India Senolytics & Anti-aging Pharmaceuticals Market Size, Share, Trends and Forecast by Product, Route of Administration, Application, and Region, 2026-2034

India Senolytics & Anti-aging Pharmaceuticals Market Summary:

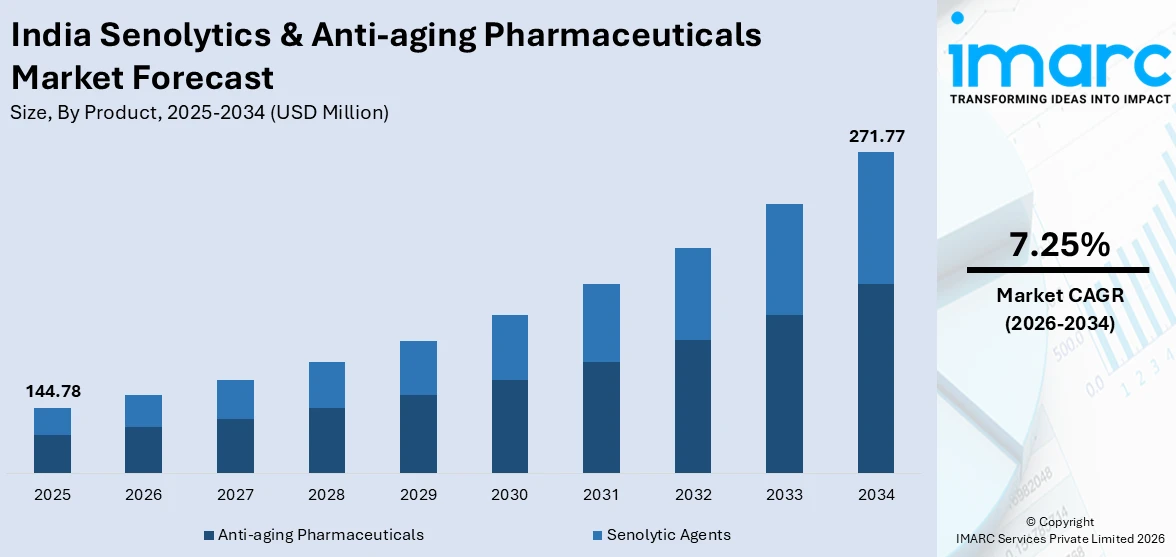

The India senolytics and anti-aging pharmaceuticals market size reached USD 144.78 Million in 2025. The market is projected to reach USD 271.77 Million by 2034, growing at a CAGR of 7.25% during 2026-2034. The market is driven by increasing government investment in biotechnology research and longevity science, expansion of specialized wellness infrastructure across urban centers, and growing adoption of advanced biopharmaceutical therapies including peptide-based interventions and regenerative medicine protocols. These factors are collectively expanding the India senolytics and anti-aging pharmaceuticals market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Market Size in 2025 | USD 144.78 Million |

| Market Forecast in 2034 | USD 271.77 Million |

| Market Growth Rate (2026-2034) | 7.25% |

| Key Segments | Product (Anti-aging Pharmaceuticals, Senolytic Agents), Route of Administration (Clinical Use/Off-label Therapeutics, Consumer Wellness/Longevity Use), and Application (Prescription-based, Over-the-Counter (OTC)/Supplements, Clinical Trials/Compassionate Use) |

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

India Senolytics & Anti-aging Pharmaceuticals Market Outlook (2026-2034):

The India senolytics and anti-aging pharmaceuticals market growth is positioned for robust expansion, propelled by substantial government funding increases for translational aging research and the emergence of specialized longevity clinics across metropolitan regions. Growing consumer awareness regarding healthspan extension and cellular senescence management, coupled with improved accessibility to advanced biopharmaceutical interventions previously available only in developed markets, will drive market penetration. Additionally, the integration of artificial intelligence in drug discovery processes promises to accelerate the identification and development of novel senolytic compounds, potentially reducing time-to-market and improving therapeutic efficacy throughout the forecast period.

To get more information on this market Request Sample

Impact of AI:

Artificial intelligence is transforming anti-aging drug discovery through deep neural network applications that screen hundreds of thousands of molecular compounds to identify promising senolytic candidates with superior efficacy and safety profiles. AI-driven platforms have successfully reduced drug screening costs by several hundred-fold while identifying three highly selective compounds from chemical libraries exceeding 800,000 molecules, demonstrating capabilities far beyond traditional high-throughput screening methodologies. As these technologies mature and become more accessible, AI is expected to accelerate the clinical translation of novel anti-aging therapeutics, compress development timelines, and improve the probability of regulatory approval for senolytic agents targeting age-related diseases.

