India Telecom Market Size, Share, Trends and Forecast by Services and Region, 2026-2034

India Telecom Market Size, Share, Trends & Forecast (2026-2034)

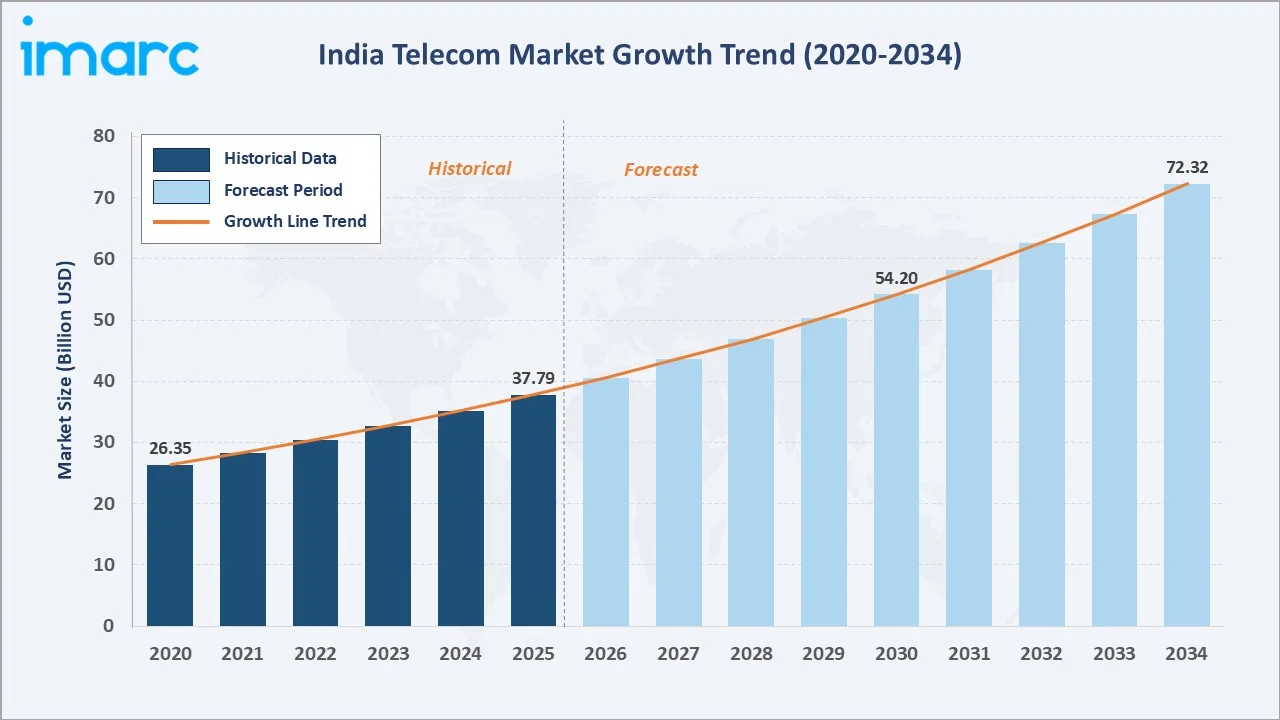

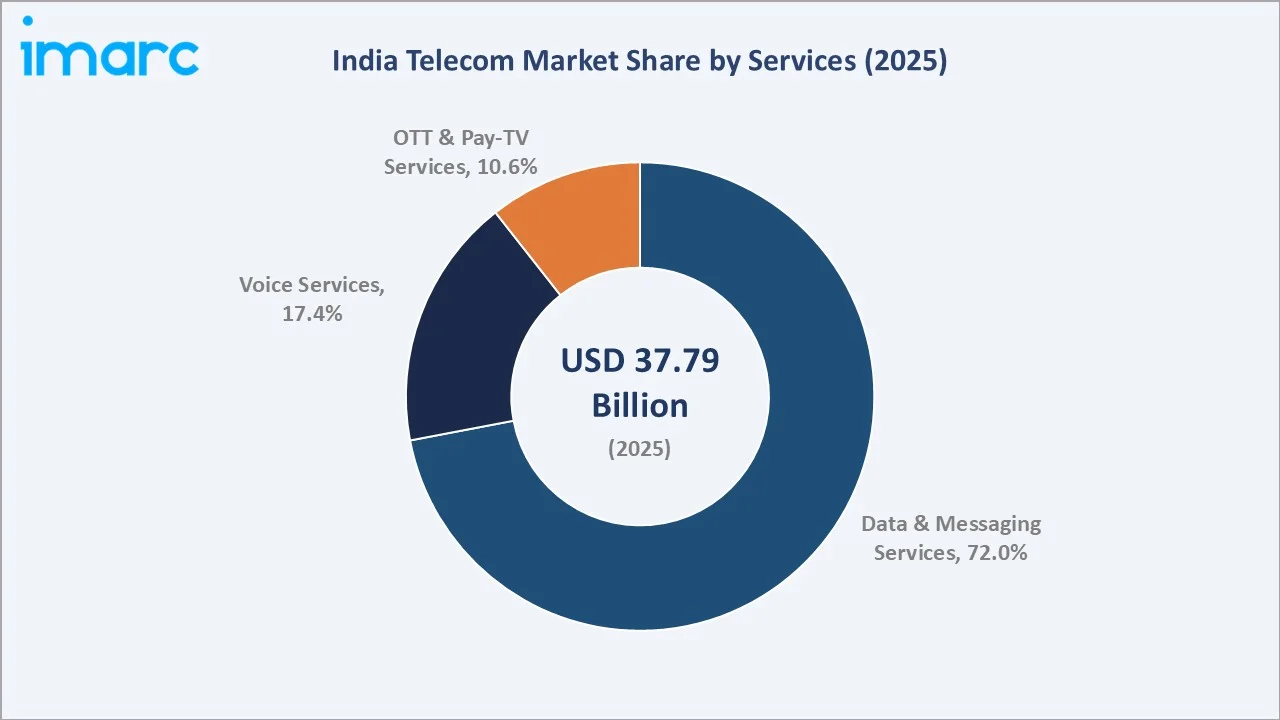

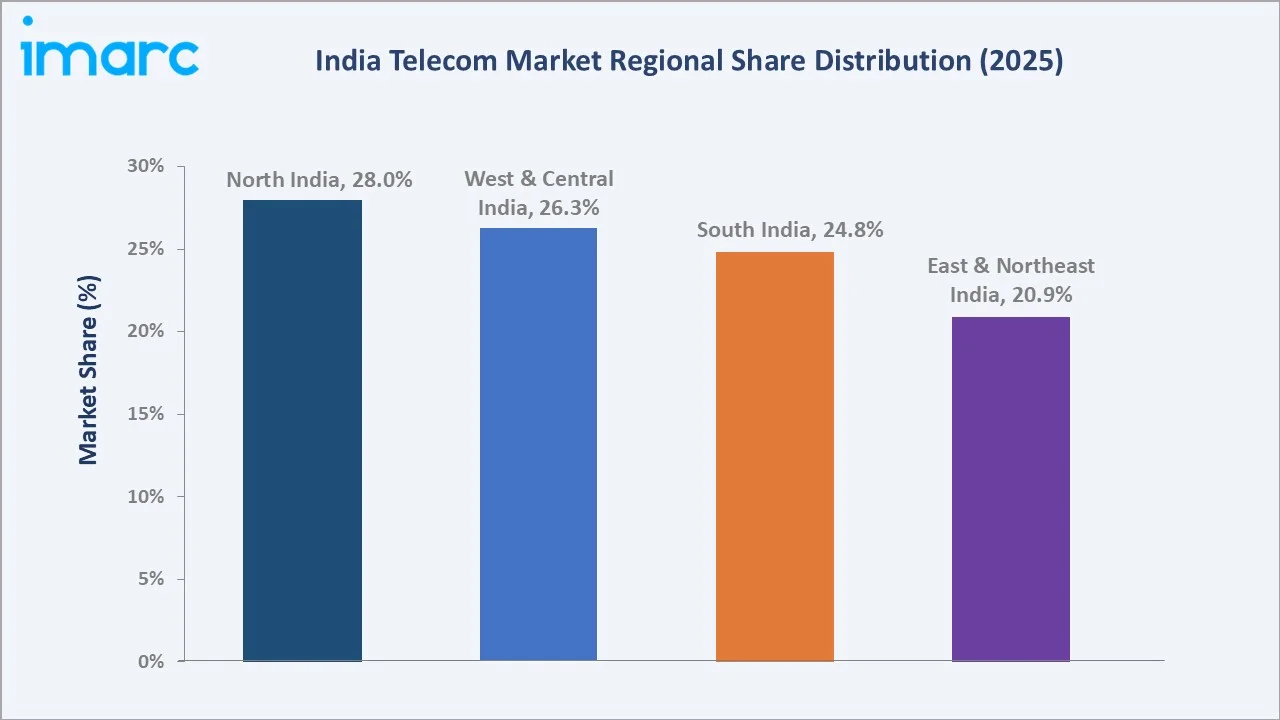

The India telecom market size was valued at USD 37.79 Billion in 2025 and is projected to reach USD 72.32 Billion by 2034, exhibiting a CAGR of 7.48% during the forecast period 2026-2034. Rapid 5G network rollout, surging mobile data consumption, and government-led digital connectivity programmes including BharatNet and Digital India are the primary forces driving India telecom market growth. Data and Messaging Services dominate with a commanding 72.0% share in 2025, reflecting the transformation to a data-first telecom economy. North India leads regionally at 28.0%, driven by dense subscriber populations in Delhi NCR and Uttar Pradesh.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 37.79 Billion |

|

Forecast Market Size (2034) |

USD 72.32 Billion |

|

CAGR (2026-2034) |

7.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (28.0% share, 2025) |

|

Fastest Growing Region |

East & Northeast India (Accelerating connectivity) |

|

Leading Segment (by Services) |

Data & Messaging Services (72.0%, 2025) |

|

Second Segment (by Services) |

Voice Services (17.4%, 2025) |

The India telecom market growth trajectory from 2020 through 2034 contrasts a robust historical expansion from USD 26.35 Billion against an accelerating forecast curve, powered by 5G commercialization, rising ARPU, enterprise digital transformation, and India's emergence as the world's second-largest smartphone market with 740 million connected users.

To get more information on this market, Request Sample

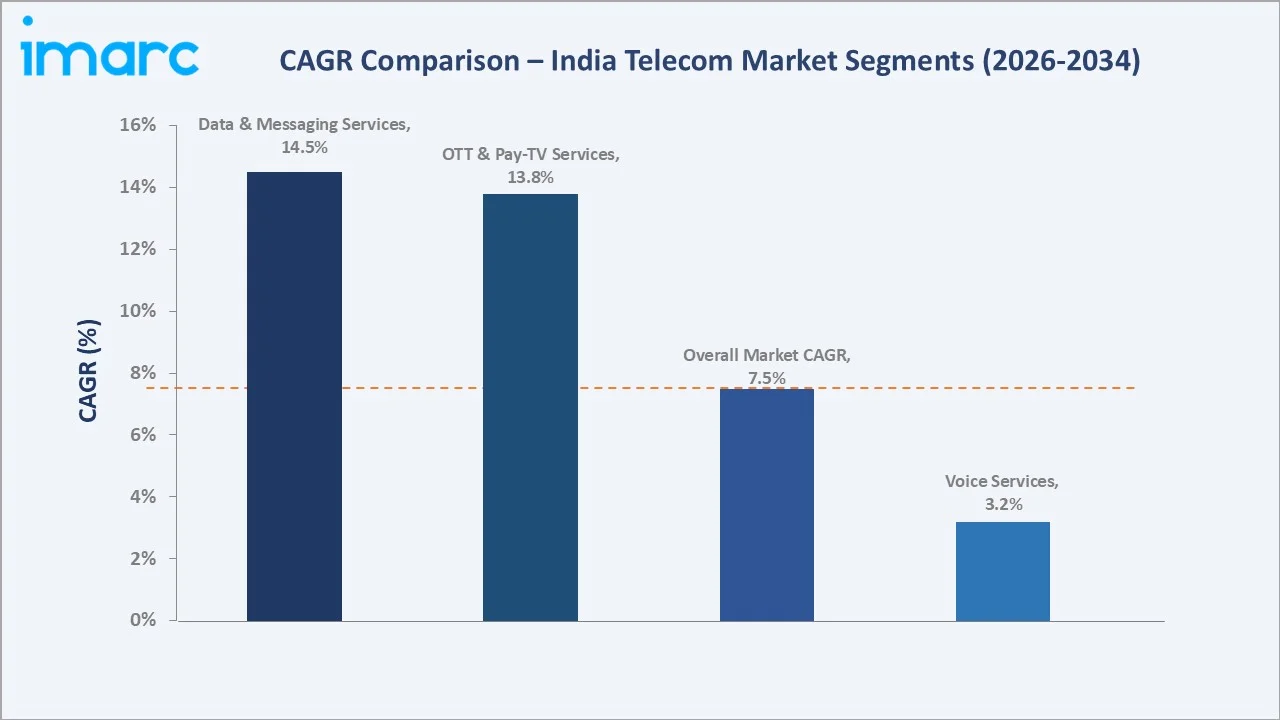

Segment-level CAGR comparisons confirm Data and Messaging Services as the highest-growth category at 14.5% CAGR through 2034, while OTT and Pay-TV services expand at 13.8%, and Voice Services contract as data bundles increasingly include voice at no incremental cost.

Executive Summary

The India telecom market is undergoing its most profound structural transformation since the Jio disruption of 2016. Valued at USD 37.79 Billion in 2025, it is forecast to reach USD 72.32 Billion by 2034 at a CAGR of 7.48%. The 5G spectrum auction of 2022, which raised INR 1.5 Lakh Crore and saw Reliance Jio and Bharti Airtel secure the largest blocks. India crossed 1200 million 5G subscribers in March 2025, making it one of the fastest 5G adoption markets globally.

Data and Messaging Services account for 72.0% of market revenue in 2025, up from approximately 52% in 2020, reflecting the structural migration of ARPU from voice to data. India's average data consumption reached 24.7 GB per user per month in 2025, ranking among the highest globally, driven by affordable data tariffs, JioPhone-enabled rural internet access, and the proliferation of short-video and OTT content platforms. Voice Services retain 17.4% of revenue, while OTT and Pay-TV Services contribute 10.6%, growing rapidly as Jio Cinema, Airtel Xstream, and regional OTT platforms compete for India's 600+ million internet users.

North India commands 28.0% of the market, anchored by Delhi NCR's enterprise telecom demand and UP's massive subscriber base and million wireless connections. South India holds 24.8%, driven by Bangalore's technology-sector enterprise data demand and Chennai's submarine cable landing stations. The India telecom market outlook is highly positive, with 5G enterprise services, satellite connectivity (Starlink, OneWeb), and the BharatNet Phase 3 rural broadband programme collectively expanding total addressable market through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Services) |

Data & Messaging Services – 72.0% share (2025) |

|

Second Segment (Services) |

Voice Services – 17.4% share (2025) |

|

Third Segment (Services) |

OTT & Pay-TV Services – 10.6% share (2025) |

|

Fastest Growing Segment |

Data & Messaging – ~14.5% CAGR (2026-2034) |

|

Leading Region |

North India – 28.0% revenue share (2025) |

|

Fastest Growing Region |

East & Northeast India – accelerating at ~14.8% CAGR |

|

Total Wireless Subscribers |

1.17 Billion (March 2025, TRAI) |

|

5G Subscribers |

100+ Million (March 2025) |

|

Top Companies |

Reliance Jio, Bharti Airtel, Vodafone Idea (Vi), BSNL, Tata Comms |

|

Market Opportunity |

Enterprise 5G services, satellite broadband, BharatNet Phase 3 |

Key Analytical Observations:

- Data & Messaging Services' 72.0% dominance in 2025 reflects India's position as the world's lowest mobile data price market at USD 0.09 per GB in 2025, driving monthly per-user data consumption of 24.7 GB - the second highest globally after Finland, and underpinning relentless ARPU growth for leading operators.

- Voice Services' 17.4% share continues its structural decline as bundled voice minutes in data plans progressively erode standalone voice revenue. However, absolute voice traffic remains high at 7.5 trillion minutes per year in 2025, supporting interconnection revenue and rural ARPU.

- OTT & Pay-TV Services at 10.6% are the fastest-growing revenue contribution, driven by Jio Cinema's 450+ million monthly active users, Disney+ Hotstar's 50 million subscribers, and the proliferation of regional-language OTT platforms across Hindi, Tamil, Telugu, and Bengali content markets.

- North India's 28.0% leadership is driven by Delhi NCR's concentration of enterprise telecom contracts, UP's 240 million wireless subscribers, and the government's PM Gati Shakti infrastructure programme anchoring extensive fibre and 5G network investments in the northern corridor.

- 5G subscriber base surpassed 100 million by March 2025, making India one of the top-5 countries globally by 5G adoption speed. Jio and Airtel have deployed 5G in 700+ cities, with Jio's True 5G standalone network covering 95% of urban India by Q1 2025.

- East & Northeast India is the fastest-growing region, benefiting from BharatNet fibre deployments, North East Special Infrastructure Development Scheme (NESIDS) connectivity projects, and the government's Digital North East Vision unlocking previously underpenetrated subscriber markets.

India Telecom Market Overview

The India telecom market encompasses mobile (wireless) telecommunications, fixed-line telephony, broadband internet, enterprise data services, and Over-The-Top (OTT) content delivery. Service providers include facilities-based operators (Jio, Airtel, Vi, BSNL), virtual network operators (MVNOs), internet service providers (ISPs), and OTT platform operators. The India telecom industry is regulated by the Telecom Regulatory Authority of India (TRAI) and the Department of Telecommunications (DoT), with spectrum allocation managed through transparent auction processes.

Macro-economic enablers include India's 1.44 billion population with a median age of 28 years, a digital-native youth demographic, and government initiatives including Digital India, BharatNet and PM Wani (public Wi-Fi hotspot scheme). India's Telecom Act 2023, replacing the colonial-era Indian Telegraph Act 1885, introduced a modernised regulatory framework enabling spectrum sharing, satellite communication licensing, and telecom project facilitation, fundamentally expanding the India telecom market trends and investment landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

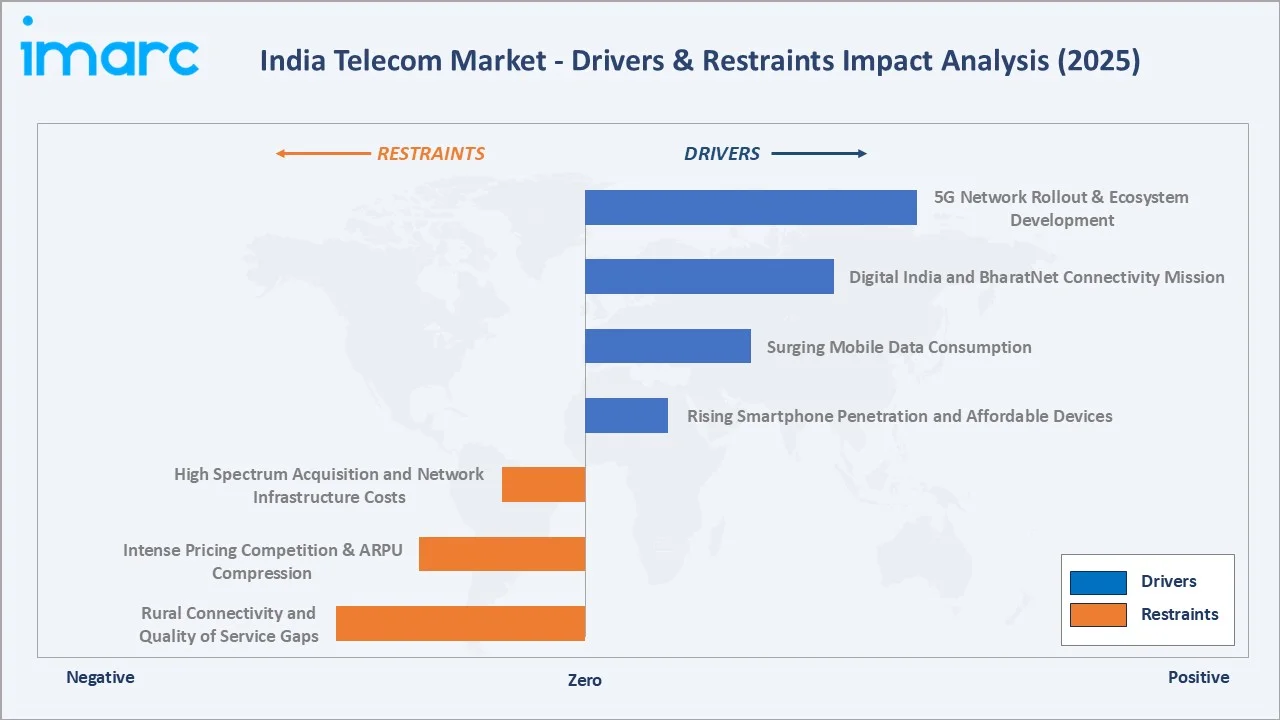

Market Drivers

- 5G Network Rollout and Ecosystem Development: India's 5G spectrum auction raised INR 1.5 Lakh Crore (approximately USD 18 Billion) in 2022, with Reliance Jio securing 24,740 MHz and Bharti Airtel 19,867 MHz across sub-6 GHz and mmWave bands. By Q1 2025, 5G services were live in 750+ Indian cities, with Jio and Airtel committing USD 35+ Billion in combined 5G capex through 2027. Enterprise 5G use cases spanning smart manufacturing (Industry 4.0), connected healthcare, and autonomous logistics are unlocking new high-ARPU revenue streams beyond consumer broadband.

- Digital India and BharatNet Connectivity Mission: BharatNet Phase 3, announced in 2024 with INR 1.39 Lakh Crore (approximately USD 16.7 Billion) in approved expenditure, targets connecting all 6.4 lakh villages with optical fibre broadband by 2026. The programme has already connected 2.15 lakh gram panchayats as of 2025, unlocking internet access for 800+ million rural Indians and driving mass-market broadband subscriber additions for all telecom operators.

- Surging Mobile Data Consumption: India's total wireless data traffic reached 290 exabytes in FY 2025. The average Indian mobile subscriber consumed 24.7 GB per month in 2025, up from 11.2 GB in 2021. Short-video platforms (Instagram Reels, YouTube Shorts, MX TakaTak), OTT streaming, and cloud gaming are the primary demand drivers. India adds approximately 10-12 million new internet users every month, creating a continuously expanding monetisable subscriber base.

- Rising Smartphone Penetration and Affordable Devices: India's smartphone installed base exceeded 800 million in 2025, with affordable 4G/5G handsets available from INR 6,000-8,000. JioPhone Next, developed jointly with Google and priced at INR 999 under an instalment scheme, has unlocked internet access for first-time users in semi-urban and rural markets, driving subscriber growth at the bottom of the pyramid and expanding ARPU from feature phone to smartphone usage patterns.

Market Restraints

- High Spectrum Acquisition and Network Infrastructure Costs: India's spectrum auction pricing, while structured, requires operators to commit multi-billion dollar capex cycles simultaneously. India's two private operators (Jio, Airtel) carry a combined spectrum deferred payment liability of approximately INR 1.09 Trillion as of 2025. This financial burden limits available free cash flow for network quality improvements, constraining Vi's 5G rollout timeline and creating competitive asymmetry in the market.

- Intense Pricing Competition and ARPU Compression; India’s mobile ARPU remains among the lowest globally, with Reliance Jio reporting ARPU of around ₹210–215 per month, while Bharti Airtel maintains a higher ARPU of ₹250–260, reflecting differing monetization strategies across operators. The Jio disruption of 2016 structurally compressed tariffs, and while selective tariff hikes in 2024 boosted ARPU by 12-15%, sub-USD 3 monthly ARPU limits return on invested capital for the industry's USD 100+ Billion infrastructure base.

- Rural Connectivity and Quality of Service Gaps: Despite BharatNet progress, 42% of India's rural population remains without reliable broadband access in 2025. Rural tower sites face challenges including power availability, right-of-way acquisition complexity, and vandalism. Maintaining service quality parity between urban and rural networks requires sustained government and operator investment that stretches financial and operational resources.

Market Opportunities

- Enterprise 5G and Private Network Services: Driven by smart factory deployments in automotive (Tata Motors, Maruti), pharmaceuticals (Sun Pharma, Cipla), and ports (JNPT, Mundra). TRAI's private captive 5G network guidelines, enabling large enterprises to deploy dedicated 5G networks without telecom licences, unlocking a new B2B revenue stream with ARPU 50-80x higher than consumer mobile.

- Satellite Broadband and Non-Terrestrial Networks (NTN): OneWeb (Eutelsat, Bharti-backed) and Starlink (SpaceX) received DoT licenses in 2024 and 2025 respectively, launching commercial satellite broadband services in India. These services address remote areas beyond terrestrial network coverage, including Himalayan, island, and tribal region markets. ISRO's Gagan and NTN integration with 5G NR (Rel-17) standards are enabling hybrid terrestrial-satellite connectivity, creating a new technology layer for India's last-mile connectivity challenge.

- OTT and Digital Content Service Bundling: India's OTT subscription market is projected to reach USD 5 Billion by 2027. Telecom operators are increasingly bundling OTT subscriptions (JioCinema, Airtel Xstream, SonyLIV) with mobile plans, improving subscriber stickiness and ARPU by INR 40-80 per month.

Market Challenges

- Vodafone Idea (Vi) Financial Viability and Market Concentration: Vi's strained financial position, with net debt of approximately INR 2.2 Lakh Crore and delayed 5G rollout, risks accelerating the effective consolidation of India's telecom market to a two-operator private duopoly (Jio + Airtel). Market concentration at this level could reduce competitive pressure on tariffs and service quality, drawing heightened TRAI regulatory scrutiny.

- Cybersecurity and Telecom Infrastructure Protection: India's CERT-In reported a 22.68 lakh telecom infrastructure-targeted cyberattacks in 2024, including SIM swap fraud, Diameter protocol vulnerabilities, and SS7 exploitation. The Telecom Act 2023's security provisions and DoT's Telecom Cyber Security Rules 2024 impose new compliance obligations, requiring significant investment in network security infrastructure across all licensed operators.

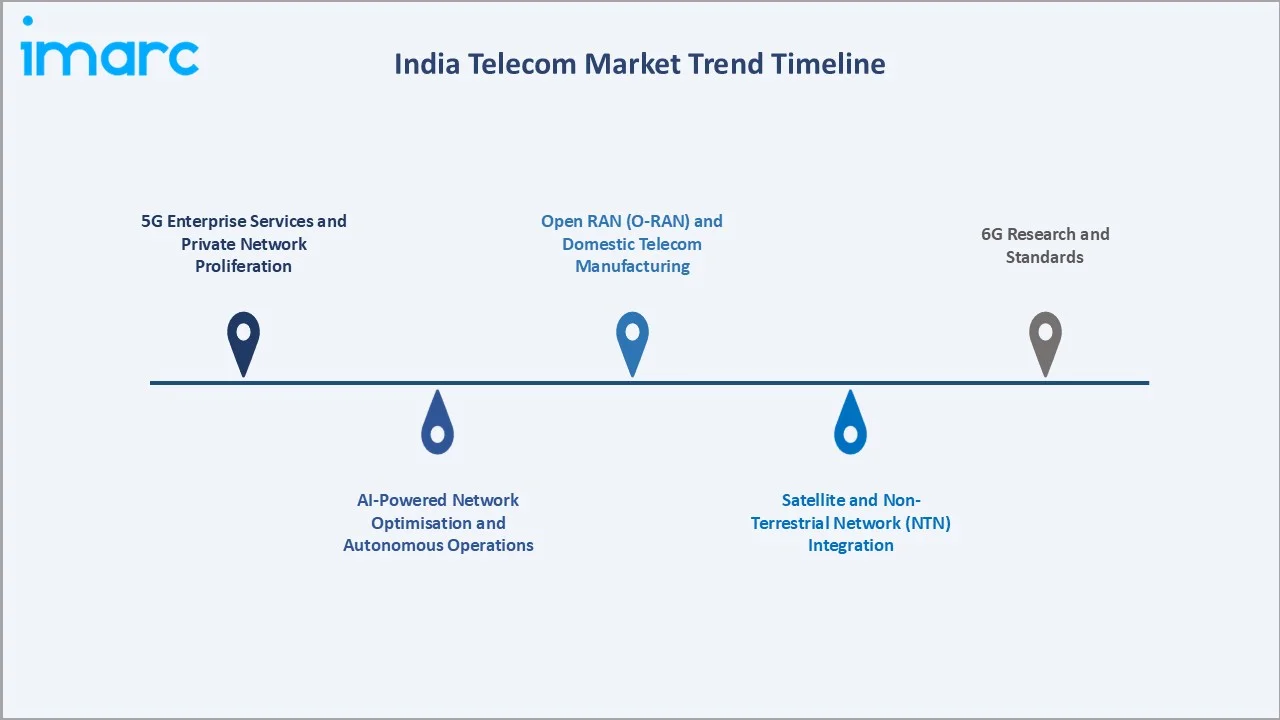

Emerging Market Trends

1. 5G Enterprise Services and Private Network Proliferation

India's 5G rollout has transitioned from consumer coverage to enterprise monetisation. Private captive 5G networks are being deployed in Gujarat Industrial Development Corporation (GIDC) industrial zones, Tata Motors' Pune plant, and JNPT port, with reported latency of under 2ms enabling real-time robotic process automation and AGV (automated guided vehicle) control. Private 5G networks are emerging as a key B2B revenue opportunity for Indian telecom operators, with early deployments across manufacturing, healthcare, and industrial sectors. While adoption is still at a nascent stage, global forecasts indicate strong growth in enterprise 5G, with India expected to capture a significant share as deployments scale..

2. AI-Powered Network Optimisation and Autonomous Operations

Jio and Airtel are deploying AI/ML-driven network management platforms that autonomously optimise spectrum allocation, predict cell congestion, and proactively resolve network anomalies without human intervention. Ericsson's Intelligent Automation Platform and Nokia's AVA AI suite are being integrated into Indian network operation centres, reducing operational costs by 15-20% while improving network quality scores. AI-driven personalised tariff recommendation engines are improving ARPU by matching subscribers to optimal plans.

3. Satellite and Non-Terrestrial Network (NTN) Integration

India's DoT licensed 7 satellite internet providers by March 2025, including Starlink, OneWeb, Amazon Kuiper, and Jio Space Technology (ISRO-backed). Satellite broadband is addressing remote connectivity gaps in Lakshadweep, Andaman & Nicobar, Himalayan regions, and tribal areas where terrestrial fibre is economically unviable. 3GPP Release-17's NTN standard enables seamless handoff between 5G terrestrial and satellite networks, positioning India as an early adopter of hybrid connectivity architecture.

4. Open RAN (O-RAN) and Domestic Telecom Manufacturing

India’s Telecom Technology Development Fund (TTDF), launched in 2022, has approved over 130 projects with funding exceeding ₹542 crore, supporting indigenous development of 4G/5G/6G technologies and accelerating domestic telecom equipment innovation.. Companies including VVDN Technologies, Tejas Networks (Tata), and HFCL are developing O-RAN compliant radio units and baseband units for deployment in BSNL's network and for export. DoT's mandate for BSNL to deploy domestically manufactured 4G/5G equipment is creating a validation pipeline for Indian telecom hardware, targeting USD 10 Billion in telecom equipment exports by 2030.

5. Digital Rupee and Telecom-FinTech Convergence

India's UPI ecosystem processed 228 Billion transactions worth INR 299.7 Lakh Crore in FY 2024-25, with telecom operators playing a critical infrastructure role through USSD-based banking for feature phone users. Jio Financial Services and Airtel Payments Bank are leveraging telecom subscriber data and distribution networks to build India's largest digital financial services platforms, creating a convergence of telecom, fintech, and insurance that could add USD 4-6 Billion in additional revenue streams for integrated operators by 2030.

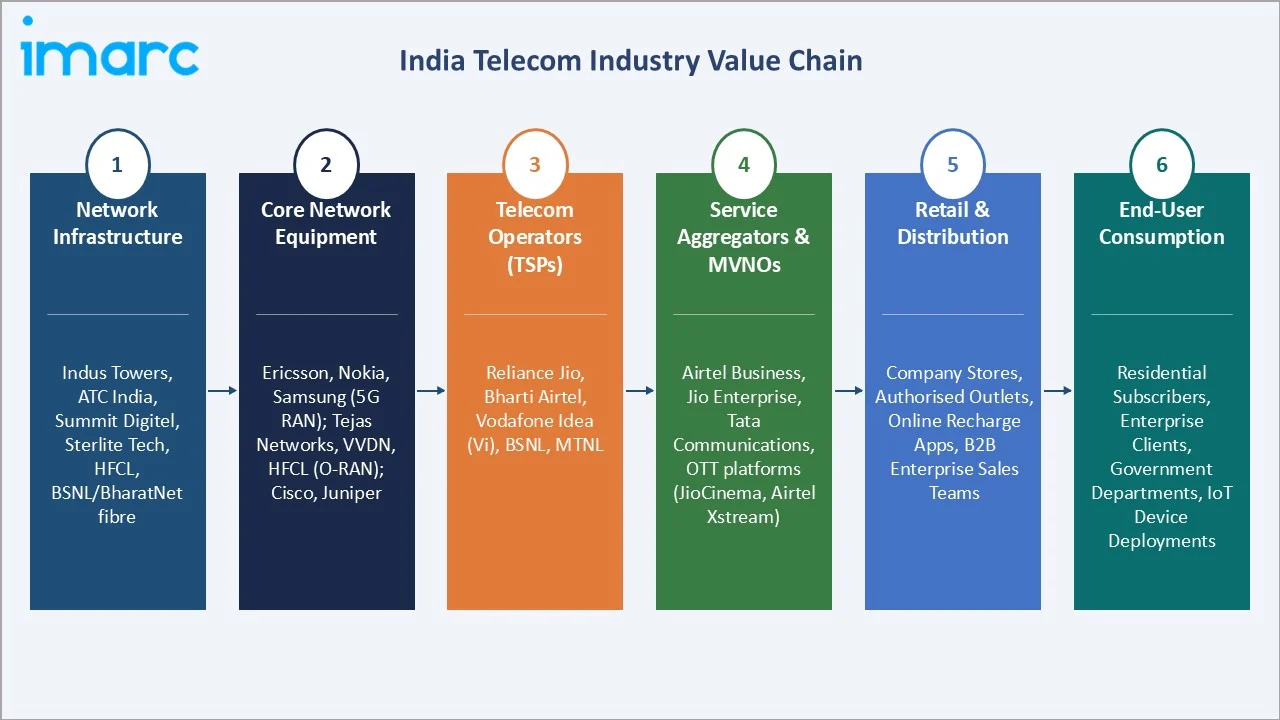

Industry Value Chain Analysis

The India telecom industry value chain spans six integrated stages from physical network infrastructure provisioning through end-consumer service consumption. Each stage presents distinct regulatory requirements, investment dynamics, and technology innovation opportunities relevant to the India telecom market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Network Infrastructure |

Tower companies (Indus Towers, ATC India, Summit Digitel), OFC cable manufacturers (Sterlite Tech, HFCL), DoT spectrum management, BSNL/BharatNet fibre grid |

|

Core Network Equipment |

Ericsson, Nokia, Samsung (5G RAN); ZTE (limited post-ban); Tejas Networks, VVDN, HFCL (domestic O-RAN); Cisco, Juniper (core routing and switching) |

|

Telecom Operators (TSPs) |

Reliance Jio, Bharti Airtel, Vodafone Idea (Vi), BSNL, MTNL – providing mobile, broadband, and enterprise services under DoT unified licences |

|

Service Aggregators & MVNOs |

Airtel Business, Jio Enterprise, Tata Communications, Ultraviolette Networks (IoT MVNO); OTT platforms (Jio Cinema, Airtel Xstream, Netflix, Hotstar) |

|

Retail & Distribution Channels |

Company-owned stores, authorised multi-brand outlets, online recharge apps, B2B enterprise sales teams, government procurement channels (EESL, CPWD) |

|

End-User Consumption |

Residential mobile/broadband subscribers, enterprise clients, government departments, IoT device deployments |

Tower infrastructure operators – Indus Towers, ATC India, and Summit Digitel – hold critical strategic value as the physical foundation of all telecom services. The shift toward active infrastructure sharing (RAN sharing under TRAI guidelines) and O-RAN architecture is reducing network deployment costs by 30-40%, enabling all operators to expand coverage at lower capex.

Technology Landscape in the India Telecom Industry

5G – Standalone (SA) and Non-Standalone (NSA) Architecture

Reliance Jio deployed India's first true 5G Standalone (SA) network, enabling network slicing, ultra-low latency (sub-5ms), and cloud-native core architecture without reliance on 4G LTE anchor nodes. Airtel operates a 5G Non-Standalone (NSA) network leveraging existing 4G core, providing faster rollout with mid-band (3.5 GHz) and millimetre-wave (26 GHz) coverage. SA architecture enables B2B use cases including private network slicing, MEC (Multi-Access Edge Computing), and mission-critical IoT deployments that NSA architecture cannot support.

Fibre Deep and Fixed Wireless Access (FWA)

India's optical fibre cable (OFC) network, driven by BharatNet and operator fibre deployments. Jio's JioFiber and Airtel's Xstream Fiber are deploying GPON (Gigabit Passive Optical Network) and XGS-PON (10-Gigabit) FTTH connections across tier-1 and tier-2 cities, with combined home passed exceeding 50 million by Q1 2025. Fixed Wireless Access (FWA) using 5G is emerging as a fast-deployment alternative to fibre for buildings where laying fibre is cost-prohibitive.

Open RAN and Network Virtualisation

India's DoT and TTDF are co-funding domestic O-RAN ecosystem development, with Tejas Networks, VVDN, and HFCL producing O-RAN compliant RUs (Radio Units) and O-DUs (Distributed Units). BSNL's 4G network, planned to cover 1 lakh+ sites by 2026, will be India's first large-scale domestically manufactured open network, serving as a proof-of-concept for O-RAN deployment at national scale. Network virtualisation (NFV/SDN) is enabling dynamic, software-defined network slicing across Jio's 5G SA core.

AI, ML and Network Automation

India's leading operators are deploying AI-driven Network Operations Centres (NOCs) that autonomously monitor, diagnose, and resolve 70-80% of network incidents without human intervention. Predictive network analytics using ML models trained on real-time KPI data are reducing Mean Time to Repair (MTTR) by 40% and optimising energy consumption at base stations by 15-20%. Personalised AI recommendation engines are improving subscriber ARPU by 8-12% through targeted plan upgrades and content bundle recommendations.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the India telecom market, along with forecasts from 2026 to 2034. The market has been analysed based on Services and Region.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Services |

Data and Messaging Services |

72.0% |

2025 |

|

Region |

North India |

28.0% |

2025 |

By Services

Data and Messaging Services dominate the India telecom market with a 72.0% revenue share in 2025, representing USD 27.21 Billion in absolute value. India's per-subscriber monthly data consumption of 24.7 GB in 2025 is the result of a decade of aggressive data tariff reduction, beginning with Jio's free data launches in 2016-17 that compressed industry data prices from INR 250 per GB to under INR 9 per GB, driven by 5G-enabled higher data speeds, video streaming proliferation, cloud gaming, and enterprise IoT data plans.

To access detailed market analysis, Request Sample

Voice Services hold 17.4% revenue share in 2025, representing USD 6.57 Billion in absolute terms. While absolute minutes of use remain high at 7.5 trillion annually, voice ARPU contribution is declining as operators bundle unlimited voice calls into data plans at marginal additional cost. The transition from standalone voice plans to data-voice bundles is a structural revenue mix shift, with voice ARPU projected to decline from INR 35-40 per month to INR 20-25 by 2030. Voice quality improvements through VoLTE (Voice over LTE) and VoNR (Voice over New Radio on 5G SA) are maintaining subscriber satisfaction during this transition.

OTT and Pay-TV Services account for 10.6% share in 2025. Jio Cinema, which streamed the 2024 ICC Cricket World Cup and IPL to 450+ million concurrent viewers, demonstrated OTT's scale in India. Telecom operators are shifting from pure pipeline providers to integrated digital content platforms, with Jio and Airtel now monetising OTT bundles directly rather than simply providing connectivity for third-party OTT services, retaining higher value from India's digital content boom.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

28.0% |

Delhi NCR enterprise data demand, UP's 240M wireless subscribers, PM Gati Shakti fibre investments, government institutional telecom procurement across 29 central ministries |

|

West & Central India |

26.3% |

Mumbai BFSI enterprise connectivity, Pune IT corridor 5G adoption, Gujarat GIFT City enterprise data hub, Maharashtra and MP Smart City connectivity rollouts |

|

South India |

24.8% |

Bangalore tech-sector enterprise 5G demand, Chennai submarine cable landing hub, Hyderabad HITEC City connectivity, Kerala's K-FON state broadband initiative |

|

East & Northeast India |

20.9% |

BharatNet Phase 3 rural connectivity, North East Special Infrastructure Development Scheme, NESIDS telecom projects, Odisha and West Bengal urban 5G rollouts |

North India commands 28.0% of the India telecom market in 2025. Uttar Pradesh alone contributes 1.6+ million wireless subscribers, the largest state-level subscriber base in India. Delhi NCR's concentration of central government offices, multinational headquarters, and India's largest data centre cluster (Noida-Greater Noida corridor hosting 40+ hyperscale data centres) generates the highest enterprise telecom revenue per capita. BSNL's national headquarters and DoT's spectrum management operations are also concentrated in the region, influencing regulatory policy and procurement.

West and Central India holds 26.3%, with Mumbai serving as India's financial capital and enterprise telecom hub. BFSI sector enterprises in Mumbai's Bandra Kurla Complex generate the highest enterprise data and SD-WAN service revenue per corporate client in India. Gujarat's GIFT City International Financial Services Centre (IFSC), India's first greenfield smart city, mandates redundant multi-operator 5G enterprise connectivity, driving premium B2B telecom adoption. Maharashtra and Madhya Pradesh Smart City projects are deploying integrated IoT-telecom platforms across 18 cities.

South India represents 24.8%, with Bangalore anchoring India's technology-sector enterprise telecom demand. The city hosts 400+ Global Capability Centres (GCCs) of Fortune 500 companies, each requiring enterprise-grade 5G private networks, MPLS connectivity, and cloud interconnect services. Chennai's status as India's primary submarine cable landing hub (with 16 of India's 17 international cable landing stations) gives South India strategic importance in India's international internet bandwidth architecture. Kerala's state-owned K-FON (Kerala Fibre Optical Network) is providing affordable broadband to 20 lakh BPL households.

East and Northeast India accounts for 20.9%, the smallest but fastest-growing regional share at an estimated 14.8% CAGR. BharatNet Phase 3's INR 1.39 Lakh Crore programme is transforming rural connectivity across West Bengal, Odisha, Jharkhand, and the eight northeastern states. The North East Special Infrastructure Development Scheme (NESIDS) has allocated INR 5,000 Crore specifically for telecom infrastructure in the northeast, connecting previously isolated communities and unlocking new subscriber markets that were economically inaccessible to private operators.

Competitive Landscape

|

Company |

Key Brand / Service |

Position |

Core Strength |

|

Reliance Jio Infocomm |

JioFiber, JioAirFiber |

Leader |

Largest subscriber base, True 5G SA, JioCinema OTT, 450M+ MAU |

|

Bharti Airtel Ltd. |

Airtel 5G Plus, Xstream |

Leader |

Premium ARPU focus, enterprise B2B strength, Airtel IQ platform |

|

Vodafone Idea (Vi) |

Vi 5G |

Challenger |

Third largest but financially strained; 5G rollout delayed to 2026 |

|

BSNL |

BSNL 4G/5G |

Challenger |

Domestic 4G/5G equipment mandate, rural coverage, government contracts |

|

Tata Communications |

Tata IZO, IZO Internet |

Challenger |

Enterprise MPLS, cloud interconnect, global Tier-1 IP backbone |

|

Sterlite Technologies |

STL Networks |

Niche |

OFC manufacturing, O-RAN system integration, BharatNet EPC |

|

Railtel Corporation |

RailWire, RailNet |

Niche |

Pan-India railway fibre backbone, rural Wi-Fi (RailWire ISP) |

|

ACT Corp |

ACT Fibernet |

Niche |

South India FTTH leadership, B2C broadband, SMB enterprise connectivity |

|

MTNL |

MTNL Delhi/Mumbai |

Niche |

Limited to Delhi and Mumbai; legacy infrastructure, government PSU |

The India telecom market's competitive landscape is rapidly consolidating into an effective duopoly at the consumer mobile tier. Reliance Jio and Bharti Airtel collectively control 81%+ of the wireless subscriber market and an even higher revenue market in 2025, as both operators have executed selective tariff increases while Vi's market share has gradually eroded. The entry of satellite operators (Starlink, OneWeb) in 2025 introduces a new competitive dimension for rural and enterprise fixed broadband, though mobile voice and data will remain TSP-dominated through 2034.

Key Company Profiles

Reliance Jio Infocomm Ltd.

Reliance Jio is India's largest telecom operator, headquartered in Mumbai, Maharashtra, and a subsidiary of Reliance Industries Ltd. (RIL). As of March 2025, Jio serves 483 million wireless subscribers, representing a 51% wireless market share. Reliance Jio reported an ARPU of ₹206.2 per month in Q4 FY2025, while Jio Platforms generated ₹1.28 lakh crore in operating revenue (₹1.50 lakh crore gross revenue) in FY2024–25, reflecting strong monetization and scale.

- Services Portfolio: Jio offers 5G SA mobile services (True 5G), JioFiber FTTH broadband (serving 10 million homes), JioAirFiber 5G fixed wireless access, JioCinema OTT platform (450M+ MAU), JioSaavn music streaming, Jio Enterprise (private 5G, IoT, cloud), and JioSpace Technology (satellite broadband).

- Recent Developments: In Q1 2025, Jio crossed 100 million 5G subscribers, the fastest 5G ramp-up by any operator globally in its first 30 months of commercial operation. In March 2025, Jio launched JioAirFiber in 5,000 new pincodes, targeting 50 million FWA subscribers by 2027. Jio Financial Services received SEBI approval for its digital lending and insurance distribution platform in February 2025.

- Strategic Focus: Jio's strategy centres on monetising its 5G SA network through enterprise private network contracts, scaling JioFiber to 50+ million homes, and building an integrated digital ecosystem combining telecom, financial services, healthcare, and education under the Jio platforms umbrella.

Bharti Airtel Ltd.

Bharti Airtel, headquartered in New Delhi, is India's second-largest telecom operator with 294 million subscribers and a 31.1% market share as of March 2025. Bharti Airtel reported an ARPU of approximately ₹245 per month in Q4 FY2025, the highest among Indian telecom operators, reflecting its premium positioning strategy. The company generated consolidated revenues of around ₹1.73 lakh crore in FY2024–25, including its Africa operations.

- Services Portfolio: Airtel offers 5G NSA mobile services (Airtel 5G Plus), Airtel Xstream Fiber FTTH broadband, Airtel Black convergent home bundle, Airtel IQ cloud communication platform, Airtel Business (enterprise MPLS, SD-WAN, cloud interconnect), and Airtel Payments Bank.

- Recent Developments: In January 2025, Airtel launched its AI-powered network personalization engine, using ML to predict and prevent network congestion for individual subscribers. In March 2025, Airtel Business is expanding its enterprise portfolio through SD-WAN and cloud connectivity solutions, with a strong presence in the BFSI sector, supporting digital transformation initiatives across banks and financial institutions..

- Strategic Focus: Airtel focuses on premium ARPU growth through 5G-led plan upgrades, enterprise B2B services expansion via Airtel IQ and Business, and Africa market consolidation through Airtel Africa's 17-country operations.

Vodafone Idea Ltd. (Vi)

Vodafone Idea (Vi), the merged entity of Vodafone India and Idea Cellular, is headquartered in Mumbai. Vi serves 127 million subscribers with an 13% market share as of March 2025. The company has faced severe financial strain, with net debt of INR 2.2 Lakh Crore and cumulative losses requiring government AGR relief and equity infusion by the Government of India, which holds a 22.6% stake in Vi as of 2025.

- Services Portfolio: Vi offers 4G mobile services across India (with limited 5G pilots in select cities), Vi Home broadband, Vi Business (enterprise connectivity), and the Vi Movies & TV OTT aggregation platform. Vi's 5G commercial launch has been deferred to 2026 pending resolution of funding constraints.

- Recent Developments: In early 2025, Vi raised INR 24,000 Crore through equity issuance, providing a 12–18-month financial runway. Vi signed an MoU with Nokia in February 2025 for 5G NSA network deployment in 17 priority circles by Q4 2026, conditional on further fund-raising.

- Strategic Focus: Vi's immediate priority is financial stabilisation through equity capital raising and 5G rollout in high-ARPU urban circles, while retaining its existing 127 million subscriber base through competitive plan offerings and network quality improvement.

Market Concentration Analysis

The India telecom market exhibits high concentration at the consumer mobile segment, with Jio and Airtel collectively holding ~81% of wireless subscribers and ~78% of wireless revenue in 2025. Vi's declining market share (18.2% subscribers, ~14% revenue) and BSNL's rural-focused base create an effective duopoly in premium urban telecom markets. TRAI's market concentration monitoring framework has flagged rising HHI (Herfindahl-Hirschman Index) levels, prompting ongoing regulatory review of spectrum sharing and MVNO licensing policies.

In the enterprise segment, market structure is more fragmented, with Tata Communications, Airtel Business, Jio Enterprise, and BSNL Enterprise competing alongside specialised players including VSNL (Tata), Reliance Data Centre Services, and AWS Direct Connect India. The enterprise segment's higher ARPU and lower churn make it strategically critical for all major operators' ARPU improvement roadmaps through 2034.

Consolidation dynamics through 2034 will be shaped by: Vi's ability to execute its 5G rollout and financial recovery; satellite operators' (Starlink, OneWeb) gradual market entry in fixed broadband; and potential MVNO licence grants by DoT enabling new specialised vertical players in IoT, healthcare telecom, and agricultural data connectivity segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Data and Messaging Services are growing at 14.5% CAGR through 2034, the highest-growth revenue category. Enterprise 5G private network services are the fastest-growing B2B sub-segment at an estimated 42% CAGR through 2030, from a USD 250 million base in 2025 to a projected USD 8.5 Billion in 2030. OTT and Pay-TV services bundled with telecom plans are expanding at 13.8% CAGR, driven by India's digital content consumption boom.

Emerging Market Expansion

India's 1.44 billion population remains underpenetrated in fixed broadband, with only 36 million home broadband subscriptions as of early 2025, representing a penetration rate of under 12% of households. This gap represents a structural 50-60 million home broadband subscription opportunity through 2030, addressable through both FTTH (JioFiber, Airtel Xstream) and 5G FWA (JioAirFiber) deployment. Rural data monetisation through affordable 5G plans targeted at BharatNet-connected gram panchayats represents an additional 100+ million subscriber opportunity.

Venture and Strategic Investment Trends

Telecom infrastructure in India attracted USD 8.5 Billion in FDI and strategic investment in FY 2024-25, including Jio Platforms' continuing investor interest and Airtel's strategic partnership with Singtel. TTDF government grants of INR 3,420 Crore are catalysing domestic telecom equipment manufacturing investments by HFCL, VVDN, and Tejas Networks. Satellite broadband venture investments in India reached USD 340 million between 2023 and 2025, including Starlink's INR 13,500 Crore India entry capex commitment and OneWeb India's ground station network investment.

Future Market Outlook (2026-2034)

The India telecom market forecast projects robust expansion from USD 37.79 Billion in 2025 to USD 72.32 Billion by 2034 at a CAGR of 7.48%, with an intermediate milestone of USD 54.20 Billion by 2030. 5G monetisation across consumer and enterprise segments is the primary growth lever in the near term (2026-2028), while 6G research and potential commercial services (2030-2034) will define the long-term technological architecture.

Technological disruptions shaping the market include: 6G research programmes (TRAI and DoT initiated 6G R&D committees in 2024, targeting 2030 commercial readiness); AI-native networks where network elements are intrinsically AI-powered rather than AI-augmented; and quantum-safe encryption for telecom core infrastructure, expected to become a DoT compliance requirement by 2028 as quantum computing threats to classical cryptography materialise.

India's vision of 'Viksit Bharat' (Developed India) by 2047 places digital connectivity as core infrastructure, committing to universal broadband access, 6G leadership, and domestic telecom equipment manufacturing at scale. These policy imperatives, backed by fiscal commitments through BharatNet, TTDF, and PLI schemes, provide structural and durable support for a highly positive India telecom market outlook through 2034 and beyond.

Research Methodology

Primary Research

Primary research comprised structured expert interviews with telecom CXOs, TRAI officials, DoT spectrum management professionals, enterprise telecom procurement heads at leading BFSI and IT companies, and tower infrastructure CEOs. Primary inputs validated market sizing, ARPU trend analysis, 5G adoption projections, and competitive positioning assessments for all profiled companies.

Secondary Research

Secondary research drew upon TRAI quarterly performance indicators and subscriber data, DoT annual reports and spectrum auction records, MoC foreign direct investment statistics for telecom, company annual reports and investor presentations for Jio, Airtel, Vi, BSNL, and Tata Communications, GSMA Intelligence India market data, ITU/3GPP standard publications for 5G and emerging technologies, and industry associations including COAI (Cellular Operators Association of India) and ISPAI (Internet Service Providers Association of India) publications.

Forecasting Models

Market size forecasts were developed through bottom-up aggregation of subscriber ARPU projections across mobile, fixed broadband, and enterprise connectivity revenue streams, cross-validated with top-down macro-economic indicators including India GDP growth, digital economy expansion rates, and telecom capex investment cycle modelling. A base-case CAGR of 7.48% was derived through triangulation with multiple scenario analyses covering 5G monetisation pace, Vi's financial recovery trajectory, and BharatNet-driven rural subscriber additions through 2034.

India Telecom Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered |

|

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Reliance Jio Infocomm, Bharti Airtel Ltd., Vodafone Idea (Vi), BSNL, Tata Communications, Sterlite Technologies, Railtel Corporation, ACT Corp, MTNL, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Telecom Market Report

The India telecom market was valued at USD 37.79 Billion in 2025 and is projected to reach USD 72.32 Billion by 2034, growing at a CAGR of 7.48% during 2026-2034.

The market is forecast to expand at a CAGR of 7.48% from 2026 to 2034, driven by 5G network monetisation, surging data consumption, BharatNet rural connectivity, and enterprise digital transformation services.

Data and Messaging Services lead with 72.0% market share in 2025, growing at 14.5% CAGR through 2034. India's 24.7 GB per user monthly data consumption is among the world's highest, driving persistent revenue growth in this category.

North India leads with 28.0% market share in 2025, driven by UP's 240 million wireless subscribers, Delhi NCR's enterprise telecom demand, and government institutional connectivity procurement concentrated in the region.

East and Northeast India is the fastest-growing region at ~14.8% CAGR, driven by BharatNet Phase 3 rural fibre connectivity, NESIDS telecom infrastructure projects, and unlocking of previously underpenetrated subscriber markets.

Key drivers include nationwide 5G rollout by Jio and Airtel in 750+ cities, BharatNet's INR 1.39 Lakh Crore rural fibre programme, India's 800 million smartphone installed base, surging data consumption at 24.7 GB/user/month, and enterprise 5G private network adoption.

Key players include Reliance Jio (482M subscribers), Bharti Airtel (387M subscribers), Vodafone Idea/Vi (213M), BSNL, Tata Communications, Sterlite Technologies, ACT Corp, Railtel Corporation, and MTNL.

India crossed 100 million 5G subscribers in March 2025, making it one of the top-5 countries globally by 5G adoption speed. Jio and Airtel together have deployed 5G in 750+ cities across India.

The India telecom market is forecast to reach USD 54.20 Billion by 2030, supported by 5G enterprise service monetisation, OTT bundling ARPU growth, and BharatNet-enabled rural subscriber additions across all four regions.

BharatNet Phase 3's INR 1.39 Lakh Crore programme connects 6.4 lakh villages with optical fibre broadband by 2026, unlocking 800+ million rural users as addressable internet subscribers and driving new broadband revenue streams for all licensed operators.

TRAI regulates tariffs, quality of service standards, spectrum utilisation, and fair competition across India's telecom industry. TRAI's interconnection regulations, MVNO framework, and broadband speed benchmarks directly shape competitive dynamics and investment decisions in the market.

Key opportunities include enterprise 5G private network services (USD 8.5B market by 2030), satellite broadband (Starlink, OneWeb), OTT and digital content bundling, domestic telecom equipment manufacturing under PLI, and telecom-fintech convergence through Jio Financial Services and Airtel Payments Bank.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade