India Taxi Market Size, Share, Trends and Forecast by Booking Type, Service Type, Vehicle Type, and Region, 2026-2034

India Taxi Market Size, Share, Trends & Forecast (2026-2034)

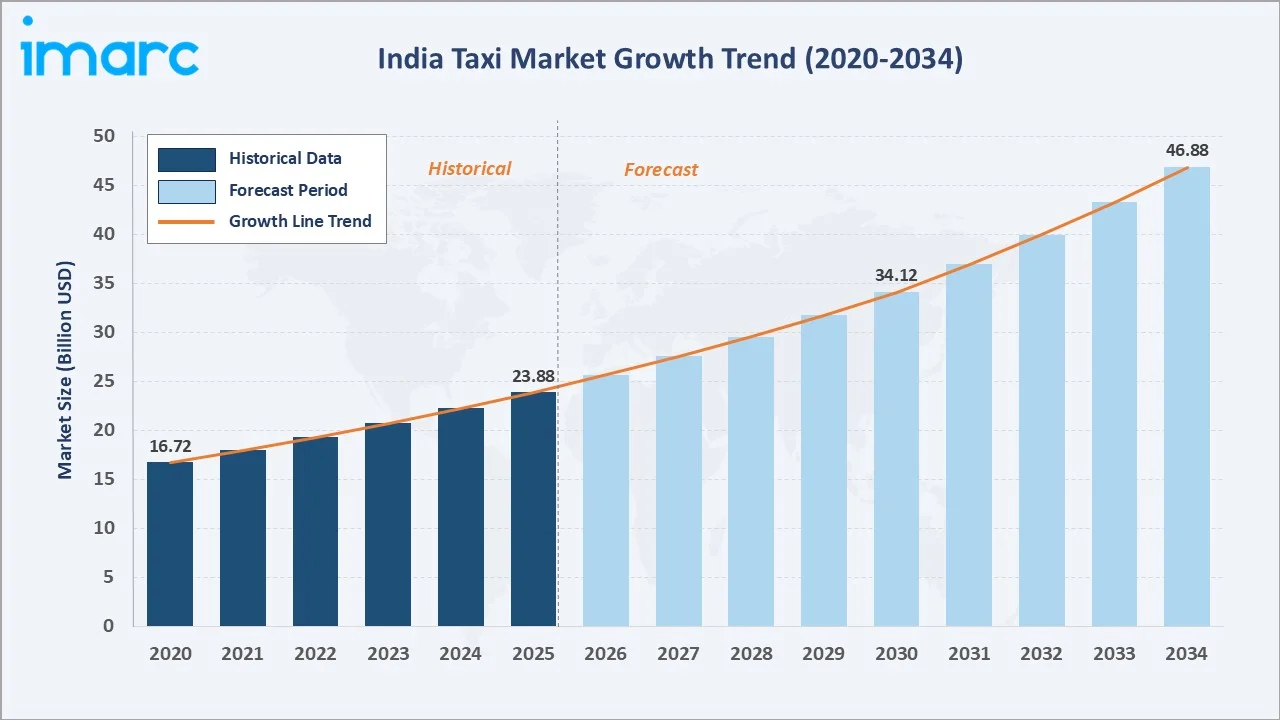

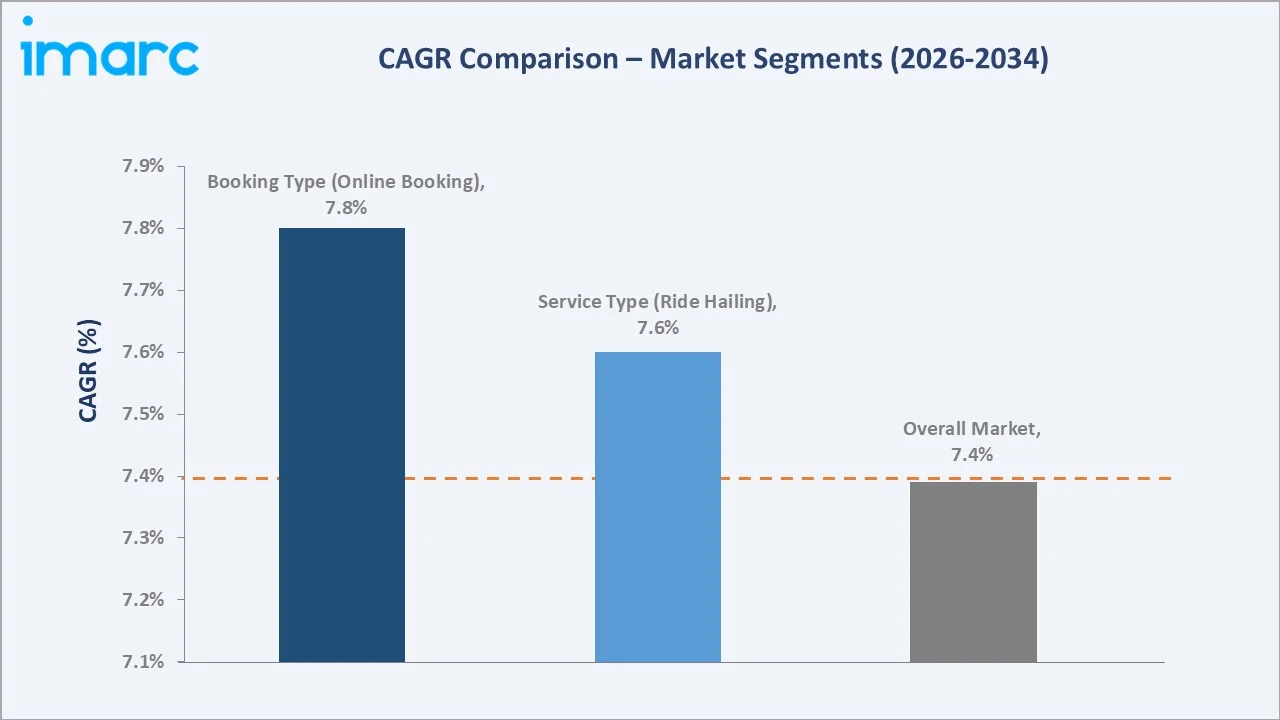

The India taxi market reached USD 23.88 Billion in 2025 and is projected to reach USD 46.88 Billion by 2034, growing at a CAGR of 7.39% during 2026-2034. Growth is driven by rapid urbanization, smartphone penetration, and rising app-based mobility demand across metropolitan and tier-two cities.

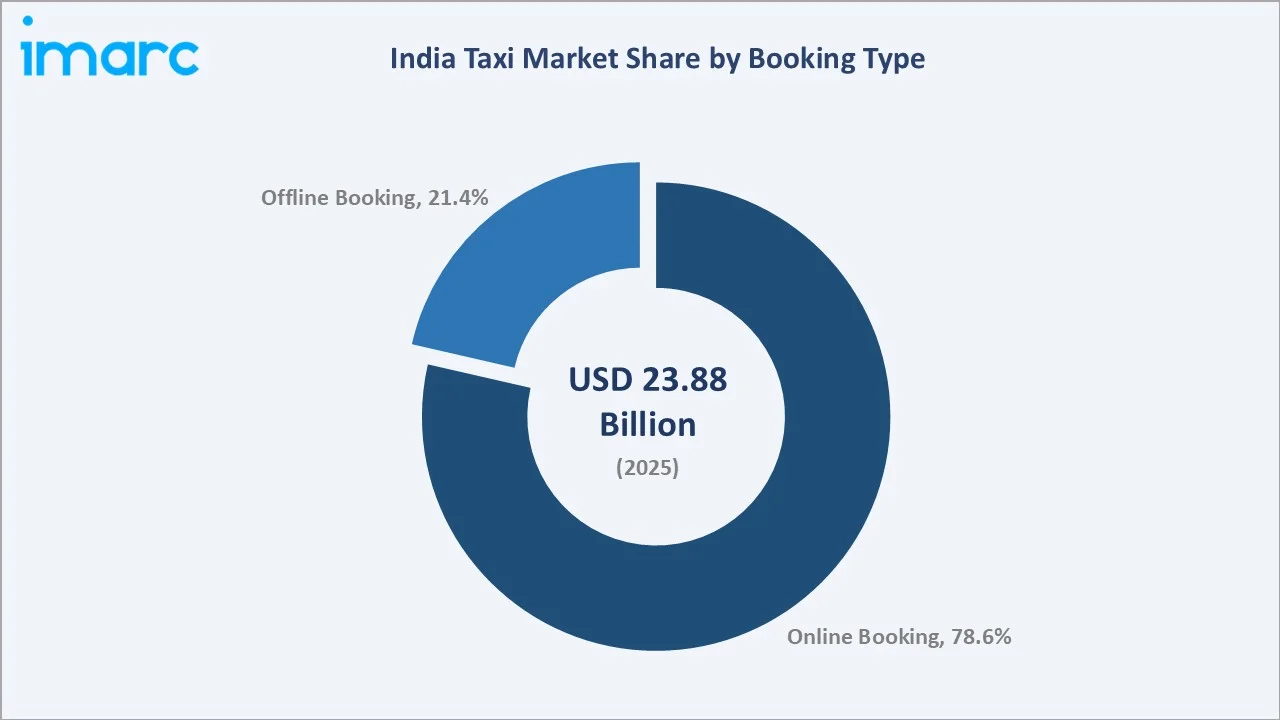

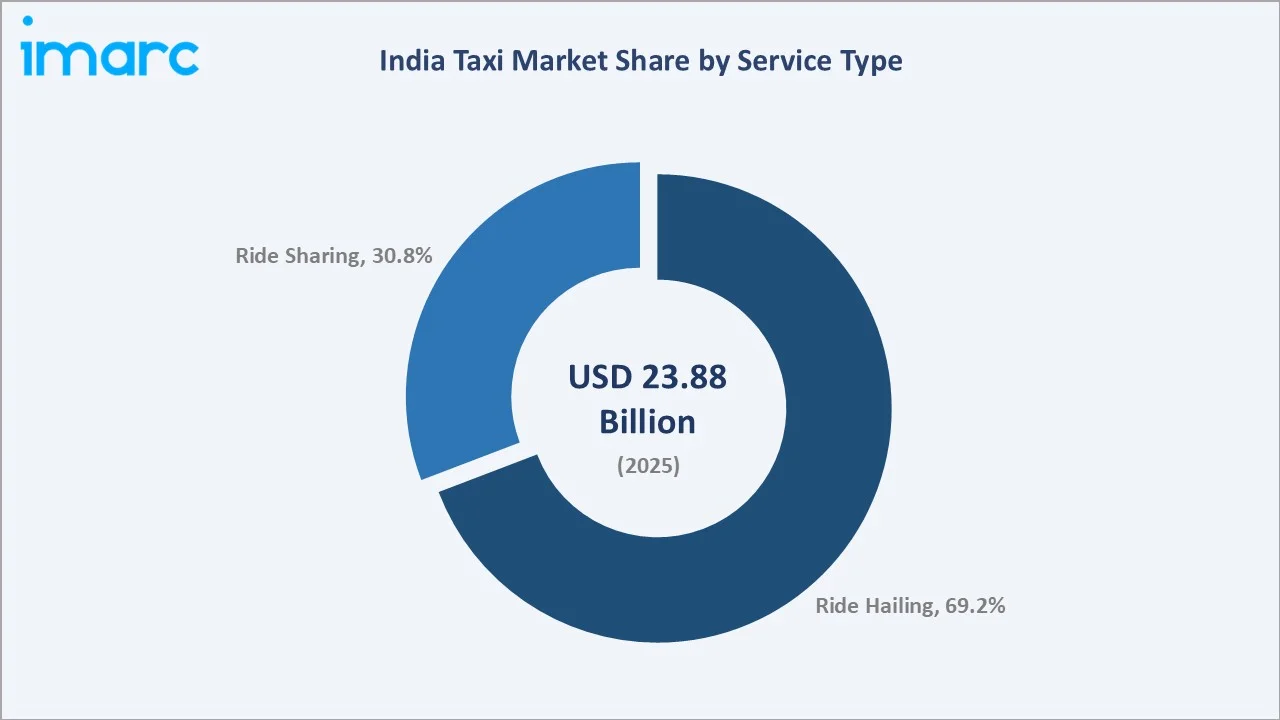

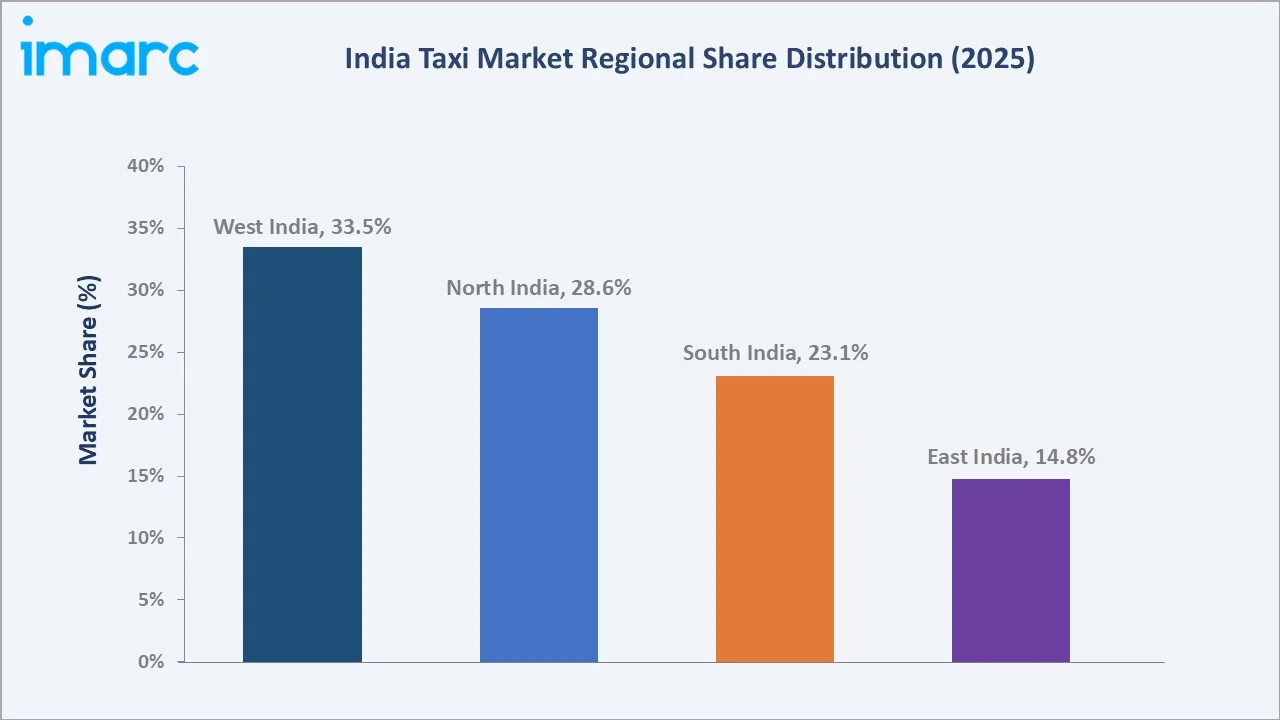

The proliferation of ride-hailing platforms has transformed urban transportation, offering door-to-door connectivity and cashless payments. Online booking dominates at 78.6%, ride hailing leads services at 69.2%, and West India commands 33.5% of the market in 2025, anchored by Mumbai and Pune.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.88 Billion |

|

Forecast Market Size (2034) |

USD 46.88 Billion |

|

CAGR (2026-2034) |

7.39% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Booking Type |

Online Booking (78.6%, 2025) |

|

Dominant Service Type |

Ride Hailing (69.2%, 2025) |

|

Leading Region |

West India (33.5%, 2025) |

The market expanded from USD 16.72 Billion in 2020 to USD 23.88 Billion in 2025, anchored at USD 34.12 Billion in 2030 and forecast to reach USD 46.88 Billion by 2034. The COVID-19 mobility disruption temporarily curtailed demand but did not reverse the structural digital-mobility growth trajectory.

To get more information on this market, Request Sample

Online booking grows fastest as UPI adoption and smartphone penetration deepen across semi-urban corridors. Ride hailing expands above market pace through last-mile connectivity, flexible pricing, and diverse vehicle categories accessed via single-platform interfaces, sustaining the highest-volume booking and service procurement category nationwide.

Executive Summary

The India taxi market reached USD 23.88 Billion in 2025, representing one of the country's highest-growth mobility segments driven by the digital transformation of urban transport. App-based ride-hailing has become the defining commercial format, replacing informal street-hailing across metropolitan and tier-two cities. The market is projected to reach USD 46.88 Billion by 2034.

Online booking at 78.6% dominates through UPI-enabled cashless payments and real-time tracking. Ride hailing at 69.2% leads on convenience and vehicle-category breadth. West India at 33.5% leads through Mumbai's financial dominance, Pune's technology ecosystem, and the region's combined commercial activity and airport infrastructure concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Booking Type |

Online Booking - 78.6% share (2025) |

|

Dominant Service Type |

Ride Hailing - 69.2% market share (2025) |

|

Leading Region |

West India - 33.5% market share (2025) |

|

Market Opportunity |

EV fleet integration; subscription models; tier-2/3 expansion; airport corridors; corporate mobility; multimodal connectivity |

Key Analytical Observations Supporting The Above Data:

- Online Booking at 78.6%: The segment dominates as smartphone-enabled apps offer real-time fares, driver tracking, and UPI payments. Internet expansion into tier-two and tier-three cities broadens the addressable market, with India reaching 806 million internet users by early 2025.

- Ride Hailing at 69.2%: Ride hailing leads through door-to-door convenience, flexible pricing, and diverse vehicle categories on single platforms.

- West India at 33.5%: West India dominates through Mumbai's metropolitan economy and Pune's technology hub. Extensive airport infrastructure, high population density, and the Ahmedabad-Vadodara intercity corridor generate consistent professional transportation demand across the region.

India Taxi Market Overview

The India taxi market encompasses the provision of on-demand passenger transportation services across all vehicle categories, including cars, motorcycles, and other vehicle types, delivered through online and offline booking channels via ride-hailing and ride-sharing service models throughout metropolitan and emerging urban centers.

The ecosystem integrates ride-hailing aggregators, fleet and vehicle providers, driver networks, payment and routing platforms, EV and charging infrastructure providers, and regulatory bodies setting aggregator guidelines. Macroeconomic factors include urbanization, rising disposable incomes, government EV incentives, smartphone proliferation, and investments in digital and transport infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

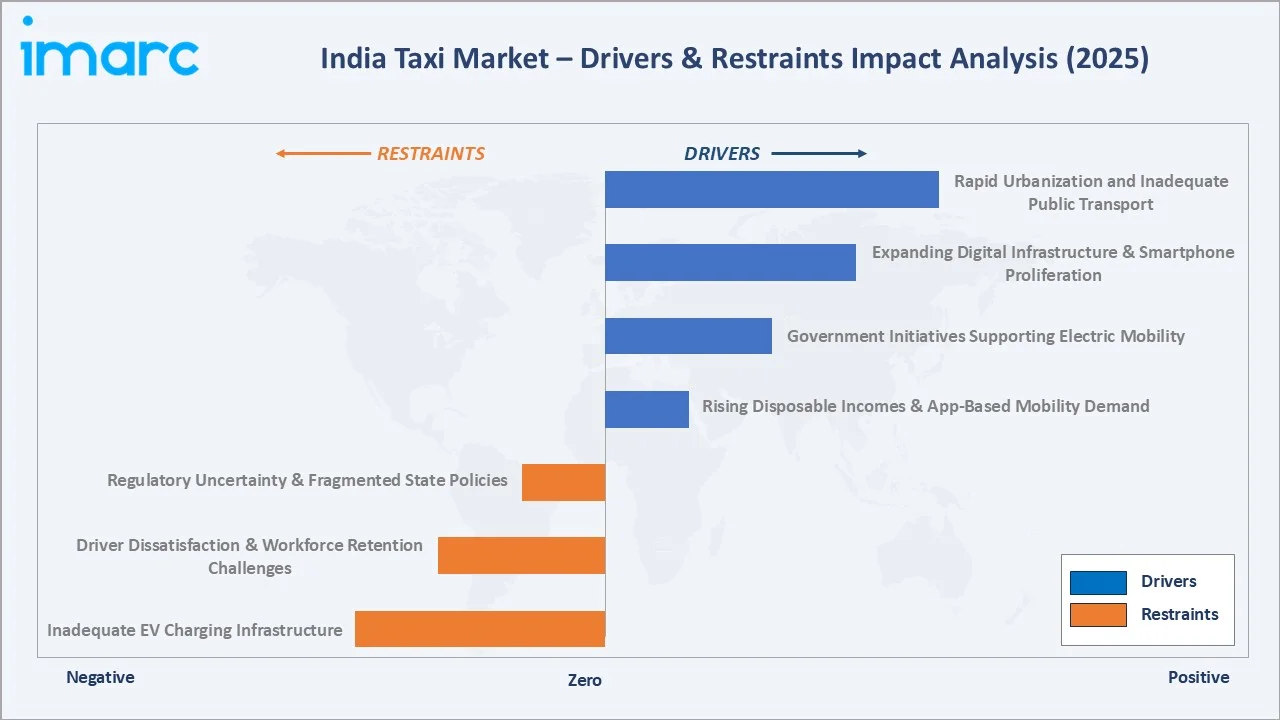

Market Drivers

- Rapid Urbanization and Inadequate Public Transport: Accelerating urbanization sustains taxi demand as residents migrate to cities. India's urban population reached 36.87% in 2024, projected to add 600 million city dwellers by 2036. Gaps between commuter needs and mass-transit capacity position taxis as essential mobility solutions.

- Expanding Digital Infrastructure and Smartphone Proliferation: Affordable smartphones and high-speed mobile internet democratize app-based taxi access. India had nearly 750 million smartphones in use by January 2026. Declining data costs and improved coverage in tier-two and tier-three cities enable platforms to capture emerging digitally connected demand.

- Government Initiatives Supporting Electric Mobility: Supportive government policies promoting electric mobility and sustainable transportation are creating favorable conditions for market expansion. Initiatives focused on encouraging EV adoption, expanding charging infrastructure, and modernizing public transportation networks are helping reduce operational barriers, accelerate fleet electrification, and drive long-term demand for advanced mobility solutions.

- Rising Disposable Incomes and App-Based Mobility Demand: Growing middle-class incomes and changing consumer preferences toward convenient, cashless transport fuel demand. UPI processed over 228 billion transactions valued at INR 300 Lakh Crore in 2025, enabling seamless fare collection that strengthens trust in organized taxi services.

Market Restraints

- Regulatory Uncertainty and Fragmented State Policies: The absence of unified national regulations creates operational complexity across disparate state-level licensing, fare, and service-category rules. Some states restrict categories such as bike taxis, compelling operators to modify offerings and creating service-availability gaps that affect fleet planning and expansion strategies.

- Driver Dissatisfaction and Workforce Retention Challenges: Persistent grievances over commission structures, earning transparency, and social security create retention challenges affecting service quality. Inconsistent earnings from complex incentives and changing commission rates trigger periodic protests in major cities, highlighting the need for equitable revenue-sharing arrangements.

- Inadequate EV Charging Infrastructure: Insufficient charging infrastructure constrains large-scale fleet electrification despite incentives. Higher upfront EV acquisition costs, range anxiety, and extended charging downtime reduce operational efficiency for high-utilization fleets, requiring strategic infrastructure investment to unlock the cost and environmental benefits of electrification.

Market Opportunities

- EV Fleet Integration for Sustainable Mobility: EV adoption reduces operational costs and emissions while capitalizing on government incentives. The FAME II scheme supported 16.29 Lakh EVs by June 2025, enabling operators to build dedicated charging networks and position for long-term advantages in sustainability-conscious urban markets.

- Subscription-Based and Zero-Commission Models: Zero-commission and subscription models improve driver economics and retention. Established aggregators adopt fixed daily or monthly fee structures rather than per-ride commissions, improving income transparency, reducing attrition, and creating new competitive differentiation among driver communities seeking predictable earnings.

Market Challenges

- Intensifying Competition from Cooperatives and New Entrants: Government-backed cooperative platforms emphasizing zero-commission, driver-ownership models introduce a new structural competitive dimension. Subscription-fee cooperatives and specialized bike-taxi entrants pressure incumbent pricing power and margins while forcing continuous service and safety-technology investment.

- Operational Volatility and Funding Pressures: Abrupt operational disruptions among funded operators create market uncertainty for riders, drivers, and fleet assets. Governance and capital constraints can rapidly redirect wallet share, particularly in high-value airport corridors, underscoring trust and continuity as frontline competitive risks during any transition.

Emerging Market Trends

1. Integration of Electric Vehicle (EV) Fleets for Sustainable Mobility

The transition toward EVs is reshaping India's taxi ecosystem as operators reduce operational costs and environmental footprints. Platform companies expand EV fleets to capitalize on government incentives and eco-friendly consumer preference. The FAME II scheme, supporting 16.29 Lakh EVs by June 2025, has accelerated fleet electrification and dedicated charging-network deployment.

2. Emergence of Subscription-Based and Zero-Commission Business Models

Platform economics are shifting as zero-commission and subscription models gain prominence among drivers seeking predictable earnings. This transformation compels established aggregators to adopt fixed daily or monthly fee structures, improving income transparency and reducing driver attrition across competitive urban markets.

3. Expansion of Multimodal Integration and Last-Mile Connectivity

Ride-hailing platforms increasingly integrate with public transit for seamless multimodal experiences. Partnerships with metro rail corporations enable in-app taxi booking through transit applications. The Delhi Metro launched bike-taxi services via its Momentum 2.0 application, enhancing first-mile and last-mile connectivity for commuters.

4. Expansion into Tier-Two and Tier-Three Cities

Operators target underserved tier-two and tier-three cities that are rapidly urbanizing. Regional-language interfaces, simplified onboarding, and affordable vehicle categories capture emerging demand where smartphone adoption accelerates while traditional taxi infrastructure remains underdeveloped, broadening platform geographic reach beyond metropolitan strongholds.

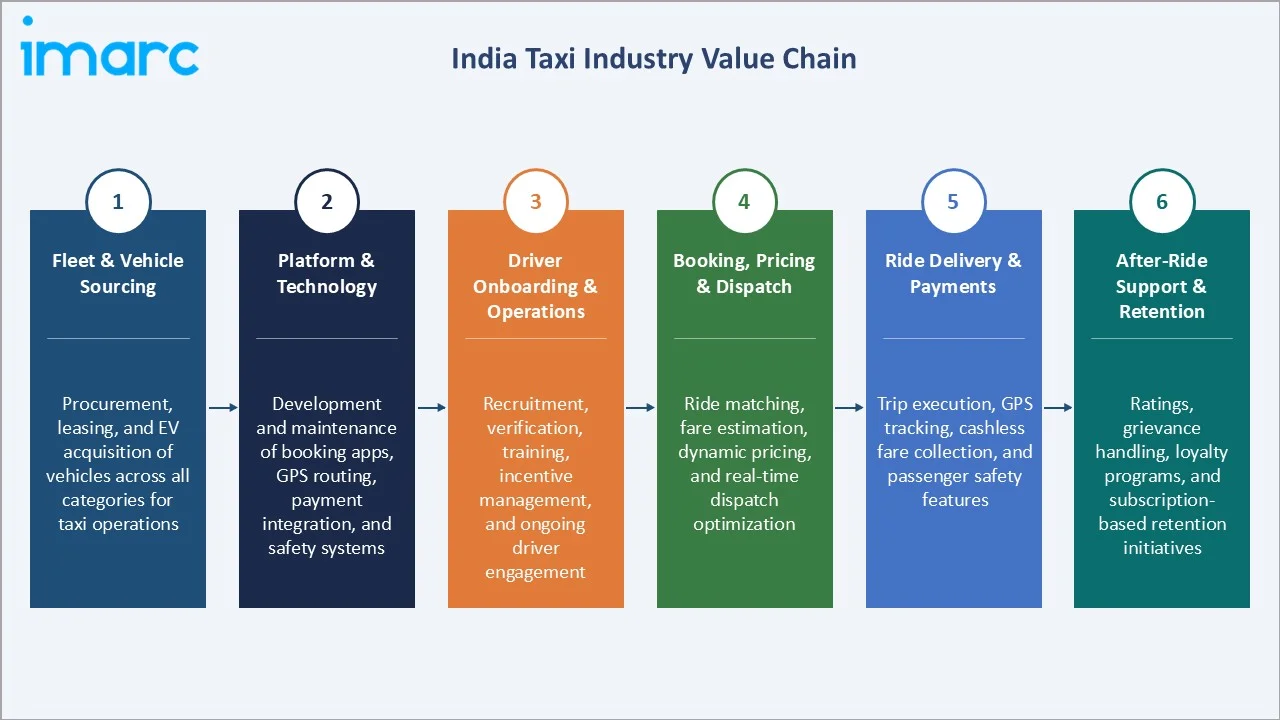

Industry Value Chain Analysis

The India taxi value chain integrates fleet and vehicle sourcing, platform and technology development, driver onboarding and operations, booking, pricing and dispatch, ride delivery and payments, and after-ride support and retention. The commercial architecture has consolidated toward integrated app-based platforms as the primary format, replacing fragmented informal operations.

|

Stage |

Description |

|

Fleet & Vehicle Sourcing |

Procurement, leasing, and EV acquisition of vehicles across all categories for taxi operations |

|

Platform & Technology |

Development and maintenance of booking apps, GPS routing, payment integration, and safety systems |

|

Driver Onboarding & Operations |

Recruitment, verification, training, incentive management, and ongoing driver engagement |

|

Booking, Pricing & Dispatch |

Ride matching, fare estimation, dynamic pricing, and real-time dispatch optimization |

|

Ride Delivery & Payments |

Trip execution, GPS tracking, cashless fare collection, and passenger safety features |

|

After-Ride Support & Retention |

Ratings, grievance handling, loyalty programs, and subscription-based retention initiatives |

The platform and technology tier is the value chain's most commercially critical stage, controlling demand aggregation and pricing power. The fleet and EV sourcing tier is experiencing the most rapid transition as operators electrify fleets to capture government incentives and reduce per-kilometer operating costs.

Technology Landscape in the India Taxi Industry

App-Based Booking and GPS Routing Technology

App-based booking with GPS routing offers real-time fare estimates, driver tracking, and efficient route optimization. These platforms enable advance scheduling, ride-history access, and multiple payment options through unified interfaces, establishing digital channels as the preferred booking method for urban commuters seeking transparency and reliability.

UPI and Digital Payment Integration

Unified Payments Interface integration has transformed fare collection, enabling seamless cashless transactions. With UPI processing over 228 billion transactions in 2025, digital payments remove friction from the booking experience while providing transparent fare calculations and secure mechanisms that build trust in organized transportation services.

EV and Charging Infrastructure Technology

EV fleet technology and dedicated charging infrastructure support sustainable taxi operations. In 2025, the PM E-DRIVE scheme allocated INR 2,000 Crore for charging infrastructure development. Improved battery range, charging-hub networks, and battery-swap models reduce downtime, enhancing operational efficiency across metropolitan corridors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Booking Type |

Online Booking |

78.6% |

2025 |

|

Service Type |

Ride Hailing |

69.2% |

2025 |

|

Vehicle Type |

Cars |

74.8% |

2025 |

|

Region |

West India |

33.5% |

2025 |

By Booking Type

Online booking leads at 78.6% in 2025, reflecting the digital transformation of consumer behavior driven by smartphone penetration and UPI adoption. Ride-hailing applications offer real-time fares, driver tracking, and multiple payment options, establishing online channels as the dominant, highest-revenue booking category in the market.

To access detailed market analysis, Request Sample

Offline booking at 21.4% captures street-hailing, taxi stands, and phone bookings, primarily in semi-urban and tier-three areas where smartphone literacy is still developing. Its share continues declining as internet connectivity and app-based adoption expand into emerging urban corridors across the country.

By Service Type

Ride hailing leads at 69.2% through door-to-door convenience, flexible pricing, and diverse vehicle categories on single platforms. The segment's dominance reflects consumer preference for on-demand transportation with safety features including driver identity, GPS tracking, and emergency-response integration that reduce street-hailing uncertainty.

Ride sharing at 30.8% captures cost-conscious commuters and intercity carpooling, reducing travel costs and congestion. Platforms incorporate shared-ride options to meet growing demand for affordable, eco-friendly mobility, with the segment benefiting from rising fuel prices and sustainability awareness across metropolitan regions.

Regional Market Insights

|

Region |

Share (2025) |

Key Characteristics |

|

West India |

33.5% |

Largest regional market driven by concentrated commercial and financial activity, high population density, and extensive airport infrastructure |

|

North India |

28.6% |

Significant market supported by large metropolitan demand, corporate mobility requirements, and growing urban commuter base |

|

South India |

23.1% |

Driven by technology hub cities, strong app-based adoption, and expanding ride-hailing penetration into emerging urban centers |

|

East India |

14.8% |

Emerging market with rising smartphone adoption and gradual expansion of organized taxi services across urban and semi-urban areas |

West India, at 33.5%, leads as the largest regional market, followed by North India at 28.6%. South India contributes 23.1% driven by technology-hub city demand, while East India at 14.8% represents an early-stage but growing market with increasing organized-taxi penetration.

West India and North India together account for over 62% of total market revenue in 2025, reflecting the concentration of commercial activity, airport infrastructure, and digital mobility adoption in these two regions. South and East India offer the highest incremental growth potential through the forecast period.

Competitive Landscape

The India taxi market is highly competitive, characterized by dominant ride-hailing platforms alongside emerging community-driven cooperatives and specialized providers. Major aggregators compete through pricing strategies, service diversification, and technology investments while facing pressure from subscription-based models challenging traditional commission structures.

|

Company Name |

Key Offerings |

Market Position |

Core Strength |

|

Uber Technologies Inc. |

Ride Hailing, Uber Reserve, Uber Auto, Uber Moto |

Market Leader |

Global ride-hailing leader with extensive city coverage, AI route optimization, and improving India unit economics. |

|

Roppen Transportation |

Bike Taxi, Auto, Cab, Subscription Model |

Strong Challenger |

Fast-growing bike-taxi aggregator with subscription revenue model and strong metro-city growth trajectory. |

|

Wise Travel India Limited |

Airport Cabs Services, Outstation Cabs Services, Hourly Rental |

Established Player |

NSE-listed corporate mobility specialist operating with blue-chip enterprise clients |

|

Suol Innovations Ltd |

Ride Hailing, Intercity, Freight, Peer-Negotiated Fare Model |

Strong Challenger |

Second-largest ride-hailing app globally by downloads; peer price-negotiation model differentiates from commission-based peers |

|

Tajwaycabs |

Airport Transfers, Outstation Cabs, Local Hourly Rental, One-Way Intercity |

Niche Specialist |

Delhi-NCR focused operator offering economical outstation and airport transfer services with transparent per-km pricing |

Key players include Uber Technologies Inc., Roppen Transportation, Wise Travel India Limited, Suol Innovations Ltd, Tajwaycabs, and others.

Key Company Profiles

Uber Technologies Inc.

Uber Technologies Inc. is a global mobility technology company with a strong presence in the India taxi market through its ride-hailing, auto, and two-wheeler offerings across metropolitan and tier-two cities.

- Key Offerings: Ride Hailing, Uber Reserve, Uber Auto, Uber Moto, and premium vehicle categories.

- Strategic Focus: Expanding pre-booked airport products, EV fleet partnerships, and safety-technology differentiation across key Indian metropolitan markets.

Roppen Transportation

Roppen Transportation, operating Rapido, is a leading bike-taxi and multi-category aggregator with strong growth across Indian metros through its subscription-based revenue model.

- Key Offerings: Bike Taxi, Auto, Cab services, and subscription-based driver plans.

- Strategic Focus: Expanding bike-taxi collaborations, scaling its subscription-fee model to improve driver economics, and growing presence in selected metros and tier-two cities.

Market Concentration Analysis

The India taxi market is moderately concentrated at the ride-hailing aggregator level, with the top two players accounting for a significant share of organized app-based ride volume. Regional and specialized operators serve tier-two, airport, and intercity niches. Concentration is gradually shifting as cooperatives and subscription-model entrants create new competitive segments.

Investment & Growth Opportunities

Highest Growth Segments

Online booking, ride hailing, EV taxi fleets, airport-corridor services, corporate mobility, and tier-two and tier-three city expansion represent the highest-growth investment vectors through 2034, supported by urbanization, digital infrastructure expansion, and government electric-mobility incentives.

Emerging Investment Opportunities

EV taxi fleet operations represent the market's highest-value emerging opportunity, as airport and premium corridors command yield premiums while government subsidies offset higher acquisition costs. Corporate duty-of-care mandates and decentralized office shuttle programs create structurally growing demand for premium fleet categories through the forecast period.

Investment Themes

- EV fleet and charging infrastructure as a structural cost advantage through 2034: Operators achieving below-market per-kilometer operating cost through EV adoption and proprietary charging hubs create a sustainable fare-economics advantage that cannot be easily replicated by competitors dependent on conventional vehicles in a rising-fuel-cost environment.

- Tier-two and tier-three city expansion capturing the fastest-growing demand pool: Rapidly urbanizing smaller cities producing a growing share of GDP require organized taxi supply, a market currently underserved by informal operators, creating scope for app-based platforms to capture high-growth, low-penetration demand.

Future Market Outlook (2026-2034)

The India taxi market is projected to grow from USD 23.88 Billion in 2025 to USD 46.88 Billion by 2034, delivering a 7.39% CAGR. The anchor value of USD 34.12 Billion in 2030 represents the market at its most transformative inflection, with EV fleets, subscription models, and multimodal integration becoming standard commercial features.

Three structural forces define growth through 2034. Urbanization creates a self-reinforcing demand cycle as city populations expand toward 600 million by 2036. Smartphone and UPI penetration deepens app-based adoption across tier-two and tier-three corridors. Government EV incentives accelerate fleet electrification, lowering operating costs and supporting sustainable, scalable taxi operations nationwide.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including ride-hailing platform executives, fleet operators, EV mobility specialists, corporate mobility leads, and state transport authority representatives across major metropolitan markets.

Secondary Research

Secondary research encompassed company filings, World Bank urbanization indicators, Ministry of Road Transport and Highways data, PM E-DRIVE and FAME II scheme documentation, DataReportal digital adoption statistics, UPI transaction reports, and state aggregator policy guidelines. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a demand-based bottom-up model: (i) urban population and smartphone-user forecasts; (ii) ride frequency per active user by city tier; (iii) average fare per ride by booking type and service type; and (iv) digital-adoption and EV-penetration adjustment factors applied across the forecast period.

India Taxi Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Booking Types Covered |

Online Booking, Offline Booking |

|

Service Types Covered |

Ride Hailing, Ride Sharing |

|

Vehicle Types Covered |

Cars, Motorcycle, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Companies Covered |

Uber Technologies Inc., Roppen Transportation, Wise Travel India Limited, Suol Innovations Ltd, Tajwaycabs, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Taxi Market Report

The India taxi market reached USD 23.88 Billion in 2025, driven by online booking dominant at 78.6%, ride hailing leading services at 69.2%, and West India commanding 33.5% market share through concentrated commercial and airport infrastructure demand.

The India taxi market grows at 7.39% CAGR during 2026-2034, reaching USD 46.88 Billion by 2034. This reflects rapid urbanization, expanding smartphone and internet penetration, government electric-mobility incentives, and rising disposable incomes across growing urban corridors.

Online booking leads at 78.6%, capturing app-based ride-hailing through smartphone penetration, UPI cashless payments, and real-time tracking. The segment grows fastest as internet connectivity expands into tier-two and tier-three cities beyond traditional metropolitan strongholds.

Ride hailing leads at 69.2% through door-to-door convenience, flexible pricing, and diverse vehicle categories on single platforms, with safety features including driver identity, GPS tracking, and emergency-response integration driving adoption.

West India leads at 33.5%, followed by North India at 28.6%, South India at 23.1%, and East India at 14.8%. West India's leadership reflects Mumbai's financial dominance, Pune's technology ecosystem, and extensive airport infrastructure.

Leading companies include Uber Technologies Inc., Roppen Transportation, Wise Travel India Limited, Suol Innovations Ltd, Tajwaycabs, and others.

The India taxi market is projected to reach approximately USD 34.12 Billion by 2030, with EV fleets, zero-commission and subscription models, multimodal transit integration, and tier-two and tier-three city expansion becoming standard market features.

Three priority opportunities: EV taxi fleet and charging infrastructure development, tier-two and tier-three city market expansion, and corporate mobility and airport-corridor premium service tiers commanding higher yield premiums through the forecast period.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)