India Robo-Advisory Market Size, Share, Trends and Forecast by Business Model, Service Type, Provider, End User, and Region, 2026-2034

India Robo-Advisory Market Summary:

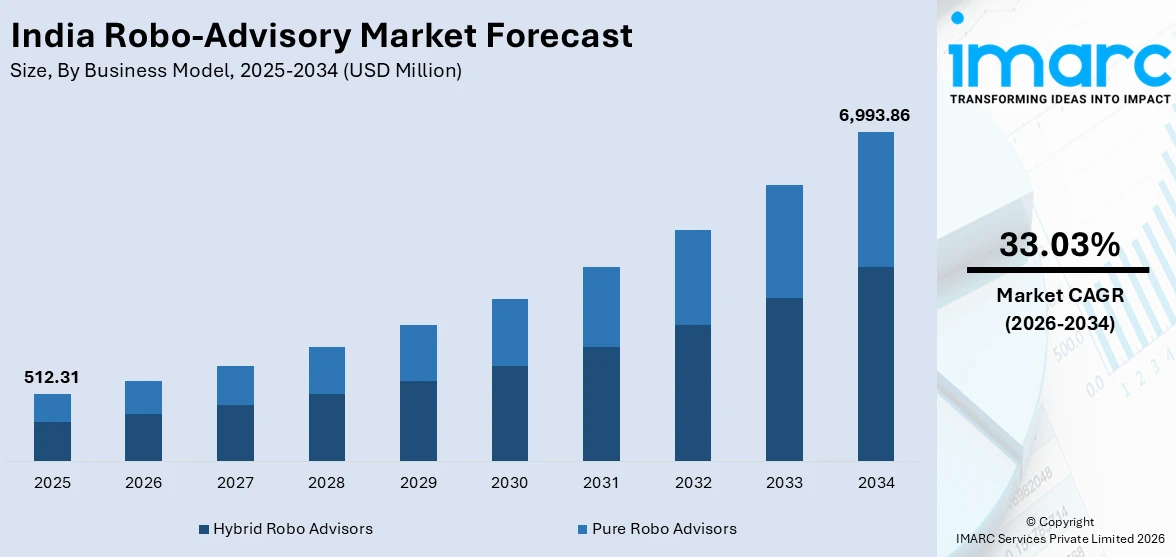

The India robo-advisory market size was valued at USD 512.31 Million in 2025 and is projected to reach USD 6,993.86 Million by 2034, growing at a compound annual growth rate of 33.03% from 2026-2034.

The India robo-advisory market is experiencing robust expansion driven by the country's accelerating digital transformation, rising financial literacy among younger demographics, and growing preference for automated investment management solutions. Increasing smartphone penetration and expanding internet connectivity across urban and semi-urban regions are facilitating wider adoption of algorithm-driven financial planning services. The convergence of artificial intelligence advancements with evolving investor expectations for personalized, cost-effective wealth management is creating a highly conducive environment for sustained market development across diverse investor segments throughout the nation.

Key Takeaways and Insights:

- By Business Model: Hybrid robo advisors dominates the market with a share of 61.5% in 2025, owing to its ability to combine algorithmic efficiency with human advisory expertise, addressing the preference among Indian investors for a blended approach that offers automated portfolio management alongside personalized financial guidance during market volatility and complex investment decisions.

- By Service Type: Direct plan-based/goal-based leads the market with a share of 54.2% in 2025. This dominance is driven by the growing demand for transparent, commission-free investment pathways that align portfolio construction directly with individual financial milestones, enabling retail investors to pursue systematic wealth accumulation through structured goal-oriented frameworks.

- By Provider: Fintech robo advisors exhibit a clear dominance in the market with 48.6% share in 2025, reflecting their technological agility, lower fee structures, and superior mobile-first user experiences that resonate strongly with digitally native investors seeking accessible and intuitive automated wealth management solutions across diverse asset classes.

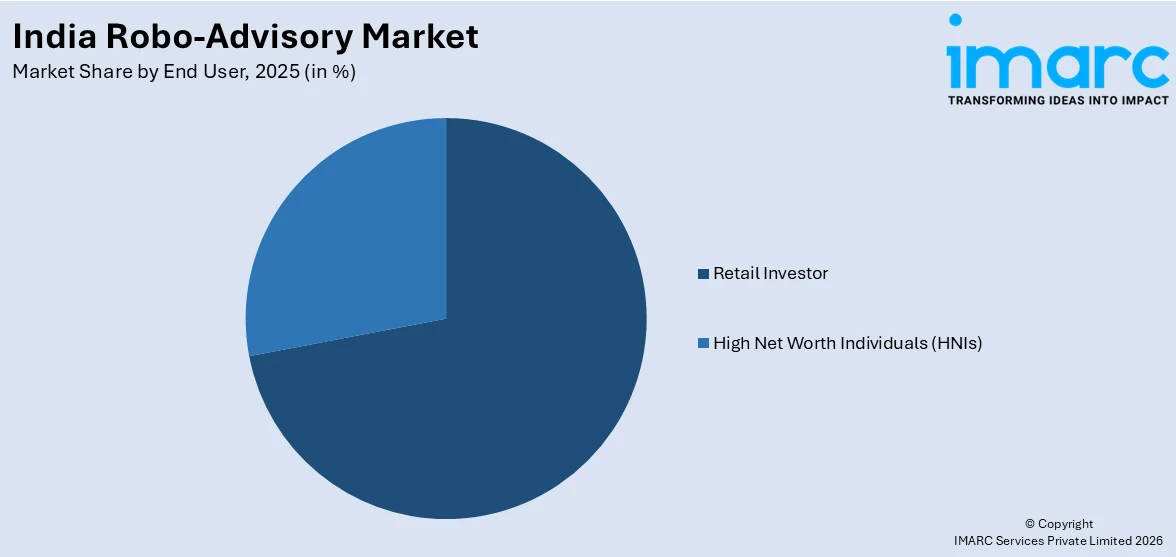

- By End User: Retail investor holds the market with a share of 72.1% in 2025, owing to the democratization of investment advisory services through low minimum investment thresholds, simplified digital onboarding processes, and affordable fee models that have unlocked participation from first-time and middle-income investors across the country.

- By Region: West India represents the largest region with 34.7% share in 2025, driven by the concentration of financial services infrastructure in Mumbai and surrounding metropolitan areas, higher disposable incomes, established fintech ecosystems, and a well-developed culture of capital market participation among the region's investor population.

- Key Players: Key players drive the India robo-advisory market by expanding product portfolios, integrating advanced artificial intelligence capabilities, and strengthening nationwide digital distribution networks. Their investments in user experience enhancement, regulatory compliance, and strategic partnerships with financial institutions accelerate adoption, boost investor confidence, and ensure consistent service availability across diverse demographic and geographic segments.

To get more information on this market Request Sample

The India robo-advisory market is driven by a combination of structural and technological elements that are transforming the financial services sector in the country. The quick development of digital infrastructure, thanks to government initiatives that encourage digital payments and financial inclusion, has created a conducive environment for the development of automated investment platforms. The demographic advantage of India, which has a young and technology-friendly population, is creating an unprecedented level of demand for accessible and affordable wealth management services that go beyond the constraints of traditional advisory services. The widespread availability of smartphones and affordable mobile internet connectivity has broken geographical constraints, allowing investors in tier-two and tier-three cities to take advantage of advanced portfolio management services that were hitherto accessible only to high-net-worth individuals in urban areas. Additionally, the growing use of artificial intelligence and machine learning in investment algorithms is improving the accuracy and personalization of portfolio suggestions, thereby increasing investor confidence and facilitating market entry in the country.

India Robo-Advisory Market Trends:

Rising Adoption of Hybrid Advisory Models Combining Automation with Human Expertise

The India robo-advisory market is witnessing a significant shift toward hybrid advisory models that seamlessly integrate algorithm-driven portfolio management with access to human financial advisors. Indian investors, particularly those navigating complex financial decisions such as retirement planning, tax optimization, and intergenerational wealth transfer, increasingly prefer platforms that offer the efficiency of automated rebalancing alongside the reassurance of human oversight during periods of market turbulence. This blended approach addresses the cultural preference for personalized counsel while leveraging the scalability and cost advantages of digital automation. Wealth management firms and fintech platforms are responding by developing tiered service architectures that cater to varying levels of advisory engagement, enabling seamless transitions between fully automated and advisor-assisted modes based on portfolio complexity and individual investor preferences.

Expansion of Robo-Advisory Services into Tier-Two and Tier-Three Cities

Robo-advisory platforms in India are rapidly expanding their footprint beyond metropolitan centers into smaller cities and semi-urban regions, driven by improving internet infrastructure and increasing financial awareness among younger demographics. The proliferation of vernacular language support within investment applications is removing linguistic barriers, enabling first-time investors from diverse cultural backgrounds to engage confidently with automated wealth management tools. This geographic democratization is particularly significant as emerging investor segments in these regions demonstrate strong appetite for systematic investment plans and goal-based financial products. Fintech platforms are tailoring their user interfaces and educational content to address the specific financial literacy requirements of these underserved markets, creating onboarding experiences that simplify complex investment concepts and foster sustained engagement with digital advisory services across previously untapped demographic segments.

Integration of Generative Artificial Intelligence for Enhanced Portfolio Personalization

The incorporation of generative artificial intelligence and advanced machine learning capabilities into robo-advisory platforms is transforming the depth and precision of investment personalization available to Indian investors. These technologies enable platforms to analyze vast datasets encompassing market conditions, macroeconomic indicators, and individual behavioral patterns to deliver highly customized portfolio recommendations that dynamically adapt to changing financial circumstances. Natural language processing capabilities are enhancing client interaction by enabling conversational interfaces that simplify complex financial queries and deliver intuitive investment guidance. This technological evolution is particularly impactful in addressing the diverse risk appetites and investment horizons prevalent among Indian investors, as platforms leverage predictive analytics to anticipate market movements and proactively suggest portfolio adjustments that align with each investor's unique financial trajectory and life-stage requirements.

Market Outlook 2026-2034:

The robo-advisory market in India is expected to register significant growth over the forecast period, driven by positive regulatory trends, the development of digital infrastructure, and shifting investor attitudes towards technology-based wealth management platforms. The growing complexity of artificial intelligence models and the rising acceptance of automated financial planning services among younger generations of investors are expected to fuel strong demand growth in the country. The progressive regulatory framework, which includes the Securities Markets Code introduced in December 2025 that specifically provides for the recognition of robo-advisory platforms, is expected to provide a more organized framework for operations, thus boosting investor sentiment. Additionally, the integration of wealth management services with the overall fintech ecosystem that includes payment systems, lending, and insurance is also expected to fuel cross-selling and engagement with the platform among existing customers over the forecast period. The market generated a revenue of USD 512.31 Million in 2025 and is projected to reach a revenue of USD 6993.86 Million by 2034, growing at a compound annual growth rate of 33.03% from 2026-2034.

India Robo-Advisory Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Business Model |

Hybrid Robo Advisors |

61.5% |

|

Service Type |

Direct Plan-Based/Goal-Based |

54.2% |

|

Provider |

Fintech Robo Advisors |

48.6% |

|

End User |

Retail Investor |

72.1% |

|

Region |

West India |

34.7% |

Business Model Insights:

- Pure Robo Advisors

- Hybrid Robo Advisors

Hybrid robo advisors dominate with a market share of 61.5% of the total India robo-advisory market in 2025.

Hybrid robo advisors command the largest share of the India robo-advisory market, driven by the inherent preference among Indian investors for advisory frameworks that combine algorithmic precision with human judgment. The hybrid model addresses the trust deficit that purely automated platforms face in a market where personal relationships have traditionally underpinned financial decision-making. These platforms offer tiered engagement options, enabling investors to access automated portfolio construction for routine allocation decisions while retaining the ability to consult human advisors for complex financial planning scenarios.

The sustained dominance of hybrid robo-advisory platforms is further reinforced by the evolving expectations of high-net-worth individuals and mass-affluent investors who demand seamless integration between digital convenience and personalized advisory depth. Leading platforms are deploying sophisticated client segmentation strategies that automatically escalate advisory interactions based on portfolio complexity, transaction value thresholds, and life-event triggers. This intelligent routing mechanism ensures that investors receive appropriately calibrated guidance without compromising the operational efficiency that automation delivers, positioning hybrid models as the most commercially viable approach for scaling advisory services across India's diverse and rapidly expanding investor base.

Service Type Insights:

- Direct Plan-Based/Goal-Based

- Comprehensive Wealth Advisory

Direct plan-based/goal-based leads with a share of 54.2% of the total India robo-advisory market in 2025.

Direct plan-based/goal-based services dominate the India robo-advisory market, reflecting the strong investor appetite for transparent, commission-free investment pathways that align portfolio construction with specific financial milestones such as retirement, education funding, and home ownership. These services leverage algorithm-driven asset allocation frameworks that automatically adjust investment strategies based on proximity to target dates and changing risk parameters. The direct plan model resonates particularly well with cost-conscious Indian investors who seek to maximize returns by eliminating distributor commissions, as the average fee for robo-advisory services in India remains approximately half a percent of assets under management compared to significantly higher charges levied by traditional advisory services.

The continued expansion of direct plan-based robo-advisory services is supported by the growing financial awareness among millennial and generation-Z investors who prioritize goal clarity and measurable progress tracking in their investment journeys. Platforms offering these services have developed intuitive visualization tools that display real-time progress toward financial objectives, incorporating scenario analysis capabilities that illustrate the impact of varying contribution levels and market conditions on goal achievement probabilities. This transparency-driven approach fosters sustained investor engagement and encourages disciplined savings behavior, strengthening the value proposition of goal-based advisory frameworks and reinforcing their market leadership position across the Indian landscape.

Provider Insights:

- Fintech Robo Advisors

- Banks

- Traditional Wealth Managers

- Others

Fintech robo advisors exhibits a clear dominance with a 48.6% share of the total India robo-advisory market in 2025.

Fintech robo advisors lead the India robo-advisory market, propelled by their technology-first approach that prioritizes user experience, mobile accessibility, and rapid product innovation. These platforms have capitalized on India's expanding digital infrastructure and the surge in retail investor participation to establish dominant market positions through intuitive application interfaces, paperless onboarding processes, and competitive pricing structures. The fintech advantage is particularly pronounced in customer acquisition, where digital-native platforms leverage social media engagement, educational content, and referral mechanisms to attract younger investor demographics. India currently hosts over one hundred and eighteen robo-advisory startups according to industry tracking platforms, reflecting the vibrant entrepreneurial activity within this segment.

The competitive edge of fintech robo-advisory providers extends beyond customer acquisition to encompass continuous technological enhancement and ecosystem integration capabilities. These platforms are increasingly embedding complementary financial services including digital payments, micro-lending, and insurance distribution within their advisory frameworks, creating comprehensive financial management ecosystems that deepen user engagement and increase lifetime customer value. Their agile development methodologies enable rapid deployment of feature enhancements and regulatory compliance updates, maintaining technological superiority over traditional financial institutions that face legacy system constraints and slower innovation cycles in the evolving robo-advisory landscape throughout India.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Retail Investor

- High Net Worth Individuals (HNIs)

Retail investor holds the largest share at 72.1% of the total India robo-advisory market in 2025.

Retail investor dominates the India robo-advisory market, reflecting the transformative impact of automated investment platforms in democratizing access to professional wealth management services for individual investors with modest capital. The low minimum investment thresholds offered by robo-advisory platforms have eliminated traditional entry barriers, enabling first-time investors and salaried professionals to participate in diversified portfolio management. India's rapidly expanding retail investor base, supported by simplified digital onboarding through Aadhaar-based electronic know-your-customer verification and unified payments interface integration, has driven unprecedented adoption. India's wealth management industry is projected to benefit from continued digitization and expanding investor participation, with retail investor engagement rising steadily across cities and smaller towns.

The retail investor segment's dominance is further strengthened by behavioral finance innovations embedded within robo-advisory platforms that address common investment pitfalls such as panic selling, timing biases, and emotional decision-making. Automated rebalancing mechanisms and systematic investment plan features enforce disciplined investing behavior, helping retail participants maintain consistent portfolio strategies regardless of short-term market fluctuations. The integration of financial education modules and interactive portfolio simulation tools within these platforms empowers retail investors with enhanced financial literacy, fostering informed decision-making and long-term platform loyalty that sustains the segment's commanding position within the broader market ecosystem.

Regional Insights:

- North India

- South India

- East India

- West India

West India represents the leading region with a 34.7% share of the total India robo-advisory market in 2025.

West India holds the largest market share in the India robo-advisory market, and this is largely driven by Mumbai's status as the financial capital of India and the presence of banking, stock market, and fintech activities in the larger Mumbai metropolitan area. The region has a deeply ingrained capital market culture, with higher average disposable incomes and a well-developed fintech ecosystem of financial technology companies that have led the way in developing digital investment solutions for the Indian market. The entrepreneurial spirit of Gujarat and the growing technology talent pool in Pune also add to the high adoption rates in the region.

The continued dominance of the region by West India is driven by the presence of stock exchanges, headquarters of regulatory bodies, and a large network of financial intermediaries that make the region extremely conducive to the development of robo-advisory solutions. The region's wealthy urban population has shown high receptivity to digital investment solutions, with a strong systematic investment plan and mutual fund penetration that naturally extends to robo-advisory solutions. Furthermore, the clustering of fintech accelerators, venture capital firms, and technology talent hubs in cities like Mumbai and Pune continues to drive product innovation and competitive differentiation among robo-advisory providers operating within the region.

Market Dynamics:

Growth Drivers:

Why is the India robo-advisory market growing?

Accelerating Digital Infrastructure and Smartphone Penetration Driving Widespread Accessibility

The rapid expansion of India's digital infrastructure serves as a foundational catalyst for the robo-advisory market, enabling millions of previously underserved individuals to access sophisticated investment management tools through their mobile devices. The government's sustained commitment to the Digital India initiative has dramatically improved internet connectivity across rural and semi-urban areas, creating new addressable markets for fintech platforms offering automated advisory services. The convergence of affordable smartphone hardware, competitively priced mobile data plans, and the widespread adoption of the unified payments interface has established a robust technological substrate upon which robo-advisory platforms can build seamless end-to-end investment experiences. This infrastructure evolution has been particularly transformative in tier-two and tier-three cities, where traditional wealth management services have historically maintained minimal presence due to the high cost of physical distribution networks. The availability of Aadhaar-based electronic know-your-customer verification has further streamlined the onboarding process, reducing account opening timelines from days to minutes and eliminating the documentation burden that previously deterred first-time investors from engaging with formal investment channels. As digital literacy continues to improve across demographic segments, the addressable market for robo-advisory services expands commensurately, positioning digital infrastructure advancement as a primary engine of sustained market growth throughout the forecast period.

Growing Financial Awareness and Shifting Investment Preferences Among Younger Demographics

India's demographic composition, characterized by a median age significantly below the global average and a rapidly expanding middle class, is generating transformative demand for accessible and affordable investment advisory services that align with the preferences and expectations of digitally native generations. Millennial and generation-Z investors demonstrate markedly different financial behaviors compared to preceding generations, exhibiting strong preferences for self-directed investment approaches, transparent fee structures, and technology-enabled convenience over traditional relationship-based advisory models. These younger cohorts are increasingly recognizing the importance of early and systematic wealth accumulation, driven by rising awareness of inflation's erosive impact on savings and the limitations of conventional fixed-deposit instruments in generating real returns. The cultural shift from physical asset accumulation toward financial asset investment is accelerating this transition, as younger Indians increasingly allocate savings toward equity-linked instruments through robo-advisory platforms rather than traditional gold and real estate holdings. Social media influencers, financial education content creators, and peer networks are amplifying awareness of automated investment solutions, creating viral adoption cycles that traditional marketing approaches cannot replicate. This demographic dividend, combined with increasing urbanization and rising household incomes, ensures a continuously expanding pool of prospective robo-advisory users who prioritize digital-first engagement models.

Cost Efficiency and Democratization of Professional Wealth Management Services

The fundamental cost advantage offered by robo-advisory platforms over traditional wealth management services represents a compelling growth driver in the Indian market, where fee sensitivity significantly influences investment product adoption across all demographic segments. Traditional financial advisory services in India typically impose management fees, distribution commissions, and transaction charges that collectively diminish net investment returns, particularly for smaller portfolio sizes where fixed advisory costs consume a disproportionate share of investment gains. Robo-advisory platforms dramatically reduce these cost burdens through algorithmic automation that eliminates the need for large advisory workforces, physical branch infrastructure, and manual portfolio management processes. This cost rationalization enables platforms to offer professional-grade investment management at fee levels accessible to investors with modest capital, effectively democratizing services previously reserved for affluent individuals. The transparent fee structures adopted by most robo-advisory platforms further enhance their value proposition, as investors can clearly quantify the total cost of ownership without navigating complex commission arrangements or hidden charges. This pricing transparency builds institutional trust among price-sensitive Indian consumers and encourages sustained platform engagement, as investors recognize the compounding benefit of reduced fees on long-term portfolio performance. The resulting expansion of the addressable market beyond traditional high-net-worth segments fuels sustainable growth trajectories for the robo-advisory sector.

Market Restraints:

Limited Financial Literacy and Trust Deficit Toward Automated Advisory Systems

Despite improving awareness levels, a significant portion of India's potential investor base continues to harbor reservations about entrusting financial decisions to algorithm-driven platforms, preferring the reassurance of human advisory relationships for investment management. This trust deficit is particularly pronounced among older demographic segments and investors in smaller cities where exposure to digital financial services remains limited. The absence of widespread understanding regarding how robo-advisory algorithms construct and manage portfolios creates apprehension about the reliability and accountability of automated investment recommendations, constraining the pace of adoption among risk-averse investor cohorts.

Evolving Regulatory Framework Creating Compliance Uncertainties

The regulatory landscape governing robo-advisory services in India remains in a transitional phase, with the Securities and Exchange Board of India continuing to refine its framework for automated investment advisory platforms under existing investment adviser regulations. The absence of dedicated robo-advisory-specific regulations creates compliance ambiguities for platform operators navigating requirements designed primarily for traditional advisory models. Registration prerequisites, net worth thresholds, and qualification mandates impose operational constraints on emerging fintech platforms, while evolving guidelines on algorithmic transparency and investor disclosure obligations add layers of regulatory complexity.

Cybersecurity Vulnerabilities and Data Privacy Concerns

The digital-first operational model of robo-advisory platforms inherently exposes them to cybersecurity threats that can undermine investor confidence and platform credibility. The handling of sensitive personal and financial data through automated systems raises legitimate concerns about data privacy, unauthorized access, and potential misuse of investor information. As robo-advisory platforms aggregate increasing volumes of financial data, they become attractive targets for cyberattacks, necessitating continuous investment in advanced security infrastructure and compliance with evolving data protection regulations that impose additional operational burdens on platform operators.

Competitive Landscape:

The India robo-advisory market has a highly dynamic competitive environment with a wide range of fintech startups, established financial institutions, and traditional wealth management companies competing on the basis of innovation in technology, pricing, and the range of services offered. The competitive landscape indicates a moderately fragmented market where technology-driven disruptors are disrupting established financial service providers with their superior digital experience and aggressive customer acquisition plans. The level of competition is expected to increase as banks and traditional wealth management companies accelerate their digital transformation plans, developing their own robo-advisory solutions to protect their existing customer bases from fintech disruption. The level of strategic differentiation is increasingly based on the complexity of algorithms, the range of financial services integrated, and the ability to provide customers with a personalized advisory experience. Collaboration between fintech platforms and established financial institutions is becoming an increasingly popular competitive approach, allowing technology companies to tap into the distribution channels of financial institutions while providing the latter with access to superior digital advisory technology and younger demographics.

India Robo-Advisory Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Business Models Covered |

Pure Robo Advisors, Hybrid Robo Advisors |

|

Service Types Covered |

Direct Plan-Based/Goal-Based, Comprehensive Wealth Advisory |

|

Providers Covered |

Fintech Robo Advisors, Banks, Traditional Wealth Managers, Others |

|

End Users Covered |

Retail Investor, High Net Worth Individuals (HNIs) |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Robo-Advisory Market Report

The India robo-advisory market size was valued at USD 512.31 Million in 2025.

The India robo-advisory market is expected to grow at a compound annual growth rate of 33.03% from 2026-2034 to reach USD 6,993.86 Million by 2034.

Hybrid robo advisors dominated the market with a share of 61.5%, driven by their ability to combine algorithmic efficiency with human advisory expertise, addressing the preference among Indian investors for blended wealth management approaches.

Key factors driving the India robo-advisory market include accelerating digital infrastructure expansion, growing financial awareness among younger demographics, cost advantages over traditional advisory services, and increasing regulatory support for automated investment platforms.

Major challenges include limited financial literacy among certain demographic segments, trust deficit toward automated advisory systems, evolving regulatory compliance requirements, cybersecurity vulnerabilities, data privacy concerns, and competition from traditional wealth management providers expanding their digital capabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade