India Supercapacitor Market Size, Share, Trends and Forecast by Product Type, Module Type, Material Type, End Use Industry, and Region, 2026-2034

India Supercapacitor Market Size, Share, Trends & Forecast (2026-2034)

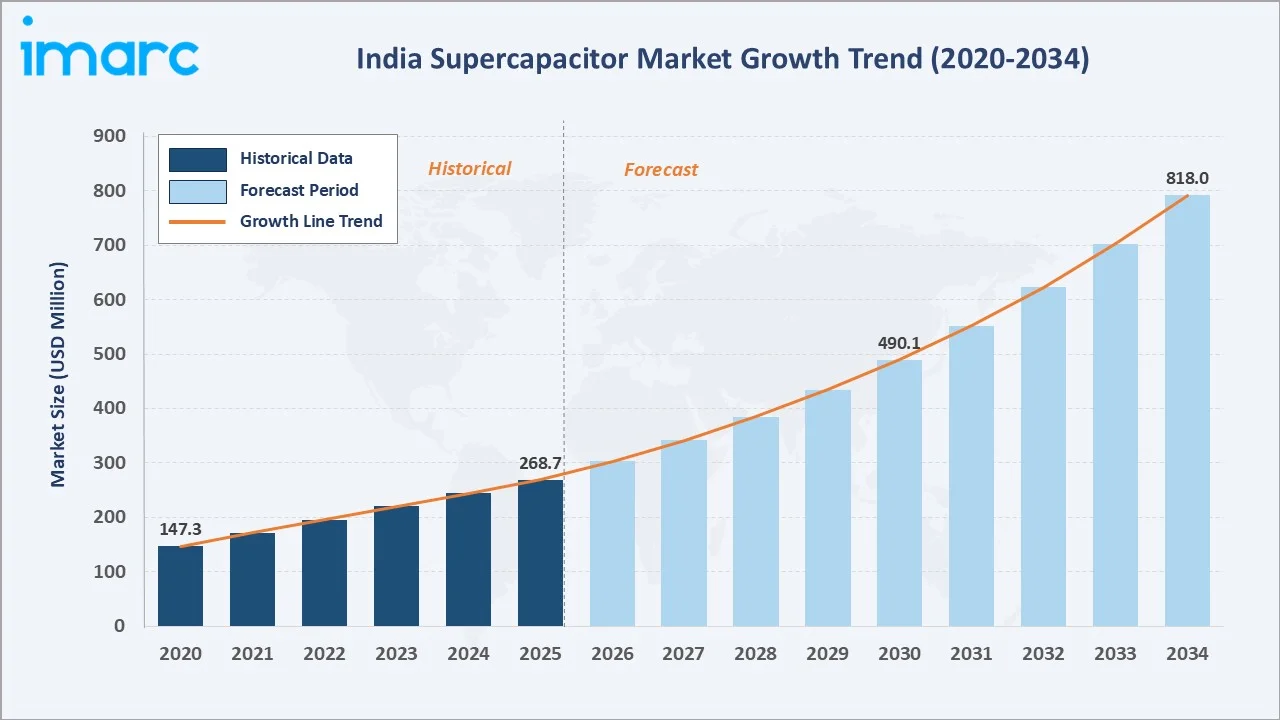

The India supercapacitor market reached USD 268.7 Million in 2025 and is projected to reach USD 818.0 Million by 2034, growing at a CAGR of 12.77% during 2026-2034. The market is driven by rising demand for fast-charging, high-power energy storage in electric vehicles, renewable energy systems, consumer electronics, and industrial backup power. Growing EV adoption, grid modernization, and clean energy investments are further supporting market growth. India aims to increase EV adoption by 2030, targeting EVs to account for 30% of private cars, 70% of commercial vehicles, 40% of buses, and 80% of two- and three-wheelers, equal to nearly 80 million EVs on the road. This is driving the market by increasing demand for fast-charging, high-power energy storage solutions used in EV acceleration, regenerative braking, battery support, and power stabilization systems. Electric double-layered capacitors (EDLC) dominate at 46.2%. Carbon and metal oxide lead material type at 49.6%. West and Central India commands 32.8% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 268.7 Million |

|

Forecast Market Size (2034) |

USD 818.0 Million |

|

CAGR (2026-2034) |

12.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

| Dominant Product Type |

Electric Double-Layered Capacitors (46.2%, 2025) |

| Dominant Material Type |

Carbon and Metal Oxide (49.6%, 2025) |

India's supercapacitor market expanded from USD 147.3 Million in 2020 to USD 268.7 Million in 2025, anchored at USD 490.1 Million in 2030, and forecast to reach USD 818.0 Million by 2034. COVID-19 created demand for the market by accelerating the adoption of medical devices, backup power systems, and digital infrastructure that require reliable and rapid energy storage solutions.

To get more information on this market, Request Sample

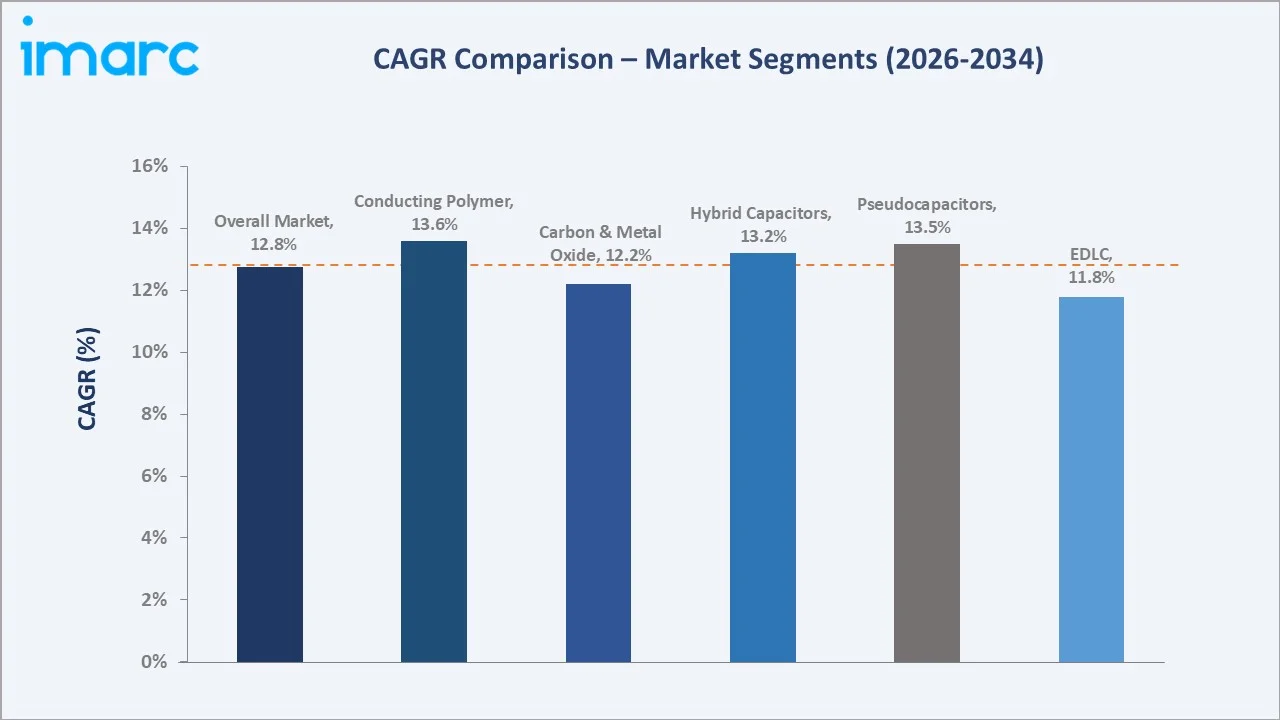

Conducting polymer materials grow fastest at ~13.6% CAGR through pseudocapacitor electrode advancement. Pseudocapacitors at ~13.5% CAGR reflect metal oxide electrode adoption in high-energy-density power applications for defense and EV fast-charge, where energy density limitation necessitates pseudocapacitor substitution.

Executive Summary

India's supercapacitor market reached USD 268.7 Million in 2025, representing one of the world's most commercially dynamic emerging supercapacitor markets. Supercapacitors are the electrochemical energy storage devices combining the high power density of conventional capacitors with the energy storage capability of batteries, bridging the performance gap between instant-discharge conventional capacitors and slow-discharge batteries, creating commercial utility in applications requiring high-power short-duration energy delivery that batteries cannot efficiently serve. The market is projected to reach USD 818.0 Million by 2034.

Electric double-layered capacitors at 46.2% lead through commercial maturity. Carbon and metal oxide at 49.6% anchors through activated carbon commercial scale, while metal oxide pseudocapacitor electrode growth creates above-market material demand expansion. West and Central India, at 32.8%, leads through Maharashtra and Gujarat's EV manufacturing, renewable energy, and industrial power quality application concentration.

Key Market Insights

|

Insight |

Data |

| Dominant Product Type | Electric Double-Layered Capacitors - 46.2% share (2025) |

| Dominant Material Type | Carbon and Metal Oxide - 49.6% market share (2025) |

| Leading Region | West and Central India - 32.8% |

| Market Opportunity | PM e-Bus electric bus supercapacitor packs; renewable energy grid frequency stabilization; metro rail regenerative braking; 5G telecom backup power; smart grid power systems |

Key Analytical Observations Supporting The Above Data:

- Electric Double-Layered Capacitors at 46.2%: The electric double-layered capacitors dominate due to their high-power density, fast charge-discharge capability, long cycle life, and strong suitability for EVs, consumer electronics, industrial backup systems, and renewable energy applications. Its lower maintenance needs and commercial maturity make it widely preferred over other supercapacitor types.

- Carbon and Metal Oxide at 49.6%: The carbon and metal oxide dominate as carbon materials offer high surface area, strong conductivity, and cost-effective energy storage performance. Metal oxides further improve capacitance and energy density, making the combination suitable for EVs, renewable energy storage, industrial electronics, and backup power applications.

- West and Central India at 32.8%: West and Central India dominate due to their strong base of automotive, electronics, renewable energy, and industrial manufacturing clusters across Maharashtra, Gujarat, and Madhya Pradesh. The region’s EV ecosystem, battery component investments, and large industrial power backup demand further support supercapacitor adoption.

India Supercapacitor Market Overview

India's supercapacitor market operates at the intersection of the world's most commercially ambitious electric vehicle transition, the world's fastest renewable energy capacity addition, and the Make in India initiative, creating manufacturing investment across the entire electronics value chain, including advanced energy storage components. Supercapacitors in India serve commercial applications across five primary sectors: transportation, renewable energy, industrial, defense, and consumer electronics.

The Indian supercapacitor ecosystem integrates imported electrode material suppliers, imported cell manufacturers distributed through authorized Indian electronics distributors, domestic system integrators, government research institutions, and end-user organizations, creating structured government-funded supercapacitor demand above commercial market dynamics. Macroeconomic factors include rapid EV adoption, renewable energy expansion, grid modernization, and growing investments in domestic electronics and energy storage manufacturing.

Market Dynamics

To evaluate market opportunities, Request Sample

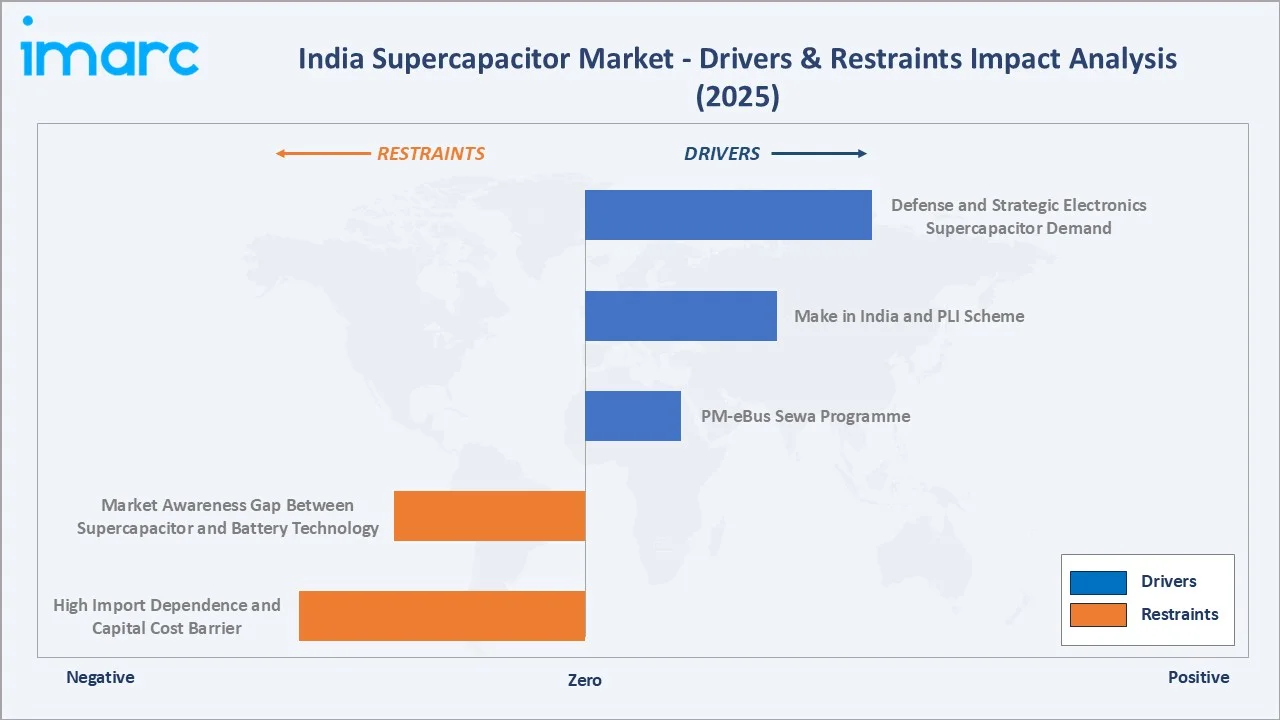

Market Drivers

- PM-eBus Sewa Programme: The Union Cabinet approved the PM-eBus Sewa scheme to deploy 10,000 electric buses across urban areas under a Public-Private Partnership model. The scheme has an estimated outlay of Rs. 57,613 crores, including Rs. 20,000 crores in central government support. This PM-eBus Sewa programme is accelerating the deployment of electric buses across Indian cities, creating demand for high-power energy storage solutions. Supercapacitors support e-buses through rapid charging, regenerative braking, power stabilization, and reduced battery stress. As public transport electrification expands, the need for durable, fast-response energy storage systems is increasing. This encourages the adoption of supercapacitor-based modules in electric mobility and charging infrastructure.

- Make in India and PLI Scheme: The Make in India and PLI Scheme encourage domestic manufacturing of EVs, batteries, electronics, and advanced energy storage components. These initiatives reduce import dependence and support local production of supercapacitor materials, modules, and power management systems. Rising investment in EV and electronics supply chains is creating wider application opportunities for supercapacitors.

- Defense and Strategic Electronics Supercapacitor Demand: Defense and strategic electronics demand is driving the market as supercapacitors support high-power, fast-response energy storage in radars, communication systems, drones, missiles, electronic warfare equipment, and military vehicles. Their long cycle life, rapid charge-discharge capability, and ability to operate in harsh environments make them suitable for mission-critical applications. Rising defense modernization and domestic electronics manufacturing are further expanding opportunities for supercapacitor adoption.

Market Restraints

- High Import Dependence and Capital Cost Barrier: High import dependence and capital cost barrier hamper the market because a significant share of advanced electrode materials, electrolytes, manufacturing equipment, and supercapacitor cells are sourced from overseas suppliers. This increases production costs and exposes manufacturers to supply chain disruptions, currency fluctuations, and longer procurement timelines. The high capital investment required for domestic manufacturing facilities and R&D infrastructure further limits market entry for new players. As a result, large-scale adoption and localization of supercapacitor technology can progress at a slower pace.

- Market Awareness Gap Between Supercapacitor and Battery Technology: The market awareness gap between supercapacitor and battery technology hampers the market, as many end users still view batteries as the default energy storage solution and have a limited understanding of supercapacitors’ advantages. This slows adoption in EVs, industrial backup, renewable energy, and defense applications where fast charging and high-power density are valuable. Limited technical awareness also makes customers hesitant to pay premium costs for supercapacitor-based systems. As a result, manufacturers need stronger education, demonstrations, and application-specific proof points to expand market acceptance.

Market Opportunities

- Metro Rail Network Expansion: India’s metro network expanded to 1,095 km in 2025 from 248 km in 2014. This metro rail network expansion increases demand for fast-charging and high-power energy storage systems in urban transit. Supercapacitors can support regenerative braking, voltage stabilization, emergency backup, and peak power management in metro trains and stations. As Indian cities expand metro corridors and modernize rail infrastructure, the adoption of durable and low-maintenance supercapacitor modules is expected to grow.

- 5G Telecom Rollout: Telecom operators invested over Rs 4 lakh crore in India’s 5G rollout. This 5G telecom rollout is increasing demand for reliable backup power and fast-response energy storage at telecom towers, base stations, and edge data centers. Supercapacitors help manage power fluctuations, short-duration outages, and peak-load requirements while extending battery life. As 5G networks expand across urban and rural India, telecom operators may adopt supercapacitor-based hybrid backup systems for improved uptime and energy efficiency.

Market Challenges

- Limited Application-Specific Standardization: Absence of clear standards for supercapacitor use in EVs, renewable energy systems, industrial equipment, and electronics creates uncertainty around performance, safety, testing, and compatibility. This makes system integration more complex for manufacturers and end users. It can also increase product development costs and delay commercial deployment across large-scale applications.

- Supply Chain Volatility for Electrode Materials and Electrolytes: Key raw materials such as activated carbon, graphene-based materials, metal oxides, and specialty electrolytes often depend on supply chains. Price fluctuations, geopolitical tensions, and logistics disruptions can increase manufacturing costs and delay production schedules. Limited domestic sourcing capabilities further expose manufacturers to import-related risks. These uncertainties can slow large-scale commercialization and reduce the competitiveness of locally produced supercapacitors.

Emerging Market Trends

1. Indian Academic Research Translating to Commercial Supercapacitor Technology Development

Indian academic research is emerging as IITs, CSIR labs, and universities increasingly focus on advanced electrode materials, graphene, carbon nanomaterials, metal oxides, and hybrid supercapacitor designs. Research outcomes are gradually moving toward prototypes, pilot-scale testing, and industry collaboration. In July 2025, Scientists from Bengaluru collaborated with Aligarh Muslim University and engineered a next-generation energy storage material that dramatically enhances supercapacitor performance. This supports domestic technology development and reduces dependence on imported energy storage solutions. As commercialization improves, India can build a stronger local supercapacitor innovation ecosystem.

2. Supercapacitor-Battery Hybrid Architecture Replacing Pure Battery Systems in Premium Applications

Supercapacitor-battery hybrid architecture is emerging as industries seek energy storage systems that combine high energy density with rapid power delivery. Hybrid configurations use supercapacitors to handle peak power demands, fast charging, and regenerative braking, while batteries provide sustained energy storage. This improves system efficiency, extends battery life, and reduces maintenance requirements. The trend is gaining traction in premium EVs, rail transit, industrial equipment, and advanced power backup applications.

3. Smart Grid and Digital India Creating Supercapacitor Demand in Power Quality Applications

Smart grid and digital India initiatives are creating supercapacitor demand in power quality applications by increasing the need for fast-response energy storage in grid stabilization, voltage regulation, and short-duration backup. Supercapacitors help manage power fluctuations, peak loads, and rapid charge-discharge cycles in smart meters, substations, telecom networks, and digital infrastructure. As India expands digital connectivity and modernizes its power grid, supercapacitor-based systems are gaining relevance for reliable and efficient power management.

4. Electric Two-Wheeler and Three-Wheeler Supercapacitor Integration for Regenerative Braking

Assam’s EV policy sets ambitious adoption targets of 1,00,000 electric two-wheelers and 75,000 electric three-wheelers by 2026. These electric two-wheeler and three-wheeler require quick energy capture during frequent braking in urban traffic. Supercapacitors can absorb and release power faster than conventional batteries, improving acceleration support and energy efficiency. This reduces stress on lithium-ion batteries and may extend battery life. As India’s electric scooter, e-rickshaw, and last-mile mobility market expands, hybrid battery-supercapacitor systems are gaining stronger commercial relevance.

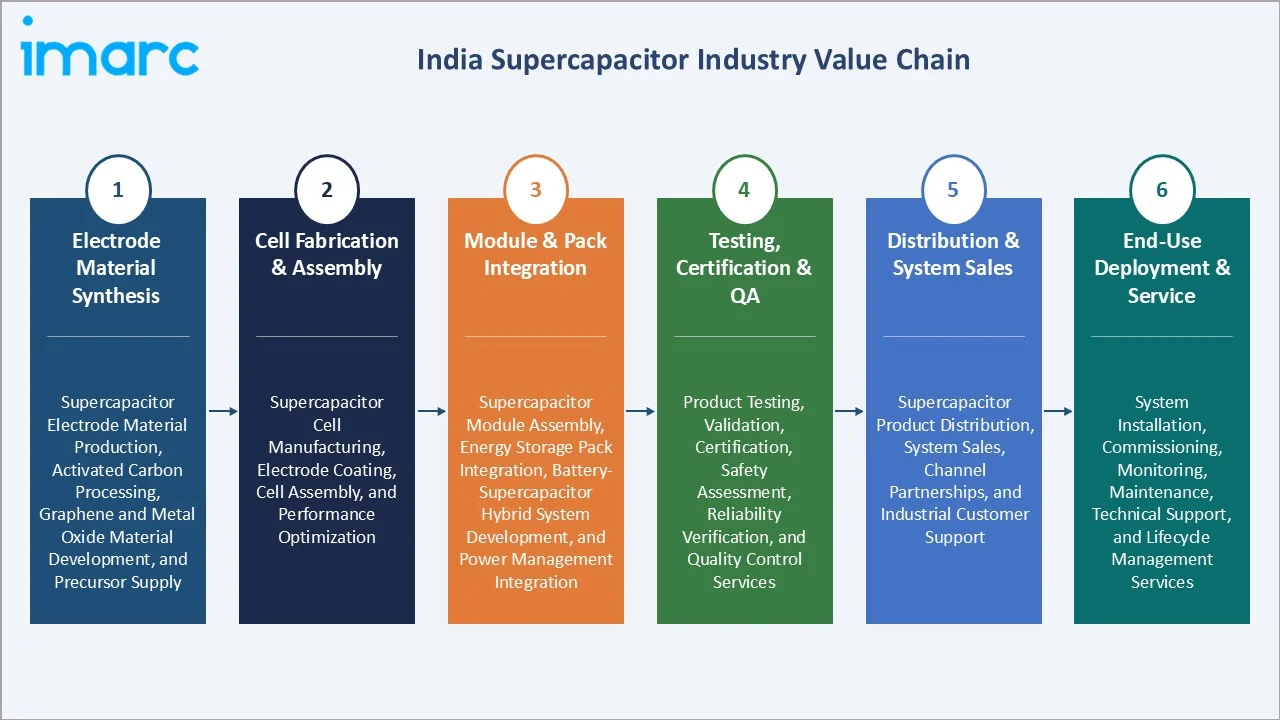

Industry Value Chain Analysis

India's supercapacitor value chain encompasses electrode material synthesis, cell fabrication and assembly, module and pack integration, testing and certification, distribution and system sales, and end-use deployment and service.

|

Stage |

Key Participants |

| Electrode Material Synthesis | Supercapacitor electrode material production, activated carbon processing, graphene and metal oxide material development, and precursor supply |

| Cell Fabrication & Assembly | Supercapacitor cell manufacturing, electrode coating, cell assembly, and performance optimization |

| Module & Pack Integration | Supercapacitor module assembly, energy storage pack integration, battery-supercapacitor hybrid system development, and power management integration |

| Testing, Certification & QA | Product testing, validation, certification, safety assessment, reliability verification, and quality control services |

| Distribution & System Sales | Supercapacitor product distribution, system sales, channel partnerships, and industrial customer support |

| End-Use Deployment & Service | System installation, commissioning, monitoring, maintenance, technical support, and lifecycle management services |

The cell fabrication stage is the value chain's most commercially critical gap for India's supercapacitor market development, the absence of domestic commercial-scale EDLC cell fabrication creating 85-90% import dependence that generates value chain leakage to Japan, USA, and Korea above India's system integration and application engineering activities.

Technology Landscape in the India Supercapacitor Industry

Electric Double-Layered Capacitor Technology

Electric double-layered capacitor (EDLC) technology offers rapid charge-discharge capability, high power density, and long operational life. EDLCs are increasingly being adopted in electric vehicles, regenerative braking systems, renewable energy storage, and industrial backup power applications. In September 2024, CollarEV Auto India announced the use of supercapacitor battery packs manufactured by PBS Korea. This marks the first use of supercapacitor battery technology in two-wheelers in India, with both companies introducing premium, high-performance EDLC batteries for the country’s electric mobility sector. Ongoing research into advanced carbon-based electrode materials is improving performance and cost efficiency. As demand for fast-response energy storage grows, EDLC technology continues to drive product innovation and commercialization in the Indian market.

Pseudocapacitor Technology and Metal Oxide Electrode Development

Pseudocapacitor technology and metal oxide electrode development are improving energy density beyond conventional EDLC systems. Advanced metal oxides such as manganese oxide, ruthenium oxide, and nickel oxide enable faster electrochemical reactions and higher charge storage capacity. Research institutions and manufacturers are exploring these materials to develop compact, high-performance energy storage solutions for EVs, renewable energy systems, and industrial electronics. This trend is accelerating innovation in next-generation supercapacitor designs with enhanced performance characteristics.

Conducting Polymer Electrode Technology

Conducting polymer electrode technology enables higher capacitance and improved energy storage performance through materials such as polyaniline, polypyrrole, and PEDOT. These polymers offer rapid charge-discharge characteristics, lightweight designs, and flexibility for compact electronic devices. Research efforts are focused on enhancing conductivity, stability, and cycle life to support commercial applications. The technology is gaining attention for use in wearable electronics, EVs, smart devices, and hybrid energy storage systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Electric Double-Layered Capacitors |

46.2% |

2025 |

|

Module Type |

🔒 |

🔒 |

2025 |

|

Material Type |

Carbon and Metal Oxide |

49.6% |

2025 |

|

End Use Industry |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

32.8% |

2025 |

By Product Type

Electric double-layered capacitors (EDLC) lead at 46.2% (2025). The EDLC segment encompasses coin-type backup power, cylindrical and prismatic industrial EDLC, and large-format transport EDLC. EDLC's ~11.8% CAGR reflects sustained industrial and transport adoption with moderate entry into renewable energy applications.

To access detailed market analysis, Request Sample

Pseudocapacitors at 30.8% grow fastest at ~13.5% CAGR through metal oxide electrode adoption in high-energy-density defense and EV applications. Hybrid capacitors at 23.0% represent the lithium-ion capacitor and asymmetric EDLC segment for metro rail and high-performance industrial applications, growing at ~13.2% CAGR through traction energy storage system procurement across India's expanding metro rail network.

By Material Type

Carbon and metal oxide lead at 49.6% (2025). Activated carbon EDLC electrode dominates the carbon component, while MnO2 and RuO2 contribute to the metal oxide pseudocapacitor electrode expansion, creating above-category-average growth within the dominant material segment.

Conducting polymer at 28.4% grows fastest at ~13.6% CAGR through pseudocapacitor electrode commercialization. Composite materials at 22.0% represent graphene composites, carbon nanotube composites, and emerging electrode materials.

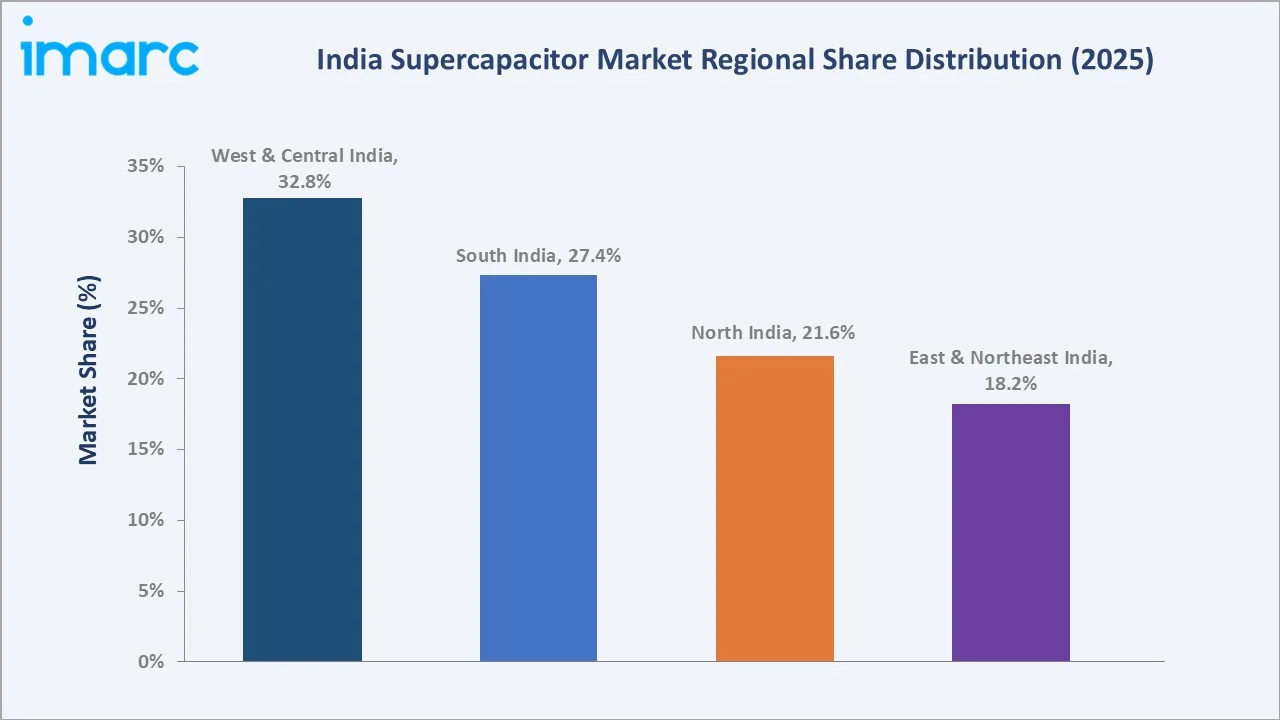

Regional Market Insights

|

Region |

Share (2025) |

Key India Supercapacitor Market Drivers & Characteristics |

| West & Central India |

32.8% |

Driven by the strong presence of automotive, EV manufacturing, electronics production, and industrial equipment industries. |

| South India |

27.4% |

Benefits from a well-established electronics, semiconductor, automotive, and renewable energy ecosystem. |

| North India |

21.6% |

Supported by the rising deployment of electric mobility, telecom infrastructure, metro rail projects, and industrial automation. |

| East & Northeast India |

18.2% |

Witnessing increased adoption of supercapacitors through renewable energy projects, electric public transportation, industrial development, and grid modernization initiatives. |

West and Central India's 32.8% market leadership reflects Maharashtra-Gujarat's combined industrial-EV-renewable energy supercapacitor demand concentration, creating the highest per-state supercapacitor procurement in India.

South India's 27.4% reflects Bengaluru's research ecosystem, creating the most commercially advanced domestic technology development, DRDO Hyderabad creating South India's highest defense supercapacitor procurement, and Chennai's automotive OEM ecosystem evaluating EV supercapacitor integration. North India's 21.6% is anchored by Delhi Metro's operational deployment and Delhi-NCR's smart meter rollout, creating coin supercapacitor demand. East and Northeast India's 18.2% reflects industrial power quality demand from steel and aluminium smelting, and the emerging renewable energy grid stabilization demand in Northeast India's weak grid environment.

Competitive Landscape

India's supercapacitor market competitive landscape is dominated by international companies collectively supplying 80-85% of the Indian supercapacitor market value through authorized importer and distribution networks, with Indian system integrators contributing 10-15% of market revenue through module assembly and complete system integration.

|

Company Name |

Key Products |

Market Position |

Core Strength |

| Eaton | Coin cell supercapacitors, Cylindrical supercapacitor cells, Medium and large supercapacitor cells, Supercapacitor modules |

Market Leader |

Eaton is a significant player in the Indian supercapacitor market, providing advanced energy storage solutions designed for high reliability, long life, and efficient power management. |

| Skeleton Technologies | SkelCap Series | Strong Challenger | Skeleton Technologies plays a key role in India's industrial sector by supplying high-performance, graphene-based supercapacitors for automation. |

| CAP-XX | Prismatic Ultra Thin Supercaps, Coin Cell Supercaps, Cylindrical Supercaps | Niche Player | CAP-XX is a leading manufacturer of ultra-thin, high-power density prismatic supercapacitors, which are crucial for space-constrained electronics, IoT devices, and renewable energy, with distribution in India through partners. |

| Panasonic Corporation | Supercapacitor (EDLC) | Market Leader | Panasonic Corporation, specifically through Panasonic Industry, is a key player in the Indian supercapacitor and high-performance capacitor market, driven by the rapid growth of AI data centers, telecommunications, and electric vehicle (EV) infrastructure. |

The competitive landscape is additionally shaped by the application-specific nature of India's supercapacitor demand. PM-eBus supercapacitor procurement is creating government-tender competition where Make in India preference gives Indian system integrators a commercial advantage; defense procurement is creating DRDO-qualification-gated competition; and metro rail procurement is creating international engineering standard competition.

Key Company Profiles

Eaton

Eaton is a power management company with a strong presence in India's energy storage, electrical, industrial, and transportation sectors. Through its supercapacitor portfolio, the company serves applications such as smart meters, industrial automation, telecom infrastructure, renewable energy systems, electric mobility, and backup power solutions. Its supercapacitors are designed to provide rapid power delivery, long cycle life, and reliable performance in demanding operating environments.

- Key Products: Coin cell supercapacitors, cylindrical supercapacitor cells, medium and large supercapacitor cells, Supercapacitor modules.

- Strategic Focus: Delivering high-reliability supercapacitor solutions for smart meters, telecom infrastructure, industrial automation, renewable energy systems, and electric mobility applications, with an emphasis on power efficiency, backup power, and grid modernization.

Skeleton Technologies

Skeleton Technologies is a manufacturer of advanced supercapacitors and energy storage systems known for its patented graphene-based technology. The company’s products are designed to deliver high power density, rapid charging, and long operational lifetimes.

- Key Products: SkelCap Series.

- Strategic Focus: Advancing the adoption of graphene-based supercapacitors for electric vehicles, rail transit, industrial automation, and renewable energy systems, where high power density, rapid charging, and long cycle life are critical performance requirements.

Market Concentration Analysis

India's supercapacitor market is highly concentrated at the imported product tier. Market concentration is decreasing as Chinese manufacturers enter India's commercial EDLC market through direct import competition, creating price-driven market share redistribution from premium Japanese and American brands toward lower-cost Chinese EDLC alternatives in cost-sensitive industrial and UPS applications. Application-specific concentration patterns create distinct competitive dynamics. The defense supercapacitor market is effectively a DRDO-qualified domestic supplier duopoly for complete systems, with imported cells; metro rail is an international traction system integrator oligopoly; IoT and smart meter is a Japanese coin supercapacitor oligopoly; and electric bus represents the most competitive segment.

Investment & Growth Opportunities

Highest Growth Segments

Conducting polymer materials (~13.6% CAGR), pseudocapacitors (~13.5% CAGR through metal oxide electrode EV and defense demand), hybrid capacitors (~13.2% CAGR through metro rail procurement), East and Northeast India regional market (~14% CAGR through renewable energy grid stabilization from low base), defense supercapacitor (~15-18% CAGR from small base through DRDO programme expansion), and smart meter coin supercapacitor (~25% CAGR from near-zero base) represent India's highest-growth supercapacitor investment vectors through 2034.

Emerging Investment Opportunities

India's smart meter AMI deployment represents the highest-volume single-programme coin supercapacitor procurement opportunity in India's market history, creating India-specific coin supercapacitor procurement above import distribution, representing the most accessible Indian market entry point for domestic coin supercapacitor cell fabrication investment.

Investment Themes

- PM-eBus supercapacitor pack indigenization through Make in India domestic content requirement anticipation: Government of India's PM e-Bus Sewa tender specifications progressively increasing domestic content requirement for supercapacitor packs from the current domestic content toward 2027-2028 creates commercial incentive for domestic supercapacitor cell assembly investment with guaranteed government procurement volume that eliminates the demand uncertainty that currently limits private investment in Indian supercapacitor manufacturing.

- Metro rail regenerative braking supercapacitor system integration for India's metro expansion: India's planned metro network expansion represents a high investment in supercapacitor energy storage system procurement through 2032. Indian system integrators developing metro-grade supercapacitor energy storage system capability by 2026-2027 can compete for domestically funded metro supercapacitor procurement through Make in India preference policies.

Future Market Outlook (2026-2034)

India's supercapacitor market is projected to grow from USD 268.7 Million in 2025 to USD 818.0 Million by 2034, delivering a 12.77% CAGR over the forecast period. The market's anchor value of USD 490.1 Million in 2030 represents an Indian supercapacitor industry at its most commercially transformative inflection point. PM-eBus Sewa will have deployed its initial electric buses, creating the largest supercapacitor pack fleet in India's history.

Three structural forces define India's supercapacitor market growth through 2034 with exceptional confidence. India's electric vehicle policy mandates create government-mandated supercapacitor demand that is policy-committed, multi-year, and budget-allocated regardless of commercial market dynamics. India's renewable energy target creates structural renewable energy grid integration challenges that supercapacitor frequency stabilization uniquely addresses among fast-response energy storage options, creating government-backed infrastructure investment in supercapacitor grid storage above commercial market demand. The Make in India electronics manufacturing ecosystem creates commercial incentives for domestic supercapacitor manufacturing investment that was absent from India's market before 2020.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025) including R&D Directors; Commercial Directors; Application Engineers; government programme managers; defense procurement specialists; and industry association representatives.

Secondary Research

Secondary research encompassed PM e-Bus Sewa programme procurement data; renewable energy capacity addition data; DRDO Annual Reports; energy storage standards documentation; international supercapacitor standards; railway energy storage specifications; company annual reports; research publications database; and India-published supercapacitor research citation analysis. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using an application bottom-up model: EV and transport; renewable energy; defense; IoT, and smart meter.

India Supercapacitor Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Electric Double-Layered Capacitors, Pseudocapacitors, Hybrid Capacitors |

| Module Types Covered | Less than 25V, 25-100V, More than 100V |

| Material Types Covered | Carbon and Metal Oxide, Conducting Polymer, Composite Materials |

| End Use Industries Covered | Automotive and Transportation, Consumer Electronics, Power and Energy, Healthcare, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Eaton, Skeleton Technologies, CAP-XX, Panasonic Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India supercapacitor market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India supercapacitor market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India supercapacitor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Supercapacitor Market Report

India's supercapacitor market reached USD 268.7 Million in 2025. The market is driven by the rapid adoption of electric vehicles, expansion of renewable energy projects, and increasing demand for fast-charging, high-power energy storage solutions. Government initiatives such as Make in India, PLI schemes, smart grid modernization, and investments in telecom and public transportation infrastructure are further accelerating market growth.

India's supercapacitor market grows at 12.77% CAGR during 2026-2034, reaching USD 818.0 Million by 2034. Conducting polymer materials grow fastest at ~13.6% CAGR. Pseudocapacitors grow at ~13.5% CAGR through metal oxide electrode EV and defense demand. The overall market growth is sustained by the PM e-Bus Sewa electric bus programme, Make in India domestic manufacturing investment, and the defense supercapacitor procurement expansion.

EDLC leads at 46.2% through commercial development, creating the most available, most specified, and most trusted supercapacitor technology in India's electronics and industrial procurement.

Carbon and metal oxide leads at 49.6% through activated carbon EDLC electrode's foundational commercial scale supplemented by MnO2 and RuO2 metal oxide pseudocapacitor electrode expansion.

West and Central India lead at 32.8% through Maharashtra's electric bus fleet, Mumbai-Pune's automotive OEM EV evaluation activity, and Gujarat's renewable energy supercapacitor frequency stabilization demand from India's highest per-state solar installed capacity.

Leading companies include Eaton, Skeleton Technologies, CAP-XX, and Panasonic Corporation, among others.

India's supercapacitor market is projected to reach approximately USD 490.1 Million by 2030, with PM e-Bus Sewa Phase 1 fully deployed, metro rail network growth with supercapacitor regenerative braking systems, India's renewable energy requiring systematic grid frequency stabilization supercapacitor deployment, and domestic EDLC cell manufacturing.

A supercapacitor is an electrochemical energy storage device that stores charge electrostatically at the electrode-electrolyte interface (EDLC) or through reversible surface faradaic reactions (pseudocapacitor) rather than through chemical reactions within electrode bulk material, as in batteries. The fundamental differences: supercapacitors deliver 10-100x higher power density (W/kg) than lithium-ion batteries, enabling faster charge-discharge for high-power short-duration applications; batteries deliver 10-50x higher energy density (Wh/kg) than supercapacitors, enabling longer discharge duration; supercapacitors achieve 100,000-1,000,000+ charge-discharge cycles versus 300-1,000 cycles for VRLA batteries and 1,000-3,000 cycles for lithium-ion batteries, creating 20-30 year maintenance-free operation versus 3-10 year battery replacement requirement.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)