India Solar Energy Market Size, Share, Trends and Forecast by Deployment, Application, and Region, 2026-2034

India Solar Energy Market Size, Share, Trends & Forecast (2026-2034)

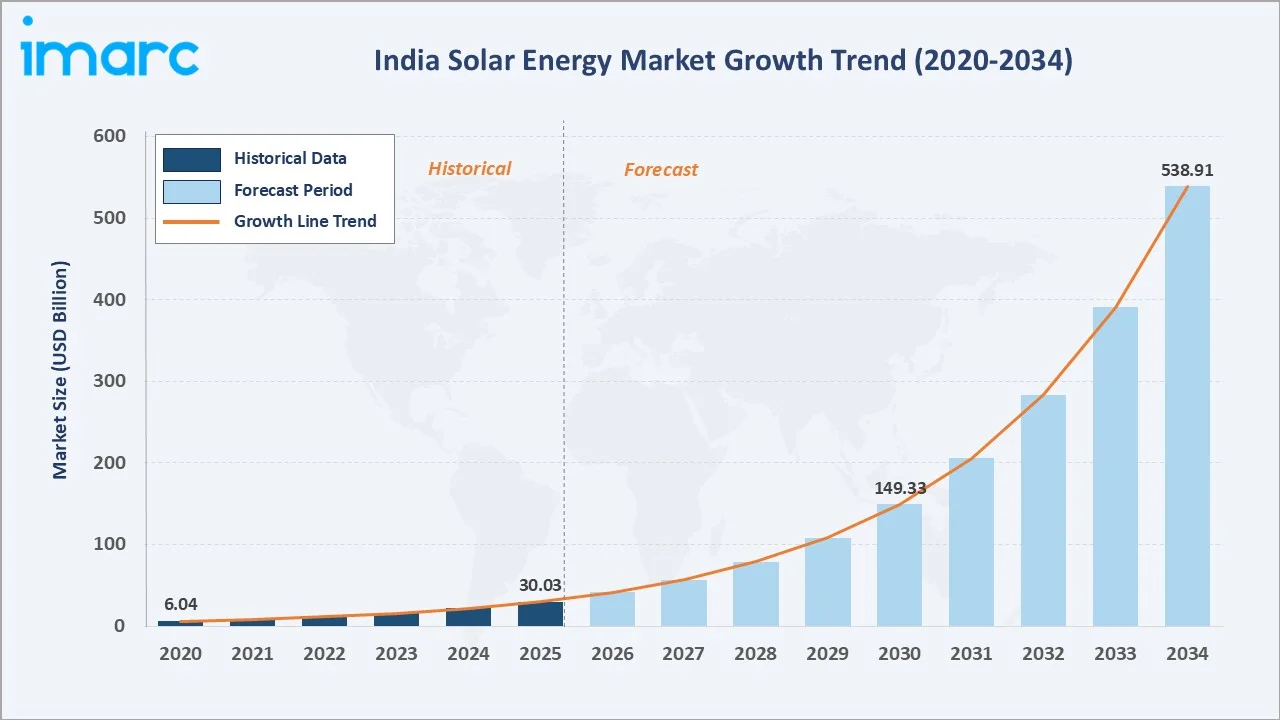

The India solar energy market grew from USD 30.03 Billion in 2025 to USD 41.39 Billion in 2026 and is projected to reach USD 538.91 Billion by 2034, exhibiting a CAGR of 37.82% during 2026-2034. Robust policy support, with India's installed solar capacity surpassing 132.85 GW by November 2025 according to the Ministry of New and Renewable Energy (MNRE), along with the rapid execution of PM Surya Ghar: Muft Bijli Yojana, falling solar module prices, and rising commercial and industrial demand for clean power, are the primary forces shaping the market growth.

