India School Stationery Supplies Market Size, Share, Trends and Forecast by Product, End User, Distribution Channel, and Region, 2026-2034

India School Stationery Supplies Market Size, Share, Trends & Forecast (2026-2034)

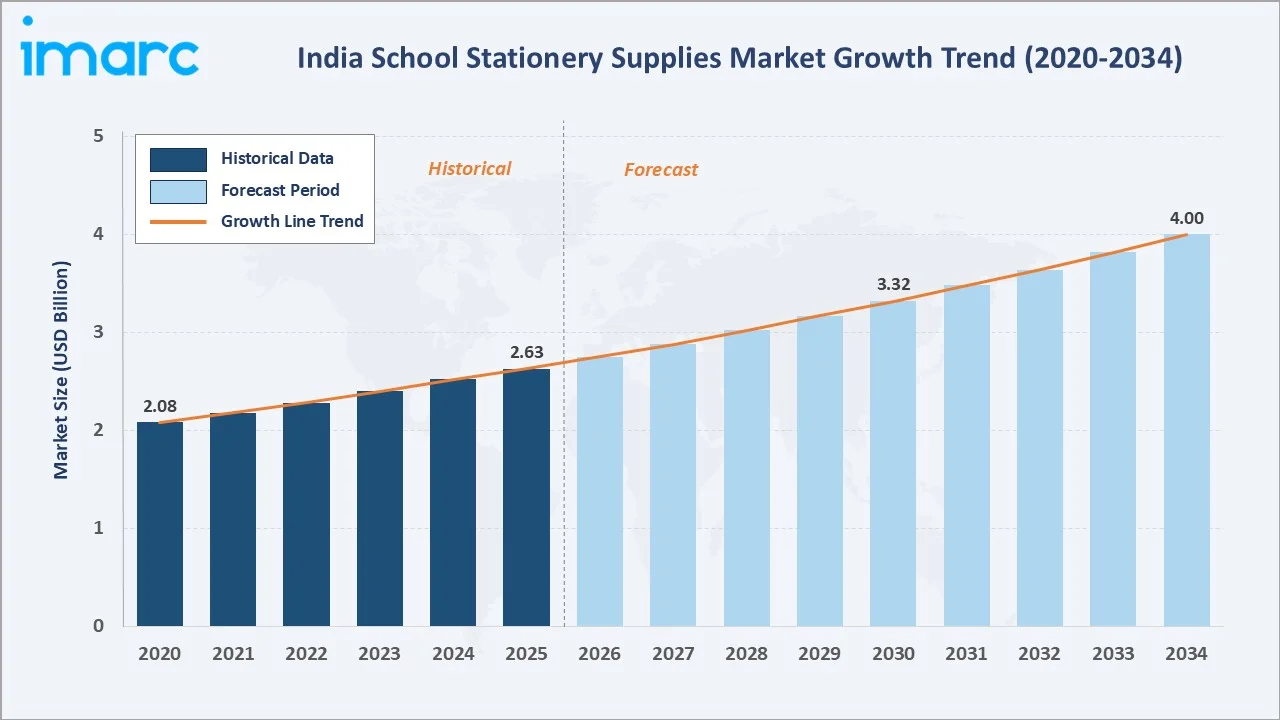

The India school stationery supplies market reached USD 2.63 Billion in 2025 and is projected to reach USD 4.00 Billion by 2034, growing at a CAGR of 4.77% during 2026-2034. The market is driven by rising school enrolment, government education spending, brand consciousness, and product innovation.

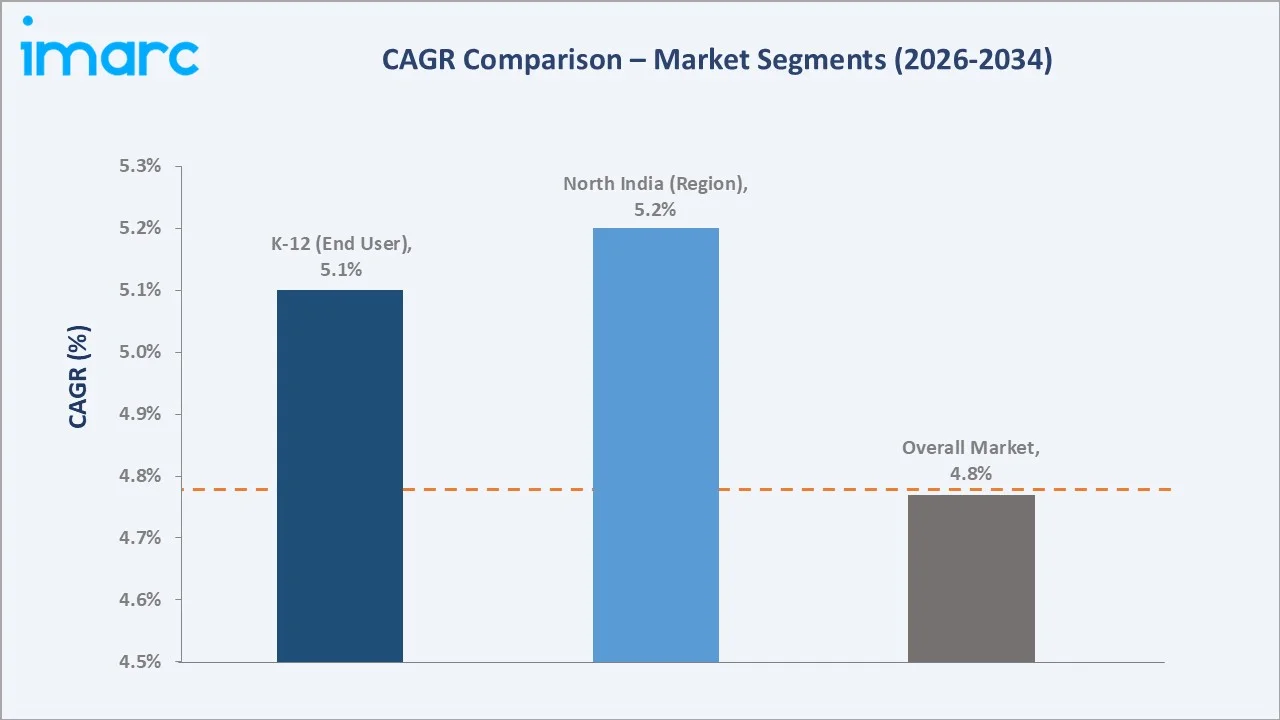

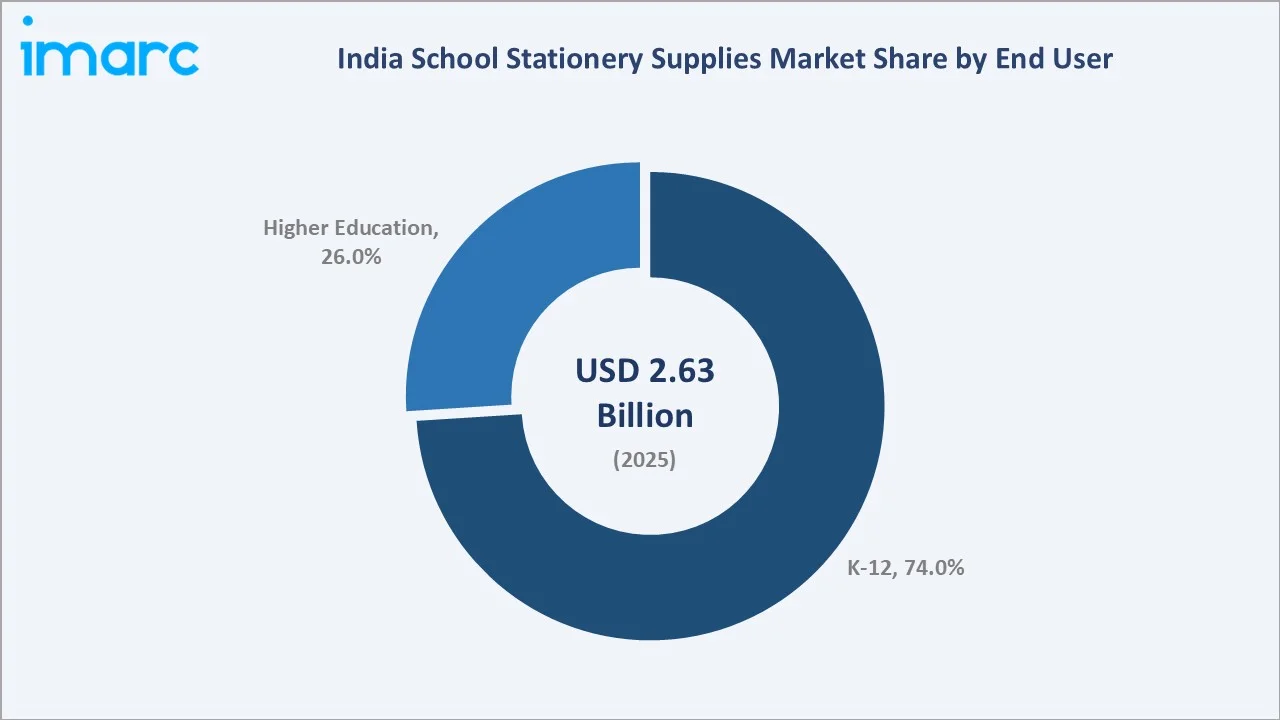

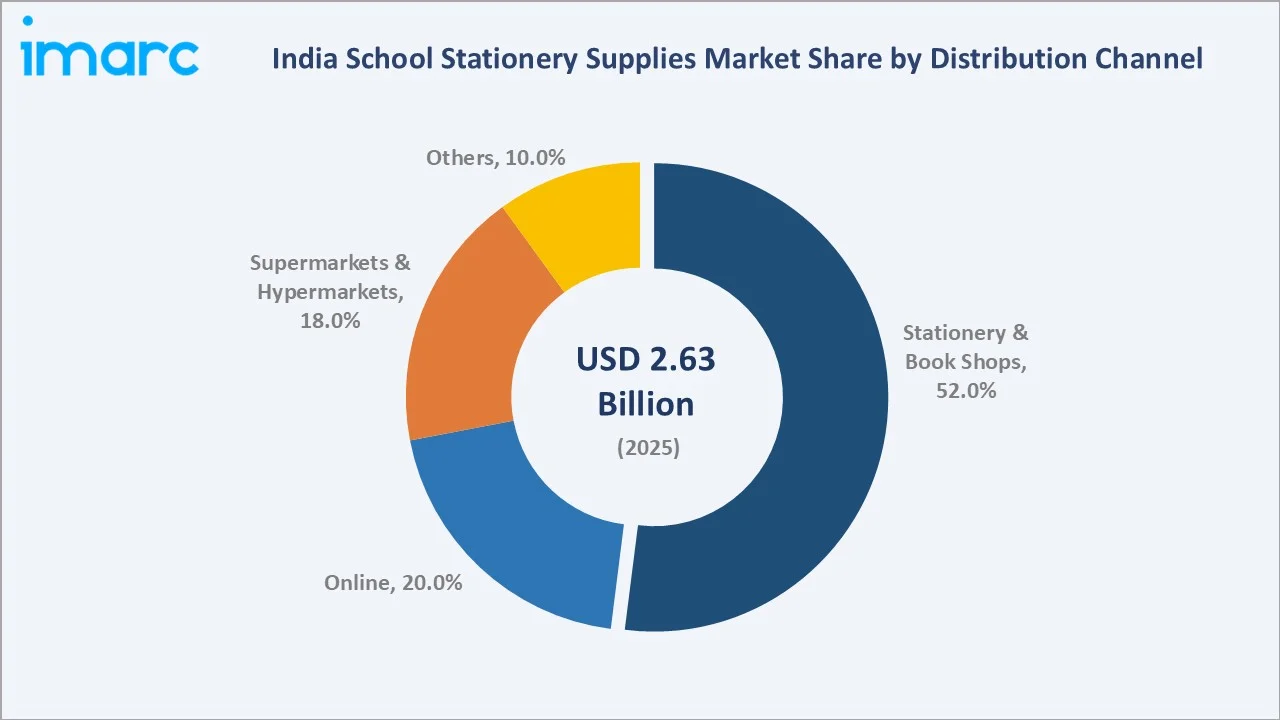

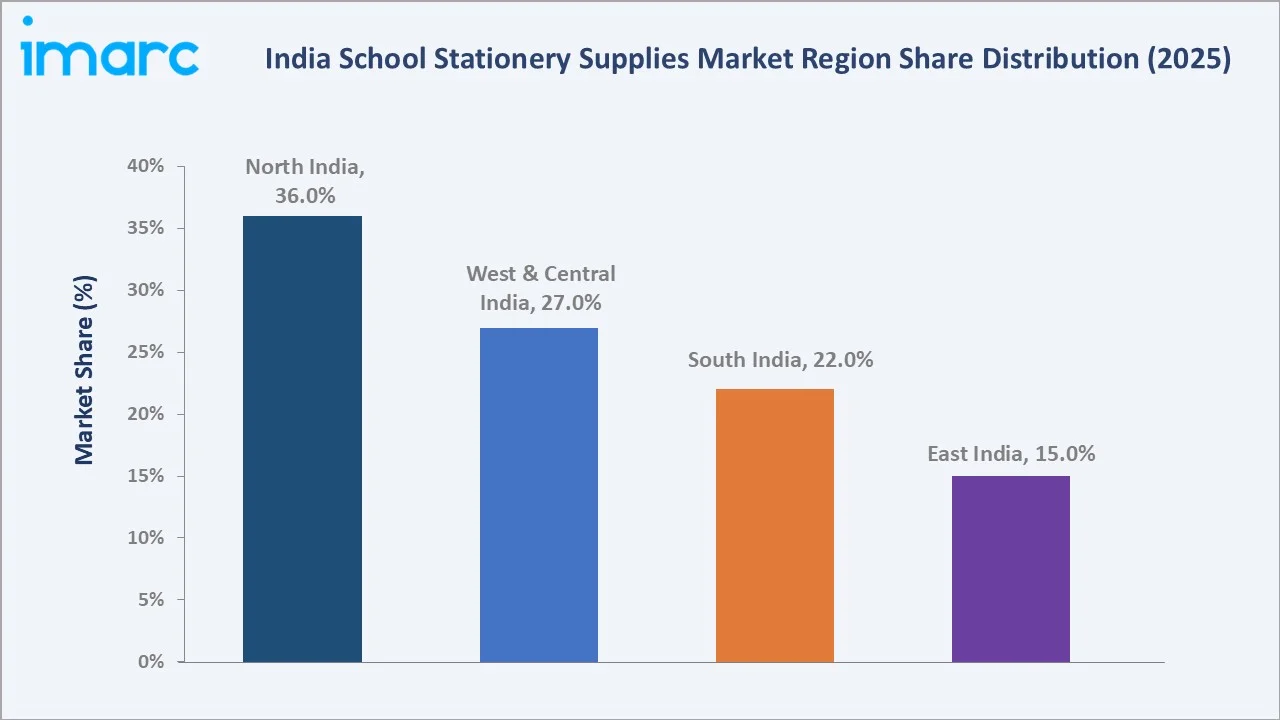

India's growing student population, expanding organized retail, and rising demand for premium and eco-friendly stationery are structurally accelerating market growth. K-12 leads at 74.0%, Stationery & Book Shops dominate distribution at 52.0%, and North India commands 36.0% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.63 Billion |

|

Forecast Market Size (2034) |

USD 4.00 Billion |

|

CAGR (2026-2034) |

4.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant End User |

K-12 (74.0%, 2025) |

|

Leading Distribution Channel |

Stationery & Book Shops (52.0%, 2025) |

|

Leading Region |

North India (36.0%, 2025) |

The market expanded steadily over the historical period 2020-2025, anchored by post-pandemic learning recovery and rising brand consciousness. Growing government education expenditure, digital-native student demand, and eco-friendly product innovation are compounding growth through 2034.

To get more information on this market, Request Sample

K-12 grows at approximately 5.1% CAGR driven by mandatory stationery procurement and rising school enrolment. Stationery & Book Shops distribution grows at approximately 4.9% CAGR through deepening retail penetration. North India leads regional CAGR at approximately 5.2% through high urban consumption and student density.

Executive Summary

The India school stationery supplies market reached USD 2.63 Billion in 2025, representing a stable and structurally growing segment driven by India's large student population and rising educational aspirations. The market is projected to reach USD 4.00 Billion by 2034.

K-12 at 74.0% dominates through mandatory stationery usage, large enrolment numbers, and diverse product requirements. Stationery & Book Shops at 52.0% leads distribution through proximity, variety, and school-adjacent retail positioning. North India at 36.0% reflects its highest student population concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant End User |

K-12 – 74.0% share (2025) |

|

Leading Distribution Channel |

Stationery & Book Shops – 52.0% market share (2025) |

|

Leading Region |

North India – 36.0% market share (2025) |

|

Market Opportunity |

Eco-friendly products; digital-integrated stationery; rural market penetration; licensed branded stationery |

Key Analytical Observations Supporting The Above Data:

- K-12 at 74.0%: The K-12 segment dominates as it encompasses the largest student population segment requiring mandatory use of notebooks, writing instruments, geometry boxes, and art supplies. School curriculum requirements create predictable, recurring annual stationery demand across all product categories.

- Stationery & Book Shops at 52.0%: Stationery and book shops dominate distribution as they are conveniently located near schools, offering extensive product variety, bulk purchase options, and personalized service. Their adjacency to the school ecosystem makes them the primary purchase point for parents and students.

- North India at 36.0%: North India leads through its highest concentration of students, dense urban school infrastructure, and strong organized retail presence. Uttar Pradesh, Delhi NCR, and Rajasthan collectively represent the country's largest stationery consumption pool.

India School Stationery Supplies Market Overview

The India school stationery supplies market encompasses the manufacture, distribution, and retail of all stationery products used in educational settings, including paper products, writing instruments, art and craft materials, and related accessories.

The ecosystem integrates raw material suppliers, product manufacturers, quality testing bodies, distributors, retail channels including stationery shops, supermarkets, and e-commerce platforms, and regulatory bodies governing product quality standards. Macroeconomic factors include rising literacy rates, government education spending, urbanization, and disposable income growth.

Market Dynamics

To evaluate market opportunities, Request Sample

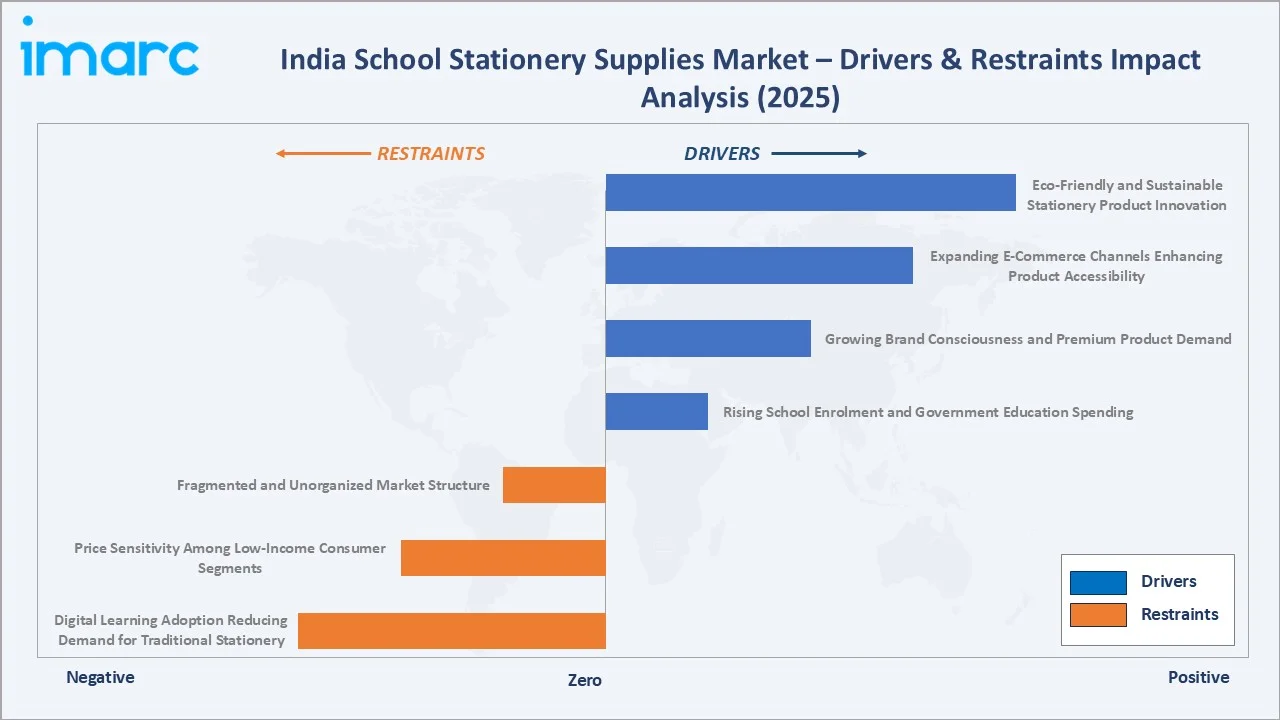

Market Drivers

- Rising School Enrolment and Government Education Spending: Rising school enrolment driven by India's young demographic and government initiatives such as NEP 2020 and the Right to Education Act is expanding the addressable student base. Increased per-student government spending on educational materials directly stimulates stationery demand across K-12 institutions.

- Growing Brand Consciousness and Premium Product Demand: Improving living standards and rising disposable incomes are elevating consumer preferences for branded, quality stationery. Manufacturers leveraging licensed character collaborations, innovative designs, and premium product variants are successfully capturing aspirational consumer segments.

- Expanding E-Commerce Channels Enhancing Product Accessibility: Rapid growth of e-commerce and emerging quick-commerce platforms is expanding stationery accessibility across Tier-2 and Tier-3 cities. Online channels enable wider SKU ranges, competitive pricing, and subscription-based replenishment, driving incremental market penetration beyond organized retail.

- Eco-Friendly and Sustainable Stationery Product Innovation: Growing environmental awareness among consumers, schools, and parents is creating demand for biodegradable, recycled-paper, and non-toxic stationery. Manufacturers introducing sustainable product variants are differentiating their portfolios and capturing premium market segments.

Market Restraints

- Digital Learning Adoption Reducing Demand for Traditional Stationery: Increasing adoption of tablets, laptops, and digital learning applications in schools is may reduce demand in select urban/private-school segments. EdTech integration and hybrid learning models are partially displacing traditional notebook and writing instrument usage, creating structural headwinds.

- Price Sensitivity Among Low-Income Consumer Segments: A significant proportion of India's school-going population is in price-sensitive rural and semi-urban households. Strong competition from the unorganized sector offering low-cost alternatives constrains branded manufacturers' pricing power and margin expansion in mass-market segments.

- Fragmented and Unorganized Market Structure: The India school stationery market remains fragmented, with the unorganized sector supplying economy-grade products through kirana stores and local vendors. This fragmentation creates distribution inefficiencies and limits manufacturers' ability to capture the full addressable market.

Market Opportunities

- Licensed and Character-Based Stationery Collaborations: Growing OTT consumption and children's media engagement is creating strong demand for stationery featuring popular characters and licensed intellectual property. Manufacturers partnering with entertainment brands can command premium pricing and build lasting loyalty.

- Rural Market Penetration through Affordable SKUs: India's rural student population represents a large underpenetrated addressable market for branded stationery. Manufacturers introducing affordable small-format SKUs through rural distribution networks can achieve high-volume penetration and long-term brand loyalty.

Market Challenges

- Seasonal Demand Concentration Creating Inventory Management Complexity: School stationery demand is heavily concentrated around the academic year start, creating significant inventory and cash flow management challenges for manufacturers and distributors. Off-peak months require efficient supply chain management to avoid excess inventory costs.

- Raw Material Price Volatility Impacting Manufacturer Margins: Volatility in paper pulp, plastic, and pigment prices creates margin pressure for stationery manufacturers, particularly smaller domestic players with limited hedging capabilities. Input cost increases are difficult to pass through to price-sensitive consumers.

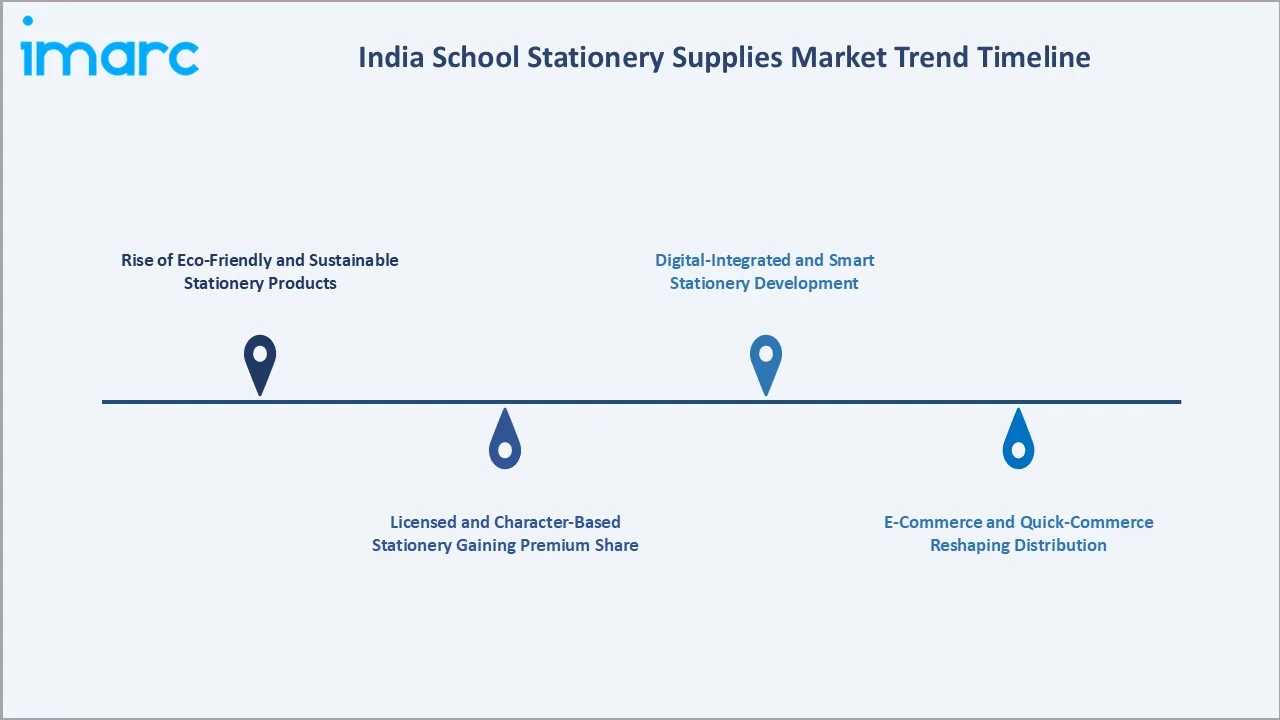

Emerging Market Trends

1. Rise of Eco-Friendly and Sustainable Stationery Products

Consumer and institutional preference for biodegradable, recycled, and non-toxic stationery is accelerating. Manufacturers are introducing plant-based inks, recycled-paper notebooks, and FSC-certified wood pencils. Schools mandating eco-friendly stationery lists are reinforcing this structural demand shift.

2. Licensed and Character-Based Stationery Gaining Premium Share

Partnerships with entertainment brands and children's television channels enable manufacturers to command premium pricing. Licensed character notebooks, pencil cases, and geometry boxes are driving impulse purchases and brand loyalty among K-12 students across urban and semi-urban markets.

3. E-Commerce and Quick-Commerce Reshaping Distribution

The rapid growth of online stationery procurement is transforming seasonal purchase behaviour. Subscription-based stationery kits and direct-to-school delivery models are emerging as growth formats, enabling brands to build direct consumer relationships beyond traditional trade channels.

4. Digital-Integrated and Smart Stationery Development

AR-enabled notebooks, QR-code-linked learning materials, and smart writing instruments are emerging as innovation frontiers. Manufacturers integrating digital and physical learning experiences are creating differentiated, premium products that appeal to digital-native students and tech-forward schools.

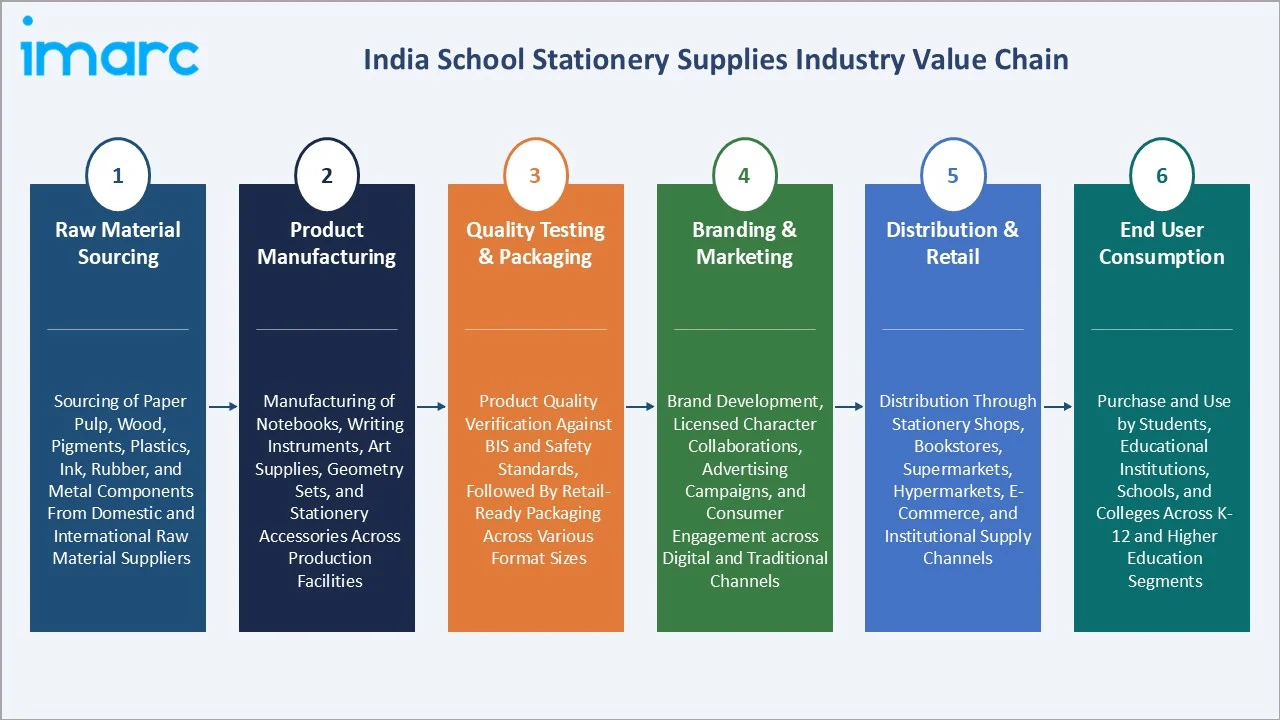

Industry Value Chain Analysis

The India school stationery supplies value chain integrates raw material procurement, product manufacturing, quality testing, packaging, branding, multi-channel distribution, and end-user consumption across K-12 and higher education institutions.

|

Stage |

Key Activities |

|

Raw Material Sourcing |

Sourcing of paper pulp, wood, pigments, plastics, ink, rubber, and metal components from domestic and international raw material suppliers |

|

Product Manufacturing |

Manufacturing of notebooks, writing instruments, art supplies, geometry sets, and computer accessories across production facilities |

|

Quality Testing & Packaging |

Product quality verification against BIS and safety standards, followed by retail-ready packaging across various format sizes |

|

Branding & Marketing |

Brand development, licensed character collaborations, advertising campaigns, and consumer engagement across digital and traditional channels |

|

Distribution & Retail |

Product distribution through stationery shops, book stores, supermarkets, hypermarkets, e-commerce, and institutional supply channels |

|

End User Consumption |

Purchase and use by students, educational institutions, schools, and colleges across K-12 and higher education segments |

The manufacturing and branding stages hold the highest value creation potential through product innovation, licensed collaborations, and quality differentiation. The distribution tier is experiencing rapid transformation as e-commerce and quick-commerce capture share from traditional stationery shop channels.

Technology Landscape in the India School Stationery Supplies Industry

Eco-Friendly and Sustainable Material Technology

Sustainable material technology applies biodegradable polymers, recycled paper pulp, plant-based inks, and FSC-certified wood to manufacture environmentally responsible stationery. These technologies reduce carbon footprint, meet institutional sustainability requirements, and enable premium product positioning.

Digital Integration and Augmented Reality Technology

AR-enabled stationery integrates QR codes into physical products, linking students to interactive digital learning content. This technology adds educational value beyond traditional stationery, creates engagement among digital-native students, and enables product differentiation in a competitive market.

Advanced Ink and Pigment Formulation Technology

Advanced ink formulations including gel, hybrid, and oil-based inks improve writing smoothness, drying speed, and colour vibrancy. Non-toxic, heavy-metal-free pigment technologies in crayons and sketch pens meet international safety standards and support premium product development.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

🔒 |

🔒 |

2025 |

|

End User |

K-12 |

74.0% |

2025 |

|

Distribution Channel |

Stationery & Book Shops |

52.0% |

2025 |

|

Region |

North India |

36.0% |

2025 |

By End User

K-12 leads at 74.0% in 2025, encompassing kindergarten through class 12 students who represent India's highest-volume stationery consumption segment. Mandatory curriculum requirements, large student enrolment, and annual purchase cycles create predictable and recurring demand across all product categories.

To access detailed market analysis, Request Sample

Higher Education at 26.0% captures university and college students requiring specialized supplies including graph notebooks, technical drawing instruments, printer supplies, and presentation materials. India's expanding college enrolment supports sustained higher education stationery demand growth through the forecast period.

By Distribution Channel

Stationery and Book Shops dominate at 52.0% as the primary purchase channel due to their proximity to schools, comprehensive product ranges, and established institutional supply relationships. These outlets benefit from concentrated footfall during peak academic season and bulk school procurement cycles.

Online channels at 20.0% are the fastest-growing distribution format, driven by e-commerce expansion, convenient home delivery, and competitive pricing. Supermarkets and Hypermarkets at 18.0% capture convenience and impulse purchases. Others at 10.0% include direct institutional sales and school cooperative stores.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

North India |

36.0% |

Driven by a large student population, high concentration of schools and educational institutions, and strong organized retail and distribution infrastructure |

|

West & Central India |

27.0% |

Supported by urban expansion, growing school infrastructure, rising middle-class educational spending, and increasing organized retail penetration |

|

South India |

22.0% |

Supported by high literacy rates, consumer preference for branded stationery, and strong government investment in education and school infrastructure |

|

East India |

15.0% |

Emerging growth driven by rising school enrolment, government education schemes, expanding distribution reach, and growing e-commerce penetration |

North India, at 36.0%, leads through its highest student population concentration, dense urban school infrastructure, and strong organized retail penetration supporting both economy and premium stationery procurement across all income segments.

West and Central India, at 27.0%, reflects urbanization and educational spending in Maharashtra and Gujarat. South India, at 22.0%, benefits from high literacy rates and premium adoption. East India, at 15.0%, represents an emerging growth region with rising enrolment and expanding e-commerce penetration.

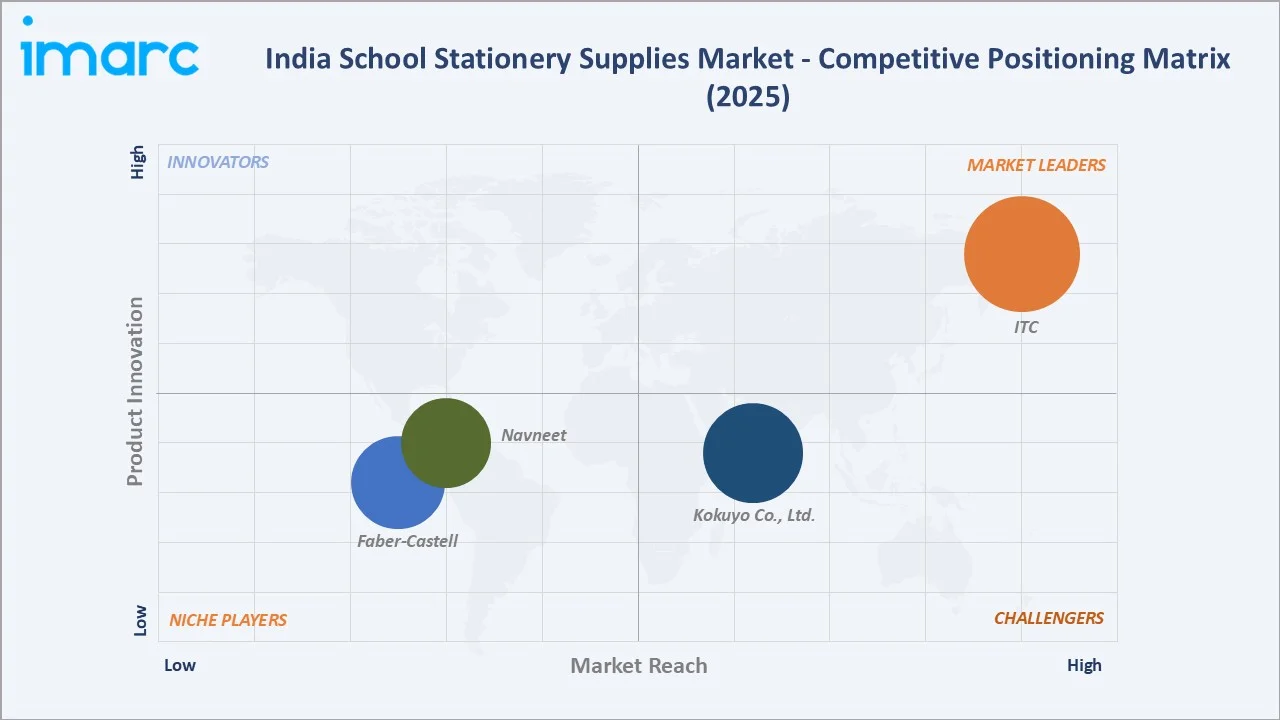

Competitive Landscape

The India school stationery supplies market competitive landscape is moderately fragmented, featuring domestic market leaders, strong domestic challengers, multinational subsidiaries, and a large unorganized sector. Competition centers on brand equity, distribution reach, product innovation, and pricing strategy.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

ITC |

Classmate Notebooks, Pens, Geometry Boxes, Sharpeners, Erasers |

Market Leader |

ITC leads India's school stationery market through Classmate, the country's largest notebook brand with premium eco-friendly paper formulations. |

|

Kokuyo Co., Ltd. |

Crayons, Sketch Pens, Watercolors, Geometry Sets, Notebooks |

Strong Challenger |

Kokuyo Camlin Limited (a subsidiary of Kokuyo Co., Ltd.) dominates the art supplies and creative stationery segment with strong brand equity. |

|

Navneet |

Notebooks, Practical Books, Drawing Books, Art Supplies |

Niche Player |

Navneet Education Limited is a leading paper and stationery products manufacturer with strong regional distribution in Maharashtra and Gujarat. |

|

Faber-Castell |

Pencils, Colour Pencils, Crayons, Markers, Erasers, Sharpeners |

Niche Player |

Faber-Castell (India) Pvt. Ltd. (a subsidiary of Faber-Castell Aktiengesellschaft) offers premium writing instruments and art supplies targeting quality-conscious consumers. |

Key players include ITC, Kokuyo Co., Ltd., Navneet, Faber-Castell, and others.

Key Company Profiles

ITC

ITC is a diversified Indian conglomerate with a strong position in the Indian school stationery market through its Classmate brand, India's largest notebook brand with a premium eco-friendly paper portfolio.

- Key Products: Classmate Notebooks, Pens, Mechanical Pencils, Geometry Boxes, Sharpeners, Erasers.

- Strategic Focus: Expanding premium eco-friendly notebook formats and branded stationery accessories while deepening rural distribution and strengthening e-commerce channel presence.

Kokuyo Co., Ltd.

Kokuyo Co., Ltd. is a leading Japan-based stationery manufacturer, operating in India through Kokuyo Camlin Limited, specializing in art supplies, creative stationery, and school products, combining domestic brand equity with Kokuyo's global R&D capabilities.

- Key Products: Camel Crayons, Sketch Pens, Watercolors, Oil Paints, Geometry Sets, Notebooks, Markers.

- Strategic Focus: Strengthening leadership in art supplies and creative stationery while expanding the school and office stationery portfolio with new sustainable product lines.

Market Concentration Analysis

The India school stationery market is moderately fragmented. The top five organized players collectively account for approximately 40-50% of the organized branded stationery market revenue.

The unorganized sector retains a significant share primarily through economy-grade products distributed via kirana stores and local vendors. Market concentration is expected to increase modestly as organized players expand rural distribution, e-commerce penetration, and institutional supply contracts through the forecast period.

Investment & Growth Opportunities

Highest Growth Segments

Online distribution channel (~8-10% CAGR), eco-friendly stationery (~12%+ CAGR from small base), licensed character stationery (~9% CAGR), higher education segment (~5.5% CAGR), and premium writing instruments (~7% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Direct-to-institution supply models targeting school procurement offices represent the market's highest-value emerging opportunity. Schools managing bulk annual purchases create structured, predictable procurement volumes enabling manufacturers to bypass fragmented retail channels and capture higher margins.

Investment Themes

- Eco-Friendly and Sustainable Product Innovation: Consumer and institutional demand for biodegradable, FSC-certified, and non-toxic stationery is structurally growing. Investments in sustainable raw materials, recyclable packaging, and plant-based ink technologies represent high-return opportunities as schools implement green procurement policies.

- E-Commerce and Direct-to-Consumer Channel Infrastructure: Building robust online and quick-commerce distribution capability represents a structural competitive advantage as India's digital retail ecosystem expands. Subscription kits, school supply bundles, and AR-enabled offerings can capture digital-native student consumers.

Future Market Outlook (2026-2034)

The India school stationery supplies market is projected to grow from USD 2.63 Billion in 2025 to USD 4.00 Billion by 2034, delivering a 4.77% CAGR. Growth is underpinned by India's young demographic, rising educational aspirations, and increasing per-student stationery spending.

Three structural forces define growth through 2034. India's large student population creates compounding stationery demand as enrolment expands across K-12 and higher education. Premiumization through branded, eco-friendly, and licensed products creates average selling price expansion above volume growth. E-commerce penetration unlocks branded product access across Tier-2 and Tier-3 markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including stationery brand managers, school procurement officers, distribution channel executives, raw material suppliers, and e-commerce category managers.

Secondary Research

Secondary research encompassed company annual reports, industry association publications, Ministry of Education enrolment data, IMARC Group retail market tracking, and regulatory filings. Over 45 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a student population-based demand model incorporating enrolment growth rates, per-student stationery spending trends, product premiumization trajectories, and channel-level distribution expansion assumptions across organized trade and e-commerce.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Paper Products, Writing Instruments, Computer and Printer Supplies, Others |

| Distribution Channels Covered | Stationary and Book Shops, Supermarkets and Hypermarkets, Online, Others |

| End Users Covered | K-12, Higher Education |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | ITC, Kokuyo Co. Ltd., Navneet, Faber-Castell, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India School Stationery Supplies Market Report

The India school stationery supplies market reached USD 2.63 Billion in 2025, driven by the K-12 segment dominant at 74.0%, Stationery & Book Shops leading distribution at 52.0%, and North India commanding 36.0% regional market share through its highest student population concentration and strong retail infrastructure.

The India school stationery supplies market grows at 4.77% CAGR during 2026-2034, reaching USD 4.00 Billion by 2034. Growth reflects rising school enrolment, growing brand consciousness, eco-friendly product innovation, e-commerce channel expansion, and increasing per-student educational spending.

K-12 leads at 74.0%, capturing mandatory stationery requirements across kindergarten through class 12 students. This segment grows at approximately 5.1% CAGR through India's expanding school enrolment and rising per-student stationery expenditure driven by brand consciousness.

Stationery and Book Shops dominate at 52.0% through proximity to schools, comprehensive product availability, and established institutional supply relationships. Online channels at 20.0% are the fastest-growing distribution format, driven by e-commerce and quick-commerce platform expansion.

North India leads at 36.0% through its highest student population concentration, dense urban school infrastructure, and strong organized retail presence supporting both economy and premium stationery demand.

Leading companies include ITC, Kokuyo Co., Ltd., Navneet, Faber-Castell, and others.

The India school stationery supplies market is projected to reach approximately USD 3.32 Billion by 2030, driven by continued school enrolment growth, eco-friendly product mainstreaming, e-commerce distribution expansion, and premiumization through licensed and branded stationery formats.

Three priority investment opportunities: eco-friendly and sustainable stationery innovation capturing institutional and premium consumer segments, e-commerce and direct-to-school supply model development, and licensed character stationery collaborations targeting the aspirational K-12 consumer segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)