its new Kanpur facility, marking a strategic expansion into North India. The plant is being developed in phases and will produce water tanks and PVC pipes, enhancing the company’s reach across key markets such as Uttar Pradesh and eastern regions.

- Strategic Focus: Astral's strategy centers on brand-led premium plumbing leadership, expansion in agri-pipes through dealer programs, and adjacent diversification into faucets, sanitaryware, and water tanks under the Astral Pipes umbrella.

Market Concentration Analysis

The India PVC pipes market is moderately fragmented. The top five organized players - Finolex Industries Ltd., Supreme Industries Ltd., Astral Limited, Prince Pipes & Fittings Ltd., APL Apollo - collectively account for an estimated 38-42% of organized market revenue in 2025. The balance is split between mid-sized regional brands such as Ashirvad Pipes Pvt. Ltd. (a Alixias Group company), Jain Irrigation Systems Ltd., Kisan Mouldings Ltd., Dutron Group and a long tail of unorganized producers.

Consolidation is gradually accelerating. Brand-led players continue to take share from the unorganized segment as BIS enforcement tightens and tier-3 distribution networks deepen. Premium plumbing categories, particularly CPVC, are more concentrated than commodity UPVC, with Astral, Supreme, and Ashirvad capturing the majority of organized CPVC volume.

Investment & Growth Opportunities

Fastest-Growing Segments

CPVC pipes are the highest-growth type at approximately 16.8% CAGR through 2030, anchored by housing plumbing demand. HVAC and plumbing applications are the fastest-growing application tiers at over 15% CAGR. PVC-O remains a small but rapidly expanding premium tier as utilities begin specifying it for trunk water mains.

Emerging Geographic Pockets

East and Northeast India represent the highest-growth regional pocket, expanding faster than the national average from a smaller base. Bihar, West Bengal, and Odisha have moved from JJM laggards to leaders in tap-connection additions during 2023-2025, opening fresh distribution territory for organized brands.

Capacity and Strategic Investment

Capex announcements across the top eight organized players exceeded INR 3,500 crore between 2023 and 2025, focused on capacity expansion, CPVC and PVC-O capability addition, and adjacent category entries into bathware, sanitaryware, and water tanks. Strategic M&A is rising, exemplified by Aliaxis's continued ownership consolidation in Ashirvad.

Future Market Outlook (2026-2034)

The India PVC pipes market forecast projects sustained volume expansion from 3.08 Million Tons in 2025 to 5.62 Million Tons by 2034 at a CAGR of 6.59%. North India will retain regional leadership, while East and Northeast India deliver the highest incremental growth on a smaller base. CPVC will continue gaining share within the premium plumbing tier.

Three structural shifts are expected to reshape the market through 2034. First, government water and sanitation capex will remain elevated through the next two five-year cycles, anchoring volume demand. Second, the lead-free formulation transition will be largely complete by 2027, raising entry barriers for sub-scale producers. Third, premium tiers led by CPVC and PVC-O will accelerate the shift in industry value pool toward branded organized players.

Research Methodology

Primary Research

Primary research conducted in 2024-2025 included structured interviews with PVC pipe manufacturers, PVC resin producers, dealer-distributors, plumbing contractors, micro-irrigation installers, and procurement managers at state water utilities. These inputs validated market sizing, segmentation shares, and pricing trends.

Secondary Research

Secondary sources include the Ministry of Jal Shakti's JJM dashboard, the Ministry of Housing and Urban Affairs PMAY-U reports, BIS standards documentation, Ministry of Agriculture micro-irrigation databases, company annual reports of Finolex, Supreme, Astral, Prince, and Apollo, and industry association data from PIPMA and the Plastics Export Promotion Council.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up models. Inputs include India's GDP and urbanization trajectory, government water and housing capex outlays, agricultural mechanization indices, and historical PVC resin pricing. Base, optimistic, and conservative scenario analysis was applied to manage macroeconomic uncertainty.

India PVC Pipes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Chlorinated PVC Pipes, Plasticized PVC Pipes, Unplasticized PVC Pipes |

| Applications Covered | Irrigation, Water Supply, Sewerage, Plumbing, HVAC, Oil and Gas |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Finolex Industries Ltd., Supreme Industries Ltd., Astral Limited, Prince Pipes & Fittings Ltd., APL Apollo, Ashirvad Pipes Pvt. Ltd. (a Aliaxis Group company), Jain Irrigation Systems Ltd., Kisan Mouldings Ltd., Dutron Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India PVC pipes market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India PVC pipes market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India PVC pipes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India PVC Pipes Market Report

The India PVC pipes market reached 3.08 Million Tons in 2025, supported by JJM water connections, urban housing under PMAY, and accelerating micro-irrigation across major agricultural states.

The market is projected to reach 5.62 Million Tons by 2034, growing at a CAGR of 6.59% during 2026-2034, driven by sustained government water capex and premium plumbing demand.

Irrigation applications lead with a 34.6% share in 2025, supported by drip and sprinkler adoption under PMKSY and over 16 million hectares of micro-irrigated farmland by 2024.

Unplasticized PVC (UPVC) pipes hold 61.8% volume share in 2025, with cost competitiveness and BIS standardization making UPVC the default choice for water supply and irrigation lines.

Chlorinated PVC (CPVC) is the fastest-growing type, expanding at roughly 16.8% CAGR through 2030, driven by hot-water plumbing demand in PMAY housing and premium residential builds.

North India leads with a 29.4% share in 2025, supported by Punjab and Haryana agriculture, Delhi-NCR housing pipelines, and JJM-driven rural water connections in UP and Rajasthan.

Key drivers include the Jal Jeevan Mission, PMKSY micro-irrigation, PMAY housing rollouts, AMRUT 2.0 urban water upgrades, Smart Cities Mission infrastructure, and rising real estate construction across tier-2 cities.

Major players include Finolex Industries Ltd., Supreme Industries Ltd., Astral Limited, Prince Pipes & Fittings Ltd., APL Apollo, Ashirvad Pipes Pvt. Ltd. (a Aliaxis Group company), Jain Irrigation Systems Ltd., Kisan Mouldings Ltd., Dutron Group.

Key restraints include PVC resin price volatility, intense unorganized sector competition, lead-free compliance transition costs, counterfeit branding, and last-mile logistics constraints in deep-rural markets.

JJM had reached over 15.7 crore tap connections by 2025, lifting rural PVC pipe demand by an estimated 18-22% annually and creating one of the largest sustained volume drivers for UPVC pipes.

CPVC is replacing galvanized iron and copper in hot-water plumbing across PMAY-Urban housing and premium residential builds. CPVC is the fastest-growing premium tier at roughly 16.8% CAGR through 2030.

Top opportunities include CPVC capacity expansion, PVC-O premium pipes for trunk water mains, recycled-content product lines, eastern India distribution build-out, and adjacent diversification into bathware and water tanks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)