India Satellite Communication (SATCOM) Market Size, Share, Trends and Forecast by Component, Application, End Use Industry, and Region, 2026-2034

India Satellite Communication (SATCOM) Market Summary:

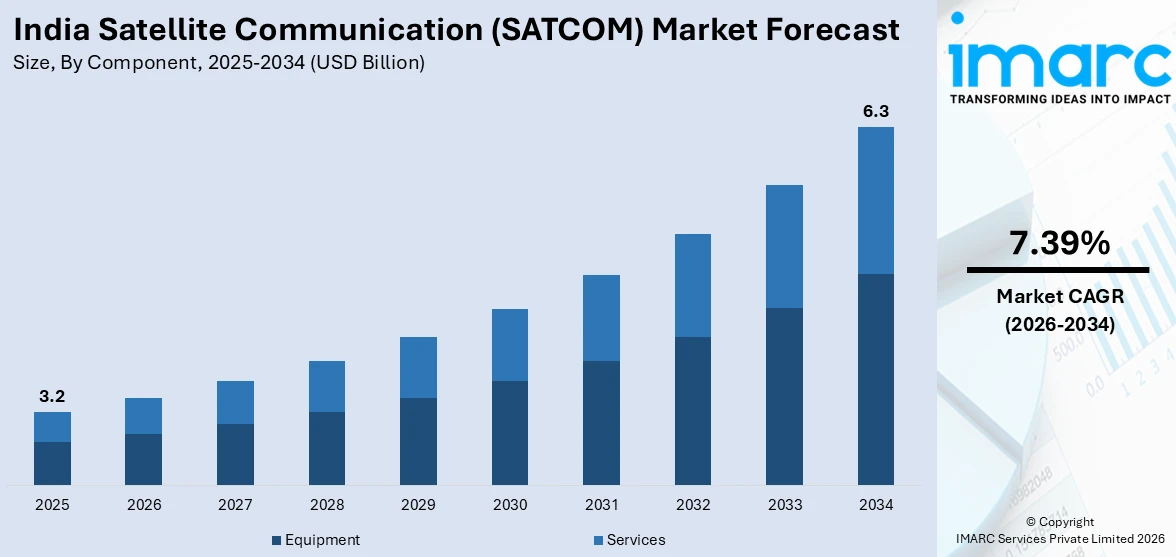

The India satellite communication (SATCOM) market size was valued at USD 3.2 Billion in 2025 and is projected to reach USD 6.3 Billion by 2034, growing at a compound annual growth rate of 7.39% during 2026-2034.

The India satellite communication (SATCOM) market is driven by rising demand for reliable connectivity across remote and rural areas, expansion of broadcasting services, and increasing use of satellite networks for defense, navigation, and disaster management. The growing adoption of satellite-based broadband, expansion of digital communication infrastructure, and advancements in space technology are also influencing the market. Additionally, government initiatives promoting space sector development and private participation in satellite services are further strengthening the expansion of SATCOM applications across multiple industries.

Key Takeaways and Insights:

- By Component: Equipment leads the market with a share of 61.3% in 2025, driven by the widespread deployment of transmitters, transponders, antennas, transceivers, and receivers across broadcasting, defense, and broadband satellite communication networks nationwide.

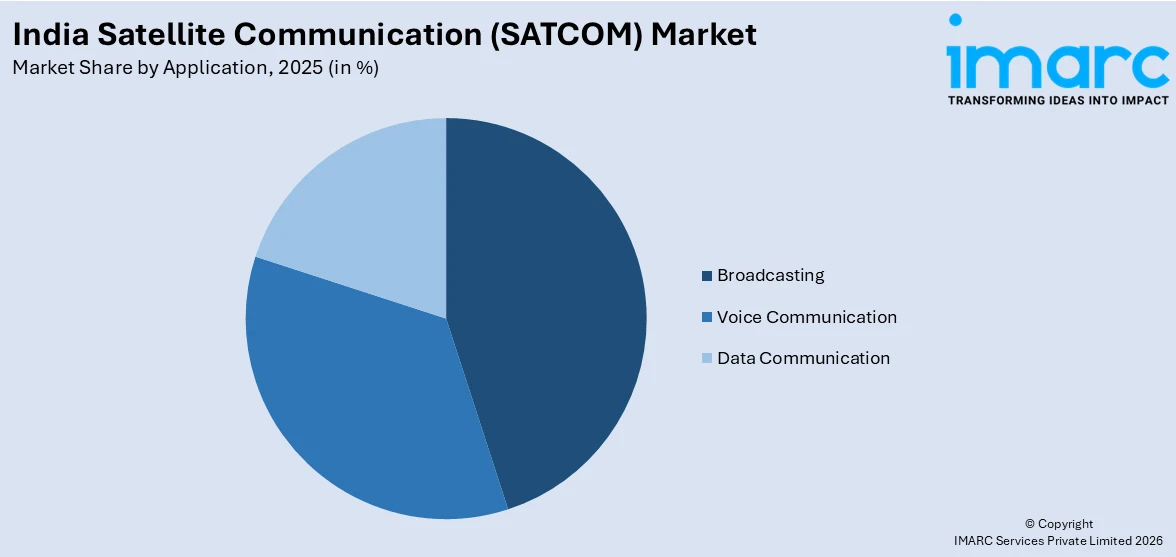

- By Application: Broadcasting dominates the market with a share of 39.7% in 2025, underpinned by India's expansive direct-to-home television ecosystem and the dependence of national and regional channels on satellite transponder capacity for content distribution.

- By End Use Industry: Media and entertainment represent the largest segment with a market share of 34.5% in 2025, reflecting satellite communication's foundational role in supporting India's expansive television broadcasting, digital content distribution, and live event transmission infrastructure.

- By Region: South India leads the market with a share of 32.8% in 2025, owing to the concentration of ISRO headquarters, Satish Dhawan Space Centre, and private aerospace technology firms in Karnataka, Tamil Nadu, and Andhra Pradesh.

- Key Players: The India satellite communication (SATCOM) market is moderately consolidated, featuring government-linked entities alongside domestic private operators and international satellite service providers competing across equipment manufacturing, satellite services, and broadband connectivity segments.

To get more information on this market Request Sample

The India satellite communication (SATCOM) market stands at the intersection of technological evolution and national development imperatives, making it one of the most strategically significant sectors in the country's digital economy. Rising demand for reliable connectivity across remote and underserved regions, expansion of digital services, and increasing dependence on satellite networks for broadcasting, navigation, defense, and disaster management are key factors driving the market. Government initiatives encouraging private sector participation and investment in space technology are also strengthening the development of satellite communication infrastructure. Reflecting the growing technological momentum, in 2026, Starlink announced plans to launch Direct-to-Cell satellites by 2027 to support mobile connectivity services, including in India. The system will enable users to connect directly to satellites using standard smartphones for voice calls, SMS, and data services, supported by a network of about 1,200 low-Earth orbit satellites, further expanding satellite-based communication capabilities.

India Satellite Communication (SATCOM) Market Trends:

Rise of Satellite Connectivity for Rural Digital Inclusion

The expansion of satellite communication infrastructure to support digital connectivity in remote and underserved regions is emerging as a major trend in the India SATCOM market. Satellite technology is increasingly viewed as an effective solution for extending broadband services to geographically challenging areas where terrestrial networks are difficult to deploy. Strengthening satellite connectivity enables improved access to digital services, education, healthcare, and government programs in rural communities. In 2025, the Government of India launched the SATCOM Summit during India Mobile Congress to accelerate satellite-based connectivity initiatives. The program included plans to connect more than 38,000 remote villages using satellite networks while also investing heavily in national communication infrastructure and monitoring capabilities, reflecting the growing role of satellite technology in bridging the digital connectivity gap.

Advancement of Direct-to-Device Satellite Broadband Technologies

The development of satellite systems capable of connecting directly to standard mobile devices is becoming a key technological trend shaping the India SATCOM market. Direct-to-device satellite broadband solutions eliminate the need for specialized satellite receivers, allowing users to access communication services through conventional smartphones. This innovation significantly expands connectivity options for users located in remote regions or areas with limited terrestrial network coverage. In 2025, ISRO launched the BlueBird-6 commercial communication satellite designed to support space-based cellular broadband services capable of connecting directly with smartphones. The mission highlighted India’s growing capabilities in advanced satellite launch services while supporting the global expansion of satellite-enabled mobile communication technologies.

Strengthening Defense Communication through Dedicated Satellites

The increasing deployment of specialized communication satellites for defense and security applications is bolstering the growth of the India SATCOM market. Military operations require secure, reliable, and real-time communication systems capable of supporting complex operations across air, land, and maritime environments. Satellite communication networks play a critical role in ensuring uninterrupted communication between defense assets operating across vast geographic areas. In 2025, ISRO launched the GSAT-7R communication satellite to enhance the Indian Navy’s satellite-based communication network. The system provided secure connectivity for naval ships, submarines, aircraft, and operational command centers, demonstrating the growing importance of satellite communication infrastructure in strengthening national defense and maritime security capabilities.

Market Outlook 2026-2034:

The India satellite communication (SATCOM) market is set for consistent revenue growth throughout the forecast period owing to the expanding demand for broadband connectivity, increasing deployment of satellite-based communication services, and the growing applications across sectors, such as broadcasting, defense, navigation, and disaster management. The market generated a revenue of USD 3.2 Billion in 2025 and is projected to reach a revenue of USD 6.3 Billion by 2034, growing at a compound annual growth rate of 7.39% from 2026-2034. In addition, the need to provide reliable connectivity in remote and underserved regions is encouraging the development of advanced satellite communication networks across India.

India Satellite Communication (SATCOM) Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Equipment |

61.3% |

|

Application |

Broadcasting |

39.7% |

|

End Use Industry |

Media and Entertainment |

34.5% |

|

Region |

South India |

32.8% |

Component Insights:

- Equipment

- Transmitter/Transponder

- Antenna

- Transceiver

- Receiver

- Others

- Services

Equipment dominates with a market share of 61.3% of the total India satellite communication (SATCOM) market in 2025.

Equipment represents the largest segment driven by the crucial function of hardware systems in facilitating satellite-based communication networks. SATCOM equipment comprises antennas, transponders, receivers, transmitters, modems, and ground station infrastructure necessary for establishing and sustaining communication links between satellites and terrestrial networks. These elements create the physical framework of satellite communication systems, facilitating applications like broadcasting, broadband access, defense communications, and remote data transmission. With the expansion of satellite services in various sectors, the need for dependable and high-performance communication devices remains on the rise. The setup of ground terminals, satellite dishes, and networking equipment is essential for maintaining reliable signal transmission and effective operations.

The swift growth of satellite-driven broadband services, broadcasting systems, and governmental communication networks is intensifying the need for SATCOM equipment in India. Telecom firms, media broadcasters, defense organizations, and remote connectivity providers depend significantly on sophisticated satellite technology to facilitate data transfer and network functions. Devices like high-frequency antennas, signal processing units, and ground station systems facilitate secure and rapid communication over extended distances. Ongoing progress in satellite technology is also propelling the creation of more efficient and compact communication devices. These advancements enhance signal dependability, bandwidth capacity, and network efficiency, strengthening the dominant position of equipment in the market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Voice Communication

- Broadcasting

- Data Communication

Broadcasting leads with a market share of 39.7% of the total India satellite communication (SATCOM) market in 2025.

Broadcasting holds the biggest market share because of the widespread implementation of satellite networks for transmitting television signals and distributing content across the nation. Satellite communication allows broadcasters to transmit television channels over extensive geographic regions, providing continuous coverage in both urban and isolated areas. Satellite systems play a crucial role in direct-to-home television services by delivering high-quality video signals to millions of homes. Broadcasting firms utilize satellite systems to transmit news, entertainment shows, and local content to cable providers and television networks at the same time. Satellites offer extensive coverage and dependable signal transmission, making them crucial for extensive broadcasting activities throughout India.

The increasing need for varied television programming and high-definition broadcasting services enhances the importance of satellite communication in broadcasting. Media organizations are progressively depending on satellite bandwidth to transmit superior audio and video signals across various channels and broadcasting platforms. Satellite networks additionally facilitate live event broadcasting, encompassing sports competitions, political gatherings, and entertainment shows that necessitate immediate transmission. Moreover, broadcasters utilize satellite communication to connect with audiences in rural and difficult geographical areas where land-based networks might be restricted. Ongoing increases in television audiences and digital broadcasting services further cement broadcasting as the top application in the industry.

End Use Industry Insights:

- Aerospace and Defense

- Transportation and Logistics

- Agriculture

- Government and Military

- Media and Entertainment

- Others

Media and entertainment exhibit a clear dominance with a 34.5% share of the total India satellite communication (SATCOM) market in 2025.

Media and entertainment dominate the market owing to the extensive reliance on satellite infrastructure for television broadcasting and content distribution. Satellite communication allows broadcasters to send television signals over extensive geographic regions, guaranteeing consistent access to channels in urban and remote locales. Direct-to-home television services, live event streaming, and news broadcasting rely significantly on satellite networks for consistent signal transmission. Media firms utilize satellite systems to deliver high-quality video content to various broadcasting stations and cable networks at the same time. The increasing demand for varied television content and extensive broadcasting coverage is continually propelling the use of satellite communication technologies in the media and entertainment sector.

The growth of digital broadcasting services and the increasing the demand for high-definition and ultra-high-definition content are enhancing the significance of satellite communication in the media and entertainment industry. Broadcasters need reliable satellite bandwidth to transmit high-quality video signals and handle substantial amounts of multimedia data throughout networks. Satellite communication enables live broadcasting of sports events, entertainment shows, and news coverage from various sites. Moreover, media organizations employ satellite networks to connect with audiences in isolated or geographically difficult regions where ground communication infrastructure is scarce. Ongoing increases in television audience numbers and digital content distribution further strengthen the dominant role of media and entertainment in the marketplace.

Regional Insights:

- North India

- South India

- East India

- West India

South India dominates with a market share of 32.8% of the total India satellite communication (SATCOM) market in 2025.

South India leads the market in terms of region due to the strong presence of space research institutions, technology companies, and advanced communication infrastructure. The region hosts major space and satellite research facilities, including key centers involved in satellite development, launch operations, and space technology innovation. Cities, such as Bengaluru and Hyderabad, serve as major hubs for aerospace companies, satellite equipment manufacturers, and technology startups working on satellite communication solutions. These organizations actively contribute to the development of satellite systems, ground infrastructure, and communication technologies. The concentration of skilled professionals and research organizations further strengthens the region’s role in satellite communication advancement.

In addition, South India benefits from a well-developed technology ecosystem and strong government and private sector investment in space and communication technologies. Several global aerospace firms, satellite service providers, and defense technology companies operate major facilities in the region. The presence of advanced research universities, innovation centers, and satellite technology laboratories supports continuous development of new communication solutions. The growing demand for satellite-based broadband, remote connectivity, broadcasting services, and defense communication systems is encouraging further expansion of SATCOM infrastructure. With strong technical expertise, established space research capabilities, and expanding commercial satellite services, South India continues to maintain a leading position in the market.

Market Dynamics:

Growth Drivers:

Why is the India Satellite Communication (SATCOM) Market Growing?

Rise of Private Sector Participation in Satellite Broadband Services

The growing participation of private companies in satellite communication services is transforming the structure of the India SATCOM market. Regulatory reforms and supportive policies are encouraging private enterprises to develop satellite infrastructure and launch commercial broadband services. Increased private investment supports innovation, expands service coverage, and enhances competition within the satellite communication ecosystem. In 2025, Ananth Technologies received regulatory approval to deploy India’s first private satellite broadband service using a domestically built communication satellite. The project involves significant investment in a high-capacity geostationary satellite designed to deliver broadband services nationwide, reflecting the growing role of private sector players in expanding India’s satellite-based connectivity landscape.

Expansion of Low-Earth-Orbit Satellite Networks

The rising development of low-Earth-orbit satellite networks is emerging as an important factor impelling of the India SATCOM market growth. These satellite systems operate closer to the Earth than traditional geostationary satellites, enabling lower latency communication and faster data transmission. Such capabilities make them highly suitable for broadband connectivity, mobile communication, and real-time digital services. The deployment of large satellite constellations improves network coverage and supports reliable connectivity across wide geographic areas. As communication providers seek to enhance service performance and coverage, low-Earth-orbit satellite systems are becoming an important technological solution for delivering high-speed satellite communication services across diverse regions of India.

Increasing Demand for Satellite Connectivity in Disaster Management

Satellite communication is playing an increasingly important role in disaster management and emergency response systems, contributing to the growth of the India SATCOM market. Natural disasters often disrupt terrestrial communication infrastructure, making satellite networks essential for maintaining connectivity during emergencies. Satellite communication enables rapid coordination between government agencies, emergency responders, and relief organizations in affected regions. Reliable communication networks help authorities monitor disaster conditions, coordinate rescue operations, and distribute emergency assistance efficiently. As governments strengthen disaster preparedness strategies, the integration of satellite communication systems into national emergency response frameworks continues to expand, supporting improved communication resilience during natural and humanitarian crises.

Market Restraints:

What Challenges the India Satellite Communication (SATCOM) Market is Facing?

High Capital Expenditure Requirements Limiting Domestic Manufacturer Scale:

The satellite communication industry demands enormous upfront investment in satellite manufacturing, launch services, ground infrastructure, and licensed spectrum, creating significant financial barriers for domestic players. Smaller Indian manufacturers and service providers face challenges in achieving economies of scale comparable to established international operators, limiting competitive participation in hardware supply chains and creating dependence on imported satellite components and subsystems for key mission requirements.

Regulatory Complexity and Spectrum Allocation Uncertainty Slowing Deployments:

The multi-layered regulatory environment governing India's SATCOM sector, involving the Department of Telecommunications, IN-SPACe, TRAI, and the Department of Space, introduces procedural complexity and extended timelines that can delay commercial deployment. Spectrum pricing and allocation frameworks remain under finalization, creating planning uncertainty for operators seeking to execute network rollout strategies and commit to multi-year capital investment programs.

Geographic and Infrastructure Challenges in Remote Connectivity Deployment:

India's vast and diverse terrain presents formidable operational challenges for satellite ground infrastructure deployment, particularly in high-altitude, island, and conflict-prone border regions. Installing and maintaining gateway stations, VSAT terminals, and associated power infrastructure in such environments involves elevated operational costs and logistical complexity, slowing the pace of coverage expansion in the geographically underserved areas that are paradoxically most in need of satellite-based connectivity solutions.

Competitive Landscape:

Key players in the SATCOM market are focusing on expanding satellite infrastructure, developing advanced communication technologies, and strengthening service capabilities to support the growing connectivity demand. Companies are investing in high-throughput satellites, ground station networks, and integrated communication systems to improve bandwidth capacity and transmission efficiency. Strategic partnerships with telecom operators, government agencies, and technology firms are also becoming common to expand service coverage and accelerate network deployment. Market participants are working on enhancing satellite manufacturing capabilities, improving launch services, and integrating satellite networks with terrestrial communication systems. In addition, companies are prioritizing innovation in areas such as low-earth-orbit satellite constellations, data security solutions, and real-time communication technologies to deliver more reliable and scalable satellite communication services.

Recent Developments:

- January 2026: Viasat and BSNL announced a strategic partnership to strengthen the Indian Navy’s satellite communication (SATCOM) capabilities. The collaboration will integrate Viasat’s Ka-band satellites and L-band infrastructure with BSNL’s gateway earth stations to provide secure, resilient connectivity for naval platforms. The initiative supports the Navy’s multi-band, multi-constellation SATCOM strategy and enhances maritime communication infrastructure.

- December 2025: The Government of India stated that satellite communication services by players, such as Starlink, OneWeb, and Jio Satellite, will launch only after meeting mandatory security clearances and spectrum allocation requirements. The Department of Telecommunications was finalizing spectrum pricing before granting commercial rollout approvals. Once compliance is completed, satcom services are expected to expand connectivity across India.

- October 2025: India highlighted a major push toward expanding its satellite communication ecosystem during the Satcom Summit at India Mobile Congress 2025 in New Delhi. Government leaders and industry stakeholders emphasized public-private partnerships and international collaboration to accelerate satellite-based connectivity and bridge the digital divide. The initiative aimed to strengthen next-generation communication infrastructure and support nationwide digital inclusion through advanced satellite technologies.

India Satellite Communication (SATCOM) Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Applications Covered | Voice Communication, Broadcasting, Data Communication |

| End Use Industries Covered | Aerospace and Defense, Transportation, Logistics, Agriculture, Government, Military, Media, Entertainment, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Satellite Communication (SATCOM) Market Report

The India satellite communication (SATCOM) market size was valued at USD 3.2 Billion in 2025.

The India satellite communication (SATCOM) market is expected to grow at a compound annual growth rate of 7.39% during 2026-2034 to reach USD 6.3 Billion by 2034.

Equipment dominates with 61.3% revenue share in 2025, driven by widespread deployment of satellite hardware including transmitters, transponders, antennas, and receiver systems across broadcasting, defense, and broadband connectivity applications.

Key factors driving the India satellite communication SATCOM market include expansion of satellite connectivity to improve digital access in remote and underserved regions. For instance, in 2025 the Government of India announced plans to connect over 38,000 remote villages through satellite networks under national connectivity initiatives.

Major challenges include high capital expenditure requirements for satellite manufacturing and ground infrastructure limiting domestic player scale, multi-agency regulatory complexity creating deployment uncertainty, and logistical difficulties in deploying and maintaining satellite infrastructure across India's geographically diverse and remote terrain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)