India Sports Betting Market Size, Share, Trends and Forecast by Platform, Betting Type, Sports Type, and Region, 2026-2034

India Sports Betting Market Size, Share, Trends & Forecast (2026-2034)

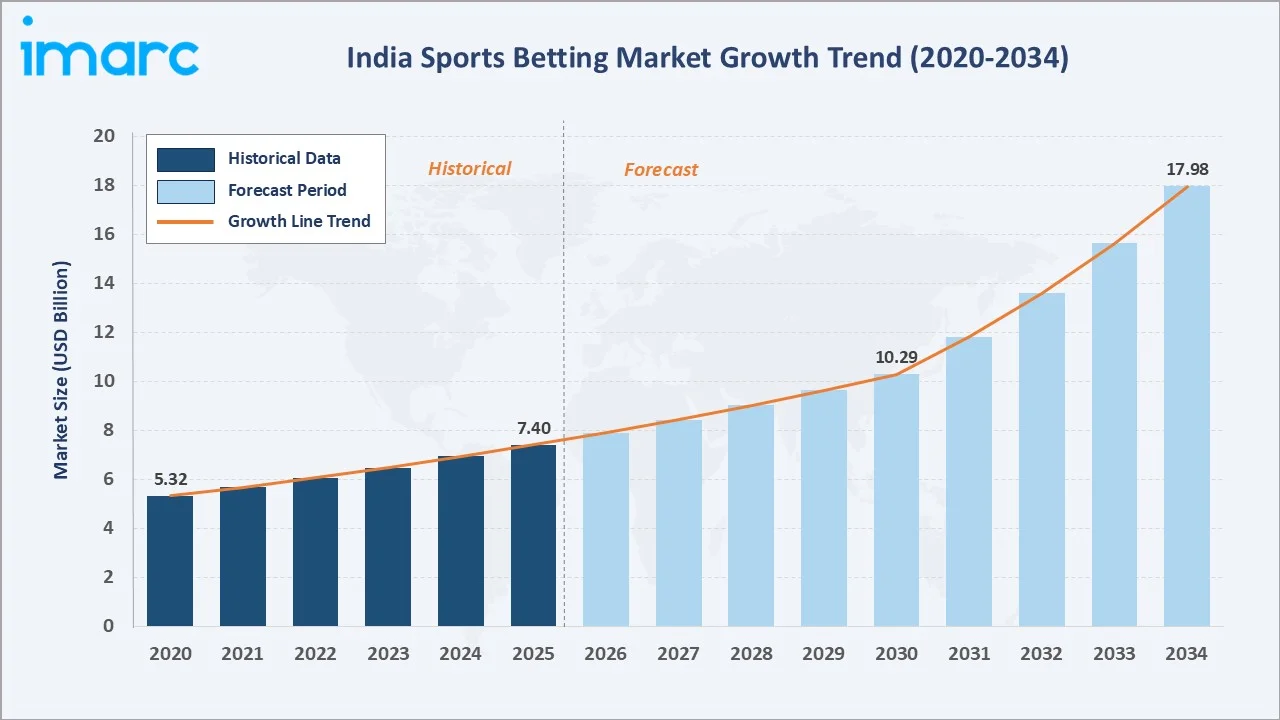

The India sports betting market was valued at USD 7.40 Billion in 2025 and is projected to reach USD 17.98 Billion by 2034, exhibiting a CAGR of 6.82% during 2026-2034. Expanding smartphone penetration, affordable mobile data availability, increasing cricket-led digital engagement, rising disposable incomes, and accelerating adoption of live and in-play betting formats are the primary drivers shaping the market growth.

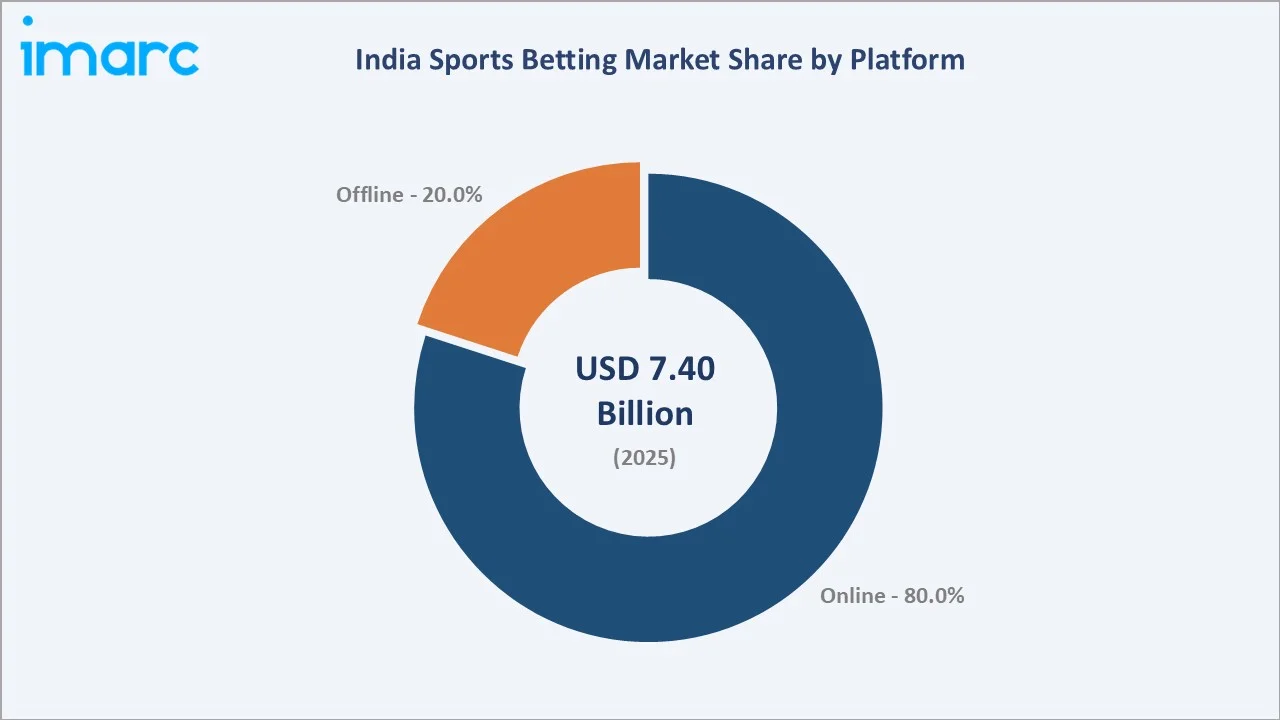

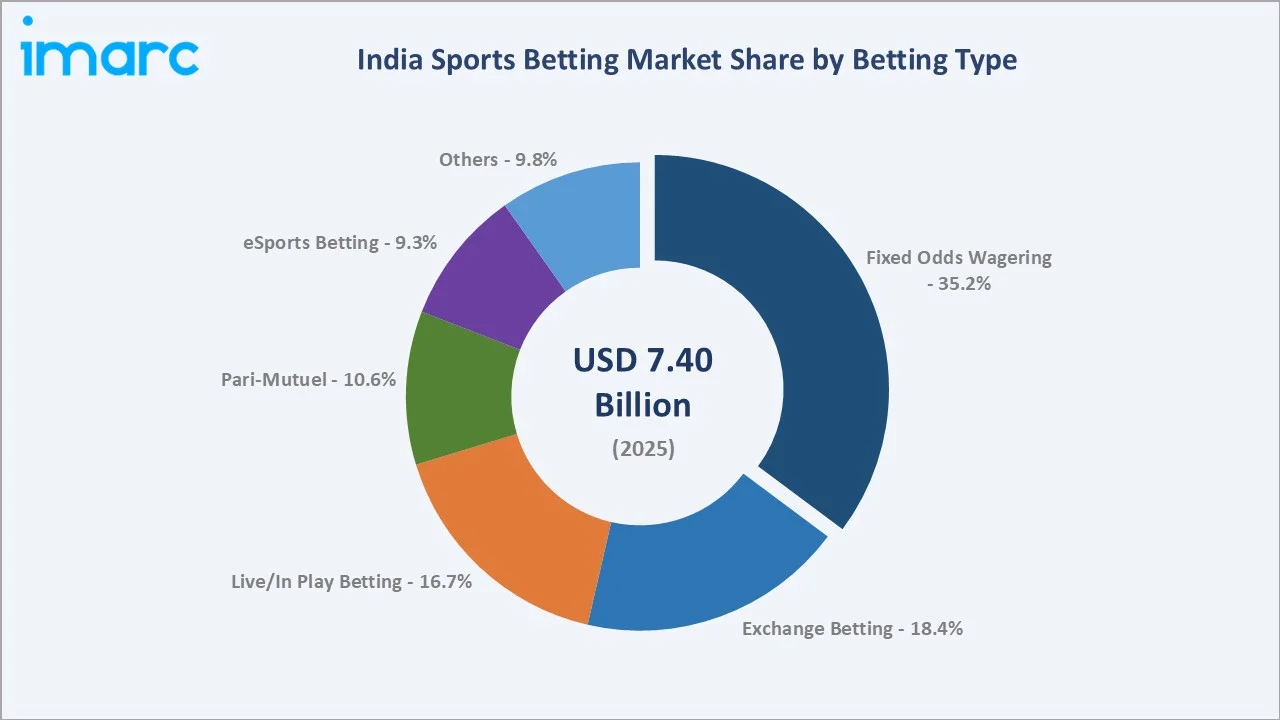

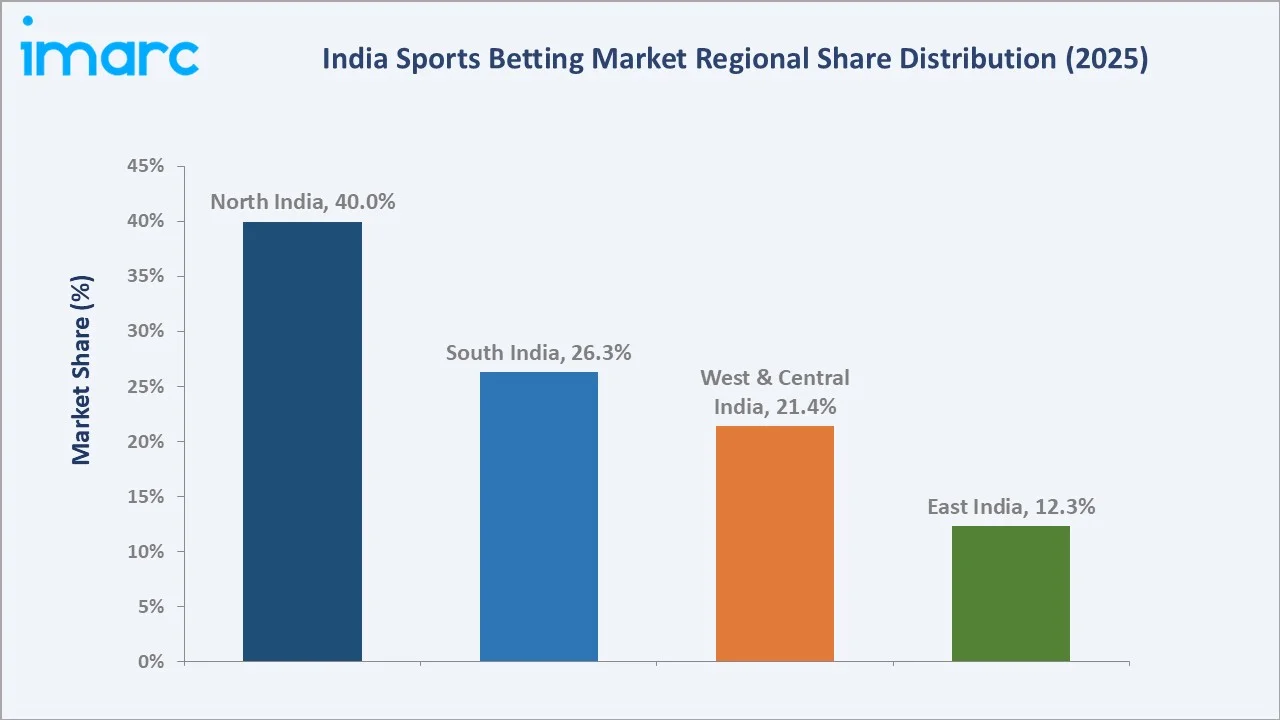

Online leads the platform segment at 80.0%, fixed odds wagering dominates the betting type segment at 35.2%, and North India commands 40.0% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.40 Billion |

|

Forecast Market Size (2034) |

USD 17.98 Billion |

|

CAGR (2026-2034) |

6.82% |

|

Base Year |

2025 |

|

Historical Period |

2026-2034 |

|

Forecast Period |

2020-2025 |

|

Largest Region |

North India (40.0%, 2025) |

|

Fastest Growing Region |

South India (26.3%, 2025) |

|

Leading Platform |

Online (80.0%, 2025) |

|

Leading Betting Type |

Fixed Odds Wagering (35.2%, 2025) |

The India sports betting market expanded from USD 5.32 Billion in 2020 to USD 7.40 Billion in 2025, driven by widening digital sports engagement, growing fantasy participation, and rapid mobile internet penetration across urban and tier-2 cities. Anchored at USD 10.29 Billion in 2030, the forecast to USD 17.98 Billion by 2034 is supported by accelerating in-play betting adoption, expanding eSports participation, and a more structured regulatory environment for permitted formats.

To get more information on this market, Request Sample

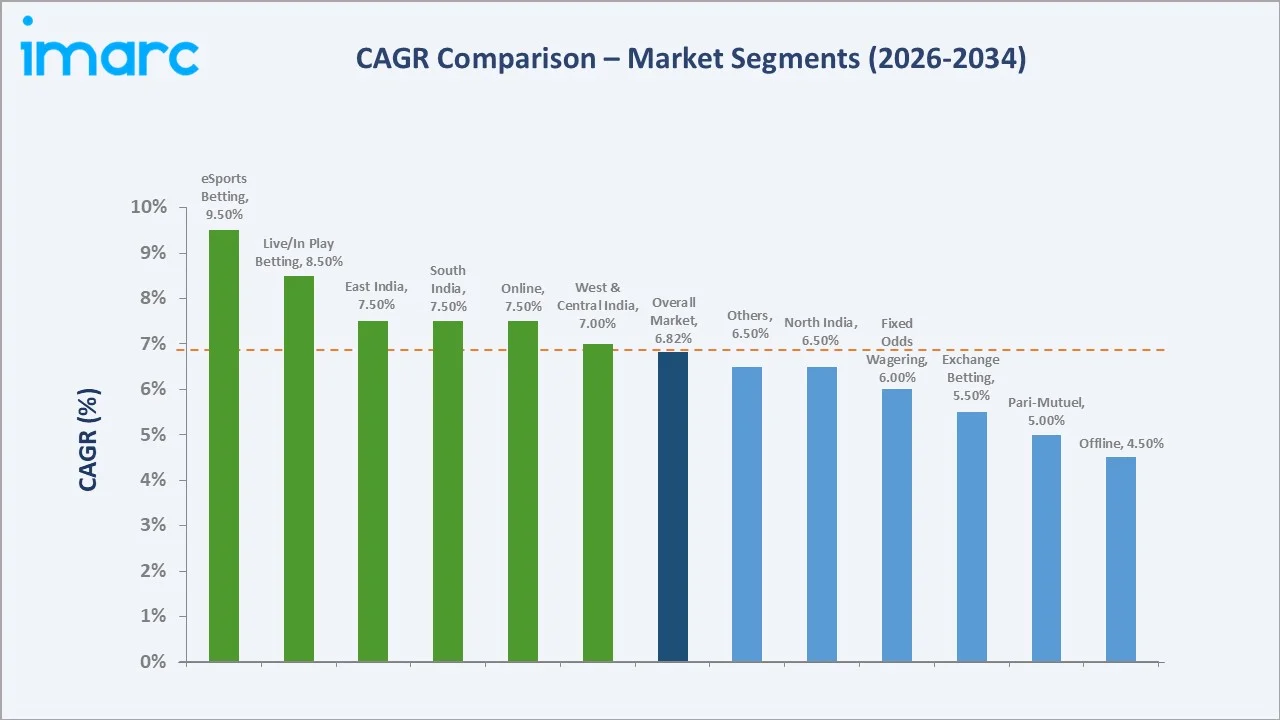

CAGR trajectories across platform and betting type sub-segments show eSports betting and live or in-play betting expanding faster than the overall 6.82% market CAGR, driven by younger audiences, real-time engagement, and growing multi-sport participation across the country.

Executive Summary

The India sports betting market is on a steady growth trajectory from USD 5.32 Billion in 2020 to USD 17.98 Billion by 2034. The segment has moved from informal, offline placement to digitally enabled, platform-led participation across cricket, football, kabaddi, and emerging multi-sport categories. Affordable smartphones, fast mobile data, and seamless digital payments are encouraging users to engage with skill-led formats.

Online dominates the platform segment at 80.0% in 2025, supported by low-friction mobile onboarding, instant deposits via UPI, and integrated live data feeds. Fixed odds wagering leads the betting type segment at 35.2%, fueled by predictable returns and broad cricket and football coverage. The ICC Men’s T20 World Cup 2026 final reached 72.5 Million simultaneous digital users in India, surpassing the global streaming record established three days prior during the second semi-final. North India commands 40.0% of the regional share, led by high population density, strong cricket fan engagement, and the largest base of digital sports users in the country.

Key Market Insights

|

Insight |

Data |

|

Leading Platform |

Online - 80.0% share (2025) |

|

Second Platform |

Offline - 20.0% share (2025) |

|

Leading Betting Type |

Fixed Odds Wagering - 35.2% share (2025) |

|

Second Betting Type |

Exchange Betting - 18.4% share (2025) |

|

Leading Region |

North India - 40.0% share (2025) |

|

Fastest Growing Region |

South India – 26.3% share (2025) |

|

Top Companies |

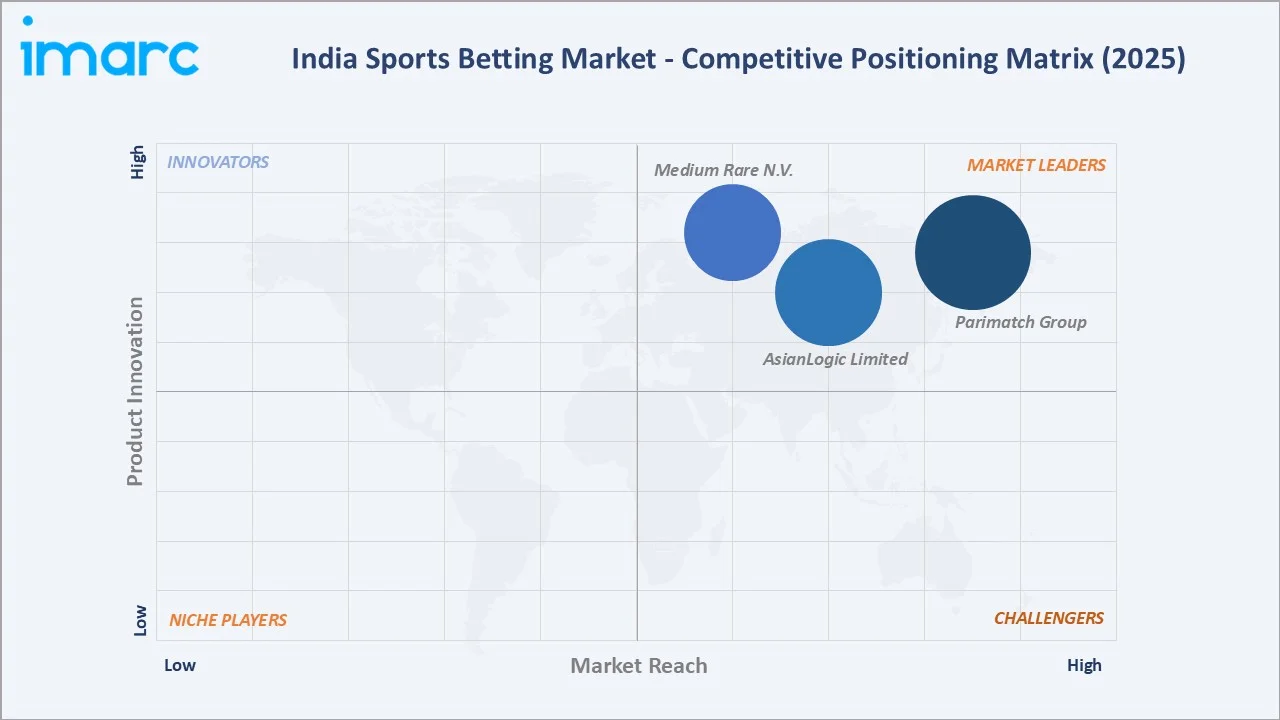

Parimatch Group, AsianLogic Limited, Medium Rare N.V. |

Key Analytical Observations Expanding on the Data Above:

- Online dominance at 80.0% is supported by deep smartphone penetration, instant UPI-based deposits, and seamless integration with live odds and data feeds. As a part of the 80th round of the National Sample Survey (NSS), the Comprehensive Modular Survey: Telecom (CMS: T), conducted from January to March, 2025, among people aged 15-29 years, around 97.1% indicated that they used a mobile phone (smartphones included), creating one of the world's largest addressable bases for digitally delivered sports engagement.

- Offline share at 20.0% is sustained by horse race betting at licensed turf clubs, on-course totalizator systems, and state-licensed lottery and gaming counters that continue to serve traditional bettor segments.

- Fixed odds wagering leadership at 35.2% reflects user preference for transparent, pre-set returns and simple selection mechanics on widely followed cricket, football, and tennis events.

- Exchange betting at 18.4% is expanding as more bettors adopt peer-to-peer matched odds, supported by deeper liquidity pools and richer pre-match and in-play market depth.

- North India at 40.0% dominates regional share, anchored by Delhi-NCR, Punjab, Haryana, and Uttar Pradesh, supported by dense cricket fan engagement and the largest base of digital sports users across the country.

India Sports Betting Market Overview

Sports betting refers to the activity of placing wagers on the outcome of sporting events, including cricket matches, football fixtures, kabaddi leagues, tennis tournaments, horse races, and competitive eSports contests, through online platforms, retail outlets, or licensed offline venues. The market spans fixed odds wagering, exchange betting, live or in-play betting, pari-mutuel pools, eSports wagering, and other niche formats.

The Indian ecosystem integrates technology and data feed providers, online platforms and operators, payment service providers, regulatory authorities at central and state levels, sports leagues and event organizers, affiliate marketing partners, and compliance and risk-management vendors. Together they enable the delivery of sports wagering experiences within an evolving legal framework.

Market Dynamics

To evaluate market opportunities, Request Sample

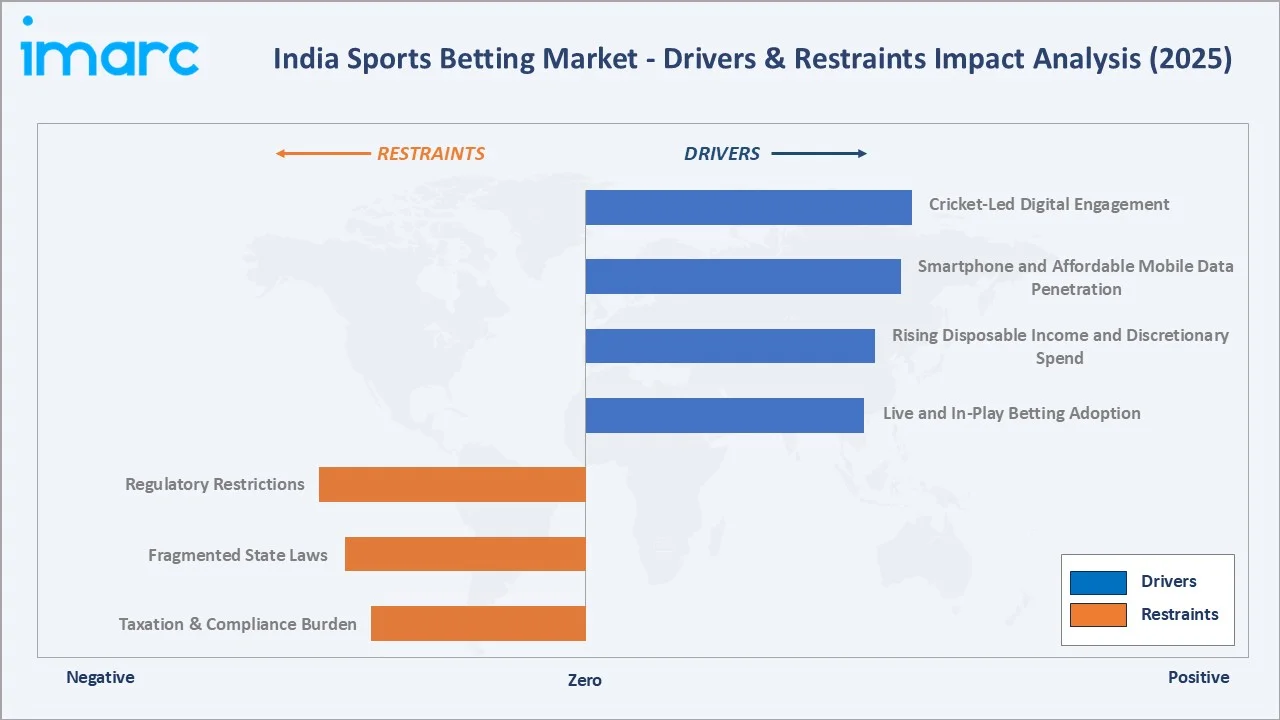

Market Drivers

- Cricket-Led Digital Engagement: India's cricket-first sports culture, anchored by the Indian Premier League, international fixtures, and domestic tournaments, drives consistent digital viewership and continuous demand for wagering products across formats and platforms.

- Smartphone and Affordable Mobile Data Penetration: Rapid expansion of low-cost smartphones and one of the lowest mobile data tariffs globally is bringing first-time digital sports users from tier-2 and tier-3 cities into platform-based participation across permitted formats. According to government data, as of March 2026, India, with 1.03 Billion Internet users had some of the lowest data rates globally at USD 0.08 to USD 0.10 per GB, compared to a worldwide average of USD 2.59 per GB.

- Rising Disposable Income and Discretionary Spend: Growing middle-class incomes, expanding urban consumption, and the increasing share of leisure spending in household budgets are supporting steady growth in digital sports entertainment and adjacent betting activity.

- Live and In-Play Betting Adoption: Increasing availability of low-latency video, real-time odds engines, and micro-market formats is enabling bettors to engage event-by-event during matches, lifting participation frequency and average session value across online platforms.

Market Restraints

- Regulatory Restrictions on Real-Money Online Gaming: Regulatory restrictions on offering and facilitating real-money online games are materially reshaping the addressable online segment for many domestic operators. The tighter compliance environment is limiting monetization opportunities and increasing operational uncertainty across digital gaming platforms.

- Fragmented State-Level Gambling Laws: Betting and gambling fall under state subjects in India's Constitution, leading to differing rules across states for skill versus chance games, permitted formats, and licensing, creating compliance complexity for nationwide platforms.

- Taxation and Compliance Burden: The introduction of a 28% Goods and Services Tax on the full face value of bets in 2023, combined with tax deduction at source on winnings and rising compliance costs, compresses operator margins and constrains promotional spending in permitted segments.

Market Opportunities

- eSports Wagering and Multi-Sport Diversification: Formal recognition of eSports and rising audiences across football, kabaddi, tennis, and emerging leagues create new revenue pools beyond cricket for licensed and compliant operators.

- Horse Race and Turf Club Modernization: Online betting on horse races, already legal in select states, presents opportunities to digitize totalizator systems, expand inter-venue betting, and integrate with mobile platforms under state-sanctioned frameworks.

Market Challenges

- Offshore and Unregulated Operators: Persistent reach of offshore betting platforms targeting Indian users creates leakage of consumer spend, weakens responsible-gambling oversight, and reduces tax capture by Indian authorities.

- Responsible Gambling and Consumer Protection: Concerns around addiction, financial distress, and underage participation have prompted stricter advertising rules, celebrity endorsement curbs, and evolving codes of practice for permitted operators.

Emerging Market Trends

1. Shift Toward Permitted Skill-Based Formats and eSports

Operators are pivoting from real-money fantasy and chance-based formats toward free-to-play models, subscription content, and licensed eSports tournaments that align with the new regulatory framework. As per IMARC Group, the India eSports market size was valued at USD 239.13 Million in 2025. The transition is also accelerating investment in original content, watch-along experiences, and creator-led sports communities that monetize through advertising and in-app purchases rather than stakes-based participation.

2. Live and In-Play Betting Becoming Mainstream

Real-time micro-markets across cricket, football, tennis, and kabaddi are rapidly displacing pre-match-only wagering on permitted platforms. Lower-latency video feeds, faster odds compilation, and richer mobile interfaces are enabling users to react ball-by-ball, supporting the India sports betting market growth through higher engagement intensity and longer in-session activity.

3. Centralized Online Gaming Authority and Stricter Compliance

The introduction of a centralized regulatory framework for online gaming is expected to strengthen oversight across registration, content review, and enforcement activities. Standardized definitions for eSports and online social games, along with tighter advertising and compliance requirements, are likely to reshape operator strategies across permitted segments of the India sports betting market.

4. UPI and Embedded Payments Reshaping Onboarding

UPI, instant settlement rails, and integrated wallet experiences are dramatically reducing friction in deposit, withdrawal, and verification flows for permitted operators. The shift is enabling faster first-time user onboarding, smoother KYC handoffs, and more granular fraud controls, supporting sustainable scale across the formal segment.

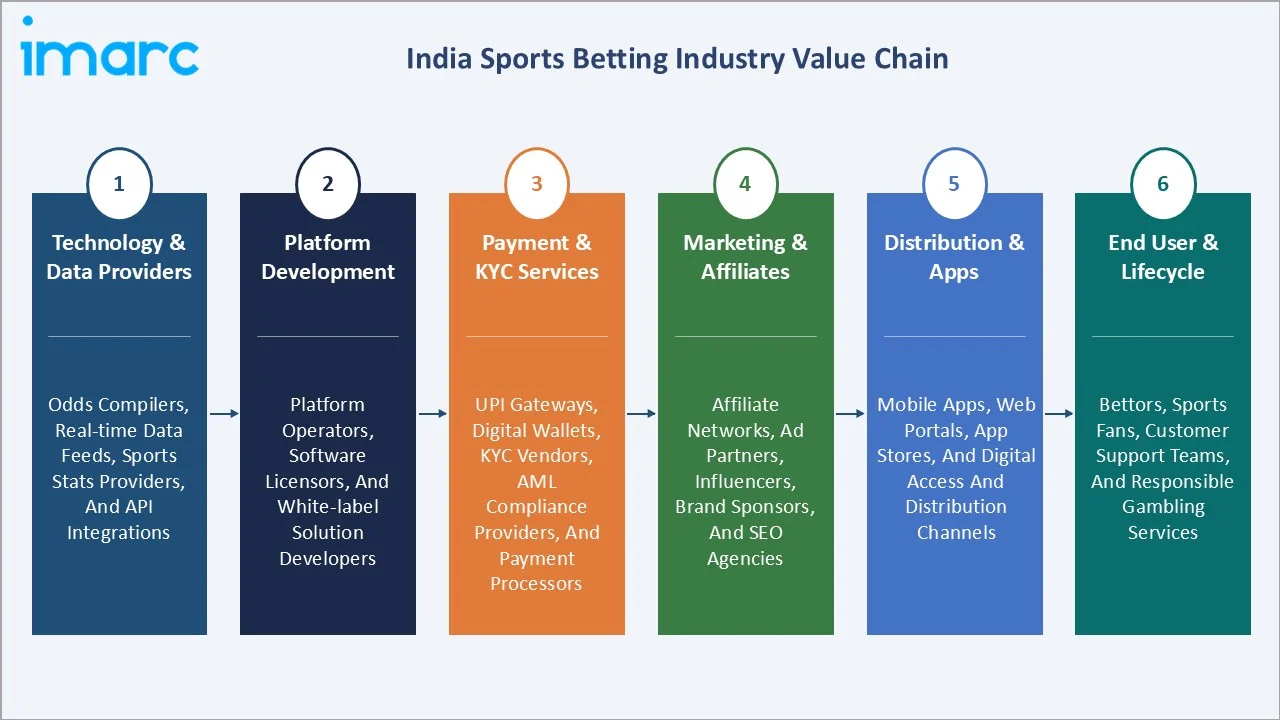

Industry Value Chain Analysis

The India sports betting value chain spans six stages from technology and data supply through end-user engagement and lifecycle management. Platform development, payment infrastructure, and marketing capture the highest value-add, while compliance and customer protection capabilities increasingly determine sustainable competitive position in this regulated category.

|

Stage |

Key Players / Examples |

|

Technology & Data Providers |

Sports data feed suppliers, odds compilers, real-time score providers, and technology platform vendors enabling backend and frontend systems |

|

Platform Development |

Online operators, mobile app developers, sportsbook software firms, and licensed offline venues such as state-sanctioned turf clubs and lottery agents |

|

Payment & KYC Services |

UPI-enabled payment gateways, digital wallet providers, banking partners, KYC and identity verification specialists supporting compliant onboarding |

|

Marketing & Affiliates |

Digital marketing agencies, affiliate networks, content creators, and advertising platforms that drive permitted user acquisition and retention |

|

Distribution & Apps |

Mobile application stores, web portals, retail counters at licensed venues, and integrated platforms delivering wagering services to end users |

|

End Use & Lifecycle |

Individual bettors, customer support providers, responsible-gambling agencies, and grievance redressal mechanisms supporting long-term user engagement |

Vertically integrated players, especially those owning proprietary technology stacks, original data feeds, and direct user relationships, are positioned to capture greater value than partners reliant on third-party infrastructure.

Technology Landscape in the India Sports Betting Industry

Odds Engines and Real-Time Trading Systems

Modern sportsbook operators are deploying low-latency odds compilation engines that ingest live feeds, statistical models, and player behavior signals to deliver dynamic in-play pricing. These systems support rapid market creation across hundreds of micro-events per match, enabling richer product depth and tighter risk management on permitted platforms.

Data Analytics, AI, and Personalization

AI and machine learning (ML) models are increasingly used for user segmentation, content recommendation, fraud detection, and responsible play interventions. AI-driven personalization is enabling operators to surface the most relevant sports and markets to each user, while behavioral models flag risky patterns for early intervention.

Mobile-First Platforms and Embedded Payments

Native mobile apps tightly integrated with UPI, digital wallets, and instant settlement rails dominate the user experience. Embedded KYC, biometric login, real-time deposit-withdrawal flows, and lightweight progressive web apps support fast onboarding and seamless cross-device usage across smartphones, tablets, and connected screens.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Platform |

Online |

80.0% |

2025 |

|

Betting Type |

Fixed Odds Wagering |

35.2% |

2025 |

|

Sports Type |

🔒 |

🔒 |

2025 |

|

Region |

North India |

40.0% |

2025 |

By Platform

Online commands an 80.0% majority share in 2025, driven by smartphone-led participation, instant UPI deposits, deep cricket and multi-sport content, and integration with live odds and streaming. The segment benefits from low operating overhead, rapid product iteration, and reach across both metro and non-metro markets.

To access detailed market analysis, Request Sample

Offline at 20.0% in 2025 covers horse race betting at licensed turf clubs, on-course totalizator pools, and state-licensed lottery and gaming counters. The segment remains relevant in markets with strong race traditions and among older bettor cohorts that prefer in-person placement, even as digital channels expand.

By Betting Type

Fixed odds wagering dominates with 35.2% share in 2025, reflecting user preference for transparent, pre-set returns and easy stake calculations on widely followed cricket, football, and tennis fixtures. The format remains the default entry point for first-time bettors due to its simplicity and predictability.

Exchange betting at 18.4% is expanding through peer-to-peer matched odds and deeper liquidity pools. Its growing appeal is supported by greater pricing transparency, competitive odds structures, and increasing user preference for flexible wagering formats.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

40.0% |

Large urban population, strong cricket fan engagement, deep smartphone penetration, and high digital sports consumption |

|

South India |

26.3% |

Rising disposable incomes, fast-growing IT-driven user base, expanding multi-sport interest, and high mobile internet adoption |

|

West & Central India |

21.4% |

Established metro markets, strong fantasy sports participation, mature digital ecosystem, and presence of licensed offline venues |

|

East India |

12.3% |

Emerging digital adoption, expanding football and kabaddi audiences, growing youth engagement, and rising tier-2 city participation |

North India at 40.0% in 2025 leads the regional landscape, anchored by Delhi-NCR, Punjab, Haryana, and Uttar Pradesh. Dense cricket fan engagement, the largest concentration of digital sports users, and a mature urban consumer base support sustained leadership across both online and offline channels.

South India at 26.3% is the fastest growing region. Rapid expansion of digital infrastructure, growing multi-sport viewership, and rising tier-2 and tier-3 city participation are accelerating regional expansion through 2034.

Competitive Landscape

The India sports betting market is moderately fragmented, with established offshore platforms leading user reach and product depth while emerging operators compete on niche formats and regional engagement. Brand strength, technology stack, payments integration, and regulatory readiness form the key competitive moats following the recent overhaul of the online gaming legal framework.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Parimatch Group |

Parimatch Sportsbook |

Leader |

Technology-driven sportsbook operator with mobile-first platform and multi-regional presence |

|

AsianLogic Limited |

Dafabet Sportsbook |

Leader |

Asia-focused sports betting operator with integrated sportsbook and peer-to-peer betting exchange |

|

Medium Rare N.V. |

Stake Sportsbook |

Leader |

Crypto-native sports betting and casino platform with community-driven engagement model |

Key players include Parimatch Group, AsianLogic Limited, and Medium Rare N.V., among others.

Key Company Profiles

Parimatch Group

Parimatch Group is an international sports betting and entertainment company headquartered in Limassol, Cyprus, founded in 1994. The group offers a wide range of online sports betting and gaming products through a mobile-first digital platform, with a strong focus on the Indian market through localized content, regional language support, and cricket-centric betting options.

- Product Portfolio: Parimatch Sportsbook covering pre-match and live betting across popular Indian sports including cricket, football, kabaddi, and tennis, along with a full online casino and support for Indian payment methods such as UPI and net banking.

- Strategic Focus: Deepening engagement in the Indian market through localized platform experiences, mobile-first product development, and expanding coverage across cricket, eSports, and other popular Indian sporting events.

AsianLogic Limited

AsianLogic Limited is a leading online and land-based gaming group with operations across several countries. The company manages several subsidiary brands, with Dafabet serving as its flagship sportsbook brand catering to the Indian market through dedicated cricket coverage and peer-to-peer exchange betting.

- Product Portfolio: Dafabet Sportsbook offering pre-match and live betting across major Indian and international sports.

- Strategic Focus: Growing its Indian user base through integrated sportsbook and exchange products, enhancing the live betting experience for cricket and football, and leveraging sports sponsorships to build brand trust among Indian bettors.

Medium Rare N.V.

Medium Rare N.V. is a Curaçao-registered online gaming company that operates the Stake brand, a fast-growing crypto-native sports betting and casino platform. The platform has been gaining traction in the Indian market by offering cryptocurrency-based transactions and a community-driven engagement model appealing to younger, digitally savvy Indian bettors.

- Product Portfolio: Stake Sportsbook offering pre-match and live betting on cricket, football, and other popular Indian sports.

- Strategic Focus: Scaling its crypto-native betting model in the Indian market, expanding cricket and eSports coverage, and leveraging blockchain-based transparency to build user trust among Indian sports betting enthusiasts.

Market Concentration Analysis

The India sports betting market is moderately concentrated, with the top three operators (Parimatch Group, AsianLogic Limited, and Medium Rare N.V.) accounting for a significant share of online sports betting activity through offshore platforms serving Indian users across cricket, football, and multi-sport formats.

Barriers to entry include high customer acquisition costs in a cricket-anchored market, the need for scalable real-time platforms, multi-state compliance capability, and the ability to navigate the evolving central framework. These factors favor well-capitalized incumbents with established user bases and diversified product portfolios.

Consolidation is accelerating as smaller players exit real-money formats and larger operators acquire content, technology, and adjacent capabilities. Strategic partnerships with sports leagues, media platforms, and payment providers are further reinforcing competitive positioning across the structured segments of the market.

Investment & Growth Opportunities

Fastest-Growing Segments

eSports betting at 9.3% share expands fastest among betting types, driven by formal recognition under recent legislation, growing tournament viewership, and a young, digitally engaged audience. Live/in-play betting at 16.7% is the next-fastest format, supported by real-time micro-markets, faster odds updates, and richer in-match wagering experiences.

Emerging Markets

South India at 26.3% is the fastest growing region, anchored by rapid digital adoption, expanding multi-sport interest, and rising tier-2 and tier-3 city participation. These markets represent significant untapped opportunity for operators able to deliver region-specific content and language-localized experiences.

Venture & Investment Trends

Investment is concentrated in free-to-play content platforms, eSports tournament operators, and sports media and creator ecosystems. Capital is also flowing into subscription-led and in-app purchase models that align with the post-2025 regulatory environment.

Future Market Outlook (2026-2034)

The India sports betting market is forecast to expand from USD 7.40 Billion in 2025 to USD 17.98 Billion by 2034 at a CAGR of 6.82%, adding roughly USD 10.58 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: a maturing central regulatory framework; the rise of live, in-play, and eSports formats; deeper integration with payments and content ecosystems; and the gradual reduction of unregulated and offshore activity through stricter enforcement.

By 2034, sports betting in India is expected to be defined by compliant, platform-led participation, with eSports and live or in-play formats collectively accounting for a significantly higher share of overall activity. Regulatory oversight, digital payment integration, and mobile-first engagement models are expected to further accelerate the evolution of formalized betting ecosystems.

Research Methodology

Primary Research

Primary research included structured interviews with platform executives, sports league commercial leads, payment service providers, regulatory specialists, and advertising agencies, validating market sizing, regional demand, platform mix, and betting type evolution.

Secondary Research

Secondary sources included Ministry of Electronics and Information Technology publications, parliamentary debates and bill texts for the Promotion and Regulation of Online Gaming Act, state-level gaming statutes, Reserve Bank of India digital payments data, and annual reports, press releases, and investor presentations from listed operators.

Forecasting Models

Market forecasts used top-down and bottom-up models combining digital sports user counts, average revenue per user, platform mix evolution, regulatory transition scenarios, and macroeconomic variables. Scenario analysis addressed regulatory pace, tax adjustments, and offshore market leakage.

India Sports Betting Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Platforms Covered | Offline, Online |

| Betting Types Covered | Fixed Odds Wagering, Exchange Betting, Live/In Play Betting, Pari-Mutuel, eSports Betting, Others |

| Sports Types Covered | Football, Basketball, Baseball, Horse Racing, Cricket, Hockey, Others |

| Regions Covered | South India, North India, West and Central India, East India |

| Companies Covered | Parimatch Group, AsianLogic Limited, Medium Rare N.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India sports betting market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India sports betting market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India sports betting industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Sports Betting Market Report

The India sports betting market was valued at USD 7.40 Billion in 2025, driven by digital sports engagement, smartphone penetration, and growing participation in skill-based formats.

The market is projected to grow at 6.82% CAGR from 2026 to 2034, reaching USD 17.98 Billion, supported by accelerating live or in-play betting adoption and expanding eSports participation.

Online leads at 80.0% in 2025, driven by smartphone penetration, UPI-led deposits, and integrated live data. Offline at 20.0% continues to serve horse racing and state-licensed channels.

Fixed odds wagering dominates at 35.2% in 2025, fueled by transparent returns and broad event coverage. eSports betting at 9.3% is the fastest-growing format.

North India commands 40.0% in 2025, led by dense cricket fan engagement, high digital adoption, and large urban populations.

Leading players include Parimatch Group, AsianLogic Limited, and Medium Rare N.V., among others.

The uniform GST levy on online gaming has reshaped operator pricing strategies and profit margins, prompting platforms to optimize cost structures, adjust user fee models, and explore value-added services to sustain competitiveness within the regulated environment.

Advances in AI, real-time data analytics, and blockchain-based transparency tools are enabling platforms to offer personalized experiences, faster odds updates, and enhanced fraud detection, raising overall trust and engagement across the ecosystem.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade