India Statcom Market Size, Share, Trends and Forecast by Rated Power, End User, and Region, 2026-2034

India Statcom Market Summary:

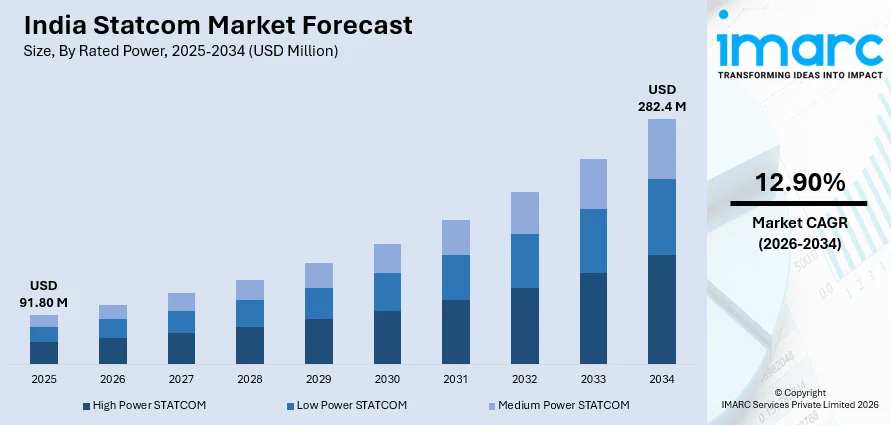

The India statcom market size was valued at USD 91.80 Million in 2025 and is projected to reach USD 282.4 Million by 2034, growing at a compound annual growth rate of 12.90% from 2026-2034.

The market is driven by the growing need for grid stability and reactive power compensation across India's expanding transmission and distribution infrastructure. Increasing integration of renewable energy sources, particularly solar and wind, is accelerating the deployment of advanced voltage regulation technologies. Government initiatives aimed at modernizing the national power grid and enhancing electricity access across rural and urban regions are further propelling demand, contributing to the India statcom market share.

Key Takeaways and Insights:

- By Rated Power: High power STATCOM dominates the market with a share of 48.7% in 2025, driven by its critical role in large-scale transmission networks requiring robust reactive power compensation and superior voltage stabilization.

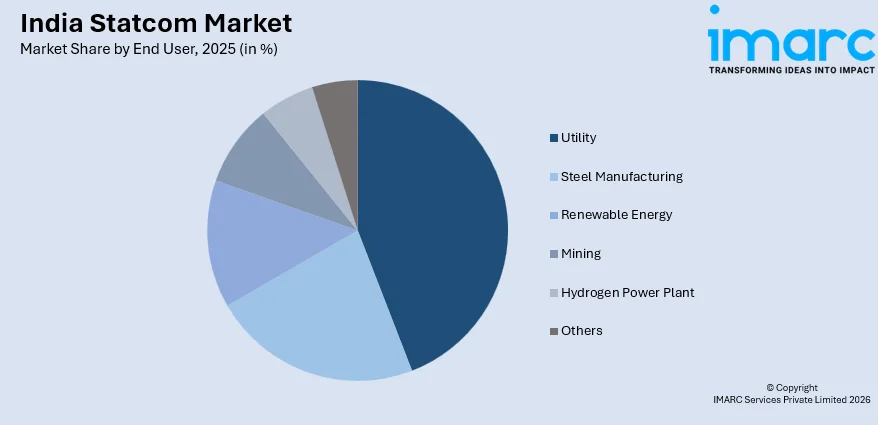

- By End User: Utility leads the market with a share of 44.9% in 2025, owing to extensive state and central transmission utilities undertaking grid modernization and regulatory mandates requiring enhanced voltage regulation.

- By Region: West India represents the market with a share of 36.5% in 2025, driven by the concentration of industrial corridors, major power transmission hubs, and significant renewable energy installations requiring advanced grid stabilization support.

- Key Players: The India statcom market features established global power electronics manufacturers competing alongside domestic electrical equipment providers, leveraging technological expertise, project execution capabilities, and strategic utility partnerships across transmission and industrial applications.

To get more information on this market Request Sample

The India statcom market is experiencing sustained growth driven by the country's ambitious plans to expand and modernize its power transmission infrastructure. The rapid integration of renewable energy sources, particularly solar and wind power, introduces intermittency and voltage fluctuation challenges that necessitate advanced reactive power compensation solutions. In June 2025, Siemens Energy reported plans to support India’s grid stability initiatives through the deployment of more than 50 STATCOM systems to manage renewable energy fluctuations and strengthen transmission reliability. Government-led initiatives focused on strengthening interstate transmission corridors and improving grid reliability across underserved regions are generating significant demand for statcom installations. The increasing electrification of industrial sectors, coupled with rising power consumption in urban centers, is placing additional strain on existing grid infrastructure, further driving the need for dynamic voltage regulation technologies. Regulatory frameworks mandating stricter power quality standards and grid code compliance are compelling utilities and industrial consumers to adopt statcom systems for enhanced grid performance and stability.

India Statcom Market Trends:

Rising Adoption of Modular Multilevel Converter Technology

The India statcom market is witnessing a notable shift toward modular multilevel converter-based designs that offer superior scalability, enhanced harmonic performance, and greater operational flexibility. These advanced topologies enable utilities and industrial operators to deploy compensation systems customized to specific grid requirements without extensive infrastructure modifications. In September 2025, Larsen & Toubro secured grid infrastructure orders that included STATCOM systems for 400 kV substations to deliver dynamic reactive power compensation and improve voltage stability in transmission networks. The modular architecture allows for easier maintenance and incremental capacity expansion, making it particularly attractive for applications where grid demands evolve over time, reshaping procurement preferences across transmission and distribution-level deployments.

Integration with Smart Grid and Digital Monitoring Platforms

Statcom systems are increasingly being integrated with advanced digital monitoring, real-time analytics, and smart grid communication platforms across India's power infrastructure. This trend enables remote diagnostics, predictive maintenance, and automated voltage regulation based on dynamic grid conditions. In April 2025, Gujarat Energy Transmission Corporation invited bids worth about ₹244.05 crore for installing a ±125 MVAR STATCOM at the 220 kV Sagapara substation to enhance grid stability and power quality. Utilities are leveraging these digitally enabled statcom installations to achieve greater operational efficiency, reduce response times to voltage disturbances, and optimize reactive power dispatch across complex transmission networks, transforming statcom systems from standalone compensators into interconnected grid management assets.

Growing Deployment in Renewable Energy Evacuation Corridors

India's expanding renewable energy evacuation infrastructure is driving dedicated statcom deployments along green energy transmission corridors connecting generation-rich regions to demand centers. These specialized installations address unique voltage stability challenges arising from large-scale intermittent power flows across long-distance transmission lines. As per sources, Power Grid Corporation of India secured a transmission project in Rajasthan that includes a 765/400 kV substation equipped with a STATCOM unit to support renewable energy evacuation from the region. The strategic placement of statcom systems at critical nodes along evacuation corridors ensures smoother power transfer, minimizes transmission losses, and maintains grid code compliance at interconnection points, reflecting the evolving role of statcom technology within India's renewable energy ecosystem.

Market Outlook 2026-2034:

The India statcom market revenue is projected to experience robust growth during the forecast period, driven by sustained investments in transmission infrastructure modernization and accelerating renewable energy integration across the national grid. Revenue expansion will be supported by increasing utility-scale deployments, rising industrial power quality requirements, and favorable regulatory frameworks mandating advanced reactive power compensation. The growing emphasis on grid resilience, coupled with the expansion of interstate and intrastate high-voltage transmission corridors, will generate sustained revenue opportunities. Technological advancements in converter designs and digital integration capabilities are expected to further enhance market revenue potential throughout the forecast period. The market generated a revenue of USD 91.80 Million in 2025 and is projected to reach a revenue of USD 282.4 Million by 2034, growing at a compound annual growth rate of 12.90% from 2026-2034.

India Statcom Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Rated Power |

High Power STATCOM |

48.7% |

|

End User |

Utility |

44.9% |

|

Region |

West India |

36.5% |

Rated Power Insights:

- Low Power STATCOM

- Medium Power STATCOM

- High Power STATCOM

High power STATCOM dominates with a market share of 48.7% of the total India statcom market in 2025.

The high power STATCOM commands the leading position in the India statcom market, driven by its indispensable role in large-scale transmission networks where substantial reactive power compensation is required. High-capacity statcom systems are deployed at critical substations along high-voltage transmission corridors to manage voltage stability across interstate power flows. The increasing complexity of India's transmission grid, resulting from the integration of diverse generation sources and rising cross-regional power exchanges, necessitates high-capacity compensation solutions capable of delivering rapid dynamic response across demanding operational environments.

The dominance of this segment is further reinforced by government-led transmission expansion programs that prioritize the strengthening of backbone infrastructure connecting renewable energy-rich states to major consumption centers. High power statcom units offer superior performance characteristics including wider operating ranges, faster response to grid disturbances, and greater capacity for managing reactive power demands during peak load conditions. The growing scale of individual transmission projects and the increasing voltage levels of new corridors continue to drive preferential adoption of high-power configurations across India's evolving grid landscape.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Utility

- Steel Manufacturing

- Renewable Energy

- Mining

- Hydrogen Power Plant

- Others

Utility leads with a share of 44.9% of the total India statcom market in 2025.

The utility holds the largest share in the India statcom market, reflecting the dominant role of central and state transmission utilities in driving statcom procurement and deployment. Utility operators are the primary consumers of statcom technology as they bear responsibility for maintaining voltage stability, power quality, and grid code compliance across extensive transmission and distribution networks. In November 2024, CERC granted a transmission licence to Powergrid Khavda IV-E2 for its 7 GW renewable energy evacuation project in Gujarat, enabling deployment of STATCOM systems at key pooling stations to support grid stability and reactive power management.

Utility driven demand is further strengthened by evolving grid code requirements that mandate enhanced voltage regulation capabilities at key network nodes. Transmission utilities are increasingly incorporating statcom systems into new substation designs and retrofitting existing facilities to address emerging stability challenges from variable renewable energy inflows. The centralized procurement processes of major transmission corporations enable large-volume deployments, while long-term grid development roadmaps provide sustained visibility for future statcom installations across both interstate and intrastate utility networks throughout India.

Regional Insights:

- North India

- South India

- East India

- West India

West India dominates with a market share of 36.5% of the total India statcom market in 2025.

West India leads the regional market, driven by the concentration of major industrial corridors, extensive transmission infrastructure, and significant renewable energy capacity installations across the region. States within western India host some of the country's most active power transmission hubs, where statcom systems are essential for maintaining voltage stability amid heavy industrial loads and variable renewable energy generation. The region's advanced grid infrastructure and higher power consumption patterns create favorable conditions for widespread statcom deployment across utility and industrial applications.

The region's dominance is further supported by substantial investments in wind and solar energy projects that require dedicated grid stabilization solutions at evacuation points and interconnection substations. Western India benefits from the presence of well-established utility infrastructure, proactive state-level energy policies, and a higher density of high-voltage transmission corridors connecting generation assets to major urban and industrial demand centers. These structural advantages position the region as the primary market for statcom technology adoption across both utility and industrial applications in India.

Market Dynamics:

Growth Drivers:

Why is the India Statcom Market Growing?

Accelerating Renewable Energy Integration Across the National Grid

India's ambitious clean energy transition is creating unprecedented demand for statcom technology as the power grid accommodates increasing volumes of intermittent renewable generation. Solar and wind power plants introduce voltage fluctuations and reactive power imbalances that conventional compensation equipment cannot effectively address. In May 2025, Gujarat’s third Green Energy Corridor plan included installation of four STATCOM units across high‑voltage substations to maintain grid quality while transmitting 16,500 MW of renewable power. Statcom systems provide the rapid dynamic response necessary to stabilize voltage levels at points of renewable energy interconnection, ensuring seamless power delivery across transmission networks. The government's commitment to expanding renewable capacity across multiple states is driving sustained statcom deployments nationwide.

Large-Scale Transmission Infrastructure Modernization Programs

India is undertaking extensive transmission infrastructure expansion and modernization to accommodate rising electricity demand and facilitate inter-regional power transfers. National programs aimed at strengthening high-voltage corridors, building new substations, and upgrading existing transmission facilities are generating significant procurement opportunities for statcom systems. The growing complexity of the transmission network, with increasing cross-regional power flows and higher voltage levels, necessitates advanced reactive power compensation to maintain system stability. Statcom technology is being embedded into new transmission project designs as a standard component for reliable power delivery.

Evolving Regulatory Standards for Grid Stability and Power Quality

Regulatory frameworks governing grid operations in India are becoming increasingly stringent regarding voltage stability, reactive power management, and power quality standards. Updated grid codes require generating stations and transmission operators to meet enhanced operational benchmarks for reactive power compensation and frequency stability. In November 2025, India’s power regulator warned solar and wind generators of possible grid disconnection for repeated violations of technical standards, including voltage stability and ride‑through norms under the Indian Electricity Grid Code. These regulatory mandates are compelling utilities and industrial consumers to invest in advanced statcom systems capable of meeting compliance requirements. The regulatory push extends to both new installations and retrofitting of existing substations, creating broad-based demand across the entire transmission and distribution landscape.

Market Restraints:

What Challenges the India Statcom Market is Facing?

High Capital Investment and Extended Payback Periods

Statcom systems require substantial upfront capital investment encompassing advanced power electronics, control systems, civil infrastructure, and specialized installation expertise. The significant initial expenditure poses a considerable barrier for smaller utilities and industrial operators with constrained capital budgets. The extended payback periods associated with these installations can discourage investment, particularly in regions where grid stability challenges are perceived as manageable.

Limited Availability of Specialized Technical Expertise

The deployment and maintenance of statcom systems demand highly specialized technical expertise in power electronics, control engineering, and grid integration that remains scarce across India. The shortage of qualified engineers and technicians capable of designing, commissioning, and maintaining complex statcom installations creates bottlenecks in project execution timelines. These skills gap also increases operational and maintenance costs significantly.

Competition for Alternative Reactive Power Compensation Technologies

The India statcom market faces competitive pressure from alternative compensation technologies including mechanically switched capacitor banks, static VAR compensators, and synchronous condensers that offer lower initial costs for specific grid applications. These conventional technologies retain appeal among cost-sensitive operators managing less demanding voltage stability requirements, potentially limiting statcom penetration in segments where rapid dynamic response is not essential.

Competitive Landscape:

The India statcom market competitive landscape is characterized by the participation of established global power electronics manufacturers alongside domestic electrical equipment providers competing across utility-scale and industrial segments. Market participants differentiate through technological capabilities, project execution track records, and after-sales service networks spanning India's geographically diverse regions. Strategic partnerships between international technology providers and domestic engineering firms facilitate market access and enable localized manufacturing, enhancing cost competitiveness. The competitive environment is shaped by large-scale government procurement processes that favor participants with proven technical expertise and established supply chain capabilities. Domestic players are increasingly investing in indigenous technology development and manufacturing capabilities to strengthen their market positioning against international competitors.

India Statcom Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Rated Powers Covered |

Low Power STATCOM, Medium Power STATCOM, High Power STATCOM |

|

End Users Covered |

Utility, Steel Manufacturing, Renewable Energy, Mining, Hydrogen Power Plant, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India statcom market size was valued at USD 91.80 Million in 2025.

The India statcom market is expected to grow at a compound annual growth rate of 12.90% from 2026-2034 to reach USD 282.4 Million by 2034.

High power STATCOM held the largest share, driven by its essential deployment in high-voltage transmission corridors, interstate power exchange substations, and large-scale renewable energy evacuation infrastructure requiring substantial reactive power compensation capabilities.

Key factors driving the India statcom market include accelerating renewable energy integration requiring grid stabilization, large-scale transmission infrastructure modernization programs, evolving regulatory standards mandating enhanced reactive power compensation, and rising industrial power quality requirements.

Major challenges include high capital investment requirements, extended project payback periods, limited availability of specialized technical expertise, competition from lower-cost conventional compensation technologies, complex procurement processes, and infrastructure constraints in remote deployment locations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)