India Security Market Size, Share, Trends and Forecast by System, Service, End User, and Region, 2026-2034

India Security Market Size & Forecast 2026-2034

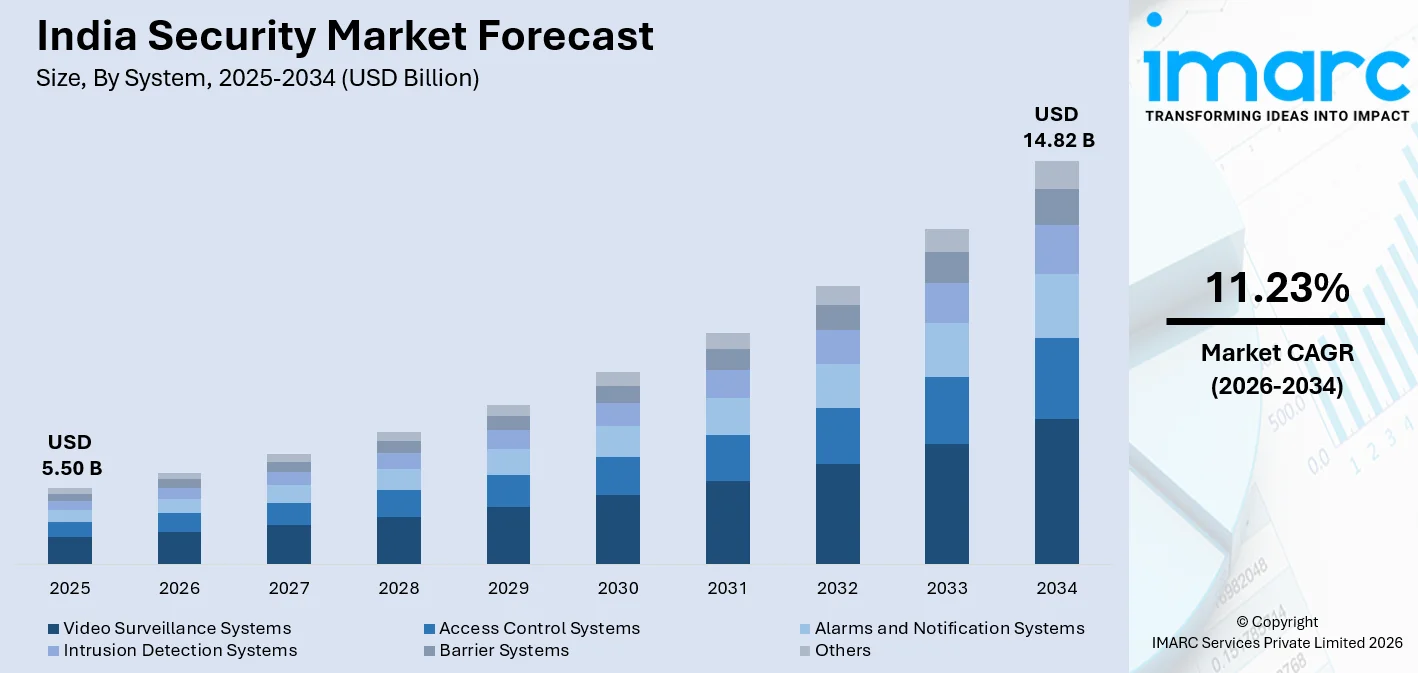

India security market size, valued at USD 5.50 Billion in 2025, is projected to reach USD 14.82 Billion by 2034, growing at a CAGR of 11.23% from 2026-2034, supported by the government's defense modernization agenda, a Union Budget 2025-26 allocation of ₹6.81 lakh crore for the Ministry of Defense, a 9.53% year-on-year increase, and the rapid integration of AI-driven surveillance across critical public infrastructure, which collectively elevate India security market share.

To get more information on this market Request Sample

India Security Industry Analysis — Key Insights

- Video Surveillance Systems commands 30.0% of the system segment in 2025 - a decisive lead, anchored by AI-enabled cameras, Smart Cities Mission deployments, and government mandates standardizing IP surveillance across transport hubs and urban command centers.

- System Integration and Consulting leads service at 33.0% in 2025 - organizations across banking, defense, and smart city verticals increasingly outsource complex multi-layered security architecture to specialized integrators, with AI-orchestrated platforms driving demand for expert design and deployment.

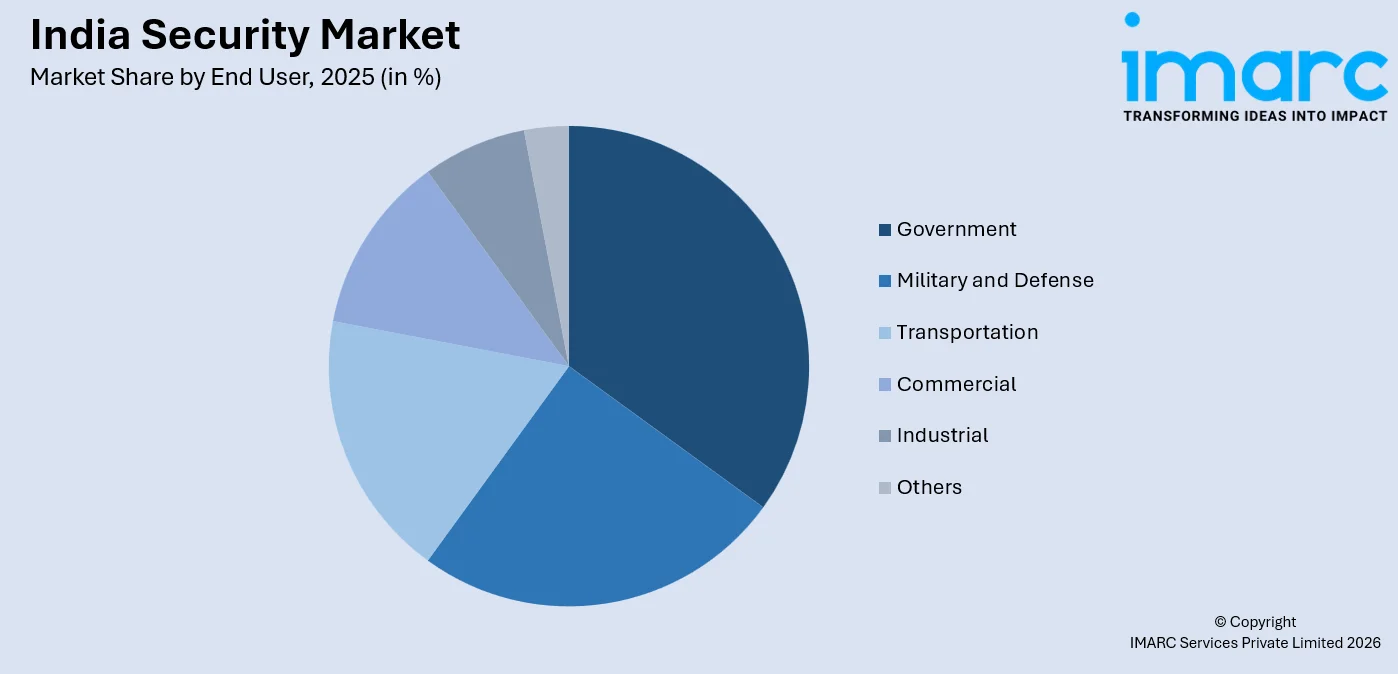

- Government holds 25.0% of the end user segment in 2025 - the single largest institutional buyer, fueled by public safety mandates, Safe City programs, and critical infrastructure protection requirements spanning border surveillance to port and airport security.

- West & Central India leads regionally with 31.6% in 2025. The growing urbanization, increasing infrastructure development, and rising concerns about safety are driving the security market in West and Central India.

India Security Market Trends and Dynamics 2026

Market Trends

AI-powered surveillance is transforming threat detection across Indian cities

India security market is witnessing accelerating adoption of AI-enabled surveillance as cities embed intelligent analytics into command centers. In December 2025, IFSEC India 2025 brought together over 150 exhibitors and 350-plus brands and around 20,000 industry professionals at Bharat Mandapam, New Delhi, showcasing AI-driven video analytics, behavioral recognition systems, mission-critical command platforms, and IoT-enabled sensors, reflecting the intensity of innovation reshaping India's physical and digital security landscape.

Make in India is accelerating indigenous security hardware development

Government policy is actively reshaping supply chains within India security market growth landscape. In June 2025, Honeywell launched its 50 Series, India's first locally designed and manufactured CCTV portfolio, developed at its Bengaluru global development center in partnership with VVDN Technologies. The Class 1 certified cameras embed advanced cybersecurity, gyro-sensor stabilization, and intelligent video analytics, directly aligned with the Atmanirbhar Bharat manufacturing push.

Mandatory STQC certification is reshaping procurement compliance standards

The Government of India enforced STQC (Standardisation Testing and Quality Certification) compliance for all internet-connected CCTV devices. In October 2024, CN Labs became India's first Bureau of Indian Standards (BIS)-approved laboratory authorized to conduct security testing of CCTV cameras, covering physical safeguards, network encryption, and penetration testing under the Compulsory Registration Scheme, raising the compliance bar for all market participants.

- AI-Enabled Video Analytics: Cities are embedding deep-learning video analytics for crowd management, automatic number plate recognition, and real-time intrusion detection across Smart City command centers.

- Cloud-Based Surveillance Adoption: Mid-market organizations are shifting to Video-Surveillance-as-a-Service models for subscription pricing and automated firmware management, broadening geographic security reach.

- Biometric and Access Control Integration: Demand for contactless biometric systems combining facial recognition and smart-card authentication is accelerating across defense, banking, and smart building verticals.

Growth Drivers

Government Smart City and public safety investments are creating sustained demand

India's Smart Cities Mission has generated structural, long-term demand for security systems. As of March 2025, over 84,000 CCTV surveillance cameras have been installed in 100 Smart Cities, complemented by 1,884 emergency call boxes, 3,000 public address systems and automated number plate recognition systems. All 100 cities now have fully operational Integrated Command and Control Centers using AI and IoT for real-time urban management, establishing a durable institutional procurement pipeline for India security market trends.

Rising defense expenditure and geopolitical pressures are accelerating modernization

Escalating border security requirements and India's Atmanirbhar Bharat defense manufacturing strategy are major structural demand drivers. The Union Budget 2025-26 earmarked ₹1,80,000 crore in capital outlay for the Ministry of Defence, with 75% of the modernization budget ring-fenced for domestic procurement. The Border Roads Organization received ₹7,146.50 crore in 2025-26, a 9.74% increase over 2024-25, directly supporting surveillance infrastructure upgrades in border regions.

- Rapid Urbanization and Real Estate Expansion: Growth of corporate offices, malls, residential complexes, and industrial parks is increasing demand for integrated physical security systems with access control and intrusion detection.

- Cybersecurity Spending Surge: In August 2024, Kyndryl launched a Security Operations Centre (SOC) in Bengaluru using AI-driven threat detection, reflecting India security market outlook of sustained enterprise-level cybersecurity investment.

- Digital Personal Data Protection Act Compliance: DPDPA 2023 obligations are compelling private operators to upgrade surveillance infrastructure to meet data residency, consent, and encryption mandates, creating additional system integration demand.

- Record Defense Export Momentum: India's defense exports reached a record ₹23,622 crore in FY 2024-25, demonstrating the maturity of domestic manufacturers and fueling further R&D investment in security technologies.

Market Restraints

Fragmented Regulatory Environment: India's security sector is governed by a complex, multi-layered regulatory framework spanning central mandates and state-specific compliance norms. This fragmentation creates inconsistent procurement standards, raises compliance costs for vendors, and can delay large-scale project rollouts across jurisdictions.

Skilled Workforce Shortage: The security industry faces a persistent deficit of technically trained professionals capable of designing, deploying, and maintaining advanced AI-integrated systems. This talent gap constrains the pace of deployment for sophisticated solutions, particularly in tier-two and tier-three cities where training infrastructure remains limited.

High Integration Complexity and Cost: Implementing multi-layered security solutions that unify physical surveillance, access control, and cybersecurity into a single managed architecture requires significant capital investment and long-term service commitments. Smaller enterprises and municipal bodies face structural affordability barriers that inhibit broad-based adoption beyond metropolitan centres.

India Security Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| System | Video Surveillance Systems | 30.0% | 2025 |

| Service | System Integration and Consulting | 33.0% | 2025 |

| End User | Government | 25.0% | 2025 |

| Region | West & Central India | 31.6% | 2025 |

System Insights

Video Surveillance Systems – 30.0% Market Share (2025) | Leading System

Video surveillance systems hold the dominant position within India security market, driven by converging demand from government safe-city programs, commercial real estate, and transport hubs. In January 2024, Uttar Pradesh announced the installation of 100,000 CCTV cameras as part of its Smart Cities initiative, led by the Urban Development Department in collaboration with the Home Department, prioritizing safety for women, children, and senior citizens, highlighting the scale of state-level surveillance procurement.

AI integration has been a decisive catalyst. Devices now ship with embedded GPUs executing object detection on the edge, reducing bandwidth demands while enabling crowd analytics, automated number plate recognition, and facial recognition. In December 2024, IFSEC India showcased over 300 brands with 5,000 security solutions, demonstrating how system integrators are advancing AI-enabled surveillance into mission-critical applications across banking, retail, and public infrastructure.

|

Segment Breakdown Video Surveillance Systems (30.0%) · Access Control Systems · Alarms and Notification Systems · Intrusion Detection Systems · Barrier Systems · Others |

Service Insights

System Integration and Consulting – 33.0% Market Share (2025) | Leading Service

System integration and consulting is the most critical service category in India's security ecosystem, reflecting the complexity of deploying multi-vendor, multi-layered solutions across banking, defense, and smart city environments. In June 2024, Tata Communications launched its Unified/ Single-Vendor Hosted Secure Access Service Edge (SASE) solution, integrating SD-WAN and security service edge (SSE) into a unified platform, a development that underscored the growing enterprise appetite for end-to-end security architecture design and managed connectivity.

India security market forecast trajectory for consulting services remains highly favorable. In November 2024, Sparsh CCTV and Cron AI partnered to integrate LiDAR, 3D perception, and AI-driven edge computing into security systems, enhancing intelligent surveillance and traffic management automation. Such innovations necessitate specialist integration expertise, expanding the addressable market for consultants and system architects across government, transport, and commercial verticals.

|

Segment Breakdown System Integration and Consulting (33.0%) · Risk Assessment and Analysis · Managed Services · Maintenance and Support |

End User Insights

Access the comprehensive market breakdown Request Sample

Government – 25.0% Market Share (2025) | Leading End User

Government is the anchor end-user in India security market, driven by stringent public safety mandates and the scale of national surveillance infrastructure rollouts. The Smart Cities Mission invested ₹1.64 lakh crore across 8,067 multi-sectoral projects, with Integrated Command and Control Centers, cementing the government as the most structurally committed buyer of advanced security solutions.

|

Segment Breakdown Government (25.0%) · Military and Defense · Transportation · Commercial · Industrial · Others |

Regional Insights

West & Central India – 31.6% Market Share (2025) | Leading Region

West & Central India:

West and Central India is an emerging growth corridor anchored by Maharashtra's financial services, pharmaceutical, and manufacturing industries. Mumbai's financial district and Pune's defence-adjacent IT sector sustain a strong managed security services demand.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

31.6%

|

|

Key States

|

Mumbai, Pune, Ahmedabad |

|

Major Growth Drivers

|

NEOM mega-project, sustainable development, technology integration |

|

Outlook

|

High-potential emerging market |

|

Regional Breakdown West & Central India (31.6%) · South India · North India · East India |

North India:

North India is the second largest region and the primary hub for public-safety surveillance procurement, driven by dense urban populations and large-scale government rollouts. In January 2024, Uttar Pradesh announced 100,000 new CCTV installations across major cities. Delhi's high-density commercial corridors, airports, and government facilities sustain year-round demand for access control and perimeter security.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Delhi, Chandigarh, Lucknow |

|

Major Growth Drivers

|

Rapid infrastructure development, rising security concerns, government push for smart city initiatives |

|

Outlook

|

Growing demand for advanced security systems in both residential and commercial sectors |

South India:

South India leads India security market by virtue of Bengaluru and Hyderabad functioning as India's primary technology and defence R&D hubs. In February 2026, Kyndryl launched its first Cyber Defense Operations Center in Bengaluru, enabling global clients to enhance cybersecurity capabilities, improve incident response, and strengthen overall IT resilience and performance.

The region benefits from a dense concentration of IT companies, defense research laboratories, and multinational security vendors that collectively create deep demand for sophisticated access control, video analytics, and managed cybersecurity services.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Chennai, Bengaluru, Hyderabad |

|

Major Growth Drivers

|

Technological advancements, increasing urbanization, government initiatives for smart cities |

|

Outlook

|

Expanding market with increasing demand for integrated security solutions |

East India:

East India represents a nascent but expanding security market, with Kolkata and Odisha emerging as early adopters of perimeter-intrusion systems and facial recognition. In December 2024, the Data Security Council of India launched its 'Cyber for HER' Hackathon under India-UK Cyber Program to strengthen cybersecurity workforce development, reflecting a nationally coordinated effort to build regional cybersecurity capacity, including in East India's growing IT talent pipeline.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Kolkata, Bhubaneswar, Patna |

|

Major Growth Drivers

|

Growing commercial and residential development, need for public safety systems, government infrastructure projects |

|

Outlook

|

Expanding market with increasing adoption of security technologies in urban areas |

Market Outlook 2026-2034

What is the future outlook of India security market?

India security market is expected to sustain steady revenue growth through 2034.

Continued government investments in smart surveillance, Atmanirbhar Bharat-driven indigenous hardware manufacturing, and the deepening of AI, IoT, and cloud-based security platforms will collectively underpin strong expansion across all segments. The mandatory STQC certification regime will consolidate market leadership among technologically sophisticated domestic and global players, while rising BFSI and critical infrastructure spending will sustain private-sector demand well into the forecast period.

India Security Market — Leading Key Players

India security market exhibits a dynamic and intensifying competitive landscape characterized by the presence of established multinational technology corporations alongside rapidly growing domestic manufacturers and specialized technology startups.

| Company | Leading Brands | Highlights |

|---|---|---|

| Tata Advanced Systems Limited | Tata Advanced Systems Security Solutions | Major Indian defense and homeland security company, provides integrated security systems, surveillance technologies, and critical infrastructure protection solutions |

| Larsen & Toubro Limited | L&T Smart World | Provides smart city surveillance, command-and-control centers, border security solutions, and integrated security infrastructure projects across India |

| Godrej Security Solutions | Godrej Safes, Godrej Locks, Godrej Security Systems | One of India’s largest physical security solution providers; offers safes, vaults, electronic security, and integrated security systems |

Some of the other key players existing in India security market includes Honeywell Automation India Ltd., Bosch Security Systems India, Aditya Infotech Ltd. (CP PLUS), PRAMA Hikvision India Pvt. Ltd., etc.

Latest Development & News

- In December 2025, IFSEC India, in its largest-ever edition, held at Bharat Mandapam, New Delhi, bringing together over 150 exhibitors and 350-plus brands to showcase AI-enabled video analytics, behavioral recognition, and IoT-integrated security technologies. The event drew 17,000-plus industry professionals and senior government officials, signaling the accelerating pace of innovation and adoption across India's physical and digital security ecosystem.

- In June 2025, Honeywell launched the 50 Series, India's first locally designed and manufactured CCTV camera portfolio, developed at its Bengaluru global development center in collaboration with VVDN Technologies. Certified as Class 1 under the Make in India policy, the cameras incorporate advanced cybersecurity measures, gyro-sensor stabilization, and intelligent video analytics, marking a landmark milestone in indigenous premium security hardware production.

- In January 2025, Bosch divested its Video, Access and Intrusion business to Keenfinity India for INR 595 crores as part of a global portfolio restructuring. The transaction transferred a comprehensive range of security hardware and access control assets to an India-based entity, reflecting a broader industry trend of international players reshaping their India-specific operations to optimize for domestic manufacturing and distribution requirements.

India Security Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Systems Covered | Access Control Systems, Alarms and Notification Systems, Intrusion Detection Systems, Video Surveillance Systems, Barrier Systems, Others |

| Services Covered | System Integration and Consulting, Risk Assessment and Analysis, Managed Services, Maintenance and Support |

| End Users Covered | Government, Military and Defense, Transportation, Commercial, Industrial, Others |

| Regions Covered | South India, North India, West & Central India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Security Market Report

India security market was valued at USD 5.50 Billion in 2025.

India security market is anticipated to reach a value of USD 14.82 Billion by 2034.

Video surveillance systems dominate the market with a share of 30.0% in 2025, reflecting accelerating smart city deployments, government public safety mandates, and the rapid integration of AI-driven cameras across urban and critical infrastructure environments nationwide.

System integration and consulting commands the market with a share of 33.0% in 2025, driven by rising enterprise demand for expert design and deployment of complex, multi-layered security architectures spanning physical surveillance, access control, and cybersecurity integration.

Government dominates the segment with a share of 25.0% in 2025, accelerated by strict public safety mandates and the scale of national surveillance infrastructure rollouts.

Key trends include the proliferation of cloud-based Video-Surveillance-as-a-Service platforms reducing storage costs for multi-site operators, expanding Digital Personal Data Protection Act compliance driving encryption and data residency investments, and the rise of edge AI chips enabling real-time on-camera analytics without server dependency across both commercial and government deployments.

West & Central India currently leads India security market with 31.6% share in 2025, driven by rapid urbanization, infrastructure growth, and increasing demand for integrated security solutions.

Key growth factors include the accelerating digitization of India's BFSI sector, which is increasing demand for network security and endpoint protection; growing adoption of biometric identity platforms across transport and government facilities, and the Atmanirbhar Bharat manufacturing push incentivizing domestic production of surveillance hardware and reducing import dependency across the security supply chain.

The market faces challenges from cybersecurity talent shortages that limit deployment velocity, particularly in tier-two and tier-three cities, inconsistent state-level regulatory frameworks that create compliance complexity for pan-India vendors; and affordability constraints among smaller municipalities that limit adoption of advanced AI-integrated security solutions beyond major metropolitan centers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)