India Server Market Size, Share, Trends and Forecast by Product, Enterprise Size, Channel, Vertical, and Region, 2026-2034

India Server Market Summary:

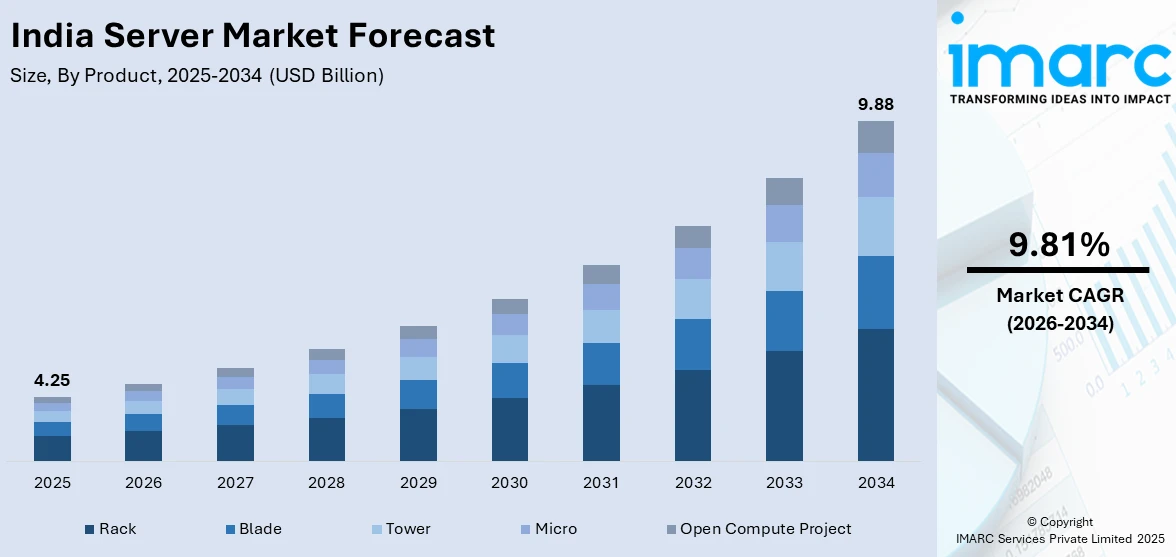

The India server market size was valued at USD 4.25 Billion in 2025 and is projected to reach USD 9.88 Billion by 2034, growing at a compound annual growth rate of 9.81% from 2026-2034.

The India server market is experiencing robust expansion driven by accelerating digital transformation initiatives across enterprises, the proliferation of hyperscale data centers, and increasing adoption of artificial intelligence and machine learning workloads. Government programs promoting digitalization and data localization requirements are encouraging investments in domestic server infrastructure. The expanding IT services sector, coupled with rising cloud computing penetration among businesses of all sizes, is further propelling demand for high-performance computing solutions across the India server market share.

Key Takeaways and Insights:

- By Product: Rack dominates the market with a share of 38% in 2025, driven by their scalability, high-density computing capabilities, and suitability for data center deployments requiring standardized infrastructure.

- By Enterprise Size: Medium leads the market with a share of 40% in 2025, owing to their rapid digital transformation journeys and increasing investments in IT infrastructure modernization.

- By Channel: Direct represents the largest segment with a market share of 35% in 2025, attributed to enterprise preference for manufacturer relationships ensuring technical support and customization.

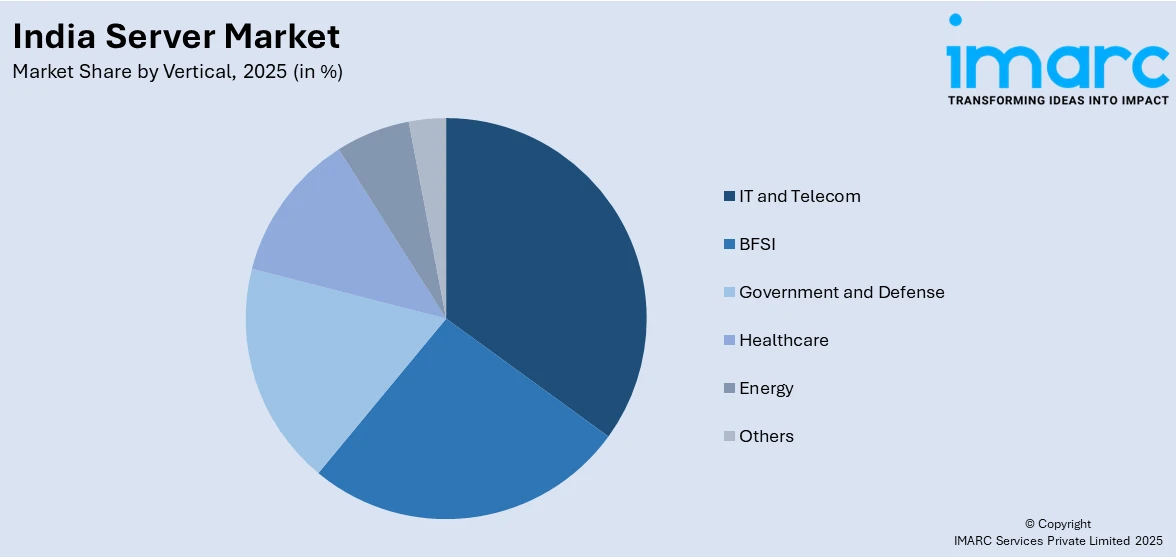

- By Vertical: IT and telecom dominate the market with a share of 33% in 2025, fueled by 5G network expansion, cloud service provider growth, and massive data processing requirements.

- By Region: North India represents 30% of the market in 2025, supported by the concentration of data centers in Delhi NCR and strong IT infrastructure development.

- Key Players: The India server market exhibits a moderately competitive landscape with global technology leaders competing alongside domestic manufacturers. Major international vendors maintain strong positions through direct sales and channel partnerships, while indigenous companies are gaining traction through government procurement preferences and Make-in-India initiatives.

To get more information on this market Request Sample

The India server market is positioned at the intersection of several transformative technological shifts reshaping enterprise computing infrastructure. The convergence of artificial intelligence adoption, cloud migration strategies, and data sovereignty requirements is creating unprecedented demand for high-performance server solutions. Organizations across banking, telecommunications, healthcare, and manufacturing sectors are investing substantially in server infrastructure to support digital operations and analytics workloads. For instance, in January 2025, Reliance Industries announced plans to construct a 3 GW data center campus in Jamnagar, Gujarat, representing one of the largest single infrastructure investments in the country and highlighting the scale of server demand. The proliferation of edge computing applications, particularly in telecommunications and industrial IoT deployments, is diversifying demand beyond traditional data center configurations toward distributed server architectures optimized for low-latency processing.

India Server Market Trends:

Artificial Intelligence Infrastructure Expansion

The deployment of AI-optimized server infrastructure is accelerating across Indian enterprises as organizations scale machine learning operations from pilot projects to production environments. GPU-enabled servers capable of handling intensive deep learning workloads are witnessing strong demand from technology companies, financial institutions, and research organizations. For instance, in December 2024, Lenovo announced plans to manufacture GPU-based servers at its Puducherry facility by mid-2025, positioning India as an export hub for AI computing hardware. The government’s IndiaAI Mission is creating a public-private infrastructure to support wider adoption of AI technologies, focusing on strengthening domestic capabilities and enabling advanced computing resources for research and enterprise applications.

Edge Computing and Distributed Architectures

The transition toward edge computing is reshaping server deployment patterns as enterprises seek to process data closer to generation points. Telecommunications operators are installing micro-data center nodes at tower sites to support 5G network functions and latency-sensitive applications. For instance, Apollo Hospitals has deployed Nutanix hyper-converged clusters across 72 facilities, enabling real-time patient monitoring while reducing IT energy consumption. Industrial manufacturers are implementing edge server solutions for predictive maintenance and quality control applications, driving demand for ruggedized, compact server configurations capable of operating in harsh environmental conditions without dedicated cooling infrastructure.

Domestic Server Manufacturing Initiatives

The Make-in-India initiative is catalyzing local server manufacturing capabilities as global technology vendors establish production facilities within the country. Government procurement preferences and production-linked incentive schemes are encouraging multinational corporations to localize assembly operations. For instance, in February 2025, Kalyani Powertrain partnered with AMD to enhance India's server infrastructure with a focus on domestic production and reducing import dependence. This trend is fostering innovation in server design and assembly processes within India. It is also creating opportunities for skilled employment and strengthening the country’s position in the global high-performance computing market.

Market Outlook 2026-2034:

The India server market outlook remains strongly positive as structural drivers including digital transformation, cloud adoption, and AI deployment, continue accelerating. Enterprise IT modernization programs across banking, telecommunications, and government sectors are creating sustained demand for contemporary server infrastructure. Recent hyperscale data center investments are expected to drive significant demand for servers over the coming years, supporting growth in procurement and deployment across India’s expanding data infrastructure. For instance, in October 2025, Google announced a USD 15 billion investment plan for an AI and data center hub in Visakhapatnam, Andhra Pradesh, reinforcing India's emergence as a regional computing infrastructure hub. The market generated a revenue of USD 4.25 Billion in 2025 and is projected to reach a revenue of USD 9.88 Billion by 2034, growing at a compound annual growth rate of 9.81% from 2026-2034.

India Server Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Rack |

38% |

|

Enterprise Size |

Medium |

40% |

|

Channel |

Direct |

35% |

|

Vertical |

IT and Telecom |

33% |

|

Region |

North India |

30% |

Product Insights:

- Rack

- Blade

- Tower

- Micro

- Open Compute Project

Rack dominates with a market share of 38% of the total India server market in 2025.

Rack servers continue to lead the market due to their adaptability, standardized design, and suitability for data center environments. They provide higher density and scalability than tower servers, allowing organizations to maximize computing performance within constrained spaces. The modular architecture of rack servers simplifies cable management, enhances cooling efficiency, and streamlines maintenance operations. These advantages make rack-mounted systems the preferred choice for enterprises, hyperscale data centers, and cloud service providers seeking reliable, high-performance infrastructure to support large-scale computing needs.

Major infrastructure investments further reinforce rack servers’ market dominance. For example, in March 2025, Larsen & Toubro revealed its intention to invest INR 3,600 crore to develop three new data centers, targeting a total combined capacity of 150 MW by 2027. Rack servers are set to form the core computing infrastructure in these facilities, highlighting their critical role in supporting large-scale, high-density deployments. This investment underscores the continued reliance on rack-mounted systems for efficient, scalable, and cost-effective data center operations in India.

Enterprise Size Insights:

- Micro

- Small

- Medium

- Large

Medium leads with a share of 40% of the total India server market in 2025.

Medium-sized enterprises are emerging as significant contributors to server market growth as they expand digital operations and modernize aging IT infrastructure. These organizations have the resources to invest in contemporary computing solutions while responding to competitive pressures that demand technology-driven business transformation. Their focus on efficiency, performance, and scalability drives the adoption of servers capable of supporting modern workloads, data processing, and hybrid IT architectures. This trend underscores the increasing role of medium enterprises in shaping demand for advanced server infrastructure across India.

The segment benefits from programs offered by cloud service providers that enable hybrid deployment models, combining on-premises servers with public cloud resources for enhanced flexibility. By leveraging such hybrid solutions, medium-sized enterprises can scale computing capacity according to business requirements while avoiding excessive upfront capital expenditure. This approach allows companies to modernize IT systems, improve operational efficiency, and integrate cloud capabilities into their workflows, positioning servers as a critical component of their digital transformation strategies in an increasingly competitive market environment.

Channel Insights:

- Direct

- Reseller

- Systems Integrator

- Others

Direct represent the highest revenue with a 35% share of the total India server market in 2025.

Direct sales channels remain the primary route for server procurement, as enterprise customers value close relationships with manufacturers that provide technical expertise, tailored solutions, and comprehensive support agreements. Large-scale server deployments often necessitate direct engagement to optimize configurations, negotiate volume pricing, and coordinate delivery logistics. Manufacturer sales teams bring specialized knowledge, assisting with solution architecture and integration planning, which enhances the overall value of procurement and ensures that enterprises receive systems aligned with their specific operational requirements.

The strength of direct sales channels is further highlighted by major industry initiatives. For instance, Hewlett Packard Enterprise launched its Made-in-India campaign in April 2024, establishing large-scale server manufacturing at Manesar, Haryana. This approach allows the company to serve enterprise clients directly while ensuring quality, customization, and timely delivery. Such strategies reinforce the preference of enterprises for direct manufacturer engagement, demonstrating how local production and hands-on support can optimize procurement outcomes and foster long-term partnerships in India’s server market.

Vertical Insights:

Access the comprehensive market breakdown Request Sample

- IT and Telecom

- BFSI

- Government and Defense

- Healthcare

- Energy

- Others

IT and telecom exhibits clear dominance with a 33% share of the total India server market in 2025.

The IT and telecommunications sector continues to lead server demand, fueled by rapid growth in data traffic, 5G network rollout, and expanding cloud infrastructure. Telecom operators such as Reliance Jio and Bharti Airtel are investing heavily in server deployments to support network functions virtualization, content delivery networks, and enterprise cloud solutions. These initiatives reflect the sector’s focus on upgrading digital infrastructure to meet increasing user demand and ensure seamless connectivity, positioning servers as a critical enabler for advanced IT and telecom operations across India.

Major IT services companies are also driving infrastructure expansion in the server market. For example, in October 2025, Tata Consultancy Services announced plans to develop 1 GW of data center capacity, committing significant investments over several years. This large-scale initiative highlights the IT sector’s dedication to scaling digital infrastructure to support enterprise clients and cloud-based services. By expanding server capacity and data center networks, IT and telecommunications companies are reinforcing India’s position as a hub for advanced computing, cloud adoption, and high-performance digital services.

Regional Insights:

- North India

- South India

- East India

- West India

North India represents the largest share of 30% of the total India server market in 2025.

North India’s server market growth is largely driven by the high concentration of data centers in the Delhi NCR region, which acts as a central hub for both government and private enterprises. Strong public sector demand, fueled by digital transformation initiatives and IT infrastructure development, creates consistent server procurement needs. The proximity to administrative headquarters and policy-making institutions further accelerates investment in advanced computing infrastructure, enabling faster deployment of enterprise and e-governance solutions across the region. This combination of factors positions North India as a leading driver of server market expansion.

Another key driver is the expansion of digital services and cloud adoption among enterprises in North India. Organizations are investing in scalable server solutions to support virtualization, content delivery, and hybrid IT deployments. Regional projects extending infrastructure to emerging cities also contribute to growth, as new facilities require high-performance servers. Additionally, partnerships between domestic and global technology providers enhance access to advanced server technologies, strengthening the overall ecosystem. These developments collectively reinforce North India’s dominance in server demand and promote broader adoption of cutting-edge computing solutions.

Market Dynamics:

Growth Drivers:

Why is the India Server Market Growing?

Hyperscale Data Center Investments

The large-scale data center investments by global technology leaders and domestic companies are reshaping server demand in India. Cloud service providers are building massive facilities to support growing customer workloads, relying on standardized server configurations optimized for cloud-native applications. These hyperscale deployments enable efficient bulk procurement and drive significant growth in server volumes. Recent announcements of major infrastructure projects, including plans by leading tech firms to establish AI and data center hubs in emerging regions, highlight the sustained momentum in India’s server market and the country’s growing prominence as a hub for advanced computing infrastructure.

Digital Transformation and Cloud Adoption

Enterprise digital transformation initiatives are generating sustained server demand as organizations modernize legacy infrastructure and implement cloud-enabled business applications. Companies across manufacturing, financial services, retail, and healthcare sectors are investing in computing infrastructure supporting analytics, automation, and customer experience enhancement. The India cloud computing market size was valued at USD 37.11 Billion in 2025 and is projected to reach USD 266.90 Billion by 2034, growing at a compound annual growth rate of 24.51% from 2026-2034, with server infrastructure forming the foundational layer. Hybrid cloud architectures, integrating on-premises servers with public cloud resources, are rapidly expanding as enterprises seek to balance high performance, scalability, and operational flexibility in their IT infrastructure and digital operations. For instance, Microsoft's January 2024 announcement of USD 3 billion investment to strengthen cloud computing and AI capabilities in India underscores hyperscaler commitment to the market.

Government Initiatives and Data Localization

Government policies promoting digitalization and data sovereignty are creating structural demand for domestic server infrastructure. The Digital India program has accelerated e-governance adoption requiring secure computing infrastructure across federal and state agencies. Data localization regulations mandate that certain categories of sensitive information be stored and processed within national borders, compelling multinational corporations to establish local computing presence. The draft National Data Centre Policy 2025 offers incentives including tax exemptions for up to 20 years, infrastructure status designation, and single-window clearances to encourage facility development. Classification of data centers as key infrastructure through inclusion in the Harmonized Master List has enabled access to favorable financing terms and policy stability, reducing investment risk and accelerating capacity expansion.

Market Restraints:

What Challenges the India Server Market is Facing?

High Infrastructure Investment Requirements

The substantial capital expenditure required for server infrastructure deployment presents barriers, particularly for small and medium enterprises. Initial hardware acquisition costs combine with supporting infrastructure requirements including power distribution, cooling systems, network connectivity, and physical security, to create significant financial hurdles. Operational expenses encompassing electricity consumption, maintenance, and software licensing further compound total cost of ownership considerations, limiting adoption among capital-constrained organizations.

Skilled Workforce Shortage

The availability of qualified IT professionals capable of managing complex server environments remains constrained relative to growing infrastructure demands. Expertise in emerging technologies including cloud architecture, containerization, and AI infrastructure management, is particularly scarce. Training and certification pipelines have not kept pace with technology evolution, creating competition for skilled personnel that elevates labor costs and delays project implementations for organizations across metropolitan and tier-2 city locations.

Power Infrastructure Limitations

Reliable power supply remains challenging in certain regions, necessitating redundant power systems and backup generation that increase infrastructure costs. High-density server configurations require substantial cooling capacity, adding to energy consumption and operational expenses. Grid connectivity constraints in emerging data center locations outside established metropolitan corridors present infrastructure development challenges, while sustainability commitments require investments in renewable energy sourcing and efficiency optimization technologies.

Competitive Landscape:

The India server market exhibits moderate competitive intensity characterized by the presence of established global technology vendors alongside emerging domestic manufacturers. International companies leverage brand recognition, extensive product portfolios, and global support capabilities to serve enterprise customers with comprehensive computing solutions. These vendors are increasingly localizing operations through manufacturing partnerships and direct investment to address procurement preferences and reduce delivery times. Indigenous manufacturers are gaining traction through government procurement programs that prioritize domestically produced equipment and through competitive pricing enabled by lower operational costs. The market is witnessing strategic partnerships between global chip designers and local system integrators to develop India-specific server configurations optimized for regional requirements. Competition extends beyond hardware to encompass financing options, managed services, and integration capabilities that differentiate vendor value propositions.

Recent Developments:

- May 2025: Onlive Server, a prominent Indian provider of web hosting, VPS, dedicated, and cloud solutions, unveiled a significant expansion of its cloud offerings with the introduction of its next-generation Cloud VPS Server Hosting platform. Now accessible across over 30 key locations worldwide, the platform emphasizes reliability, customization, and global availability. By combining flexible configuration options with consistent performance, Onlive Server enables businesses to operate efficiently and seamlessly across multiple regions, distinguishing itself from other providers in the competitive cloud hosting landscape.

- April 2025: India unveiled its first completely designed artificial intelligence (AI) server, created by VVDN Technologies, a hardware manufacturing firm headquartered in Manesar, Haryana. The announcement was made by Union Minister for Electronics and Information Technology, Ashwini Vaishnaw, during his visit to VVDN’s Global Innovation Park, where he also inaugurated a new Surface Mount Technology (SMT) production line, marking a significant step forward in the country’s indigenous server manufacturing and high-performance computing capabilities.

India Server Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Rack, Blade, Tower, Micro, Open Compute Project |

| Enterprise Sizes Covered | Micro, Small, Medium, Large |

| Channels Covered | Direct, Reseller, Systems Integrator, Others |

| Verticals Covered | IT and Telecom, BFSI, Government and Defense, Healthcare, Energy, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Server Market Report

The India server market size was valued at USD 4.25 Billion in 2025.

The India server market is expected to grow at a compound annual growth rate of 9.81% from 2026-2034 to reach USD 9.88 Billion by 2034.

Rack servers dominated the India server market with a 38% share in 2025, driven by their scalability, standardized form factors, and widespread adoption in data center environments requiring high-density computing configurations.

Key factors driving the India server market include hyperscale data center investments from global technology companies, enterprise digital transformation and cloud adoption initiatives, government programs promoting digitalization and data localization, and increasing artificial intelligence workload deployments across industries.

Major challenges include high infrastructure investment requirements for server deployment, shortage of skilled IT professionals capable of managing complex computing environments, power supply reliability and cooling infrastructure limitations in certain regions, and component supply chain constraints affecting procurement timelines.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)