India Residential Construction Market Size, Share, Trends and Forecast by Project Size, Building Type, Construction, and Region, 2026-2034

India Residential Construction Market Summary:

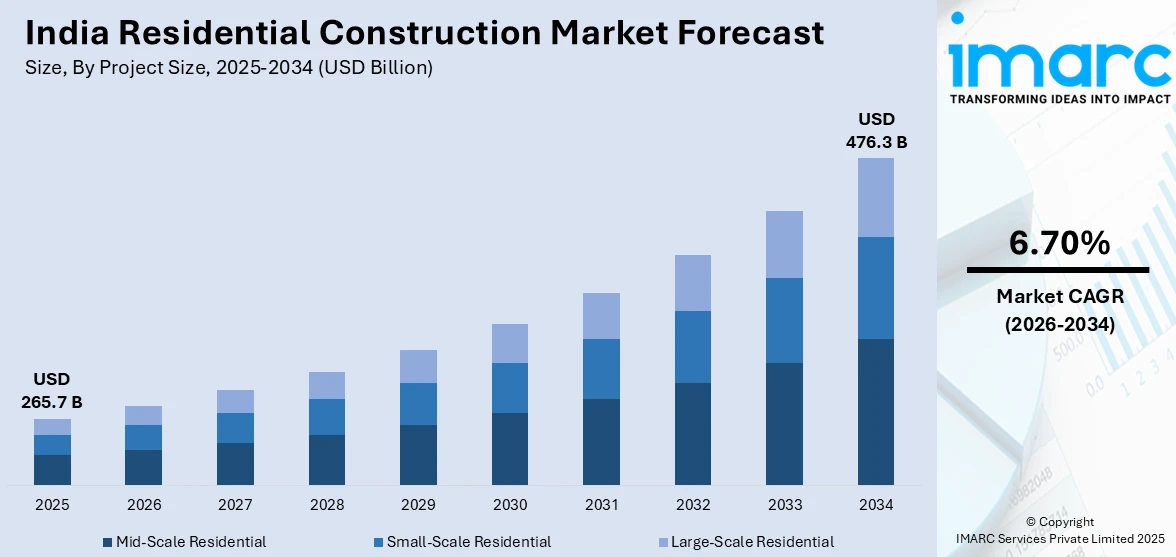

The India residential construction market size was valued at USD 265.7 Billion in 2025 and is projected to reach USD 476.3 Billion by 2034, growing at a compound annual growth rate of 6.70% from 2026-2034.

India's residential construction sector is experiencing robust expansion driven by rapid urbanization, rising disposable incomes, and favorable government housing initiatives. The market demonstrates strong momentum across metropolitan regions and tier-two cities, supported by infrastructure development and evolving consumer preferences for modern living spaces. Sustainable building practices and technological adoption are reshaping construction methodologies, while demographic shifts and nuclear family trends continue fueling housing demand nationwide.

Key Takeaways and Insights:

- By Project Size: Mid-scale residential dominates the market with a share of 41.8% in 2025, owing to its alignment with middle-class affordability thresholds and increasing demand from first-time homebuyers. Government subsidies under housing schemes and competitive mortgage rates drive sustained expansion.

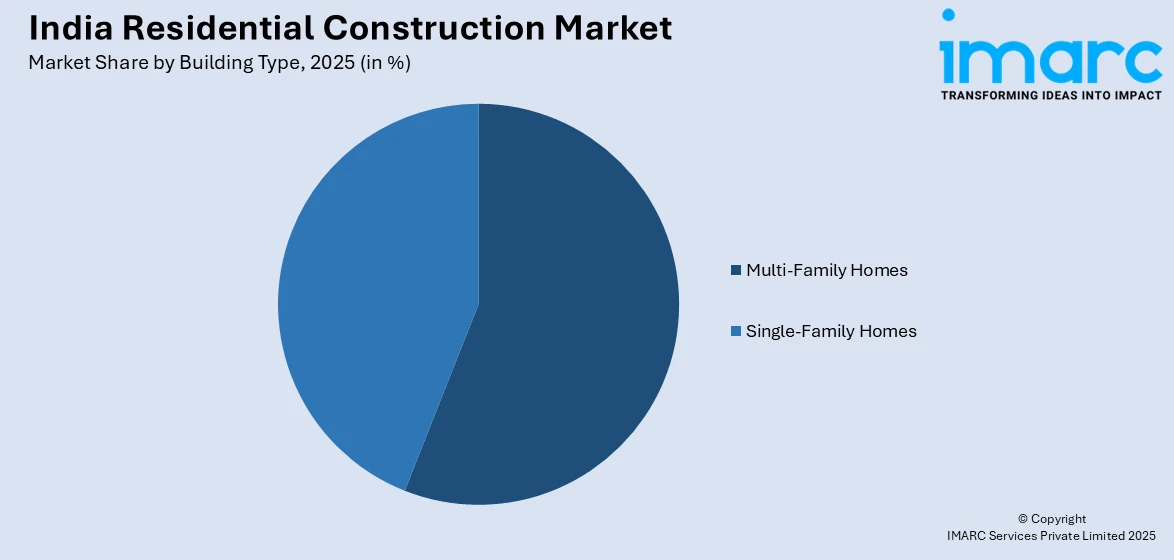

- By Building Type: Multi-family homes lead the market with a share of 53.6% in 2025. This dominance is driven by urbanization patterns, land scarcity in metropolitan areas, and preference for apartment living with shared amenities among working professionals and nuclear families.

- By Construction: Conventional construction exhibits a clear dominance in the market with 58.9% share in 2025, reflecting established contractor networks, abundant labor availability, and familiarity among developers with traditional building techniques across diverse regional markets.

- By Region: West India is the largest region with 32.4% share in 2025, driven by the concentration of financial services in Mumbai Metropolitan Region, industrial corridors in Gujarat, and robust real estate activity across Maharashtra and Goa.

- Key Players: Leading developers drive the India residential construction market by expanding project portfolios, investing in sustainable technologies, and strengthening distribution networks. Their focus on smart home integration, green building certifications, and strategic land acquisitions enables consistent project delivery across premium and affordable segments nationwide.

To get more information on this market Request Sample

India's residential construction market is propelled by comprehensive government initiatives and accelerating urban migration patterns. The Pradhan Mantri Awas Yojana Urban 2.0 program, targeting the construction of one crore homes with central assistance of INR 2.50 Lakh Crore over five years, demonstrates the government's commitment to addressing housing shortages. Rapid urbanization continues reshaping India's demographic landscape, with approximately thirty people migrating from rural areas to cities every minute, creating sustained demand for residential accommodation across metropolitan regions. The market benefits from favorable financing conditions, with digital mortgage platforms compressing loan approval timelines and improving housing affordability for first-time buyers. Non-Resident Indian investments contribute significantly to luxury segment resilience, while tier-two and tier-three cities emerge as growth frontiers following infrastructure improvements. Developer strategies increasingly incorporate smart home technologies, energy-efficient designs, and modular construction methodologies to address skilled labor constraints and accelerate project completion timelines. Rising household incomes, nuclear family proliferation, and evolving lifestyle preferences toward modern amenities underpin the residential construction market share expansion across diverse price segments.

India Residential Construction Market Trends:

Smart Home Technology Integration Reshaping Residential Development

The integration of Internet of Things devices and artificial intelligence systems is fundamentally transforming residential construction across India. Developers increasingly incorporate pre-installed smart automation systems, including automated lighting, climate control, and security features, during the construction phase rather than as aftermarket additions. Urban apartments lead adoption due to bulk procurement advantages and centralized building management capabilities. Voice-controlled devices and smart speakers are gaining significant traction among homeowners, while energy management systems enable optimized consumption patterns. Premium residential projects position comprehensive home automation as distinguishing features, attracting technology-conscious buyers seeking connected living experiences with enhanced convenience and operational efficiency.

Sustainable Construction Practices Gaining Market Momentum

Green building certification programs are experiencing accelerated adoption throughout India's residential construction sector. The Indian Green Building Council has facilitated a paradigm shift in design and construction methodologies, with certified projects demonstrating substantial reductions in energy consumption and water usage compared to conventional structures. Developers increasingly utilize eco-friendly materials, rainwater harvesting systems, and renewable energy installations including rooftop solar panels. Environmental consciousness among homebuyers is driving preference for certified green residences that offer reduced operational costs and healthier indoor environments. Government incentives including tax rebates and expedited approvals encourage developers to pursue sustainability certifications across project portfolios.

Tier-Two and Tier-Three Cities Emerging as Growth Corridors

Residential construction activity is expanding beyond traditional metropolitan centers into emerging urban clusters. Infrastructure improvements including expressways, metro rail networks, and improved telecommunications connectivity are transforming secondary cities into attractive residential destinations. Affordable land availability compared to saturated tier-one markets enables developers to offer competitively priced housing while maintaining attractive margins. The hybrid work model proliferation following recent workplace transformations allows professionals to relocate from expensive metropolitan areas while maintaining employment. Industrial corridors and special economic zone development generate employment opportunities driving localized housing demand, while improved social infrastructure including healthcare facilities and educational institutions enhance livability perceptions.

Market Outlook 2026-2034:

The India residential construction market outlook remains optimistic, supported by sustained urbanization, favorable demographics, and continued government investment in housing infrastructure. Strengthening buyer activity, quality supply inflow from established developers in prime locations, and growth of peripheral micro-markets are expected to diversify the residential sector landscape. The market generated a revenue of USD 265.7 Billion in 2025 and is projected to reach a revenue of USD 476.3 Billion by 2034, growing at a compound annual growth rate of 6.70% from 2026-2034. Increased institutional investments, rising demand for technology-enabled modern homes, and expanding housing finance accessibility are expected to define supply and demand momentum throughout the forecast period. Developers are increasingly focusing on sustainable construction practices and integrated township development to meet evolving consumer expectations.

India Residential Construction Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Project Size |

Mid-Scale Residential |

41.8% |

|

Building Type |

Multi-Family Homes |

53.6% |

|

Construction |

Conventional Construction |

58.9% |

|

Region |

West India |

32.4% |

Project Size Insights:

- Small-Scale Residential

- Mid-Scale Residential

- Large-Scale Residential

Mid-scale residential dominates with a market share of 41.8% of the total India residential construction market in 2025.

Mid-scale residential projects align optimally with India's expanding middle-class affordability thresholds and housing finance accessibility parameters. These developments balance construction economics with consumer purchasing power, enabling developers to achieve volume efficiencies while maintaining attractive price points. The segment benefits substantially from government housing subsidies and mortgage interest rate reductions targeting first-time homebuyers. Central bank monetary policy adjustments enhancing borrowing affordability have stimulated mid-segment housing demand across metropolitan and tier-two markets throughout the country, supporting sustained construction activity in this category.

Developer strategies increasingly focus on mid-scale residential projects due to favorable risk-return profiles and consistent absorption rates. These developments typically feature standardized floor plans enabling construction cost optimization while incorporating modern amenities demanded by contemporary homebuyers. Suburban locations along metro corridors and expressway networks provide land cost advantages supporting competitive pricing structures. Information technology hubs and emerging employment centers demonstrate particular mid-scale segment strength, reflecting sustained demand from salaried professionals seeking quality housing within accessible price ranges that align with available financing options and household budget constraints.

Building Type Insights:

Access the comprehensive market breakdown Request Sample

- Single-Family Homes

- Multi-Family Homes

Multi-family homes lead with a share of 53.6% of the total India residential construction market in 2025.

Multi-family residential developments dominate India's construction landscape due to urbanization dynamics, land scarcity in metropolitan centers, and evolving lifestyle preferences among working professionals and nuclear families. Apartment complexes offer shared amenity advantages including security, recreational facilities, and maintenance services that individual homes cannot efficiently provide. High-rise construction maximizes land utilization in premium urban locations where property values justify vertical development investments. India's residential property market recorded growth of eleven percent in 2024, with total sales reaching 2.03 Lakh Units, the highest annual sales volume in sector history according to industry research.

Developer focus on multi-family housing reflects superior construction economics and consumer financing accessibility through housing loan programs. Gated communities incorporating integrated amenities including gymnasiums, swimming pools, and community spaces attract premium pricing while ensuring steady absorption from quality-conscious buyers. The segment demonstrates resilience across market cycles due to broad demographic appeal spanning young professionals, growing families, and downsizing retirees seeking maintenance-free living arrangements. Multi-family apartments comprise the predominant share of residential transactions across diverse price segments, driven by urbanization patterns and evolving lifestyle preferences favoring shared amenity access and professional property management services.

Construction Insights:

- Conventional Construction

- Modular Construction

- Prefabricated Construction

- Green Building Construction

Conventional construction exhibits a clear dominance with 58.9% share of the total India residential construction market in 2025.

Conventional on-site construction methods maintain market leadership through established contractor networks, abundant labor availability, and widespread familiarity among developers and homebuyers with traditional building techniques. Cast-in-place concrete and brick masonry construction benefit from mature supply chains ensuring material availability across diverse regional markets. Skilled tradespeople including masons, carpenters, and electricians demonstrate proficiency with conventional methodologies accumulated through generations of practice. Training ecosystems and apprenticeship traditions ensure knowledge transfer supporting workforce continuity across construction trades.

Conventional construction accommodates customization flexibility valued by residential buyers seeking personalized design elements and layout modifications during construction phases. Site-specific adaptation capabilities address varying soil conditions, local building codes, and regional architectural preferences across India's geographically diverse markets. Cost competitiveness relative to modern construction methods remains compelling, particularly for projects where material procurement benefits from local sourcing advantages. Developer familiarity with conventional project management workflows reduces execution risks compared to adopting alternative construction technologies requiring specialized equipment and training investments. Quality control processes refined through decades of implementation ensure consistent construction outcomes meeting regulatory compliance standards and buyer expectations across residential project categories.

Regional Insights:

- North India

- South India

- East India

- West India

West India represents the leading segment with 32.4% share of the total India residential construction market in 2025.

West India's residential construction leadership reflects Mumbai Metropolitan Region's position as India's financial capital, attracting sustained housing demand from professionals employed across banking, financial services, and entertainment industries. Maharashtra's progressive real estate policies and infrastructure investments support development activity, while Gujarat's industrial growth creates employment-driven housing requirements in emerging urban centers. The region benefits from established developer ecosystems, mature financing infrastructure, and robust regulatory frameworks that enhance buyer confidence and project execution certainty.

Redevelopment projects in established Mumbai neighborhoods create new housing inventory in land-constrained premium locations, commanding significant price premiums from buyers seeking central accessibility. Coastal Road completion and metro expansion enhance connectivity to suburban growth corridors including Thane and Navi Mumbai, extending residential development potential beyond traditional boundaries. Pune emerges as a significant residential market within the region, with technology sector employment driving housing demand across diverse price segments from affordable to premium categories. Gujarat's connectivity improvements and industrial corridor development attract residential construction investment in cities experiencing rapid economic transformation and population growth driven by manufacturing sector expansion.

Market Dynamics:

Growth Drivers:

Why is the India Residential Construction Market Growing?

Comprehensive Government Housing Initiatives Stimulating Market Expansion

Government commitment to addressing housing deficits through targeted programs provides substantial impetus for residential construction growth across India. The Pradhan Mantri Awas Yojana represents the cornerstone of national housing policy, providing direct subsidies, credit-linked interest subvention, and infrastructure support enabling affordable housing delivery to economically disadvantaged populations. Program implementation encompasses urban and rural components targeting comprehensive housing accessibility improvements throughout diverse demographic segments. Policy continuity and budgetary allocation increases demonstrate sustained governmental prioritization of housing sector development as fundamental to broader socioeconomic advancement objectives. Recent central allocations for housing programs represent substantial increases from prior years, expanding construction targets significantly beyond previous implementation phases. Additionally, the SWAMIH Fund focused on completing stalled residential projects unlocks developer cash flows and encourages construction restarts, addressing inventory overhangs that previously constrained market growth and buyer confidence in project completion timelines.

Accelerating Urbanization Creating Sustained Housing Demand

India's urbanization trajectory generates continuous residential construction requirements as populations migrate from rural areas seeking employment opportunities, educational access, and improved lifestyle standards in metropolitan centers. Urban population concentration creates density pressures requiring vertical development solutions maximizing land utilization efficiency in established city cores while simultaneously driving horizontal expansion into suburban growth corridors. Infrastructure improvements including metro networks, expressways, and industrial corridors enhance peripheral area accessibility, transforming previously undeveloped zones into viable residential destinations. Migration patterns demonstrate concentration toward employment hubs spanning information technology, manufacturing, and services sectors distributed across multiple metropolitan regions. India's urban population continues expanding rapidly, generating immense housing requirements as demographic projections indicate substantial growth in coming decades. Continuous rural-to-urban migration creates sustained demand for residential accommodation across metropolitan regions and emerging tier-two urban centers benefiting from connectivity improvements and economic development initiatives transforming regional employment landscapes.

Rising Household Incomes and Expanding Middle Class Population

Economic growth translates into household income improvements enabling greater residential property purchasing capacity across India's expanding middle class demographic. Rising affluence shifts housing preferences toward larger units incorporating modern amenities previously considered luxury features, driving construction activity across premium market segments. Nuclear family proliferation replaces traditional joint family living arrangements, multiplying residential unit requirements independent of population growth rates. Employment formalization improves mortgage eligibility among salaried professionals, expanding the qualified homebuyer pool accessible to developers across diverse price segments. Digital mortgage platforms compress loan approval timelines while reducing documentation burdens, improving financing accessibility particularly for first-time purchasers navigating complex home loan procedures. The housing market demonstrates sustained demand across price categories, with premium properties experiencing significant year-over-year sales increases reflecting higher purchasing power among Indian homebuyers willing to invest in quality residential properties offering superior specifications and amenities catering to aspirational lifestyle preferences.

Market Restraints:

What Challenges the India Residential Construction Market is Facing?

Skilled Labor Shortage Constraining Construction Capacity

The construction sector faces acute shortages of skilled tradespeople including carpenters, masons, plumbers, and electricians essential for quality residential project execution. Insufficient vocational training infrastructure fails to produce adequate qualified workforce replacement for aging construction professionals approaching retirement. Inadequate compensation and working condition perceptions discourage younger generations from pursuing construction careers, perpetuating skilled labor supply constraints. Migration pattern disruptions following pandemic-related workforce displacement continue affecting labor availability in major construction markets.

Raw Material Price Volatility Impacting Project Economics

Construction material costs demonstrate significant volatility affecting project profitability and pricing strategies across residential developments. Steel and cement prices fluctuate with global commodity market movements, energy cost variations, and supply chain disruptions beyond developer control. Long-gestation residential projects remain vulnerable to unexpected material cost escalations occurring between project launch and completion phases. Cost-escalation clauses provide partial protection but may affect buyer affordability perceptions and sales momentum, creating challenging trade-offs between margin protection and market competitiveness.

Regulatory Complexity and Approval Delays Affecting Timelines

Multiple regulatory approvals required across municipal, state, and environmental authorities create extended project gestation periods affecting construction timelines and investment returns. Bureaucratic delays in obtaining construction permits, environmental clearances, and occupancy certificates add uncertainty to development schedules. Regulatory changes during project execution necessitate design modifications and re-approval processes adding costs and timeline extensions. Despite Real Estate Regulatory Authority implementation improving transparency, administrative processing capacities remain constrained in high-activity markets experiencing substantial approval backlogs.

Competitive Landscape:

The India residential construction market exhibits a competitive structure combining national developers with regional specialists serving localized consumer preferences. Market consolidation trends favor established players possessing financial strength, land banking capabilities, and brand recognition enabling premium pricing power. Competitive differentiation strategies emphasize sustainable construction practices, smart home technology integration, and amenity-rich community development addressing evolving buyer expectations. Strategic land acquisitions in high-potential growth corridors position leading developers for medium-term project launches while creating entry barriers for capital-constrained competitors. Joint venture arrangements between developers and landowners enable risk-sharing models supporting expansion into new geographic markets while optimizing capital deployment efficiency. Real Estate Regulatory Authority compliance requirements favor organized sector participants demonstrating financial stability and project execution track records over informal builders lacking regulatory adherence capabilities.

Recent Developments:

- In January 2025, Godrej Properties secured a twenty-four acre land parcel in Indore for premium plotted residential development comprising approximately 6.2 Lakh square feet of saleable area. This acquisition reflects the developer's strategic expansion into tier-two cities demonstrating strong housing demand growth potential.

India Residential Construction Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Project Sizes Covered |

Small-Scale Residential, Mid-Scale Residential, Large-Scale Residential |

|

Building Types Covered |

Single-Family Homes, Multi-Family Homes |

|

Constructions Covered |

Conventional Construction, Modular Construction, Prefabricated Construction, Green Building Construction |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Residential Construction Market Report

The India residential construction market size was valued at USD 265.7 Billion in 2025.

The India residential construction market is expected to grow at a compound annual growth rate of 6.70% from 2026-2034 to reach USD 476.3 Billion by 2034.

Mid-scale residential dominated the market with a share of 41.8%, driven by alignment with middle-class affordability and strong demand from first-time homebuyers benefiting from government housing subsidies.

Key factors driving the India residential construction market include government housing initiatives, accelerating urbanization, rising household incomes, expanding middle-class population, and favorable housing finance accessibility.

Major challenges include skilled labor shortages affecting construction capacity, raw material price volatility impacting project economics, regulatory complexity causing approval delays, land cost escalation in metropolitan areas, and infrastructure gaps in emerging growth corridors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)