India Satellite Antenna Market Size, Share, Trends and Forecast by Frequency Band, Technology, Antenna Type, Platform, and Region, 2026-2034

India Satellite Antenna Market Summary:

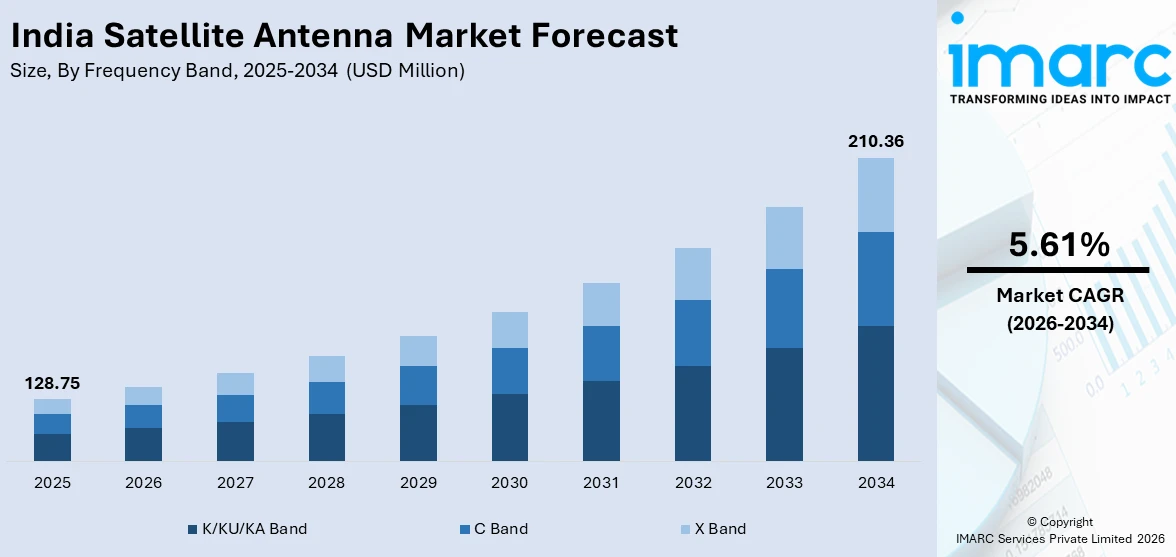

The India satellite antenna market size was valued at USD 128.75 Million in 2025 and is projected to reach USD 210.36 Million by 2034, growing at a compound annual growth rate of 5.61% from 2026 to 2034.

The India satellite antenna market is gaining significant momentum as the country accelerates its digital connectivity ambitions and strengthens space-based defense capabilities. Government-led reforms enabling private sector participation in satellite manufacturing, rising demand for broadband services in remote and underserved regions, and increasing investments in military communication infrastructure are reshaping the competitive landscape. Advancements in antenna technologies, expanding low Earth orbit satellite constellations, and the growing adoption of satellite-on-the-move solutions are contributing to the India satellite antenna market share.

Key Takeaways and Insights:

- By Frequency Band: K/KU/KA band represents the largest segment with a market share of 45% in 2025, driven by superior bandwidth capacity supporting high-throughput satellite broadband and advanced defense communications across the country.

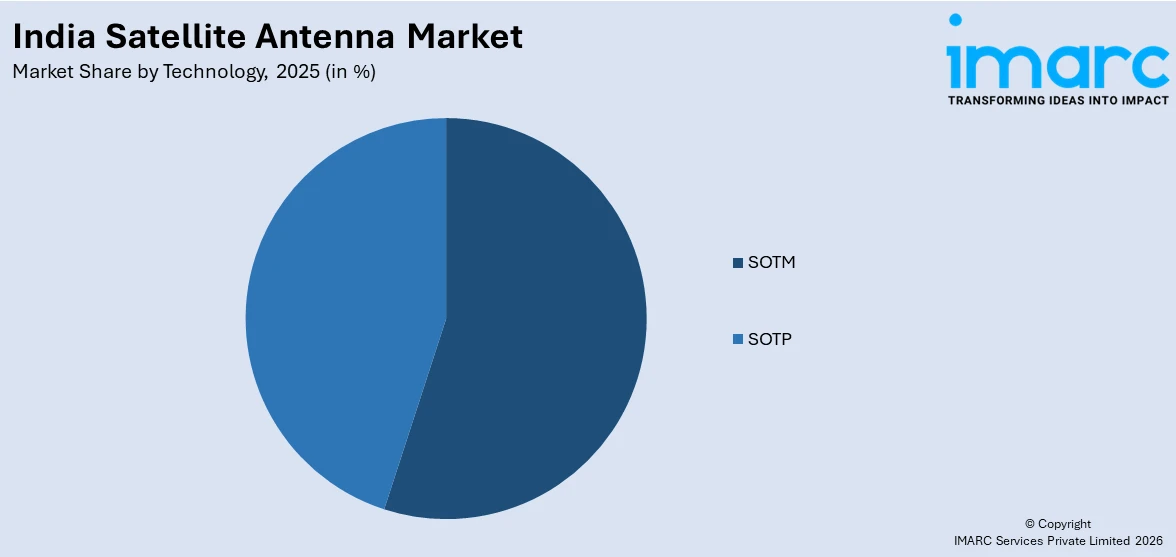

- By Technology: SOTM leads the market with a share of 53% in 2025, supported by the continuous high-speed communication for mobile military and commercial platforms across India.

- By Antenna Type: Flat panel antenna dominates the market with a share of 40% in 2025, owing to its compact design, electronic beam steering capability, and suitability for LEO satellite tracking applications.

- By Platform: Land fixed represents the largest segment with a market share of 25% in 2025, reflecting strong demand for permanent ground-based satellite communication infrastructure supporting broadcasting, telecommunications, and defense operations throughout India.

- Key Players: The India satellite antenna market exhibits strong competitive dynamics, with established global manufacturers competing alongside emerging domestic players, driving innovation in antenna design, multi-band compatibility, and indigenous manufacturing capabilities.

To get more information on this market Request Sample

India's satellite antenna market is experiencing transformative growth as the nation positions itself as a major hub for satellite communications and space technology. The rapid deployment of Low Earth Orbit satellite constellations is fundamentally changing connectivity paradigms, requiring advanced electronically steered antennas capable of tracking multiple fast-moving satellites simultaneously. India's Cabinet Committee on Security approved the Space Based Surveillance Phase-III program in October 2024 with an investment of approximately Rs 26,968 Crore for developing and launching 52 surveillance satellites, significantly driving demand for defense-grade satellite antenna systems. Government policies promoting indigenous manufacturing, including the Production Linked Incentive scheme for telecom equipment, are encouraging domestic production of critical antenna components such as feed horns, radomes, and radio frequency integrated circuit subsystems, strengthening supply chain resilience and reducing import dependency.

India Satellite Antenna Market Trends:

Rapid Expansion of LEO Satellite Broadband Ecosystem

The India satellite antenna market is experiencing significant transformation driven by the entry of multiple satellite broadband operators targeting the country's vast underserved population. The deployment of LEO satellite constellations is creating unprecedented demand for advanced flat panel and phased array antenna systems capable of electronically steering beams to track rapidly moving satellites at altitudes between 550 and 1,200 kilometers, ensuring uninterrupted high-speed connectivity across urban and rural regions.

Integration of Direct-to-Device Satellite Communication Technology

The emergence of direct-to-device satellite communication represents a groundbreaking trend reshaping India satellite antenna market growth. This technology enables standard smartphones and IoT devices to connect directly with orbiting satellites without specialized hardware, expanding the addressable market beyond traditional fixed and mobile satellite terminals. The development of non-terrestrial network standards and geostationary L-band satellite integration is opening new frontiers for satellite antenna miniaturization and mass-market deployment.

Growing Adoption of Multi-Band Defense Communication Systems

India's defense sector is increasingly investing in sophisticated multi-band satellite antenna systems that operate simultaneously across C, Ku, Ka, and X frequency bands. These advanced antenna platforms provide encrypted voice, data, and video transmission capabilities for naval vessels, military aircraft, and ground forces, enabling real-time coordination and enhanced situational awareness. The emphasis on indigenous development of defense-grade antenna solutions is accelerating technology transfer and domestic manufacturing capabilities.

Market Outlook 2026-2034:

The India satellite antenna market demonstrates notable growth potential, underpinned by irreversible trends, including government-led space sector liberalization, defense modernization programs, and rapidly growing demand for satellite broadband connectivity. The market generated a revenue of USD 128.75 Million in 2025 and is projected to reach a revenue of USD 210.36 Million by 2034, growing at a compound annual growth rate of 5.61% from 2026-2034. The convergence of advanced antenna technologies, expanding LEO and GEO satellite deployments, and increasing private sector participation in indigenous satellite manufacturing will continue driving revenue growth across frequency bands, platforms, and application domains throughout the forecast period.

India Satellite Antenna Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Frequency Band |

K/KU/KA Band |

45% |

|

Technology |

SOTM |

53% |

|

Antenna Type |

Flat Panel Antenna |

40% |

|

Platform |

Land Fixed |

25% |

Frequency Band Insights:

- C Band

- K/KU/KA Band

- X Band

K/KU/KA band dominates with a market share of 45% of the total India satellite antenna market in 2025.

K/KU/KA band leads the market due to its wide adoption in broadcasting, broadband connectivity, and defense communication applications. This higher frequency band supports greater bandwidth capacity and faster data transmission, making it suitable for high-definition television, direct to home services, and enterprise data networks. With the rising demand for high-speed internet in remote and rural areas, service providers increasingly deploy KU and KA band satellite systems. Its ability to deliver reliable connectivity across challenging terrains strengthens its position in commercial and government projects.

Another key reason for the dominance of K/KU/KA band is the expansion of satellite based broadband and mobility services across aviation, maritime, and disaster management sectors. This frequency band enables smaller antenna sizes and higher throughput, which reduces installation complexity and improves operational efficiency. Indian space initiatives and private satellite operators are also investing in high throughput satellites that primarily operate in KU and KA frequencies. The growing defense modernization programs and secure communication requirements further accelerate adoption, reinforcing the leadership of this frequency band in the market.

Technology Insights:

Access the comprehensive market breakdown Request Sample

- SOTM

- SOTP

SOTM leads with a market share of 53% of the total India satellite antenna market in 2025.

SOTM represents the largest segment owing to the growing need for uninterrupted connectivity in mobile environments. This technology enables satellite communication while vehicles, ships, or aircraft are in motion, making it highly valuable for defense operations, emergency response, and transportation sectors. With increasing demand for real time data transfer, surveillance, and secure communication, SOTM antenna is widely adopted across government and commercial applications. Its ability to maintain stable links without signal disruption gives it a strong advantage over fixed systems.

Another major driver is the rapid expansion of mobility-based satellite services in India, including connected vehicles, maritime broadband, and airborne communication networks. SOTM antenna supports advanced tracking and automatic beam steering, ensuring reliable performance even in challenging conditions. Defense modernization and border security initiatives also boost the demand, as armed forces require robust communication systems during movement. Additionally, the rise of private satellite operators and high throughput satellite deployments further supports SOTM adoption, making it a leading technology segment in the market.

Antenna Type Insights:

- Flat Panel Antenna

- Parabolic Reflector Antenna

- Horn Antenna

Flat panel antenna exhibits a clear dominance with a 40% share of the total India satellite antenna market in 2025.

Flat panel antenna dominates the market attributed to its compact design, lightweight structure, and ability to deliver high performance connectivity. Unlike traditional parabolic antennas, flat panel system is easier to install and integrate into modern platforms such as vehicles, aircraft, and maritime vessels. Its low profile makes it suitable for mobility-based applications where space and aerodynamics are critical. With rising demand for broadband satellite services, defense communication, and in-flight connectivity, flat panel antenna is gaining strong traction across commercial and government sectors in India.

Another reason for its dominance is the technological advancement in electronically steered flat panel antenna, which provides faster beam switching and improved signal reliability. This antenna supports seamless connectivity for satellite on the move systems, making it ideal for defense, disaster response, and remote connectivity projects. Indian telecom operators and satellite service providers are also adopting flat panel solution to expand high speed coverage in underserved regions. Additionally, increasing investments in next generation satellite networks and high throughput satellites further strengthen the demand for flat panel antenna nationwide.

Platform Insights:

- Land Fixed

- Land Mobile

- Airborne

- Maritime

- Space

Land fixed dominates with a market share of 25% of the total India satellite antenna market in 2025.

Land fixed holds the biggest market share driven by the extensive use in telecommunications, broadcasting, and government communication infrastructure. Fixed land based satellite antenna is widely deployed for direct to home services, broadband backhaul, and enterprise connectivity, especially in areas with limited terrestrial network reach. Its stable installation ensures consistent signal strength and high reliability, making it preferred for long term communication needs. With increasing demand for rural connectivity and digital inclusion initiatives, land fixed satellite continues to see strong adoption across India’s commercial and public sectors.

Another key driver is the growing role of land fixed antenna in defense networks, disaster management, and critical communication systems. These platforms support secure and uninterrupted connectivity for command centers, surveillance operations, and emergency response coordination. Land based installation is also more cost effective compared to mobile platforms, requiring lower maintenance and offering higher durability. Additionally, the expansion of satellite broadband services and the development of high throughput satellite infrastructure further boost the demand for fixed ground stations, reinforcing their dominance in the market.

Regional Insights:

- North India

- South India

- East India

- West India

North India holds a significant share in the market attributed to strong defense presence, border surveillance requirements, and a high concentration of government communication projects. The region hosts key military installations and strategic infrastructure, increasing demand for secure satellite systems. In addition, the growing broadcasting networks and expanding enterprise connectivity across Delhi NCR, Punjab, and Haryana support the market growth.

South India is a major growth hub driven by its strong space and technology ecosystem. With ISRO facilities and several aerospace and defense companies located in Karnataka, Tamil Nadu, and Telangana, the region supports advanced satellite communication development. Rising IT parks, maritime activities, and demand for broadband connectivity in semi urban areas further contribute to increased adoption of satellite antennas.

East India shows gradual growth in the satellite antenna market due to increasing rural connectivity initiatives and disaster management requirements. States, such as West Bengal and Odisha, rely on satellite systems for emergency communication during cyclones and floods. Expanding telecom infrastructure and government backed digital programs are improving satellite adoption, particularly in remote and geographically challenging areas.

West India is a crucial segment in the market, supported by strong industrial activity and major port operations in Maharashtra and Gujarat. The region benefits from high demand for maritime communication, enterprise networks, and broadcasting services. Presence of large telecom operators and private satellite service providers also strengthens the market. Continuous infrastructure development and smart city projects further drive satellite antenna installations.

Market Dynamics:

Growth Drivers:

Why is the India Satellite Antenna Market Growing?

Government Space Sector Liberalization Catalyzing Private Investment

India's satellite antenna market is experiencing accelerated growth driven by comprehensive government reforms that have fundamentally transformed the space sector from a predominantly state-controlled domain into an open ecosystem welcoming private enterprise. The Indian Space Policy 2023 and subsequent implementation guidelines have established clear authorization frameworks for non-governmental entities to participate in satellite manufacturing, launch services, and ground segment operations. These policy reforms, combined with the Make in India initiative and Production Linked Incentive schemes for telecom equipment manufacturing, are encouraging domestic production of critical satellite antenna components. The government's decision to allow up to hundred percent foreign direct investment in various space sector segments through automatic and government approval routes has further liberalized entry norms, attracting global antenna manufacturers and technology providers to establish manufacturing and research facilities in India.

Massive Defense Modernization Driving Demand for Military-Grade Antenna Systems

National security imperatives are creating substantial demand for sophisticated satellite antenna systems designed to support secure, reliable military communications across India's vast territorial and maritime domains. The Indian Armed Forces are undergoing significant modernization of their space-based surveillance and communication capabilities, recognizing the critical role of satellite technology in modern warfare and strategic intelligence gathering. India's Cabinet Committee on Security approved the Space Based Surveillance Phase-III program in October 2024 with an investment of approximately Rs 26,968 Crore for deploying 52 defense satellites equipped with AI-driven analytics and synthetic aperture radar systems. This program requires extensive ground-based antenna infrastructure for satellite command, control, data reception, and processing, creating sustained demand for defense-grade antenna solutions across multiple frequency bands and operational environments.

Expanding Satellite Broadband Ecosystem Creating New Demand Verticals

The entry of multiple satellite broadband operators into India's telecommunications market is generating unprecedented demand for consumer and enterprise satellite antenna terminals. India's massive population of over 1.4 Billion people, with approximately 41 percent still lacking reliable internet access, presents an enormous addressable market for satellite-based connectivity solutions. The regulatory framework enabling satellite internet services has attracted global and domestic operators, with three companies receiving full licensing authorization and more than ten satellite operators expressing interest in Indian operations as of April 2025. In July 2025, Hyderabad-based Ananth Technologies received regulatory approval from IN-SPACe to become India's first private company to offer satellite communication services using a domestically-built satellite, with plans to deploy a four-tonne geostationary communication satellite delivering up to 100 Gbps data capacity with an initial investment of Rs 3,000 Crore.

Market Restraints:

What Challenges the India Satellite Antenna Market is Facing?

High Equipment Costs Limiting Broader Market Adoption

The significant capital expenditure required for advanced satellite antenna systems, particularly electronically steered phased array and flat panel technologies, continues to constrain market penetration among price-sensitive user segments and smaller enterprises. Sophisticated multi-band antenna systems incorporating advanced beam-forming capabilities and high-quality RF components carry substantial procurement and installation costs that remain prohibitive for mass-market deployment in developing regions.

Regulatory and Spectrum Allocation Complexities

The evolving regulatory landscape surrounding satellite communications in India creates uncertainty for antenna system manufacturers and service providers. Ongoing deliberations regarding spectrum allocation methodologies, security compliance requirements, and gateway authorization procedures introduce delays in commercial deployment timelines. Multiple regulatory approvals from different agencies are required before operators can launch services, adding complexity and timeline uncertainty.

Signal Attenuation and Atmospheric Interference Challenges

Higher frequency bands, particularly Ka and Ku bands, experience significant signal degradation during heavy rainfall events prevalent across tropical and monsoon-affected regions of India. Rain fade attenuation can exceed several decibels during intense precipitation, forcing operators to implement costly mitigation strategies, including adaptive coding modulation, site diversity configurations, and dual-band terminal architectures, that increase system complexity and operational expenditure.

Competitive Landscape:

The India satellite antenna market exhibits intensifying competition as global technology leaders establish manufacturing and service capabilities alongside emerging domestic enterprises. Market dynamics reflect strategic positioning across diverse application segments, with players competing on antenna performance, multi-band compatibility, electronic beam steering capabilities, and cost-effectiveness. The competitive landscape is increasingly shaped by indigenous manufacturing initiatives, partnerships between international antenna suppliers and Indian defense contractors, and the growing investment in R&D for next-generation phased array technologies. The government's emphasis on self-reliance in space and defense technologies is creating opportunities for domestic manufacturers to capture market share through localized production of critical antenna components and systems.

Recent Developments:

- In July 2025, Hyderabad-based Ananth Technologies received regulatory approval from IN-SPACe to become India's first private company to offer satellite communication services using a domestically-built satellite. The company plans to deploy a four-tonne geostationary communication satellite with data capacity of up to 100 Gbps, with commercial services expected to begin in 2028, backed by an initial investment of Rs 3,000 Crore.

- In July 2025, Starlink received final regulatory clearance from the Indian National Space Promotion and Authorization Centre to operate its LEO satellite constellation in India, utilizing Ka and Ku frequency bands. This approval positioned Starlink as the third satellite internet provider fully licensed in India, alongside Eutelsat OneWeb and Jio Satellite Communications, with commercial services expected by early 2026.

- In November 2024, BSNL, in partnership with California-based Viasat, launched India's first Direct-to-Device satellite connectivity service. The service utilized non-terrestrial network technology through geostationary L-band satellites positioned 36,000 kilometers above Earth, enabling emergency calls, SOS messaging, and UPI payments in remote areas where cellular networks are unavailable.

India Satellite Antenna Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Frequency Bands Covered | C Band, K/KU/KA Band, X Band |

| Technologies Covered | SOTM, SOTP |

| Antenna Types Covered | Flat Panel Antenna, Parabolic Reflector Antenna, Horn Antenna |

| Platforms Covered | Land Fixed, Land Mobile, Airborne, Maritime, Space |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Satellite Antenna Market Report

The India satellite antenna market size was valued at USD 128.75 Million in 2025.

The India satellite antenna market is expected to grow at a compound annual growth rate of 5.61% from 2026-2034 to reach USD 210.36 Million by 2034.

The K/KU/KA band dominates the market with a revenue share of 45% in 2025, driven by superior bandwidth capacity supporting high-throughput satellite broadband, direct-to-home television, and advanced military communication applications.

Key factors driving the India satellite antenna market include the entry of satellite broadband operators targeting underserved regions and the deployment of LEO constellations. This increases demand for advanced flat-panel and phased-array antennas, like those used by Starlink, to ensure high-speed connectivity in urban and rural areas.

Major challenges include high equipment costs for advanced phased array antenna systems, regulatory complexities surrounding spectrum allocation and gateway authorizations, signal attenuation during heavy rainfall affecting higher frequency bands, and dependency on imported RF components and semiconductor chipsets for antenna manufacturing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)