India Spices Market Size, Share, Trends and Forecast by Product Type, Application, Form, and Region, 2026-2034

India Spices Market Size, Share, Trends & Forecast (2026-2034)

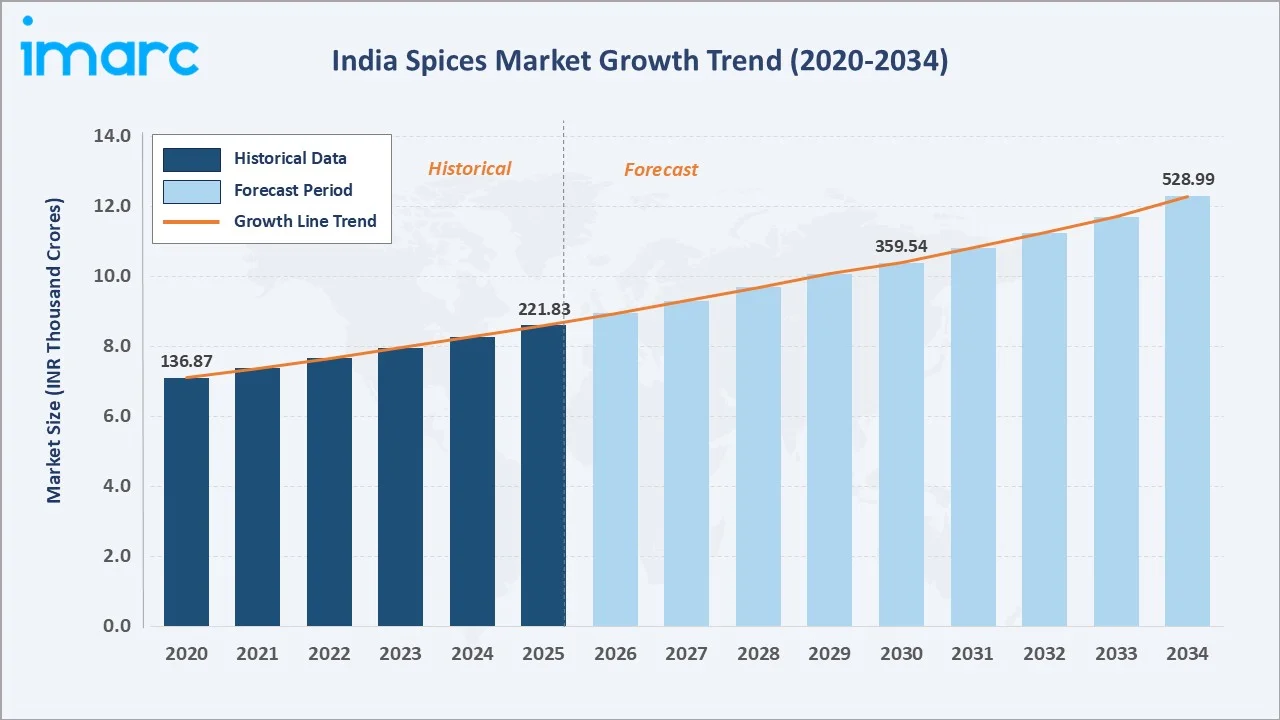

India spices market size was valued at INR 221.83 Thousand Crores in 2025 and is projected to reach INR 528.99 Thousand Crores by 2034, exhibiting a CAGR of 10.14% during 2026-2034. India, the world's largest producer, consumer, and exporter of spices, accounts for more than 70% of global spice exports, growing over 75 varieties across diverse agro-climatic zones.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 221.83 Thousand Crores |

|

Forecast Market Size (2034) |

INR 528.99 Thousand Crores |

|

CAGR (2026-2034) |

10.14% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

North India – 30.0% |

|

Fastest Growing Region |

West and Central India |

India's spice market growth is anchored by deeply rooted culinary traditions, rising demand for organic and clean-label products, rapid expansion of the food processing industry, and the transformational growth of e-commerce and quick-commerce distribution channels.

To get more information on this market, Request Sample

India's spice market continues to expand steadily, supported by rising urbanization, changing consumer preferences, and increased demand for convenience foods. Growth is also fueled by strong export potential, government support, and the increasing global popularity of Indian cuisine.

Executive Summary

As the world's largest producer, consumer, and exporter of spices, cultivating approximately 75 of the 109 ISO-listed varieties, India commands an unparalleled position in global spice supply chains. India spices market, valued at INR 221.83 Thousand Crores in 2025, is forecast to reach INR 528.99 Thousand Crores by 2034, expanding at a CAGR of 10.14%.

Pure spices dominate with a 63% product type share, driven by household procurement of essential cooking spices, turmeric, red chilli, coriander, cumin, and pepper, across traditional kirana retail and modern organized trade channels. Blended spices and ready-to-cook masala formats are growing rapidly, capturing convenience-seeking urban consumers.

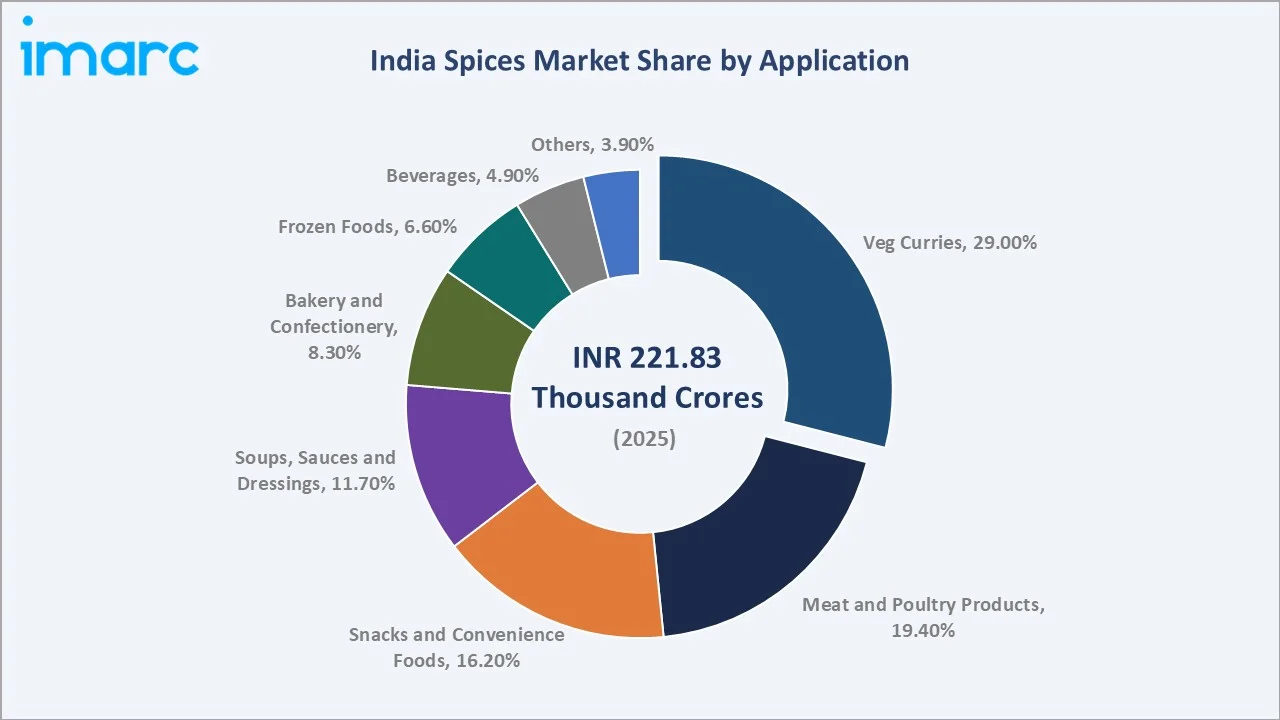

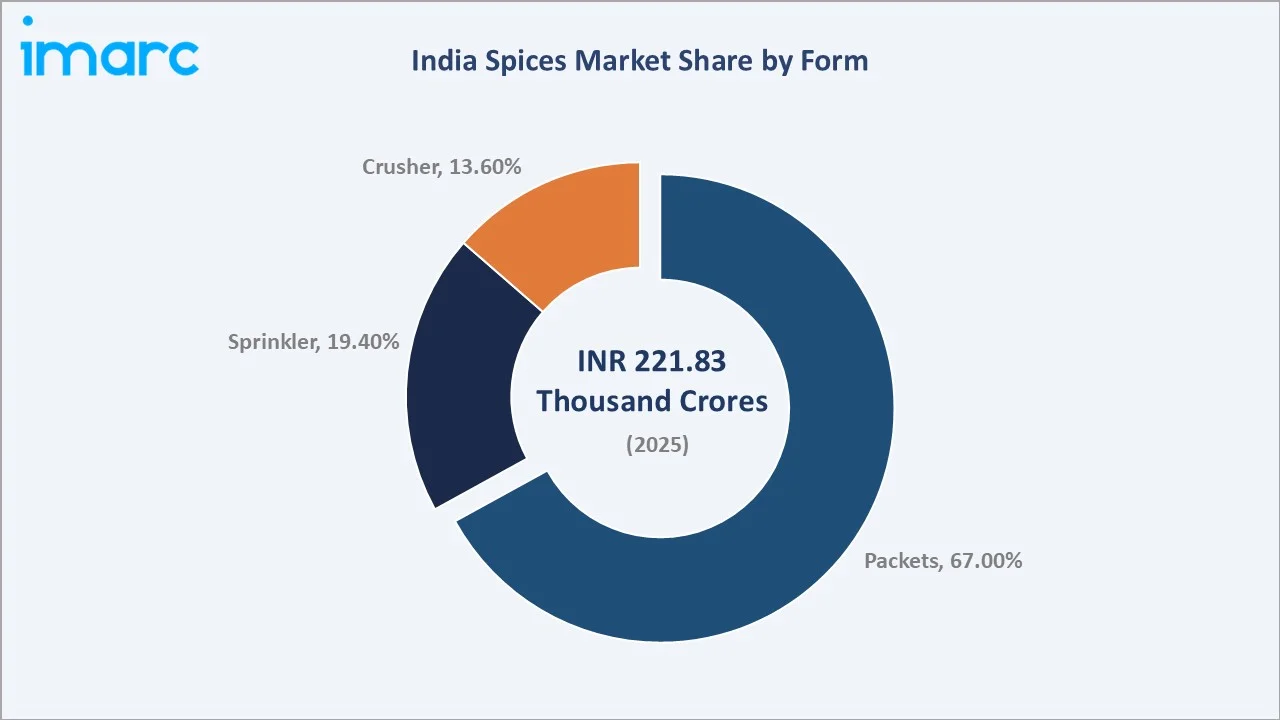

Packets represent the dominant form at 67.0%, reflecting consumers' shift away from loose, unbranded spices toward hygienic, traceable, packaged formats with standardized quality. Veg curries lead application demand at 29.0%, consistent with India's predominantly vegetarian cooking culture across diverse regional cuisines.

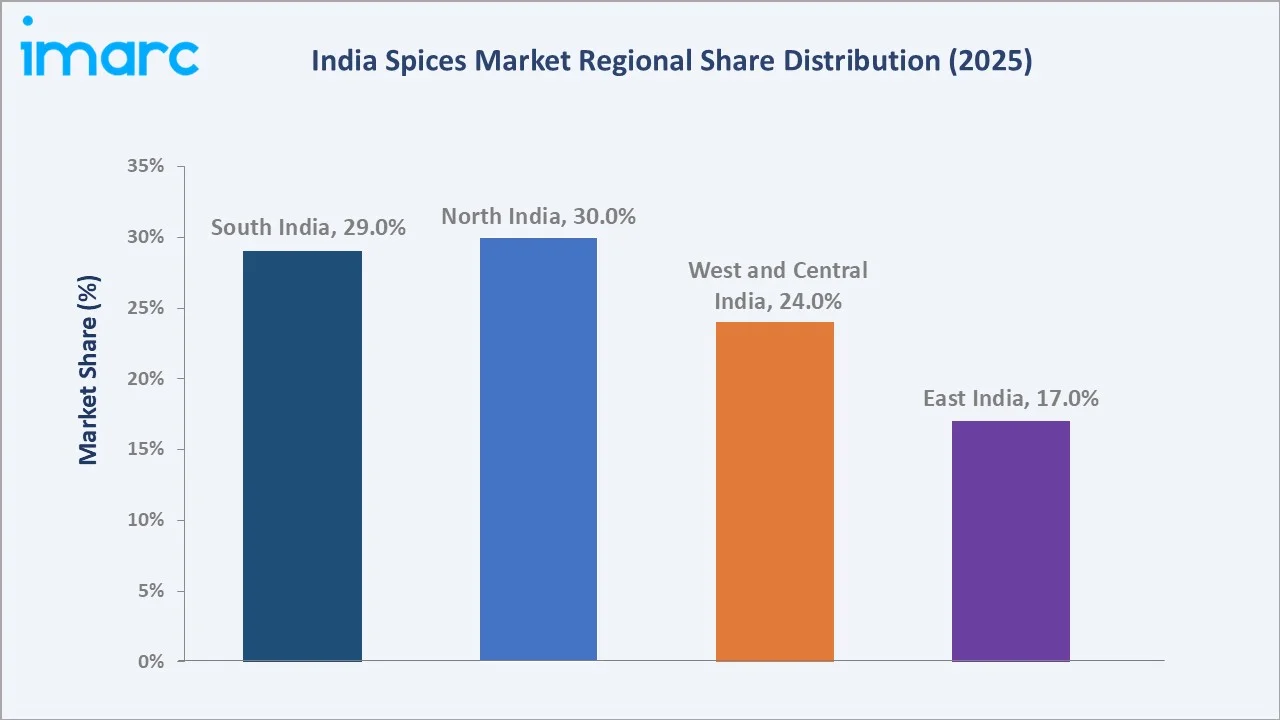

North India leads regional markets at 30.0%, driven by high per-capita spice consumption and the spice-intensive culinary traditions of Punjab, Rajasthan, and Uttar Pradesh. South India follows at 29.0%, supported by year-round cultivation of premium spices, including cardamom, black pepper, and turmeric, across Kerala, Tamil Nadu, and Karnataka.

Key Market Insights

|

Insight |

Data |

|

Top Application Segment |

Veg Curries - 29.0% share (2025) |

|

Leading Form Segment |

Packets - 67.0% share (2025) |

|

Dominant Region |

North India - 30.0% share (2025) |

|

Fastest Growing Channel |

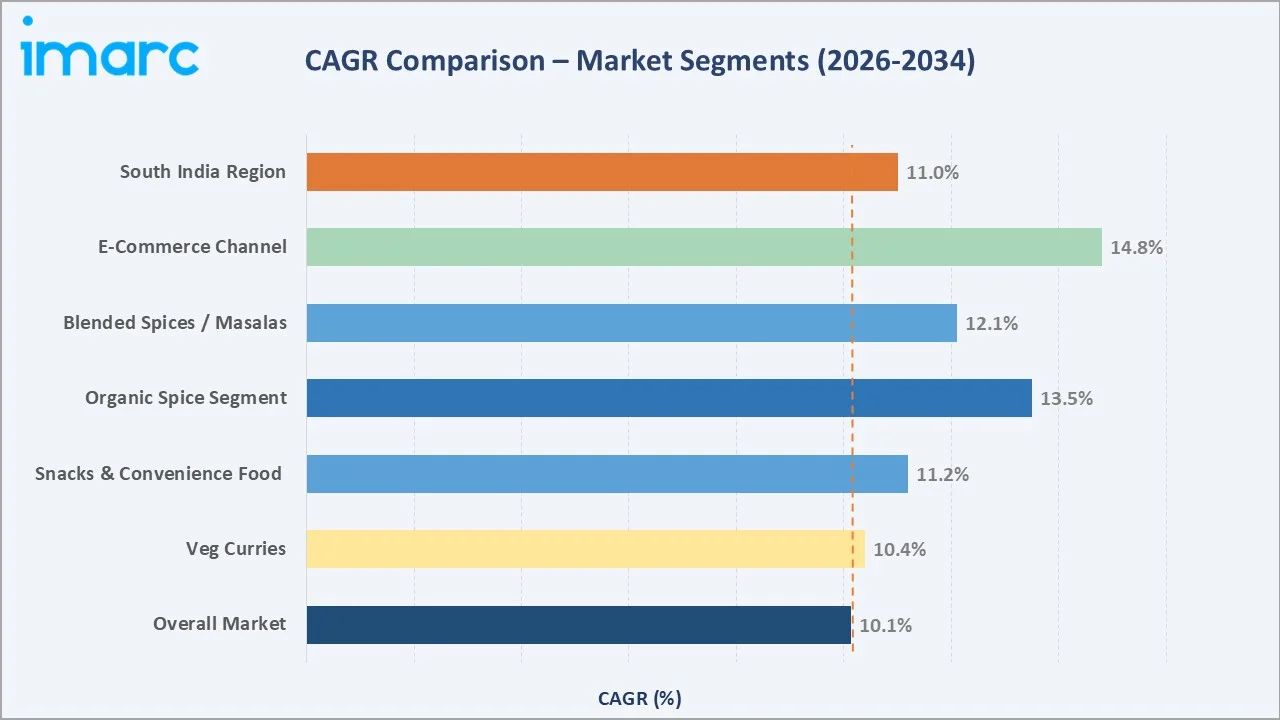

E-Commerce/Quick Commerce – CAGR ~14.8% (2026-2034) |

|

Fastest Growing Segment |

Organic & Clean-Label Spices – CAGR ~13.5% (2026-2034) |

|

India's Global Export Position |

World's largest spice exporter; >70% of global exports |

|

Key Companies |

Everest Foods, MDH, Aashirvaad (ITC), Catch Foods, Badshah, MTR (Orkla), Patanjali |

Key Analytical Observations:

- Veg Curries lead application demand at 29.0% (2025), driven by India's predominantly vegetarian population and the diverse, spice-intensive regional vegetable cuisines across states.

- Packets dominate the form segment at 67.0% (2025), as consumers shift from loose, unbranded spices to hygienic, tamper-proof packaged formats offering standardized quality, extended shelf life, and convenient portion control.

- North India leads regionally at 30.0% (2025), driven by the region’s strong culinary culture, high household consumption of spice blends, and rising demand from food processing, snacks, ready-to-cook meals, and HoReCa sectors.

- E-commerce is transforming retail channels, with ZOFF Foods reporting 75% of revenues from online retail with 65% from quick-commerce channels. It reflects a structural shift toward digital purchasing, particularly among urban millennials and working professionals.

India Spices Market Overview

India's spice industry is built on millennia of agricultural tradition and culinary heritage, making it the world's pre-eminent spice nation, producing approximately one-fifth of the world's total spice output across approximately 75 of the 109 varieties listed by the International Standards Organization. The country's diverse agro-climatic zones enable the cultivation of everything from the warm-weather crops of Gujarat and Rajasthan to the tropical spices of Kerala and the chilli-growing belts of Andhra Pradesh and Madhya Pradesh.

India spices market ecosystem spans a complex value chain connecting millions of smallholder farmers, large corporate processing units, branded FMCG companies, traditional wholesale mandis, modern organized retail, and rapidly growing digital commerce platforms. The market serves multiple demand segments: households consuming spices for daily cooking, the food processing industry using bulk spice ingredients in packaged foods, and the pharmaceutical and nutraceutical industries leveraging spices' documented medicinal properties.

India spices market outlook is reinforced by powerful structural tailwinds. Urbanization and rising disposable incomes are driving premiumization toward branded, organic, and specialty spice products. The food processing sector in India is expected to achieve a growth rate of 11-13% in 2025-26 (FY26) and FY27, up from 10% in FY25, and is generating sustained institutional spice demand.

Market Dynamics

To evaluate market opportunities, Request Sample

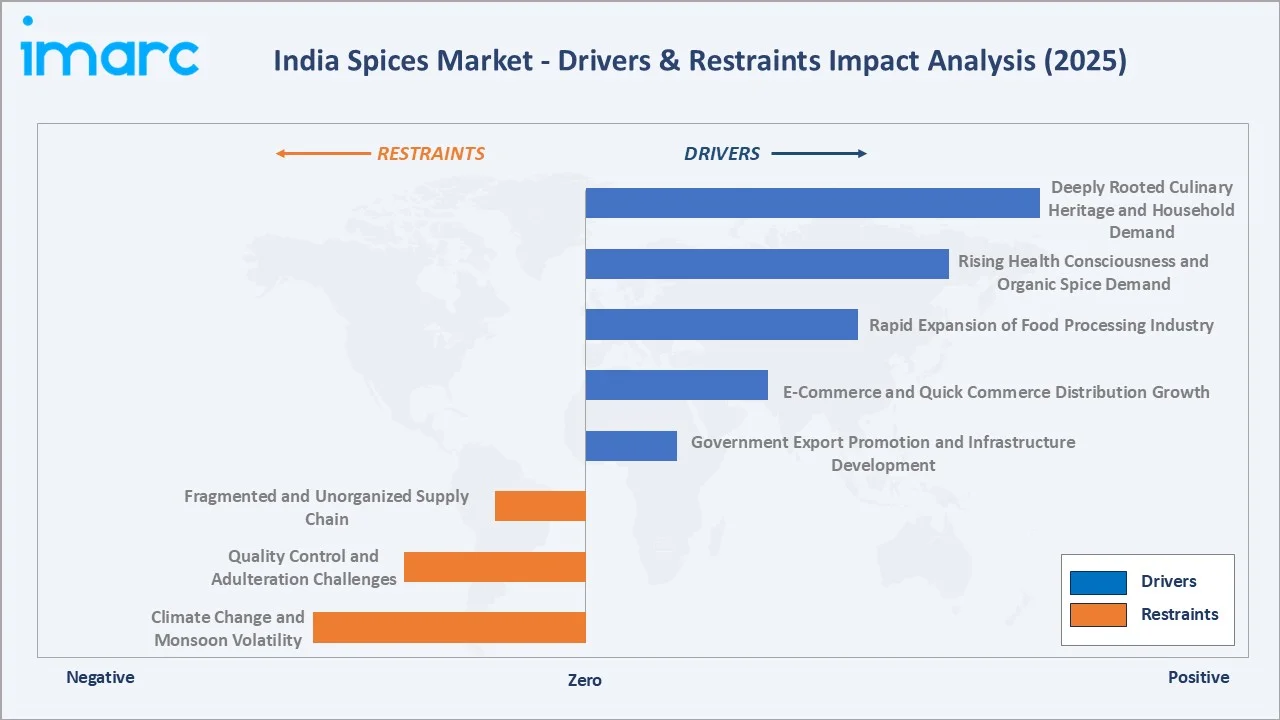

Market Drivers

- Deeply Rooted Culinary Heritage and Household Demand: Spices are non-discretionary household essentials across India's 300+ million households. The country's diverse regional cuisines, from the spice-rich curries of the South to the aromatic Mughal-influenced dishes of the North, require a consistent supply of multiple spice varieties.

- Rising Health Consciousness and Organic Spice Demand: The well-documented medicinal properties of Indian spices are driving demand for premium, additive-free spice products. An ASSOCHAM survey reported 95% growth in urban organic produce purchases, with 62% of metropolitan consumers buying organic products, including spices.

- Rapid Expansion of Food Processing Industry: As of February 28, 2025, the Ministry of Food Processing Industries (MoFPI) approved 1,608 projects, including 41 Mega Food Parks, 394 Cold Chain projects, 75 Agro-processing Clusters, and 536 Food Processing Units, under the relevant components of PMKSY across the country.

- E-Commerce and Quick Commerce Distribution Growth: Digital retail is fundamentally reshaping spice distribution. India's e-commerce industry, valued at Rs. 10,82,875 crore (USD 125 billion) in 2024, is expected to reach Rs. 29,88,735 crore (USD 345 billion) by 2030, representing a compound annual growth rate (CAGR) of 15%.

- Government Export Promotion and Infrastructure Development: The Spices Board of India's SPICED scheme (INR 422.30 Crore outlay through FY 2025-26) supports export promotion, quality upgradation, and processing infrastructure.

Market Restraints

- Climate Change and Monsoon Volatility: Spice cultivation is highly sensitive to rainfall patterns and temperature extremes. Erratic monsoons, unseasonal frosts, and extended droughts can devastate crop yields, directly impact supply availability, and cause sharp price spikes.

- Quality Control and Adulteration Challenges: High-profile food safety incidents, including pesticide residue concerns in exported spice products, have prompted tighter regulatory scrutiny by the FSSAI and international food safety authorities, increasing compliance burden for manufacturers.

- Fragmented and Unorganized Supply Chain: Despite organized sector growth, approximately 60% of India spices market remains unorganized, with numerous small traders, regional brands, and loose-spice vendors.

Market Opportunities

- Premium Organic and GI-Tagged Spice Development: Geographical Indication (GI)-tagged spices such as Byadgi chilli and Coorg cardamom, command significant premium pricing. In June 2025, ITC completed its INR 472.50 Crore acquisition of Sresta Natural Bioproducts (24 Mantra Organic), signaling the major growth potential of the organic spice segment.

- Ready-to-Cook Spice Blend Innovation: In June 2025, ZOFF Foods partnered with Reliance Retail to launch its Quick Homestyle Food range, including 5-Minute Gravies and 1-Minute Marinades, across 400+ stores nationwide. This innovation platform offers significant revenue diversification for spice manufacturers.

- Export Market Expansion: India, with a presence in over 200 countries, exports more than 225 unique spice products, solidifying its role as a reliable global supplier of both raw and value-added spices.

Market Challenges

- Price Volatility Impact on Consumer Demand: The price of jeera, a key spice, has experienced a substantial rise since the second half of 2021. Recently, it surpassed the INR 60,000 per 100 kilograms mark in both futures and the major spot market of Unjha, Gujarat.

- International Competition in Export Markets: While India remains the dominant global spice exporter, competition from China, Vietnam, and Indonesia in specific spice categories (pepper, star anise, ginger) is intensifying.

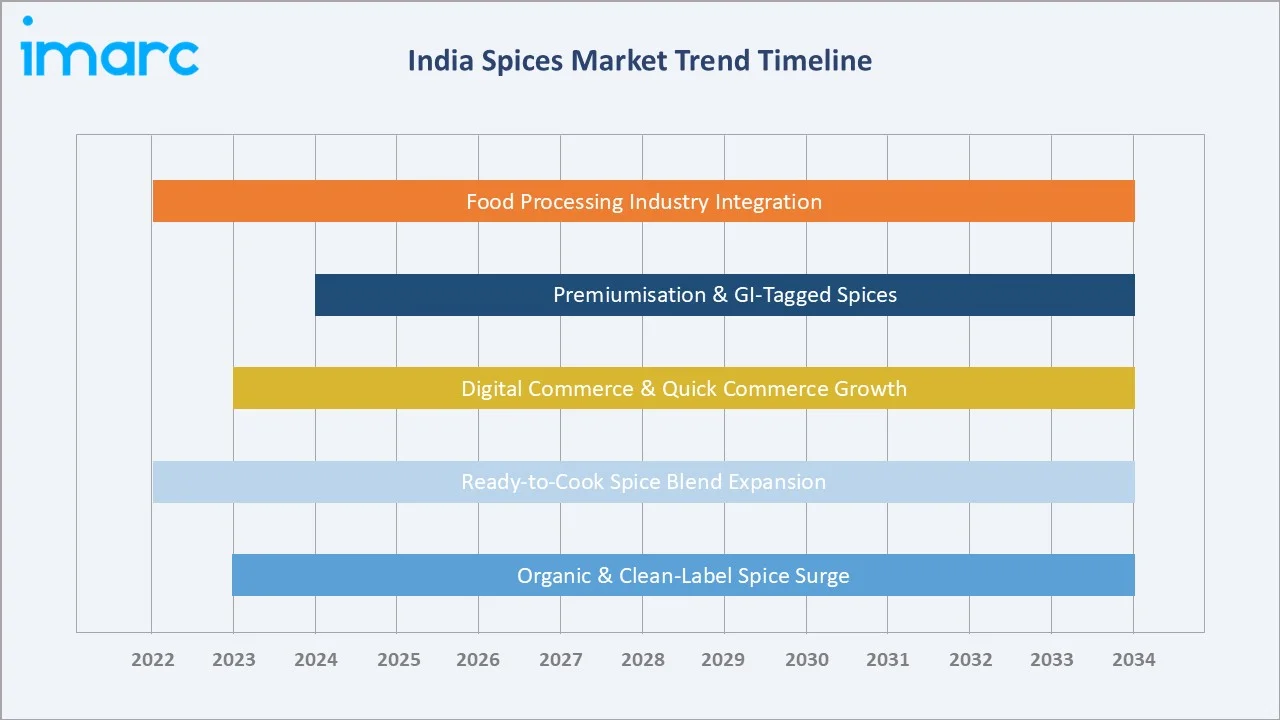

Emerging India Spices Market Trends

1. Growing Preference for Organic and Clean-Label Spices

In June 2025, ITC completed the INR 472.50 Crore acquisition of Sresta Natural Bioproducts, owner of 24 Mantra Organic, significantly expanding its organic spices portfolio for both domestic premium retail and international markets. Organic demand is particularly pronounced among urban consumers, who prioritize ingredient transparency and are willing to pay 15-25% premiums for certified organic products.

2. Expansion of Ready-to-Cook Spice Blends and Convenience Formats

In June 2025, ZOFF Foods partnered with Reliance Retail to launch its Quick Homestyle Food range, including 5-Minute Gravies and 1-Minute Marinades, across 400+ stores nationwide. This category innovation is attracting both established FMCG companies and digital-native spice brands who recognize the substantial revenue opportunity in convenience-oriented spice formats.

3. Digital Commerce and Quick Commerce Transformation

ZOFF Foods reported in October 2025 that 75% of its revenue derives from online retail, with 65% from quick-commerce platforms, validating the structural shift in how Indian consumers purchase spices. Quick-commerce platforms (10-15 minute delivery) are particularly driving impulse purchases and expanding the addressable market for premium and specialty spice products.

4. Premiumization, GI Tags, and Specialty Spice Development

Geographically Indicated (GI)-tagged spices, Byadgi chilli for its deep red color, Lakadong turmeric for its high curcumin content, Malabar pepper for its pungency, command 2–4x price premiums over generic equivalents. VAHDAM India's launch of VAHDAM Spices, targeting premium domestic and international consumers, exemplifies this trend.

5. Food Processing Industry Integration and Institutional Demand

The rapid expansion of India's food processing sector, supported by MoFPI's approval of 1,608 projects under PMKSY schemes, including 41 Mega Food Parks and 394 Cold Chain projects, is generating large-scale, consistent institutional demand for processed spice ingredients.

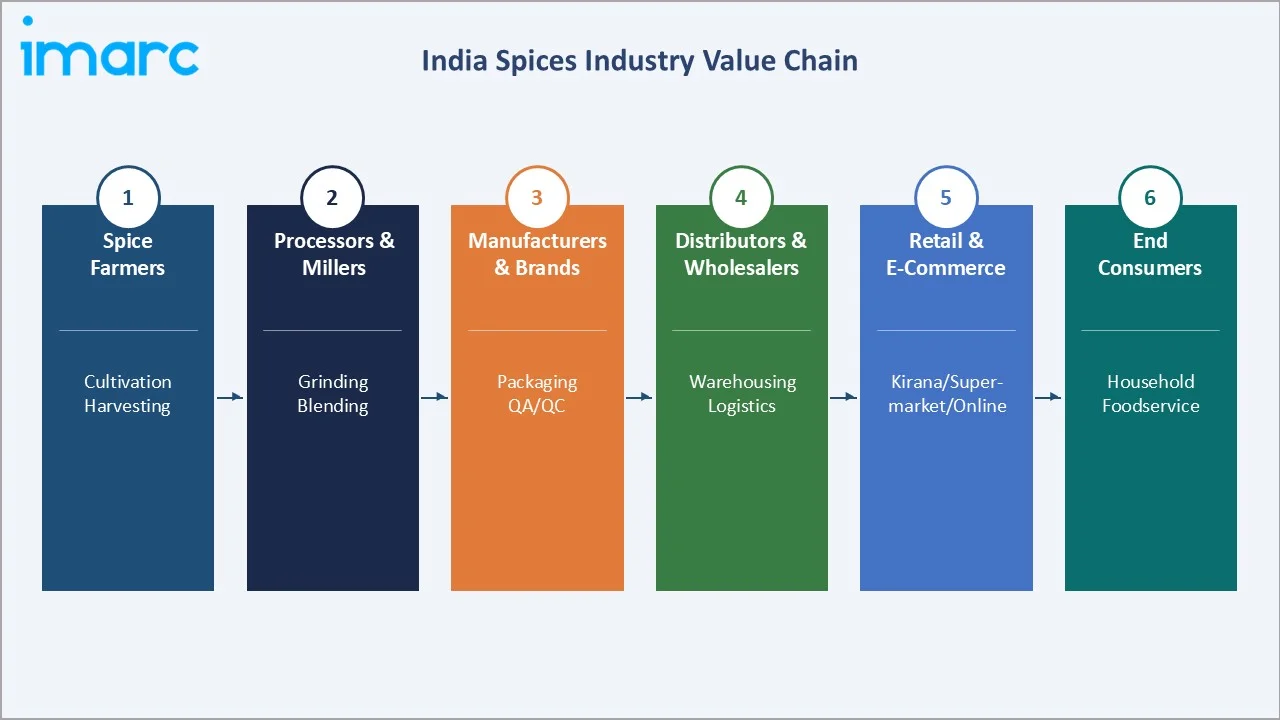

Industry Value Chain Analysis

The India spices value chain integrates millions of smallholder spice farmers, agricultural processors and millers, branded manufacturers, national and regional distributors, diverse retail channels, and ultimately India's vast consumer base. Each stage adds critical value, from agronomy and harvesting through to brand-building and last-mile distribution, with food safety and quality assurance increasingly required at every node.

|

Value Chain Stage |

Representative Players |

|

Spice Farmers |

6 million+ smallholder families; Spices Board farmer clusters |

|

Processors & Millers |

Synthite Industries, Kancor, Mane Kancor, Akay Natural |

|

Manufacturers & Brands |

Everest, MDH, ITC (Aashirvaad), DS Group (Catch), Badshah, MTR, Patanjali |

|

Distributors & Wholesalers |

FMCG national distributors, Spices Board-registered exporters |

|

Retail & E-Commerce |

Reliance Retail, D-Mart, Amazon India, Blinkit, Swiggy Instamart, Zepto |

|

End Consumers |

300M+ households, restaurants, hotels, QSRs, food manufacturers |

Technology Landscape in India Spices Industry

AI-Powered Quality Control and Sensor-Based Grading

The Indian Institute of Spices Research (IISR) collaborated with processors to implement sensor-based grading systems for turmeric and black pepper, enabling objective quality classification that replaces subjective human assessment. AI-powered vision systems are being deployed on spice sorting lines to detect foreign matter, sub-standard grades, and adulteration indicators with greater accuracy and speed than traditional manual inspection.

Cold Grinding and Aroma Preservation Technology

Cold grinding technology, which maintains low temperatures through cryogenic cooling or refrigerated milling, is gaining adoption among premium spice brands seeking to deliver superior flavor and fragrance in packaged products. This enables a meaningful quality differentiation between premium branded spices and commodity grinding operations.

Blockchain Traceability and Supply Chain Transparency

Consumer and institutional demand for traceable, farm-to-fork supply chains is driving the adoption of blockchain-based traceability platforms in the spice industry. These systems enable end-to-end documentation of cultivation origin, processing facilities, testing certifications, and the logistics chain. Traceability platforms are also enabling premium pricing differentiation for origin-specific spices with verified provenance claims.

Advanced Packaging Innovations

Packaging technology is evolving rapidly in the branded spice segment, with innovations including vacuum-sealed pouches for extended freshness, UV-barrier laminate films, and smart QR-code-enabled packaging. These packaging advancements are enabling India spices market to command a premium positioning in organized retail and already commands 67.0% of market share by form.

India Spices Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Form |

Packets |

67.0% |

2025 |

|

Application |

Veg Curries |

29.0% |

2025 |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Region |

North India |

30.0% |

2025 |

Segmentation by Application

To access detailed market analysis, Request Sample

Veg curries dominate application demand at 29.0% in 2025, as India's vegetarian culinary tradition creates constant, high-volume spice consumption in both households and the vast food service sector. Meat and poultry products represent the second-largest application at 19.4%, reflecting rising protein consumption across urban India and the growth of non-vegetarian quick-service restaurant chains requiring consistent spice seasoning blends for marinades and cooking.

Segmentation by Form

Packets command the dominant form share at 67.0% in 2025, reflecting the broad consumer shift from loose spice purchases in traditional wet markets toward hygienic, branded, and portion-controlled packaged formats. Sprinkler format (19.4%) is growing steadily, particularly in the dining and food service segments where direct-application convenience is valued. Crusher format (13.6%) caters to premium consumers who prefer freshly crushed whole spices for superior freshness and aroma intensity.

Regional India Spices Market Insights

North India leads the market with a 30.0% share in 2025, fueled by both domestic consumption and significant export demand, particularly in markets like the Middle East and Southeast Asia. Additionally, the growing popularity of Indian cuisine globally continues to bolster demand for spices.

|

Region |

Share (2025) |

Key States & Drivers |

Regulatory Impact |

Major Companies |

|

South India |

29.0% |

Kerala, Tamil Nadu, Karnataka, Andhra Pradesh; cardamom, pepper, turmeric, chilli |

Spices Board quality standards, export incentives, and GI registrations (e.g., Malabar pepper, Kazhakoottam turmeric) |

Synthite, Kancor, Akay Natural, Everest, MDH |

|

North India |

30.0% |

Punjab, Rajasthan, UP, Delhi; cumin, coriander, spice blends; dense urban population |

Food Safety & Standards Authority of India (FSSAI) regulations, GI tags (e.g., Kashmiri chilli) |

DS Group (Catch), Badshah Masala, MTR, Everest, MDH |

|

West and Central India |

24.0% |

Gujarat, Maharashtra, Madhya Pradesh; cumin from Mehsana, chilli from Guntur |

FSSAI quality/compliance rules, state agriculture extension for export crops |

Patanjali, MDH, Everest, VKV & Sons Exports, Indian Spice & Food Store |

|

East India |

17.0% |

West Bengal, Odisha, Bihar, Northeast; mustard, turmeric; growing organized retail |

FSSAI standards & labelling, E‑commerce compliance (packaged foods) |

Gits Food, Eastern Condiments, Local co‑ops & exporters |

West and Central India held a 24.0% share in 2025 and represent the highest growth potential region, with Gujarat and Maharashtra driving rapid market expansion. Gujarat's Mehsana district is India's largest cumin exporter, with INR 3,995 Crore worth of cumin, fennel, and Isabgol in 2025. Maharashtra and Madhya Pradesh contribute chilli, turmeric, and garlic.

Competitive Landscape

India spices market exhibits a highly fragmented competitive structure, with national FMCG brands competing alongside strong regional players, private-label offerings from organized retail, and a vast base of unorganized local manufacturers.

The top national brands, Everest Foods, MDH Spices, ITC's Aashirvaad, Catch Foods (DS Group), and Badshah Masala, command disproportionate brand awareness and organized retail shelf space but collectively account for less than 30% of total market revenue, reflecting the market's structural fragmentation.

|

Company Name |

Key Brands / Products |

Market Position |

Core Strength |

|

Everest Food Products Pvt. Ltd. |

Everest Masala, Tikhalal, Tikhal Garam |

Leader |

Broadest national distribution; 52+ blended masala variants; strong West & North India presence |

|

Mahashian Di Hatti (MDH) |

MDH Masala, Chunky Chat, Kitchen King |

Leader |

Premium North Indian masala; decades of brand equity; high household penetration |

|

ITC Ltd. (Aashirvaad) |

Aashirvaad Spices, 24 Mantra Organic |

Leader |

Organic expansion through 24 Mantra acquisition (INR 472.5 Cr, 2025); premium & mass segments |

|

DS Group (Catch Foods) |

Catch Masala, Catch Salt, spice blends |

Challenger |

Innovative seasoning and sprinkler formats; impulse and food service channel focus |

|

Badshah Masala |

Badshah Masala, Pav Bhaji, Garam Masala |

Challenger |

Strong Maharashtra and Gujarat presence; authentic regional formulations |

|

Orkla India / MTR Foods |

MTR Masala, Spice Mixes, Ready Mixes |

Challenger |

South India leadership; ready-to-cook integration; premium organic range |

|

Patanjali Ayurved Ltd. |

Patanjali Spices, Organic Masala |

Specialist |

Ayurvedic and organic positioning; mass-market price points; pan-India distribution |

|

Aachi Masala Foods |

Aachi Masala, Biryani Masala, Sambar Powder |

Specialist |

South India stronghold; authentic regional flavour formulations; institutional supply |

|

Goldiee Group |

Goldiee Masala, Pure Spices Range |

Emerging |

North India regional strength; pure spice + blended range; growing organised trade footprint |

Key Company Profiles

Everest Food Products Private Limited

India's prominent spice company by retail reach, headquartered in Mumbai, Maharashtra, with pan-India distribution presence and 52+ masala variants serving diverse regional cooking preferences.

- Product Portfolio: Everest Masala (blended spices), Tikhalal (red chilli powder), pure spice range, and specialty blends for vegetarian, non-vegetarian, and snack applications.

- Recent Developments: Continued focus on food safety, quality assurance, and export market development. Active in expanding modern trade and e-commerce distribution alongside the traditional kirana store network.

- Strategic Focus: Distribution depth across tier-2 and tier-3 cities; product formulation for diverse regional cuisines; organic product line development for premium urban consumers.

ITC Limited (Aashirvaad Spices / 24 Mantra Organic)

Diversified Indian conglomerate with strong FMCG and agribusiness presence. Aashirvaad is ITC's flagship food brand. In June 2025, ITC completed the INR 472.50 Crore acquisition of Sresta Natural Bioproducts (24 Mantra Organic).

- Product Portfolio: Aashirvaad Spices (branded pure spices and blends), 24 Mantra Organic (certified organic spices and food products), targeting both mass and premium consumer segments.

- Recent Developments: The 24 Mantra acquisition represents ITC's most significant move into the organic food segment, strengthening its portfolio for domestic premium retail and international organic spice export markets simultaneously.

- Strategic Focus: Organic and clean-label segment leadership; international export market expansion for organic spices; premium-to-mass product range spanning multiple consumer tiers.

DS Group (Catch Foods)

Noida-based diversified conglomerate with Catch Foods as its flagship spice and seasoning brand, known for innovative packaging formats and strong impulse-purchase channel presence.

- Product Portfolio: Catch Masala (spice blends), Catch Salt (table and cooking), seasoning sprinklers, grinders, and a comprehensive range of pure and blended spice products.

- Recent Developments: Expanding into the ready-to-cook and convenience seasoning segment with innovative product formats targeting urban food service and household consumers seeking culinary convenience.

- Strategic Focus: Impulse channel and food service growth; innovative packaging (sprinklers, crushers); premiumization through specialty and international flavor-inspired seasoning blends.

Market Concentration Analysis

India spices market remains highly fragmented, with the organized branded segment accounting for approximately 30–35% of total market value and the unorganized segment comprising the majority. Among branded players, Everest Foods, MDH, ITC Aashirvaad, Catch Foods, and Badshah Masala are the most recognized national brands.

Regional fragmentation is significant: South India has its own set of dominant regional brands (MTR Foods/Orkla, Aachi Masala, Eastern Condiments), North India is dominated by MDH, Everest, and Goldiee, while West India features Badshah and other regional brands.

ZOFF Foods' rapid digital scale-up demonstrates how technology-native challengers can capture significant market share without traditional distribution infrastructure. These dynamics suggest the market is entering a gradual consolidation phase, with premium and organic segments consolidating fast while commodity-grade segments remain fragmented.

Investment & Growth Opportunities

Fastest Growing Segments

- Ready-to-Cook Spice Blends and Convenience Formats (CAGR ~12.1%): The convenience-food megatrend is creating structural demand for innovative masala blends. ZOFF Foods' INR 170 Crore revenue target and Reliance Retail partnership validate the commercial scale achievable through RTC spice innovation, particularly among urban consumers aged 22–40.

Emerging Markets and Export Opportunities

- East India Market Development: With only 17.0% share, East India is significantly underserved relative to its population. Rapid e-commerce adoption in tier-2 cities (Patna, Bhubaneswar, Guwahati) and modern trade expansion in Kolkata are creating new distribution opportunities for branded spice manufacturers.

Investment Trends

Private equity and strategic FMCG investment in India's spice sector accelerated in 2024–2025. The government's INR 422.30 Crore Spices Board SPICED scheme and MoFPI's approval of 41 Mega Food Parks are mobilizing both public and private infrastructure investment. Digital-native brands like ZOFF Foods are attracting venture capital investment on the strength of their e-commerce-first distribution model.

Future India Spices Market Outlook (2026-2034)

India spices market is positioned for sustained, robust growth through 2034, underpinned by demographic and consumption megatrends that are structural rather than cyclical. From INR 221.83 Thousand Crores in 2025 to INR 528.99 Thousand Crores by 2034, an absolute value addition of over INR 307 Crores, the market's expansion will be driven by the powerful intersection of India's 1.4 billion population, rapidly rising disposable incomes, and food processing sector growth.

Premiumization will be the defining theme of market evolution through 2034. Organic, GI-tagged, and single-origin specialty spices will command a growing revenue share as urban consumers with rising incomes shift toward quality over price. Packaged, branded spice products will continue displacing loose, unbranded sales, supported by improving cold-chain logistics, modern retail expansion, and the penetration of e-commerce and quick-commerce into tier-2 and tier-3 Indian cities.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys with over 200 industry participants in 2025, including spice company management teams, agricultural commodity traders, food processing industry procurement heads, organized retail category managers, e-commerce platform executives, and farmer group representatives across South India, North India, and West India.

Secondary Research

Secondary research encompassed a comprehensive review of Spices Board of India export data, FSSAI regulatory databases, Ministry of Agriculture and Farmers Welfare crop production statistics, company annual reports, trade publications (Spice India, Food Business News India), IBEF sectoral reports, and academic research on Indian spice cultivation, processing, and trade.

Forecasting Models

Market size estimations used bottom-up modelling across product types (pure spices by variety, blended masalas by type), application segments, form categories, and regional markets, validated against top-down benchmarks from Spices Board export-import data and FMCG sector revenue databases.

India Spices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Crores |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered |

|

| Applications Covered | Veg Curries, Meat and Poultry Products, Snacks and Convenience Foods, Soups, Sauces and Dressings, Bakery and Confectionery, Frozen Foods, Beverages, Others |

| Forms Covered | Packets, Sprinkler, Crusher |

| Regions Covered | South India, North India, West and Central India, East India |

| Companies Covered | Everest Food Products Pvt. Ltd., Mahashian Di Hatti (MDH), ITC Ltd. (Aashirvaad), DS Group (Catch Foods), Badshah Masala, Orkla India / MTR Foods, Patanjali Ayurved Ltd., Aachi Masala Foods, Goldiee Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Spices Market Report

India spices market was valued at INR 221.83 Thousand Crores in 2025 and is projected to reach INR 528.99 Thousand Crores by 2034, growing at a CAGR of 10.14% during 2026-2034.

The market is forecast to grow at a CAGR of 10.14% during 2026-2034, driven by rising domestic consumption, organic spice demand, food processing industry expansion, and growing international export volumes for premium and organic spice products.

North India leads with a 30.0% market share in 2025, driven by its rich agricultural heritage and diverse spice production. This region’s dominance is fueled by both domestic consumption and significant export demand.

Key drivers include India's deep culinary heritage and household spice demand, rising health consciousness driving organic spice adoption, food processing industry expansion, rapid e-commerce and quick-commerce channel growth, and government export promotion through the Spices Board of India.

Veg curries lead with a 29.0% application share in 2025, driven by India's predominantly vegetarian cooking tradition, diverse regional vegetable cuisines, and the central role of spices in both household and food service meal preparation nationally.

Key trends include growing demand for organic and clean-label spices, expansion of ready-to-cook masala blends, rapid e-commerce and quick-commerce adoption, premiumization toward GI-tagged specialty spices, and food processing industry integration.

Leading companies include Everest Food Products, Mahashian Di Hatti (MDH), ITC (Aashirvaad Spices / 24 Mantra Organic), DS Group (Catch Foods), Badshah Masala, Orkla India (MTR Foods), Patanjali Ayurved, Aachi Masala Foods, and Goldiee Group.

Packets dominate the form segment at 67.0% in 2025, driven by consumer preference for hygienic, tamper-proof, portion-controlled packaging with standardized quality and extended shelf life, available across organized retail and e-commerce channels.

Top investment opportunities include certified organic spice processing and GI-tagged specialty products, ready-to-cook masala blend innovation, e-commerce and quick-commerce distribution platforms, East India market development, and high-value pharmaceutical spice extract.

India exported over 793,000 tons of spices valued at USD 4.45 billion, supplying China, Bangladesh, the UAE, the U.S., and Europe. Gujarat's Mehsana alone exported INR 3,995 Crore of cumin and fennel in 2025, reflecting the strength and geographic diversity of India's spice export markets.

Key challenges include climate change and monsoon variability affecting crop yields, quality control and food safety compliance requirements, market fragmentation with ~70% unorganized, price volatility in key spice commodities, and competition from China and Vietnam in international spice export markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade