India Safes and Vaults Market Size, Share, Trends and Forecast by Type, Function Type, Application, End User, and Region, 2026-2034

India Safes and Vaults Market Size, Share, Trends & Forecast (2026-2034)

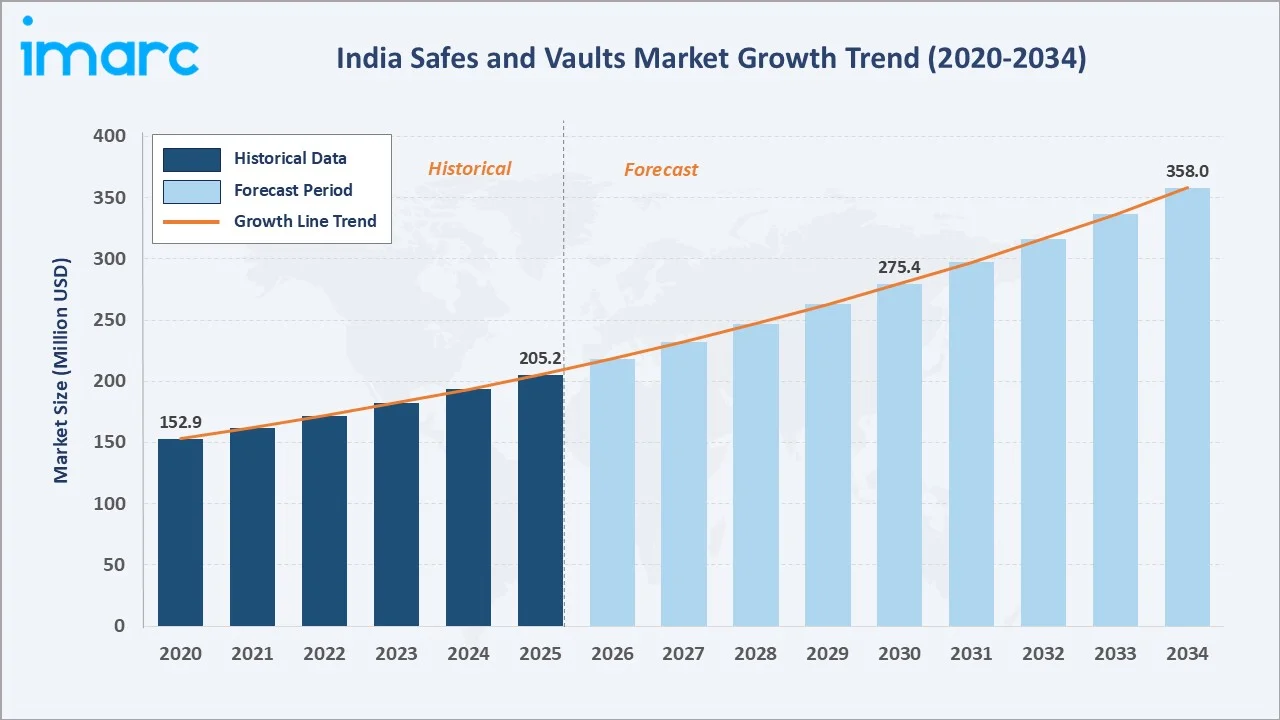

The India safes and vaults market reached USD 205.2 Million in 2025 and is projected to reach USD 358.0 Million by 2034, growing at a CAGR of 6.06% during 2026-2034. The market is driven by rising demand for secure storage across banks, NBFCs, retail outlets, homes, jewelry stores, ATMs, and commercial establishments. India's bank branch expansion with Richmax Finvest targeting 1,000 branches across India by 2030, smart safe adoption with biometric and IoT connectivity, and growing residential premium safe demand anchor the market's sustained growth through 2034. Commercial applications dominate at 64.8%. The banking sector leads end-user demand at 62.5%. West and Central India command 38.6% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 205.2 Million |

|

Forecast Market Size (2034) |

USD 358.0 Million |

|

CAGR (2026-2034) |

6.06% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Application |

Commercial (64.8%, 2025) |

|

Dominant End User |

Banking Sector (62.5%, 2025) |

|

Leading Region |

West & Central India (38.6%, 2025) |

The market expanded from USD 152.9 Million in 2020 to USD 205.2 Million in 2025, anchored at USD 275.4 Million in 2030, and forecast to reach USD 358.0 Million by 2034. India's demonetization legacy, combined with the post-COVID economic recovery driving new PSU bank branch openings and the jewellery sector's record gold demand, collectively generated the market's CAGR trajectory through 2025.

To get more information on this market, Request Sample

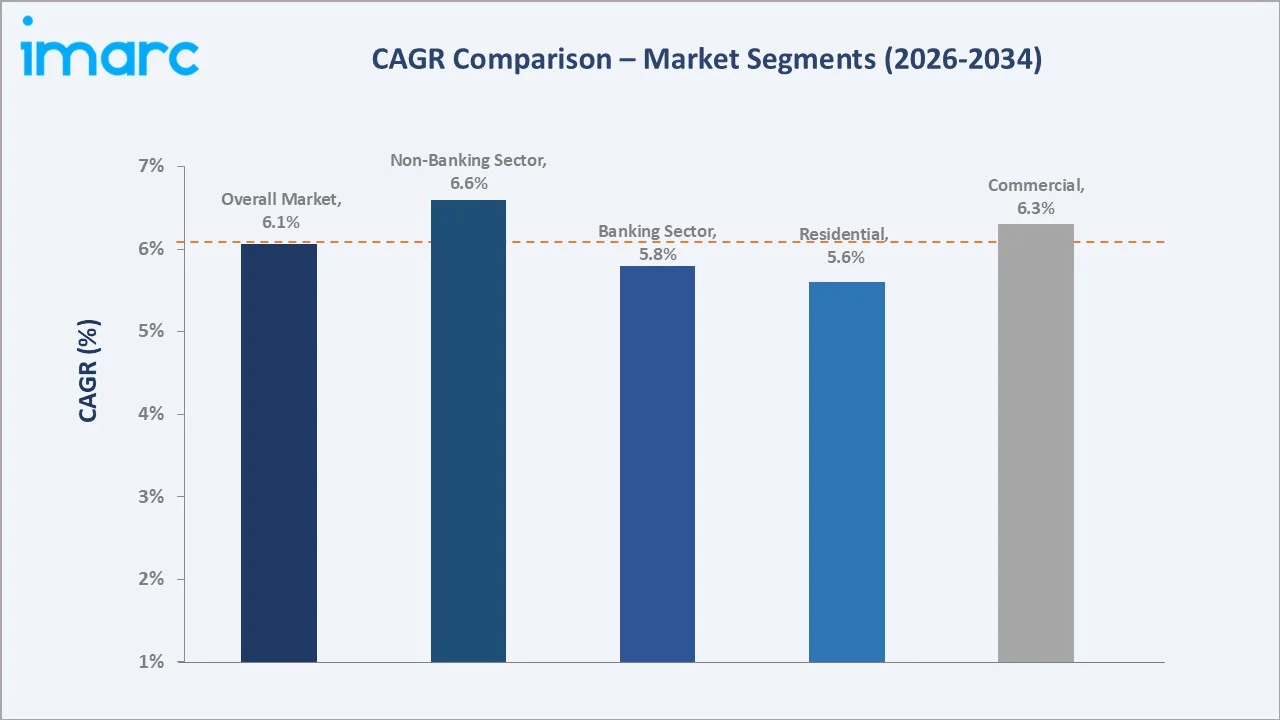

The non-banking sector grows fastest at ~6.6% CAGR (2026-2034), driven by India's jewellery retail expansion, gold loan NBFC branch proliferation, and corporate document vault demand from India's expanding GCC and BFSI services sector. Commercial application leads at ~6.3% CAGR through banking sector procurement, hotels, and SME cash management.

Executive Summary

The India safes and vaults market reached USD 205.2 Million in 2025, representing a mature-but-growing physical security market where the fundamental value proposition, protecting cash, gold, jewellery, and sensitive documents from theft and fire, remains unchanged, while the delivery mechanism is being transformed by smart technology integration, biometric authentication, and IoT-enabled remote monitoring. India's unique market characteristics create structural demand depth that generates consistent, safe and vault market growth regardless of short-term economic cycles. The market is projected to reach USD 358.0 Million by 2034 at 6.06% CAGR.

Commercial applications command 64.8% market share (2025), reflecting the organized commercial sector's comprehensive safe procurement across banking, jewellery retail, hospitality, corporate offices, and logistics. The banking sector at 62.5% is the market's structural backbone, creating predictable, large-volume demand that sustains the market's fundamental revenue base. West and Central India at 38.6% leads through Mumbai's financial sector concentration and Gujarat's diamond industry.

Key Market Insights

|

Insight |

Data |

|

Dominant Application |

Commercial - 64.8% share (2025) |

|

Dominant End User |

Banking Sector - 62.5% market share (2025) |

|

Leading Region |

West & Central India - 38.6% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Commercial at 64.8% anchored by the banking sector's regulatory-mandated safe infrastructure across branches: The Reserve Bank of India (RBI) mandates stringent, specific physical security standards for bank branches, especially those operating Currency Chests (CCs) or offering Safe Deposit Locker facilities, strong room construction specifications, and ATM safe cassette standards for all ATMs nationally.

- Banking Sector at 62.5% sustained by India's financial inclusion-driven branch expansion: India's banking sector is in the midst of a historically unprecedented rural branch expansion driven by Indian government programs and the RBI's financial inclusion mandate. Each new bank branch requires a minimum certified strong room (vault) and safe deposit lockers.

- West and Central India at 38.6% through financial hub concentration and precious metals industry density: Maharashtra accounts for more in India's total safe and vault market revenue as Mumbai concentrates India's financial services, jewellery industry, and high-value manufacturing.

India Safes and Vaults Market Overview

India's safes and vaults market encompasses all physical security products designed to protect valuables, documents, cash, and weapons from unauthorized access, fire, and natural disasters. Products range from compact residential key-lock safes through biometric floor safes and wall safes to vault doors and certified strong room systems for banking, jewellery, and industrial applications. Product categories include burglary-resistant safes, fire-resistant safes, bank safe deposit lockers, cash management safes, in-room hotel safes, gun/weapon safes, and custom vault room construction.

The ecosystem integrates steel and raw material suppliers, safe manufacturers, electronic lock and biometric module suppliers, BIS certification and testing laboratories, dealer and distribution networks, installation and vault construction contractors, and end-user segments spanning banking, jewellery, corporate offices, hospitality, residential, and government institutions. Macroeconomic factors include rising urbanization, growth in banking and financial services, expanding organized retail, increasing household incomes, and higher commercial infrastructure development.

Market Dynamics

To evaluate market opportunities, Request Sample

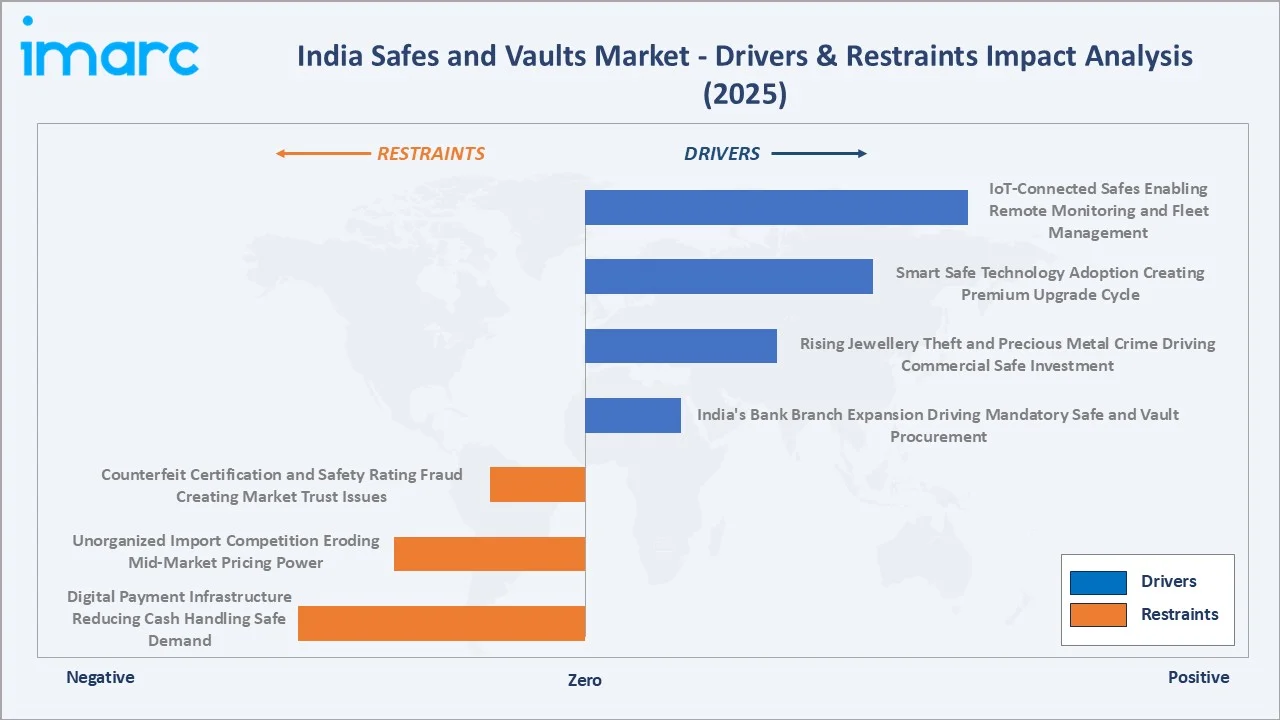

Market Drivers

- India's Bank Branch Expansion Driving Mandatory Safe and Vault Procurement: As of March 2025, scheduled commercial banks (SCBs) operated 164,000 domestic branches. Each new branch opening triggers mandatory procurement through RBI's physical security regulations: a strong room or certified vault door, safe deposit lockers, and a branch safe for day cash handling.

- Rising Jewellery Theft and Precious Metal Crime Driving Commercial Safe Investment: Rising jewellery theft is creating acute commercial safe upgrade demand from jewellery retailers, gold loan companies, and wealthy households. The formalization of jewellery retail, requiring documented inventory, has simultaneously increased the financial value of jewellery stock, requiring secure storage.

- Smart Safe Technology Adoption Creating Premium Upgrade Cycle: In July 2025, MySafe India launched an all-automatic safe deposit vault system in Gurugram. IoT-connected safes (Bluetooth/Wi-Fi enabled with smartphone monitoring apps) are entering India's hotel in-room safe segment and corporate cash management applications. AI-powered anomaly detection in vault room CCTV systems is creating premium vault room management service revenues.

Market Restraints

- Digital Payment Infrastructure Reducing Cash Handling Safe Demand: India's UPI transaction represents most of India's consumer retail payment value, dramatically reducing the cash volumes requiring secure storage at retail and SME locations.

- Unorganized Import Competition Eroding Mid-Market Pricing Power: India's online marketplace import-enabled product listings include uncertified safe SKUs from Chinese manufacturers at 40-60% below comparable certified domestic products, capturing the residential and small commercial safe segment where buyers lack technical knowledge to evaluate BIS certification requirements or understand fire and burglary resistance rating standards.

Market Opportunities

- India's Premium Residential Safe Market Driven by HNWI Wealth Expansion: India’s high-net-worth individuals population (HNWI) is expected to rise to 93,753 by 2028, representing a structurally growing addressable market for premium in-home safes.

- Gun Safe Market Expansion: Gun safe market expansion creates an opportunity by increasing demand for secure, tamper-resistant storage solutions among licensed firearm owners, defense personnel, security agencies, and shooting clubs. Stricter safety expectations and responsible weapon storage practices can support demand for compact gun lockers, biometric safes, and reinforced vault systems.

Market Challenges

- Counterfeit Certification and Safety Rating Fraud Creating Market Trust Issues: India's safe market experiences persistent counterfeit certification labeling. The Bureau of Indian Standards' surveillance inspection frequency is insufficient to police safe SKUs in the India market, allowing fraudulent certification claims to persist and undermining premium domestic manufacturer pricing power.

- Safe Deposit Locker Regulation Uncertainty: Safe deposit locker regulation uncertainty is delaying procurement decisions among banks, NBFCs, and financial institutions. Frequent compliance updates, liability concerns, and changing security standards may increase product customization needs, certification costs, and replacement-cycle uncertainty for vault and locker manufacturers.

Emerging Market Trends

1. Biometric and Multi-Factor Authentication Replacing Mechanical Locks

Biometric and multi-factor authentication systems are emerging as users increasingly prefer advanced security over traditional mechanical locks. Manufacturers are integrating fingerprint recognition, PIN access, RFID cards, mobile connectivity, and dual-authentication features to improve convenience, access control, and theft protection. This trend is gaining traction across banks, jewelry stores, hospitality, retail, offices, and high-income households seeking smart and tamper-resistant storage solutions.

2. IoT-Connected Smart Safes Enabling Remote Monitoring and Fleet Management

IoT-connected smart safes are enabling remote monitoring, real-time alerts, automated cash tracking, and centralized access management. Businesses such as banks, retail chains, fuel stations, hospitality operators, and cash-handling companies are increasingly adopting connected safes to improve security, reduce pilferage, and streamline cash logistics. These systems also support fleet-level monitoring, predictive maintenance, audit trails, and cloud-based analytics, making smart safes more efficient for multi-location operations.

3. Custom Vault Room Design as a Premium Commercial Service

Custom vault room design is emerging as banks, jewelry retailers, luxury residences, data centers, and high-value commercial facilities seek tailored security infrastructure. Clients are increasingly demanding reinforced vault rooms with biometric access, fire resistance, surveillance integration, modular layouts, and customized storage configurations based on operational requirements. This trend is encouraging manufacturers and security solution providers to offer end-to-end design, installation, engineering, and maintenance services as part of high-value commercial security projects.

4. Fire-Resistant Data Media Safes Growing Through Digital Asset Protection Awareness

Fire-resistant data media safes are emerging due to rising awareness around the protection of digital assets, confidential records, and electronic storage devices. Businesses, financial institutions, healthcare providers, and corporate offices are increasingly investing in specialized safes designed to protect hard drives, servers, documents, and backup media from fire, heat, humidity, and physical damage. The trend is being further supported by growing cybersecurity concerns, data compliance requirements, disaster recovery planning, and the increasing value of sensitive digital information.

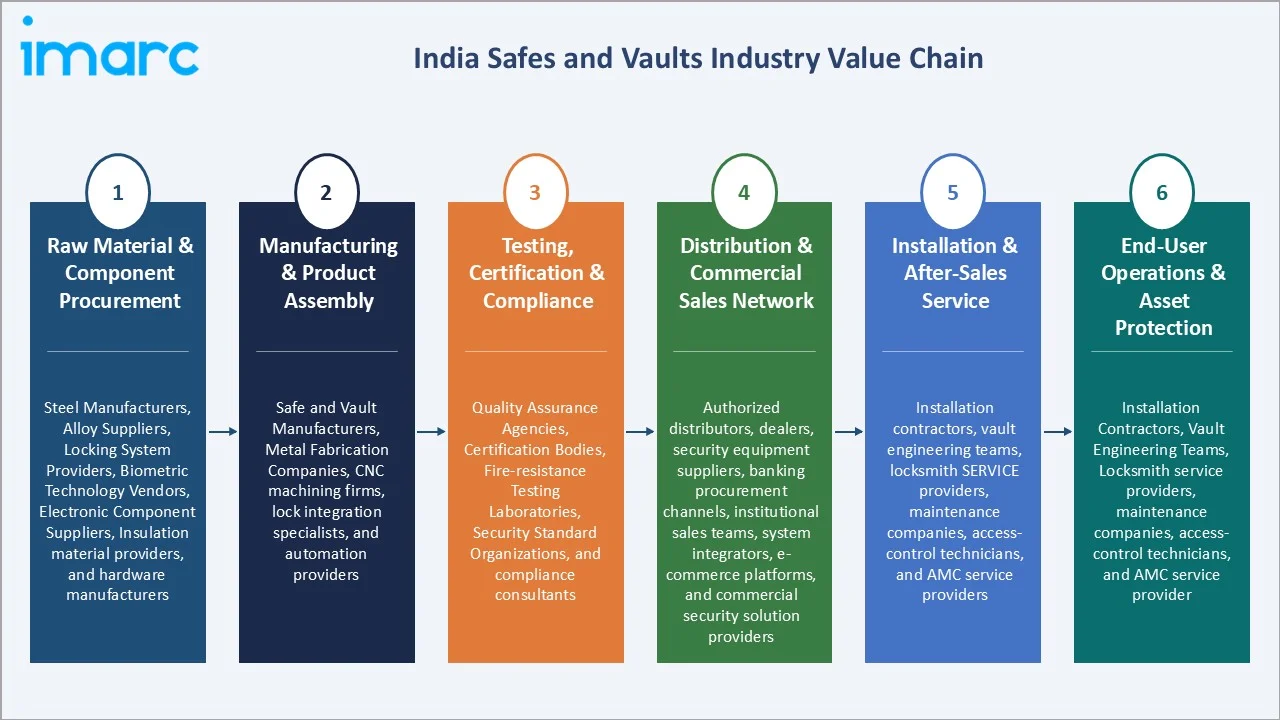

Industry Value Chain Analysis

India's safes and vaults value chain integrates steel and raw material procurement, manufacturing and lock mechanism integration, certification and quality testing, dealer and B2B distribution, installation services, and end-user operation. Safe manufacturers operate with 20-35% gross margins on standard products and 35-50% on custom vault room projects. Dealers earn a 15-25% margin on retail sales; installation services earn INR 5,000-50,000 per installation depending on product weight and vault complexity. Premium imported brands earn 40-60% gross margins through premium positioning against certified domestic equivalents.

|

Stage |

Key Participants |

|

Raw Material & Component Procurement |

Steel manufacturers, alloy suppliers, locking system providers, biometric technology vendors, electronic component suppliers, insulation material providers, and hardware manufacturers. |

|

Manufacturing & Product Assembly |

Safe and vault manufacturers, metal fabrication companies, CNC machining firms, lock integration specialists, and automation providers. |

|

Testing, Certification & Compliance |

Quality assurance agencies, certification bodies, fire-resistance testing laboratories, security standard organizations, and compliance consultants. |

|

Distribution & Commercial Sales Network |

Authorized distributors, dealers, security equipment suppliers, banking procurement channels, institutional sales teams, system integrators, e-commerce platforms, and commercial security solution providers. |

|

Installation & After-Sales Service |

Installation contractors, vault engineering teams, locksmith service providers, maintenance companies, access-control technicians, and AMC service providers. |

|

End-User Operations & Asset Protection |

Banks, NBFCs, jewelry retailers, hospitality establishments, retail chains, offices, government institutions, logistics operators, and residential users. |

The certification and quality testing tier is the India safe market's most critical value chain differentiation element. Godrej Security Solutions' decades-long BIS certification, IBA approval, and RBI currency chest specification compliance give it structural advantages in the institutional segment that cannot be replicated by new or small manufacturers without equivalent certification investment and time commitment.

Technology Landscape in the India Safes and Vaults Industry

Electronic and Biometric Locking Systems

Electronic and biometric locking systems are transforming by replacing conventional key-based security with advanced digital access control solutions. Manufacturers are increasingly integrating fingerprint authentication, PIN-based access, RFID systems, mobile app connectivity, and multi-factor authentication to improve security, convenience, and user tracking. These technologies are gaining adoption across banks, jewelry stores, hospitality, retail, offices, and residential segments seeking tamper-resistant, intelligent, and remotely manageable storage systems.

Vault Door Engineering and Construction Specifications

Vault door engineering and advanced construction specifications are shaping the technology landscape through the use of reinforced steel structures, multi-layer protection systems, fire-resistant barriers, and precision locking mechanisms. Manufacturers are focusing on high-security vault doors with anti-drill, anti-cut, blast-resistant, and tamper-detection technologies to meet evolving security requirements across banks, jewelry retailers, data centers, and government facilities. The industry is also witnessing increased adoption of modular vault construction, automated access systems, and customized engineering solutions for large-scale commercial security infrastructure.

AI-Powered Vault Room Security Systems

AI-powered vault room security systems are known for intelligent surveillance, real-time threat detection, facial recognition, access analytics, and automated security monitoring. These systems improve asset protection by enabling predictive alerts, remote monitoring, digital audit trails, and integrated biometric access control for residential, banking, and commercial applications. The trend is further supported by partnerships such as Prestige Group’s collaboration with Aurm to introduce advanced in-community safe-deposit locker facilities in upcoming residential projects, reflecting rising demand for technology-enabled secure storage solutions beyond traditional bank lockers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

🔒 |

🔒 |

2025 |

|

Function Type |

🔒 |

🔒 |

2025 |

|

Application |

Commercial |

64.8% |

2025 |

|

End-User |

Banking Sector |

62.5% |

2025 |

|

Region |

West and Central India |

38.6% |

2025 |

By Application

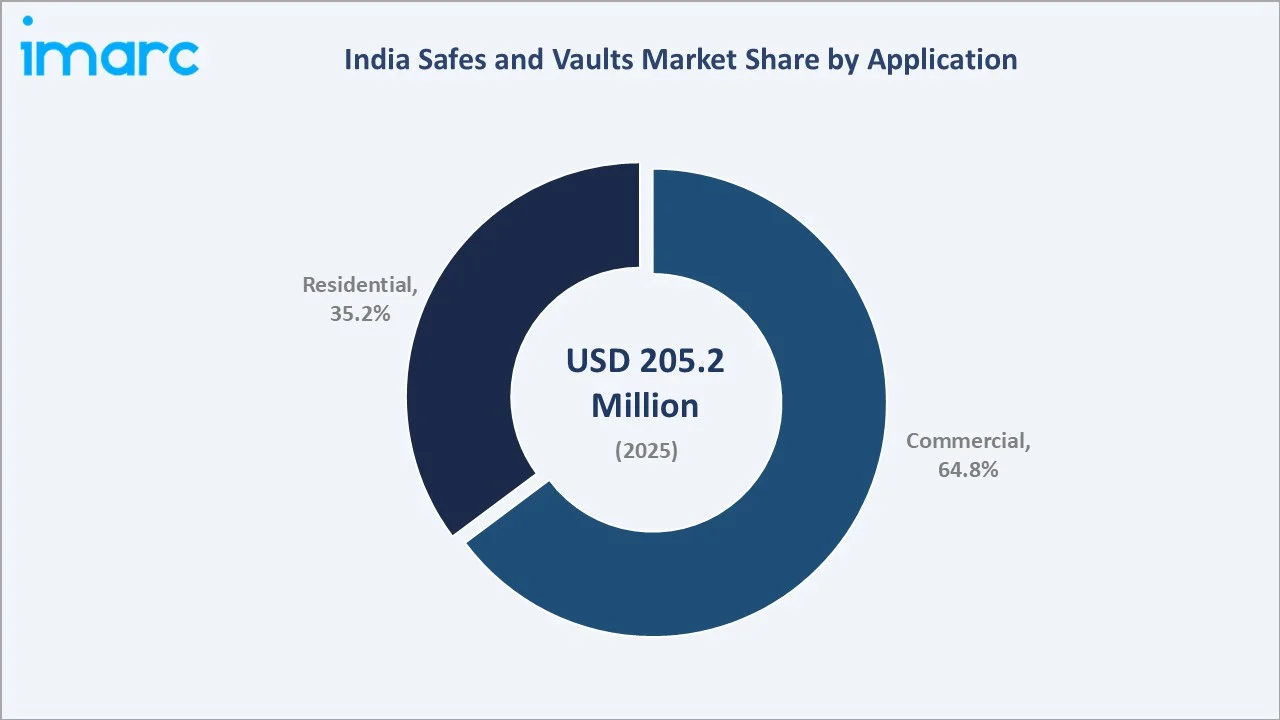

Commercial applications lead at 64.8% market share (2025). India's commercial safe market encompasses all non-residential safe and vault procurement, such as the banking sector, jewellery retail, hospitality, corporate offices, government institutions, factories, and commercial storage. Commercial safes are specified to higher security ratings and command higher per-unit values versus residential equivalents.

To access detailed market analysis, Request Sample

Residential applications at 35.2% grow at ~5.6% CAGR, driven by India's expanding urban middle class, increasing home gold storage following pandemic-era bank locker access difficulties, and premium residential developers incorporating safe storage as a standard apartment amenity. India's residential safe market remains significantly under-penetrated compared to comparable Asian markets, representing the largest market development opportunity through 2034 as awareness grows and product accessibility improves through e-commerce.

By End User

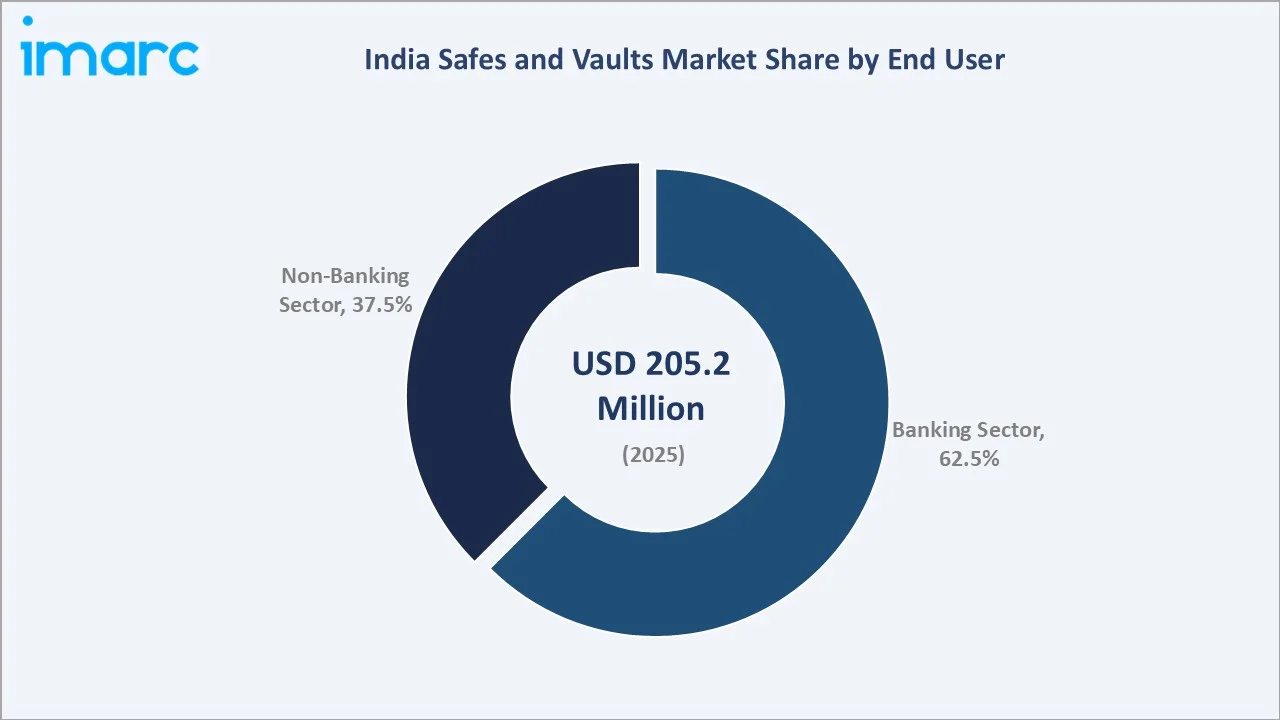

The banking sector leads at 62.5% market share (2025). India's scheduled commercial banks operate branches, ATMs, and currency chests and strong rooms, a physical security infrastructure of extraordinary scale. Safe deposit locker installation creates recurring vault room maintenance and upgrade demand.

The non-banking sector at 37.5% grows fastest at ~6.6% CAGR, encompassing jewellery retail, gold loan NBFCs, cash-in-transit companies, corporate document archival, government non-banking institutions, educational institutions, healthcare facilities, and premium residential.

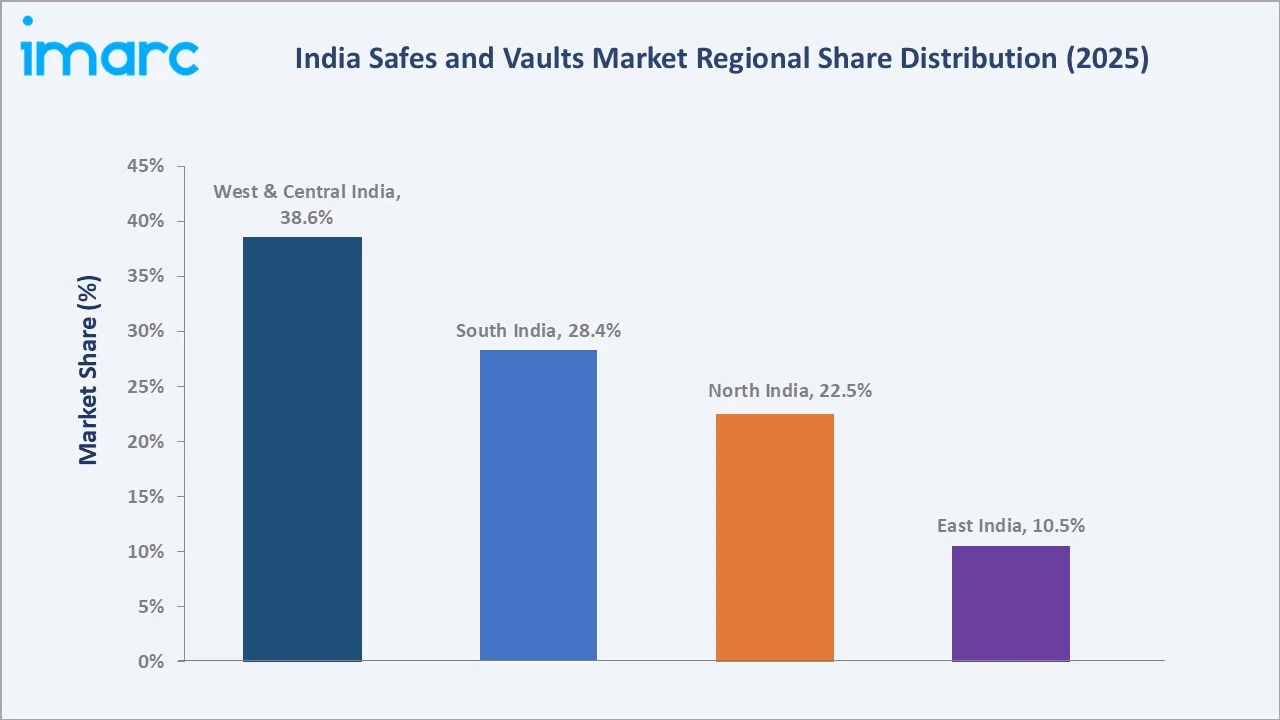

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

West & Central India |

38.6% |

Strong banking infrastructure, organized retail expansion, commercial real estate growth, and rising demand for secure cash and asset storage. The region benefits from high adoption across financial institutions, jewelry retailers, corporate offices, hospitality establishments, and residential users. |

|

South India |

28.4% |

Strong jewelry consumption, expanding banking networks, IT and commercial infrastructure growth, and rising adoption of advanced security systems. Demand is increasing for biometric safes, vault rooms, smart lockers, and fire-resistant storage solutions across commercial and residential sectors. |

|

North India |

22.5% |

Growing demand from government institutions, banks, retail chains, offices, hospitality, and high-income households. Infrastructure development, rising urbanization, and increasing awareness regarding asset protection and digital locking technologies are contributing to regional market growth. |

|

East India |

10.5% |

Supported by expanding retail activity, jewelry trade, financial services, and improving commercial infrastructure. The region is witnessing gradual adoption of modern security storage systems across small businesses, banks, educational institutions, and residential applications. |

West and Central India's 38.6% market leadership is structurally cemented by the combination of India's financial capital, India's diamond capital, India's jewellery capital, and Maharashtra-Gujarat's combined industrial output, requiring cash management safe infrastructure.

South India's 28.4% reflects the region's gold consumption leadership, creating India's highest jewellery safe density. Kerala's unique gold loan banking model creates the country's highest per-branch vault security standard and procurement value. North India's 22.5% is anchored by government and PSU institutional procurement from Delhi, and Punjab-Haryana's industrial belt payroll safety requirements. East India's 10.5% represents the market's most significant growth opportunity through 2034 as the region's banking penetration improvement and Kolkata's jewellery sector expansion create new institutional demand foundations.

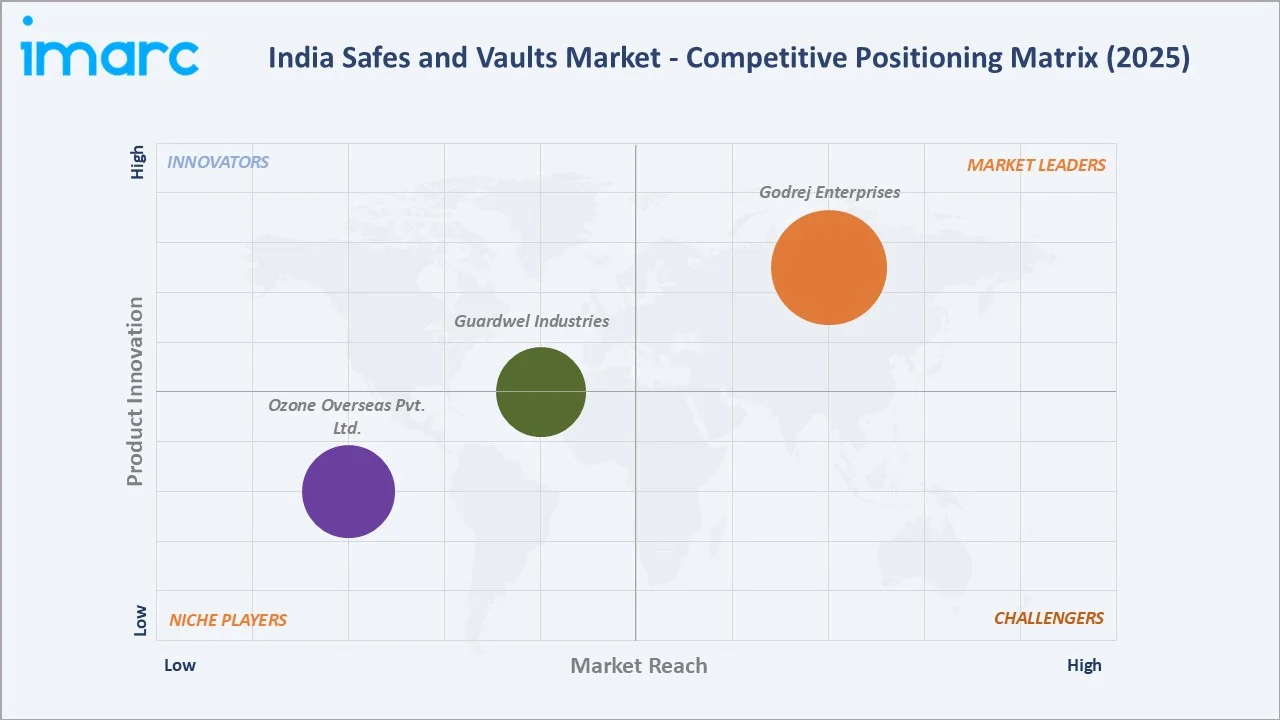

Competitive Landscape

India's safes and vaults market is moderately concentrated in the institutional banking segment while being fragmented in the residential and mid-commercial segments. This bifurcated structure reflects the institutional procurement channel's certification requirements, creating a protective competitive moat in the high-value banking segment, while the retail segment remains openly competitive.

|

Company Name |

Product Line |

Market Position |

Core Strength |

|

Godrej Enterprises |

Godrej Steel Fabricated Portable Strong Room (SFSR), Aurum Pro Royal, Secunex, Intelli- Access, Defender Prime Safes |

Market Leader |

Godrej safes offer high-quality products related to security, from a central safe deposit locker to a personal home vault. Built to superior, certified standards, Godrej provides extreme protection. |

|

Ozone Overseas Pvt. Ltd. |

Fingerprint Safes, Digital Safes, Manual Safes, Fire-resistant Safes, Anti-burglary Safes |

Niche Player |

Ozone is India’s leading architectural hardware manufacturer & supplier |

|

Guardwel Industries |

TRTL AAA CLASS, TRTL AA CLASS, TRTL A CLASS, TRTL BB CLASS, FBR C CLASS, GOLD LOAN SAFE |

Established Player |

With decades of experience in designing, manufacturing, and testing fire-resistant cabinets and TRTL-grade safes, Guardwel quickly emerged as a trusted name across India's financial and institutional sectors and beyond. |

The competitive landscape is being reshaped by three dynamics: technology differentiation (IoT-connected safes, biometric multi-factor authentication, AI vault room management) creating premium product tiers where global brands compete effectively against domestic incumbents; e-commerce channel democratization enabling new entrants to build viable businesses in the residential and SOHO segments without traditional dealer networks; and the potential regulatory certification for all safe categories that would structurally eliminate unorganized import competition, benefiting all certified domestic manufacturers.

Key Company Profiles

Godrej Enterprises

Godrej’s trusted brand heritage, spanning over a century, assures high-level security. The company’s safe vault and safe deposit locker solutions feature innovative, certified technology that withstands fire and burglary. Every Godrej purchase is supported by reliable, nationwide customer care, guaranteeing peace of mind and long-term asset protection.

- Product Portfolio: MX Portable Modular Strong Room Door, Aurum Pro Royal, Secunex, Intelli- Access, Defender Prime Safes.

- Recent Developments: In April 2025, Godrej Enterprises Group launched its latest range of premium technology-enabled home lockers, strengthening its position in Telangana’s expanding security solutions market. The company is focusing on increasing its presence across Hyderabad and other parts of Telangana by addressing the growing demand for advanced residential security and storage solutions.

- Strategic Focus: Expanding premium digital security solutions through smart safes, biometric lockers, institutional vault systems, and technology-enabled home security products.

Ozone Overseas Pvt. Ltd.

Ozone Overseas Pvt. Ltd. is a leading Indian manufacturer and supplier of architectural hardware, digital safes, locking systems, and security solutions with a strong presence across residential, commercial, hospitality, and institutional segments.

- Product Portfolio: Fingerprint Safes, Digital Safes, Manual Safes, Fire-resistant Safes, Anti-burglary Safes.

- Strategic Focus: Expanding technology-enabled security solutions through biometric safes, digital locking systems, smart access control, and premium residential and commercial security products.

Market Concentration Analysis

India's safes and vaults market exhibits a classic two-tier concentration structure: high concentration in the institutional banking segment alongside much lower concentration in the residential and small commercial segments. This bifurcation reflects the certification requirement barrier, creating a protected institutional market versus an openly competitive retail market.

The organized sector collectively accounts for approximately 60-65% of total India safe market revenues by value, with the remaining 35-40% captured by unorganized imports and uncertified domestic small manufacturers serving price-sensitive segments. Market concentration is expected to gradually increase in the banking segment, remain fragmented in residential, and consolidate in the premium commercial and vault room segments. International strategic acquisitions represent the most likely concentration event through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Non-banking sector (~6.6% CAGR), commercial application (~6.3% CAGR), gun safe sub-segment (~12-15% CAGR from Arms Act mandate), biometric safe technology (~18% CAGR within residential segment), and IoT-connected commercial safes (~20%+ CAGR from small base) represent India's highest-growth safe and vault investment vectors through 2034.

Emerging Market Opportunities

India's gold loan NBFC sector represents the most concentrated institutional vault replacement opportunity. Most gold loan branch vaults were installed in the 2010-2016 expansion era and are approaching their 10-15 year vault door replacement cycle.

Investment Themes

- Gold loan NBFC vault infrastructure upgrade program: Muthoot Finance and Manappuram Finance's branches operating with aging 2010-2016 era vault installations entering the replacement cycle represent an addressable procurement opportunity.

- Gun safe first-mover market development: India's licensed arms holders requiring certified gun safe storage represent an entirely new safe category that currently has minimal organized sector product coverage.

Future Market Outlook (2026-2034)

The India safes and vaults market is projected to grow from USD 205.2 Million in 2025 to USD 358.0 Million by 2034, delivering a 6.06% CAGR and 74% market expansion over the forecast period. The market's anchor value of USD 275.4 Million in 2030 represents a safes and vaults industry where smart technology integration has become the standard specification rather than a premium differentiator. The gun safe category has emerged as India's fastest-growing safe sub-segment, and the residential market's share has expanded, and awareness elevation drives premium in-home safe adoption comparable to other high-income Asian markets.

Three structural forces define India's safes and vaults market growth through 2034 with high confidence: the Indian banking sector's continuing branch expansion creating mandatory vault and safe procurement demand from new branch openings and the simultaneous 2010-2018 generation safe replacement cycle beginning from 2026; India's jewellery and precious metals industry formalization driving certified vault room procurement; and the smart safe technology transition creating average transaction value expansion of 30-50% as biometric, IoT, and AI-enabled products replace mechanical equivalents at premium price points, sustaining market revenue growth above unit volume growth throughout the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including VP Sales and Product Directors; procurement directors from State Bank of India, Punjab National Bank, and Bank of Baroda safe procurement departments; jewellery chain security managers from Tanishq, Malabar Gold, and PC Jeweller; Muthoot Finance and Manappuram Finance vault infrastructure managers; BIS safe certification division officers; insurance underwriters specifying safe requirements for commercial policy endorsements; and 30+ dealer and distributor network representatives across North, South, West, and East India.

Secondary Research

Secondary research encompassed BIS (Bureau of Indian Standards) IS:3655 standard documentation, IBA (Indian Banks' Association) Safe Deposit Locker Guidelines 2023, RBI Master Circular on Physical Security of Bank Premises, NCRB Crime in India Statistics (2024) for jewellery theft data, RBI Annual Report (bank branch statistics), MCA MSME sector data, IBEF India jewellery industry report 2025, GJEPC (Gem and Jewellery Export Promotion Council) annual statistics, company annual reports, GEM portal tender data for safe procurement, import trade data (DGFT HS code 8303 - armoured safes and strongboxes). Over 70 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up application and end-user models calibrated against BIS-certified manufacturer sales data, RBI branch expansion projections, IBA safe deposit locker installation statistics, GJEPC jewellery retail outlet count by state, and import data. Key inputs include the RBI five-year bank branch expansion projection, Arms Act 2024 compliance timeline and licensed arms holder count (Ministry of Home Affairs), India HNWI population growth projections, gold loan NBFC branch expansion plans (Muthoot Finance, Manappuram Finance investor presentations), and BIS QCO implementation timeline scenarios for organized market share projection.

India Safes and Vaults Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Electronic, Biometric, Mechanical |

| Function Types Covered | Cash Management Safes, Depository Safes, Gun Safes and Vaults, Vaults and Vault Doors, Media Safes, Others |

| Applications Covered | Residential, Commercial |

| End Users Covered | Banking Sector, Non Banking Sector |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Godrej Enterprises, Ozone Overseas Pvt. Ltd., Guardwel Industries, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India safes and vaults market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India safes and vaults market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India safes and vaults industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Safes and Vaults Market Report

The India safes and vaults market reached USD 205.2 Million in 2025, driven by bank branches requiring certified vault infrastructure, India's world-leading jewellery industry creating jewellery safe demand, PMLA compliance mandating certified physical document storage, rising precious metal theft incidents, and smart biometric safe technology adoption accelerating premium replacement cycles.

The market grows at 6.06% CAGR during 2026-2034, reaching USD 358.0 Million by 2034, driven by banking sector branch expansion, gun safe mandatory demand, gold loan NBFC vault replacement cycles, and smart biometric safe average transaction value expansion.

Commercial leads at 64.8%, driven by banking sector mandatory RBI physical security specifications, jewellery retail vault rooms, hospitality in-room safes, and corporate document vaults. Commercial grows at ~6.3% CAGR versus residential's ~5.6% CAGR as institutional procurement waves (branch expansion, locker room installations) sustain commercial volume growth.

The banking sector leads at 62.5% through branch vault and safe procurement, ATM safe cassettes, and RBI-mandated currency chest construction.

West and Central India leads at 38.6%, anchored by Mumbai's financial sector concentration, Gujarat's diamond industry vault demand, Maharashtra's jewellery retail density, and Rajasthan's gem and jewellery cluster requiring certified vault infrastructure.

Leading companies include Godrej Enterprises, Ozone Overseas Pvt. Ltd., and Guardwel Industries, among others.

The market is projected to reach approximately USD 275.4 Million by 2030, with regulations eliminating uncertified imports and expanding organized sector share, gun safe compliance reaching peak adoption, biometric safes becoming standard specification, and gold loan NBFC vault replacement cycles.

India's jewellery industry represents the single largest non-banking safe and vault market segment. Insurance company mandates, BIS Hallmarking point-of-care infrastructure, and organized retail expansion generate new certified vault room installations annually.

Biometric fingerprint safes have grown in India's residential safe units, with IoT-connected safes entering hotel, retail, and corporate segments. AI-powered vault room management creates premium service revenue per vault room installation, expanding revenue per relationship beyond hardware product values.

Three priority opportunities: BIS QCO readiness investment; gold loan NBFC vault replacement program targeting Muthoot-Manappuram combined branches; and gun safe first-mover category development through BIS-certified product launch and licensed arms dealer distribution network establishment capturing India's mandatory buyers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade