India Rechargeable Battery Market Size, Share, Trends and Forecast by Battery Type, Capacity, Application, and Region, 2026-2034

India Rechargeable Battery Market Summary:

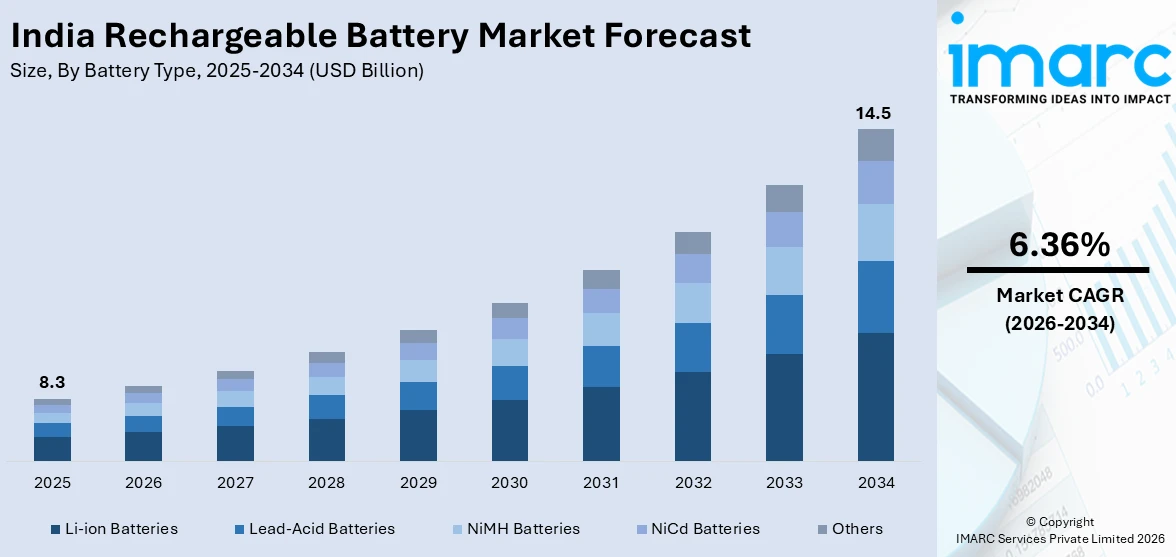

The India rechargeable battery market size was valued at USD 8.3 Billion in 2025 and is projected to reach USD 14.5 Billion by 2034, growing at a compound annual growth rate of 6.36% from 2026-2034.

The India rechargeable battery market is experiencing growth driven by the rapid electrification of transportation, expanding consumer electronics adoption, and the nation’s ambitious renewable energy storage targets. Supportive government policies, increasing domestic manufacturing investments, and technological advancements in lithium-ion and advanced chemistry cells are reshaping the energy storage ecosystem. Rising urbanization, higher per capita income, and heightened awareness about sustainable energy solutions are further strengthening market momentum, positioning India as a key player in the market.

Key Takeaways and Insights:

- By Battery Type: Li-ion batteries lead the market with a share of 40% in 2025, driven by their superior energy density, lightweight design, extended cycle life, and broad applicability across consumer electronics, electric vehicles (EVs), and grid-scale energy storage systems.

- By Capacity: 6000-10000 mAh dominates the market with a share of 25% in 2025, propelled by the growing demand from high-performance smartphones, portable power banks, and mid-range electronic devices requiring extended battery backup and enhanced power delivery capabilities.

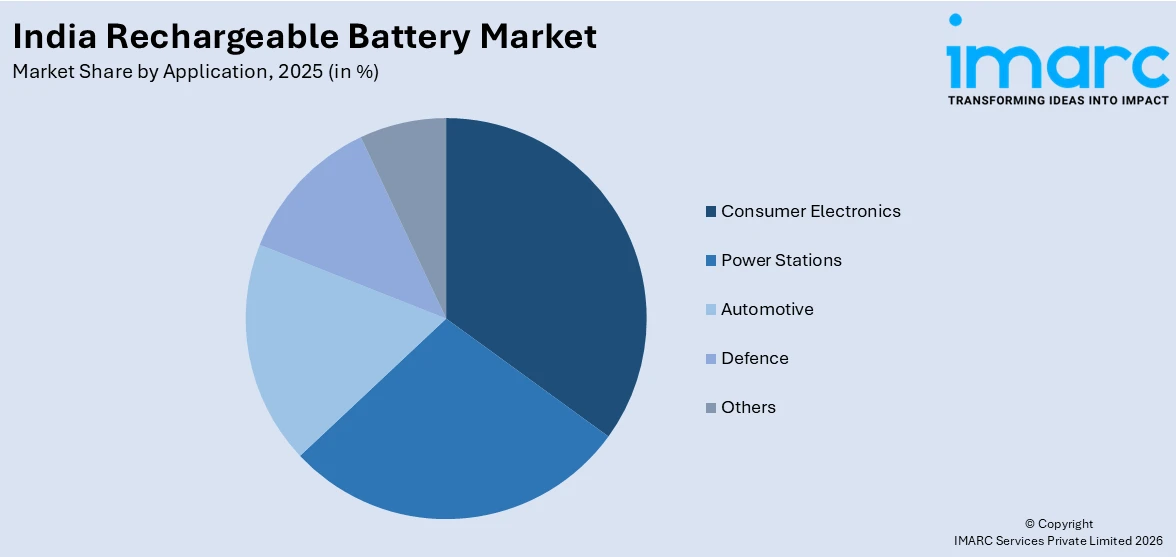

- By Application: Consumer electronics represent the largest segment with a market share of 33% in 2025, underpinned by India’s position as the second-largest smartphone market globally, expanding laptop penetration, and rising adoption of wearable devices and smart home technologies.

- Key Players: The India rechargeable battery market features a moderately competitive landscape, with established domestic manufacturers and global corporations investing in capacity expansion, advanced chemistry development, and strategic partnerships to strengthen their market positioning across mobility and storage applications.

To get more information on this market Request Sample

The India rechargeable battery market is progressing steadily as the country advances its clean energy transition and digital transformation objectives. Expanding electric vehicle (EV) adoption, rising renewable energy installations, and higher utilization of connected electronic devices are collectively increasing the demand for reliable and high-performance battery technologies across mobility, grid, residential, and industrial applications. Large energy users are integrating battery energy storage systems to improve load management, ensure backup power, and support renewable energy utilization. In line with this momentum, in 2025, Cummins India launched modular Battery Energy Storage Systems under its “Destination Zero” strategy, offered in 10ft and 20ft container configurations with capacities ranging from 200 kWh to 2 MWh, incorporating lithium ferrophosphate rechargeable batteries with liquid cooling and multi layer fire protection. Such advancements highlight the growing strategic importance of rechargeable batteries in strengthening India’s sustainable energy infrastructure.

India Rechargeable Battery Market Trends:

Government Incentives and Localization Policies

Policy support aimed at strengthening domestic manufacturing capabilities is encouraging investment in rechargeable battery production. Incentive schemes focused on advanced chemistry cell manufacturing, electric mobility, and clean energy technologies are promoting capacity expansion and technology transfer within the country. Efforts to reduce import dependence and build integrated supply chains are improving long term industry stability. Financial incentives, infrastructure development support, and regulatory frameworks are fostering private sector participation in battery assembly and component manufacturing. For example, in 2025, the Ministry of Electronics and IT strengthened India’s push in rechargeable battery technology through its Centre of Excellence at CMET Pune, focused on lithium-ion, sodium-ion, and lithium-polymer cells. An industry meet brought together government bodies, associations, and companies to scale indigenous battery manufacturing and reduce import dependence. This policy driven push toward localization is enhancing competitiveness and stimulate sustained growth in the rechargeable battery market.

Accelerated Electric Vehicle Adoption

The rapid growth of India’s EV ecosystem is significantly increasing the demand for rechargeable batteries across mobility segments. Rising fuel prices, policy incentives, and greater environmental awareness are accelerating the shift toward electric two wheelers, three wheelers, passenger cars, buses, and commercial fleets. Automotive manufacturers are expanding production capacities and introducing new electric models, strengthening the need for advanced lithium-ion battery technologies. In line with this transition, India has set a target to achieve 30% EV penetration in private cars, 70% in commercial vehicles, 40% in buses, and 80% in two and three wheelers by 2030, representing nearly 80 million EVs, further reinforcing long term battery demand.

Growth in Consumer Electronics and Portable Devices

Increasing adoption of smartphones, laptops, tablets, wearables, and wireless accessories is driving the demand for compact and high-performance rechargeable batteries in India. Rising digital penetration, urbanization, and higher disposable incomes are supporting growth in device ownership and replacement cycles, prompting manufacturers to enhance battery life, charging efficiency, and durability. This focus on energy efficient design is evident in product innovations such as Logitech’s 2025 launch of the Signature Slim Solar+ K980 wireless keyboard in India, featuring Logi LightCharge technology and a rechargeable battery designed to last up to 10 years. Such advancements reinforce the central role of rechargeable batteries in sustaining India’s expanding consumer electronics ecosystem.

Market Outlook 2026-2034:

The India rechargeable battery market demonstrates strong revenue growth potential throughout the forecast period, supported by structural demand drivers across electric mobility, consumer electronics, and energy storage applications. The market generated a revenue of USD 8.3 Billion in 2025 and is projected to reach a revenue of USD 14.5 Billion by 2034, growing at a compound annual growth rate of 6.36% from 2026-2034. Domestic manufacturing capacity expansion, favorable government policies, technological innovation in advanced battery chemistries, and rising electrification of transportation are expected to sustain revenue momentum and reshape the competitive dynamics of India’s rechargeable battery ecosystem.

India Rechargeable Battery Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Battery Type | Li-ion Batteries | 40% |

| Capacity | 6000-10000 mAh | 25% |

| Application | Consumer Electronics | 33% |

Battery Type Insights:

- Lead-Acid Batteries

- Li-ion Batteries

- NiMH Batteries

- NiCd Batteries

- Others

Li-ion batteries dominate with a market share of 40% of the total India rechargeable battery market in 2025.

Li-ion batteries hold the biggest market share driven by their high energy density and lightweight structure. These batteries deliver longer backup time while occupying less space, making them ideal for smartphones, laptops, electric vehicles, and portable electronics. Rapid growth in consumer electronics adoption across India is catalyzing the demand for efficient and compact power solutions. Li-ion technology also offers faster charging capability compared to traditional alternatives, improving user convenience. Falling production costs and expanding domestic assembly under government initiatives have further supported adoption. Their longer cycle life reduces replacement frequency, increasing overall cost efficiency for consumers and industrial users nationwide.

Another reason for Li-ion dominance is the accelerating transition toward electric mobility and renewable energy storage solutions. Electric two-wheelers, passenger vehicles, and battery energy storage systems rely heavily on Li-ion chemistry for stable performance and scalability. Government incentives promoting EV adoption and local battery manufacturing have encouraged large-scale investments in Li-ion cell production. These batteries also exhibit lower self-discharge rates and improved thermal management compared to older rechargeable technologies. The growing awareness about environmental sustainability is encouraging industries to prefer energy-efficient storage options. Strong demand from telecom towers, power backup systems, and residential solar installations continues to reinforce Li-ion’s leading share in the market.

Capacity Insights:

- 150-1000 mAh

- 1300-2700 mAh

- 3000-4000 mAh

- 4000-6000 mAh

- 6000-10000 mAh

- More Than 10000 mAh

6000-10000 mAh leads with a market share of 25% of the total India rechargeable battery market in 2025.

The 6000–10000 mAh segment represents the largest segment owing to rising demand for longer backup across mid-sized electronic devices. This range is widely used in power banks, portable speakers, handheld gaming devices, and select medical equipment, where moderate weight and extended runtime are essential. Indian users increasingly prefer batteries that support full-day usage without frequent charging, especially in regions with inconsistent power supply. The capacity balance between portability and performance makes this segment commercially attractive. Manufacturers also find it cost-effective to produce at scale, supporting competitive pricing and higher adoption across individuals and small business applications nationwide.

Another factor driving the dominance of the 6000–10000 mAh range is its suitability for expanding outdoor and mobility-driven lifestyles. With the growth of travel, remote work, and digital learning, reliable portable power solutions have become essential. This capacity range supports multiple device charges while remaining compact enough for everyday carrying. It is also widely integrated into rechargeable lighting systems and backup units used in rural and semi-urban households. E-commerce platforms promote this segment heavily due to strong consumer demand and repeat purchases. Its adaptability across personal electronics and small-scale backup systems continues to secure the largest share within India’s rechargeable battery capacity market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Consumer Electronics

- Power Stations

- Automotive

- Defence

- Others

Consumer electronics exhibit a clear dominance with a 33% share of the total India rechargeable battery market in 2025.

Consumer electronics leads the market due to the widespread adoption of smartphones, laptops, tablets, wearable devices, and wireless accessories. According to the IBEF, around 85.5% of households in India owned at least one smartphone. India’s expanding digital ecosystem is increasing reliance on portable devices for communication, entertainment, education, and work. Each of these products depends heavily on rechargeable battery technology for performance and mobility. Rising disposable income and frequent device upgrades further stimulate battery demand. The rise in online streaming, gaming, and remote working is intensifying daily device usage, creating consistent charging cycles. This sustained utilization pattern ensures steady replacement demand and strengthens the dominance of consumer electronics within the rechargeable battery application landscape nationwide.

Another reason for this leadership is the rapid growth of smart home devices and connected consumer products. Items, such as wireless earbuds, smartwatches, Bluetooth speakers, portable cameras, and home security systems, rely on compact rechargeable batteries. Seasonal sales and festive promotions drive high device turnover, indirectly increasing battery production volumes. Local assembly and government incentives supporting electronics manufacturing are expanding domestic battery integration. Product innovation focused on faster charging and longer backup also pushes manufacturers to adopt advanced rechargeable solutions. As digital lifestyles deepen across urban and rural markets, consumer electronics continues to generate the largest share of battery demand in India’s rechargeable battery industry.

Regional Insights:

- North India

- West and Central India

- East India

- South India

North India represents a key market for rechargeable batteries, supported by strong automotive demand, rising electric vehicle adoption, and a broad consumer electronics base. Uttar Pradesh led the country’s EV transition in 2024, accounting for 19% of total national EV sales with nearly 3.6 lakh units sold. This leadership in sustainable mobility is generating significant demand for rechargeable battery systems across lead-acid and lithium-ion chemistries, strengthening regional market growth.

West and Central India is emerging as a critical hub for rechargeable battery manufacturing and consumption, anchored by Gujarat and Maharashtra’s industrial infrastructure and government incentives for clean energy investments. The region benefits from multiple gigafactory developments, including Agratas’ 20 GWh facility in Sanand, Gujarat, with construction rapidly advancing as of 2025, positioning the region as a key manufacturing center for advanced rechargeable battery technologies.

South India is a prominent hub for rechargeable battery manufacturing and innovation, with Telangana, Karnataka, and Tamil Nadu hosting major producers and research centers. The region benefits from a strong electronics manufacturing base and close links to key automotive clusters, supporting production scale, supply chain efficiency, and technology development.

East India represents a growing market for rechargeable batteries, supported by increasing electrification initiatives, expanding telecommunications infrastructure, and rising consumer electronics penetration in both urban and semi-urban areas. The region’s demand is driven by requirements for backup power solutions, electric three-wheelers for last-mile connectivity, and the gradual expansion of renewable energy installations that require battery storage solutions for managing intermittent power generation.

Market Dynamics:

Growth Drivers:

Why is the India Rechargeable Battery Market Growing?

Advancements in Battery Technology and Cost Optimization

Ongoing advancements in battery chemistry, energy density, safety parameters, and lifecycle durability are strengthening the commercial prospects of rechargeable batteries across diverse applications. Sustained research initiatives are enabling faster charging capabilities, longer operational life, and lower production costs, improving overall value propositions for end users. Expansion of domestic manufacturing capacities is generating economies of scale, resulting in more competitive pricing and improved supply chain stability. Progress in battery management systems is enhancing operational efficiency and safety, while improvements in recycling technologies are supporting resource recovery and environmental sustainability. Collectively, these developments are broadening application scope and reinforcing long term industry growth.

Renewable Energy Expansion Necessitating Battery Storage Solutions

India’s accelerated transition toward renewable energy is generating sustained demand for rechargeable battery based energy storage systems to manage variability in solar and wind power generation. As renewable capacity expands, grid reliability increasingly depends on large scale storage deployment. According to the National Electricity Plan, India will require 16.13 GW and 82.37 GWh of energy storage capacity by 2026-27, including 7.45 GW and 47.65 GWh from pumped storage projects and 8.68 GW and 34.72 GWh from battery energy storage systems. These projections underscore the scale of infrastructure investment needed to stabilize the grid. The resulting capacity additions represent a strong structural driver for long term growth in the rechargeable battery market.

Growing Demand for Backup Power Solutions

Persistent power fluctuations and the growing requirement for uninterrupted electricity supply across residential, commercial, and institutional environments are driving the demand for rechargeable battery based backup systems. Households are increasingly adopting inverters and home energy storage units to sustain essential appliances during grid outages. Businesses, hospitals, and data centers depend on dependable backup infrastructure to avoid financial losses and service interruptions. Expanding digital services, cloud operations, and remote work arrangements have further elevated the importance of continuous power availability. With rising electricity consumption and higher expectations for reliability, rechargeable batteries are playing a critical role in strengthening decentralized energy resilience across India.

Market Restraints:

What Challenges the India Rechargeable Battery Market is Facing?

Raw Material Import Dependency Constraining Supply Chain Resilience

India lacks substantial domestic reserves of critical battery raw materials including lithium, cobalt, and nickel, creating significant supply chain vulnerabilities and exposure to international price volatility. This dependency on imports for essential cathode and anode materials increases manufacturing costs and creates strategic risks, particularly amid evolving global trade dynamics and export restrictions from key mineral-producing nations.

High Capital Requirements Limiting Manufacturing Scale-Up

Establishing advanced battery cell manufacturing facilities requires significant capital expenditure on equipment, technology, and quality control systems. High upfront investment thresholds limit entry opportunities for smaller domestic manufacturers and lengthen the path to commercially viable scale. These challenges are further intensified by stringent performance, safety, and reliability standards associated with automotive battery applications.

Technology Gap and Skilled Workforce Shortage

India’s rechargeable battery manufacturing ecosystem faces challenges related to limited indigenous technological capabilities and a shortage of specialized workforce trained in advanced cell manufacturing processes. The reliance on technology transfer agreements with established international manufacturers creates dependency risks, while developing domestic research and development (R&D) infrastructure requires sustained investment and time.

Competitive Landscape:

The India rechargeable battery market features a dynamic competitive landscape characterized by established domestic battery manufacturers diversifying into advanced lithium-ion technologies alongside global corporations establishing manufacturing operations in the country. Competition is intensifying as multiple players invest in gigawatt-scale manufacturing facilities, ranging form technology partnerships, and pursue backward integration strategies to strengthen supply chain capabilities. The market dynamics are further shaped by government incentive programs that encourage domestic production, creating a favorable environment for both incumbents expanding their technology portfolios and new entrants bringing advanced manufacturing capabilities to India’s growing energy storage ecosystem.

Recent Developments:

- December 2025: Portronics launched its USB-C rechargeable “Lithius Cell” lithium-ion batteries in AA and AAA formats, aimed at replacing disposable cells. Each battery features a built-in Type-C charging port, 1.5V stable output, LED charge indicator, and safety protections against overheating and short circuits. The reusable batteries target everyday devices like remotes, keyboards, and gaming controllers as a more sustainable alternative.

- July 2025: Eveready Industries launched India’s first patent-applied Hybrid Torch featuring a built-in rechargeable Li-ion battery along with support for 3xAA batteries for dual power use. The torch charged via USB Type-C in 2.5 hours and included a 1W front LED and 1W side light with overcharge and deep discharge protection.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Battery Types Covered | Lead-Acid Batteries, Li-ion Batteries, NiMH Batteries, NiCd Batteries, Others |

| Capacity Covered | 150-1000 mAh, 1300-2700 mAh, 3000-4000 mAh, 4000-6000 mAh, 6000-10000 mAh, More Than 10000 mAh |

| Applications Covered | Consumer Electronics, Power Stations, Automotive, Defence, Others |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Rechargeable Battery Market Report

The India rechargeable battery market size was valued at USD 8.3 Billion in 2025.

The India rechargeable battery market is expected to grow at a compound annual growth rate of 6.36% from 2026-2034 to reach USD 14.5 Billion by 2034.

Li-ion batteries hold the largest revenue share of 40% in 2025, driven by their superior energy density, extended cycle life, broad applicability across consumer electronics, electric vehicles, and energy storage systems, and declining manufacturing costs that enhance market accessibility.

Key factors driving the India rechargeable battery market include strong policy support for domestic manufacturing, capacity expansion, and reduced import dependence. In 2025, the Ministry of Electronics and IT advanced indigenous battery development through its Centre of Excellence at CMET Pune, promoting lithium-ion, sodium-ion, and lithium-polymer technologies.

Major challenges include raw material import dependency for critical minerals like lithium and cobalt, high capital requirements for manufacturing scale-up, technology gaps requiring foreign partnerships, supply chain vulnerabilities, and shortage of specialized workforce trained in advanced cell manufacturing processes.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)