India Smart Packaging Market Size, Share, Trends and Forecast by Technology, Industry Vertical, and Region, 2026-2034

India Smart Packaging Market Size, Share, Trends & Forecast (2026-2034)

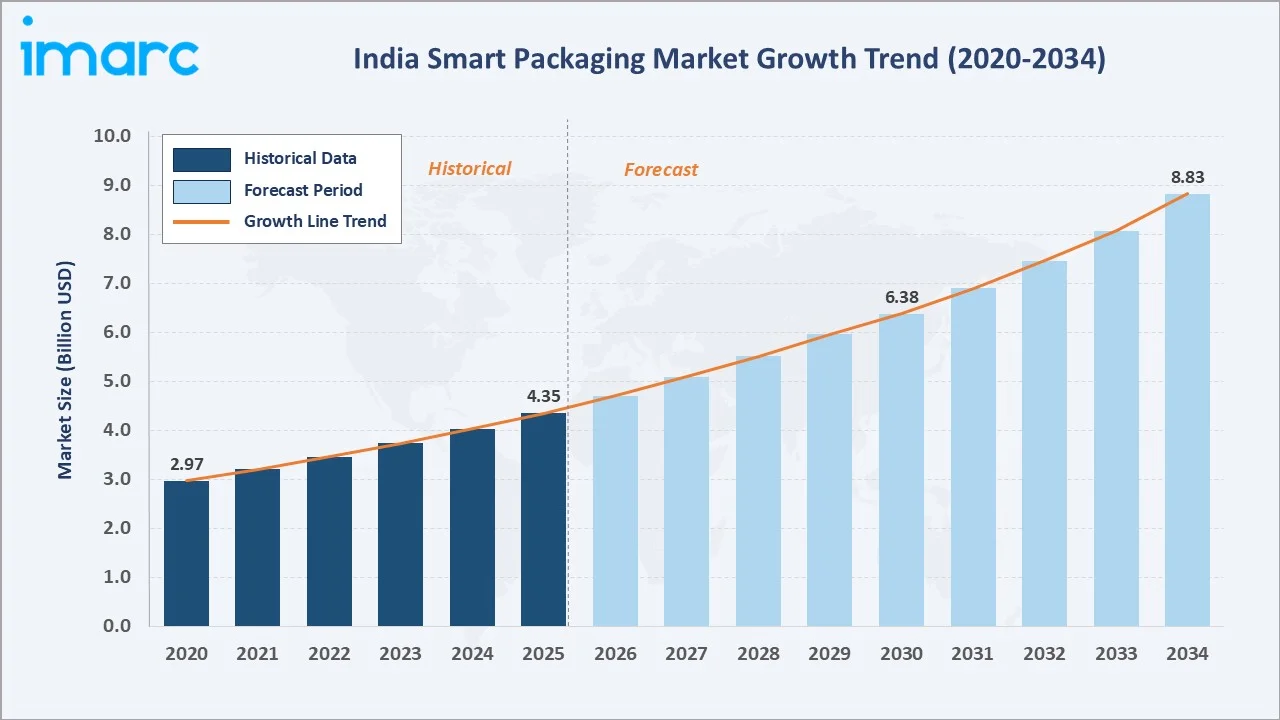

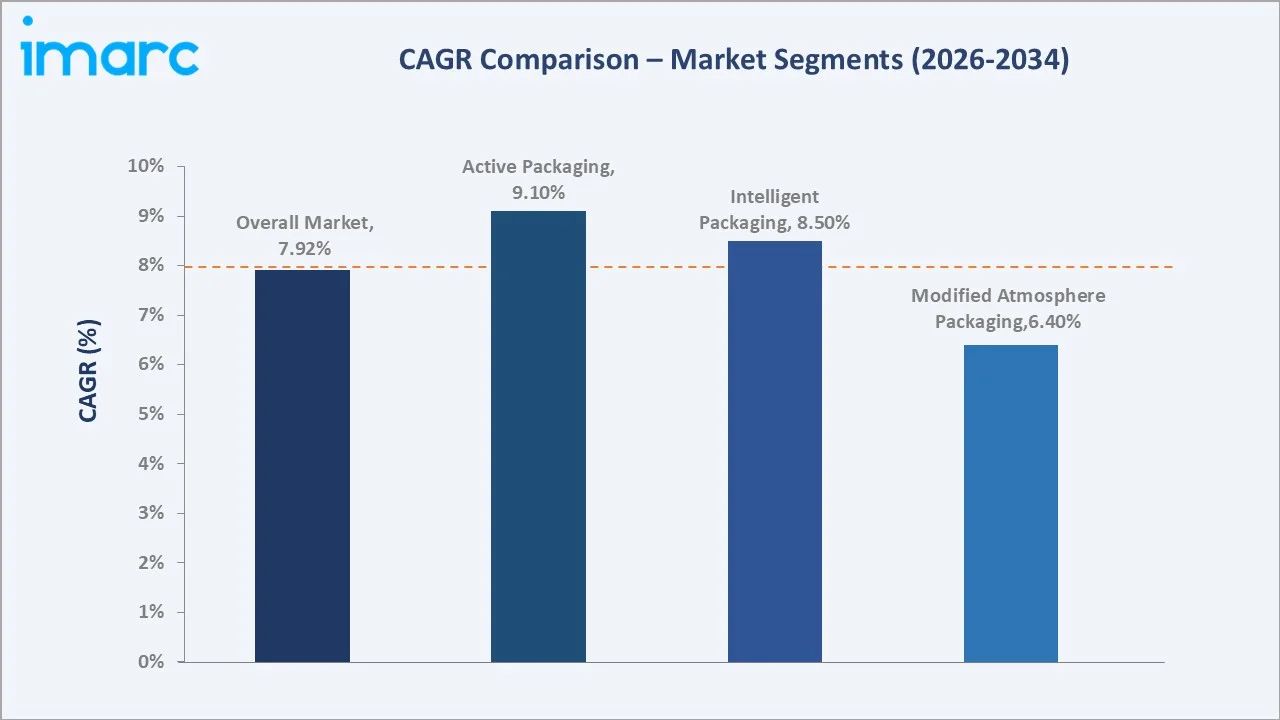

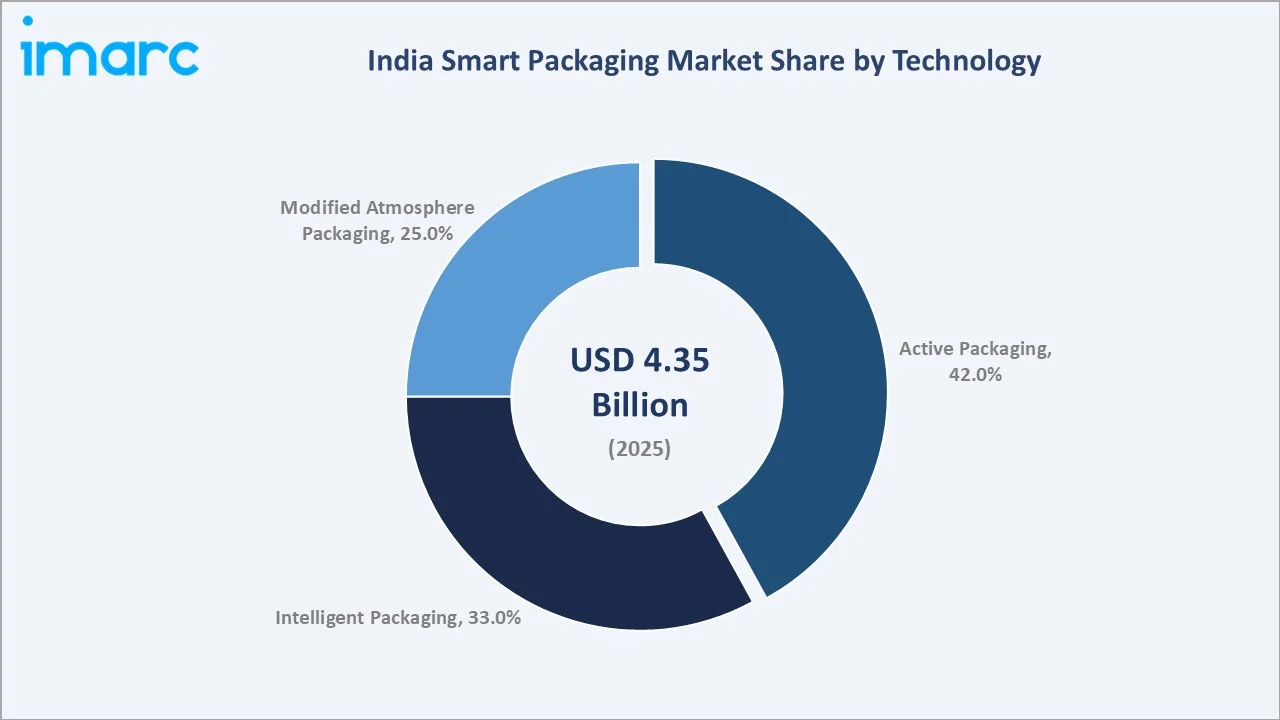

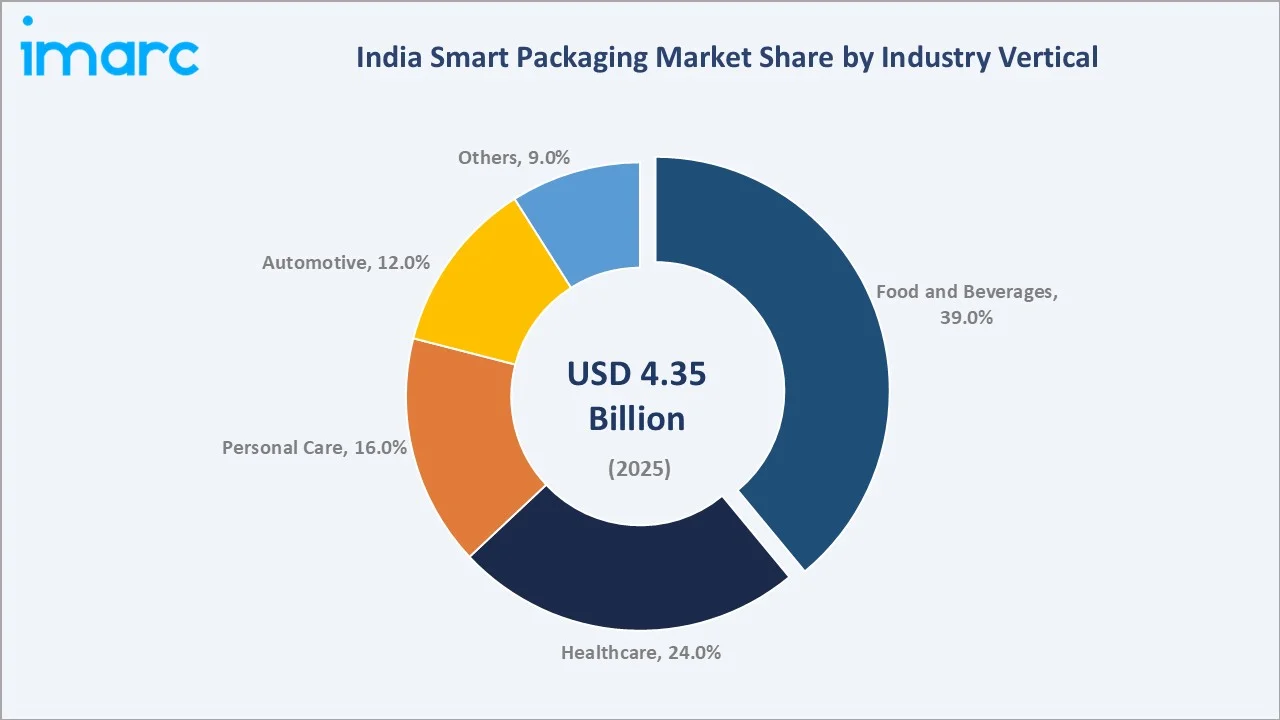

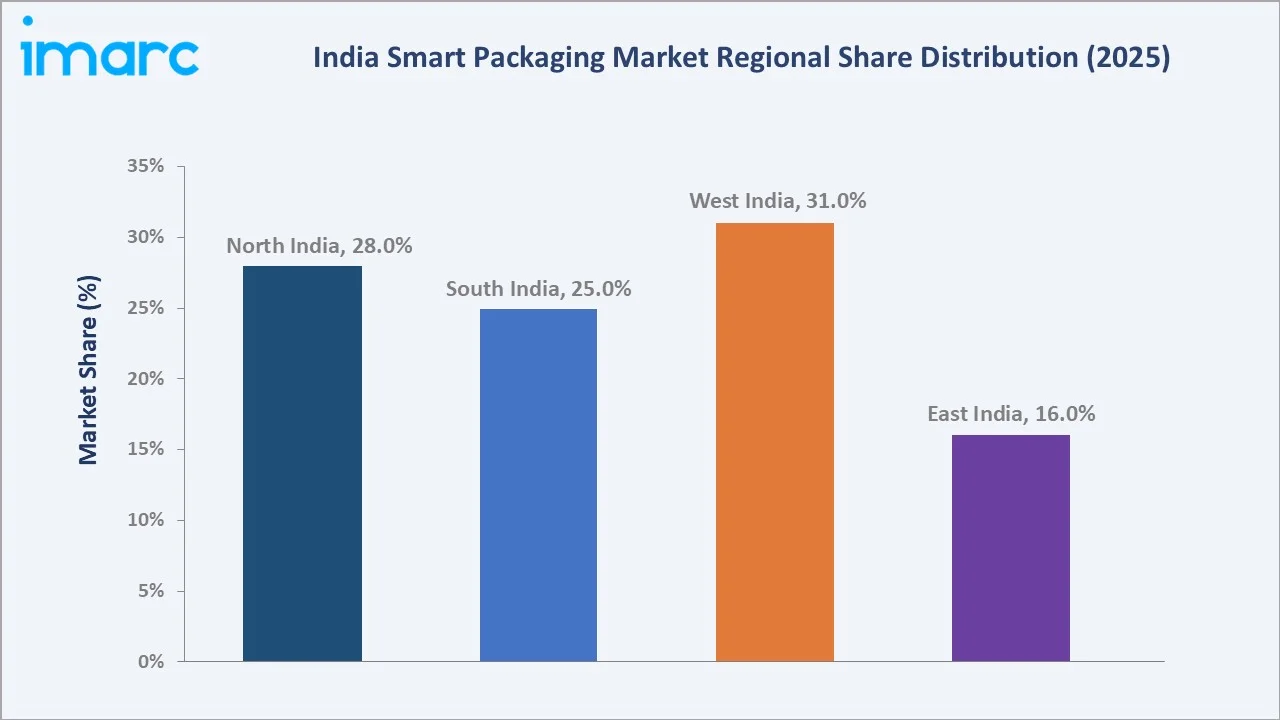

The India smart packaging market reached USD 4.35 Billion in 2025 and is projected to reach USD 8.83 Billion by 2034, growing at a CAGR of 7.92% during 2026-2034. The market is driven by rising consumer demand for transparency, product authentication, and real-time supply chain visibility. Expanding adoption of RFID, NFC, QR codes, and IoT-enabled technologies across food, pharmaceuticals, and personal care is fueling growth. Active Packaging leads at 42.0% technology share. Food and Beverages dominate industry verticals at 39.0%. West India commands 31.0% of the regional market share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.35 Billion |

|

Forecast Market Size (2034) |

USD 8.83 Billion |

|

CAGR (2026-2034) |

7.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Technology |

Active Packaging (42.0%, 2025) |

|

Dominant Industry Vertical |

Food and Beverages (39.0%, 2025) |

|

Leading Region |

West India (31.0%, 2025) |

India smart packaging market expanded from USD 2.97 Billion in 2020 to USD 4.35 Billion in 2025, anchored at USD 6.38 Billion in 2030, and forecast to reach USD 8.83 Billion by 2034. The market is commercially unique-combining one of Asia's fastest-growing consumer economies with a sharp rise in digital literacy, anti-counterfeiting mandates in pharmaceuticals, and extensive e-commerce logistics expansion.

To get more information on this market, Request Sample

Active Packaging grows robustly through moisture control and antimicrobial solutions critical to India's food supply chain. Intelligent Packaging is the fastest-growing sub-segment, driven by QR code adoption, RFID mandates in pharma track-and-trace, and consumer demand for product authentication.

Executive Summary

India smart packaging market at USD 4.35 Billion in 2025 represents one of Asia's most commercially dynamic packaging markets. The country's rapid digitalization, pharmaceutical sector expansion, and food safety regulatory tightening are jointly accelerating adoption of intelligent and active packaging technologies. The market is projected to reach USD 8.83 Billion by 2034 at a 7.92% CAGR. India's pharmaceutical industry-valued at over USD 50 Billion-is a primary demand anchor, requiring serialization, tamper-evident seals, and blockchain-based track-and-trace systems.

Active Packaging at 42.0% leads through its critical role in extending shelf life for perishable food products and maintaining sterile conditions in medical packaging. Intelligent Packaging at 33.0% reflects the fast-rising adoption of QR codes, NFC tags, and RFID tracking devices. Food and Beverages dominate industry verticals at 39.0%, supported by India's massive organized retail growth and cold chain logistics investments. West India commands 31.0% regional leadership through Mumbai's FMCG hub concentration and Pune's pharmaceutical manufacturing cluster.

Three structural forces define this market's 2026-2034 trajectory: India's expanding middle class creating demand for premium packaged goods; government regulations mandating anti-counterfeiting measures in pharma and food; and deep e-commerce penetration requiring smart logistics labels. The market's foundation is robust and diversified across technologies and end-use verticals.

Key Market Insights

|

Insight |

Data |

|

Dominant Technology |

Active Packaging - 42.0% share (2025) |

|

Second Largest Technology |

Intelligent Packaging - 33.0% share (2025) |

|

Dominant Industry Vertical |

Food and Beverages - 39.0% share (2025) |

|

Leading Region |

West India - 31.0% share (2025) |

|

Top Companies |

Avery Dennison Corporation, CCL Industries Inc., Zebra Technologies Corporation, and SML Group |

|

Market Opportunity |

Pharma track-and-trace mandates; cold chain smart sensors; D2C brand QR marketing; e-commerce anti-theft packaging |

Key Analytical Observations Supporting The Data Above:

- Active Packaging at 42.0% (2025): Leads due to strong demand for moisture control, antimicrobial solutions, and gas scavengers across India's food processing and cold chain sector.

- Intelligent Packaging at 33.0% (2025): Rapid growth driven by India's QR-code requirements, export-market serialization rules mandate and Ministry of Health track-and-trace guidelines requiring RFID serialization on pharmaceutical products.

- Modified Atmosphere Packaging at 25.0% (2025): Growing alongside India's organized fresh produce and meat processing sector, which is expanding at approximately 12-15% annually as per APEDA data.

- Food and Beverages at 39.0% (2025): India's packaged food market, valued at over USD 129.18 Billion in 2025, is a principal end-use driver. FSSAI's progressive labeling mandates are accelerating adoption of smart labels across this vertical.

- West India at 31.0% (2025): Concentration of FMCG and pharmaceutical manufacturing in Maharashtra and Gujarat, combined with Mumbai's port-based import-export logistics, creates the highest smart packaging density.

- Healthcare at 24.0% (2025): India's pharma sector, the world's third-largest by volume, mandates serialization, creating structural intelligent packaging demand.

India Smart Packaging Market Overview

India smart packaging market sits at the intersection of rapid industrialization, digital consumer behavior, and an increasingly stringent regulatory environment. Smart packaging encompasses active solutions that interact with packaged contents-such as moisture absorbers, oxygen scavengers, and antimicrobial coatings-alongside intelligent systems that communicate product status through sensors, QR codes, RFID, and NFC technologies. The ecosystem is shaped by India's food processing industry (Ministry of Food Processing Industries), pharmaceutical manufacturing (Indian Pharmaceutical Alliance), and fast-moving consumer goods sector.

India's e-commerce logistics boom-with platforms like Flipkart and Amazon India processing over 15 million daily shipments, is creating structural demand for smart shipping labels and tamper-evident packaging. Government programs including Make in India and Production Linked Incentive (PLI) schemes for food processing and pharma are encouraging domestic smart packaging manufacturers to scale production capacity.

Market Dynamics

To evaluate market opportunities, Request Sample

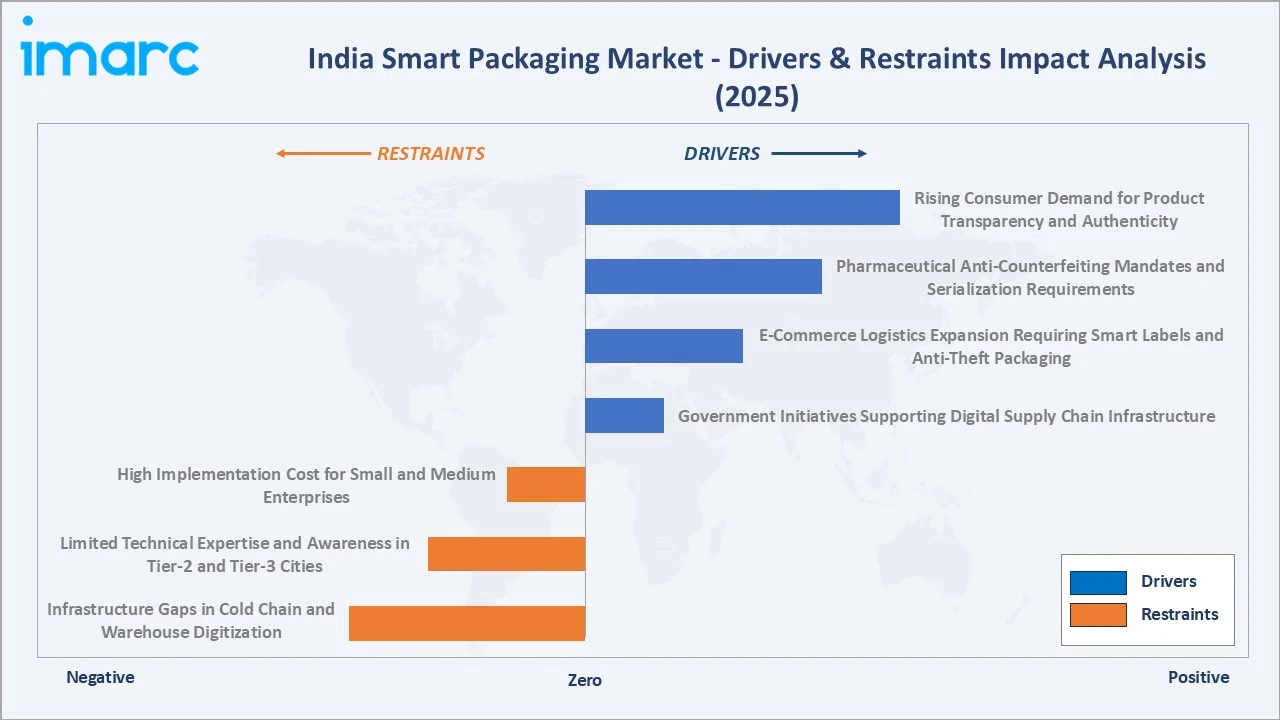

Market Drivers

- Rising Consumer Demand for Product Transparency and Authenticity: Indian consumers increasingly rely on digital verification before purchases. KRBL Limited's 2025 launch of QR-enabled India Gate Basmati Rice packaging-developed with Landor Associates-exemplifies how FMCG brands are embedding smart packaging to deliver product sourcing, nutrition, and authenticity data directly to consumers' smartphones. This trend is scaling across premium categories, including edible oils, snacks, and dairy.

- Pharmaceutical Anti-Counterfeiting Mandates and Serialization Requirements: India's Ministry of Health and Family Welfare mandates serialization on pharmaceutical exports under the Drugs and Cosmetics Act. This creates a regulatory pull for RFID tags, tamper-evident seals, and blockchain-based track-and-trace systems. India's pharmaceutical export market, valued at approximately USD 27.9 Billion in FY2024 (as per Pharmexcil data), requires smart packaging compliance for key regulated markets including the US, EU, and Japan.

- E-Commerce Logistics Expansion Requiring Smart Labels and Anti-Theft Packaging: India's e-commerce sector, growing at approximately 25-30% annually, generates massive demand for barcoded, RFID-enabled, and tamper-evident shipping packaging. Logistics companies including Blue Dart, Delhivery, and Ekart are investing in smart warehouse management systems requiring compatible intelligent labels on packaging units.

- Government Initiatives Supporting Digital Supply Chain Infrastructure: The Digital India program and National Logistics Policy (2022) are driving investments in cold chain traceability, GPS-enabled cargo monitoring, and IoT-connected warehousing. These systemic upgrades create enabling infrastructure for smart packaging technologies, particularly in temperature-sensitive pharmaceutical and agricultural supply chains.

Market Restraints

- High Implementation Cost for Small and Medium Enterprises: RFID tags, NFC-enabled packaging, and IoT sensor integration carry per-unit costs significantly above conventional packaging. India's MSME packaging sector-which represents over 60% of packaging industry participants-finds these costs prohibitive, limiting smart packaging adoption to larger organized players.

- Limited Technical Expertise and Awareness in Tier-2 and Tier-3 Cities: Implementation of intelligent packaging requires knowledge of NFC programming, RFID middleware, and blockchain APIs. The concentration of this expertise in metro cities creates an adoption gap in Tier-2 and Tier-3 manufacturing clusters, despite their growing production volumes.

- Infrastructure Gaps in Cold Chain and Warehouse Digitization: Effective smart packaging for temperature-sensitive goods requires integrated cold chain monitoring infrastructure. India's cold storage network-covering only approximately 40 million metric tonnes against a requirement of over 60 million metric tonnes (National Centre for Cold-Chain Development)-limits smart packaging effectiveness in perishable supply chains.

Market Opportunities

- Pharmaceutical Track-and-Trace Mandate Expansion: India's Central Drugs Standard Control Organisation (CDSCO) is progressively extending serialization requirements beyond pharmaceutical exports to domestic medicines. This regulatory expansion represents a multi-hundred-crore market opportunity for intelligent packaging providers-RFID integrators, barcode solution firms, and serialization software companies.

- Food Safety and Standards Authority of India (FSSAI) Digital Labeling Regulations: FSSAI's evolving framework for digital food labels, including QR code-based nutritional disclosures and allergen information, creates mandatory smart packaging adoption across India's 1.72 lakh micro-food processing enterprises registered with the authority.

- Agri-Export Smart Packaging for Premium Produce: India's agricultural export sector-targeting USD 100 Billion by 2030 as per APEDA's export strategy-is investing in MAP solutions and intelligent freshness indicators to meet importing country standards for mango, grapes, and basmati rice exports.

Market Challenges

- Data Privacy and Cybersecurity Risks in Connected Packaging: Smart packaging involving NFC, RFID, and IoT connectivity creates consumer data collection touchpoints. India's Digital Personal Data Protection Act (2023) mandates data minimization and consent management, requiring smart packaging technology providers to implement compliant data architectures-adding design complexity and compliance costs.

- Consumer Skepticism and Low Smart Packaging Literacy in Rural Markets: A substantial portion of India's consumer base in semi-urban and rural regions lacks smartphone access or digital literacy required to leverage QR code or NFC-enabled packaging features. This limits the effective commercial return on smart packaging investments for brands targeting mass market, price-sensitive consumer segments.

