India Teleradiology Market Size, Share, Trends and Forecast by Component, Imaging Technique, End User, and Region, 2026-2034

India Teleradiology Market Summary:

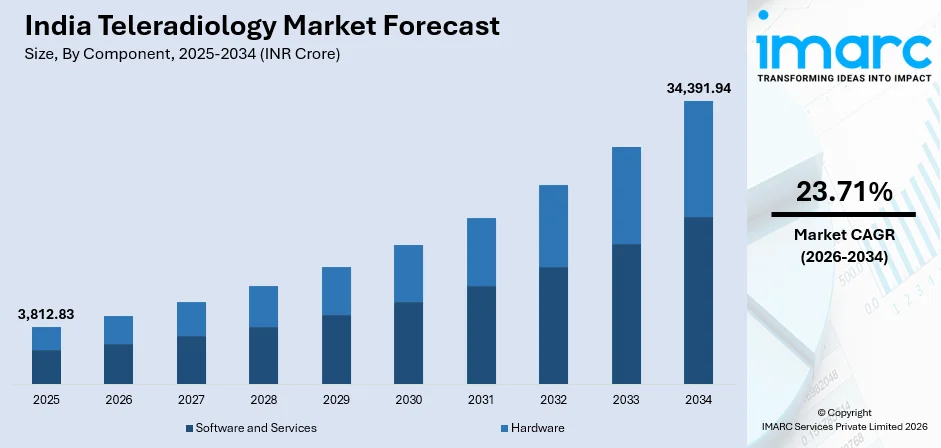

The India teleradiology market size was valued at INR 3,812.83 Crore in 2025 and is projected to reach INR 34,391.94 Crore by 2034, growing at a compound annual growth rate of 23.71% from 2026-2034.

The India teleradiology market is gaining strong traction, as hospitals and diagnostic centers increasingly rely on remote imaging specialists to address critical radiologist shortages across the country. The rising prevalence of chronic diseases, expanding digital health infrastructure, and growing patient awareness about early diagnosis are accelerating service adoption. Advances in artificial intelligence (AI)-assisted reporting tools, cloud-based platforms, and broadband connectivity are enabling faster and more accurate image transmission, collectively reinforcing the market share.

Key Takeaways and Insights:

- By Component: Software and services dominate the market with a share of 74.0% in 2025, reflecting strong demand for AI-powered platforms, cloud-based picture archiving and communication systems (PACS), and integrated digital workflow solutions across hospitals and diagnostic centers.

- By Imaging Technique: X-rays lead the market with a share of 36.0% in 2025, owing to their cost-effectiveness, widespread availability, and versatile application across primary diagnostics including orthopedics, chest imaging, and cardiovascular assessment.

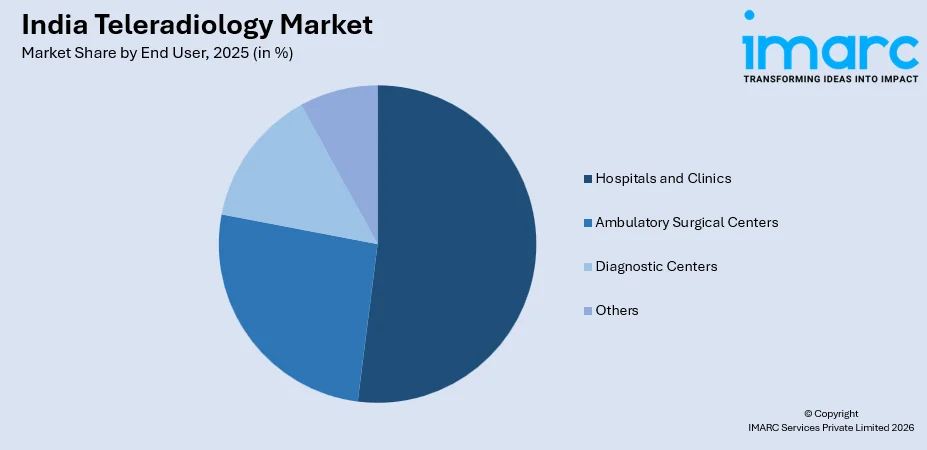

- By End User: Hospitals and clinics comprise the largest market share at 52.0% in 2025, driven by high imaging volumes, round-the-clock diagnostic demands, and the need to overcome on-site radiologist shortages through remote reporting solutions.

