India Spectacles Market Size, Share, Trends and Forecast by Product Type, Modality, Distribution Channel, and Region, 2026-2034

India Spectacles Market Size, Share, Trends & Forecast (2026-2034)

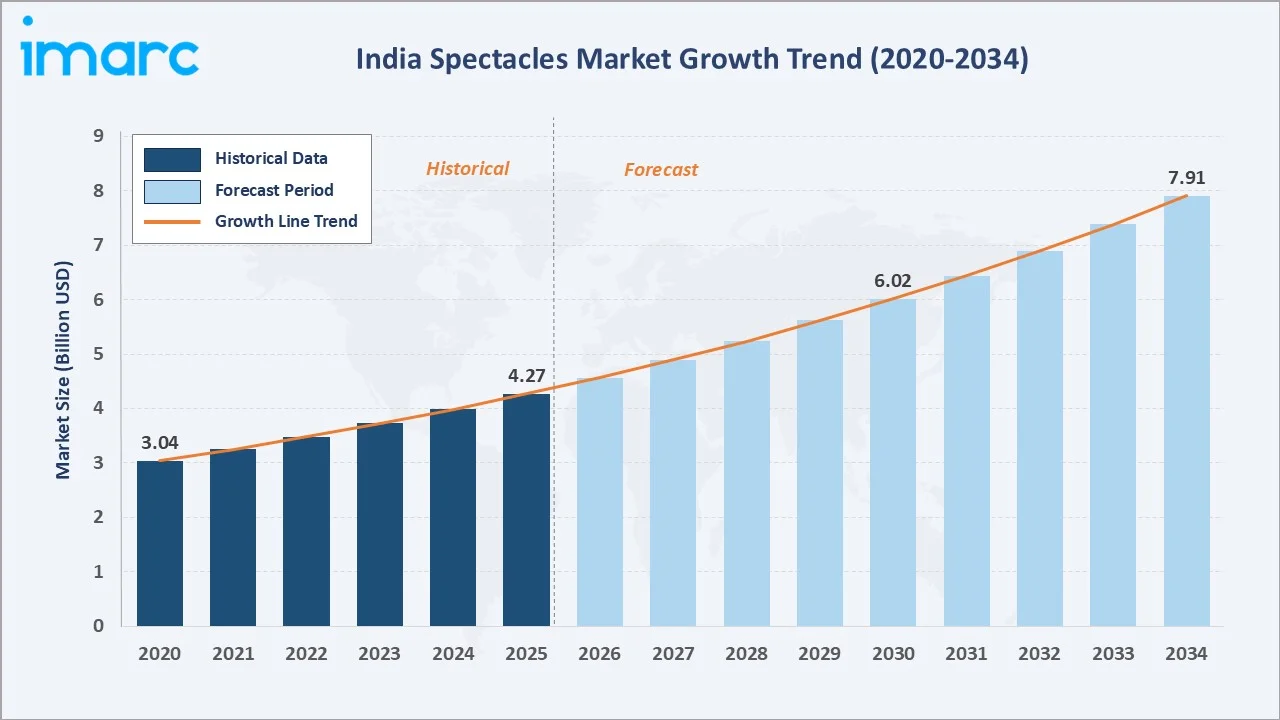

The India spectacles market was valued at USD 4.27 Billion in 2025 and is projected to reach USD 7.91 Billion by 2034, exhibiting a CAGR of 7.08% during 2026-2034. Rising prevalence of refractive errors, expanding organized optical retail, and increasing screen-led digital eye strain across age groups are the primary drivers shaping market growth.

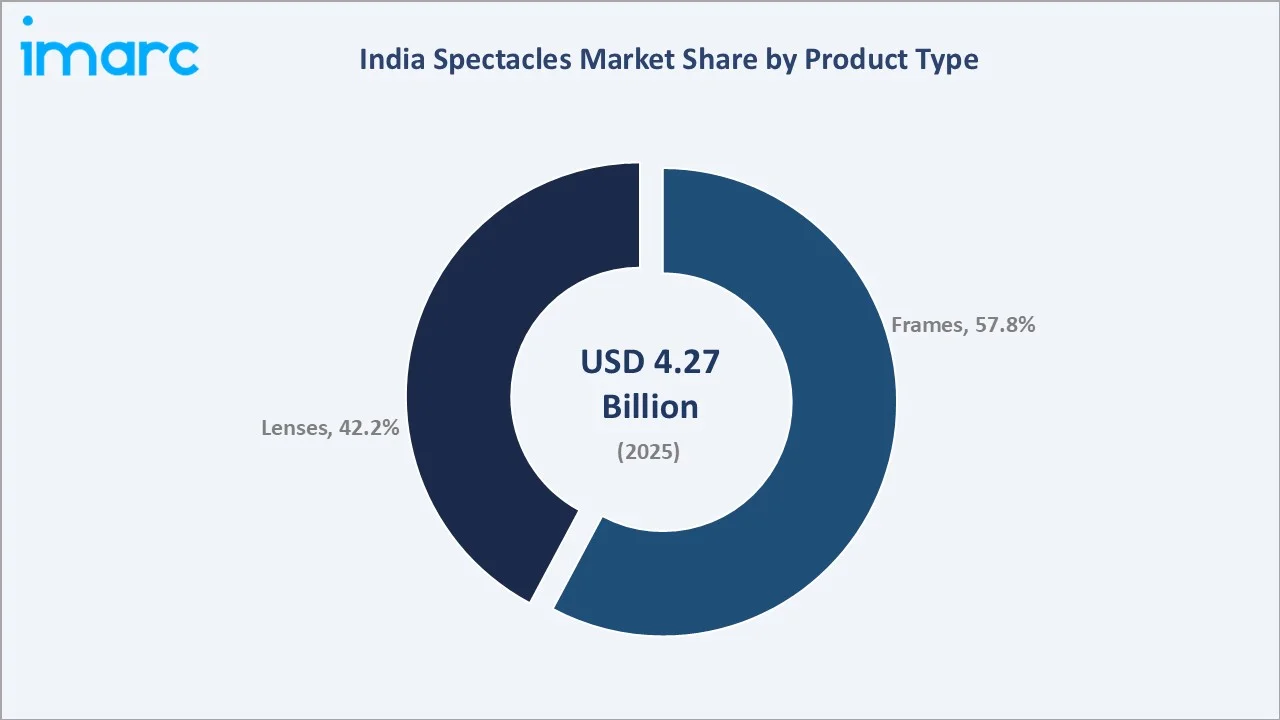

Frames lead the product type segment at 57.8%, prescription dominates the modality segment at 68.4%, and North India commands 30.6% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.27 Billion |

|

Forecast Market Size (2034) |

USD 7.91 Billion |

|

CAGR (2026-2034) |

7.08% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

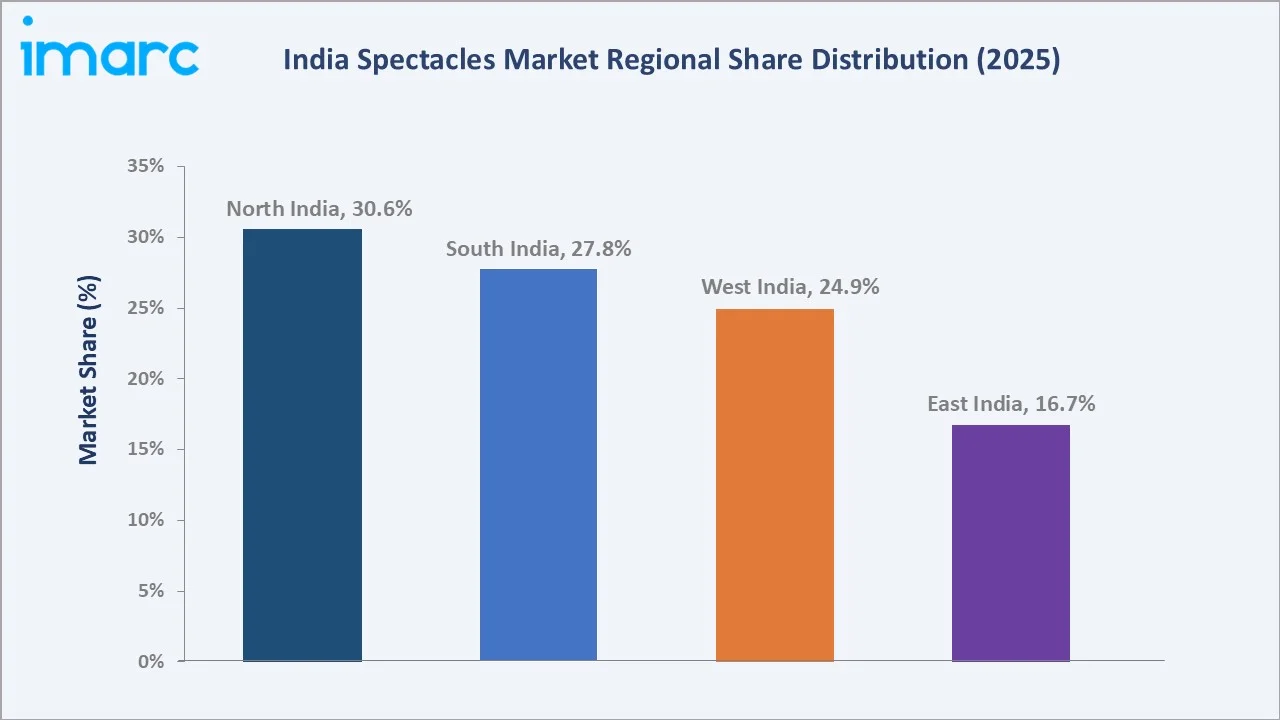

North India (30.6%, 2025) |

|

Second Largest Region |

South India (27.8%, 2025) |

|

Leading Product Type |

Frames (57.8%, 2025) |

|

Leading Modality |

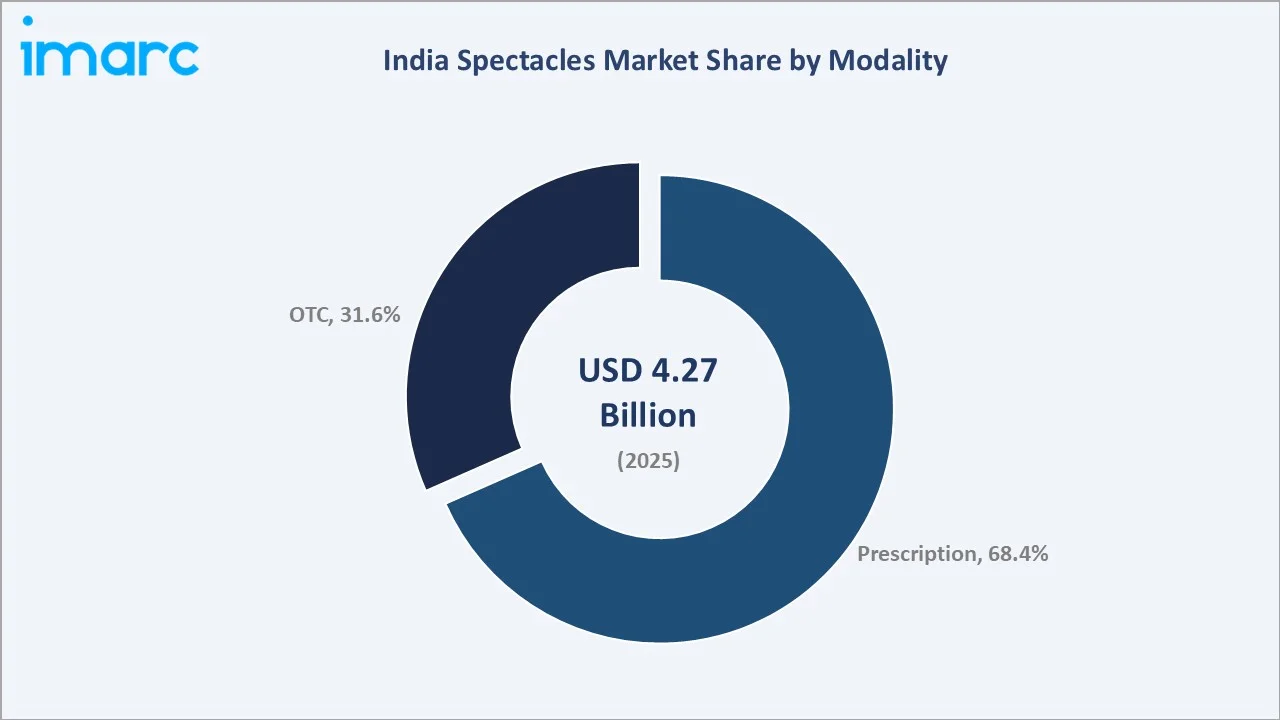

Prescription (68.4%, 2025) |

The India spectacles market expanded from USD 3.04 Billion in 2020 to USD 4.27 Billion in 2025, supported by widening access to eye care, growing retail optical chains, and rising consumer willingness to invest in corrective and fashion eyewear. Anchored at USD 6.02 Billion in 2030, the forecast to USD 7.91 Billion by 2034 is underpinned by increasing incidence of myopia among school-age children, rapid growth of online eyewear platforms, and product premiumization across both frames and lenses.

To get more information on this market, Request Sample

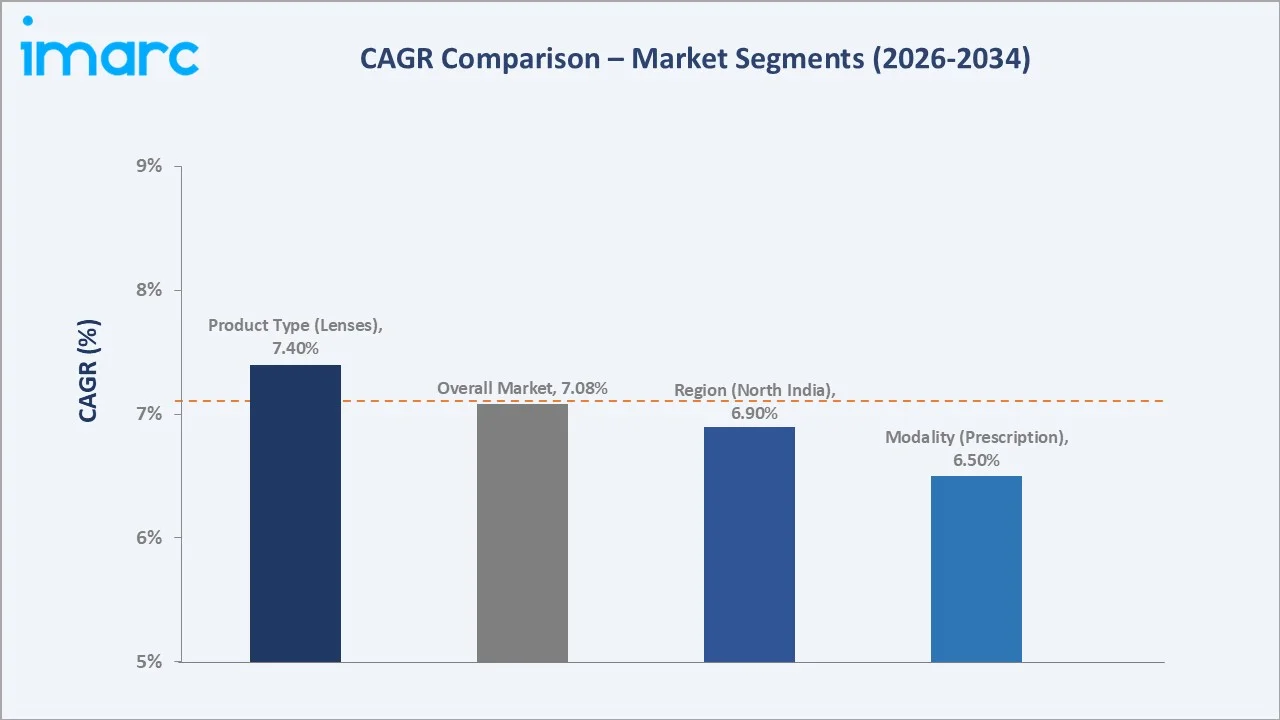

CAGR trajectories across product type and modality segments show prescription and lenses expanding faster than the overall 7.08% market CAGR, driven by aging population demographics, rising presbyopia prevalence, and growing consumer preference for advanced lens technologies that combine vision correction with blue-light protection.

Executive Summary

The India spectacles market is on a robust growth trajectory, rising from USD 3.04 Billion in 2020 to USD 7.91 Billion by 2034. The market has transitioned from predominantly unorganized, independent optical shop formats to a rapidly organizing retail ecosystem led by national chains, franchise operators, and technology-enabled online platforms.

Frames dominate the product type segment at 57.8% in 2025, driven by robust demand for both corrective and fashion frames across consumer segments. Prescription commands 68.4% of modality share, reflecting the large addressable base of vision-impaired consumers seeking professional correction. North India commands 30.6% of regional share, led by high urban concentration, dense retail optical presence, and strong consumer awareness in cities, such as Delhi, Lucknow, and Chandigarh. In April 2026, GKB Opticals launched two new retail stores in Motinagar and Greenpark, in the Delhi-NCR region, signifying further progress in the brand's expansion strategy.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Frames – 57.8% share (2025) |

|

Second Largest Product Type |

Lenses – 42.2% share (2025) |

|

Leading Modality |

Prescription – 68.4% share (2025) |

|

Second Largest Modality |

OTC – 31.6% share (2025) |

|

Leading Region |

North India – 30.6% share (2025) |

|

Second Largest Region |

South India – 27.8% share (2025) |

|

Top Companies |

Titan Company, Lenskart Solutions Limited, EssilorLuxottica, Safilo Group S.P.A. |

Key Analytical Observations Expanding On The Data Above:

- Frames leadership at 57.8% is sustained by strong demand from first-time prescription buyers, school-age children diagnosed with myopia, and fashion-conscious adults seeking regular frame updates. Frames account for the majority of repeat purchase decisions as consumers upgrade styles alongside prescription renewals.

- Lenses at 42.2% are driven by increasing demand for advanced vision correction solutions, including blue-light filtering, anti-reflective, photochromic, and progressive lenses. Rising digital device usage and growing consumer preference for premium lens coatings and customized optical solutions are supporting steady segment growth.

- Prescription dominance at 68.4% reflects the large and growing base of myopia, hyperopia, and astigmatism patients in India who require optical-quality lenses with professional dispensing, driving consistent footfall to licensed optical outlets and increasing average transaction values.

- OTC at 31.6% spans reading glasses and non-prescription fashion eyewear available without a professional consultation, growing in appeal among consumers aged 40 and above managing early presbyopia and among fashion buyers seeking style-led eyewear without clinical involvement.

- North India at 30.6% leads regional share, anchored by Delhi-NCR, Punjab, Haryana, and Uttar Pradesh, supported by dense optical retail presence, high consumer awareness of branded eyewear, and a large working-age population with significant screen time driving vision correction demand.

India Spectacles Market Overview

Spectacles refer to corrective and non-corrective optical devices worn in front of the eyes, consisting of frames and lenses designed to address refractive errors, protect eyes from environmental hazards, and serve aesthetic and fashion functions. The India spectacles market encompasses prescription eyewear, OTC reading and fashion glasses, sports and protective eyewear, and fashion-led lifestyle frames spanning mass-market, mid-range, and premium price tiers.

The Indian ecosystem integrates raw material suppliers, frame and lens manufacturers, wholesale distributors, organized retail chains, independent opticians, online eyewear platforms, ophthalmologists, optometrists, and eye care hospitals. Together they deliver a full spectrum of vision care and eyewear solutions to a diverse consumer base spanning urban, semi-urban, and rural markets. Macroeconomic drivers, including rising healthcare awareness, growing disposable incomes, rapid urbanization, and increasing digital screen time, are collectively expanding the addressable market.

Market Dynamics

To evaluate market opportunities, Request Sample

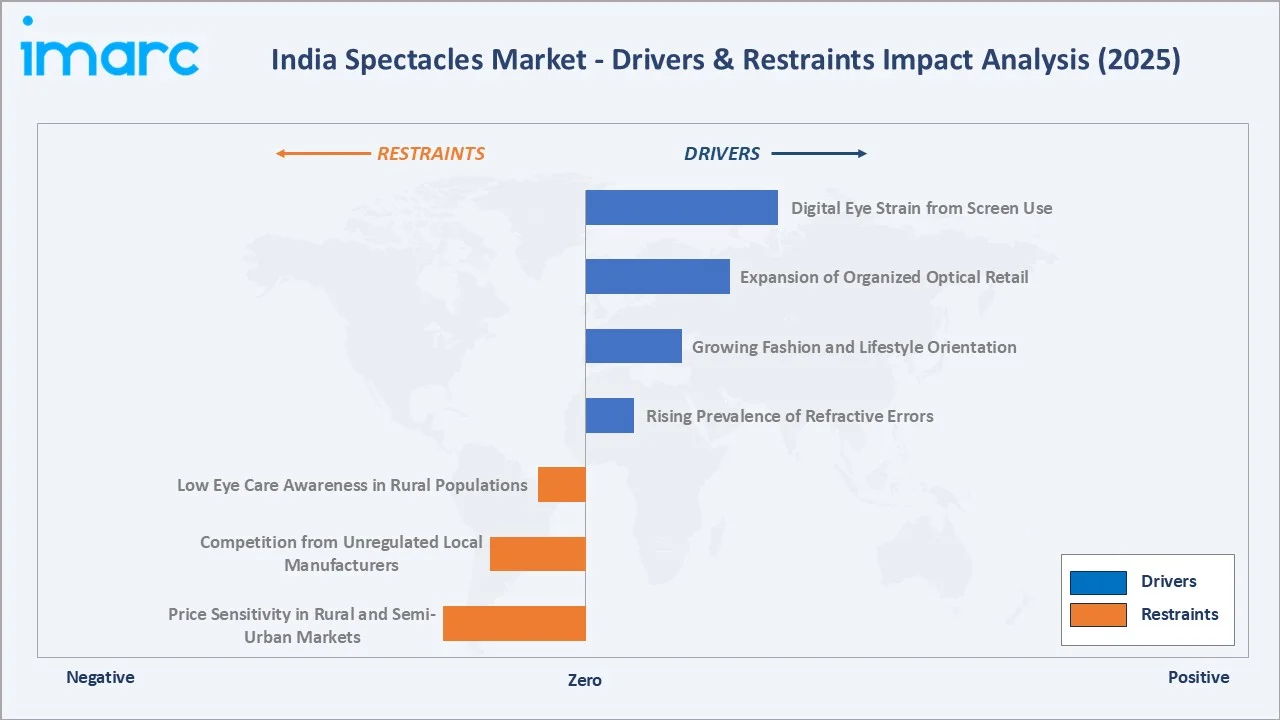

Market Drivers

- Rising Prevalence of Refractive Errors: India carries one of the world's largest burdens of uncorrected refractive error, with myopia growing rapidly among school-age children and presbyopia expanding with an aging population. This structural demographic demand forms the consistent foundation of spectacle sales across corrective categories.

- Growing Fashion and Lifestyle Orientation: Rising consumer awareness of eyewear as a fashion accessory is driving premiumization and frame trade-up cycles, particularly among urban millennials and Gen Z consumers. Multiple frame ownership, driven by seasonal and outfit-linked eyewear preferences, is increasing average units sold per customer.

- Expansion of Organized Optical Retail: Rapid growth of national optical chains, franchise models, and omnichannel retail formats is increasing consumer access to branded eyewear and professional dispensing. The organized segment is expanding coverage across tier-2 and tier-3 cities, unlocking markets previously served only by independent opticians.

- Digital Eye Strain from Screen Use: The widespread adoption of smartphones, computers, and other digital devices for work, education, and entertainment is increasing the incidence of digital eye strain and vision-related discomfort across all age groups. This trend is driving higher demand for prescription eyewear, blue-light filtering lenses, and regular eye examinations, supporting sustained growth in the spectacles market. As per the Comprehensive Modular Survey: Telecom (CMS: T), conducted from January to March 2025, around 85.5% of households in India owned at least one smartphone.

Market Restraints

- Price Sensitivity in Rural and Semi-Urban Markets: A significant proportion of the Indian population outside major metros remains price-sensitive, limiting penetration of premium and branded eyewear. Affordability constraints restrict upgrade cycles and make consumers more susceptible to low-cost unbranded alternatives from unorganized players.

- Competition from Unregulated Local Manufacturers: The presence of a large unorganized sector offering low-cost frames and uncertified lenses continues to undercut organized players on price, particularly in smaller cities. This constrains margin expansion for branded players and limits standardization of optical quality across market tiers.

- Low Eye Care Awareness in Rural Populations: Limited access to qualified optometrists, infrequent vision screening programs, and low awareness of refractive error among rural populations reduce the rate of diagnosis and spectacle uptake in these markets, constraining the full realization of latent demand.

Market Opportunities

- Online Eyewear Retail Expansion: Rapidly growing internet penetration and consumer comfort with online purchasing are driving significant growth in direct-to-consumer eyewear platforms. Online channels offer wider frame selection, home try-on services, and competitive pricing, particularly attractive to younger, digitally native consumers.

- Premiumization and Value-Added Lens Technologies: Growing consumer willingness to invest in anti-reflective, blue-light-blocking, photochromic, and progressive lens technologies is increasing per-unit revenue realization across optical retailers and creating upsell opportunities for lens replacement.

- School Eye Health Programs and Vision Screening Initiatives: Government and NGO-led school vision screening drives are expanding diagnosis rates among children, creating a structured funnel of first-time prescription spectacle buyers who represent long-term loyal customers for optical chains and brands.

Market Challenges

- Contact Lens and Refractive Surgery Substitution: Growing adoption of contact lenses among young urban consumers and increasing affordability and accessibility of laser eye correction surgeries represent partial substitution threats to corrective spectacle demand among specific consumer segments.

- Supply Chain Complexity and Import Dependence: Significant dependence on imported optical-grade lens blanks, specialized coatings, and premium frame materials from China, Italy, and Japan exposes manufacturers and retailers to currency fluctuation, tariff changes, and supply chain disruptions that can affect product availability and pricing.

Emerging Market Trends

1. Rapid Growth of Online Eyewear Retail Platforms

Online eyewear retail is establishing a strong foothold in the India spectacles market, driven by digital-first consumer behavior, wide frame selection, home try-on services, and competitive pricing models that attract millennial and Gen Z buyers. Players with proprietary online fitting technology and strong social media presence are acquiring customers at scale beyond the reach of physical stores.

2. Blue-Light Blocking and Functional Lens Mainstreaming

Functional lens technologies are moving from premium add-ons to mainstream offerings across organized optical chains. Blue-light-blocking coatings, photochromic lenses, and high-definition progressive designs are being routinely recommended at point-of-dispensing, increasing average lens revenue per transaction.

3. Fashion Eyewear and Multiple Frame Ownership

Fashion-forward frame design is accelerating multiple ownership among urban consumers who treat eyewear as an accessory category rather than purely a medical device. International designer collaborations, India-specific capsule collections, and influencer-driven eyewear styling content are normalizing frame change frequency beyond the traditional prescription renewal trigger.

4. Expansion of Organized Retail into Tier-2 and Tier-3 Cities

National optical chains and franchise operators are rapidly expanding their footprint beyond metros into tier-2 and tier-3 cities, bringing standardized clinical services, branded product assortments, and professional dispensing to markets previously dominated by independent opticians. This structural expansion is formalizing demand, improving average transaction values, and reducing dependence on unbranded low-cost alternatives.

5. AI-Powered Vision Testing and Digital Refraction Tools

Adoption of AI-powered auto-refraction systems, remote vision screening tools, and digital optometry platforms is improving diagnostic accuracy and reducing consultation time at optical outlets. These technologies are enabling chains to deliver clinical-grade eye testing in smaller store formats without full-time optometrist presence, supporting faster geographic expansion and higher patient throughput per store.

Industry Value Chain Analysis

The India spectacles value chain spans six stages from raw material supply through end consumer use and aftercare. Manufacturing, professional dispensing, and digital retail command the highest value-add, while clinical credentialing and customer relationship management increasingly determine sustainable competitive position.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Acetate, metal alloy, polycarbonate, and optical-grade CR-39 resin suppliers, titanium wire providers, and anti-reflective coating chemical manufacturers |

|

Component Manufacturing |

Hinge and screw component makers, lens blank producers, coating equipment suppliers, and optical machinery manufacturers supporting frame and lens production |

|

Frame & Lens Production |

Frame manufacturers, optical lens grinders and fitters, anti-reflective and photochromic coating facilities, and precision grinding operations |

|

Wholesale Distribution |

National and regional optical distributors, brand wholesale arms, import-export agencies, and third-party logistics providers serving the optical trade |

|

Retail & Dispensing |

Optical retail chains, independent opticians, department store eyewear sections, online eyewear retailers, and hospital-linked optical outlets |

|

End Consumer Use |

Vision correction patients, fashion and lifestyle eyewear buyers, sports and safety eyewear users, and repeat prescription renewal customers |

Vertically integrated players, particularly those owning proprietary frame manufacturing, in-house lens surfacing, and direct retail relationships, are positioned to capture greater margin than operators reliant on third-party frame sourcing and external lens suppliers. Online players that own the customer relationship and offer repeat lens replacement subscriptions are emerging as a structurally distinct value capture model.

Technology Landscape in the India Spectacles Industry

Advanced Lens Manufacturing Technologies

Modern optical lens production leverages computer numerical control (CNC) surfacing, free-form digital lens design, and precision anti-reflective coating deposition technologies to deliver high-definition vision correction with minimal aberration. These manufacturing advances enable individualized progressive and occupational lens designs tailored to each wearer's visual requirements and frame geometry.

Smart Eyewear and Augmented Reality (AR) Integration

Early-stage integration of smart glasses with hearing aid functions, activity tracking sensors, and AR overlays is beginning to expand the functional scope of the spectacles category. While mainstream adoption in India remains a longer-horizon development, premium segments and enterprise applications represent initial growth vectors for technology-embedded eyewear platforms.

Digital Inventory and Omnichannel Retail Systems

Cloud-based inventory management, integrated prescription record systems, and omnichannel point-of-sale platforms are enabling optical chains to synchronize clinical data, frame stock, and customer purchase history across physical and online touchpoints. These systems reduce stockouts, improve cross-sell and upsell effectiveness, and support loyalty and recall management programs.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Frames |

57.8% |

2025 |

|

Modality |

Prescription |

68.4% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North India |

30.6% |

2025 |

By Product Type

Frames command a 57.8% majority share in 2025, driven by robust demand across corrective, protective, and fashion eyewear categories. The segment benefits from consistent replacement cycles tied to prescription updates, lens changes, and evolving frame style preferences among Indian consumers across urban, semi-urban, and rural markets.

To access detailed market analysis, Request Sample

Lenses at 42.2% in 2025 represent the technically complex value-adding component of the spectacles category. The segment is increasingly defined by premium coatings and specialty designs including anti-reflective, blue-light-blocking, photochromic, and progressive formats, all of which command higher per-unit revenues and are growing faster than single-vision clear lens volumes.

By Modality

Prescription dominates modality with 68.4% share in 2025, reflecting the large base of diagnosed refractive error patients in India who require clinical dispensing, optometrist sign-off, and lens specification tailored to individual prescriptions. The segment benefits from predictable repeat purchase cycles driven by annual or biannual prescription renewals, patient recall programs run by organized chains, and the medically essential nature of the purchase.

OTC at 31.6% encompasses reading glasses available without prescription, non-corrective fashion frames, tinted and UV-protection sunglasses, and screen-protection glasses marketed directly to consumers through pharmacies, fashion retailers, and online platforms. The segment is growing as aging demographics expand the presbyopia-affected population seeking convenient self-directed reading correction, and as fashion eyewear becomes more accessible through mainstream retail channels.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

30.6% |

High urban density, strong eyewear retail penetration, large working-age population, and established optical chain presence across major cities |

|

South India |

27.8% |

Rising awareness of vision care, growing organized retail penetration, expanding digital eye strain-related demand, and strong healthcare infrastructure |

|

West India |

24.9% |

High disposable incomes, fashion-forward consumer base, mature organized retail presence, and strong brand consciousness in metro markets |

|

East India |

16.7% |

Growing urban population, expanding healthcare access, rising awareness of vision correction, and increasing retail optical outlet footprint |

North India at 30.6% in 2025 leads the regional landscape, anchored by Delhi-NCR, Punjab, Haryana, and Uttar Pradesh. Dense urban population, high concentration of organized optical retail chains, and strong consumer awareness of branded and fashion eyewear support sustained regional leadership across both prescription and OTC categories.

South India at 27.8% is the second largest region. Rapid expansion of organized optical retail in Bengaluru, Hyderabad, Chennai, and Kochi, combined with a large IT-sector workforce experiencing high screen time and digital eye strain, is accelerating vision correction demand and lens upgrade cycles through 2034.

Competitive Landscape

The India spectacles market is moderately fragmented, with established organized retail chains, international frame and lens brands, and rapidly scaling online platforms competing across premium, mid-market, and value segments. Brand strength, clinical service quality, retail footprint, and technology integration form the key competitive moats across the organized segment.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Titan Company |

Fastrack, Titan Eye+ |

Leader |

Expanding organized optical retail network and integrated eyewear ecosystem |

|

Lenskart Solutions Limited |

Lenskart, John Jacobs, Owndays |

Leader |

Technology-driven online-to-offline eyewear retail with AI-powered fit tools |

|

EssilorLuxottica |

Ray-Ban, Oakley |

Leader |

Global leadership in prescription lens technology and branded eyewear retail |

|

Safilo Group S.P.A. |

Safilo, Carrera |

Challenger |

Premium and fashion-forward international frame portfolio for mid-to-premium segments |

Key players include Titan Company, Lenskart Solutions Limited, EssilorLuxottica, and Safilo Group S.P.A., among others.

Key Company Profiles

Titan Company

Titan Company is one of India’s leading lifestyle and consumer products companies. Its eyewear division operates through Titan Eye+, one of India’s largest organized optical retail chains, and the Fastrack sub-brand targeting the youth eyewear segment. The company offers a comprehensive range of prescription eyewear, fashion frames, contact lenses, and eye care services through an extensive network of stores across India.

- Product Portfolio: Titan Eye+ offers prescription frames and lenses across fashion, classic, and sport categories, including anti-reflective, blue-light-blocking, and photochromic lens options. The Fastrack sub-brand serves youth and fashion eyewear with trend-forward designs at accessible price points.

- Recent Developments: In November 2025, Titan Eye+ initiated a campaign urging parents throughout India to utilize a star for assessing their child's eyesight. The initiative creatively addresses the unnoticed epidemic affecting over thirty million children with undiagnosed vision problems, which interferes with their early development.

- Strategic Focus: Expanding organized optical retail across under-penetrated markets and integrating technology-enabled clinical services.

Lenskart Solutions Limited

Lenskart Solutions Limited is India’s largest online and omnichannel eyewear retailer, headquartered in Gurugram, Haryana. The company pioneered the direct-to-consumer online eyewear model in India and has since built an extensive omnichannel presence across the country.

- Product Portfolio: Prescription eyeglasses, sunglasses, and contact lenses under Lenskart, John Jacobs, and Owndays brands across premium, affordable-premium, and economy price points. The company offers virtual try-on and AI-powered frame recommendation tools across its digital platforms.

- Recent Developments: The company has been expanding its store network, investing in proprietary lens manufacturing, and growing international operations across Southeast Asia and the Middle East.

- Strategic Focus: Scaling omnichannel retail through technology differentiation, building vertically integrated manufacturing to improve lens quality and margins, and expanding internationally using the India omnichannel model.

EssilorLuxottica

EssilorLuxottica is a Franco-Italian multinational and among the world’s leading eyewear companies. The company operates across lens manufacturing, branded frame design, and optical retail, serving markets in several countries, including India.

- Product Portfolio: Ray-Ban and Oakley frames distributed through licensed optical retailers in India.

- Recent Developments: The company has been growing its India distribution partnerships for both lenses and frames, expanding Ray-Ban retail presence across organized optical chains, and growing the smart eyewear category through the Ray-Ban Meta glasses platform.

- Strategic Focus: Deepening premium lens technology penetration in Indian optical retail, growing branded frame distribution across organized and e-commerce channels, and driving premiumization through global lens innovation leadership.

Market Concentration Analysis

The India spectacles market is moderately fragmented, with the organized segment led by Titan Company, Lenskart Solutions Limited, and EssilorLuxottica, with international challengers such as Safilo Group S.P.A. competing via distributor-led channels, while a large and diverse unorganized sector of independent opticians, regional frame wholesalers, and local lens grinders continues to serve the mass market across smaller cities and rural areas.

Barriers to entry in the organized segment include significant retail capex requirements, the need for registered optometry professionals in each outlet, established supplier relationships for branded frame and lens assortments, and strong brand-building investments to attract consumers away from their trusted neighborhood opticians. These factors favor well-capitalized incumbents with national brand recognition and proven retail operating models.

Consolidation is ongoing through organic expansion of organized chains into tier-2 markets, franchise model proliferation, and selective acquisitions as larger players look to acquire established store networks, loyal customer bases, and proprietary optical lab capabilities. The online segment continues to grow faster than physical retail, gradually shifting market concentration toward technology-enabled omnichannel operators over the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Prescription is expanding the fastest among within the modality segment, driven by consumer premiumization in organized retail contexts and growing optometrist recommendation rates for functional lens upgrades. Increasing awareness of preventive eye care and rising demand for premium lens features, such as blue-light filtering, anti-glare coatings, and progressive designs, are further accelerating the growth of the prescription segment.

Emerging Markets

East India at 16.7% represents significant untapped opportunity for organized optical retail expansion. Tier-2 and tier-3 cities across all regions represent a large and underserved addressable market currently dominated by independent opticians offering limited brand assortment and clinical service standardization, creating strong franchise and chain expansion opportunities.

Venture & Investment Trends

Investment is concentrated in technology-enabled omnichannel eyewear platforms, AI-driven clinical tools for automated refraction and frame recommendation, and D2C online eyewear brands with proprietary manufacturing. Capital is also flowing into vision screening technology startups and optical lab automation providers that improve dispensing speed and lens quality.

Future Market Outlook (2026-2034)

The India spectacles market is forecast to expand from USD 4.27 Billion in 2025 to USD 7.91 Billion by 2034 at a CAGR of 7.08%, adding roughly USD 3.64 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: continued rise in myopia and age-related presbyopia prevalence across the population; rapid formalization of optical retail through organized chains and online platforms replacing unorganized players; sustained premiumization of lens and frame categories driven by consumer awareness and optometrist recommendation; and integration of AI and digital technology into clinical service delivery and retail operations.

By 2034, the India spectacles market is expected to be defined by a structurally larger organized segment, significantly higher average transaction values driven by premium lens adoption, and a more balanced distribution between physical and online retail. Smart eyewear and AR-integrated devices will begin gaining initial traction in the premium consumer segment, while school-linked vision correction programs and government eye health initiatives will continue to expand the diagnosed patient base across rural and semi-urban markets.

Research Methodology

Primary Research

Primary research included structured interviews with optical retail chain executives, independent opticians, ophthalmologists, optometrists, frame and lens distributors, optical lab operators, and industry association representatives. Interviews validated market sizing estimates, product mix trends, regional demand patterns, and competitive dynamics across organized and unorganized segments.

Secondary Research

Secondary sources included Ministry of Health and Family Welfare publications, All India Ophthalmological Society data, annual reports and investor presentations from listed optical retail and consumer product companies, trade association publications from the Optical Retailers Association, and import-export data on optical goods from the Directorate General of Commercial Intelligence and Statistics.

Forecasting Models

Market forecasts used top-down and bottom-up models combining diagnosed refractive error patient counts, average spend per prescription, lens replacement frequency rates, retail channel mix evolution, and premium product adoption curves. Scenario analysis addressed organized versus unorganized segment share shift velocity, online penetration pace, and macroeconomic demand variability.

India Spectacles Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Frames, Lenses |

| Modalities Covered | Prescription, OTC |

| Distribution Channels Covered | Retail Stores, Online Stores, Ophthalmic Clinics |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Titan Company, Lenskart Solutions Limited, EssilorLuxottica, Safilo Group S.P.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India spectacles market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India spectacles market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India spectacles industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Spectacles Market Report

The India spectacles market was valued at USD 4.27 Billion in 2025, driven by rising refractive error prevalence, expanding organized optical retail, and growing consumer demand for fashion and functional eyewear.

The market is projected to grow at 7.08% CAGR from 2026-2034, reaching USD 7.91 Billion, supported by premiumization in lens and frame categories and rapid growth of organized and online retail channels.

Frames dominate with 57.8% share in 2025, driven by strong demand across corrective, fashion, and lifestyle eyewear categories with consistent replacement cycles.

Prescription leads at 68.4% in 2025, fueled by a large base of diagnosed refractive error patients and professional dispensing ecosystems.

North India commands 30.6% in 2025, led by dense urban population, strong organized optical retail presence, and high consumer awareness of branded eyewear across Delhi-NCR and other major cities.

Leading players include Titan Company, Lenskart Solutions Limited, EssilorLuxottica, and Safilo Group S.P.A., among others.

Rising screen time across smartphones, tablets, and computers is increasing demand for blue-light-blocking and functional lenses, accelerating prescription renewals among working-age adults and driving premium lens upgrade adoption.

Online eyewear retail is growing rapidly, driven by digital-native consumers, virtual try-on technology, wide selection, and competitive pricing. Platforms are expanding through AI-powered frame recommendation and D2C lens replacement subscription services.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)