Emerging Market Trends

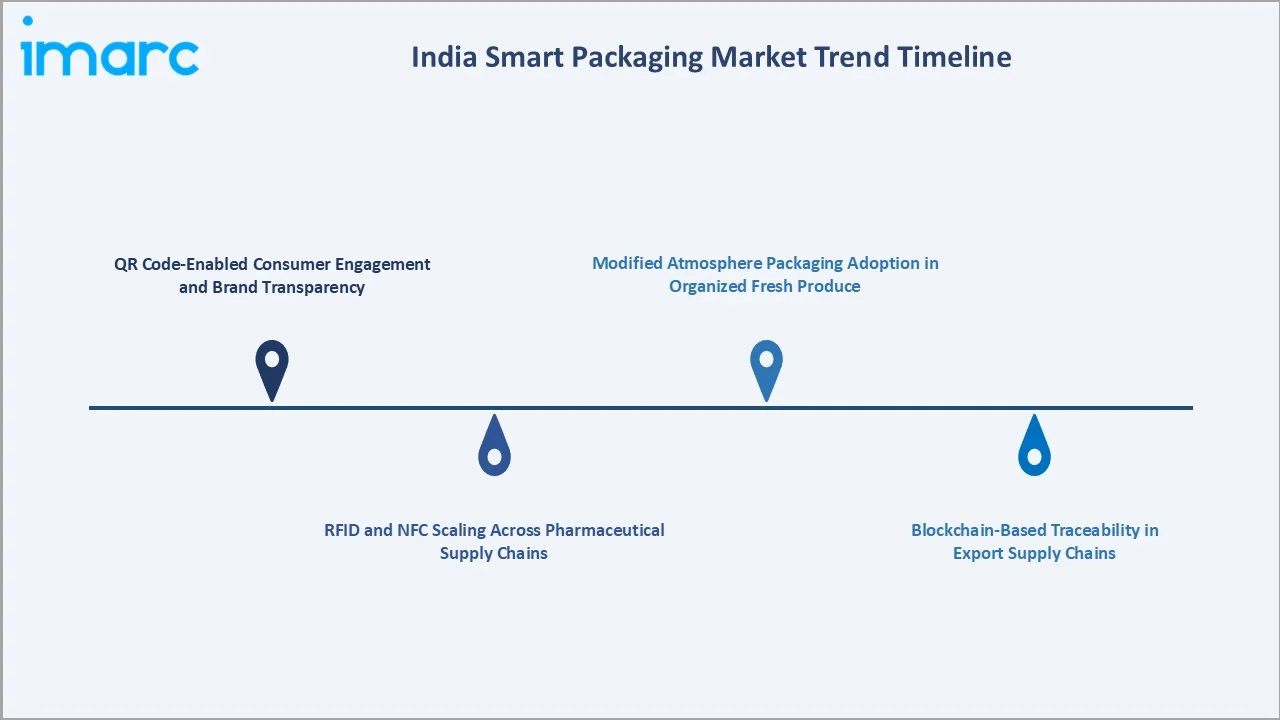

1. QR Code-Enabled Consumer Engagement and Brand Transparency

QR codes have evolved from logistics tools to direct consumer communication channels. In 2025, KRBL Limited introduced QR-enabled India Gate Basmati Rice packaging allowing consumers to access origin, quality certifications, and nutritional data via smartphones. This engagement layer is becoming standard across premium packaged food, beverage, and personal care categories, transforming packaging from passive container to digital touchpoint.

2. RFID and NFC Scaling Across Pharmaceutical Supply Chains

India's pharmaceutical companies are accelerating RFID deployment to meet global regulatory requirements for exported medicines. Myprotein's 2024 launch of QR verification on Impact Whey Protein packaging in India-enabling consumers to verify batch codes, country of origin, and expiry dates-illustrates how nutraceutical and pharmaceutical companies are using smart packaging to address counterfeiting. RFID scaling will intensify as CDSCO expands domestic serialization mandates.

3. Modified Atmosphere Packaging Adoption in Organized Fresh Produce

India's organized retail and modern trade expansion is driving MAP adoption for fresh produce, processed meats, and ready-to-eat food categories. Retailers including Reliance Fresh, DMart, and Spencer's are requiring MAP-certified products from suppliers to extend display shelf life and reduce shrinkage losses. The Council of Scientific and Industrial Research (CSIR)'s 2024 National Mission for sustainable packaging solutions is also accelerating development of bio-based MAP materials.

4. Blockchain-Based Traceability in Export Supply Chains

India's agri-export sector is adopting blockchain-based packaging traceability for premium commodities. The Agricultural and Processed Food Products Export Development Authority (APEDA) has piloted blockchain traceability for basmati rice exports to European markets, embedding smart labels that record farm-to-port provenance data. This trend is expanding to spices, organic produce, and frozen seafood export supply chains.

5. IoT-Enabled Cold Chain Monitoring Packaging

Temperature-sensitive pharmaceutical and food products are driving demand for IoT-enabled time-temperature indicator (TTI) packaging. These solutions use embedded sensors to log cold chain integrity data throughout distribution. India's vaccine distribution network-operated through the government's Electronic Vaccine Intelligence Network (eVIN)-has begun integrating smart temperature logging that is catalyzing TTI adoption in commercial pharmaceutical cold chain logistics.

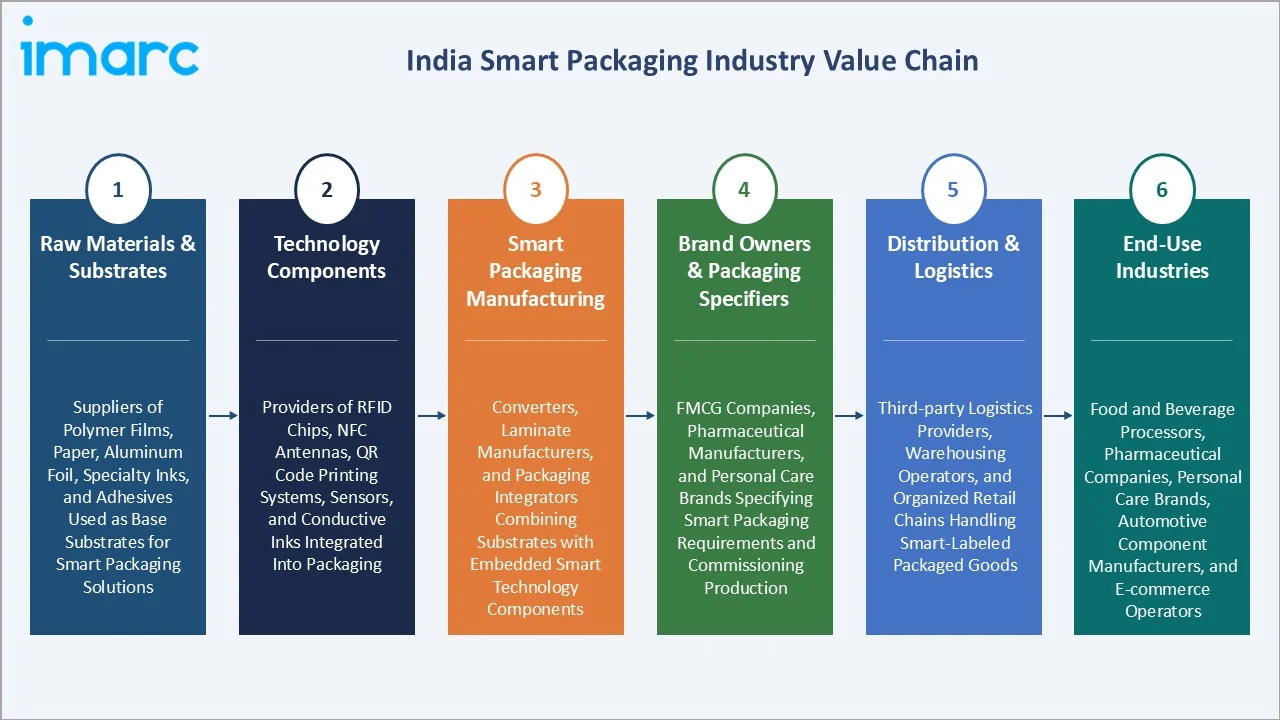

Industry Value Chain Analysis

India smart packaging value chain integrates domestic material suppliers, imported technology components, manufacturing and integration units, distribution networks, and diverse end-use industries. The value chain is evolving rapidly as domestic electronics manufacturing-under the PLI scheme-begins to include RFID chip production, reducing India's dependence on imported smart packaging components.

|

Stage |

Key Participants |

|

Raw Materials & Substrates |

Suppliers of polymer films, paper, aluminum foil, specialty inks, and adhesives used as base substrates for smart packaging solutions |

|

Technology Components |

Providers of RFID chips, NFC antennas, QR code printing systems, sensors, and conductive inks integrated into packaging |

|

Smart Packaging Manufacturing |

Converters, laminate manufacturers, and packaging integrators combining substrates with embedded smart technology components |

|

Brand Owners & Packaging Specifiers |

FMCG companies, pharmaceutical manufacturers, and personal care brands specifying smart packaging requirements and commissioning production |

|

Distribution & Logistics |

Third-party logistics providers, warehousing operators, and organized retail chains handling smart-labeled packaged goods |

|

End-Use Industries |

Food and beverage processors, pharmaceutical companies, personal care brands, automotive component manufacturers, and e-commerce operators |

Technology component import represents India's smart packaging value chain's most commercially significant input stage. The domestic RFID chip manufacturing ecosystem remains nascent, with the majority of high-frequency and ultra-high-frequency RFID chips sourced from suppliers in China, Taiwan, and Germany. This import dependency creates margin pressure for Indian smart packaging converters.

Technology Landscape in the India Smart Packaging Industry

Active Packaging Technologies

Active packaging encompasses oxygen scavengers, moisture control sachets, antimicrobial films, and ethylene absorbers. India's food processing sector is the primary adopter of oxygen scavenging and MAP systems for bakery, dairy, meat, and ready-to-eat products. Antimicrobial packaging using silver nanoparticles and essential oil coatings is an emerging area receiving research investment from CSIR institutes.

Intelligent Packaging Technologies

Intelligent packaging includes RFID, NFC, QR codes, time-temperature indicators (TTIs), and freshness indicators. QR codes represent the lowest-cost intelligent packaging entry point and have achieved mass adoption across Indian FMCG. RFID deployment is concentrated in pharmaceutical serialization and organized retail apparel supply chains. NFC tags are emerging in premium beverages, luxury personal care, and electronics retail for authentication.

Modified Atmosphere Packaging Technology

MAP uses precise gas mixtures-typically nitrogen, carbon dioxide, and oxygen-to extend shelf life of fresh produce, processed meats, and ready-to-eat foods. India's modern retail expansion and restaurant supply chain growth are primary MAP demand drivers. Gas flush packaging systems and high-barrier multilayer films are the core technology inputs, with domestic film suppliers such as Uflex and Cosmo Films supplying significant portions of the value chain.

Digital Connectivity and IoT Integration

IoT-enabled smart packaging integrates Bluetooth Low Energy (BLE) sensors, time-temperature loggers, and cloud-connected data platforms for cold chain and pharmaceutical logistics. India's National Cold Chain Development Policy and eVIN program are catalyzing TTI adoption. Startups including StaTwig (blockchain food traceability) and LogiNext are building platforms interfacing with smart packaging data streams.

Market Segmentation Analysis

The report covers the following market segments with data for 2025:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Active Packaging |

42.0% |

2025 |

|

Industry Vertical |

Food and Beverages |

39.0% |

2025 |

|

Region |

West India |

31.0% |

2025 |

By Technology

Active Packaging commands 42.0% of the market in 2025, reflecting its essential role in India's food and pharmaceutical sectors. The sub-segment includes antimicrobial films used for meat and dairy packaging, gas scavengers critical for modified atmosphere applications, moisture control sachets for biscuits and snacks, and corrosion control solutions for automotive and electronics component packaging.

To access detailed market analysis, Request Sample

Intelligent Packaging at 33.0% is the fastest-growing technology segment, driven by regulatory mandates and consumer engagement requirements. Modified Atmosphere Packaging at 25.0% supports India's export-oriented fresh produce sector, where MAP compliance is required by EU and US import standards for mangoes, grapes, and fresh herbs.

By Industry Vertical

Food and Beverages at 39.0% is the largest end-use segment, anchored by India's USD 129.18 Billion packaged food market and FSSAI's progressive digital labeling regulations. Healthcare at 24.0% reflects pharmaceutical serialization requirements under India's Drug and Cosmetics Act, creating structural demand for RFID and barcode-enabled intelligent packaging solutions across generic drug manufacturers.

Personal Care at 16.0% is growing as premium beauty and wellness brands adopt NFC authentication to combat counterfeiting. Automotive at 12.0% uses corrosion control active packaging for component exports. Others-including e-commerce retail, electronics, and agri-exports-represent 9.0% and are growing above the market average rate.

Regional Market Insights

|

Region |

Share (2025) |

Key Characteristics & Growth Drivers |

|

West India |

31.0% |

Largest regional market driven by concentration of FMCG and pharmaceutical manufacturing in Maharashtra and Gujarat. Mumbai's port logistics hub, Pune's pharma cluster, and Ahmedabad's packaging industry base create the highest smart packaging demand density. |

|

North India |

28.0% |

Strong e-commerce and organized retail penetration in Delhi-NCR fueling smart label demand. Haryana's pharmaceutical manufacturing and Punjab's agri-export sector supporting intelligent and MAP adoption. |

|

South India |

25.0% |

Bengaluru's technology and FMCG brand concentration, Hyderabad's pharmaceutical hub (Genome Valley), and Chennai's automotive cluster driving active and intelligent packaging adoption across multiple verticals. |

|

East India |

16.0% |

Emerging market with growing organized retail penetration in Kolkata and Bhubaneswar. Odisha's steel and chemicals sector driving corrosion control packaging. Growing e-commerce logistics footprint accelerating smart label adoption. |

West India's 31.0% regional leadership reflects Maharashtra's dual commercial advantage: the state accounts for approximately 14% of India's pharmaceutical manufacturing output. North India's 28.0% share is anchored by Delhi-NCR's largest-in-India e-commerce fulfillment center concentration, generating significant smart packaging label demand.

South India's 25.0% reflects Hyderabad's pharmaceutical API manufacturing cluster requiring intelligent packaging for API and finished dosage exports. East India's 16.0% is commercially underdeveloped relative to population size but growing at above-market-average rates as Kolkata's FMCG distribution expands and northeast India's agri-export sector matures.

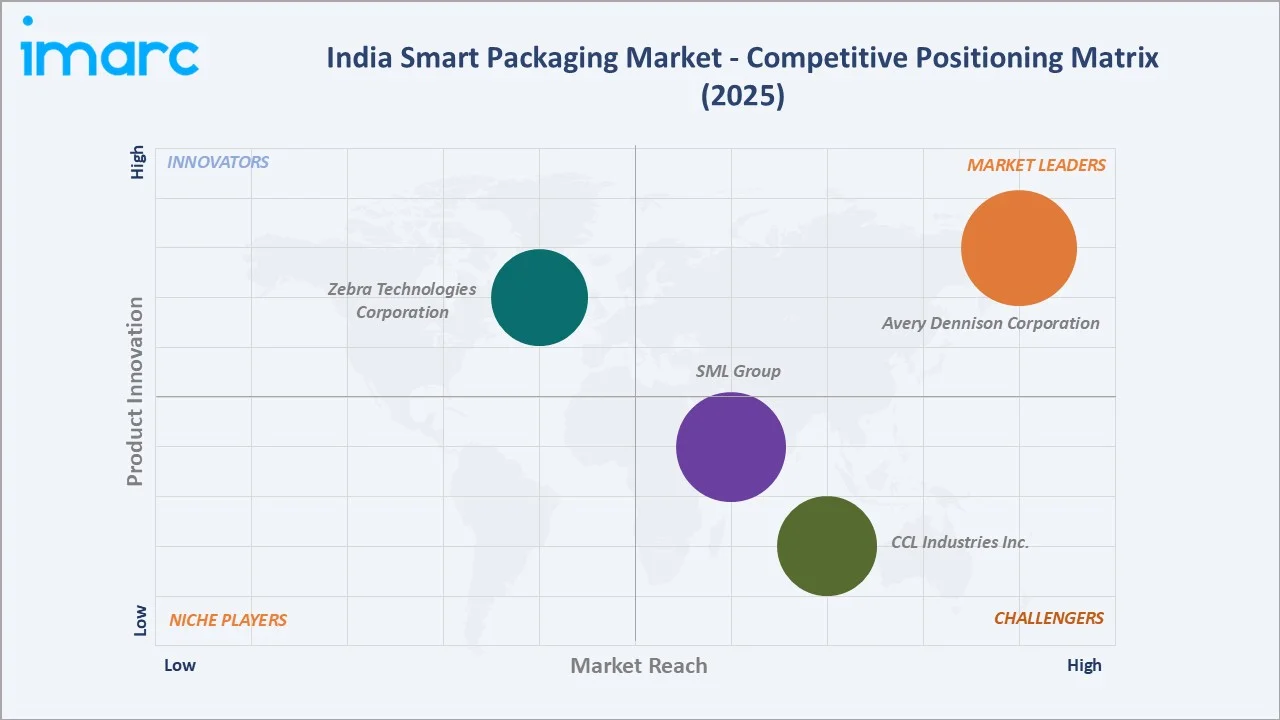

Competitive Landscape

India smart packaging market competitive landscape is moderately consolidated at the technology integration tier, with global players including Avery Dennison and CCL Industries Inc. providing branded smart packaging solutions, while domestic converters compete intensely in active and MAP packaging on price and local customization capability. Competition is intensifying through increasing e-commerce packaging requirements, pharmaceutical serialization mandates, and FMCG brand smart packaging investments.

|

Company |

Key Brands / Divisions |

Market Position |

Core Strength |

|

Avery Dennison Corporation |

Avery Dennison Smartrac, AD Cobra |

Market Leader |

RFID and intelligent label solutions for pharma and retail |

|

CCL Industries Inc. |

CCL Label, CCL Healthcare, CCL Design |

Strong Challenger |

Specialty label and packaging materials with anti-counterfeit features |

|

Zebra Technologies Corporation |

Zebra RFID |

Innovator |

RFID printer and label solutions for supply chain and pharma |

|

SML Group |

Inspire, EcoInspire |

Strong Challenger |

Smart label and RFID tag manufacturing with India operations |

The competitive landscape is being reshaped by India's domestic smart packaging manufacturing capability. Domestic companies including Uflex Limited, Huhtamaki India, and EPL Limited are building intelligent packaging capabilities through technology partnerships and in-house R&D investments, creating a more competitive market structure at the mid-market tier.

Key Company Profiles

Avery Dennison Corporation

Avery Dennison Corporation is a leader in labeling and intelligent packaging solutions, with a significant presence in India through its RBIS (Retail Branding and Information Solutions) and Label and Graphic Materials divisions. The company provides RFID, NFC, and QR-based labeling solutions to India's pharmaceutical, apparel, and FMCG sectors.

- Key Brands / Divisions: Avery Dennison Smartrac, AD Cobra, and others

- Recent Developments: In April 2025, Avery Dennison opened its first RFID (Radio Frequency Identification) inlay and label manufacturing facility in Pune, India, to reinforce its commitment to smart, sustainable labeling technologies.

- Strategic Focus: Leveraging RFID and digital identity leadership to capture pharmaceutical serialization and organized retail smart label demand in India's growing market.

CCL Industries Inc.

CCL Industries is a specialty packaging company with label and packaging solutions across healthcare, consumer goods, and automotive verticals. Its CCL Healthcare division provides pharmaceutical serialization labels and tamper-evident packaging to India's pharmaceutical export manufacturers.

- Key Brands / Divisions: CCL Label, CCL Healthcare, CCL Design, and others.

- Recent Developments: In December 2025, CCL Industries won an Innovation award in the Smart Packaging category at the 2025 Just Drinks Excellence Awards.

- Strategic Focus: Growing pharmaceutical label market share through compliant serialization solutions aligned with CDSCO and global drug authority mandates.

Market Concentration Analysis

India smart packaging market exhibits a moderately concentrated structure at the technology-integrated intelligent packaging tier, where global players including Avery Dennison and CCL Industries Inc. command significant value-added market positions.

The top companies- Avery Dennison Corporation, CCL Industries Inc., Zebra Technologies Corporation, and SML Group-collectively account for an estimated 35-40% of India's organized smart packaging market value. This concentration is highest in pharmaceutical intelligent packaging (where regulatory compliance requirements favor established credentialed suppliers) and lowest in food active packaging (where multiple domestic converters compete effectively on price and customization).

Market consolidation trends are emerging through technology partnerships: domestic flexible packaging companies are signing technology licensing and distribution agreements with global RFID and NFC solution providers to expand intelligent packaging capability without full acquisition costs. This alliance-based consolidation is reshaping the competitive landscape's mid-tier from fragmented domestic-only players toward hybrid domestic-international partnerships.

Investment & Growth Opportunities

Highest Growth Segments

Intelligent Packaging-growing at an estimated 9-10% CAGR through RFID pharma mandates and NFC consumer engagement adoption-represents India's highest-growth smart packaging investment vector. Pharmaceutical serialization is a regulatory-driven guaranteed demand segment. Food QR code and NFC smart label investment is growing at 15-20% CAGR from a smaller base as FMCG brands accelerate digital packaging strategies.

Emerging Investment Opportunities

- Pharmaceutical RFID Serialization Infrastructure: India's CDSCO serialization mandate expansion creates a multi-year investment opportunity for RFID tag manufacturers, serialization software providers, and compliant packaging convertors serving India's approximately 10,500 registered pharmaceutical manufacturing units.

- Cold Chain IoT Packaging for Agricultural Exports: India's USD 100-plus Billion agricultural export target by 2030 (APEDA strategy) requires IoT time-temperature indicator packaging for high-value fresh produce, flowers, and dairy exports. This segment is at an early adoption stage with significant growth runway.

- Sustainable Smart Packaging Innovation: India's plastic waste management rules (PWM Rules 2022) and the government's emphasis on extended producer responsibility are creating demand for smart packaging solutions using biodegradable substrates, compostable films, and recyclable RFID inlays.

Investment Themes

- Domestic RFID Inlay Manufacturing: India's dependence on imported RFID chips and inlays creates a strategic import substitution investment opportunity aligned with the PLI scheme for electronics. Domestic inlay manufacturing would reduce costs by 20-35% for Indian smart packaging converters, dramatically expanding the addressable market.

- QR Code Platform and Analytics Ecosystem: Digital packaging platforms that aggregate consumer interaction data from QR code scans represent a B2B SaaS investment opportunity. Brands generating QR scan data on packaging require analytics platforms to monetize this consumer engagement data for targeted marketing and supply chain intelligence.

- Agri-Export Smart Packaging Solutions: Premium Indian agricultural exports-basmati rice, alphonso mango, Darjeeling tea-require smart freshness indicator and blockchain provenance packaging to command premium pricing in EU and North American markets. Investment in MAP and TTI solutions tailored for India's premium agri-exports is a commercially underdeveloped opportunity.

Future Market Outlook (2026-2034)

India smart packaging market is projected to grow from USD 4.35 Billion in 2025 to USD 8.83 Billion by 2034, delivering a 7.92% CAGR over the forecast period. The market's anchor value of USD 6.38 Billion in 2030 represents a structural inflection point where pharmaceutical serialization is fully mainstreamed, organized retail has scaled MAP adoption, and QR and NFC consumer engagement packaging becomes standard practice across premium FMCG.

Three structural forces define growth through 2034: India's pharmaceutical export compliance requirements creating non-discretionary intelligent packaging investment; India's organized food retail expansion from approximately 15% of total food retail to an estimated 30% by 2034 driving MAP and active packaging adoption; and India's digital consumer base-projected to exceed 1 billion internet users by 2030-creating economically viable QR and NFC consumer engagement packaging at scale across a broad brand universe.

Technological disruptions shaping the 2030-2034 horizon include AI-enabled packaging performance analytics, where smart label data feeds predictive quality models for supply chain waste reduction; bio-based intelligent packaging integrating biodegradable RFID substrates with compostable active components; and augmented reality-enabled packaging where smart labels unlock immersive consumer experiences beyond current QR scan capabilities. India's technology startup ecosystem is an active participant in this next-generation smart packaging innovation, positioning India as both a major smart packaging demand market and an emerging smart packaging technology innovation hub.

Research Methodology

Primary Research

Primary research comprised structured interviews with India smart packaging industry stakeholders, including Packaging Technology Directors, Supply Chain Heads, Pharma Compliance Managers, FMCG Brand Managers, cold chain logistics operators, and retail category managers from organized retail chains. Consumer survey data from packaged goods buyers across West, North, South, and East India was incorporated to validate demand-side insights on smart packaging feature recognition and engagement.

Secondary Research

Secondary research encompassed government regulatory publications (CDSCO Schedule M notifications, FSSAI labeling directives, Ministry of Food Processing Industries annual reports, APEDA export data), industry association reports (Indian Flexible Packaging and Folding Carton Manufacturers Association, Confederation of Indian Industry Packaging Committee), company annual reports, investor presentations, and packaging technology trade publications.

Forecasting Models

Market revenue forecasts were developed using a bottom-up segment aggregation model: active packaging, intelligent packaging, and MAP sub-market forecasts were built independently using end-use industry growth rates, regulatory adoption timelines, and technology cost curve projections. A top-down validation using India's overall packaging market size (Ministry of Commerce data) and smart packaging penetration benchmarking against comparable Asian markets was applied to validate aggregate estimates.

India Smart Packaging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered |

|

| Industry Verticals Covered | Food and Beverages, Automotive, Healthcare, Personal Care, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Avery Dennison Corporation, CCL Industries Inc., Zebra Technologies Corporation, SML Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India smart packaging market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India smart packaging market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India smart packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Smart Packaging Market Report

The India smart packaging market reached USD 4.35 Billion in 2025, driven by rising pharmaceutical serialization mandates, FMCG digital labeling adoption, and e-commerce logistics growth requiring smart packaging labels across supply chains.

The India smart packaging market grows at a CAGR of 7.92% during 2026-2034, reaching USD 8.83 Billion by 2034. Growth is sustained by pharmaceutical compliance requirements, FSSAI digital labeling directives, and expanding organized food retail adoption of active packaging solutions.

Active Packaging leads at 42.0% in 2025 through critical demand from India's food processing sector for moisture control, antimicrobial films, and oxygen scavengers that extend shelf life of perishable products across modern trade supply chains.

Food and Beverages dominates at 39.0% in 2025, driven by FSSAI labeling compliance requirements and the organized food retail sector's adoption of active and MAP packaging. India's USD 129.18 Billion packaged food market is the primary end-use anchor.

West India leads at 31.0% in 2025 through Maharashtra's pharmaceutical and FMCG manufacturing concentration, Mumbai's port logistics hub, and Pune's active pharmaceutical ingredient production cluster requiring smart packaging compliance.

Leading companies include Avery Dennison Corporation, CCL Industries Inc., Zebra Technologies Corporation, and SML Group, among others.

India smart packaging market is projected to reach approximately USD 6.38 Billion by 2030. Pharmaceutical serialization mainstreaming, organized retail MAP adoption, and QR-enabled consumer packaging across FMCG will anchor this growth.

Intelligent Packaging holds a 33.0% share of India's smart packaging market in 2025, valued at approximately USD 1.44 Billion. RFID pharma serialization and QR consumer engagement are the primary growth catalysts through 2034.

CDSCO's pharmaceutical serialization requirements, FSSAI's digital labeling framework, the National Logistics Policy (2022), and Plastic Waste Management Rules (2022) are the primary regulatory drivers accelerating smart packaging adoption across India's packaging ecosystem.

Top opportunities include pharmaceutical RFID serialization infrastructure for CDSCO mandate compliance, domestic RFID inlay manufacturing under the PLI electronics scheme, cold chain IoT packaging for agri-exports, and QR/NFC consumer engagement platform development for India's growing premium FMCG sector.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)