India Soft Drinks Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

India Soft Drinks Market Summary:

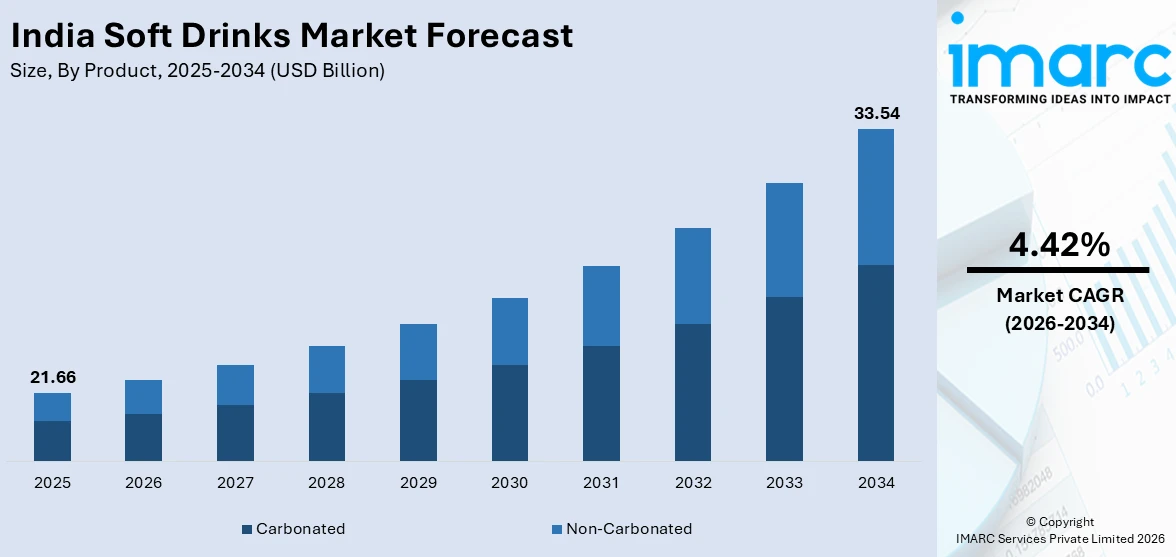

The India soft drinks market size was valued at USD 21.66 Billion in 2025 and is projected to reach USD 33.54 Billion by 2034, growing at a compound annual growth rate of 4.42% from 2026-2034.

The India soft drinks market encompasses a diverse range of carbonated and non-carbonated beverages, catering to an expansive and demographically young consumer base. Growing consumer preferences for convenience, taste innovation, and the introduction of health-conscious variants continue to reshape the market landscape. Expanding retail infrastructure, rising urban incomes, and seasonal demand peaks further accelerate the market share across geographies.

Key Takeaways and Insights:

- By Product: Carbonated dominates the market with a share of 52.3% in 2025, owing to entrenched consumer preferences for fizzy beverages, robust brand loyalty cultivated by established players, and continuous innovation in low-calorie and zero-sugar formats that sustain broad consumer appeal.

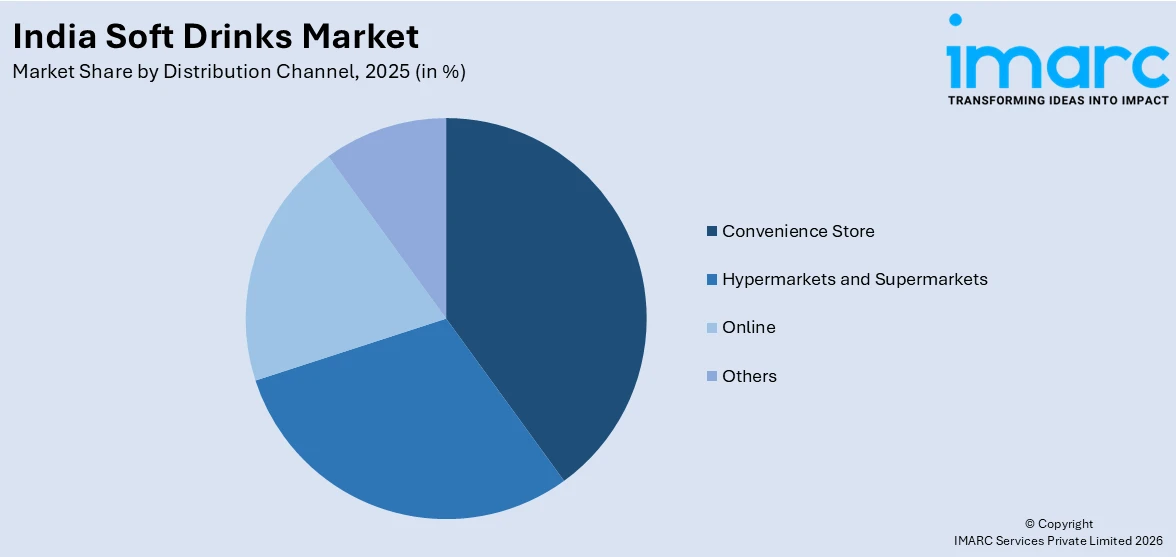

- By Distribution Channel: Convenience store leads the market with a share of 38.4% in 2025. This dominance reflects growing urbanization trends, extended operating hours, and the convenience-driven purchasing behavior of busy consumers across Tier 1 and Tier 2 cities.

- By Region: West and Central India comprises the largest region with a market share of 32.5% in 2025, driven by Maharashtra and Gujarat's concentrated urban populations, high consumer spending capacity, and the dense retail network facilitating widespread product accessibility.

- Key Players: Leading market participants intensify competition through strategic pricing, portfolio diversification, sustainable packaging initiatives, and distribution network expansion across Tier 2 and Tier 3 cities, collectively advancing market penetration and brand visibility throughout India.

To get more information on this market Request Sample

The India soft drinks market is underpinned by robust structural growth drivers that reflect the country's broader economic transformation and evolving consumer preferences. Rapid urbanization, a youthful demographic profile, and rising disposable incomes have combined to fuel steady demand for packaged beverages across urban and semi-urban areas. The market growth is supported by the proliferation of modern retail formats, including convenience stores and hypermarkets, which significantly improve product accessibility and visibility. Growing awareness around health and wellness has encouraged manufacturers to innovate with low-sugar, functional, and natural ingredient-based options, broadening the market's appeal beyond traditional demographics. As per IMARC Group, the India health and wellness market size was valued at USD 164.35 Billion in 2025. Cultural and seasonal influences, particularly the tropical climate and festive consumption patterns, further amplify demand, reinforcing soft drinks as a mainstream beverage category deeply embedded in India's consumer culture and daily routines.

India Soft Drinks Market Trends:

Growing Demand for Health-Oriented and Low-Sugar Variants

The India soft drinks market is undergoing a notable transformation, as health-conscious consumers increasingly seek beverages with reduced sugar content, natural ingredients, and functional benefits. This shift is particularly pronounced among urban millennials and Gen Z consumers who demand products that complement active lifestyles. Products featuring digestive, probiotic, and immunity-boosting claims have gained traction, prompting manufacturers to reformulate offerings. This trend is also accelerating innovation in low-calorie, plant-based, and fortified beverage segments across the market.

Rise of Ready-to-Drink (RTD) and Convenience-Format Beverages

The proliferation of RTD beverages continues to gain momentum across India, driven by evolving consumer lifestyles centered around convenience and on-the-go consumption. Urbanization has accelerated the demand for single-serve packaging and grab-and-go formats suited to fast-paced routines. Growing quick-commerce and e-commerce penetration has further amplified this trend, enabling consumers across Tier 2 and Tier 3 cities to access a wider variety of RTD products. As per IBEF, the India e-commerce industry, valued at INR 10,82,875 Crore (USD 125 Billion) in 2024, is set to grow to INR 29,88,735 Crore (USD 345 Billion) by 2030, reflecting a compound annual growth rate (CAGR) of 15%.

Flavor Innovations and Premiumization Trends

In order to differentiate portfolios and draw in discriminating customers, Indian soft drink companies are adopting taste innovation as a key strategy and developing functional, exotic, and region-specific flavors. Drink concentrates, mixed carbonated drinks, and iced tea are the subcategories that are expanding the fastest, due to consumers' growing desire for new beverage experiences. By customizing flavors to suit local tastes, homegrown companies are gaining substantial regional followings. Limited-edition releases and seasonal variations that improve customer engagement and brand recall further bolster this strategy.

Market Outlook 2026-2034:

The India soft drinks market is poised for consistent expansion throughout the forecast period, driven by favorable demographic trends, expanding distribution infrastructure, and sustained product innovation. The market generated a revenue of USD 21.66 Billion in 2025 and is projected to reach a revenue of USD 33.54 Billion by 2034, growing at a compound annual growth rate of 4.42% from 2026-2034. Manufacturers are increasingly investing in developing healthier product variants, leveraging digital and quick-commerce platforms to penetrate underserved geographies, and adopting sustainable packaging practices aligned with evolving regulatory frameworks. Seasonal demand peaks, particularly during India's summer months, continue to provide significant revenue opportunities. The entry of domestic challengers offering aggressive pricing alongside the premiumization strategies of established players are expected to collectively shape a dynamic and competitive market environment, creating sustained value creation opportunities across the forecast horizon.

India Soft Drinks Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Carbonated |

52.3% |

|

Distribution Channel |

Convenience Store |

38.4% |

|

Region |

West and Central India |

32.5% |

Product Insights:

- Carbonated

- Non-Carbonated

Carbonated dominates with a market share of 52.3% of the total India soft drinks market in 2025.

Carbonated maintains a commanding presence across India's soft drinks landscape, anchored by decades of brand loyalty and a vast product portfolio spanning cola-based drinks, lemon-lime sodas, flavored sparkling beverages, and sparkling water. The segment's dominance is reinforced by continuous innovation, with manufacturers introducing low-calorie, zero-sugar, and naturally flavored variants to capture health-conscious consumers without compromising its broad appeal. Strong distribution networks and widespread retail availability further reinforce the segment’s sustained market leadership across urban and rural regions.

The carbonated segment benefits significantly from India's tropical climate and youthful consumer base, for whom fizzy beverages serve as a primary refreshment choice during hot seasons and social occasions. Strategic marketing initiatives, including celebrity endorsements, sports sponsorships, and large-scale promotional campaigns by major beverage brands, consistently drive consumer engagement and volume growth. The entry of value-driven domestic players has further expanded the segment's reach into price-sensitive Tier 2 and Tier 3 markets, intensifying competitive dynamics and encouraging differentiated product positioning across packaging formats, flavor profiles, and price points catering to diverse socioeconomic segments across the country.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Hypermarkets and Supermarkets

- Convenience Store

- Online

- Others

Convenience store leads with a share of 38.4% of the total India soft drinks market in 2025.

Convenience store possesses the biggest distribution channel share in the soft drink industry in India, which is indicative of its critical position in urban retail ecosystems and the impulsive buying habits of customers looking for quick, convenient refreshment. These establishments are vital touchpoints for urgent consumption demands because of their long operating hours and their proximity to busy locations. Their significance in promoting high-frequency beverage purchases is further strengthened by their capacity to hold a wide range of stock keeping units (SKUs) and provide instant product awareness.

The quick spread of contemporary convenience formats and neighborhood retail stores throughout Tier 2 and Tier 3 cities, where customers value accessibility and transactional ease, further solidifies the convenience store channel's supremacy. In order to execute successful merchandising methods, such as refrigerated units, prominent product placement, and promotional displays that influence purchase decisions at the point of sale, beverage makers are increasingly collaborating with these outlets. The channel is positioned to be a consistently powerful distribution driver throughout the course of the projected period, due to its connection with the expanding on-the-go consuming culture among India's working population and younger demographics.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India comprises the largest region with a market share of 32.5% of the total India Soft Drinks market in 2025.

West and Central India represents the largest regional market for soft drinks, led by Gujarat and Maharashtra, which together contain some of India's most populous cities, such as Mumbai and Pune. The area enjoys some of the greatest per capita consumer expenditure in the nation as well as a well-established organized retail network. Strong urbanization levels and a high concentration of working professionals further drive consistent demand for ready-to-consume beverages.

The dense concentration of significant beverage manufacturing facilities, which facilitate effective supply chain operations and wide product availability, further supports the region's dominance. Soft drink consumption is increased by higher disposable incomes, a booming tourism and hospitality industry, especially in Goa and Maharashtra, and the expansion of quick-commerce and contemporary retail formats. According to the 66th edition of the ‘India Tourism Data Compendium 2025,’ published by the Ministry of Tourism (MoT), Maharashtra saw 3.71 Million Foreign Tourist Visits (FTVs) in 2024, establishing itself as India's leading destination.

Market Dynamics:

Growth Drivers:

Why is the India Soft Drinks Market Growing?

Rapid Urbanization and Expanding Consumer Base

Urbanization continues to function as one of the most consequential structural forces reshaping demand within the India soft drinks market. As a growing proportion of the population transitions to urban environments, consumption behavior shifts measurably towards packaged and ready-to-consume beverage formats that accommodate faster daily routines and the convenience-oriented retail infrastructure characteristic of city living. The expansion of organized retail, quick-commerce platforms, and neighborhood convenience stores has substantially reduced friction between consumer intent and point of purchase, supporting higher transaction frequency and more consistent brand engagement across urban geographies. Digital and social media channels have further amplified this dynamic, enabling product discovery and brand interaction among younger consumer cohorts at a speed and scale that conventional marketing channels were structurally unable to deliver. India's climatic conditions provide an additional and persistent demand stimulus. Sustained heat across large parts of the country throughout much of the year reinforces soft drinks as an accessible and immediate category response. Collectively, these factors do not merely support incremental market expansion, they reinforce one another in ways that compound the market's growth trajectory over the medium and long term.

Rising Disposable Incomes and Growing Middle-Class Demand

India's expanding middle class and rising disposable incomes represent one of the most powerful structural drivers of growth within the soft drinks market. As household incomes increase across urban and semi-urban demographics, consumers demonstrate a greater willingness to spend on branded packaged beverages, premium product variants, and innovative flavors that were previously considered discretionary indulgences. This income-driven premiumization effect is creating dual growth pathways: a mass market anchored by value-priced beverages and a premium tier catering to affluent health-conscious consumers. India's GDP growth was projected at 6.5% for FY2024-25, reflecting the macroeconomic tailwinds supporting consumer spending across FMCG categories, including soft drinks. The penetration of soft drinks into rural and semi-urban markets is accelerating, driven by expanding organized retail infrastructure and improved cold chain logistics that sustain product quality and availability beyond metro cities.

Innovations in Product Portfolio and Health-Conscious Variants

The India soft drinks market is experiencing a wave of product innovation, as manufacturers respond to evolving consumer health consciousness and demand for differentiated beverage experiences. Brands are investing in the development of low-calorie, zero-sugar, functional, and naturally flavored variants that bridge the gap between refreshment and wellness. This innovation is further supported by the incorporation of fortified ingredients, such as vitamins, minerals, botanicals, and plant-based extracts that cater to specific health benefits, including immunity, hydration, and digestive wellness. Companies are also experimenting with unique flavor combinations inspired by regional tastes and global trends, enhancing product appeal across diverse consumer segments. Additionally, advancements in packaging formats, such as single-serve, on-the-go bottles and sustainable materials, are improving convenience while aligning with environmental concerns. Strategic collaborations, limited-edition launches, and premiumization efforts are further enabling brands to capture evolving consumer preferences and drive category growth.

Market Restraints:

What Challenges the India Soft Drinks Market is Facing?

High Taxation on Aerated and Carbonated Soft Drinks

Aerated beverages in India are subject to a high tax burden under the GST framework, including an additional compensation cess applicable to sin goods. This elevated taxation significantly increases retail prices, reducing affordability, particularly among price-sensitive consumers in rural and semi-urban markets. In September 2024, the Indian Beverage Association advocated for GST rationalization, highlighting that lower tax rates could stimulate sector investments, improve pricing accessibility, and support broader market expansion.

Fluctuating Raw Material Prices

The soft drinks industry's dependence on raw materials, such as sugar, carbon dioxide, natural flavorings, and packaging materials, exposes manufacturers to significant cost volatility. Fluctuations in sugar prices have historically impacted production cost structures, compressing profit margins and forcing manufacturers to either absorb costs or pass them on to consumers through retail price increases. This pricing instability particularly affects small and mid-sized beverage producers with limited procurement scale.

Supply Chain and Distribution Inefficiencies

India’s fragmented retail landscape and infrastructural gaps, particularly in rural and remote regions, create logistical challenges for beverage distribution. Maintaining cold chain integrity, managing inventory across diverse outlets, and ensuring timely product availability can increase operational costs. These inefficiencies may limit market penetration and affect product quality, especially for smaller manufacturers lacking robust distribution networks.

Competitive Landscape:

The India soft drinks market features a highly competitive landscape, characterized by the coexistence of established multinational corporations, homegrown FMCG majors, and a growing cohort of regional and challenger brands. Leading international players maintain competitive advantages through substantial marketing budgets, celebrity endorsements, sports sponsorships, and decades of brand equity that ensure consistent consumer recognition and category leadership. Domestic challengers are intensifying competition through aggressive pricing, value-oriented positioning, and culturally resonant branding strategies that align with India's national sentiment and regional taste preferences. The competitive landscape is also witnessing increased participation from health-focused entrants introducing functional and better-for-you beverage formats targeting urban wellness-oriented consumers. Key competitive dimensions include pricing strategy, distribution network depth, product innovation velocity, and sustainability commitments.

Recent Developments:

- In April 2025, Reliance Consumer Products announced plans to establish a new bottling plant for its Campa Cola brand in the Begusarai district of Bihar, with an investment of approximately INR 1,000 Crore. The facility, spanning 35 acres, will integrate both bottling and manufacturing operations and is expected to significantly strengthen Campa Cola's distribution footprint across Eastern and Northeastern India.

- In March 2025, Coca-Cola and PepsiCo simultaneously introduced no-sugar soft drink variants priced at INR 10 across multiple brands, including Thums Up X Force, Coke Zero, Sprite Zero, and Pepsi No-Sugar. This marked the first time both beverage multinationals introduced diet and light beverages at this mass-market price point in India, reflecting the intensifying competitive pressure from value-oriented domestic brands.

India Soft Drinks Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Carbonated, Non- Carbonated |

| Distribution Channels Covered | Hypermarkets and Supermarkets, Convenience Store, Online, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Soft Drinks Market Report

The India soft drinks market size was valued at USD 21.66 Billion in 2025.

The India soft drinks market is expected to grow at a compound annual growth rate of 4.42% from 2026-2034 to reach USD 33.54 Billion by 2034.

Carbonated dominated the market with a share of 52.3%, driven by deep consumer brand loyalty, extensive product variety spanning cola and flavored carbonated beverages, and continuous innovation in low-calorie and zero-sugar formats that sustain broad consumer appeal.

Key factors driving the India soft drinks market include rapid urbanization, rising disposable incomes among the expanding middle class, growing demand for convenience and RTD beverages, continuous product innovation in health-oriented variants, and the proliferation of organized retail infrastructure.

Major challenges include fluctuating raw material costs particularly for sugar and packaging materials, growing health consciousness among urban consumers shifting away from high-sugar soft drinks, and intensifying competition from value-oriented domestic and regional beverage brands.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)