India Synthetic Leather Market Size, Share, Trends and Forecast by Type, Application, End Use Industry, and Region, 2026-2034

India Synthetic Leather Market Summary:

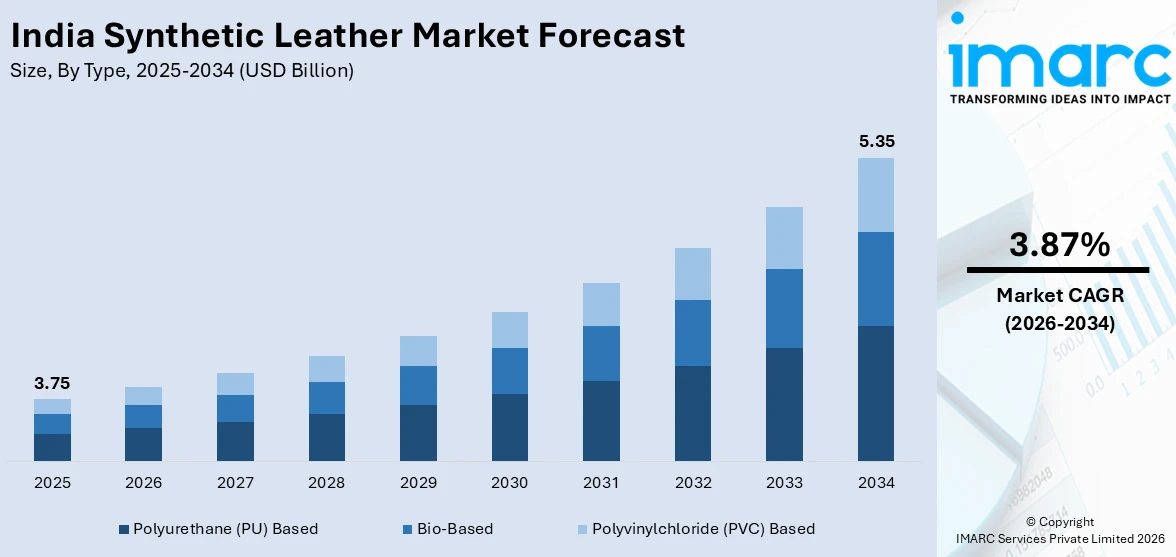

The India synthetic leather market size was valued at USD 3.75 Billion in 2025 and is projected to reach USD 5.35 Billion by 2034, growing at a compound annual growth rate of 3.87% from 2026-2034.

India's synthetic leather market is witnessing robust expansion, driven by the rapid growth of the footwear, automotive, and furniture industries, all of which depend on faux leather as a cost-effective and animal-friendly material. Increasing urbanization, rising disposable incomes, and a growing middle class are amplifying demand for fashionable, sustainable, and durable synthetic leather products across a wide range of applications. The market's trajectory is further supported by significant manufacturing investments and government-backed programs to strengthen domestic production of leather and footwear goods. These macro-level factors, combined with growing consumer consciousness around ethical and eco-friendly materials, are collectively shaping India's India synthetic leather market share.

Key Takeaways and Insights:

- By Type: Polyurethane (PU) based dominates the market with a share of 55.5% in 2025, owing to its superior flexibility, durability, and eco-friendliness compared to PVC alternatives, making it the preferred choice across footwear, automotive, and furniture segments.

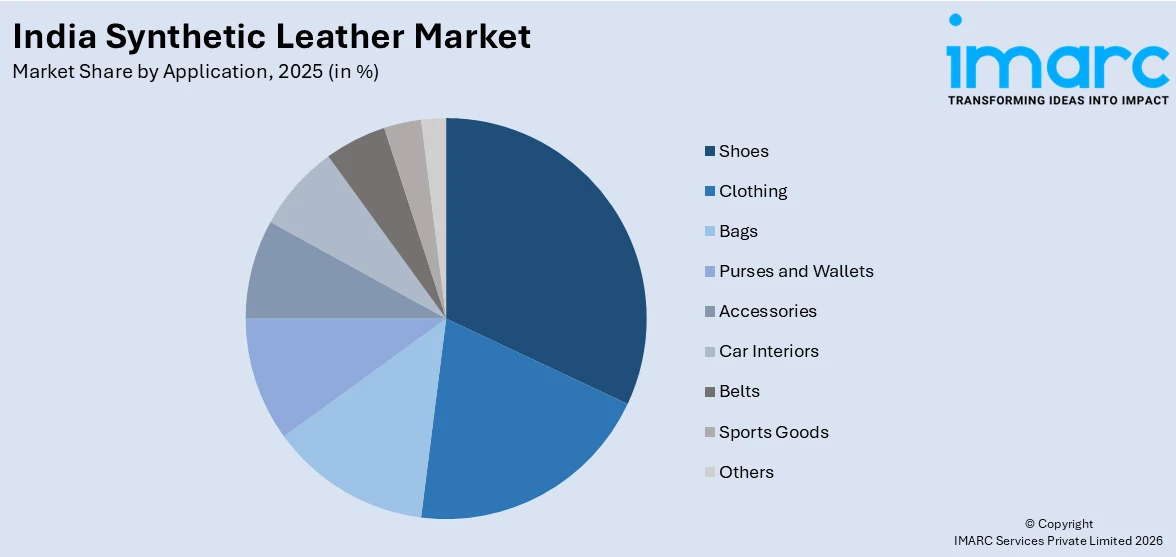

- By Application: Shoes leads the market with a share of 32.5% in 2025, driven by India's position as the world's second-largest footwear producer and strong consumer preference for affordable, cruelty-free synthetic leather footwear.

- By End Use Industry: Footwear represent the largest market share of 34.2% in 2025, supported by India's massive domestic footwear consumption base and the expanding presence of both domestic and global footwear brands.

- By Region: West and Central India represents the largest segment with a market share of 32.5% in 2025, underpinned by the concentration of major manufacturing hubs, automotive clusters, and textile industries in states such as Maharashtra and Gujarat.

- Key Players: India’s synthetic leather industry is characterized by the presence of both domestic producers and international chemical companies competing across various product types, applications, and end-use sectors. The market landscape reflects strong competition driven by product innovation, diverse application demand, and expanding manufacturing capabilities.

To get more information on this market Request Sample

India's synthetic leather market is undergoing a structural transformation as demand intensifies from diverse end-use industries. The footwear sector remains the primary consumption driver, accounting for the largest share of synthetic leather usage in the country, while rising vehicle production is generating fresh demand from the automotive upholstery segment. The expansion of organized furniture retail and growing urban housing development is propelling demand in the furnishing industry, where synthetic leather is widely preferred for sofas, chairs, and office seating. For instance, in October 2024, Japanese firms Kyowa Leather Cloth Company, part of the Toyota Group, and Meira Corporation applied to the Yamuna Expressway Industrial Development Authority (YEIDA) for 10 acres of land each to establish manufacturing facilities near Noida airport. The proposed projects together represent an investment of approximately Rs 900 crore. Such investments are expected to strengthen domestic manufacturing capacity and support the evolving supply chain of synthetic leather products in India.

India Synthetic Leather Market Trends:

Rising Adoption of Polyurethane-Based Synthetic Leather Across Industries

Polyurethane-based synthetic leather is increasingly preferred in India, reflecting a gradual shift away from PVC-based alternatives. Compared with traditional materials, PU leather provides better moisture resistance, lighter weight, and enhanced softness, making it suitable for a wide range of applications. It is widely utilized in footwear, automotive interiors, and furniture upholstery due to its durability and flexibility. Additionally, polyurethane-based materials are considered more environmentally responsible, as their production involves fewer harmful emissions. These advantages have encouraged manufacturers to adopt PU synthetic leather to meet performance expectations while aligning with evolving environmental standards.

Growing Demand for Bio-Based and Sustainable Synthetic Leather Alternatives

Consumer awareness around animal welfare, environmental sustainability, and circular manufacturing is accelerating the adoption of bio-based synthetic leather alternatives across India. Domestic startups and innovators are developing leather substitutes using agricultural waste streams including floral waste, banana crop residues, sugarcane bagasse, and tomato pomace. The Bio Company (TBC), based in Surat, began commercial production of its Bioleather, manufactured from tomato agro-waste without PU or PVC, in late 2024, achieving production of approximately 5,000 meters per month and receiving strong market traction. This wave of bio-based innovation, supported by the Make in India initiative, is positioning India as an emerging hub for sustainable leather alternatives.

Customization and Digital Printing Driving New Application Opportunities

Customization is emerging as a transformative trend within India's synthetic leather market, with consumers and brands increasingly demanding personalized textures, prints, finishes, and colour options that genuine leather cannot match at scale. Manufacturers are investing in advanced coating technologies, digital printing capabilities, and surface treatment innovations to deliver bespoke products across fashion accessories, upholstery, and footwear segments. This trend is particularly pronounced in the premium and mid-range fashion segments, where brands seek differentiated product aesthetics. South Korea's Hwaseung Enterprise committed Rs 1,720 crore to establish a synthetic leather manufacturing facility in Tirunelveli, Tamil Nadu, targeting production of customized faux leather soles for global brands including Nike and Adidas, and committing to create approximately 20,000 jobs.

Market Outlook 2026-2034:

India’s synthetic leather market is expected to experience steady expansion in the coming years, driven by the growth of key downstream sectors such as footwear, automotive interiors, and furnishings. Supportive government initiatives aimed at strengthening the leather and footwear industry are also encouraging domestic production and investment. In addition, increasing export potential in international markets is creating new opportunities for manufacturers. The growing shift toward bio-based and waterborne polyurethane materials is likely to unlock premium product segments while enabling producers to align with evolving environmental and sustainability requirements.The market generated a revenue of USD 3.75 Billion in 2025 and is projected to reach a revenue of USD 5.35 Billion by 2034, growing at a compound annual growth rate of 3.87% from 2026-2034.

India Synthetic Leather Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Polyurethane (PU) Based |

55.5% |

|

Application |

Shoes |

32.5% |

|

End Use Industry |

Footwear |

34.2% |

|

Region |

West and Central India |

32.5% |

Type Insights:

- Bio-Based

- Polyvinylchloride (PVC) Based

- Polyurethane (PU) Based

Polyurethane (PU) based dominates with a market share of 55.5% of the total India synthetic leather market in 2025.

Polyurethane-based synthetic leather commands the leading position in India's market owing to a combination of performance, versatility, and environmental attributes that set it apart from PVC alternatives. PU leather is inherently softer and lighter, offering a closer tactile resemblance to genuine leather, while being waterproof, resistant to sunlight degradation, and suitable for dry-cleaning. Its absence of dioxin emissions during manufacturing positions it as the more environmentally responsible choice among synthetic options. PU leather is extensively used in the footwear industry for shoe uppers and linings, in the automotive segment for seat covers and door trims, and in furniture manufacturing for upholstered sofas and office chairs across India's rapidly expanding urban market.

Polyurethane (PU)-based materials also dominate the India synthetic leather market due to their adaptability across multiple end-use industries and compatibility with modern manufacturing processes. PU synthetic leather can be engineered in a wide range of textures, finishes, and colors, allowing manufacturers to replicate the look and feel of natural leather while maintaining consistent quality and cost efficiency. Its flexibility and durability make it suitable for mass-market as well as premium applications. As consumer preferences shift toward stylish, lightweight, and cruelty-free alternatives, PU-based synthetic leather continues to gain widespread adoption across fashion, automotive, and lifestyle product segments.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Clothing

- Bags

- Shoes

- Purses and Wallets

- Accessories

- Car Interiors

- Belts

- Sports Goods

- Others

Shoes leads with a share of 32.5% of the total India synthetic leather market in 2025.

Shoes represent the largest application segment for synthetic leather in India, underpinned by the country's status as the world's second-largest footwear producer and consumer. Synthetic leather, especially polyurethane-based varieties, is widely utilized in footwear components such as uppers, linings, and soles because of its durability, water resistance, and ease of manufacturing. Compared to genuine leather, it offers a more cost-effective option while maintaining functional performance. Growing consumer interest in cruelty-free, stylish, and affordable footwear continues to encourage manufacturers to incorporate synthetic leather materials in shoe production. In May 2024, Bata India announced plans to open 100 to 150 new stores per annum in Tier 2 and Tier 3 cities, emphasising product innovation that increasingly leverages synthetic leather.

Another factor reinforcing the dominance of the footwear segment is the rapid expansion of India’s organized and unorganized shoe manufacturing ecosystem. Large-scale production clusters, combined with growing exports and rising domestic consumption, are increasing the demand for cost-efficient and versatile materials. Synthetic leather offers design flexibility, lightweight properties, and consistent quality, making it well suited for mass footwear production. As brands continue to diversify product ranges and target value-conscious consumers, the reliance on synthetic leather in shoe manufacturing is expected to remain strong across the Indian market.

End Use Industry Insights:

- Footwear

- Furniture

- Automotive

- Textile

- Sports

- Electronics

- Others

Footwear represents the largest market share of 34.2% of the total India synthetic leather market in 2025.

The footwear industry is the most significant end-use of synthetic leather in India because of its wide shoe manufacturing industry. Synthetic leather, more specifically PU-based versions, has also been extensively applied across the product population, in formal footwear, athletic, and casual shoes, providing a practical combination of looks, durability, and cost. The government's activities to boost the leather and footwear ecosystem are complementing the growth of the industry. Such facilitative policies will trigger domestic output, enhance exports, and strengthen synthetic leather as an essential substance to be used in making footwear in India.

The footwear segment leads the overall India synthetic leather market due to the large and expanding domestic demand for affordable, durable, and stylish shoes. Synthetic leather is widely preferred by manufacturers because it offers consistent quality, design flexibility, and cost efficiency compared to natural leather. Its resistance to wear, moisture, and easy maintenance makes it suitable for mass-produced footwear. In addition, the growth of organized retail, e-commerce footwear brands, and fast-fashion trends is further strengthening the demand for synthetic leather materials across various shoe categories in India.

Regional Insights:

- Northern India

- West and Central India

- South India

- East and Northeast India

West and Central India represents the highest revenue share of 32.5% of the total India synthetic leather market in 2025.

West and Central India commands the leading regional share of the synthetic leather market, driven by the concentration of large-scale manufacturing infrastructure in Maharashtra and Gujarat. Synthetic leather is widely used for footwear uppers, automotive interiors, and upholstery due to its durability, affordability, and design flexibility. The presence of well-developed logistics infrastructure and major ports also facilitates raw material supply and product distribution. Additionally, rising urbanization and growing consumer demand for fashionable yet cost-effective products are encouraging manufacturers to expand production, strengthening the region’s demand for synthetic leather.

In Central India, the growth of the synthetic leather market is supported by the expansion of small and medium-scale manufacturing units and increasing demand for affordable footwear and accessories. Local manufacturers prefer synthetic leather because it is economical, easy to process, and suitable for mass production. The gradual development of urban centers and retail networks is also boosting demand for synthetic leather in furniture upholstery and interior applications. Moreover, improving transportation infrastructure is enabling better connectivity with major industrial regions, allowing manufacturers to access raw materials and distribute finished products more efficiently.

Market Dynamics:

Growth Drivers:

Why is the India Synthetic Leather Market Growing?

Expanding Footwear Industry and Rising Domestic Consumption

India’s footwear industry serves as a major driver of synthetic leather demand in the country. The India footwear market size was valued at USD 20.67 Billion in 2025 and is projected to reach USD 47.53 Billion by 2034, growing at a compound annual growth rate of 9.7% from 2026-2034. With a large consumer base and strong manufacturing ecosystem, the sector generates substantial need for cost-efficient materials, making synthetic leather a widely preferred alternative to genuine leather due to its durability, water resistance, and affordability across various product categories. Government initiatives aimed at strengthening the leather and footwear industry are encouraging technological improvements and production expansion. At the same time, evolving fashion preferences among the country’s young urban population are increasing demand for stylish and affordable synthetic leather footwear.

Rapid Growth of Automotive and Furniture Manufacturing Sectors

India's automotive industry is a critical and expanding source of demand for synthetic leather, particularly for vehicle seat upholstery, door panels, steering wheel covers, and headliners. With India's total vehicle production reaching 2,773,039 units in September 2024, automakers are incorporating PU synthetic leather at scale to deliver premium-looking interiors at competitive price points. The Society of Indian Automobile Manufacturers (SIAM) has reported consistent growth in domestic passenger vehicle sales, driving upholstery material demand in parallel. PU synthetic leather is the preferred upholstery material for sofas, chairs, and commercial seating due to its wear resistance, easy maintenance, and textural versatility, making the furniture segment a significant and growing end-use channel for the market.

Government Policy Support and Sustainability-Driven Manufacturing Initiatives

Policy support from the Government of India has significantly reinforced market growth for synthetic leather manufacturers. The 'Make in India' and 'Atmanirbhar Bharat' programs have encouraged domestic production of synthetic leather materials and leather goods by providing production-linked incentives and enabling 100% FDI in the sector under the automatic route. These frameworks have attracted both domestic investment and foreign capital, with South Korea's Hwaseung Enterprise committing Rs 1,720 crore for a synthetic leather manufacturing facility in Tirunelveli, Tamil Nadu, targeting production of faux soles for global sportswear brands including Nike and Adidas. The Indian Leather Development Program (ILDP) and its successor schemes have channelled resources into technological upgradation of production units and establishment of Common Effluent Treatment Plants (CETPs), enabling manufacturers to adopt cleaner production methods. The confluence of government incentives, growing export demand, and rising consumer preference for cruelty-free materials creates a compelling environment for sustained market expansion.

Market Restraints:

What Challenges the India Synthetic Leather Market is Facing?

Environmental and Health Concerns Associated with PU and PVC Raw Materials

The production of PU and PVC synthetic leather relies on petrochemical raw materials that pose significant health and environmental risks. PVC manufacturing emits toxic dioxins, while PU production can expose workers to fumes causing respiratory issues. Both materials are non-biodegradable, contributing to long-term environmental pollution. Regulatory tightening around volatile organic compound (VOC) emissions and plasticiser use is increasing compliance costs for manufacturers, potentially limiting growth in certain segments.

Competitive Pressure from Low-Cost Chinese Imports

China's continued dumping of inexpensive synthetic leather products in the Indian market creates significant pricing pressure for domestic manufacturers. The price gap between Chinese imports and locally produced synthetic leather challenges the competitiveness of Indian firms, particularly in the mass-market footwear and accessories segments. While the Indian government has taken protective measures to support domestic producers, the import pressure persists and constrains margins across the value chain.

Higher Production Cost and Complexity of Bio-Based Alternatives

While bio-based synthetic leather is gaining attention as a sustainable alternative, its adoption at scale is constrained by significantly higher production costs compared to conventional PU and PVC variants. Complex manufacturing processes, limited raw material standardisation, and the need for extensive quality testing make bio-based leather economically unviable for mass-market applications at present. The longer commercialisation timelines for these materials slow the transition toward truly sustainable synthetic leather and limit the near-term market opportunity in this subsegment.

Competitive Landscape:

India's synthetic leather market is moderately fragmented, with a mix of large-scale domestic manufacturers and specialised regional players competing across type, application, and end-use segments. Companies compete primarily on material quality, product customisation capabilities, pricing, and the ability to deliver consistently at scale for industrial buyers. Innovation in eco-friendly formulations, advanced surface treatments, and compliance with global export standards has become a key differentiator. Investment in research and development, particularly in polyurethane chemistry, bio-based substrates, and waterborne coatings, is growing as players seek to address both domestic premiumisation trends and the sustainability demands of international buyers. Strategic capacity expansions, domestic partnerships, and export-oriented production strategies are shaping the competitive landscape of this market.

Recent Developments:

- May 2024: BASF opened its Polyurethane Technical Development Center in Mumbai, spanning approximately 2,000 square meters, to provide Indian synthetic leather manufacturers with customer support services including bespoke formulation development, troubleshooting, line trials, and technical training sessions.

India Synthetic Leather Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Bio-Based, Polyvinylchloride (PVC) Based, Polyurethane (PU) Based |

| Applications Covered | Clothing, Bags, Shoes, Purses and Wallets, Accessories, Car Interiors, Belts, Sports Goods, Others |

| End Use Industries Covered | Footwear, Furniture, Automotive, Textile, Sports, Electronics, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Synthetic Leather Market Report

The India synthetic leather market size was valued at USD 3.75 Billion in 2025.

The India synthetic leather market is expected to grow at a compound annual growth rate of 3.87% from 2026-2034 to reach USD 5.35 Billion by 2034.

Polyurethane (PU) based held the largest market share at 55.5% in 2025, driven by its superior durability, versatility across multiple end-use industries, lower environmental impact compared to PVC, and widespread adoption in footwear, automotive, and furniture applications.

Key factors driving the India synthetic leather market include the rapid expansion of the domestic footwear and automotive industries, rising consumer preference for cruelty-free and sustainable materials, government policy support through IFLADP and the Focus Product Scheme, growing urbanization and disposable incomes, and continuous innovation in polyurethane and bio-based leather manufacturing technologies.

Major challenges facing the India synthetic leather market include environmental and health concerns associated with PU and PVC raw materials, competitive pressure from low-cost Chinese imports depressing domestic manufacturer margins, and the higher production costs and complex commercialisation timelines of bio-based synthetic leather alternatives limiting their near-term scalability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)