Market Dynamics:

Key Market Trends & Growth Drivers:

Government Investment Driving Biotechnology Research and Clinical Translation

India's Department of Biotechnology has strategically prioritized aging research through substantial funding increases, with a 25% boost in 2023 specifically allocated to translational research in anti-aging therapeutics, positioning India as an emerging leader in Asia-Pacific longevity science. This governmental commitment manifests through initiatives like the Bio-RIDE scheme, which consolidates research and development efforts while promoting commercialization pathways for biotechnology innovations. The establishment of the Longevity India Initiative at the Indian Institute of Science represents a landmark development, creating India's first dedicated research platform focused on aging biomarkers, organ health preservation, and age-related clinical trials tailored to the Indian demographic context. This research infrastructure provides critical support for domestic pharmaceutical companies exploring senolytic drug development while facilitating international collaborations with leading aging research institutions globally. The government's emphasis on biotechnology innovation aligns with broader national health priorities, including the management of non-communicable diseases that disproportionately affect India's aging population. By investing in fundamental aging research and supporting translational pathways from laboratory discoveries to clinical applications, Indian policymakers are creating an ecosystem conducive to pharmaceutical innovation in the longevity sector.

Expansion of Wellness Infrastructure and Longevity-Focused Healthcare Delivery

The Indian healthcare landscape has witnessed transformative infrastructure development with specialized longevity clinics emerging across major metropolitan areas, fundamentally altering the delivery model for preventive and anti-aging medicine. Pioneering facilities such as C4 Lifestyle Diagnostics, established in 2018 as India's first integrated wellness and longevity center, have demonstrated the commercial viability of comprehensive preventive healthcare approaches that extend beyond traditional disease treatment paradigms. The 2024 launch of Biopeak, India's first dedicated longevity clinic offering advanced diagnostic assessments including over 130 biomarker panels, DEXA scans, VO2 max testing, genetic and epigenetic profiling, gut and oral microbiome mapping, and comprehensive hormonal analysis, establishes new benchmarks for personalized preventive care sophistication in emerging markets. These facilities cater to an affluent urban demographic increasingly prioritizing healthspan extension over conventional reactive medicine, reflecting broader societal shifts toward proactive health optimization and longevity enhancement. The geographic concentration of these advanced wellness centers in cities like Mumbai, Delhi, and Bangalore creates knowledge hubs where medical professionals gain expertise in cutting-edge anti-aging interventions, potentially catalyzing broader adoption across secondary markets as awareness expands and treatment protocols become standardized.

Growing Adoption of Advanced Biopharmaceuticals and Regenerative Medicine Modalities

Peptide therapy and regenerative medicine have transitioned from experimental treatments available exclusively abroad to mainstream offerings within India's premium wellness sector, with specialized clinics across Mumbai, Delhi, and Bangalore integrating these advanced interventions into comprehensive anti-aging protocols. The improved domestic accessibility of therapies like NAD boosters, peptide-based cellular rejuvenation treatments, and ozone therapy reflects both supply-side developments (including local manufacturing capacity expansion) and demand-side drivers (growing consumer sophistication regarding longevity interventions). The 2025 acquisition of a Swiss peptide manufacturer by an Indian pharmaceutical company represents a strategic inflection point, demonstrating institutional confidence in the commercial viability of peptide therapeutics while establishing domestic manufacturing capabilities that reduce import dependence and improve price competitiveness. This vertical integration enables Indian companies to capture greater value across the biopharmaceutical supply chain while potentially positioning India as a peptide manufacturing hub for regional export markets. The scientific validation of peptide therapy efficacy through peer-reviewed research, including a 2024 review published by Hyderabad-based scientists highlighting peptide-based treatments' effectiveness and low-risk profiles in aging interventions, has enhanced physician confidence and patient acceptance of these novel modalities. Clinical success stories circulating within India's wellness community generate powerful word-of-mouth marketing effects, accelerating adoption rates among affluent consumers seeking evidence-based longevity interventions.

Key Market Challenges:

Limited Clinical Evidence and Regulatory Complexity Constraining Market Development

Despite promising preclinical research demonstrating senolytic agents' potential to selectively eliminate senescent cells and ameliorate age-related diseases, the global evidence base for human clinical efficacy remains remarkably constrained, with only two compounds (dasatinib and quercetin in combination therapy) having demonstrated efficacy in human clinical trials. This limited clinical validation creates significant barriers to physician adoption, as medical practitioners trained in evidence-based medicine protocols exhibit understandable hesitancy to prescribe or recommend therapeutics lacking robust phase three clinical trial data and long-term safety profiles established through post-market surveillance. The situation is further complicated by the Central Drugs Standard Control Organisation's stringent new drug approval requirements, which mandate comprehensive safety and efficacy demonstration through multi-phase clinical trials conducted per Schedule Y regulations, creating substantial financial and temporal barriers for pharmaceutical companies seeking market entry. The complexity of aging as a biological phenomenon, involving multiple interrelated pathways and cellular mechanisms, complicates clinical trial design and endpoint selection, as traditional pharmaceutical development paradigms focus on specific disease treatment rather than aging process modification. Senolytic agents' mechanism of action, targeting cellular senescence accumulation rather than specific disease symptoms, challenges conventional regulatory frameworks designed for traditional pharmaceuticals, requiring novel approaches to demonstrating clinical benefit and safety.

High Treatment Costs and Insurance Coverage Gaps Limiting Market Accessibility

Advanced anti-aging therapeutics, particularly peptide-based interventions and comprehensive regenerative medicine protocols offered by specialized longevity clinics, remain financially inaccessible to the vast majority of Indian consumers, with initial consultations and diagnostic assessments frequently exceeding typical monthly household incomes for middle-class families. The absence of insurance reimbursement for preventive and longevity-focused treatments forces patients to bear full out-of-pocket expenses, creating a significant affordability barrier that restricts market penetration to high-net-worth individuals concentrated in major metropolitan areas. This economic exclusivity is reinforced by insurance companies' classification of anti-aging interventions as elective or cosmetic procedures rather than medically necessary treatments, despite growing scientific evidence linking cellular senescence to age-related disease pathogenesis including cancer, cardiovascular disease, and neurodegenerative conditions. The pricing challenge is particularly acute for novel biopharmaceuticals like senolytic agents, which command premium pricing reflecting substantial research and development investments, complex manufacturing processes, and limited competition in early-stage markets. Even as domestic manufacturing capabilities expand and supply chain efficiencies improve, the fundamental economics of specialty pharmaceuticals development necessitate pricing structures that generate sufficient return on investment to justify continued innovation, creating inherent tension between commercial viability and broad accessibility.

Awareness Deficits Among Healthcare Professionals Impeding Clinical Adoption

The rapid evolution of senolytic science and cellular aging research has significantly outpaced medical education curricula, leaving the majority of Indian healthcare professionals unfamiliar with emerging therapeutic modalities and their appropriate clinical applications in age-related disease management. Most physicians completing medical training in India receive minimal exposure to longevity medicine concepts, cellular senescence mechanisms, or the clinical implementation of novel biopharmaceutical interventions targeting aging processes, creating knowledge gaps that manifest as reluctance to prescribe or recommend these treatments to appropriate patient populations. This educational deficit is particularly pronounced outside major metropolitan centers with teaching hospitals and research institutions, where access to continuing medical education on cutting-edge aging research remains severely limited, hindering market expansion into tier-two and tier-three cities despite growing consumer interest in preventive health interventions. The knowledge gap extends beyond basic familiarity with senolytic agents to encompass sophisticated understanding of patient selection criteria, contraindications, potential drug interactions, appropriate dosing protocols, and monitoring parameters necessary for safe and effective clinical implementation, requiring substantial professional development investments that many practicing physicians cannot accommodate within existing practice demands. The situation is further complicated by the inherent complexity of aging biology, which involves intricate interactions between genetic factors, environmental exposures, lifestyle behaviors, and multiple physiological systems, necessitating interdisciplinary expertise that transcends traditional medical specialty silos and requires physicians to synthesize knowledge across endocrinology, immunology, oncology, and other domains.

India Senolytics & Anti-aging Pharmaceuticals Market Report Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India senolytics and anti-aging pharmaceuticals market, along with forecasts at the country and regional levels for 2026-2034. The market has been categorized based on product, route of administration, and application.

Analysis by Product:

- Anti-aging Pharmaceuticals

- Senolytic Agents

The report has provided a detailed breakup and analysis of the market based on the product. This includes anti-aging pharmaceuticals and senolytic agents.

Analysis by Route of Administration:

- Clinical Use/Off-label Therapeutics

- Consumer Wellness/Longevity Use

A detailed breakup and analysis of the market based on the route of administration have also been provided in the report. This includes clinical use/off-label therapeutics and consumer wellness/longevity use.

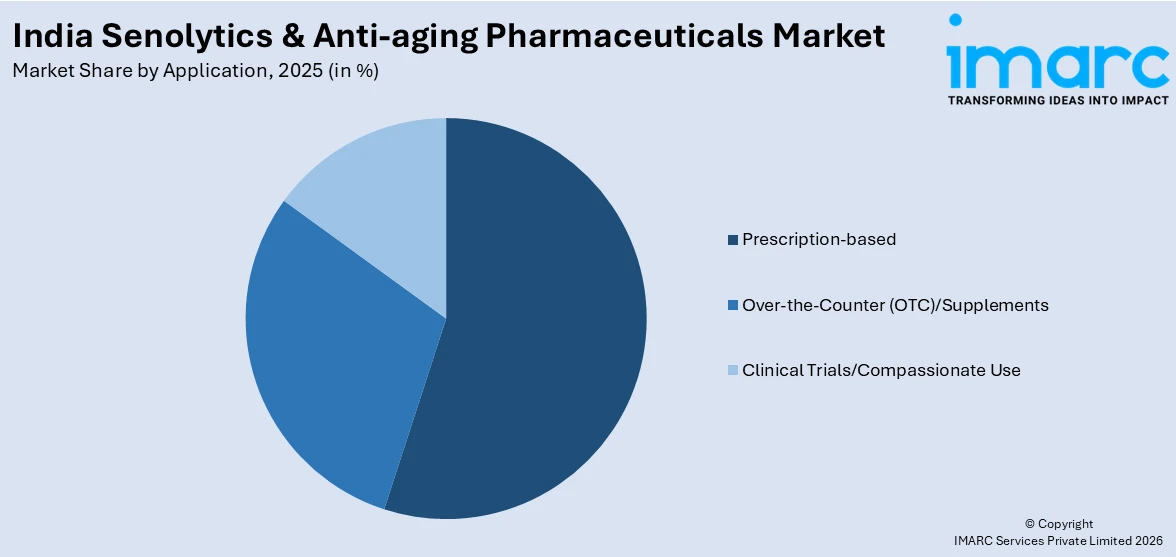

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Prescription-based

- Over-the-Counter (OTC)/Supplements

- Clinical Trials/Compassionate Use

The report has provided a detailed breakup and analysis of the market based on the application. This includes prescription-based, over-the-counter (OTC)/supplements, and clinical trials/compassionate use.

Analysis by Region:

- North India

- South India

- East India

- West India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The India senolytics and anti-aging pharmaceuticals market exhibits an emerging competitive structure characterized by limited domestic manufacturing capabilities and heavy reliance on imported specialty biopharmaceuticals, with multinational pharmaceutical companies maintaining dominant positions through established distribution networks and brand recognition. Competition primarily revolves around product quality, clinical evidence substantiation, and pricing strategies, as domestic players seek to differentiate through cost advantages while international companies leverage superior research and development capabilities and comprehensive clinical trial data. The market is witnessing increasing interest from Indian pharmaceutical companies exploring strategic partnerships, licensing agreements, and acquisition opportunities to rapidly build capabilities in the longevity therapeutics space, recognizing the substantial long-term growth potential as awareness expands and regulatory pathways become clearer.

India Senolytics & Anti-aging Pharmaceuticals Industry Latest Developments:

- January 2025: Bonerge initiated a clinical trial involving 108 participants to evaluate the combined effects of fisetin, urolithin A, and ergothioneine on skin health and multi-organ rejuvenation when administered orally, representing an important step toward validating natural senolytic compounds and expanding the evidence base for oral anti-aging pharmaceutical interventions beyond synthetic drug candidates.

- July 2024: SkinCeuticals announced the launch of P-TIOX, a clinically backed peptide serum designed to reduce the appearance of contraction lines and enhance skin radiance, demonstrating continued innovation in topical anti-aging formulations and reflecting growing consumer demand for evidence-based skincare solutions that bridge cosmetic and pharmaceutical applications.

India Senolytics & Anti-aging Pharmaceuticals Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Anti-aging Pharmaceuticals, Senolytic Agents |

| Route of Administrations Covered | Clinical Use/Off-label Therapeutics, Consumer Wellness/Longevity Use |

| Applications Covered | Prescription-based, Over-the-Counter (OTC)/Supplements, Clinical Trials/Compassionate Use |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India senolytics & anti-aging pharmaceuticals market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India senolytics & anti-aging pharmaceuticals market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India senolytics & anti-aging pharmaceuticals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Senolytics & Anti-aging Pharmaceuticals Market Report

The India senolytics & anti-aging pharmaceuticals market reached a value of USD 144.78 Million in 2025.

The market is projected to grow at a CAGR of 7.25% during 2026-2034, reaching USD 271.77 Million by 2034.

Key growth drivers include government biotech research investment, specialized wellness infrastructure expansion, peptide-based therapy adoption, and regenerative medicine demand.

The report covers segmentation by product, route of administration, application, and region. Each segment includes detailed market size and forecast analysis.

Key trends include AI-assisted drug discovery, longevity clinic proliferation, peptide therapy mainstreaming, and rising consumer interest in cellular rejuvenation interventions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)