- By Region: South India represents the largest region with 35.0% share in 2025, benefiting from a well-developed private healthcare ecosystem, high technology adoption, and a strong concentration of multi-specialty hospitals across key urban centers.

- Key Players: Key players in the India teleradiology market are driving growth by investing in AI-powered imaging platforms, expanding digital radiologist networks, and forging strategic partnerships with hospitals and diagnostic centers. Their efforts to enhance reporting accuracy, improve turnaround times, and extend services to Tier-2 and Tier-3 cities are strengthening service delivery and reinforcing the India teleradiology market share. Key players operating in the market include Agfa-Gevaert Group, Everlight Radiology, GE Healthcare, Koninklijke Philips NV, Apollo Telehealth, 5C Network (INDIA) Pvt Ltd., RxDx Healthcare, Teleradiology Solutions, Technidoc, and Oshin Infotech Services Private Limited.

To get more information on this market Request Sample

The India teleradiology market is rapidly evolving, as healthcare providers and policymakers recognize the critical role of remote diagnostic services in bridging geographical disparities in medical care. Teleradiology enables radiologists to electronically interpret medical images, ensuring timely diagnoses across hospitals, clinics, and diagnostic centers regardless of location. The persistent shortage of radiologists remains a defining catalyst for market growth. According to NITI Aayog (2023), India had one radiologist per 100,000 population, far below the global benchmark, creating an acute gap in diagnostic coverage. This disparity has accelerated adoption of teleradiology platforms connecting facilities with qualified remote specialists, improving diagnostic access in underserved regions. The market is further supported by rising health awareness, an expanding burden of chronic conditions, and favorable government policies advancing digital health.

India Teleradiology Market Trends:

Integration of AI in Radiology Workflows

AI is rapidly transforming how radiological images are processed, interpreted, and reported in the India teleradiology sector. AI-powered tools assist radiologists in detecting abnormalities across X-rays, computed tomography (CT) scans, and magnetic resonance imaging (MRI) scans with enhanced speed and accuracy, while significantly reducing manual reporting workloads. In August 2025, Samsung India, in collaboration with NeuroLogica, launched a next-generation mobile CT portfolio in India featuring AI-assisted imaging and seamless PACS and EMR integration, designed to expand advanced diagnostic capabilities across hospitals and underserved regions nationwide.

Growing Adoption of Radiology Reporting Outsourcing

An increasing number of hospitals and diagnostic centers across India are outsourcing their radiology reporting to specialist teleradiology providers, driven by a critical shortage of in-house radiologists and the need to manage operational costs. This trend is accelerating as institutions prioritize subspecialty access and faster turnaround times. In September 2024, Krsnaa Diagnostics collaborated with Medikabazaar and United Imaging to establish more than 30 state-of-the-art diagnostic centers in Tier-2 and Tier-3 cities across India, with a total investment exceeding INR 300 Crore to expand outsourced diagnostic and teleradiology services.

Expansion of Cloud-Based PACS Platforms Across Healthcare Networks

The adoption of cloud-based PACS is emerging as a defining trend in India's teleradiology landscape. These platforms enable healthcare facilities to store, retrieve, and share radiological images remotely, facilitating real-time access for radiologists regardless of geographic location, improving workflow efficiency, and broadening institutional uptake. Cloud deployment also reduces the need for costly on-site storage infrastructure and simplifies system maintenance and scalability. Additionally, it supports seamless integration with hospital information systems, strengthening coordinated and data-driven diagnostic services.

Market Outlook 2026-2034:

The India teleradiology market is positioned for sustained expansion over the forecast period, driven by the convergence of digital health infrastructure growth, increasing chronic disease burden, and accelerating technological innovation. Healthcare facilities across urban, semi-urban, and rural India are increasingly adopting remote imaging solutions to address radiologist shortages and improve diagnostic accessibility. The market generated a revenue of INR 3,812.83 Crore in 2025 and is projected to reach a revenue of INR 34,391.94 Crore by 2034, growing at a compound annual growth rate of 23.71% from 2026-2034. The growing emphasis on preventive healthcare, early diagnosis, and value-based care delivery will further elevate adoption of cloud-based and AI-enhanced teleradiology solutions throughout the forecast period.

India Teleradiology Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Software and Services |

74.0% |

|

Imaging Technique |

X-rays |

36.0% |

|

End User |

Hospitals and Clinics |

52.0% |

|

Region |

South India |

35.0% |

Component Insights:

- Software and Services

- Hardware

Software and services dominate with a market share of 74.0% of the total India teleradiology market in 2025.

Software and services represent the backbone of India's teleradiology ecosystem, including workflow management tools, radiological information systems, AI-powered diagnostic apps, and cloud-based PACS solutions. The need for integrated software solutions that facilitate smooth picture transfer, remote reporting, and real-time collaboration is growing, as hospitals and diagnostic centers quicken their digital transformation. By removing the requirement for radiologists and imaging facilities to be physically close to one another, these technologies allow for round-the-clock diagnostic coverage.

The software layer is complemented by services like technical support, subspecialty consulting, and radiology reporting outsourcing, which provide operational continuity for medical facilities without internal radiology specialists. These services are especially helpful for smaller hospitals, community health clinics, and establishments in Tier-2 and Tier-3 cities where there is still a shortage of specialized radiology personnel. Without having to retain full-time expert teams, the services segment gives facilities access to qualified interpreters for complicated imaging modalities, such as pediatric radiology, musculoskeletal imaging, and neuroradiology.

Imaging Technique Insights:

- X-rays

- Computed Tomography (CT)

- Ultrasound

- Magnetic Resonance Imaging (MRI)

- Nuclear Imaging

- Others

X-rays lead with a share of 36.0% of the total India teleradiology market in 2025.

X-rays remain the most widely utilized imaging technique in the India teleradiology sector, because of their affordability, simplicity of use, and wide diagnostic usefulness in a variety of clinical situations. They are essential for both primary care and specialty facilities, as they are the main diagnostic tool for respiratory disorders, orthopedic injuries, dental anomalies, and cardiovascular evaluations. Rapid remote interpretation is made possible by the improved image quality and transmission efficiency of digitized X-ray systems.

This technique's dominance within the India teleradiology framework has been further strengthened by the extensive use of digital radiography systems and filmless X-ray technologies. The number of studies requiring remote interpretation is steadily increasing as imaging centers in rural and semi-urban locations make investments in digital X-ray technology. X-rays continue to be the recommended option for regular diagnostic screenings due to their ease of use, shorter scan times, and reduced radiation exposure when compared to CT scans.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Diagnostic Centers

- Others

Hospitals and clinics prevail the market with a share of 52.0% of the total India teleradiology market in 2025.

Hospitals and clinics are the dominant consumers of teleradiology services in India, driven by the high volume and variety of imaging studies generated across emergency departments, intensive care units, oncology wards, and general medical floors. These institutions require continuous round-the-clock access to radiology expertise to support timely clinical decision-making and patient management. The government's target to raise healthcare expenditure has spurred significant infrastructure investment, leading to a proliferation of hospital networks, particularly in Tier-2 and Tier-3 cities, which increasingly depend on outsourced teleradiology services to address in-house radiologist shortages and maintain high-quality diagnostic operations.

Large hospital networks and multi-specialty clinics are increasingly integrating teleradiology platforms into their existing hospital information systems and PACS infrastructure, creating end-to-end digital diagnostic workflows. These arrangements allow hospitals to access subspecialty reports for complex imaging studies, including neuroradiology, cardiac imaging, and oncological assessments, without maintaining full-time on-site specialists. Growing public-private partnerships (PPPs) have further enabled government-run hospitals to benefit from private sector teleradiology expertise and technological capabilities.

Regional Insights:

- North India

- West and Central India

- South India

- East India

South India exhibits a clear dominance with a 35.0% share of the total India teleradiology market in 2025.

South India's leadership in the India teleradiology market is underpinned by its advanced healthcare ecosystem, high density of private hospitals, and progressive technology adoption across key urban centers. States, including Tamil Nadu, Karnataka, Telangana, and Kerala, are home to large multi-specialty hospital networks and health-tech companies that are early adopters of cloud-based diagnostic platforms and AI-enabled imaging tools. The region's robust IT infrastructure facilitates the rapid deployment of teleradiology solutions at scale.

South India's well-developed medical education ecosystem, encompassing prominent institutions and radiology training programs, has fostered a strong pool of qualified radiologists who actively participate in teleradiology networks. The region's private healthcare sector leads investment in advanced imaging equipment, AI-driven diagnostic tools, and secure data transmission infrastructure. Higher patient awareness of preventive healthcare and early diagnosis in urban South Indian centers drives increased imaging volumes and greater demand for remote reporting services.

Market Dynamics:

Growth Drivers:

Why is the India Teleradiology Market Growing?

Acute Shortage of Qualified Radiologists Driving Remote Reporting Adoption

India faces a severe and well-documented shortage of qualified radiologists, which remains the most compelling structural driver of teleradiology market growth. The uneven geographic distribution of radiological expertise leaves hospitals, clinics, and diagnostic centers in Tier-2, Tier-3, and rural areas critically underserved. This shortage forces healthcare facilities to seek remote reporting solutions as a practical and cost-effective alternative to recruiting and retaining on-site specialists. Teleradiology directly addresses this gap by enabling a limited pool of qualified radiologists to serve multiple facilities simultaneously, regardless of geographic location. The growing trend of radiology reporting outsourcing, which is driven by hospital chains and diagnostic centers seeking to improve turnaround times and reduce staffing costs, has created a sustainable and expanding revenue base for teleradiology service providers. As India's imaging volumes continue to grow on account of rising chronic disease prevalence and expanding diagnostic infrastructure, this structural demand catalyst is expected to remain a dominant force throughout the forecast period. India recorded a total of 14,96,972 cancer cases in 2023 and 15,33,055 in 2024.

Government Digital Health Initiatives Supporting Teleradiology Expansion

The Indian government's commitment to advancing digital healthcare through policy support, financial investment, and regulatory frameworks has created a strongly enabling environment for teleradiology market growth. The National Digital Health Mission (NDHM), known as the Ayushman Bharat Digital Mission (ABDM), facilitates the creation of health data registries, unified digital health identities, and telemedicine frameworks that directly support teleradiology service delivery. Government investments in broadband connectivity are progressively enabling teleradiology platforms to reach previously inaccessible regions. Public hospitals under state and central government management are increasingly adopting PPPs with teleradiology providers to extend quality diagnostic services to underserved populations. These policy initiatives collectively reduce barriers to adoption, foster confidence among healthcare providers, and create sustained demand for teleradiology platforms across both urban and rural healthcare settings.

Growing Adoption of Advanced Imaging Technologies Across Healthcare Facilities

The increasing installation of advanced diagnostic imaging equipment, such as CT scanners, MRI systems, and digital X-ray machines, across hospitals and diagnostic laboratories is driving the need for specialized radiology interpretation services. Many smaller hospitals and standalone diagnostic centers lack the expertise required to interpret complex imaging studies, particularly in specialized areas, such as neuroradiology and cardiac imaging. Teleradiology services provide access to subspecialty expertise without requiring facilities to hire multiple full-time specialists. This capability improves diagnostic accuracy and enables healthcare providers to deliver higher-quality care. As India continues to invest in expanding its diagnostic infrastructure, the demand for remote radiology interpretation services is expected to rise significantly. This trend is further reinforced by the rapid expansion of private diagnostic chains and multi-specialty hospitals across the country.

Market Restraints:

What Challenges the India Teleradiology Market is Facing?

Data Privacy and Cybersecurity Vulnerabilities in Remote Imaging Networks

The electronic transmission of sensitive patient imaging data across digital networks creates significant data privacy and cybersecurity risks for teleradiology providers in India. Healthcare organizations handling radiological images must comply with stringent data protection standards. However, inconsistent adoption of encryption protocols, secure transmission channels, and access controls creates vulnerabilities. Data breaches can expose confidential patient information and expose providers to legal liability, eroding institutional trust and creating hesitation among hospitals considering cloud-based teleradiology platforms.

Absence of Standardized Reimbursement and Regulatory Frameworks

The lack of a unified national reimbursement framework for teleradiology services in India creates significant uncertainty for both service providers and healthcare facilities. Unlike conventional in-person radiology, remote reporting lacks consistent compensation guidelines across states and insurance systems, making it difficult for teleradiology providers to establish sustainable pricing models and discouraging wider institutional adoption. The regulatory environment, while improving with the Telemedicine Practice Guidelines, still lacks comprehensive standards for data ownership, liability allocation, and quality assurance across teleradiology networks, limiting structured market growth and creating operational ambiguity.

Integration Challenges with Legacy Hospital IT Systems

Many hospitals and diagnostic centers in India continue to operate legacy hospital information systems, radiology information systems, and imaging storage platforms that are not fully compatible with modern teleradiology solutions. Integrating these older systems with new cloud-based or remote reporting platforms can require significant technical upgrades, additional investment, and specialized IT expertise. The complexity of system interoperability can delay implementation timelines and increase operational costs for healthcare providers. These integration challenges create hesitation among smaller healthcare facilities that lack the technical capacity to manage large-scale digital system transitions.

Competitive Landscape:

The India teleradiology market is characterized by a dynamic mix of established healthcare technology companies, specialized domestic teleradiology providers, and global medical imaging leaders competing for share in this rapidly expanding market. Companies are investing heavily in AI-powered imaging platforms, cloud-based PACS infrastructure, and expanded radiologist networks to enhance service quality and differentiate their offerings. Competitive intensity is driven by the growing outsourcing trend among hospitals and diagnostic centers seeking subspecialty radiology coverage at scale. Key players are pursuing strategic partnerships, technology integrations, and geographic expansion to reach underserved Tier-2 and Tier-3 markets. The market features both national providers delivering high-volume general radiology reporting and niche players focusing on subspecialty reads, emergency radiology, and cross-border outsourcing. Continuous innovation in AI-assisted diagnostics, turnaround time optimization, and secure data management is emerging as a critical differentiator.

Key players operating in the market include:

- Agfa-Gevaert Group

- Everlight Radiology

- GE Healthcare

- Koninklijke Philips NV

- Apollo Telehealth

- 5C Network (INDIA) Pvt Ltd.

- RxDx Healthcare

- Teleradiology Solutions

- Technidoc

- Oshin Infotech Services Private Limited

India Teleradiology Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Crore |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software and Services, Hardware |

| Imaging Techniques Covered | X-rays, Computed Tomography (CT), Ultrasound, Magnetic Resonance Imaging (MRI), Nuclear Imaging, Others |

| End Users Covered | Hospitals and Clinics, Ambulatory Surgical Centers, Diagnostic Centers, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Agfa-Gevaert Group, Everlight Radiology, GE Healthcare, Koninklijke Philips NV, Apollo Telehealth, 5C Network (INDIA) Pvt Ltd., RxDx Healthcare, Teleradiology Solutions, Technidoc, Oshin Infotech Services Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Teleradiology Market Report

The India teleradiology market size was valued at INR 3,812.83 Crore in 2025.

The India teleradiology market is expected to grow at a compound annual growth rate of 23.71% from 2026-2034 to reach INR 34,391.94 Crore by 2034.

Software and services dominated the market with a share of 74.0%, driven by widespread adoption of AI-powered platforms, cloud-based PACS systems, and digital workflow solutions across hospitals and diagnostic centers throughout the country.

Key factors driving the India teleradiology market include the acute shortage of qualified radiologists, rising chronic disease burden, expanding government digital health initiatives, growing adoption of AI-assisted imaging technologies, and improving broadband and telecom infrastructure enabling cost-effective remote diagnostic services.

Major challenges include data privacy and cybersecurity vulnerabilities in remote imaging networks, absence of standardized reimbursement and regulatory frameworks, high infrastructure costs, and persistent digital access gaps in rural and semi-urban areas limiting widespread service adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade