India Reusable Water Bottle Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Region, 2026-2034

India Reusable Water Bottle Market Size, Share, Trends & Forecast (2026-2034)

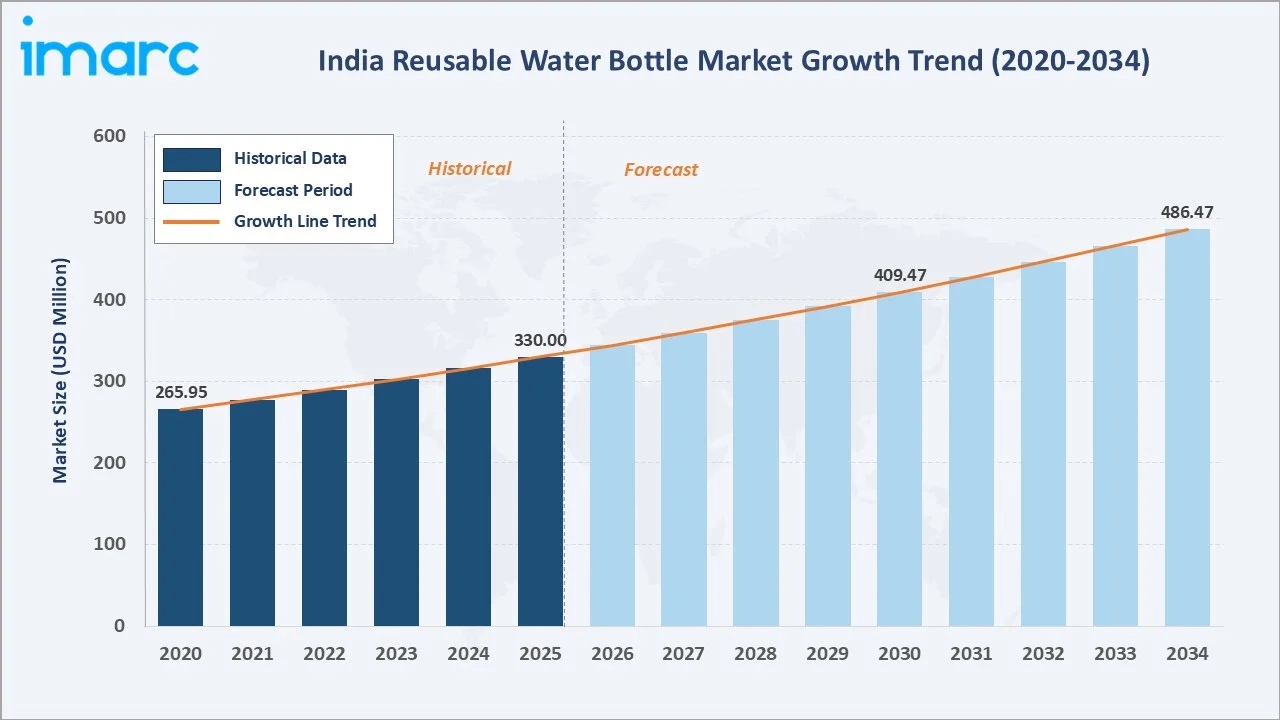

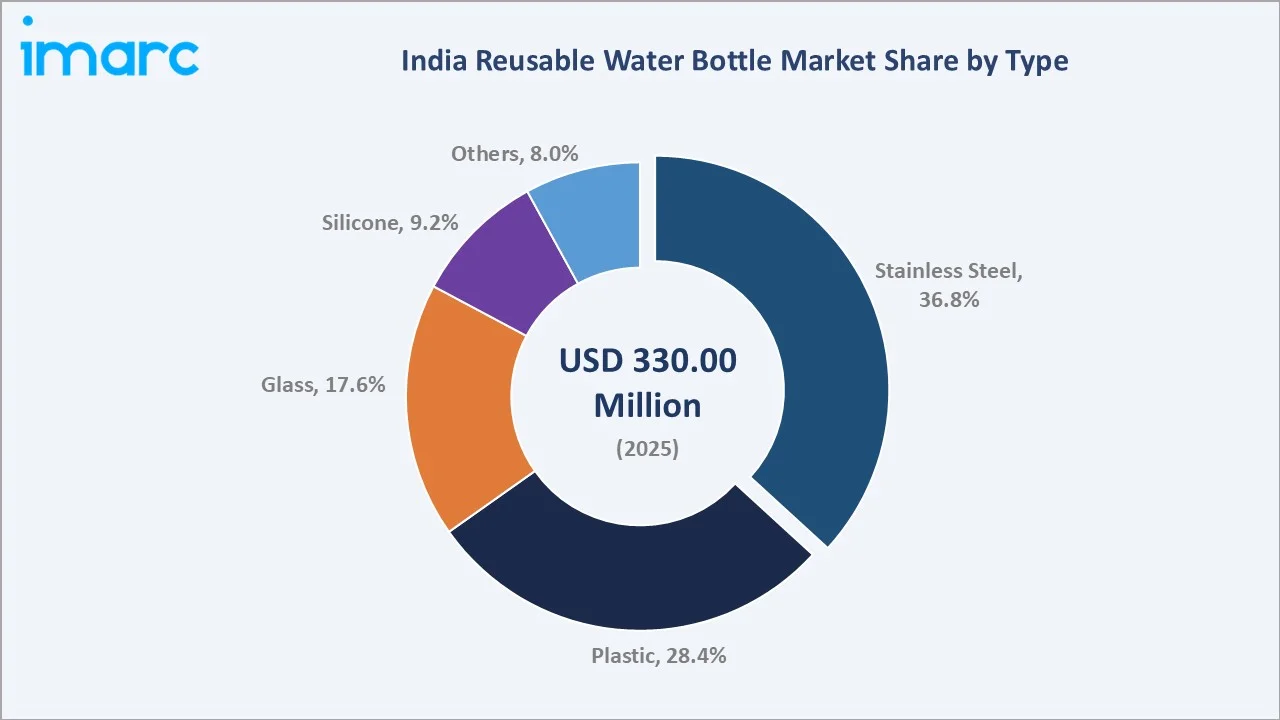

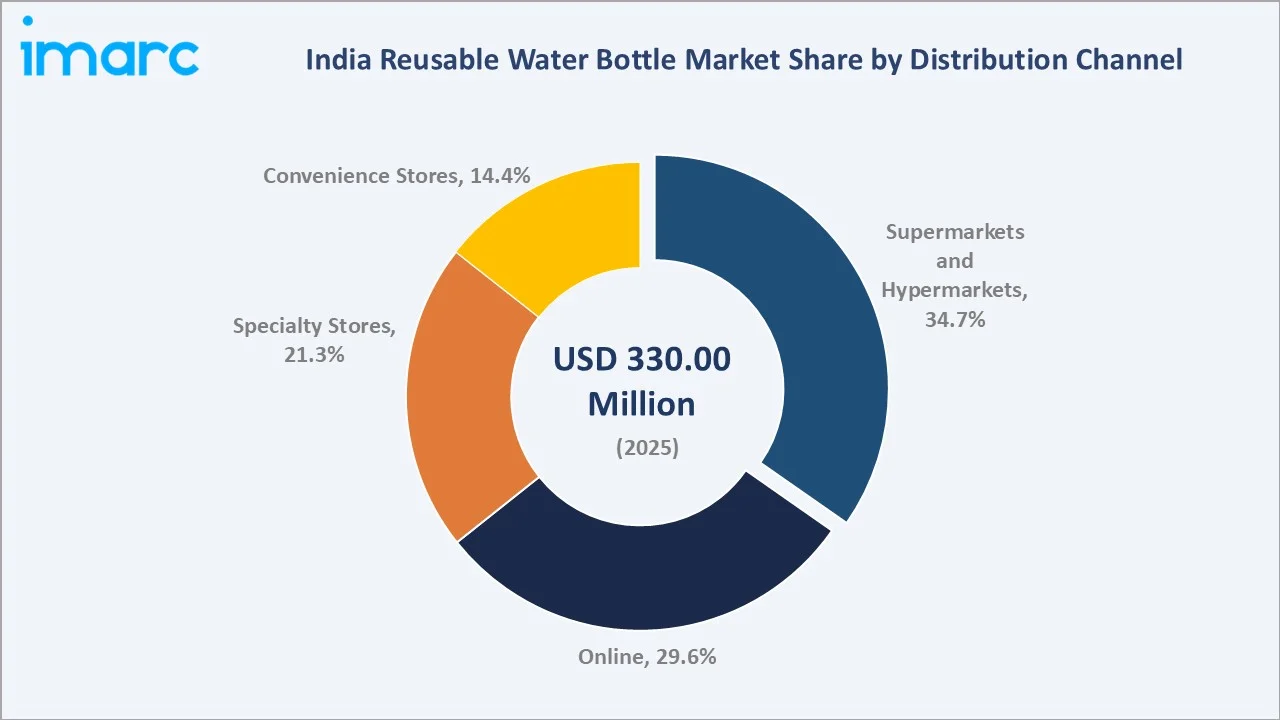

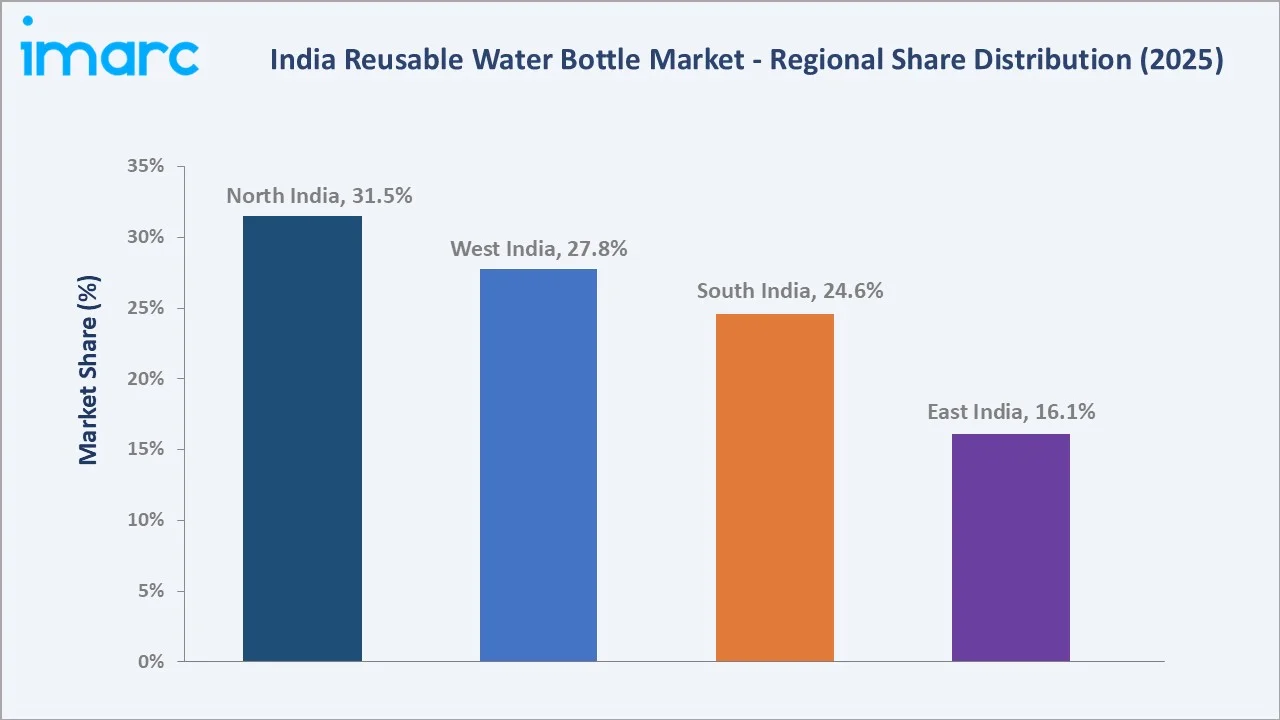

The India reusable water bottle market reached USD 330.00 Million in 2025 and is projected to reach USD 486.47 Million by 2034, growing at a CAGR of 4.41% during 2026-2034. The market is driven by rising health awareness, 43% of India’s total plastic waste still consisting of single-use plastics despite regulatory bans, expanding fitness and outdoor lifestyles, and increasing demand for durable, eco-friendly hydration products. Stainless steel leads at 36.8% type share. Supermarkets and hypermarkets lead the distribution channel at 34.7%. North India commands 31.5% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 330.00 Million |

|

Forecast Market Size (2034) |

USD 486.47 Million |

|

CAGR (2026-2034) |

4.41% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Stainless Steel (36.8%, 2025) |

|

Dominant Distribution Channel |

Supermarkets & Hypermarkets (34.7%, 2025) |

|

Leading Region |

North India (31.5%, 2025) |

The market expanded from USD 265.95 Million in 2020 to USD 330.00 Million in 2025, anchored at USD 409.47 Million in 2030, and forecast to reach USD 486.47 Million by 2034. COVID-19's hygiene awareness surge permanently elevated personal water bottle adoption. Consumers who previously shared water containers or relied on disposable bottles shifted to personal reusable bottles for COVID-related hygiene safety, establishing behavioral patterns that sustained reusable bottle demand beyond the pandemic and creating a permanent baseline expansion of the addressable market across all bottle types.

To get more information on this market, Request Sample

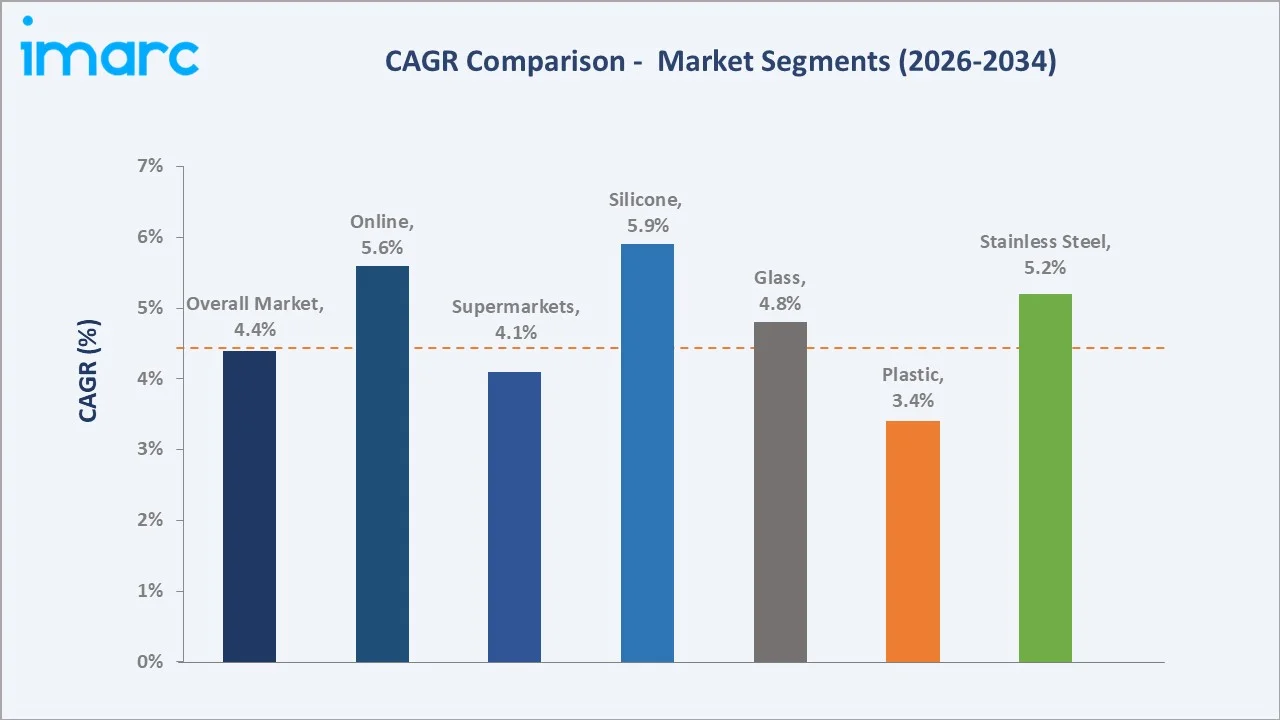

Silicone bottles grow fastest at ~5.9% CAGR (2026-2034), driven by BPA-free health positioning, collapsible/foldable travel format innovation, and premium yoga and fitness community adoption. Online distribution channel grows at ~5.6% CAGR as Amazon India and Flipkart's D2C brand marketplace, premium product discovery, and customer review-driven purchase decisions make e-commerce the primary channel for premium stainless steel and glass bottle purchases.

Executive Summary

The India reusable water bottle market reached USD 330.00 Million in 2025, driven by a powerful convergence of regulatory, health, environmental, and economic forces creating the strongest structural growth conditions in the market's history. The market is projected to reach USD 486.47 Million by 2034 at 4.41% CAGR.

Stainless steel at 36.8% leads as India's premium bottle category, driven by insulation performance, BPA-free safety credentials, durability for product lifespans, and aspirational premium branding. Supermarkets and hypermarkets at 34.7% reflect D-Mart, Big Bazaar, and Reliance Smart's broad reach across urban and semi-urban India. North India at 31.5% leads through Delhi NCR's premium consumer base and strong distribution networks.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Stainless Steel - 36.8% share (2025) |

|

Dominant Distribution Channel |

Supermarkets & Hypermarkets - 34.7% market share (2025) |

|

Leading Region |

North India - 31.5% market share (2025) |

Key Analytical Observations Supporting The Above Data:

- Stainless steel at 36.8% anchored by insulation performance and BPA-free safety positioning as an aspirational purchase: India's brutal summer climate creates critical functional demand for vacuum-insulated stainless steel bottles, maintaining cold water temperature.

- Supermarkets and hypermarkets at 34.7% through D-Mart's nationwide reach and impulse purchase dynamics: D-Mart stores across India create the largest single-chain reusable bottle retail platform. Impulse purchase dynamics at supermarket billing queues, seasonal promotion endcaps during summer months, and family pack purchases drive supermarket channel volumes above premium-seeking individual purchase behavior.

- North India at 31.5% through Delhi NCR's premium consumption and North India's heat-driven insulated bottle demand: Delhi metropolitan population with India's highest urban disposable income creates the country's largest premium bottle addressable market.

India Reusable Water Bottle Market Overview

India's reusable water bottle market encompasses all non-disposable water carrying vessels, including stainless steel insulated bottles, BPA-free plastic bottles, borosilicate glass bottles, food-grade silicone collapsible bottles, and hybrid formats combining materials. Products range from affordable plastic school bottles to premium imported stainless steel thermal bottles, serving school children, office workers, fitness enthusiasts, trekkers, and corporate gifting buyers across India.

The ecosystem integrates stainless steel suppliers, food-grade resin manufacturers, glass specialists, bottle manufacturers, BIS certification laboratories, national distributors, modern trade retailers, online marketplaces, specialty retailers, and end consumers across age groups and income segments. Macroeconomic factors include rising disposable incomes, rapid urbanization, expanding middle-class consumption, and growing spending on health, wellness, travel, and fitness products.

Market Dynamics

To evaluate market opportunities, Request Sample

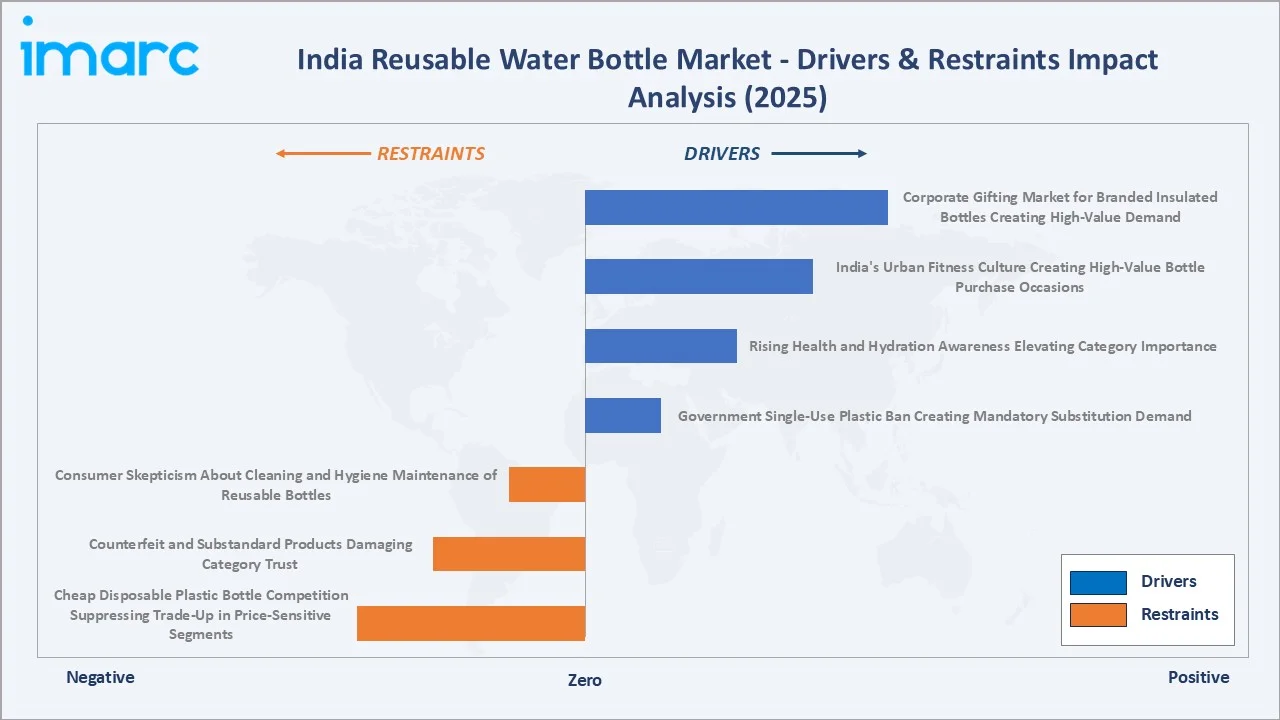

Market Drivers

- Government Single-Use Plastic Ban Creating Mandatory Substitution Demand: India banned the manufacture, import, stocking, distribution, sale and use of identified single-use plastic items, which have low utility and high littering potential, across the country from July 1, 2022, and this created structural demand for reusable alternatives across India.

- Rising Health and Hydration Awareness Elevating Category Importance: India's growing health consciousness, driven by COVID-19 health awareness, fitness app adoption, and social media wellness influencers, is elevating hydration from an unconscious daily activity to a tracked health behavior.

- India's Urban Fitness Culture Creating High-Value Bottle Purchase Occasions: As of 2024, there are approximately 46,500 fitness facilities in India, encompassing gyms, studios, and wellness centers across both urban and semi-urban regions. Each gym member represents a high-value potential bottle consumer. Gym-goers require dedicated workout bottles separate from daily use bottles, upgrading more frequently, and are willing to pay for premium insulated stainless steel or sports silicone bottles.

Market Restraints

- Cheap Disposable Plastic Water Bottle Competition Suppressing Trade-Up in Price-Sensitive Segments: India's branded 1-litre PET water bottle represents the direct competitive substitute for reusable bottles in the INR 0-200 price segment. This price sensitivity maintains disposable bottle market share and limits reusable bottle market penetration to India's urban and semi-urban population segments with sufficient disposable income for the initial purchase.

- Counterfeit and Substandard Products Damaging Category Trust: India's informal sector produces substantial volumes of counterfeit stainless steel and glass bottles; products sold as food-grade stainless steel that test positive for nickel and chromium leaching beyond FSSAI permissible limits or claimed borosilicate glass bottles that are lower-grade soda-lime glass lacking thermal shock resistance. These substandard products enter the market through local kirana stores, weekly markets, and online marketplace third-party sellers, typically priced 40-60% below genuine products.

Market Opportunities

- Corporate Gifting Market for Branded Insulated Bottles Creating High-Value Demand Segment: India's corporate gifting market has adopted branded stainless steel insulated bottles as one of the most preferred gifting items for festival seasons, employee onboarding kits, and client appreciation gifts.

- School Bottle Mandate Expansion and Institutional Procurement Creating Volume Market: State governments' school health initiatives requiring students to carry personal reusable water bottles are creating institutional procurement of reusable bottles at competitive prices for school students.

Market Challenges

- Consumer Skepticism About Cleaning and Hygiene Maintenance of Reusable Bottles: One of the most significant behavioral barriers to India's reusable bottle adoption is consumer perception that reusable bottles are difficult to clean thoroughly and may harbor bacteria, particularly relevant in India's hot climate, where mold growth inside bottle caps and narrow-mouth designs occurs rapidly without proper cleaning. Bottles with complex lids accumulate residue in difficult-to-reach areas that standard brushing cannot clean.

- Fragmented Organized-to-Unorganized Market Structure Creating Price Discovery Challenges: India's reusable bottle market operates across an enormous price spectrum. This fragmentation makes category-level brand building difficult, as consumer price anchors vary by 50x between the least expensive and most premium products. The lack of standardized product quality communication makes quality differentiation difficult for consumers selecting stainless steel bottles that appear visually similar but differ substantially in steel grade, insulation technology, and manufacturing standards.

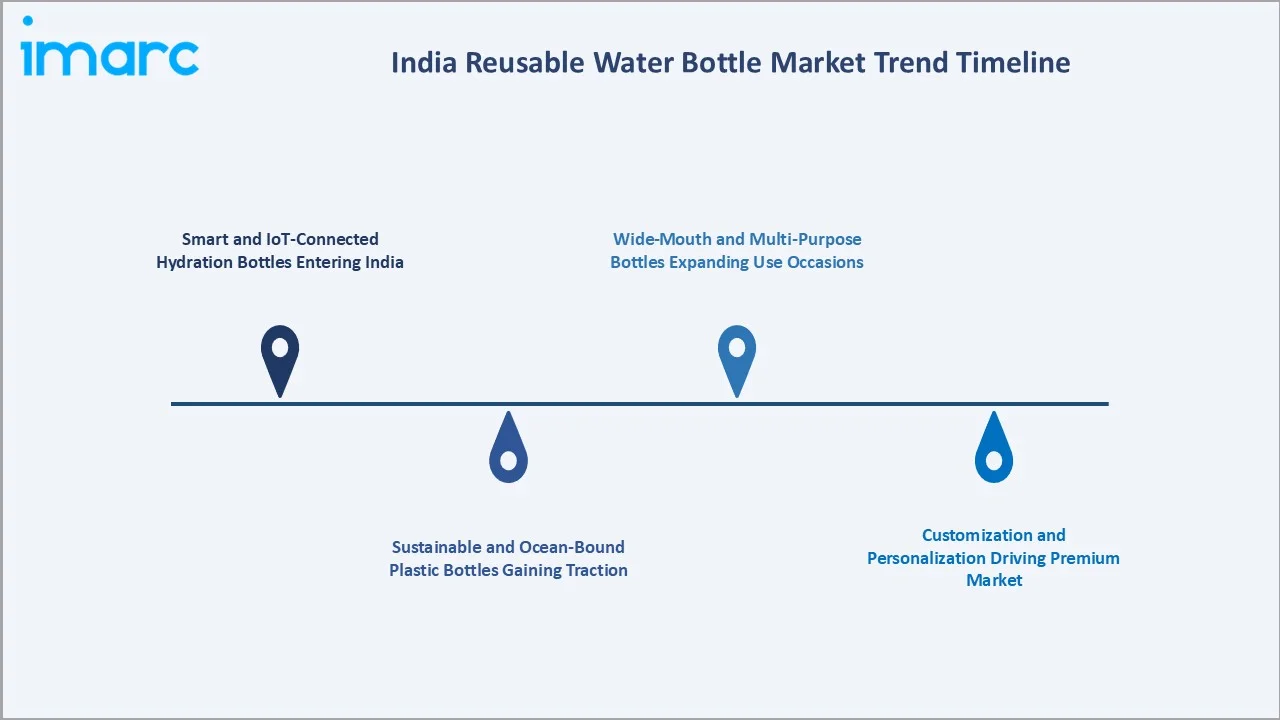

Emerging Market Trends

1. Smart and IoT-Connected Hydration Bottles Entering India

Smart and IoT-connected hydration bottles are emerging in India as consumers increasingly seek personalized wellness, fitness tracking, hydration reminders, and app-linked lifestyle products. In March 2025, Adivaa Smart Powering Solutions Pvt. Ltd. launched its state-of-the-art hydrogen water bottles. Adivaa’s advanced hydrogen water solution enriches drinking water with molecular hydrogen, reaching concentrations of up to 6,000 ppb within minutes, among the highest levels offered in India. The technology is designed to support cellular hydration, enhance antioxidant benefits, and help neutralize free radicals, positioning it as a wellness-focused alternative to regular drinking water.

2. Sustainable and Ocean-Bound Plastic Bottles Gaining Traction

Sustainable and ocean-bound plastic bottles are gaining traction in India as consumers and brands increasingly focus on reducing single-use plastic waste and supporting circular economy practices. This trend is encouraging manufacturers to use recycled, reusable, BPA-free, stainless-steel, and responsibly sourced materials, creating stronger demand for eco-friendly water bottle options among urban and sustainability-conscious consumers.

3. Customization and Personalization Driving Premium Market

Customization and personalization are driving the premium segment as consumers seek products that reflect lifestyle, identity, gifting preferences, and workplace or fitness branding. Brands are offering engraved names, colors, prints, logos, temperature-control features, and limited-edition designs, helping reusable bottles move from basic utility products to premium lifestyle accessories.

4. Wide-Mouth and Multi-Purpose Bottles Expanding Use Occasions

Wide-mouth and multi-purpose bottles are expanding use occasions in India as consumers prefer bottles that are easy to clean, refill, and use for water, infused drinks, protein shakes, juices, and travel hydration. Their convenience, leak-proof designs, durability, and compatibility with ice cubes or fruit add-ons are making them popular across gyms, offices, schools, outdoor activities, and daily commuting.

Industry Value Chain Analysis

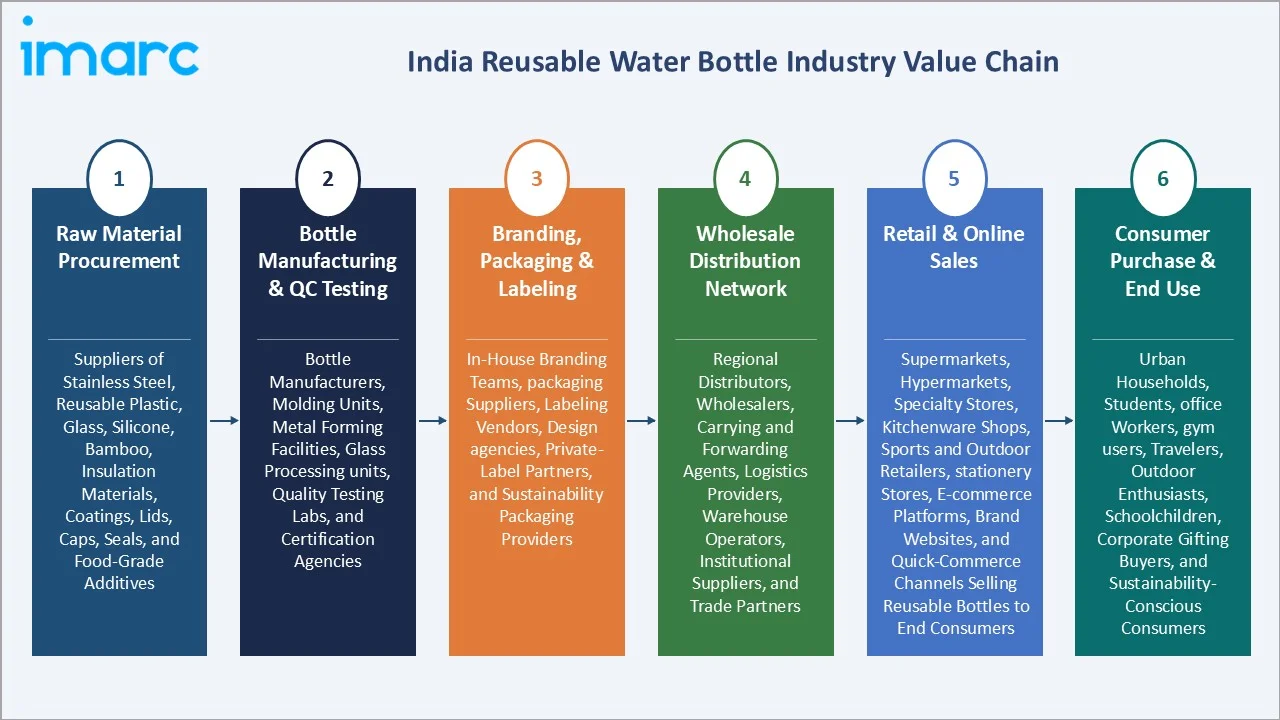

India's reusable water bottle value chain integrates raw material procurement through manufacturing, branding, wholesale distribution, and retail/online sales to end consumers. Manufacturer gross margins range from 20-35% for branded domestic manufacturers to 8-15% for unbranded OEM producers. Distributors earn 8-12% margins; modern trade retailers earn 18-25% margins; online marketplaces charge 15-25% platform fees. Premium D2C brands capturing direct-to-consumer sales bypass distributor and retailer layers to capture 40-55% gross margins, explaining the commercial viability of the D2C model despite lower volumes.

|

Stage |

Key Participants |

|

Raw Material Procurement |

Suppliers of stainless steel, reusable plastic, glass, silicone, bamboo, insulation materials, coatings, lids, caps, seals, and food-grade additives. |

|

Bottle Manufacturing & QC Testing |

Bottle manufacturers, molding units, metal forming facilities, glass processing units, quality testing labs, and certification agencies. |

|

Branding, Packaging & Labeling |

In-house branding teams, packaging suppliers, labeling vendors, design agencies, private-label partners, and sustainability packaging providers. |

|

Wholesale Distribution Network |

Regional distributors, wholesalers, carrying and forwarding agents, logistics providers, warehouse operators, institutional suppliers, and trade partners. |

|

Retail & Online Sales |

Supermarkets, hypermarkets, specialty stores, kitchenware shops, sports and outdoor retailers, stationery stores, e-commerce platforms, brand websites, and quick-commerce channels selling reusable bottles to end consumers. |

|

Consumer Purchase & End Use |

Urban households, students, office workers, gym users, travelers, outdoor enthusiasts, schoolchildren, corporate gifting buyers, and sustainability-conscious consumers. |

The online sales tier is the most strategically contested competitive battleground. Brands investing INR 50-100 per unit in Amazon-sponsored advertising are building customer review portfolios that create self-reinforcing visibility advantages, while established brands like Milton leverage category leadership without proportional advertising investment through brand search-driven organic discovery.

Technology Landscape in the India Reusable Water Bottle Industry

Vacuum Insulation Technology Innovation

Innovations such as double-wall and tri-ply insulation, leak-proof construction, and durable stainless-steel designs are helping brands differentiate premium products and target office, travel, fitness, and outdoor-use consumers. In March 2023, Pexpo launched its sustainable stainless steel water bottle range, positioned as the only ISI-certified products in the category. The company highlighted its advanced manufacturing technology and automation, along with tri-ply vacuum insulation that uses three metal layers and vacuum insulation to retain hot and cold temperatures longer than conventional double-wall bottles.

Borosilicate Glass Production Technology

Borosilicate glass production technology enables lightweight, heat-resistant, odor-free, and chemically stable bottles suitable for daily hydration and hot or cold beverages. Its durability, clarity, and premium appearance help brands target health-conscious consumers seeking safe, reusable, BPA-free, and easy-to-clean alternatives to plastic bottles.

BPA-Free Plastic Compound Development

BPA-free plastic compound development enabling safer, lightweight, durable, and affordable alternatives to conventional plastic bottles. These materials support leak-proof, impact-resistant, colorful, and easy-to-carry bottle designs, helping brands target students, office users, travelers, and fitness consumers seeking safe reusable hydration products.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Stainless Steel | 36.8% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 34.7% | 2025 |

| Region | North India | 31.5% | 2025 |

By Type

Stainless steel leads at 36.8% market share (2025). This segment serves India's premium and functional hydration market through 18/8 food-grade stainless steel construction, vacuum insulation technology, and BPA-free safety positioning. Double-wall vacuum bottles dominate within stainless steel, with single-wall non-insulated stainless bottles serving cost-sensitive consumers seeking steel durability without insulation performance.

To access detailed market analysis, Request Sample

Plastic at 28.4% serves India's volume mass market across school bottles, household use, and office water bottles. BIS IS:10955 mandatory certification has eliminated the lowest-quality substandard plastic bottles from formal retail, improving segment quality. Glass at 17.6% grows at ~4.8% CAGR through Borosil's premium borosilicate range and generic glass bottles serving traditional South Indian kitchen culture. Silicone at 9.2% grows fastest at ~5.9% CAGR through fitness and travel segment premium adoption. Others at 8.0% includes copper bottles, bamboo bottles, and hybrid glass-steel designs.

By Distribution Channel

Supermarkets and hypermarkets lead at 34.7% market share (2025). D-Mart stores, Big Bazaar, and Reliance Smart create India's most comprehensive organized retail reusable bottle network, with seasonal end-cap promotions during summer, driving 60%+ of annual supermarket bottle volume in a concentrated 4-month window.

Online at 29.6% grows fastest at ~5.6% CAGR through Amazon India, Flipkart, Myntra, and emerging quick commerce channels. Specialty stores at 21.3% cover Decathlon India's sports stores, Hamleys India and toy stores (children's bottles), and standalone kitchenware stores in metro areas. Convenience stores at 14.4% include local kirana stores, petrol station forecourt retail, and railway/bus station stalls serving impulse and travel purchase occasions with mid-range plastic and steel bottles.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

North India |

31.5% |

Large urban population, rising disposable incomes, expanding school and office-going consumer base, and strong demand for stainless steel, insulated, and reusable plastic bottles support market growth across major cities and tier-II markets. |

|

West India |

27.8% |

Strong retail networks, industrial hubs, corporate gifting demand, fitness-oriented consumers, and premium lifestyle adoption drive sales of reusable water bottles through supermarkets, specialty stores, e-commerce, and institutional channels. |

|

South India |

24.6% |

High urbanization, strong IT and education ecosystems, growing sustainability awareness, and rising use of reusable bottles in offices, schools, colleges, gyms, and travel settings support demand for premium and durable hydration products. |

|

East India |

16.1% |

Expanding retail access, growing middle-class consumption, increasing awareness of plastic reduction, and demand from students, households, workers, and travelers support the gradual adoption of affordable reusable plastic, glass, and stainless-steel bottles. |

North India's 31.5% leadership reflects the confluence of India's highest per-capita income urban consumers, extreme summer climate creating acute insulated bottle functional demand, and the country's most developed wholesale distribution infrastructure. The NCR corporate gifting market additionally sustains premium stainless steel segment growth, with MNC headquarters cluster representing one of India's most concentrated corporate bottle gifting markets.

West India's 27.8% includes Gujarat's manufacturing concentration, providing proximity advantages for domestic distribution at lower logistics costs. Maharashtra's student population represents India's largest school bottle market. South India's 24.6% is growing fastest as Bengaluru's tech workforce and South Indian fitness culture adoption accelerate premium stainless steel and glass bottle purchases. East India's 16.1% remains the most price-sensitive region.

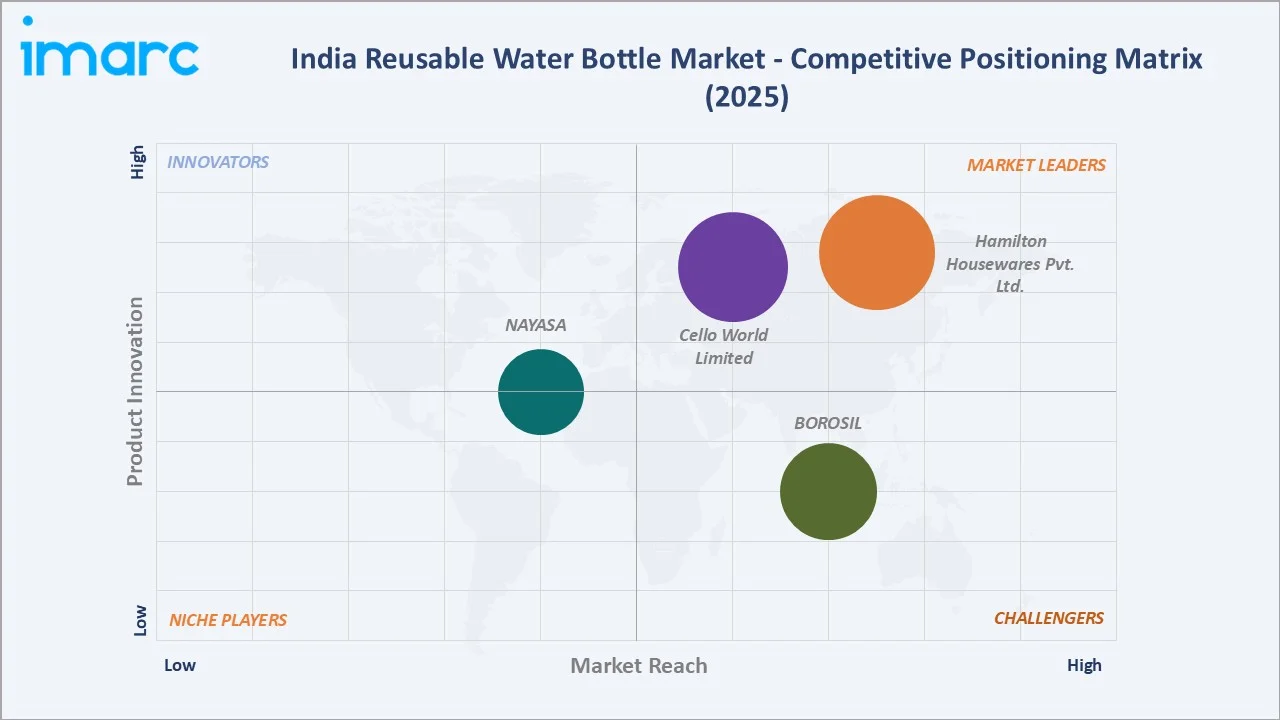

Competitive Landscape

India's reusable water bottle market is moderately concentrated at the brand level but highly fragmented at the manufacturer level. Milton and Cello brands together command approximately 35-40% of India's organized retail reusable bottle revenues. However, the market includes hundreds of unorganized local manufacturers supplying kirana stores, weekly markets, and e-commerce third-party sellers with unbranded bottles. These unorganized players collectively serve an estimated 40-50% of India's total volume units, particularly in the plastic segment.

|

Company Name |

Brand |

Market Position |

Core Strength |

|

Hamilton Housewares Pvt. Ltd. |

Milton |

Market Leader |

One of India's largest kitchenware brands with over 50 years of experience |

|

Cello World Limited |

Cello |

Market Leader |

With 13 manufacturing facilities across five strategic locations in India and Cello's expansive distribution network, comprising over 700 distributors and 50,000 retail touchpoints, ensures that Cello products are accessible to millions of customers across the country. |

|

BOROSIL |

BOROSIL |

Strong Challenger |

India's premium glass bottle leader, borosilicate glass technology |

|

Nayasa |

NAYASA |

Established Player |

NAYASA is a home and kitchenware company that grew out of the sheer determination of one man. |

The competitive landscape is undergoing significant disruption from three directions: D2C digital brands building premium businesses through Amazon and Instagram without traditional distribution investment; international premium brands establishing premium benchmark pricing that legitimizes Indian brand premium positioning; and quick commerce platforms compressing the purchase cycle to impulse, changing which brands and formats win consumer selection decisions.

Key Company Profiles

Hamilton Housewares Pvt. Ltd.

Hamilton Housewares Pvt. Ltd. is India's undisputed market leader in reusable water bottles, with 30 years of experience. With global presence in over 80 countries, Hamilton India provides best-in-class products to international markets.

- Brands: Milton

- Recent Developments: In January 2024, Milton partnered with cult.fit to introduce a line of colored bottles at cult.fit gyms. These bottles are available at key cult.fit locations in Mumbai, Delhi/NCR, and Bangalore.

- Strategic Focus: Expanding durable, affordable, and design-focused hydration products through strong retail, e-commerce, and mass consumer distribution channels.

Cello World Limited

Cello has built a strong manufacturing and distribution presence with 13 facilities across five key locations in India, supported by more than 700 distributors and 50,000 retail touchpoints. The company’s products reach millions of customers nationwide, while its international presence across over 65 countries reinforces its position as a recognized global brand.

- Brands: Cello

- Recent Developments: In February 2026, Cello World Limited’s board approved a ₹600 crore capital restructuring plan for its subsidiary CCPL, including the conversion of ₹500 crore in loans into equity and a fresh capital infusion of ₹100 crore. The funding supports manufacturing expansion, working capital needs, and general corporate requirements at the Falna facility.

- Strategic Focus: Expanding manufacturing capacity, strengthening mass retail and e-commerce distribution, and offering affordable, durable, and premium consumer ware hydration products.

Market Concentration Analysis

India reusable water bottle market is moderately concentrated, with the top 4 brands (Milton, Cello, Borosil, Nayasa) collectively commanding approximately 55-60% of organized retail revenues. The remaining 40-45% is served by regional brands, D2C digital brands, and imported premium brands. This concentration is significantly lower than comparable consumer goods categories, reflecting the reusable bottle category's lower brand loyalty and the ease of online discovery for new premium brands.

Market concentration is more pronounced at the type level. Borosil commands 40-50% of India's organized glass bottle segment; Milton commands 30-40% of the premium insulated stainless steel segment. Concentration is lowest in the plastic segment, where hundreds of BIS-certified and uncertified manufacturers compete primarily on price in traditional trade channels. The online channel is the least concentrated.

Investment & Growth Opportunities

Fastest Growing Segments

Silicone bottles (~5.9% CAGR), online channel (~5.6% CAGR), stainless steel premium segment (INR 800+, ~6.5% CAGR within stainless steel), smart bottles (~30%+ CAGR from small base), and corporate gifting-targeted branded bottles (~8%+ CAGR) represent India's highest-growth reusable bottle investment vectors.

Emerging Market Opportunities

The rural and semi-urban market represents India's largest unaddressed reusable bottle opportunity. India's villages and Tier-3 towns house India's population with very limited organized retail access to quality reusable bottles. Government programs creating clean water access and plastic awareness in these markets, combined with improving rural internet connectivity, enabling Meesho social commerce penetration, are creating an addressable market in affordable BPA-free reusable bottles that no organized brand currently serves effectively.

Investment Themes

- Premium D2C brand building in stainless steel: Capital investment of INR 5-15 Crore in manufacturing equipment, Amazon catalog management, and Instagram brand building can establish an INR 30-50 Crore annual revenue business within 3-5 years in India's fastest-growing premium stainless segment.

- School institutional supply program for BIS-certified affordable bottles: Government education programs creating institutional bottle procurement annual tender opportunities. Manufacturers with BIS IS:10955 certification, domestic production, and national distribution capability are well-positioned to win state government school bottle supply contracts.

Future Market Outlook (2026-2034)

The India reusable water bottle market is projected to grow from USD 330.00 Million in 2025 to USD 486.47 Million by 2034, delivering a 4.41% CAGR over the forecast period. The market's anchor value of USD 409.47 Million in 2030 represents a reusable bottle industry that has crossed a critical adoption inflection point, where reusable bottles have transitioned from a niche environmental-choice product to a mainstream consumer purchase for India's urban middle class, driven by the convergence of plastic ban regulations, health consciousness, and the growing social norm of carrying a personal reusable bottle in fitness and professional environments.

Three structural forces define India's reusable water bottle market's growth trajectory through 2034: the progressive tightening of single-use plastic regulations that would directly mandate the most common disposable water bottle substitution and create the market's most significant regulatory tailwind; India's urban fitness culture growth, representing the consumer segment with the highest reusable bottle purchase frequency and premium price tolerance; and the online channel's continued penetration enabling brand discovery and purchase for premium bottles in Tier-2 and Tier-3 cities where modern trade currently limits organized brand access.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including VP Sales and Marketing executives from Milton Consumer Products, Cello World Ltd., and Borosil Ltd.; purchasing directors from D-Mart, Amazon India Home & Kitchen category management, and Decathlon India Sports category; government officials from MoEFCC Plastic Waste Management division; BIS officials overseeing IS:10955 and IS:15570 certification; D2C brand founders; and consumer research interviews with 200+ urban and semi-urban water bottle purchasers across North, West, South, and East India.

Secondary Research

Secondary research encompassed plastic waste management rules enforcement reports, BIS certification database for IS:10955 and IS:15570 registered manufacturers (2020-2025), ASSOCHAM India housewares market survey 2024, Amazon India Best Seller and Amazon's Choice data analysis for bottle categories, Cello World IPO prospectus including market size and competitive data, Borosil Ltd. annual reports, Nielsen India consumer health and wellness survey, ASSOCHAM FMCG reports, and India brand finance consumer goods brand survey 2025. Over 85 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up type x distribution channel models calibrated against FMCG volume growth correlation with India's urban disposable income growth, BIS certification database manufacturer capacity expansion tracking, Cello World and Borosil annual report volume disclosures, Amazon India category GMV growth proxy analysis, and MoEFCC plastic ban progressive restriction implementation timeline modeling. Key inputs include India's urban middle class growth projections, online channel FMCG penetration growth trajectory (IBEF e-commerce India data), gym and fitness center growth projections, and stainless steel price forecast scenarios.

India Reusable Water Bottle Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Glass, Plastic, Stainless Steel, Silicone, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Online, Speciality Stores, Convenience Stores |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Hamilton Housewares Pvt. Ltd., Cello World Limited, BOROSIL, Nayasa, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India reusable water bottle market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India reusable water bottle market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India reusable water bottle industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Reusable Water Bottle Market Report

The India reusable water bottle market reached USD 330.00 Million in 2025, driven by the government's single-use plastic ban, rising health and hydration awareness, India's urban fitness culture, D2C brand e-commerce growth, and expanding organized retail coverage through D-Mart and modern trade hypermarkets.

The market grows at 4.41% CAGR during 2026-2034, reaching USD 486.47 Million by 2034, driven by progressive plastic regulations, premium stainless steel segment trade-up, silicone bottle adoption in fitness segments, online channel expansion to Tier-2/3 cities, and India's growing corporate gifting market for branded insulated bottles.

Stainless steel leads at 36.8%, driven by insulation performance, BPA-free safety credentials, and aspirational premium branding.

Supermarkets and hypermarkets lead at 34.7% through D-Mart stores, Big Bazaar, and Reliance Smart's nationwide reach with seasonal summer promotions.

North India leads at 31.5%, driven by Delhi NCR's premium consumer base, extreme summer heat creating critical insulated bottle demand, and India's largest wholesale distribution hub supplying pan-India retail networks.

Leading companies include Hamilton Housewares Pvt. Ltd., Cello World Limited, BOROSIL, and Nayasa, among others.

The market is projected to reach approximately USD 409.47 Million by 2030, with the premium insulated stainless steel segment growing 12%+ annually, the online channel reaching 40%+ of revenues, and smart bottle adoption beginning in the fitness segment.

Online grows at ~5.6% CAGR through Amazon India's premium discovery marketplace, Flipkart's volume segment reach, Meesho's Tier-2/3 social commerce expansion, and quick commerce enabling impulse premium bottle purchases with 10-minute delivery.

State government school health programs create high annual procurement opportunities for BIS IS:10955-certified affordable bottles. Government procurement preference for Make in India-certified domestic manufacturers gives organized domestic brands structural advantages over imported alternatives.

India's corporate gifting market has adopted branded insulated stainless-steel bottles as one of India's most preferred festival and employee gifting items. A branded 600ml vacuum bottle with logo engraving retails for bulk procurement.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)