India Steel Market Size, Share, Trends and Forecast by Type, Product, Application, and Region, 2026-2034

India Steel Market Size & Forecast 2026-2034

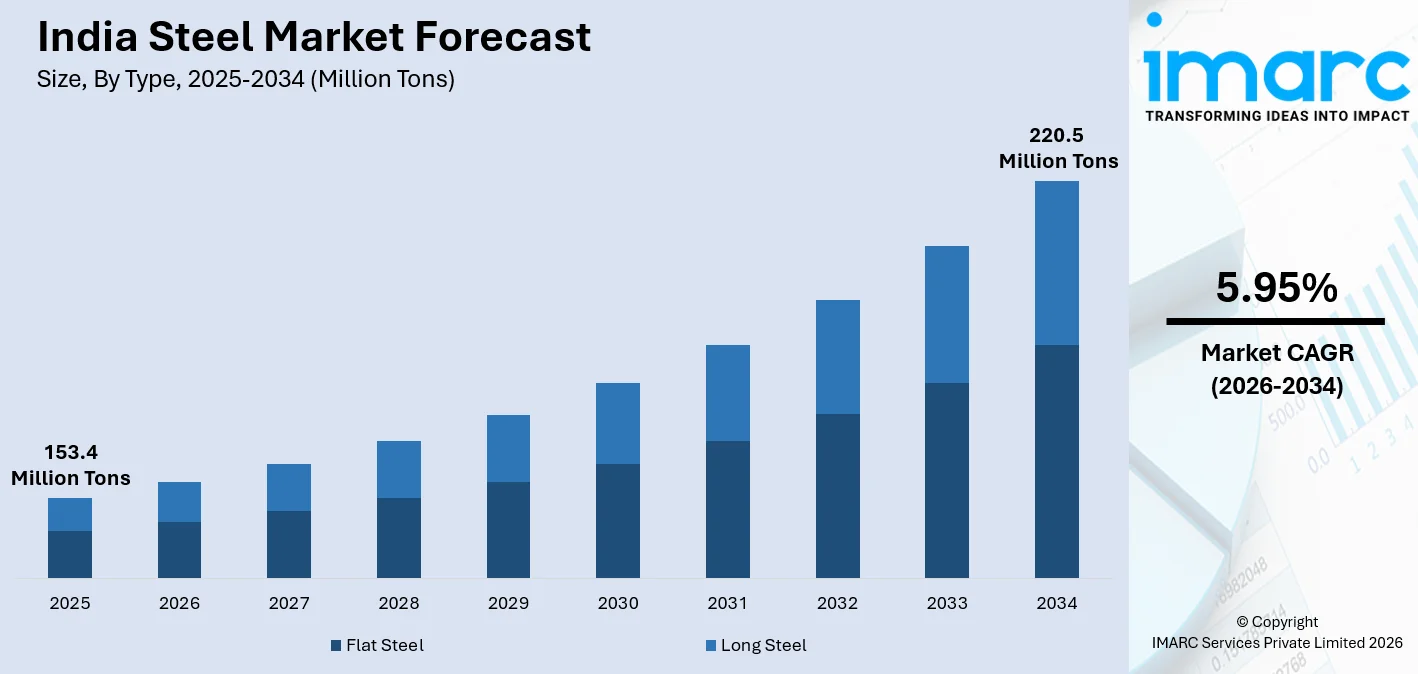

India steel market size was volumed at 153.4 Million Tons in 2025, and it is expected to reach 220.5 Million Tons by 2034, with a compound annual growth rate (CAGR) of 5.95% during 2026-2034. India has established itself as the world’s second-largest steel-producing nation with a raw steel output of more than 144.3 million tonnes in the last financial year of 2023-24. The steel sector is growing due to the large amounts of government expenditure on infrastructure. The government has planned to spend ₹12.2 lakh crore on capital expenditure for the financial year 2026-27. A large part of this is invested in steel-intensive projects like the construction of roads, railways, bridges, and urban metro projects. The automobile sector is the second-largest steel-consuming sector in India. The sector produced more than 28 million vehicles in the last financial year of 2024-25. This has ensured the demand for flat steel products like cold rolled and galvanized sheets.

To get more information on this market Request Sample

India Steel Industry Analysis: Key Insights

- Flat Steel captured a significant 54.2% of the market share by type in 2025. This can be attributed to the flourishing automotive industry, which dispatched over 28 million vehicles during the financial year 2024-25. Additionally, coated steel used for roofing, cladding, and structural components maintained the high demand for the material in the construction of the country’s infrastructure.

- Structural Steel accounted for a significant 33.6% of the market share by product in 2025. This can be attributed to the hefty capital outlay of ₹12.2 lakh crore by the government for the financial year 2026-27. The segment can also be attributed to the ongoing metro rail projects as well as the Delhi-Mumbai Industrial Corridor project.

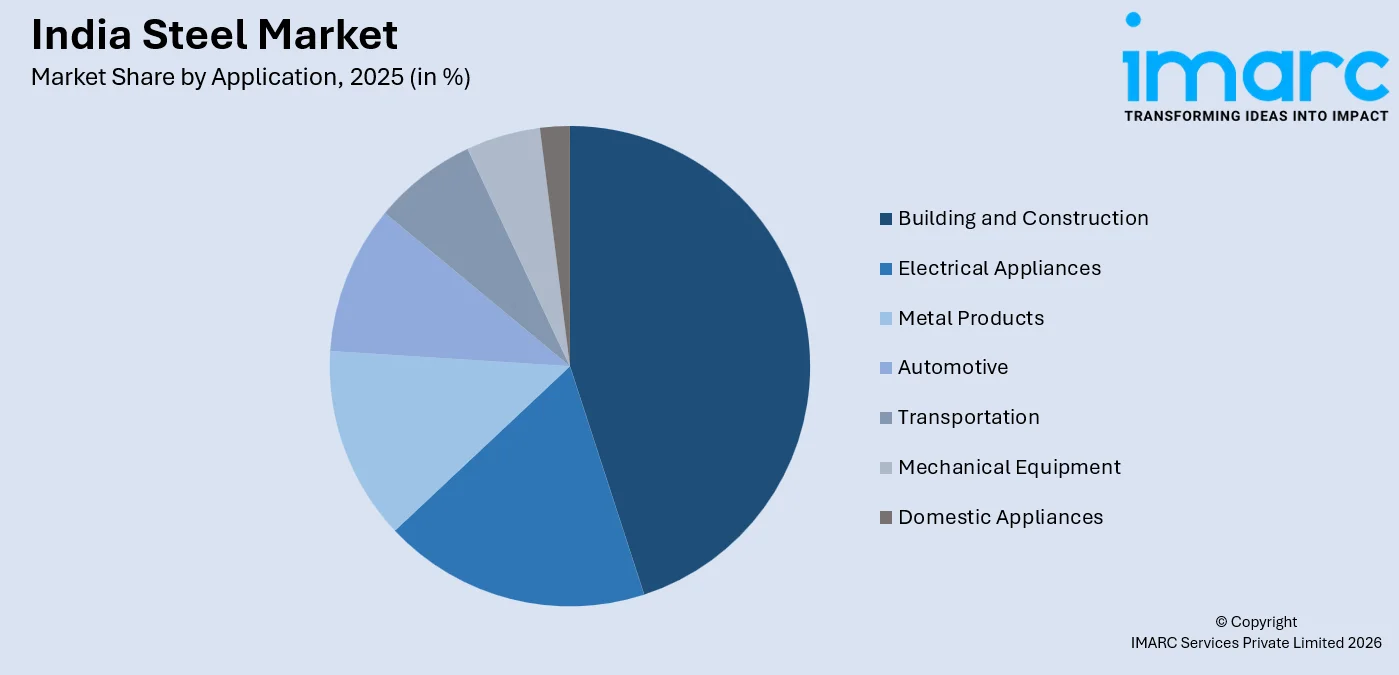

- The Building & Construction accounted for a significant 41.9% of the market share by application in 2025. This can be attributed to the Pradhan Mantri Awas Yojana project, which aims to develop over 2 crores of houses in rural and urban areas. This project is complemented by the construction of commercial properties in the metropolitan areas of the country.

- The West & Central India accounted for the largest market share of 34.7% by region in 2025. This can be attributed to the substantial integrated steel production capacity of the states of Chhattisgarh and Madhya Pradesh. Additionally, the region can be attributed to the substantial downstream demand of the automotive industry located around the city of Pune as well as Aurangabad.

India Steel Market Trends and Dynamics 2026:

Market Trends

Green Steel and Decarbonization Investments Gaining Momentum

The transition towards green steel is coming up as a key structural theme in the India steel market. The India steel market ranks among the most carbon-intensive industries in the country, contributing approximately 8% of total industrial CO₂ emissions. In response to both local regulatory needs and foreign market demands, key companies in the market have started outlining their decarbonization strategies. Tata Steel has pledged a goal of cutting its carbon intensity to 1.8 tonnes of CO₂ per tonne of steel by 2030, while JSW Steel has pledged a hydrogen-based steel production strategy for some plants.

Rapid Expansion of Electric Arc Furnace Capacity Driven by Scrap Availability

India’s electric arc furnace (EAF) industry is growing at a faster rate than the growth rate of the country’s integrated blast furnace industry. The government introduced a new vehicle scrapping policy, which is being implemented gradually since 2021, which is expected to produce millions of tons of scrap by the end of the decade. The growth of EAF melting capacity is also seen in western and central India. Secondary steel producers have increased EAF melting capacity to balance the steel production evenly.

Import Substitution Accelerating in Specialty and High-Grade Steel

India still has a major requirement for specialty steel products like stainless steel, electrical steel, high-alloy steels, etc., with the consumption of finished steel standing at 92.50 MT in FY26 (April-October 2025). To bridge this ongoing requirement gap for specialty steel, the government has linked a production-linked incentive scheme for specialty steel. This scheme has five segments including coated steel products, high strength steel products, specialty rails, alloy steel bars/rods, and electrical steel, with a total outlay of ₹6,322 crore.

Growth Drivers

Record government capital expenditure sustaining construction-led steel demand

The Indian government has consistently increased its capex over the past few years. In fact, the budget for FY 2026-27 has allocated ₹12.2 lakh crores for infrastructure development. This is over three times the amount spent on infrastructure development during FY 2019-20. Road development alone requires millions of tonnes of steel material every year. In addition, the Indian railway modernization drive, which includes the development of Vande Bharat trains and the freight corridor, continues to fuel the demand for structural steel products.

Automotive sector recovery and electric vehicle transition creating new steel demand profiles

The automobile sector in India produced 28.4 million vehicles in FY 2024-25. Passenger cars sold a record 4.3 million units. As electric vehicles increasingly drive the market; these cars are changing the type of steel in cars. EVs require high-strength steels for lighter body and battery enclosures. Non-grain-oriented electrical steels are also required for motors and generators.

Rising financial awareness and infrastructure ambition driving long-term demand

The urban population in India is growing and is expected to reach 630 million by 2030. This means that a constant and structural demand will exist for housing, commercial space, and infrastructure, thereby supporting a strong demand for steel in the coming years. In addition, apart from demand for housing, automobiles, and infrastructure, initiatives like smart cities, logistics policy, and port development are opening up more demand avenues for both flat and structural steel products.

- National Monetization Pipeline: The government’s asset monetization initiative is expected to attract private sector investments in assets worth ₹5.8 lakh crore in the near term, leading to new construction activity and steel demand.

- Defence and Aerospace Indigenization: The push to increase domestic procurement in the defence sector to 75% is leading to an increase in the demand for special steel grades used in the manufacture of defence equipment, ships, and aerospace.

- Make in India and PLI Schemes: The beneficiaries of the PLI schemes for the electronics, machinery, and consumer durables sectors are expanding domestic manufacturing facilities, leading to new demand for flat steel products for the construction of equipment.

Market Restraints

Coking Coal Import Dependency and Input Cost Volatility: Steel production in India is highly dependent on coking coal imports, as the availability of coking coal in India is limited in terms of both quantity and quality. This makes the industry vulnerable to fluctuations in coking coal prices, which in turn makes the production cost more volatile in nature. When faced with a dip in international steel prices, these increased production costs affect the profit margins of integrated steel players in India.

Competition from Low-Cost Steel Imports, Especially from China: Low-cost imports, especially from China, are a challenge for steel players in India, as China is currently in a state of oversupply, causing a dip in their export prices, attracting price-conscious buyers in India as well. While the government does impose safeguard and anti-dumping duties on these imports from time to time, the uncertainty about their continuation makes things difficult for steel players in India.

High Logistics Costs Constraining Competitiveness: Another challenge faced by the Indian steel industry is its logistics cost, as plants in the eastern part of India, where most of the raw materials are available, are located far from demand centers, resulting in a high logistics cost for transporting finished products to reach demand centers on time.

India Steel Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

|

Type |

Flat Steel |

54.2% |

2025 |

|

Product |

Structural Steel |

33.6% |

2025 |

|

Application |

Building and Construction |

41.9% |

2025 |

|

Region |

West & Central India |

34.7% |

2025 |

Type Insights

Flat Steel- 54.2% Market Share (2025) | Leading Type

Flat products are the backbone of the Indian steel consumption pattern. This segment accounts for 54.2% of the Indian steel market in 2025. This includes hot rolled coils, cold rolled sheets, galvanized products, color coated coils, and stainless-steel flat products. Among all the segments of the automotive industry, the automotive segment uses the largest volume of steel products. This includes both passenger vehicles as well as commercial vehicles. The automotive industry uses large volumes of cold rolled flat products as well as coated products.

|

Segment Breakdown Flat Steel (54.2%) · Long Steel |

Product Insights

Structural Steel- 33.6% Market Share (2025) | Leading Product

The largest segment of the Indian steel market is the structural steel segment. This accounts for 33.6% of the Indian steel market in 2025. This is mainly due to large infrastructure projects as well as the rapid development of industrial as well as commercial properties. This includes a variety of products such as beams, columns, channels, angles, hollow sections, and plates. This is the main load-bearing component of steel-intensive construction. One of the major volume drivers of the structural steel segments is the metro rail project of the Indian government. This now covers 24 cities and the network is over 1,036 km long.

|

Segment Breakdown Structural Steel (33.6%) · Prestressing Steel · Bright Steel · Welding Wire and Rod · Iron Steel Wire · Ropes · Braids |

Application Insights

Access the comprehensive market breakdown Request Sample

Building and Construction- 41.9% Market Share (2025) | Leading Application

Building and Construction is the leading steel-consuming sector in India, with a total domestic steel demand of 41.9% in 2025. The steel products consumed in the sector vary from a wide range of products that include TMT products and re-bars for RCC constructions, steel sections for steel frame constructions, flat products for roofing and claddings, to pre-engineered buildings for industrial and warehousing sectors. The Pradhan Mantri Awas Yojana scheme has been successful in sanctioning more than 4 crore houses under the rural and urban housing schemes. This has helped create a base demand for long products for residential constructions in tier 2 and tier 3 cities.

|

Segment Breakdown Building and Construction (41.9%) · Electrical Appliances · Metal Products · Automotive · Transportation · Mechanical Equipment · Domestic Appliances |

Regional Insights

West & Central India- 34.7% Market Share (2025) | Leading Region

West and Central India leads the pack with a total steel market share of 34.7% in India in 2025. This is due to the presence of large steel manufacturing facilities as well as large steel-consuming industries. The region is home to large steel manufacturers like JSW Steel Limited's 13 million tonne-per-annum Vijayanagar steel plant in Karnataka State, which is near the west-central region. The region is also home to large secondary steel manufacturers like the ones in Maharashtra, Chhattisgarh, and Madhya Pradesh.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 34.7% |

| Major States | Maharashtra, Gujarat, Chhattisgarh, Madhya Pradesh, Goa |

| Key Growth Drivers | Diversified manufacturing base, large automotive and engineering sector concentration, strong port connectivity via JNPT and Mundra, significant integrated steel production within the region |

| Outlook | Sustained leadership through manufacturing corridor development and continued infrastructure spending in Maharashtra and Gujarat |

|

Segment Breakdown West & Central India (34.7%) · North India · South India · East India |

North India:

North India is an important steel-consuming area that is witnessing increasing demand, where major construction centers are located in Uttar Pradesh, Haryana, Punjab, and Delhi NCR regions. The Delhi NCR region is one of the largest steel-consuming centers, where a strong demand for steel structures, as well as flat products, is witnessed owing to ongoing commercial property development, expansion of metro lines, and substantial investments in data centers.

|

Metric

|

Details

|

|---|---|

| Major States | Uttar Pradesh, Delhi NCR, Haryana, Punjab, Uttarakhand |

| Key Growth Drivers | Large population base, Uttar Pradesh expressway and infrastructure investments, expanding logistics parks, rising commercial real estate activity |

| Outlook | Strong growth anchored by Uttar Pradesh’s accelerating infrastructure investment and sustained construction demand in Delhi NCR |

South India:

South India is another structurally important steel-consuming area where demand is coming from industries like IT services, automotive, petrochemicals, etc., located in this region. The Chennai-Bengaluru industrial corridor is home to a cluster of automotive manufacturers including Hyundai, Toyota, Kia, BMW, etc., who have established automobile manufacturing units, making this region one of the largest steel-consuming centers for flat products in the country.

|

Metric

|

Details

|

|---|---|

| Major States | Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala |

| Key Growth Drivers | Strong automotive sector, IT infrastructure development, port-led industrial activity, growing urban real estate demand in Bengaluru and Hyderabad |

| Outlook | Continued growth supported by automotive corridor expansion and urban development in Bengaluru, Chennai, and Hyderabad |

East India:

East India is referred to as the steel capital of India, where the highest concentration of primary steel manufacturing units is located. This region accounts for the highest crude steel production of the country, where Odisha, Jharkhand, and West Bengal together contribute a substantial portion of the country's total crude steel production capacity, where major steel manufacturing units are located for industry players including SAIL, Tata Steel, JSW Steel, RINL, etc. This region also enjoys the proximity of high-grade iron ore mines located in Keonjhar, Sundargarh, Singhbhum districts of Odisha.

|

Metric

|

Details

|

|---|---|

| Major States | Odisha, Jharkhand, West Bengal, Assam, Bihar |

| Key Growth Drivers | Proximity to iron ore reserves, expanding steel production capacity, growing port and logistics infrastructure, rising construction activity in Bhubaneswar and Kolkata |

| Outlook | Strong production base with improving local consumption as industrial and infrastructure investment accelerates across the region |

Market Outlook (2026-2034)

What is the future outlook of the India steel market?

The India Steel market is expected to sustain steady volume growth through 2034

The Indian steel industry is expected to grow steadily over the period until 2034, with upgrades in infrastructure, urbanization, and industrial growth. The investments made by the government in transportation, housing, renewable energy, and industrial corridors are expected to create a robust market for steel products. Add to that the impetus provided by the domestic manufacturing drive, as well as the capacity expansions undertaken by steelmakers, to create a robust supply side for the industry. Also, the increasing demand from the automobile, capital goods, and infrastructure sectors, as well as the modernization of logistics and production technology, are expected to boost the growth of the Indian steel industry over the longer term, thereby cementing its position as a growth driver for the country.

India Steel Market: Leading Key Players

The India steel market is dominated by a small group of large integrated steelmakers who collectively command a majority share in India’s domestic crude steel production. The rest is a highly fragmented secondary market comprising hundreds of electric arc furnace-based operators. The main competition areas are sustaining quality in the product mix, delivery commitments, prices, and technical support. The high-end segments, such as automotive and coated flat products, offer relatively higher margins. Many domestic operators are also investing in downstream activities such as setting up service centers, cut-to-length lines, and blanking operations to capture greater value and build deeper relationships.

| Company | Leading Brands/Products | Highlights |

|---|---|---|

|

Steel Authority of India Limited (SAIL) |

SAIL TMT Bars, HR Coils, Structural Sections, Rails, Plates |

India’s largest state-owned integrated producer with a total crude steel capacity of approximately 19.17 million tonnes per annum across five integrated plants; dominant supplier to railways, defence, and public infrastructure projects with a significant presence in eastern and central India |

|

JSW Steel Limited |

JSW Neo Steel TMT Bars, Galvano, Color Coated Sheets, HR/CR Coils, JSW Pragati |

India’s largest private sector steel producer with total capacity approaching 28 million tonnes per annum; strong position in flat products with major hot strip mills at Vijayanagar and Dolvi; aggressive capacity expansion targeting 50 million tonnes per annum by 2030 |

|

Tata Steel Limited |

Tata Tiscon, Tata Structura, Tata Shaktee, Tata Steelium, Tata Wiron |

One of India’s most diversified steel producers with integrated operations at Jamshedpur and Kalinganagar; strong brand recognition in automotive, construction, and retail segments; leading sustainability commitments targeting net-zero by 2045 |

Other major key players in the India Steel market include Jindal Steel and Power Limited (JSPL), Rashtriya Ispat Nigam Limited (RINL/Vizag Steel), APL Apollo Tubes Limited, Bhushan Power & Steel, Shyam Steel Industries Limited, Jindal Stainless Limited, Essar Steel India Limited, and Uttam Galva Steels Limited.

Latest Development & News:

- In January 2026, JSW Steel announced its proposal to accelerate its capacity expansion to 50 million tonnes a year till 2030. The steelmaker has confirmed its investments in the Dolvi plant in Maharashtra as well as a new greenfield project in Odisha. This is with an estimated investment of over 2 lakh crore to be spent over the next five years. This is considered to be one of the largest single investments in the steel sector in India.

- In October 2025, Jindal (India), which is a part of the BC Jindal Group, a manufacturer of downstream steel products, has commissioned 0.6 million metric tons of additional downstream steel capacity at its plants in West Bengal. The launch of the cold rolling complex marks the near completion of the expansion project.

- In May 2025, Tata Steel India has announced its plans to increase the hot strip mill capacity at Kalinganagar in the state of Odisha. This is to increase the production capacity of flat products intended for the automotive and packaging industries. The Kalinganagar plant is being developed to have an integrated steel plant capacity of 8 million tons annually. This plant will have finishing facilities for high-grade flat products.

India Steel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Flat Steel, Long Steel |

| Products Covered | Structural Steel, Prestressing Steel, Bright Steel, Welding Wire and Rod, Iron Steel Wire, Ropes, Braids |

| Applications Covered | Building and Construction, Electrical Appliances, Metal Products, Automotive, Transportation, Mechanical Equipment, Domestic Appliances |

| Regions Covered | South India, North India, West and Central India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India steel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India steel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India steel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Steel Market Report

The India steel market is volumed at 153.4 Million Tons in 2025. India is the second-largest steel-producing and consuming nation in the world.

The India steel market is expected to reach 220.5 Million Tons by 2034. The India steel market is expected to grow at a CAGR of 5.95% from 2026 to 2034.

Flat steel is leading the India steel market with a market share of 54.2% in 2025. This is because the India steel market is leading due to the large demand from the automobile industry. The automobile industry is producing over 28 million vehicles in FY 2024-25.

Structural steel is leading the product segment with a market share of 33.6% in 2025. This is because the product is inevitable for the construction of bridges, metro rails, commercial buildings, etc. The government has planned to extend the metro rail across 27 cities. Additionally, the government has planned to extend the airport across 100 cities.

The largest segment in the India steel market in terms of applications is Building and Construction, which accounts for 41.9% in 2025. The growth in Building and Construction is due to the capital expenditure by the government for FY 2025-26 amounting to ?11.1 lakh crore, affordable housing for over 4 crore houses, and commercial and industrial development in cities like Mumbai and Tier 2 cities.

The largest segment in the India steel market in terms of regions is West and Central India, which accounts for 34.7% in 2025. The growth in West and Central India is due to a high concentration of both steel production and industrial demand. The region comprises the state of Maharashtra’s automotive sector, the state of Gujarat’s engineering and chemical sector, and the state of Chhattisgarh’s integrated steel sector.

The key drivers for the India steel market include the record infrastructure spending by the government, the growth in the automobile sector, urbanization in India that is expected to touch 600 million by 2030, industrial capacity expansion through PLI schemes, and renewable energy infrastructure development.

The India steel market faces various challenges, including cost volatility of imported raw materials due to dependence on 55-60 million tonnes of imported coking coal every year, competition from Chinese exports that are sold at USD 50-100 per tonne lower than domestic steel, high logistics costs that are currently at 13-14 percent of India's GDP, and the financial and technical challenge of adopting greener technologies that are of lower carbon content.

The major players of the India steel market are Steel Authority of India Limited (SAIL), JSW Steel Limited, Tata Steel Limited, Jindal Steel and Power Limited, Rashtriya Ispat Nigam Limited (RINL), APL Apollo Tubes, Bhushan Power & Steel, and Jindal Stainless Limited.

The India steel market is expected to grow steadily over the coming years till 2034, registering a CAGR of 5.95 percent. The country is witnessing development of infrastructures under the National Infrastructure Pipeline, expansion of automotive and manufacturing industries, increasing urbanization, and a gradual shift towards higher value-added specialty steels and coated products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)