India Shoulder Arthroplasty Market Size, Share, Trends and Forecast by Device, Procedure, Indication, End User, and Region, 2026-2034

India Shoulder Arthroplasty Market Summary:

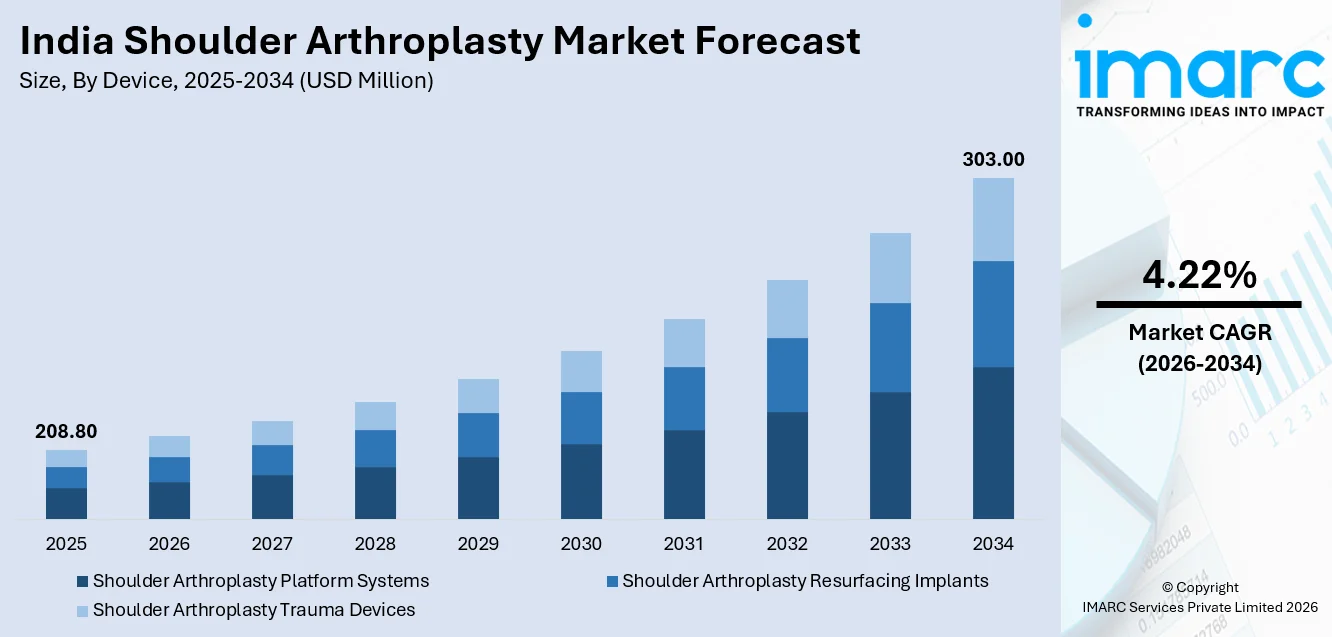

The India shoulder arthroplasty market size was valued at USD 208.80 Million in 2025 and is projected to reach USD 303.00 Million by 2034, growing at a compound annual growth rate of 4.22% from 2026-2034.

India market is experiencing steady growth driven by the country's aging demographics, rising prevalence of degenerative shoulder conditions, and improving access to advanced orthopedic care. The market reflects the growing adoption of surgical interventions for debilitating shoulder pathologies as healthcare infrastructure strengthens across urban and semi-urban regions, complemented by increasing awareness among orthopedic surgeons about contemporary implant technologies and surgical techniques, thereby expanding the India shoulder arthroplasty market share.

Key Takeaways and Insights:

- By Device: Shoulder arthroplasty platform systems dominate the market with a share of 46% in 2025, benefiting from their modular design flexibility that enables surgeons to customize implant configurations based on individual patient anatomy and pathology during procedures.

- By Procedure: Total shoulder arthroplasty leads the market with a share of 44% in 2025, as it provides comprehensive joint replacement for patients with severe glenohumeral arthritis where both humeral and glenoid surfaces require reconstruction.

- By Indication: Arthritis represents the largest segment with a market share of 41% in 2025, reflecting the substantial burden of osteoarthritis and rheumatoid arthritis affecting shoulder joints in India's aging population and middle-aged demographic.

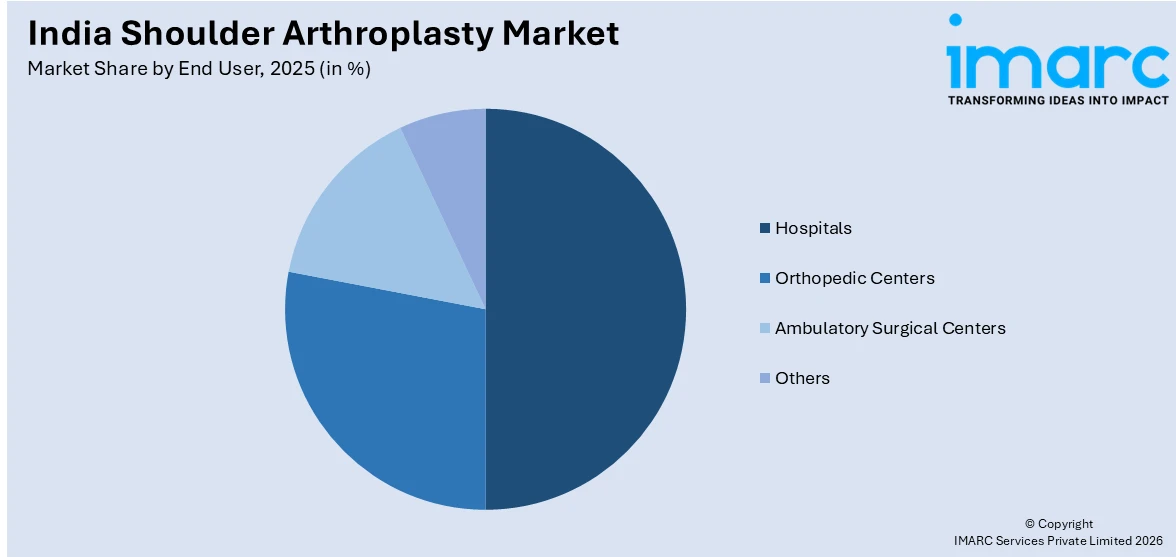

- By End User: Hospitals account for the largest segment with a market share of 50% in 2025, given their comprehensive infrastructure for complex orthopedic surgeries, availability of specialized orthopedic teams, and capacity for post-operative care management.

- By Region: North India leads with a market share of 30% in 2025, driven by the concentration of tertiary care hospitals in metropolitan areas like Delhi NCR, established orthopedic specialty centers, and higher healthcare expenditure capacity.

- Key Players: The India shoulder arthroplasty market exhibits moderate to high competitive intensity, with established multinational orthopedic device manufacturers competing alongside emerging domestic players across premium and mid-range implant segments.

To get more information on this market Request Sample

The India shoulder arthroplasty market stands at a transformative juncture where demographic shifts intersect with healthcare modernization. The country's rapidly aging population, projected to see those aged 60 and above reach 194 million by 2031 according to census projections, creates an expanding patient pool susceptible to degenerative shoulder conditions requiring surgical intervention. Apart from this, the proliferation of multi-specialty hospitals with dedicated orthopedic departments in tier-2 and tier-3 cities is democratizing access to shoulder replacement procedures previously concentrated in metropolitan centers. For instance, in 2024, Stryker, a top medical technology firm globally, has unveiled the Tornier shoulder arthroplasty range in India and has launched its first new Tornier item, the Perform® Humeral Stem, at the Shoulder Conclave in Pune. Enhanced by Blueprint planning software and the Tornier Perform anatomic and reverse glenoid, the Tornier Perform Humeral Stem provides clinical solutions for the easiest to the most intricate shoulder arthroplasty procedures. It is designed for anatomic, reverse, and hemiarthroplasty procedures of the shoulder. It also permits the transformation from an anatomic to a reverse shoulder prosthesis during revision.

India Shoulder Arthroplasty Market Trends:

Increasing Adoption of Reverse Shoulder Arthroplasty Techniques

Reverse shoulder arthroplasty is gaining significant traction among Indian orthopedic surgeons for treating complex shoulder pathologies, particularly rotator cuff tear arthropathy and proximal humerus fractures in elderly patients. This technique inverts the conventional ball-and-socket anatomy, allowing the deltoid muscle to compensate for deficient rotator cuff function. Leading orthopedic institutions including the Indian Orthopaedic Association have incorporated reverse shoulder arthroplasty training modules into advanced fellowship programs, reflecting the growing clinical acceptance of this approach. The technique's superior functional outcomes in patients with irreparable rotator cuff damage and its expanding indications are driving procedural volume growth. In 2024, Kokilaben Dhirubhai Ambani Hospital (KDAH) in Mumbai introduced an Arthrex Modular Glenoid System featuring VIP (Virtual Implant Positioning), aimed at improving shoulder replacement surgeries in India. This advancement was showcased through a live demonstration of a Reverse Total Shoulder Replacement using the VIP system.

Rising Medical Tourism for Orthopedic Procedures

India's emergence as a preferred destination for international patients seeking orthopedic procedures is contributing to shoulder arthroplasty market expansion. The cost differential remains compelling, with shoulder replacement procedures in India typically ranging from one-fifth to one-third of costs in Western countries while maintaining international quality standards. Cities like Chennai, Mumbai, and Bangalore have established dedicated international patient departments within major hospital networks, offering comprehensive packages including surgery, rehabilitation, and recovery accommodation. This medical tourism influx not only generates direct revenue but also elevates clinical standards as hospitals compete for international accreditation from bodies like Joint Commission International. IMARC Group predicts that India medical tourism market is projected to attain USD 72.1 Billion by 2034.

Integration of Patient-Specific Instrumentation and Pre-Operative Planning

Advanced pre-operative planning technologies utilizing three-dimensional CT-based modeling are increasingly being adopted by high-volume shoulder arthroplasty centers across India. These systems enable surgeons to analyze patient-specific anatomy, simulate implant positioning, and create customized surgical guides that enhance intraoperative precision. Several tertiary care centers in Delhi, Mumbai, and Chennai have established partnerships with implant manufacturers to access these planning platforms, resulting in improved component alignment accuracy and potentially better long-term outcomes. The technology addresses the anatomical variability observed in Indian populations, allowing for more tailored surgical approaches compared to standard instrumentation techniques. In 2025, JSS Hospital achieved a successful reverse total shoulder arthroplasty (RTSA) with innovative Virtual Implant Positioning (VIP) technology, representing a major breakthrough in advanced orthopedic surgery.

Market Outlook 2026-2034:

The India shoulder arthroplasty market is positioned for sustained growth throughout the forecast period, underpinned by demographic tailwinds, healthcare infrastructure expansion, and evolving clinical practices. The government's focus on strengthening tertiary healthcare facilities under programs like Pradhan Mantri Swasthya Suraksha Yojana is improving surgical capacity in underserved regions. Additionally, the inclusion of joint replacement procedures under government-sponsored health insurance schemes like Ayushman Bharat is enhancing affordability for economically vulnerable populations. The market generated a revenue of USD 208.80 Million in 2025 and is projected to reach a revenue of USD 303.00 Million by 2034, growing at a compound annual growth rate of 4.22% from 2026-2034. Moreover, several states including Maharashtra and Tamil Nadu have incorporated shoulder arthroplasty into their state health scheme coverage, removing financial barriers for eligible patients.

India Shoulder Arthroplasty Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Device |

Shoulder Arthroplasty Platform Systems |

46% |

|

Procedure |

Total Shoulder Arthroplasty |

44% |

|

Indication |

Arthritis |

41% |

|

End User |

Hospitals |

50% |

|

Region |

North India |

30% |

Device Insights:

- Shoulder Arthroplasty Resurfacing Implants

- Shoulder Arthroplasty Trauma Devices

- Shoulder Arthroplasty Platform Systems

Shoulder arthroplasty platform systems dominate with a market share of 46% of the total India shoulder arthroplasty market in 2025.

Shoulder arthroplasty platform systems represent the most widely adopted device category in India's shoulder reconstruction landscape, accounting for nearly half of all implant utilization. These modular systems offer surgeons unparalleled intraoperative flexibility through interchangeable components that can be assembled based on real-time anatomical assessment during surgery. The platform architecture typically includes multiple humeral stem options with varying sizes and offsets, interchangeable humeral heads with different diameters and heights, and glenoid components in both standard and augmented configurations. This modularity proves particularly valuable in the Indian context where anatomical variability across the diverse population necessitates customizable solutions rather than fixed-configuration implants.

The dominance of platform systems reflects their clinical versatility across multiple indications and patient demographics. Surgeons can address primary osteoarthritis with standard configurations while utilizing the same platform's specialized components for complex cases involving bone loss, deformity correction, or revision scenarios. Major implant manufacturers have responded to this preference by developing India-specific platform offerings that consider the generally smaller anthropometric dimensions observed in Indian populations compared to Western counterparts. For instance, several multinational companies now offer Asia-Pacific variants of their platform systems featuring smaller humeral stem sizes and reduced glenoid component dimensions, enhancing anatomical fit and potentially improving outcomes. The platform approach also offers economic advantages for hospitals, as maintaining inventory of one versatile system proves more cost-effective than stocking multiple specialized implant types for different indications.

Procedure Insights:

- Partial Shoulder Arthroplasty

- Total Shoulder Arthroplasty

- Revision Shoulder Arthroplasty

Total shoulder arthroplasty leads with a share of 44% of the total India shoulder arthroplasty market in 2025.

Total shoulder arthroplasty has emerged as the predominant surgical approach for addressing end-stage glenohumeral arthritis in the Indian population, replacing both the humeral head and glenoid surface to restore joint mechanics and alleviate pain. This procedure's market leadership stems from its comprehensive solution for patients presenting with bilateral joint surface deterioration, a common scenario in advanced osteoarthritis and inflammatory arthropathies like rheumatoid arthritis. The surgical technique involves resecting the arthritic humeral head and replacing it with a prosthetic ball component mounted on an intramedullary stem, while simultaneously resurfacing the glenoid with a polyethylene or metal-backed component that recreates the socket anatomy. The dual-component reconstruction addresses pain generation sources from both joint surfaces while optimizing biomechanical function.

The procedure's growing adoption in India reflects evolving surgeon confidence and patient awareness regarding shoulder replacement outcomes. Training initiatives by professional societies including the Indian Shoulder and Elbow Society have standardized surgical techniques and disseminated best practices across the orthopedic community. The availability of cemented and cementless fixation options allows surgeons to tailor the approach based on bone quality, with younger patients often receiving uncemented stems for potential biological fixation while elderly patients with osteoporotic bone receive cemented components for immediate stability. Major teaching hospitals like AIIMS Delhi and CMC Vellore have established high-volume shoulder arthroplasty programs that generate outcomes data demonstrating the efficacy of total shoulder replacement in Indian populations.

Indication Insights:

- Arthritis

- Fracture/Dislocation

- Rotator Cuff Tear Arthropathy

- Hill Sachs Defect

- Others

Arthritis exhibits a clear dominance with a 41% share of the total India shoulder arthroplasty market in 2025.

Arthritis constitutes the predominant clinical indication driving shoulder arthroplasty procedures across India, reflecting the substantial disease burden of degenerative and inflammatory joint conditions affecting the glenohumeral articulation. Osteoarthritis represents the most common arthritic etiology, typically manifesting in individuals over 60 years of age with progressive cartilage deterioration leading to bone-on-bone articulation, severe pain, and functional impairment. The pathophysiology involves gradual erosion of articular cartilage on both humeral and glenoid surfaces, often accompanied by osteophyte formation and capsular contracture that collectively compromise range of motion and quality of life. Primary osteoarthritis develops idiopathically through aging-related wear patterns, while secondary osteoarthritis may result from previous trauma, chronic instability, or avascular necrosis of the humeral head.

Rheumatoid arthritis represents the second major arthritic indication for shoulder arthroplasty in India, particularly affecting younger patient demographics through autoimmune-mediated synovial inflammation that progressively destroys cartilage and underlying bone. The Indian population exhibits relatively high rheumatoid arthritis prevalence, translating to several million individuals potentially requiring joint replacement interventions as disease progresses. The systemic nature of rheumatoid arthritis often results in polyarticular involvement, with many patients having already undergone hip or knee replacement before addressing shoulder pathology. Shoulder involvement in rheumatoid patients frequently presents with complex pathology including rotator cuff deficiency, bone loss, and soft tissue compromise, often necessitating reverse shoulder arthroplasty configurations rather than anatomic replacements. The growing recognition among rheumatologists and orthopedic surgeons about the impact of shoulder arthritis on activities of daily living is driving earlier surgical referrals and expanding the candidate pool for arthroplasty procedures.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Orthopedic Centers

- Ambulatory Surgical Centers

- Others

Hospitals leads with a share of 50% of the total India shoulder arthroplasty market in 2025.

Hospitals maintain their position as the primary setting for shoulder arthroplasty procedures in India, capturing half of all surgical volumes through their comprehensive infrastructure and multidisciplinary care capabilities. Multi-specialty and super-specialty hospitals offer the complete ecosystem required for complex joint replacement procedures, including advanced imaging facilities for pre-operative assessment, state-of-the-art operation theaters with laminar air flow systems to minimize infection risk, dedicated orthopedic surgical teams with specialized fellowship training, anesthesiology support for regional and general anesthesia techniques, and post-operative care units for monitoring patients during critical recovery phases. This integrated infrastructure proves particularly crucial for shoulder arthroplasty, which often involves elderly patients with multiple comorbidities requiring careful perioperative management to optimize outcomes and minimize complications.

The hospital dominance reflects both clinical necessity and patient preference patterns in the Indian healthcare landscape. Major hospital chains have established dedicated joint replacement programs with high-volume shoulder arthroplasty practices that generate institutional expertise and improved outcomes through procedural volume. These centers typically maintain relationships with multiple implant manufacturers, providing surgeons with choice across various platform systems and enabling hospitals to negotiate favorable pricing through volume commitments. The hospital setting also facilitates comprehensive rehabilitation services, with most major facilities operating in-house physiotherapy departments that initiate post-operative mobilization protocols and coordinate longer-term rehabilitation programs essential for functional recovery. For patients, the hospital environment provides psychological reassurance through visible infrastructure investment and perceived quality standards, factors that influence decision-making for elective procedures like shoulder replacement.

Regional Insights:

- North India

- South India

- East India

- West India

North India exhibits a clear dominance with a 30% share of the total India shoulder arthroplasty market in 2025.

North India commands the largest regional market share for shoulder arthroplasty procedures, driven by the concentration of tertiary care infrastructure in the Delhi National Capital Region and surrounding states. The region benefits from the presence of premier government institutions like All India Institute of Medical Sciences (AIIMS) Delhi, which serves as a referral hub for complex orthopedic cases from across northern states and operates high-volume joint replacement programs that establish clinical protocols and train successive generations of orthopedic surgeons. The NCR additionally hosts numerous private hospital chains with advanced orthopedic capabilities, creating a competitive healthcare marketplace that drives quality improvements and procedure volume growth.

The region's demographic profile contributes significantly to its market leadership position. North India's urban centers exhibit higher per capita incomes and greater health insurance penetration compared to many other regions, enhancing affordability and access to elective orthopedic procedures like shoulder arthroplasty. Cities like Gurgaon have emerged as medical tourism destinations for shoulder replacement, attracting patients from neighboring countries including Nepal, Bangladesh, and Middle Eastern nations seeking quality care at competitive costs. The northern region also benefits from well-established medical education ecosystems, with multiple orthopedic residency and fellowship programs producing specialists with shoulder arthroplasty training who subsequently establish practices in the region. Government initiatives including the expansion of AIIMS institutions to cities like Jodhpur and Rishikesh are further strengthening orthopedic surgical capacity across North India, positioning the region for sustained market leadership throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Shoulder Arthroplasty Market Growing?

Demographic Aging and Rising Prevalence of Degenerative Shoulder Conditions

India's demographic transition toward an aging population structure fundamentally drives shoulder arthroplasty market expansion, as advancing age represents the primary risk factor for degenerative joint conditions requiring surgical intervention. The country's elderly population is growing at an accelerated pace, with those aged 60 and above projected to constitute approximately fifteen percent of the total population by 2030 according to demographic projections. This age cohort exhibits substantially higher incidence rates of glenohumeral osteoarthritis, rotator cuff pathology, and other shoulder disorders that progressively compromise joint function and quality of life. The biological aging process involves cartilage degeneration, reduced synovial fluid production, altered biomechanics from muscle weakening, and diminished tissue healing capacity, collectively predisposing elderly individuals to shoulder pathology warranting arthroplasty consideration. Beyond chronological aging, lifestyle factors including sedentary behavior patterns and rising obesity rates compound joint stress and accelerate degenerative processes affecting shoulder articulations across middle-aged populations as well.

Expanding Healthcare Infrastructure and Surgical Capacity

Systematic healthcare infrastructure development across India is removing geographical and logistical barriers that historically limited access to advanced orthopedic procedures like shoulder arthroplasty. Government initiatives including Pradhan Mantri Swasthya Suraksha Yojana aim to establish multi-specialty hospitals and upgrade existing district hospitals with orthopedic surgical capabilities in underserved regions. A key emphasis throughout 2025 was the enhancement of health infrastructure through the PM–Ayushman Bharat Health Infrastructure Mission (PM-ABHIM). Initiated to improve pandemic readiness and public health infrastructure, the initiative sanctioned more than 10,600 Ayushman Arogya Mandirs, 2,151 Block Public Health Units, 744 Integrated Public Health Laboratories, and 621 Critical Care Blocks nationwide. Private sector investment has complemented these public initiatives, with hospital chains expanding into tier-2 and tier-3 cities where growing middle-class populations demand quality healthcare services. This infrastructure proliferation manifests in increasing numbers of operation theaters equipped with modern surgical technology, availability of trained orthopedic surgeons through expanding residency programs, and establishment of blood banks and intensive care units essential for supporting complex surgical procedures.

Improving Insurance Coverage and Financial Accessibility

Enhanced health insurance penetration and government-sponsored coverage schemes are systematically reducing financial barriers to shoulder arthroplasty procedures across socioeconomic segments. The Ayushman Bharat Pradhan Mantri Jan Arogya Yojana provides health coverage of ₹ 5,00,000 per family per year for secondary and tertiary care hospitalization to over 10.74 crores poor and vulnerable families (around 50 crore beneficiaries) that form bottom 40% of the Indian population. Several state governments have supplemented central schemes with additional coverage programs that further expand the insured population. This expanding insurance architecture transforms shoulder arthroplasty from an out-of-pocket expense, often financially prohibitive for average families, to a covered procedure accessible through insurance mechanisms.

Market Restraints:

What Challenges the India Shoulder Arthroplasty Market is Facing?

Limited Awareness and Late-Stage Presentation

Insufficient awareness about shoulder arthroplasty as a treatment option results in many patients enduring prolonged disability before seeking surgical consultation, with some never accessing appropriate care despite severe functional impairment. Cultural factors including tolerance for chronic pain and preference for conservative management contribute to delayed presentations. Educational gaps among primary care physicians regarding appropriate referral timing mean patients often exhaust ineffective treatments before reaching orthopedic specialists. This awareness deficit particularly affects rural and semi-urban populations where medical literacy remains limited and access to specialized orthopedic consultation proves challenging.

Cost Sensitivity and Economic Constraints

Despite insurance expansion, significant portions of India's population remain uninsured or underinsured, rendering shoulder arthroplasty financially inaccessible for many potential candidates. Implant costs represent substantial components of total procedure expenses, with premium systems imported from multinational manufacturers commanding prices beyond the reach of economically constrained patients. Even insured individuals face gaps in coverage including co-payment requirements, hospitalization caps, and exclusions for advanced implant technologies. The out-of-pocket burden extends beyond surgery itself to encompass pre-operative investigations, post-operative medications, and rehabilitation services that collectively create financial strain for middle and lower-income families.

Shortage of Specialized Shoulder Surgeons and Geographic Concentration

India faces an undersupply of orthopedic surgeons with specialized shoulder arthroplasty training, with expertise heavily concentrated in metropolitan centers leaving vast geographic areas underserved. Shoulder replacement requires specific technical skills and anatomical knowledge distinct from other joint arthroplasties, yet fellowship training programs remain limited compared to countries with mature shoulder arthroplasty markets. The urban-rural divide in specialist availability means patients in smaller cities often must travel considerable distances for consultation and surgery, creating logistical barriers and deterring some from pursuing treatment. This specialist shortage also limits case volumes at many centers, preventing surgeons from achieving the procedural experience associated with optimal outcomes.

Competitive Landscape:

The India shoulder arthroplasty market exhibits a moderately consolidated competitive structure with established multinational orthopedic device manufacturers maintaining dominant market positions alongside emerging domestic players pursuing market share through differentiated strategies. Leading international companies leverage their extensive product portfolios encompassing multiple platform systems, comprehensive instrumentation sets, and established clinical evidence from global markets to capture premium segments focused on advanced implant technologies and reverse shoulder arthroplasty configurations. These multinational entities typically maintain direct distribution operations in major metropolitan markets while engaging regional distributors for penetration into secondary and tertiary cities, creating extensive commercial footprints that reach high-volume hospitals and specialty orthopedic centers. Domestic manufacturers have carved niches by offering value-oriented implant systems targeting cost-conscious segments and government hospitals operating under budget constraints, competing primarily through aggressive pricing while gradually enhancing product sophistication. The competitive dynamics reflect tension between innovation-driven differentiation pursued by premium players and price-based competition characterizing value segments, with hospitals and surgeons balancing outcome optimization against economic considerations when selecting implant systems.

India Shoulder Arthroplasty Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Devices Covered | Shoulder Arthroplasty Resurfacing Implants, Shoulder Arthroplasty Trauma Devices, Shoulder Arthroplasty Platform Systems |

| Procedures Covered | Partial Shoulder Arthroplasty, Total Shoulder Arthroplasty, Revision Shoulder Arthroplasty |

| Indications Covered | Arthritis, Fracture/Dislocation, Rotator Cuff Tear Arthropathy, Hill Sachs Defect, Others |

| End Users Covered | Hospitals, Orthopedic Centers, Ambulatory Surgical Centers, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Shoulder Arthroplasty Market Research Report and Industry Forecast Report

The India shoulder arthroplasty market size was valued at USD 208.80 Million in 2025.

The India shoulder arthroplasty market is expected to grow at a compound annual growth rate of 4.22% from 2026-2034 to reach USD 303.00 Million by 2034.

Shoulder arthroplasty platform systems dominated the device segment with a 46% market share in 2025, driven by their modular design flexibility that enables surgeons to customize implant configurations intraoperatively based on patient-specific anatomy and pathology, along with their clinical versatility across multiple indications from primary arthritis to complex revision scenarios.

Key factors driving the India shoulder arthroplasty market include the country's rapidly aging demographic profile with increasing prevalence of degenerative shoulder conditions, systematic expansion of healthcare infrastructure bringing advanced orthopedic surgical capabilities to previously underserved regions and improving financial accessibility through government-sponsored insurance schemes and growing private coverage penetration.

Major challenges include limited patient and primary physician awareness about shoulder arthroplasty leading to delayed presentations and underutilization, persistent cost sensitivity with substantial uninsured populations finding procedures financially inaccessible despite insurance expansion, shortage of specialized shoulder surgeons with geographic concentration in metropolitan areas creating access barriers for rural and semi-urban populations, and implant cost pressures particularly for advanced technologies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)