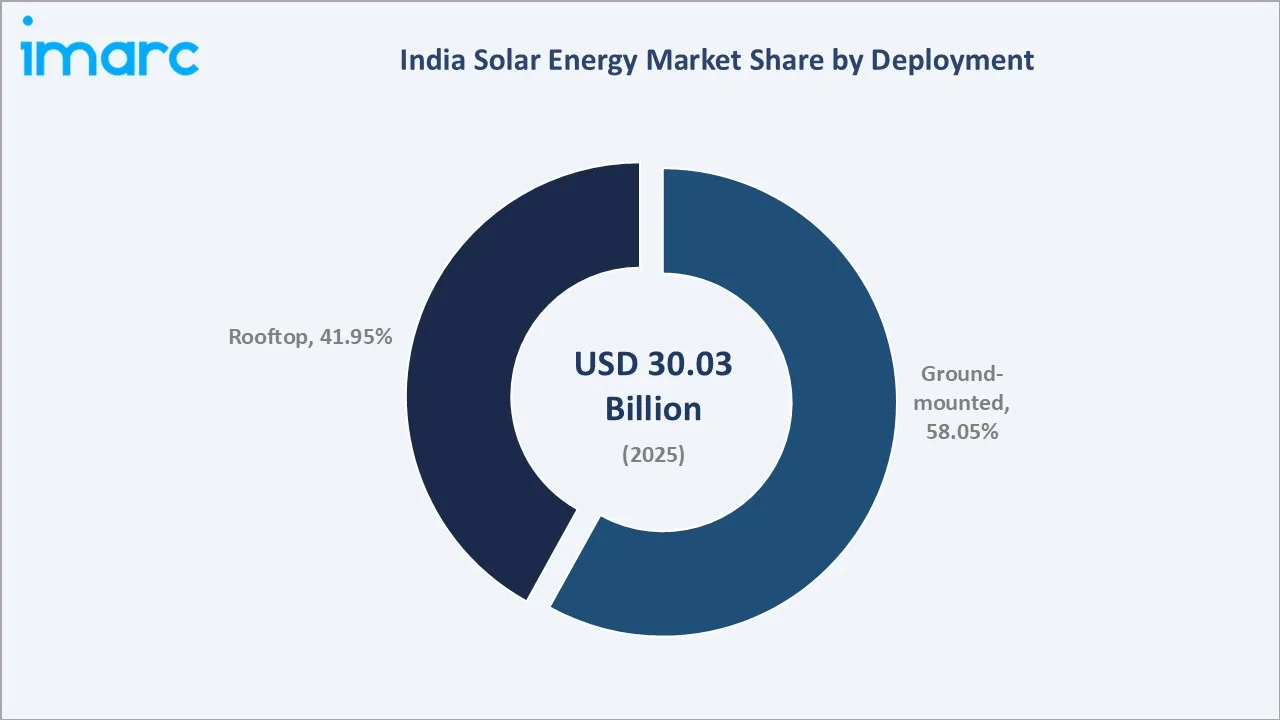

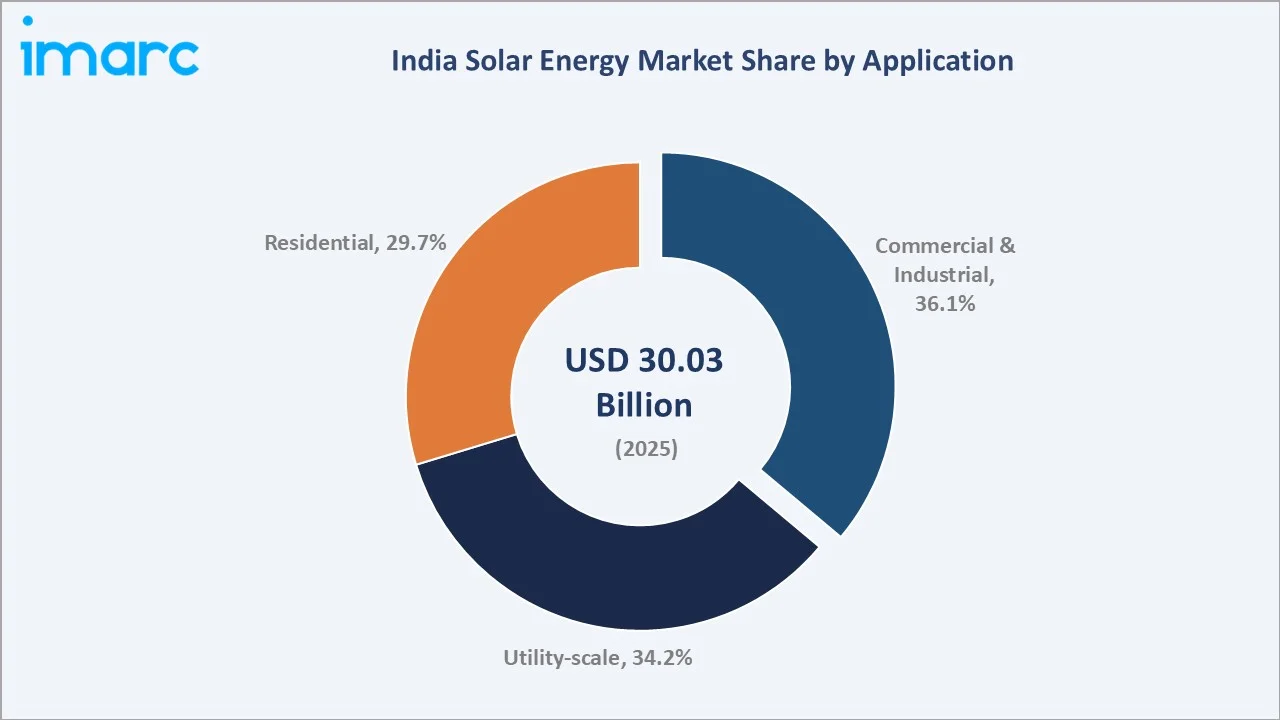

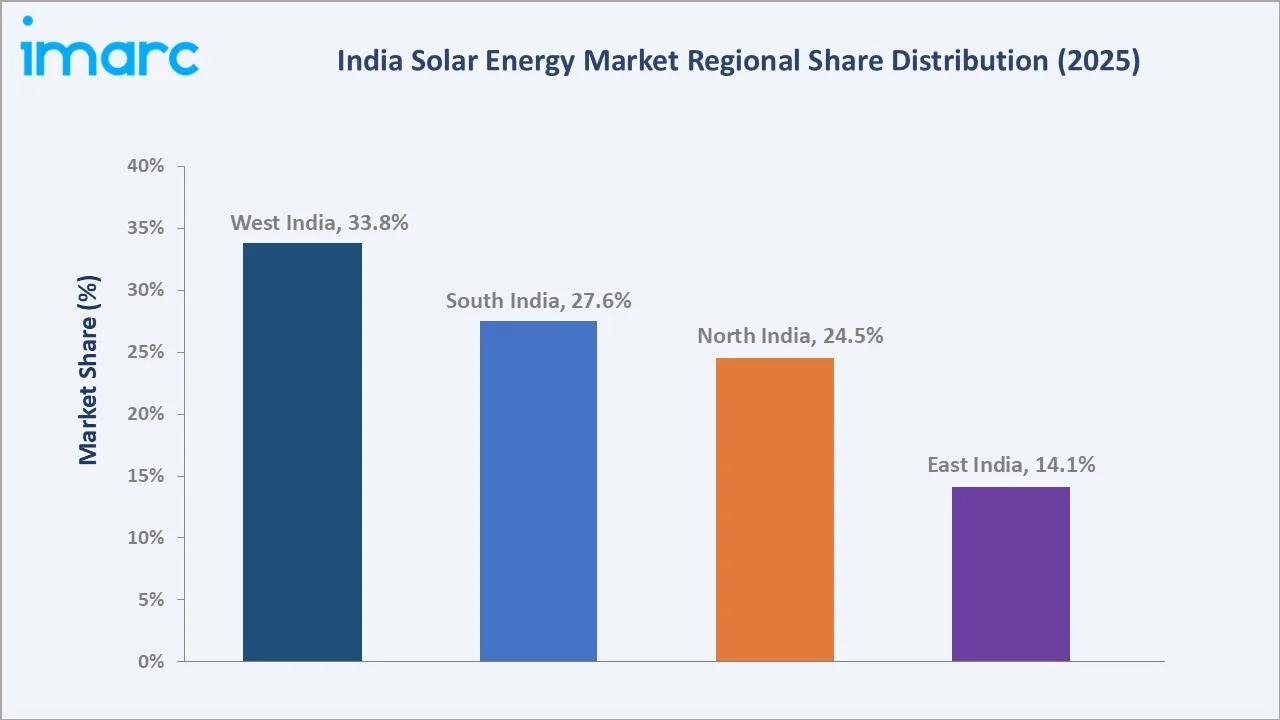

Ground-mounted leads the deployment segment at 58.05%, commercial and industrial dominates the application segment at 36.1%, and West India commands a 33.8% regional share.

Market Snapshot

|

Metric |

Value |

|

Base Year Market Size (2025) |

USD 30.03 Billion |

|

Market Size (2026) |

USD 41.39 Billion |

|

Forecast Market Size (2034) |

USD 538.91 Billion |

|

CAGR (2026-2034) |

37.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

| Largest Region |

West India (33.8%, 2025) |

| Fastest Growing Region |

East India (14.1%, 2025) |

| Leading Deployment |

Ground-mounted (58.05%, 2025) |

| Leading Application | Commercial and Industrial (36.1%, 2025) |

The India solar energy market expanded from USD 6.04 Billion in 2020 to USD 30.03 Billion in 2025 and an estimated USD 41.39 Billion in 2026, supported by aggressive utility-scale auctions, mature rooftop financing options, and falling module costs. Anchored at USD 149.33 Billion in 2030, the forecast to USD 538.91 Billion by 2034 is underpinned by India's commitment to expanding non-fossil fuel capacity, accelerating commercial and industrial open-access adoption, and the maturation of solar-plus-storage projects.

To get more information on this market, Request Sample

CAGR trajectories across regional and application sub-segments show East India and the residential rooftop categories expanding faster than the overall 37.82% market CAGR, propelled by household subsidies, easy financing, expanding installer networks in eastern states, and rising electricity tariffs across most state utilities.

Executive Summary

The India solar energy market is on a strong growth trajectory, expanding from USD 6.04 Billion in 2020 to USD 41.39 Billion in 2026 and reaching USD 538.91 Billion by 2034. Solar power has shifted from a complementary energy source to the centerpiece of India's electricity strategy. Tumbling module prices, supportive central policies, and rising power consumption from data centers, manufacturing, and transport electrification are reshaping the sector. The country's solar capacity anchors its renewable energy expansion plans through 2030 and beyond.

Ground-mounted dominates deployment at 58.05% in 2025, supported by large utility-scale parks in Rajasthan, Gujarat, and Andhra Pradesh. In March 2024, Adani Green Energy Limited (AGEL) activated a total capacity of 1,000 MW of solar energy at the largest RE park worldwide located in Khavda, Gujarat. Commercial and industrial leads the application segment at 36.1%, fueled by open-access reforms and corporate sustainability mandates. West India commands 33.8%, led by Gujarat and Maharashtra, driven by industrial clusters, supportive state policies, and high solar irradiance.

Key Market Insights

|

Insight |

Data |

| Leading Deployment | Ground-mounted - 58.05% share (2025) |

| Second Deployment |

Rooftop - 41.95% share (2025) |

| Leading Application | Commercial and Industrial - 36.1% share (2025) |

| Second Application | Utility-scale - 34.2% share (2025) |

| Leading Region | West India - 33.8% share (2025) |

| Fastest Growing Region | East India - 14.1% share (2025) |

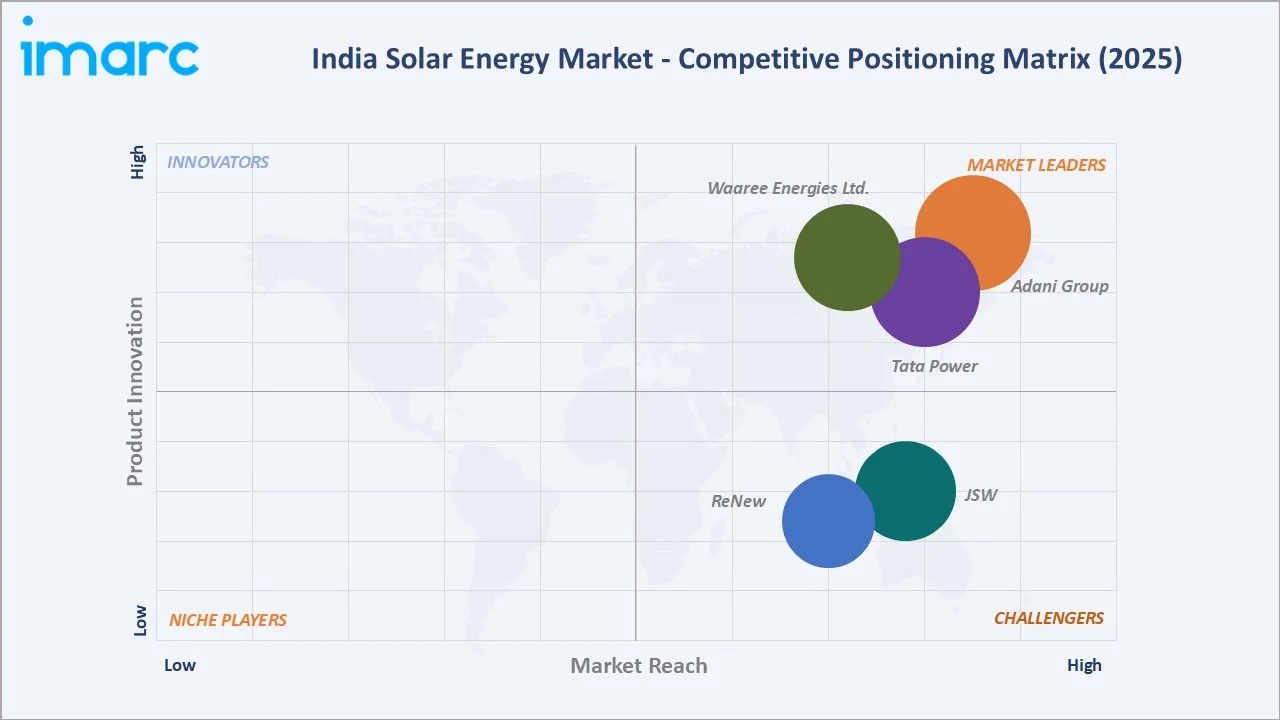

| Top Companies | Adani Group, Tata Power, Waaree Energies Ltd., ReNew, and JSW |

Key Analytical Observations Expanding On The Data Above:

- Ground-mounted dominance at 58.05% is driven by India's large utility-scale solar parks, including the Bhadla Solar Park, Rajasthan, where land availability and economies of scale enable competitive tariffs. State-led auctions and central PSU procurements continue to anchor this segment.

- Rooftop share at 41.95% is sustained by accelerating residential adoption under PM Surya Ghar: Muft Bijli Yojana, supportive net-metering frameworks, and corporate captive consumption. As of February 2026, over 26 lakh households had been solarized under the scheme, marking it as one of the world's largest domestic rooftop solar initiatives.

- Commercial and industrial leadership at 36.1% reflects the rising preference among manufacturing units, IT campuses, and warehouses for open-access solar power, captive plants, and group captive structures. Many corporates are signing long-term Power Purchase Agreements (PPAs) to hedge against rising grid tariffs.

- Utility-scale at 34.2% is anchored by central agencies, alongside state utilities procuring solar power through reverse auctions. Hybrid and Round-the-Clock tenders are reshaping procurement patterns within this category.

- West India at 33.8% dominates owing to Gujarat's Khavda Renewable Energy Park, Maharashtra's industrial corridor demand, and supportive state-level renewable purchase obligations. The region also hosts a significant share of India's solar module manufacturing capacity.

India Solar Energy Market Overview

Solar energy in India encompasses electricity generated from photovoltaic (PV) systems and concentrated solar power (CSP) plants deployed across utility-scale, commercial, industrial, and residential applications. The sector spans cell and module manufacturing, EPC services, operations and maintenance, and balance-of-system equipment.

The Indian ecosystem connects upstream polysilicon and wafer suppliers with domestic cell and module manufacturers, EPC firms, project developers, financiers, transmission utilities, and end users such as discoms, commercial off-takers, and households. Central agencies orchestrate auctions, grid connectivity, and policy frameworks.

Market Dynamics

To evaluate market opportunities, Request Sample

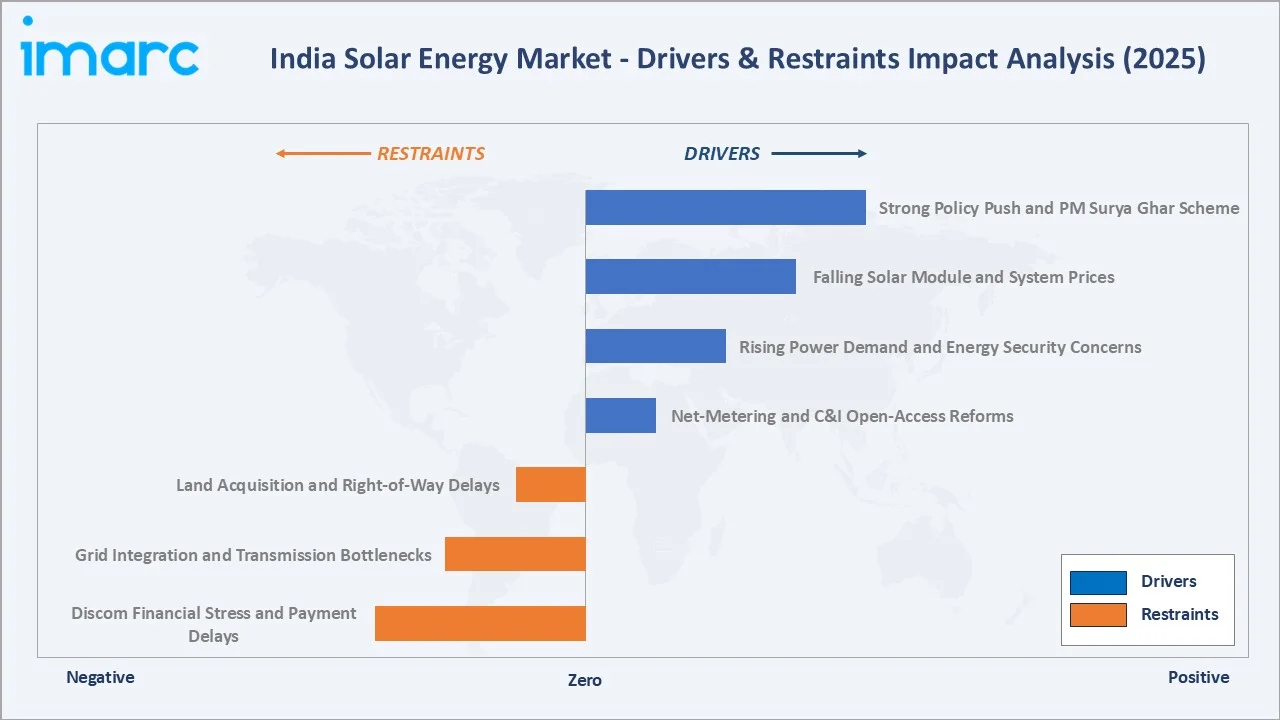

Market Drivers

- Strong Policy Push and PM Surya Ghar Scheme: Central and state-level policies, including PM Surya Ghar: Muft Bijli Yojana and the National Solar Mission, are accelerating solar adoption. The PM Surya Ghar scheme alone targets one crore residential rooftop installations by March 2027, backed by a financial outlay of INR 75,021 Crore, approved in February 2024.

- Falling Solar Module and System Prices: Expanding domestic and global manufacturing scale has pushed module and system costs lower, improving project economics and unlocking new business cases for residential and commercial buyers across the country.

- Rising Power Demand and Energy Security Concerns: India's peak electricity demand continues to grow with industrial expansion, urbanization, and rising air-conditioning load. Solar power, with its short construction timelines, is emerging as the preferred choice for both peak shaving and base capacity additions.

- Net-Metering and Commercial and Industrial Open-Access Reforms: State-level open-access reforms, group captive structures, and predictable net-metering regimes are enabling commercial and industrial consumers to procure solar power directly. Corporate sustainability commitments and rising grid tariffs are reinforcing this trend.

Market Restraints

- Land Acquisition and Right-of-Way Delays: Securing contiguous land parcels for utility-scale solar projects continues to face challenges around titling, local approvals, and forest clearances. Project timelines often stretch beyond original schedules, raising development costs.

- Grid Integration and Transmission Bottlenecks: Rapid renewable capacity additions are placing pressure on inter-state transmission corridors and substation infrastructure. Delays in transmission project execution and right-of-way constraints further risk curtailment and evacuation challenges for new capacity additions.

- Discom Financial Stress and Payment Delays: Several state discoms continue to face working capital pressure, leading to delayed payments to renewable generators. This raises perceived counterparty risk and limits debt financing appetite for new solar projects.

Market Opportunities

- Solar-plus-Storage and Round-the-Clock Tenders: Hybrid auctions combining solar with wind and battery storage are unlocking firm renewable supply contracts, opening a new revenue stream for developers and supporting grid stability.

- Domestic Manufacturing Under Production Linked Incentive (PLI) Scheme: The PLI scheme for high-efficiency solar PV modules is enabling fully integrated domestic manufacturing, reducing import dependence, and creating opportunities for component suppliers across the value chain.

- Green Hydrogen and Industrial Decarbonization: The push toward green hydrogen is creating incremental demand for renewable power, particularly from hard-to-abate sectors, such as refining and steel. Policy support and pilot-scale project deployments are accelerating ecosystem development, opening long-term opportunities for solar developers.

Market Challenges

- Polysilicon and Wafer Supply Volatility: India remains heavily reliant on imported polysilicon, wafers, and ingots. Global pricing swings and trade measures can disrupt domestic module production schedules and project economics.

- Skilled Workforce and O&M Quality Gaps: Rapid project additions are stretching the availability of certified installers, electrical contractors, and qualified O&M technicians. Quality consistency in rooftop installations remains an area of active regulatory focus.

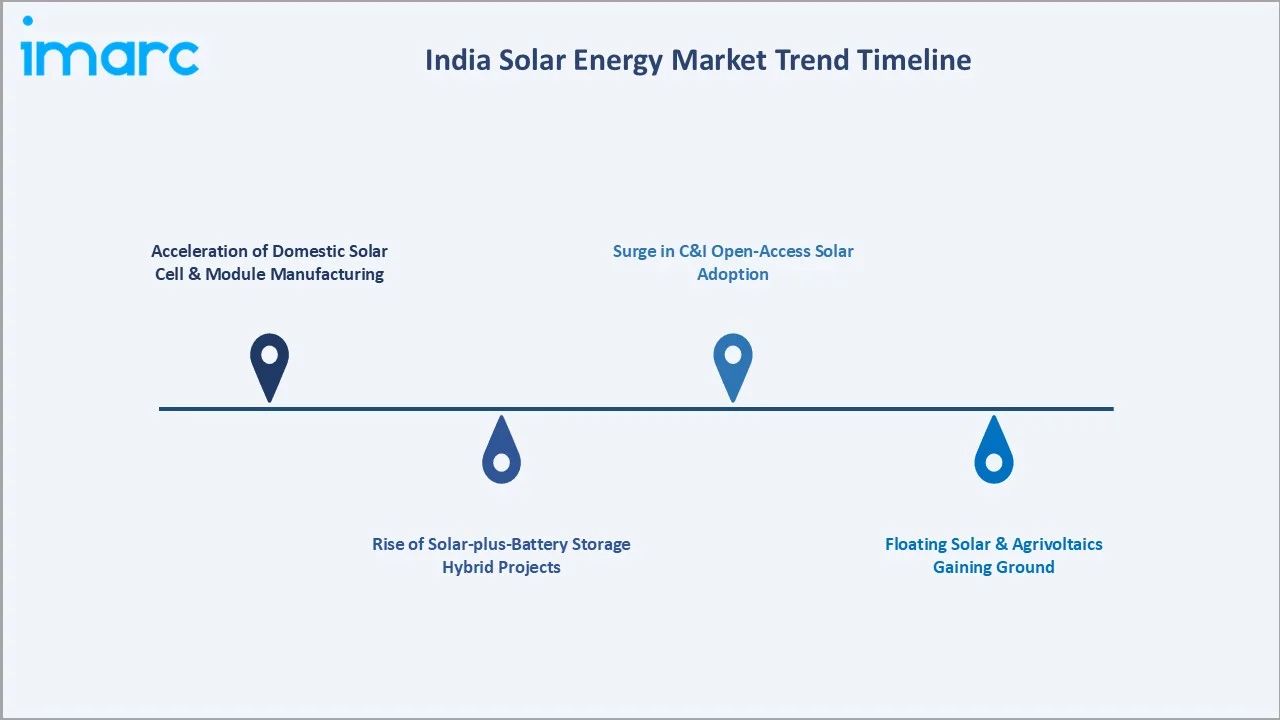

Emerging Market Trends

1. Acceleration of Domestic Solar Cell and Module Manufacturing

Indian module manufacturers are expanding capacity rapidly under the PLI scheme to meet domestic auction requirements and reduce import dependence. According to MNRE, India added around 81 GW of solar module manufacturing capacity under ALMM List-I in calendar year 2025, nearly doubling the additions recorded in 2024 and taking the country's total ALMM-listed module production capacity to around 144 GW.

2. Rise of Solar-plus-Battery Storage Hybrid Projects

Solar-plus-battery hybrid auctions are emerging as a structural shift, offering firm or dispatchable renewable supply that addresses evening peak demand. Central agencies are auctioning Round-the-Clock and Firm and Dispatchable Renewable Energy projects, reshaping how developers structure project economics.

3. Surge in Commercial and Industrial Open-Access Solar Adoption

Commercial and industrial consumers are increasingly procuring solar power through open access, group captive, and third-party PPA structures. Several IT parks, manufacturing clusters, and data center campuses have signed long-term solar contracts to lock in tariffs and meet sustainability targets.

4. Floating Solar and Agrivoltaics Gaining Ground

Floating solar projects on reservoirs and water bodies, along with agrivoltaic pilots that combine solar generation with crop cultivation, are expanding the deployment frontier beyond conventional ground-mounted parks. Public sector developers have commissioned floating projects, while several state agencies are exploring agrivoltaic models to address land-use pressure and farmer income concerns.

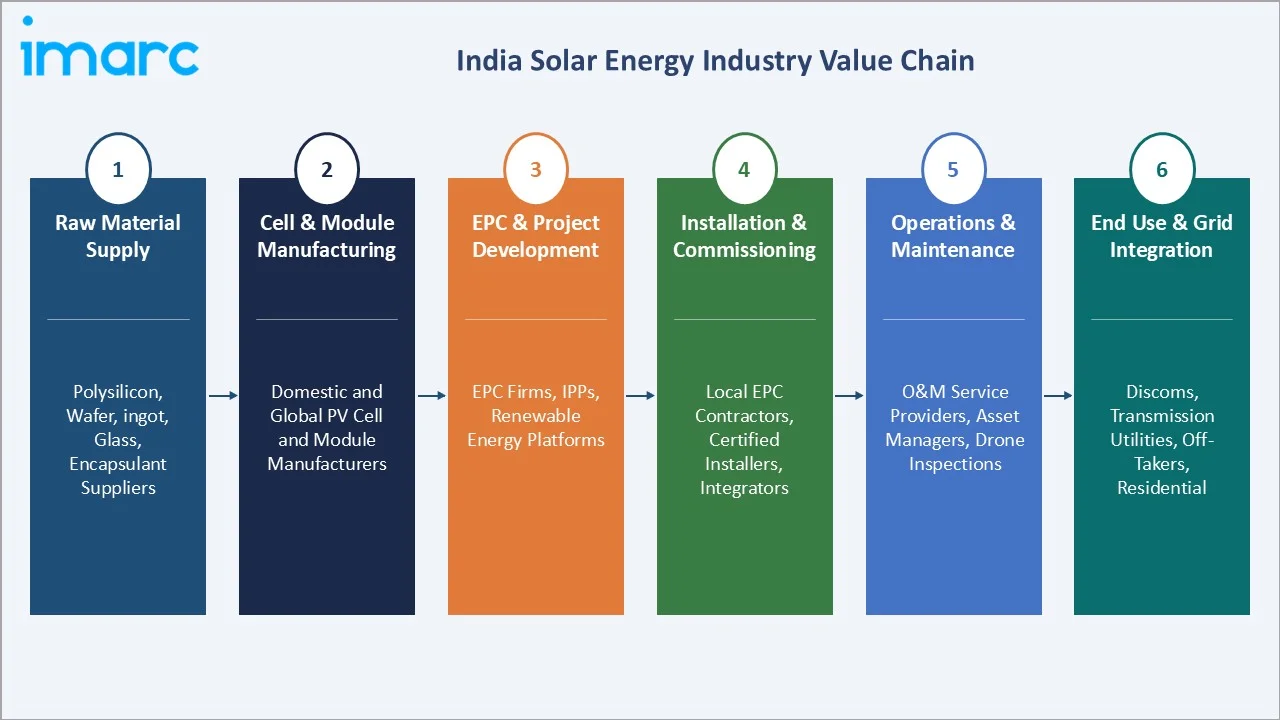

Industry Value Chain Analysis

The India solar energy value chain spans six major stages from raw material supply through end-use grid integration. Cell and module manufacturing along with EPC and project development capture the highest share of value creation, while operations and maintenance is emerging as a sticky, recurring revenue layer for established players.

|

Stage |

Key Participants |

|

Raw Material Supply |

Polysilicon, wafer, ingot, glass, encapsulant, and aluminum frame suppliers - largely a mix of domestic processors and global upstream producers |

| Cell and Module Manufacturing | Polysilicon, wafer, ingot, glass, encapsulant, and aluminum frame suppliers - largely a mix of domestic processors and global upstream producers |

| EPC and Project Development | Engineering, procurement, and construction companies, independent power producers, and renewable energy platforms developing utility-scale and rooftop projects |

| Installation and Commissioning | Local EPC contractors, channel partners, certified installers, and system integrators delivering turnkey rooftop and ground-mounted solutions |

| Operations and Maintenance | Specialized O&M service providers, asset management firms, drone-based inspection companies, and inverter OEM service teams |

| End Use and Grid Integration | Discoms, transmission utilities, commercial and industrial off-takers, residential consumers, and storage solution providers |

Vertically integrated players, which combine module manufacturing with EPC and project development, achieve superior cost control and supply security versus pure-play developers reliant on third-party module sourcing.

Technology Landscape in the India Solar Energy Industry

Cell and Module Innovation

Tunnel Oxide Passivated Contact (TopCon) and heterojunction (HJT) modules are progressively replacing mono PERC as the preferred technology for new utility-scale projects, owing to higher efficiency and improved temperature coefficients. Bifacial modules paired with single-axis trackers are increasingly the default configuration for large parks, lifting per-MW energy yields significantly compared to earlier deployments.

Inverters, Trackers, and Power Electronics

String and central inverters from established global and domestic manufacturers continue to dominate utility-scale installations, while microinverters and hybrid inverters are gaining traction in rooftop and residential applications. Smart trackers with weather-adaptive algorithms are improving generation, particularly in cyclone-prone coastal states.

Storage, Smart Grid, and Forecasting

Lithium iron phosphate (LFP) battery integration with solar projects is rapidly maturing, supported by falling battery cell prices and dedicated storage tenders by state utilities. Cloud-based generation forecasting, AI-driven O&M tools, and digital twin platforms are emerging across leading developers, supporting better dispatch and asset performance management.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Deployment | Ground-mounted | 58.05% | 2025 |

| Application | Commercial and Industrial | 36.1% | 2025 |

| Region | West India | 33.8% | 2025 |

By Deployment

Ground-mounted commands a 58.05% majority share in 2025, anchored by mega solar parks across Rajasthan, Gujarat, and Andhra Pradesh, where land availability, high solar irradiance, and central PSU procurement converge. Most utility-scale auctions remain ground-mounted, with trackers and bifacial modules now standard.

To access detailed market analysis, Request Sample

Rooftop at 41.95% in 2025 is the fastest-growing deployment category, driven by PM Surya Ghar: Muft Bijli Yojana, simplified net-metering, and the expanding presence of organized rooftop EPC players. Residential and small commercial rooftops are scaling rapidly across Gujarat, Maharashtra, Kerala, and Uttar Pradesh.

By Application

Commercial and industrial dominates with 36.1% share in 2025, reflecting strong corporate demand for open-access power, group captive plants, and rooftop systems on factories and warehouses. Sustainability commitments by listed companies and rising grid tariffs are reinforcing the structural shift.

Utility-scale at 34.2% in 2025 covers central and state auctions executed by state agencies, along with merchant solar power plants. The category benefits from long-term PPAs, large parks, and access to inter-state transmission corridors.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

West India |

33.8% |

Strong industrial and commercial power demand, supportive state-level renewable policies, high solar irradiance, and access to large land parcels |

|

South India |

27.6% |

Robust commercial and industrial open-access framework, growing IT and manufacturing footprint, and well-established rooftop installer ecosystem |

|

North India |

24.5% |

Large-scale utility solar parks, central agency procurement, expanding residential rooftop adoption, and rising agricultural solarization |

|

East India |

14.1% |

Emerging industrial corridors, growing rooftop awareness, and increasing focus on rural electrification through decentralized sola |

West India at 33.8% in 2025 leads the country, driven by Gujarat's Khavda Renewable Energy Park, Maharashtra's industrial demand, and Madhya Pradesh's competitive utility-scale auctions. The region also hosts a substantial share of India's solar module manufacturing footprint, creating a deep ecosystem advantage that further consolidates its leadership.

South India at 27.6% benefits from progressive commercial and industrial open-access norms in Karnataka and Tamil Nadu, large rooftop programs in Telangana and Kerala, and the steady growth of utility-scale auctions in Andhra Pradesh. The region is expected to remain a high-growth market through 2034.

Competitive Landscape

The India solar energy market is moderately fragmented, with vertically integrated developers and module manufacturers leading project pipelines while specialized EPCs and rooftop integrators serve regional and segmental niches. Land-bank depth, manufacturing scale, and execution speed form the core competitive moats.

|

Company Name |

Brand |

Market Position |

Core Strength |

| Adani Group | Adani Green Energy Limited (AGEL) utility-scale solar and hybrid generation portfolio |

Leader |

Vertically integrated solar generation with large-scale park development |

| Tata Power | Tata Power Solar / TP Renewable Microgrid |

Leader |

Diversified solar generation, EPC, and rooftop solutions across segments |

| Waaree Energies Ltd. | Waaree Radiance All in one Solar Kit; solar PV modules and EPC offerings | Leader | Module manufacturing scale paired with EPC and rooftop distribution |

| ReNew | G12R TOPCon Bifacial, TOPCon Bifacial, Mono PERC Bifacial | Challenger | Independent renewable power producer with utility-scale solar focus |

| JSW | JSW Neo Energy Limited | Challenger | Diversified power generation expanding into utility-scale solar and hybrid renewables |

Key players include Adani Group, Tata Power, Waaree Energies Ltd., ReNew, and JSW, among others.

Key Company Profiles

Adani Group

Adani Group is one of India's largest diversified business conglomerates, headquartered in Ahmedabad, Gujarat, with operations spanning energy, ports, logistics, mining, airports, and infrastructure. The group's renewable energy footprint is spearheaded by its listed subsidiary Adani Green Energy Limited (AGEL), one of India's largest renewable power developers.

- Product Portfolio: Utility-scale solar parks, wind-solar hybrid plants, and integrated renewable generation assets, including the Khavda Renewable Energy Park in Gujarat planned to scale capacity across solar, wind, and storage.

- Recent Developments: In March 2025, Adani Green Energy Limited (AGEL), the subsidiary of Adani Group, commissioned a 250 MW solar plant in Bhimsar, Rajasthan, expanding operating capacity across major solar-rich states.

- Strategic Focus: Expanding renewable capacity by 2030 through large parks, hybrid configurations, and progressive integration of battery storage to deliver firm renewable supply.

Waaree Energies Ltd.

Waaree Energies Ltd., headquartered in Mumbai, is a leading solar PV module manufacturer in India. The company operates module manufacturing facilities in Gujarat with a significant export footprint across several countries, alongside EPC and rooftop offerings across India.

- Product Portfolio: Waaree Radiance All-in-One Solar Kit, rooftop solutions, and solar inverters for residential, commercial, and utility-scale applications.

- Recent Developments: In December 2025, Waaree Energies Ltd.'s Chikhli plant was added to MNRE's ALMM list with 16.444 GW approved capacity, taking its total Indian module manufacturing capacity to 20.17 GW.

- Strategic Focus: Scaling integrated cell and module manufacturing capacity, expanding into solar EPC and rooftop installation services, and growing its export-oriented business across the United States and the Middle East.

ReNew

ReNew is one of India's largest pure-play renewable energy independent power producers. The company operates a diversified portfolio of utility-scale solar, wind, and hybrid projects, supported by a domestic solar cell and module manufacturing facility in Dholera, Gujarat.

- Product Portfolio: G12R TOPCon Bifacial modules, TOPCon Bifacial modules, utility-scale solar power generation, wind-solar hybrid projects, Round-the-Clock renewable supply contracts, and corporate PPA structures for commercial and industrial consumers.

- Recent Developments: As of September 2025, ReNew's total portfolio stood at approximately 18.5 GW, including 1.1 GWh of battery energy storage. The company continues to expand its hybrid and round-the-clock renewable offerings, strengthening its position in integrated clean energy solutions.

- Strategic Focus: Building a firm renewable supply portfolio combining solar, wind, and storage to deliver dispatchable clean power for utilities and large commercial and industrial customers.

Market Concentration Analysis

The India solar energy market is moderately concentrated, with the top five players - Adani Group, Tata Power, Waaree Energies Ltd., ReNew, and JSW - estimated to hold a meaningful share of operating capacity and module supply in 2025.

Barriers to entry include high capital requirements for utility-scale projects, multi-year track record expectations in central tenders, and the scale required to remain competitive in increasingly aggressive bid environments.

Consolidation is gradually intensifying through acquisitions of operating solar assets, vertical integration into module manufacturing, and the entry of public sector and large industrial groups into renewable platforms. Manufacturing scale, balance-sheet depth, and execution capability are reinforcing the leadership of established incumbents.

Investment & Growth Opportunities

Fastest-Growing Segments

Rooftop at 41.95% and residential at 29.7% are expected to expand faster than the overall 37.82% market CAGR through 2034, supported by PM Surya Ghar: Muft Bijli Yojana, easy financing, and rising household tariffs. Commercial and industrial open-access solar is also expected to outpace the broader market.

Emerging Markets and Sub-segments

East India at 14.1% and tier-2 cities across the country represent significant untapped potential as rooftop awareness, EPC networks, and financing options expand. Floating solar, agrivoltaics, and green hydrogen-linked solar capacity are emerging as new high-growth sub-segments.

Venture and Investment Trends

Investment activity is concentrated in solar manufacturing under the PLI scheme, large utility-scale park developers, and storage-integrated renewable platforms. Climate-focused private equity and infrastructure funds continue to back domestic IPPs, while public capital is supporting transmission and storage build-out.

Future Market Outlook (2026-2034)

The India solar energy market is forecast to expand from USD 30.03 Billion in 2025 to an estimated USD 41.39 Billion in 2026 and further to USD 538.91 Billion by 2034 at a CAGR of 37.82%, adding more than USD 500 Billion in cumulative market value over the forecast period.

Four forces will shape the market through 2034: continued declines in module and storage costs; the scaling of solar-plus-storage and Round-the-Clock renewable contracts; rapid growth of residential rooftop solar under PM Surya Ghar; and the expansion of green hydrogen and industrial decarbonization use cases.

By 2034, solar power is expected to anchor a significant share of India's electricity generation mix, with battery storage integration becoming standard practice for new utility-scale projects. Vertically integrated developers and module manufacturers are likely to consolidate further, while rooftop and residential segments will continue to deepen across geographies.

Research Methodology

Primary Research

Primary research included structured interviews with solar project developers, module manufacturing executives, EPC firms, rooftop installers, financiers, central agency officials, and industrial off-takers, validating market sizing, regional demand patterns, deployment splits, and application-mix evolution.

Secondary Research

Secondary sources included MNRE statistics, Central Electricity Authority data, SECI auction outcomes, NITI Aayog reports, IRENA and IEA publications, listed company annual reports and investor presentations, and reputed energy news outlets, such as the Press Information Bureau.

Forecasting Models

Market forecasts combine top-down and bottom-up models built around installed capacity additions, module price trajectories, segment-wise tariff trends, central and state-level policy schedules, and sectoral consumption patterns. Scenario analysis covers module price variation, currency movement, and policy execution outcomes.

India Solar Energy Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Deployments Covered | Rooftop, Ground-mounted |

| Applications Covered | Residential, Commercial and Industrial, Utility-scale |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Adani Group, Tata Power, Waaree Energies Ltd., ReNew, JSW, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Solar Energy Market Report

The India solar energy market size is estimated at USD 41.39 Billion in 2026, supported by strong policy push, falling module prices, and rising commercial and industrial demand for clean power.

The market is projected to grow at a CAGR of 37.82% from 2026-2034, reaching USD 538.91 Billion, driven by capacity expansion, residential rooftop adoption, and solar-plus-storage tenders.

Ground-mounted leads at 58.05% in 2025, driven by utility-scale parks. Rooftop at 41.95% is expanding faster, fueled by PM Surya Ghar and net-metering reforms.

Commercial and industrial dominate at 36.1% in 2025, driven by rising open-access adoption and strong demand for reliable power among businesses. It is followed by utility-scale at 34.2%, supported by large project deployments and central auctions.

West India commands 33.8% in 2025, led by Gujarat and Maharashtra, supported by high solar irradiation, strong policy support, and large-scale project installations in key states. South India at 27.6% follows, driven by favorable regulations and established renewable ecosystems.

Leading players include Adani Group, Tata Power, Waaree Energies Ltd., ReNew, and JSW.

Domestic manufacturing under the PLI scheme is rapidly scaling cell and module capacity, reducing import dependence, and supporting the ALMM-led domestic content requirements.

Key challenges include land acquisition delays, transmission and grid integration bottlenecks, discom payment delays, and dependence on imported polysilicon and wafers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade