India Soy Milk Market Size, Share, Trends and Forecast by Product, Flavor, Type, Distribution Channel, and Region, 2026-2034

India Soy Milk Market Summary:

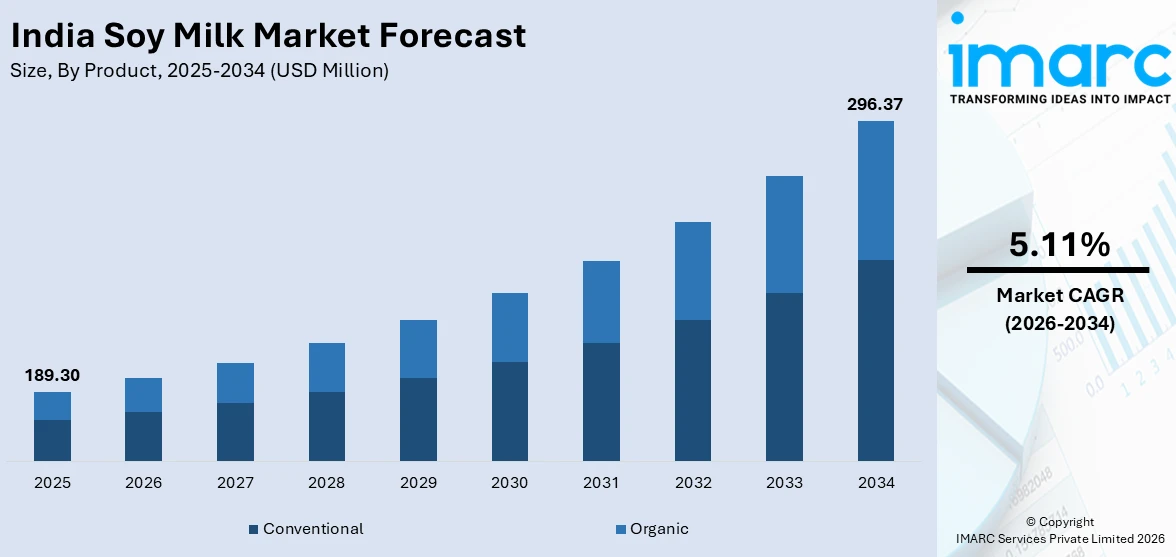

The India soy milk market size was valued at USD 189.30 Million in 2025 and is projected to reach USD 296.37 Million by 2034, growing at a compound annual growth rate of 5.11% from 2026-2034.

The India soy milk market is seeing significant growth fueled by the growing health awareness among urban consumers, the prevalent incidence of lactose intolerance, and the rising adoption of vegan and flexitarian dietary choices. Enhancing access via structured retail channels, innovations in flavors and fortifications, along with increasing disposable incomes, is further driving the adoption. Innovations in packaging technology, the growing e-commerce platforms, and supportive government policies for plant-based food processing are collectively transforming the competitive environment and contributing to the India soy milk market share.

Key Takeaways and Insights:

- By Product: Conventional represents the largest segment with a market share of 88.7% in 2025, driven by its broad availability, competitive pricing compared to organic options, and established consumer recognition in urban and semi-urban retail outlets.

- By Flavor Outlook: Plain/unflavored dominates the market with a share of 67.5% in 2025, supported by its adaptability in everyday cooking uses, such as tea, coffee, smoothies, and classic Indian dishes that need neutral-tasting foundational ingredients.

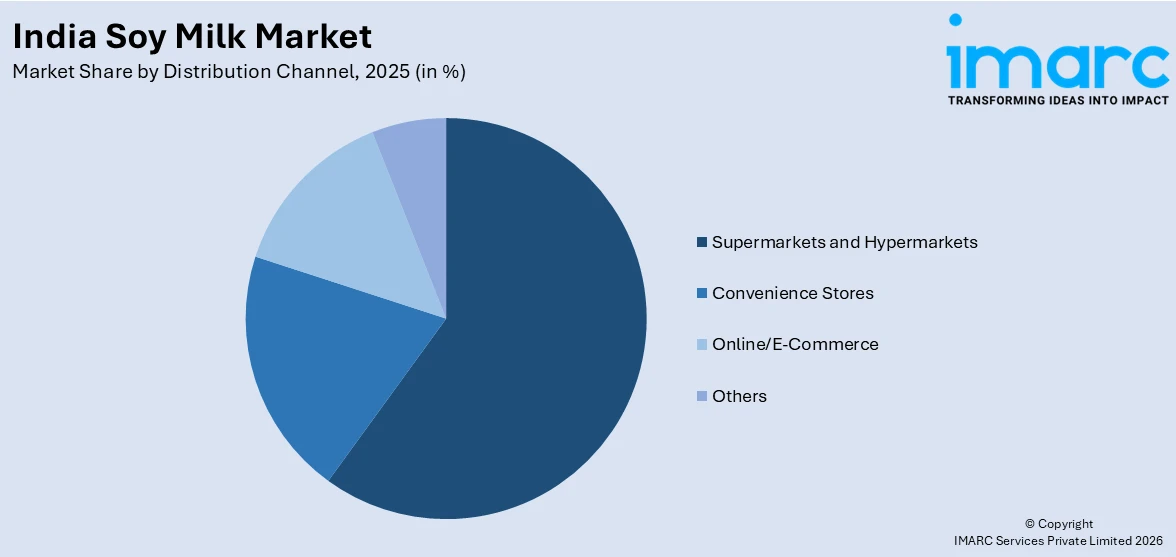

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 59.8% in 2025, owing to their wide range of product offerings, competitive pricing tactics, and expanding organized retail presence throughout Indian urban regions.

- By Region: North India represents the largest segment with a market share of 36.5% in 2025, benefiting from increased urbanization, greater purchasing power, and a robust retail infrastructure that facilitates a variety of plant-based products.

- Key Players: The India soy milk market presents a moderately competitive environment, with well-established international brands and local producers vying for market share through innovative products, varied flavors, fortification methods, and broader distribution channels to enhance market visibility.

To get more information on this market Request Sample

The soy milk industry in India is being driven by rising health awareness, the growing environmental concerns, and enhanced consumer purchasing power. An increasing number of people are transitioning to plant-based diets to control cholesterol levels, promote heart health, and tackle lactose intolerance, thus boosting the demand for soy-based products. Moreover, the growing worries about the environmental effects of animal-derived dairy production are motivating eco-aware families to choose more sustainable drink options. Additionally, increased disposable incomes are enhancing individuals' capacity to try out premium and value-added products. The Ministry of Statistics (MoSPI) announced that per capita Net National Income increased to ₹2,05,324 in FY2024–25, up from ₹1,88,892 in FY2023–24, indicating enhanced earnings and increased consumption ability. The increase in income, along with enhanced retail distribution and product innovation, is facilitating wider acceptance of soy milk in urban and semi-urban areas, thus strengthening the market growth.

India Soy Milk Market Trends:

Growing Integration of Soy Milk in Foodservice and Café Culture

Soy milk is increasingly being adopted by cafés, bakeries, and foodservice establishments across India as a mainstream dairy alternative for beverages and culinary applications. This trend is normalizing soy milk consumption in social settings and introducing the product to new consumer segments. For instance, in 2025, Dolci, a premium European-themed café, opened its third outlet on New BEL Road, Bengaluru, expanding its presence in the city. The café offered artisanal European cuisine, signature beverages, and multiple milk alternatives like A2 cow, soy, and almond milk, catering to diverse dietary preferences.

Sustainability and Environmental Concerns

Consumers are recognizing the ecological footprint of animal-based dairy, including resource-intensive production and greenhouse gas emissions. Plant-based alternatives like soy milk are viewed as environmentally responsible options, aligning with the preferences of eco-conscious consumers. This consideration, combined with the growing discourse on climate change and sustainable agriculture, motivates households to incorporate soy milk into their diets. Manufacturers are responding by expanding product portfolios, enhancing taste, nutrition, and shelf life, and adopting sustainable sourcing practices. For instance, in 2024, 1.5 Degree launched a complete range of plant-based dairy products, including Oat Milk, Soy Milk, flavored milkshakes, and gelatos in 12 flavors, at the 7th India International Hospitality Expo in Greater Noida. These vegan, gluten-free, and lactose-free offerings cater to health-conscious consumers seeking sustainable and nutritious dairy alternatives.

Increased Retail and E-commerce Penetration

The expansion of modern retail outlets, supermarkets, and online marketplaces is greatly improving the availability and visibility of soy milk products in India. This trend significantly influences tier-II and tier-III cities, where organized retail expansion is introducing soy milk to populations that were previously underserved. E-commerce platforms also provide a wide array of branded and fortified soy milk options, delivering convenience directly to consumers’ homes, along with attractive pricing and subscription plans that promote both initial purchases and repeat orders. In line with this trend, the IBEF estimates that India’s e-commerce market is expected to attain INR 29,88,735 Crore (USD 345 Billion) by 2030, underscoring the increasing potential of online channels for soy milk distribution.

Market Outlook 2026-2034:

The India soy milk market shows strong growth potential over the forecast period, supported by positive demographic trends, changing dietary choices, and expanding retail infrastructure. The market generated a revenue of USD 189.30 Million in 2025 and is projected to reach a revenue of USD 296.37 Million by 2034, growing at a compound annual growth rate of 5.11% from 2026-2034. Enhanced domestic soybean production abilities, improved e-commerce adoption, and the growing consumer awareness about plant-based nutrition are likely to support revenue growth across various product categories and distribution channels throughout the forecast period.

India Soy Milk Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Conventional |

88.7% |

|

Flavor Outlook |

Plain/Unflavored |

67.5% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

59.8% |

|

Region |

North India |

36.5% |

Product Insights:

- Conventional

- Organic

Conventional dominates with a market share of 88.7% of the total India soy milk market in 2025.

Conventional commands the largest market share attributed to its extensive availability, cost-effectiveness, and robust presence throughout mainstream retail outlets. The majority of shoppers still buy traditional options due to their easy availability in supermarkets, neighborhood grocery shops, and online sites. Conventional soy milk products are typically manufactured on a larger scale, enabling brands to provide competitive prices in comparison to premium organic alternatives. This positions it as a favored option for middle-income families looking for healthy dairy alternatives without incurring extra expenses. The category gains from recognizable packaging styles and uniform taste characteristics, promoting repeat purchases.

The prevalence of conventional soy milk is further fueled by the rising demand for plant-based drinks in regular diets. Numerous people opt for traditional items for everyday consumption in tea, coffee, breakfast cereals, and cooking purposes. Major food and beverage firms vigorously market traditional soy milk via promotions, price reductions, and expanded distribution channels, enhancing market presence. Furthermore, the restricted awareness and elevated price of organic soy milk limit its uptake outside of specific consumer segments. As lactose intolerance issues increase and the demand for budget-friendly plant-based options rises, traditional soy milk remains dominant in the market.

Flavor Outlook Insights:

- Plain/Unflavored

- Flavored

Plain/unflavored leads with a market share of 67.5% of the total India soy milk market in 2025.

Plain/unflavored exhibits a clear dominance in the market because of its broad appeal among health-conscious consumers seeking a natural and minimally processed beverage. Many buyers prefer plain variants as they contain fewer additives and allow greater flexibility in daily consumption. Unflavored soy milk is widely used in tea, coffee, cereals, smoothies, and cooking, making it a staple choice for households shifting toward plant-based alternatives. Its neutral taste suits both traditional Indian recipes and modern dietary routines, supporting adoption among vegan consumers, lactose-intolerant individuals, and those focused on clean eating habits.

The dominance of plain soy milk is also supported by increasing awareness around sugar reduction and balanced nutrition. Consumers often view unflavored options as a healthier substitute compared to sweetened or flavored varieties, especially for diabetes management and weight control. Food service operators, cafés, and health-focused restaurants also prefer plain soy milk as a base ingredient for customized drinks and recipes. Retailers stock plain variants prominently due to consistent demand across urban and semi-urban markets. With rising preference for simple, versatile, and functional plant-based beverages, plain soy milk continues to strengthen its leading position in India’s soy milk flavor segment.

Type Insights:

- Unsweetened

- Sweetened

Unsweetened dominates the market driven by the rising health consciousness and a growing preference for low-calorie beverages. Consumers are progressively steering clear of added sugars for weight management, diabetes control, and cardiovascular health practices. City-dwelling families, health-conscious individuals, and those on vegan or lactose-free diets frequently opt for unsweetened options due to their clean labels and adaptability. This variety is commonly utilized in smoothies, protein shakes, tea, coffee, and culinary applications without changing flavor profiles. The lack of added sugar attracts parents looking for healthier choices for kids and adults wanting to lower their daily sugar consumption across different age ranges.

The segment's leadership is further bolstered by increasing awareness about lifestyle-related diseases and nutrition knowledge in India. Healthcare providers and nutritionists often suggest unsweetened soy milk as a dairy substitute appropriate for those with lactose intolerance or cholesterol issues. Food service establishments and cafés likewise favor unsweetened options as a neutral foundation for drinks and recipes. Retail shelves prominently display unsweetened choices, indicating steady demand. As plant-based diets and clean eating become more popular, unsweetened soy milk maintains its status as the top selection for health-conscious consumers in both metropolitan and developing urban areas.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Online/E-Commerce

- Others

Supermarkets and hypermarkets exhibit a clear dominance with a 59.8% share of the total India soy milk market in 2025.

Supermarkets and hypermarkets represent the largest segment owing to their wide product assortment and strong consumer footfall. These retail formats provide dedicated shelves for plant-based beverages, allowing buyers to compare brands, flavors, and packaging sizes in one place. Organized retail chains in metro and tier-one cities are expanding rapidly, improving access to soy milk for urban consumers. Attractive in-store promotions, combo offers, and sampling activities further encourage trial purchases. The availability of refrigeration facilities also ensures proper storage, maintaining product freshness and quality, which builds consumer trust in soy-based dairy alternatives across major cities.

The prevalence of supermarkets and hypermarkets is further reinforced by the increasing desire for contemporary retail experiences among middle-class families. Consumers appreciate the ease of buying groceries, health products, and drinks in one trip, leading to these stores being a popular option. Brand visibility is enhanced in major retail chains, where businesses allocate resources for shelf positioning and point-of-sale promotions. Moreover, private label soy milk items provided by retail stores improve affordability and draw in cost-conscious consumers. With the ongoing increase of organized retail reaching smaller cities, supermarkets and hypermarkets are anticipated to uphold their dominant role in the distribution of soy milk in India.

Regional Insights:

- North India

- South India

- East India

- West India

North India dominates with a market share of 36.5% of the total India soy milk market in 2025.

North India leads the market due to its substantial urban population and increasing awareness about plant-based diets. Major cities like Delhi, Chandigarh, and Jaipur are experiencing a growing demand for lactose-free and dairy-alternative drinks among health-focused consumers. Rising worries regarding lactose intolerance, cholesterol control, and weight management are motivating numerous families to try soy-based beverages. The existence of structured retail networks, grocery stores, and online shopping sites enhances the accessibility and visibility of products. Furthermore, promotional campaigns for vegan and high-protein diets have significantly appealed to younger consumers in urban areas of North India.

The region’s leadership is also influenced by evolving dietary preferences and expanding middle-class income levels. North India has seen a steady rise in gym culture, wellness communities, and fitness-focused lifestyles, all of which contribute to higher adoption of soy milk as a nutritious beverage option. Educational institutions and corporate offices in major cities are also increasing consumption of ready-to-drink (RTD) plant-based beverages. Food service outlets, cafés, and quick-service restaurants are incorporating soy milk into coffee and smoothie menus, further normalizing its usage. For instance, in 2025, the Coffee Bean & Tea Leaf® opened its new flagship café in Janakpuri, Delhi, expanding in India through a partnership with Ekaagra Ostalaritza Pvt. Ltd. The café serves specialty coffee and tea with options like soy, almond, and oat milk, along with vegan and gluten-free menu items.

Market Dynamics:

Growth Drivers:

Why is the India Soy Milk Market Growing?

Urbanization and Changing Lifestyles

Rapid urbanization in India is leading to shifts in lifestyle and dietary habits, contributing to the growth of the soy milk market. This demand is underscored by demographic trends, as according to World Bank data, approximately 36.87% of India’s total population resided in urban areas in 2024. Urban consumers increasingly prioritize convenience, health, and quality in their food choices. Busy routines, dual-income households, and limited access to fresh dairy encourage adoption of packaged, ready-to-consume plant-based beverages. The urban population’s exposure to international food trends, coupled with a growing café and beverage culture, is creating favorable conditions for soy milk consumption as a mainstream alternative.

Rising Awareness about Diabetes and Weight Management

The growing concern about lifestyle diseases, particularly diabetes and obesity, is driving the demand for soy milk. This prevalence is supported by the data provided by the International Diabetes Federation, which stated that India’s adult population with diabetes reached 89.8 Million in 2024. Consumers are actively seeking low-glycemic, low-fat, and cholesterol-free alternatives to traditional dairy. Soy milk, with its plant-based protein content and favorable nutritional profile, is perceived as a healthier option for blood sugar management and weight control. Health advisories, medical recommendations, and dietitian guidance further reinforce the role of soy milk as a functional dietary component, encouraging adoption among health-conscious and medically vulnerable populations.

Growing Health Awareness

The rising consumer awareness about the health advantages of plant-based diets is a major factor bolstering the soy milk market in India, as individuals increasingly prioritize heart health, cholesterol management, and lactose intolerance solutions. Soy milk, valued for its high protein content, low saturated fat, and potential cardiovascular benefits, is becoming a preferred alternative to traditional dairy. Additionally, campaigns and health-focused media coverage are educating the public on plant-based options, strengthening the preference for soy milk among both urban and semi-urban populations. For example, in 2025, PETA India launched its “Choose Kindness in ’26” campaign, featuring billboards in Chandigarh, Guwahati, Kochi, and Pune, emphasizing that each vegan can save up to 200 animals annually while highlighting both health benefits and environmental impacts.

Market Restraints:

What Challenges the India Soy Milk Market is Facing?

Higher Price Points Relative to Conventional Dairy Limiting Mass Adoption

The significant price gap between soy milk and conventional dairy milk remains a fundamental barrier to broader market penetration across India’s price-sensitive consumer segments. Soy milk products typically command a premium of two to three times over regular dairy milk, restricting adoption primarily to higher-income urban consumers and limiting growth potential in semi-urban and rural markets where affordability is the primary purchase determinant.

Deep-Rooted Cultural Preference for Traditional Dairy Products

India’s strong cultural affinity toward conventional dairy consumption, deeply embedded in dietary traditions, religious practices, and culinary heritage, presents a significant challenge for soy milk market expansion. Many consumers perceive dairy milk as nutritionally superior and culturally essential, creating psychological resistance toward switching to plant-based alternatives even when health considerations would favor such a transition.

Regulatory Uncertainty Surrounding Plant-Based Milk Labeling

The evolving regulatory landscape governing plant-based product labeling in India creates compliance challenges and consumer confusion for soy milk manufacturers. Restrictions on using conventional dairy terminology for plant-based products require brands to navigate complex labeling requirements, potentially impacting brand recognition and consumer understanding about product positioning in retail environments.

Competitive Landscape:

The India soy milk market exhibits a moderately fragmented competitive structure characterized by the coexistence of established multinational corporations and emerging domestic brands competing across price tiers and distribution channels. Market participants are strategically differentiating through product innovation, including fortified and flavored variants, clean-label formulations, and sustainable packaging solutions. Competition is intensifying as companies expand their distribution footprints across organized retail, e-commerce, and quick-commerce platforms while investing in brand-building through digital marketing campaigns and influencer collaborations targeting health-conscious millennial and Generation Z consumers.

Recent Developments:

- November 2024: The ICAR–Indian Institute of Soybean Research (Indore) announced plans to collaborate with industries to support startups developing soybean-based products. The institute provided technology guidance, incubation support, and marketing platforms, helping entrepreneurs produce items like tofu, soya milk, and ready-to-eat foods, while addressing challenges in funding and market access.

- September 2024: Oxbow Brands launched its new venture, Vegan Drink Company (VDC), offering plant-based milk alternatives such as Almond, Oats, Millet, Soy, and Coconut. The products, enriched with essential vitamins and free from added sugar, catered to vegan and lactose-intolerant consumers across retail and foodservice channels in India.

India Soy Milk Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Conventional, Organic |

|

Flavor Outlooks Covered |

Plain/Unflavored, Flavored |

|

Types Covered |

Unsweetened, Sweetened |

|

Distribution Channels Covered |

Supermarkets and Hypermarkets, Convenience Stores, Online/E-Commerce, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Soy Milk Market Report

The India soy milk market size was valued at USD 189.30 Million in 2025.

The India soy milk market is expected to grow at a compound annual growth rate of 5.11% from 2026-2034 to reach USD 296.37 Million by 2034.

Conventional dominates the India soy milk market with a share of 88.7% in 2025, supported by established manufacturing processes, competitive pricing, and broad consumer acceptance across income segments.

Key factors driving the India soy milk market include the growing awareness about the environmental impact of dairy, which is encouraging consumers to adopt soy milk as a sustainable alternative. This shift is reinforced by climate change concerns and ethical consumption trends. For example, in 2024, 1.5 Degree launched diverse plant-based dairy products at the India International Hospitality Expo, promoting eco-friendly choices.

Major challenges include higher price points relative to conventional dairy milk limiting mass adoption, deep-rooted cultural preferences for traditional dairy products, regulatory uncertainty surrounding plant-based milk labeling, limited consumer awareness in semi-urban and rural areas, and competition from alternative plant-based milks such as almond and oat milk.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)