India Smart Grid Market Size, Share, Trends and Forecast by Component, End User, and Region, 2026-2034

India Smart Grid Market Summary:

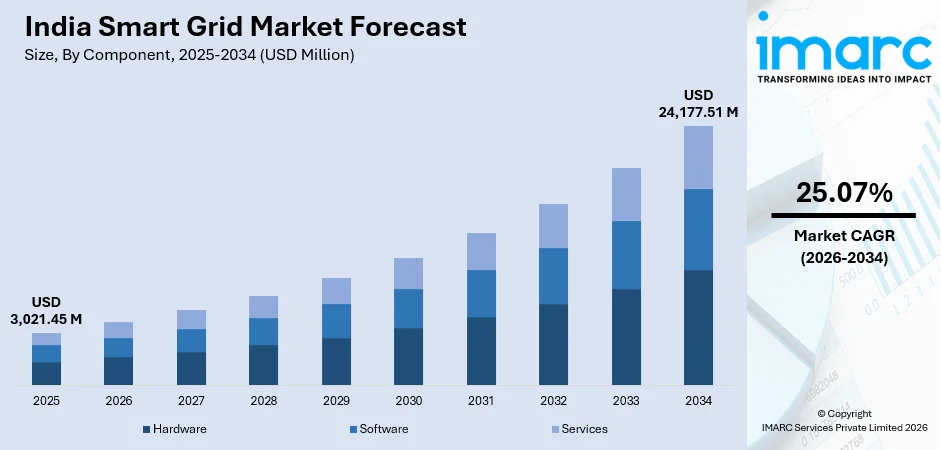

The India smart grid market size was valued at USD 3,021.45 Million in 2025 and is projected to reach USD 24,177.51 Million by 2034, growing at a compound annual growth rate of 25.07% from 2026-2034.

India's smart grid sector is undergoing rapid transformation as the country intensifies efforts to modernize its aging electricity distribution infrastructure and integrate expanding renewable energy capacity. Government-led digitalization programs, rising electricity demand across industrial and urban centers, and the growing necessity for real-time grid monitoring are fundamentally reshaping how power is generated, transmitted, and consumed, driving widespread adoption of advanced metering and automation technologies throughout the India smart grid market.

Key Takeaways and Insights:

- By Component: Hardware dominates the market with a share of 55.0% in 2025, driven by large-scale advanced metering infrastructure rollout under government schemes, particularly AMI meters deployed across distribution networks nationwide.

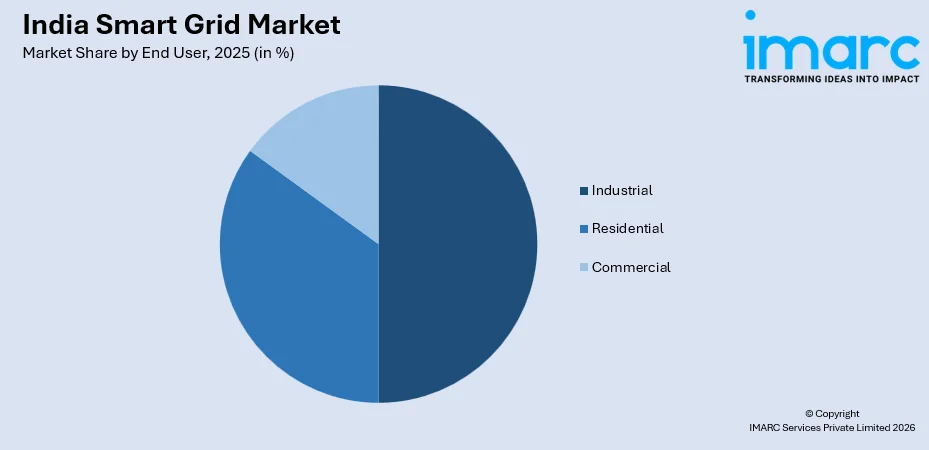

- By End User: Industrial leads the market with a share of 45.0% in 2025, supported by high electricity consumption, demand for reliable real-time power management, and growing adoption of demand response programs in manufacturing zones.

- By Region: West and Central India represents the largest regional share of 30.0% in 2025, anchored by robust industrial bases in Maharashtra and Gujarat, which host major smart grid pilot projects and significant renewable energy transmission infrastructure.

- Key Players: The India smart grid market features a moderately fragmented competitive landscape, with global technology conglomerates, domestic engineering companies, and specialized metering solution providers competing across hardware, software, and services segments.

To get more information on this market Request Sample

India's smart grid landscape is being reshaped by converging forces including escalating electricity demand, policy-driven infrastructure investment, and the imperative to integrate variable renewable energy at scale. Government-led initiatives are playing a central role in accelerating the modernization of India’s electricity distribution network through the deployment of advanced metering infrastructure, automated distribution systems, and upgraded substations. These programs are encouraging utilities to adopt digital technologies that improve grid visibility and operational efficiency. At the same time, the integration of technologies such as IoT, artificial intelligence, and cloud-based platforms is transforming grid management by enabling predictive maintenance, improved monitoring, and more efficient demand response mechanisms. Together, these developments are strengthening the reliability, flexibility, and overall performance of the power distribution network while supporting the transition toward a more intelligent and responsive electricity grid. For instance, in February 2025, a major Indian power utility partnered with a leading cloud technology provider to migrate 23 critical grid management applications to AI-powered platforms, enabling real-time data analytics and significantly reducing operational disruptions across its distribution network.

India Smart Grid Market Trends:

Large-Scale Deployment of Advanced Metering Infrastructure

India's smart metering rollout has emerged as a defining trend, underpinned by the RDSS which mandates 250 million prepaid smart meter installations and the NSGM framework that has structured deployment since 2015. The growing deployment of consumer-level smart meters is strengthening the adoption of advanced metering infrastructure across several Indian states. These systems enable two-way communication between electricity distribution companies and consumers, supporting features such as dynamic pricing, remote connection management, and detailed energy monitoring. As a result, utilities can improve operational efficiency, enhance billing accuracy, and better manage electricity consumption across urban and semi-urban distribution networks.

AI and IoT Integration in Grid Operations

Electric utilities in India are increasingly integrating artificial intelligence and Internet of Things technologies into grid management systems to enhance operational efficiency and reliability. These technologies support predictive maintenance, rapid fault detection, and improved load management across electricity networks. Collaboration with global cloud technology providers is further enabling the development of advanced data platforms that allow utilities to analyze large volumes of grid data and optimize performance. At the transmission level, real-time monitoring systems are being implemented to improve visibility of grid conditions and support timely interventions. For instance, in November 2025, the Eastern Regional Load Dispatch Centre under Grid Controller of India Limited partnered with the Indian Institute of Technology Delhi to develop a smart device featuring a Real Time-of-Use tariff–based demand-side management controller for improved electricity load management.

Renewable Energy Integration Driving Grid Modernization

The rapid expansion of renewable energy capacity in India is increasing the need for advanced grid management systems capable of handling the variability of solar and wind power generation. Integrating large volumes of renewable energy into the electricity network requires stronger transmission infrastructure and the adoption of smart grid technologies that support grid stability and efficient power flow. As a result, utilities and policymakers are investing in solutions such as battery energy storage systems, automated substations, and digital grid management platforms. These developments are particularly prominent in states with high renewable energy penetration, where modern grid technologies are essential for maintaining reliability and supporting sustainable energy integration.

Market Outlook 2026-2034:

The India smart grid market is set for sustained expansion throughout the forecast period, driven by continued policy support, increasing renewable energy penetration, and a growing imperative for grid resilience across industrial and urban centers. The ongoing nationwide smart meter rollout under government-led distribution sector reforms is expected to stimulate significant investment in communication technologies, grid management software, and related service solutions. As renewable energy capacity continues to expand, utilities and state authorities are increasingly focusing on modernizing grid infrastructure capable of supporting bidirectional power flows and integrating distributed energy resources. The market generated a revenue of USD 3,021.45 Million in 2025 and is projected to reach a revenue of USD 24,177.51 Million by 2034, growing at a compound annual growth rate of 25.07% from 2026-2034.

India Smart Grid Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Hardware |

55.0% |

|

End User |

Industrial |

45.0% |

|

Region |

West and Central India |

30.0% |

Component Insights:

- Software

- Advanced Metering Infrastructure

- Smart Grid Distribution Management

- Smart Grid Network Management

- Substation Automation

- Others

- Hardware

- Sensor

- Programmable Logic Controller

- AMI Meter

- Networking Hardware

- Others

- Services

- Consulting

- Support and Maintenance

- Deployment and Integration

Hardware leads the market with a share of 55.0% of the total India smart grid market in 2025.

The hardware segment's dominance is a direct consequence of India's large-scale rollout of physical devices underpinning grid digitalization. AMI meters represent the most critical hardware component, serving as the primary interface for two-way communication between utilities and consumers. Government-backed distribution reforms are driving large-scale deployment of consumer smart meters, highlighting the significant demand for advanced metering hardware. Advanced Metering Infrastructure systems enable features such as time-based pricing, prepaid billing, and remote connection management. These capabilities help utilities improve billing accuracy, enhance operational efficiency, and reduce distribution losses across both urban and semi-urban electricity networks.

Networking hardware and programmable logic controllers (PLCs) are gaining momentum as distribution utilities upgrade substation infrastructure and deploy SCADA systems for real-time grid management. The Unified Real Time Dynamic State Measurement (URTDSM) project had installed 1,093 phasor measurement units (PMUs) on 400 kV lines and 148 on 765 kV lines as of early 2025, reflecting the growing deployment of sensing and monitoring hardware across India's high-voltage transmission network. Sensor technologies are also proliferating across distribution feeders, enabling automated fault detection, voltage regulation, and load balancing that directly improve grid reliability and reduce outage durations for all consumer categories.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

Industrial represents the largest share of 45.0% of the total India smart grid market in 2025.

Industrial consumers represent the largest end-user category given their disproportionately high electricity consumption and the critical importance of power quality and reliability to manufacturing operations. Smart grid technologies enable real-time energy monitoring, demand response participation, and peak load management, allowing industrial units to optimize consumption and reduce energy costs. The Smart Grid Naroda Pilot Project in Gujarat, implemented by the Uttar Gujarat Vij Company Limited (UGVCL) with Ministry of Power funding, specifically incorporated AMI systems for both residential and industrial consumers, demonstrating measurable efficiency gains in peak load management and billing accuracy in high-consumption industrial settings.

India's manufacturing sector, bolstered by the "Make in India" initiative and the expansion of special economic zones and industrial corridors, has significantly elevated demand for uninterrupted and high-quality power supply. Industrial users are increasingly deploying smart energy management systems to meet sustainability targets and reduce carbon footprints, particularly in energy-intensive sectors such as steel, cement, and chemicals. The Aurangabad Industrial City (AURIC) in Maharashtra, inaugurated as India's first greenfield industrial smart city, exemplifies how industrial zones are being designed with integrated smart grid infrastructure from inception, reinforcing the industrial segment's commanding position in the overall market.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India exhibits a clear dominance with a 30.0% share of the total India smart grid market in 2025.

West and Central India's market leadership is underpinned by the high industrial density and energy demand in Maharashtra and Gujarat, two of India's highest electricity-consuming states. Gujarat has played a pioneering role in smart grid adoption through early pilot projects and large-scale renewable energy developments that require advanced grid management systems. These initiatives highlight the growing need for modernized electricity infrastructure capable of efficiently handling complex power flows. In response, government programs aimed at upgrading distribution networks are prioritizing regions with high energy consumption, supporting the deployment of advanced grid technologies and strengthening overall system reliability.

The region's smart grid momentum is further reinforced by its renewable energy leadership. For instance, in November 2024, POWERGRID acquired the Khavda V-A Power Transmission Limited SPV to construct a ±800 kV HVDC link capable of transmitting 6,000 MW from Khavda in Gujarat to Nagpur in Maharashtra. Sterlite Power's Lakadia-Vadodara Transmission Project, spanning 335 kilometers and representing an investment of USD 244.4 million, further exemplifies the scale of grid infrastructure investment linking renewable generation zones in Western India to national load centers, creating an integrated smart grid corridor with significant monitoring and automation requirements.

Market Dynamics:

Growth Drivers:

Why is the India Smart Grid Market Growing?

Government Policy Momentum and Large-Scale Funding Programs

Government-led programs such as the National Smart Grid Mission and the Revamped Distribution Sector Scheme are creating a structured pathway for the deployment of smart grid infrastructure across India. These initiatives encourage the adoption of prepaid smart meters and the modernization of distribution networks to improve operational efficiency and reduce system losses. Innovative financial models involving Advanced Metering Infrastructure Service Providers allow private participants to finance and manage metering systems, reducing the upfront investment burden on distribution companies and enabling faster rollout. Continued policy support and targeted funding for grid modernization are stimulating demand for hardware, software, and service solutions throughout the smart grid ecosystem.

Accelerating Renewable Energy Integration

India’s push to significantly expand non-fossil fuel energy capacity has made grid modernization a critical national priority. The growing share of renewable sources such as solar and wind introduces variability in power generation, creating a need for advanced grid technologies that support real-time balancing, demand response, and energy storage integration. As renewable energy projects continue to expand across several states, utilities are increasingly focusing on upgrading transmission and distribution infrastructure. These improvements are essential to ensure reliable electricity delivery, efficiently manage fluctuating renewable output, and support the long-term transition toward a cleaner and more resilient energy system. The Green Energy Corridor Phase-II, with an investment of INR 12,031.33 crore, is specifically designed to integrate 20 GW of renewable capacity by 2026, supported by advanced smart grid technologies. This deepening renewable penetration is fundamentally structuring the long-term investment case for smart grid technology deployment across the Indian power sector, creating robust demand for distribution automation, grid-edge sensors, and energy management platforms.

Rising Industrial Electricity Demand and Energy Efficiency Imperative

India's industrial sector is the single largest consumer of electricity nationally, and the growing scale of manufacturing activity, supported by Make in India, Production Linked Incentive (PLI) schemes, and the expansion of dedicated freight and industrial corridors, has significantly elevated demand for smart, reliable power management. Industrial users are increasingly deploying smart grid solutions to optimize consumption, participate in demand response programs, and meet sustainability targets for regulatory compliance and ESG reporting. The Smart Grid Naroda Pilot Project in Gujarat, implemented by UGVCL under Ministry of Power funding, demonstrated measurable gains in peak load management and energy billing efficiency, specifically among industrial consumers. As India's industrial base expands alongside GDP growth, utilities and industrial users are jointly investing in smart metering, real-time monitoring, and distribution automation to ensure power quality, operational continuity, and cost efficiency.

Market Restraints:

What Challenges the India Smart Grid Market is Facing?

High Capital Requirements and DISCOM Financial Weakness

Smart grid implementation requires significant initial investment in advanced metering hardware, communication networks, and digital management systems. However, many state electricity distribution companies face financial constraints that limit their ability to independently finance modernization projects. As a result, large-scale smart grid deployment often depends on government support programs and private-sector participation to fund infrastructure upgrades.

Uneven Smart Meter Deployment Across States

Progress in smart meter rollout remains highly uneven across Indian states. While Delhi has achieved full consumer smart metering and states such as Bihar and Assam have led early RDSS-backed deployment, Maharashtra and Rajasthan lag significantly behind sanctioned targets, creating operational inconsistencies and limiting the network-wide data benefits of advanced metering infrastructure.

Cybersecurity and Grid Vulnerability Risks

The increasing digitalization of power infrastructure introduces significant cybersecurity risks, as smart meters, communication networks, and grid management software become potential vectors for cyberattacks. Ensuring robust data security across millions of connected devices requires sophisticated encryption standards and continuous monitoring, a complex and costly challenge for utilities operating across India's heterogeneous grid environment.

Competitive Landscape:

The India smart grid market is moderately fragmented, characterized by the participation of global technology conglomerates, domestic engineering companies, and specialized metering solution providers competing across hardware, software, and services segments. Leading global players maintain strong positions in grid automation, SCADA systems, and high-voltage transmission solutions, while domestic firms have carved significant roles in smart meter manufacturing, AMISP operations, and distribution automation. The RDSS framework has intensified competition among AMISPs for large-scale state-level meter deployment contracts, with multiple entities forming strategic joint ventures and partnerships to strengthen technical and financial capabilities. The market's ongoing digitalization, encompassing AI-based grid analytics and IoT-driven monitoring, is expanding the competitive perimeter to include cloud technology and data analytics providers.

Recent Developments:

- July 2025: The Indian Ministry of Power reported that 3.46 crore smart electricity meters had been installed across the country as of June 30, 2025, with 2.27 crore units sanctioned under the Revamped Distribution Sector Scheme. The Ministry confirmed that full installation of all sanctioned meters is targeted for completion by March 2028, marking a significant milestone in India's distribution network digitalization drive.

- February 2025: EDF India and Actis announced a joint venture to develop and operate an Advanced Metering Infrastructure Service Provider (AMISP) platform in India, aimed at strengthening the country's smart metering ecosystem and improving power distribution efficiency for consumers across multiple states.

India Smart Grid Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| End Users Covered | Residential, Commercial, Industrial |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Smart Grid Market Report

The India smart grid market size was valued at USD 3,021.45 Million in 2025.

The India smart grid market is expected to grow at a compound annual growth rate of 25.07% from 2026-2034 to reach USD 24,177.51 Million by 2034.

The hardware segment held the largest share of the India smart grid market in 2025, accounting for 55.0% of total revenue. Its dominance is driven by the large-scale deployment of AMI meters, sensors, and networking hardware under the RDSS and NSGM, representing the physical foundation of India's grid digitalization initiative.

Key factors driving the India smart grid market include government-led initiatives such as the NSGM and RDSS, accelerating integration of renewable energy requiring real-time grid management, growing industrial electricity demand, widespread adoption of AMI technologies and distribution automation, and increasing deployment of artificial intelligence and IoT across grid operations.

Major challenges include high capital expenditure requirements for grid infrastructure upgrades, financial distress among state electricity distribution companies, inconsistent smart meter deployment across states, cybersecurity vulnerabilities in increasingly digitalized grid infrastructure, and the technical workforce gaps needed for large-scale smart grid operations and maintenance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade