India Solar Rooftop Market Size, Share, Trends and Forecast by Grid Type, End User, and Region, 2026-2034

India Solar Rooftop Market Summary:

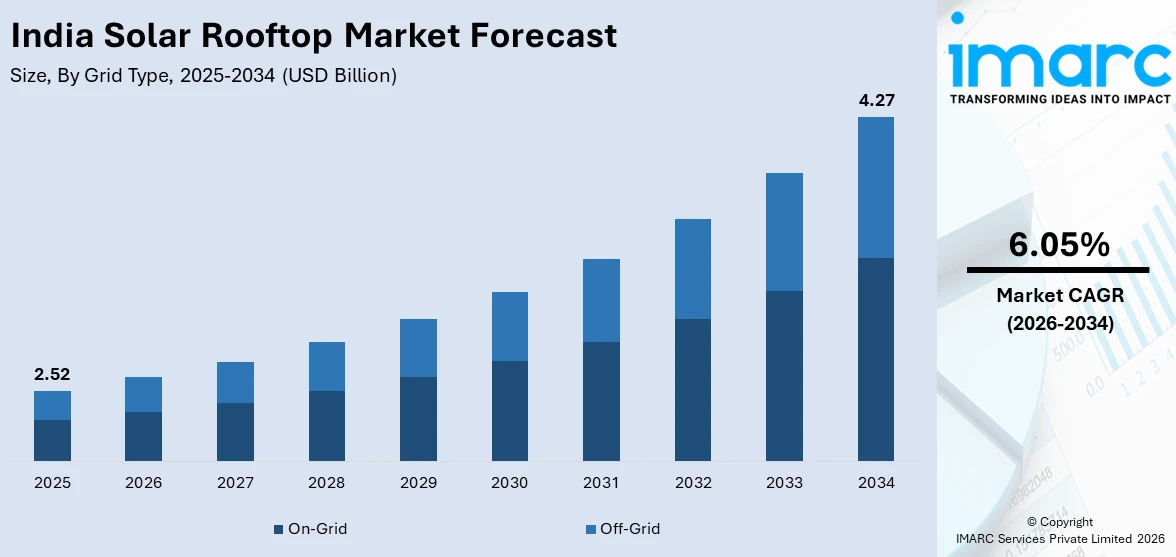

The India solar rooftop market size was valued at USD 2.52 Billion in 2025 and is projected to reach USD 4.27 Billion by 2034, growing at a compound annual growth rate of 6.05% from 2026-2034.

The India solar rooftop market is witnessing notable growth driven by favorable government policies, rising electricity tariffs, and rising adoption of decentralized energy solutions across residential and commercial segments. Increasing environmental consciousness, supportive net metering frameworks, declining solar panel costs, and rapid urbanization are accelerating the transition toward rooftop solar installations. The proliferation of digital monitoring platforms, innovative financing models, and corporate sustainability mandates are further strengthening adoption trends, positioning India as a leading hub for distributed solar energy generation.

Key Takeaways and Insights:

- By Grid Type: On-grid dominates the market with a share of 90% in 2025, driven by the widespread adoption of net metering policies across states and the economic advantage of feeding surplus electricity back to the grid, which significantly reduces payback periods for consumers.

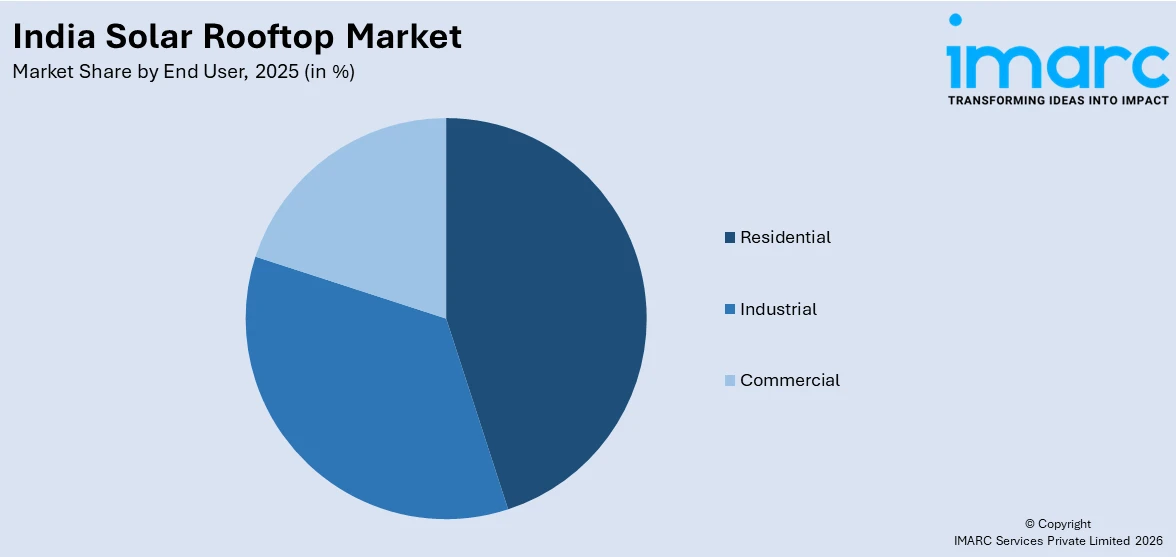

- By End User: Residential represents the largest segment with a market share of 41% in 2025, driven by government subsidy programs, rising household electricity costs, and the growing user awareness about long-term savings from rooftop solar installations.

- By Region: South India leads the market with a share of 35% in 2025, supported by favorable solar irradiance levels, progressive state-level solar policies, established distribution networks, and strong rooftop solar adoption in states like Kerala, Karnataka, and Tamil Nadu.

- Key Players: The India solar rooftop market features a mix of established integrated energy companies and specialized engineering, procurement, and construction (EPC) providers competing through product innovation, financing solutions, digital monitoring capabilities, and expanding distribution networks across urban and semi-urban areas.

To get more information on this market Request Sample

The India rooftop solar market is driven by strong policy backing, rising electricity demand, and the growing individual interest in affordable and sustainable energy solutions. Government subsidy programs, net metering frameworks, and renewable targets are improving project feasibility across residential and commercial segments. Rapid urbanization and higher power utilization are encouraging decentralized generation to reduce dependence on grid supply. Declining technology costs and improved system performance are further strengthening adoption. Market growth is also supported by awareness-building initiatives, as in 2025, SolarSquare launched its nationwide “Apna Desh, Apni Bijli” campaign aligned with the PM Surya Ghar Muft Bijli Yojana and Atmanirbhar Bharat vision. The company reported supporting over 30,000 families across more than 20 cities through residential rooftop installations. Innovative financing options, domestic manufacturing expansion, and stronger distribution networks continue to strengthen the market growth.

India Solar Rooftop Market Trends:

Availability of Innovative Financing and Solar Leasing Models

The expansion of innovative financing options that reduce upfront investment barriers for individuals is a crucial factor bolstering the market growth. Models, such as loans, leasing arrangements, and power purchase agreements, are improving affordability and enabling wider participation among households and small enterprises. This trend gained momentum in 2025 when Tata Power Renewable Energy Limited introduced EMI-based rooftop solar solutions in Bhubaneswar under its Ghar Ghar Solar campaign, supported by central and Odisha state subsidies through the PM Surya Ghar Muft Bijli Yojana. By allowing small initial payments and monthly installments, such financing structures are accelerating residential adoption and supporting the growth in the rooftop solar market.

Rising Commercial and Industrial Adoption

The India solar rooftop market is experiencing growth due to increasing adoption among commercial and industrial users, supported by targeted utility-led programs tailored to energy-intensive sectors. These initiatives address key adoption barriers by offering end-to-end solutions, technical support, and accessible financing structures. This approach was highlighted in 2025 when Tata Power Renewables launched the “Scale Sustainably with Tata Power” campaign in Raipur, focusing on commercial and industrial users in Chhattisgarh. By providing easy financing options, including low-interest and collateral-free loans, and aligning with regional renewable energy priorities, such programs are accelerating rooftop solar deployment across industrial clusters and supporting the market growth.

Expansion of Integrated Rooftop Solar Product Offerings

The India solar rooftop market is being supported by the growing availability of integrated and user-friendly solar product packages delivered through strategic industry collaborations. Bundled rooftop solar kits simplify adoption by providing complete solutions that include modules, inverters, and essential balance-of-system components, reducing complexity for households and small enterprises. This trend was reinforced in 2025 when Redington partnered with Websol Energy System to launch bundled residential rooftop solar kits, ranging from 2 kW to 10 kW across India. By leveraging Redington’s distribution network and enabling access to subsidies of up to ₹78,000 under the PM Surya Ghar scheme, such initiatives are accelerating market penetration and household adoption.

Market Outlook 2026-2034:

The India solar rooftop market revenue is expected to witness notable growth over the forecast period, supported by strong government policy incentives, falling solar technology costs, and increasing awareness of clean energy adoption among residential, commercial, and industrial users. The market generated a revenue of USD 2.52 Billion in 2025 and is projected to reach a revenue of USD 4.27 Billion by 2034, growing at a compound annual growth rate of 6.05% from 2026-2034. Rising electricity demand, supportive net metering frameworks, and investment in distributed renewable energy systems will continue to strengthen rooftop solar deployment across India.

India Solar Rooftop Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Grid Type |

On-Grid |

90% |

|

End User |

Residential |

41% |

|

Region |

South India |

35% |

Grid Type Insights:

- On-Grid

- Off-Grid

On-grid dominates with a market share of 90% of the total India solar rooftop market in 2025.

On-grid holds the biggest market share owing to its cost effectiveness, reliability, and ability to integrate seamlessly with existing power infrastructure. This system allows users to draw electricity from the grid when solar generation is insufficient and export excess power during peak production periods. Net metering mechanisms make on-grid installations financially attractive by enabling bill reductions and faster payback periods. As grid connectivity remains widespread across urban and semi urban areas, on-grid rooftop solar continues to gain strong adoption.

The dominance of on-grid system is further reinforced by supportive government policies and regulatory frameworks that promote grid connected renewable energy. Utilities encourage on-grid rooftop installations to reduce peak load stress and enhance distributed generation. On-grid system also requires lower upfront investment compared to hybrid or off-grid solutions, as it does not rely heavily on battery storage. This affordability, combined with simplified maintenance requirements, makes on-grid rooftop solar the preferred choice for residential, commercial, and industrial users across India.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Industrial

- Commercial

- Residential

Residential leads with a market share of 41% of the total India solar rooftop market in 2025.

Residential represents the largest segment driven by the rising household electricity demand, increasing awareness about clean energy benefits, and supportive government incentives. Rooftop solar systems help homeowners reduce monthly power bills while providing greater energy independence. Net metering policies and subsidy schemes are making residential installations more affordable, encouraging adoption across urban and semi urban areas. The growing preference for sustainable living and long-term cost savings continue to position households as the largest contributor to rooftop solar demand in India.

The dominance of the residential segment is further reinforced by rapid urbanization and the expansion of housing developments across the country. Homeowners increasingly view rooftop solar as a practical investment that enhances property value and supports reliable power supply. Higher panel efficiency and falling equipment costs are making adoption easier for middle-income households, while simplified installation and financing options are speeding uptake. For example, in 2025, Tata Power launched its ‘Ghar Ghar Solar’ campaign in Pune under the PM Surya Ghar Yojana, reporting 775 MWp installed capacity in Maharashtra by July 2025.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

South India exhibits a clear dominance with a 35% share of the total India solar rooftop market in 2025.

South India leads the market due to its high solar irradiation levels, strong policy support, and early adoption of renewable energy solutions. States in the region have implemented favorable net metering regulations, subsidy programs, and streamlined approval processes, encouraging rooftop solar installations across residential, commercial, and industrial users. For instance, in 2025, Kondareddypalli village in Telangana became South India’s first fully solar-powered model village under the state’s Green Energy Mission. The project equipped 514 homes and 11 government buildings with rooftop solar systems, reaching a total installed capacity of 1,500 kW.

The dominance of South India is further reinforced by the region’s strong industrial base and the growing focus on sustainable energy practices. Commercial establishments and manufacturing facilities increasingly adopt rooftop solar to reduce electricity costs and improve energy security. High awareness about clean energy benefits, combined with active participation from private developers and financing institutions, accelerates market penetration. Additionally, grid constraints in certain areas make decentralized rooftop generation an attractive solution. As renewable targets expand, South India continues to represent the most mature and high growth regional market for solar rooftop systems.

Market Dynamics:

Growth Drivers:

Why is the India Solar Rooftop Market Growing?

Growth of Domestic Solar Manufacturing and Supply Chain Strengthening

India’s push to strengthen domestic solar manufacturing is playing a key role in supporting the rooftop solar market by improving supply chain resilience and reducing dependence on imports. Expanded local production of modules, inverters, and balance-of-system components is enhancing price stability and equipment availability. This trend is reflected in industry developments, as in 2025 Premier Energies expanded into solar inverter and transformer manufacturing through majority stakes in KSolar Energy and Transcon India, targeting residential rooftop demand under the PM Surya Ghar scheme. Such diversification supports job creation, technological capability, and faster project execution, enabling rooftop solar deployment to scale more efficiently and sustain long-term market growth.

Rising Electricity Demand and Urban Energy Utilization Growth

India’s rapid urbanization and economic growth are driving higher electricity demand across residential and commercial sectors, driving the need for decentralized energy solutions. Rooftop solar is emerging as an effective option to meet rising utilization from household appliances, cooling needs, and business operations while easing pressure on grid infrastructure. This demand is reflected in state-level initiatives, as in 2025 Tata Power–led Odisha distribution companies launched a 1-kW rooftop solar scheme under the PM Surya Ghar Muft Bijli Yojana, enabling households to generate around 100 units monthly with a ₹5,000 payment and subsidy support. Such programs highlight rooftop solar’s growing role in scalable, distributed power generation.

Government Policy Support and National Renewable Energy Targets

Supportive government policies are influencing the India solar rooftop market, as national and state authorities continue to promote renewable energy adoption and reduce dependence on fossil fuels. Regulatory frameworks, net metering provisions, and targeted subsidy schemes are improving project feasibility across residential and commercial segments. This policy momentum was reinforced in 2025 when the Maharashtra government announced the SMART Solar Scheme, offering additional state subsidies under the PM Suryaghar Yojana to households employing below 100 units per month. Targeting five lakh domestic users with a ₹655 crore budget, the program aimed to strengthen investor confidence, increase individual awareness, and enable wider rooftop solar adoption across urban, semi-urban, and remote regions.

Market Restraints:

What Challenges the India Solar Rooftop Market is Facing?

Domestic Module Supply Constraints and Quality Concerns

Despite rapid expansion of solar manufacturing capacity, the availability of domestic content requirement-compliant solar modules remains a significant challenge constraining market growth. The mismatch between domestic cell capacity and the much larger module manufacturing capacity creates bottlenecks in meeting subsidy-linked procurement requirements, leading to project delays and discouraging certain consumer segments from pursuing subsidized installations.

Complex Regulatory and Approval Processes Across States

Inconsistent regulatory frameworks, varying net metering policies, and complex approval procedures across different Indian states create confusion among individuals and delay project execution timelines. While the government mandates an approval and commissioning period, real-world timelines often extend significantly, undermining user confidence and discouraging adoption in states with less supportive regulatory environments.

Limited Consumer Awareness and Financing Accessibility in Semi-Urban Areas

Despite growing urban awareness, significant knowledge gaps persist among people in semi-urban and rural areas regarding the benefits, financing options, and operational aspects of rooftop solar systems. Limited outreach in regional languages, dependence on vendor-driven information, and the perceived complexity of application processes continue to suppress adoption rates in these markets.

Competitive Landscape:

The India solar rooftop market features a dynamic competitive landscape characterized by the presence of large integrated energy companies, specialized solar EPC providers, and emerging technology-focused startups competing across residential, commercial, and industrial segments. Market participants are increasingly differentiating through end-to-end solutions that combine panel manufacturing, installation services, digital monitoring platforms, and flexible financing options. Competition is intensifying as companies expand their geographic reach into tier-two and tier-three cities, invest in advanced module technologies, and develop innovative business models including subscription-based solar services and carbon-accountable rooftop power purchase agreements to capture the growing demand driven by government incentives and corporate sustainability mandates.

Recent Developments:

- December 2025: Tata Power Delhi Distribution Limited launched the Solar Ambassador initiative to promote rooftop solar adoption under the PM Surya Ghar Muft Bijli Yojana. The program appointed 20 specially trained officials to work directly with communities in North-West Delhi, spreading awareness and guiding households on rooftop solar benefits. Unveiled at the TPSDI–CENPEID Green Energy Skill Centre, the initiative aimed to bridge government policy with grassroots action and accelerate residential solar uptake.

- June 2025: India’s Ministry of New and Renewable Energy launched an Innovative Projects Start-Up Challenge to accelerate rooftop solar and distributed renewable energy solutions. The initiative invited startups to develop ideas around affordability, resilience, inclusivity, and sustainability, with a total prize pool of ₹2.3 crore. Winners will also receive incubation support, pilot opportunities, and expert mentorship, with applications open until 20 August 2025.

India Solar Rooftop Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Grid Types Covered | On-Grid, Off-Grid |

| End Users Covered | Industrial, Commercial, Residential |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Solar Rooftop Market Research Report and Industry Forecast Report

The India solar rooftop market size was valued at USD 2.52 Billion in 2025.

The India solar rooftop market is expected to grow at a compound annual growth rate of 6.05% from 2026-2034 to reach USD 4.27 Billion by 2034.

On-grid holds the largest revenue share at 90% in 2025, driven by widespread net metering adoption, grid connectivity advantages, and the economic benefits of feeding surplus electricity back to distribution networks across Indian states.

Key factors driving the India solar rooftop market include the availability of flexible financing models that lower upfront costs and improve affordability. This was evident in 2025 when Tata Power Renewables launched EMI-based rooftop solar options in Bhubaneswar, supported by PM Surya Ghar subsidies, accelerating household-level adoption.

Major challenges include domestic module supply constraints and quality concerns, complex regulatory and approval processes varying across states, limited user awareness in semi-urban areas, financing accessibility barriers, and infrastructure gaps in net metering and grid connectivity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)