India Tomato Ketchup Market Size, Share, Trends and Forecast by Type, Packaging, Distribution Channel, Application, and Region, 2026-2034

India Tomato Ketchup Market Summary:

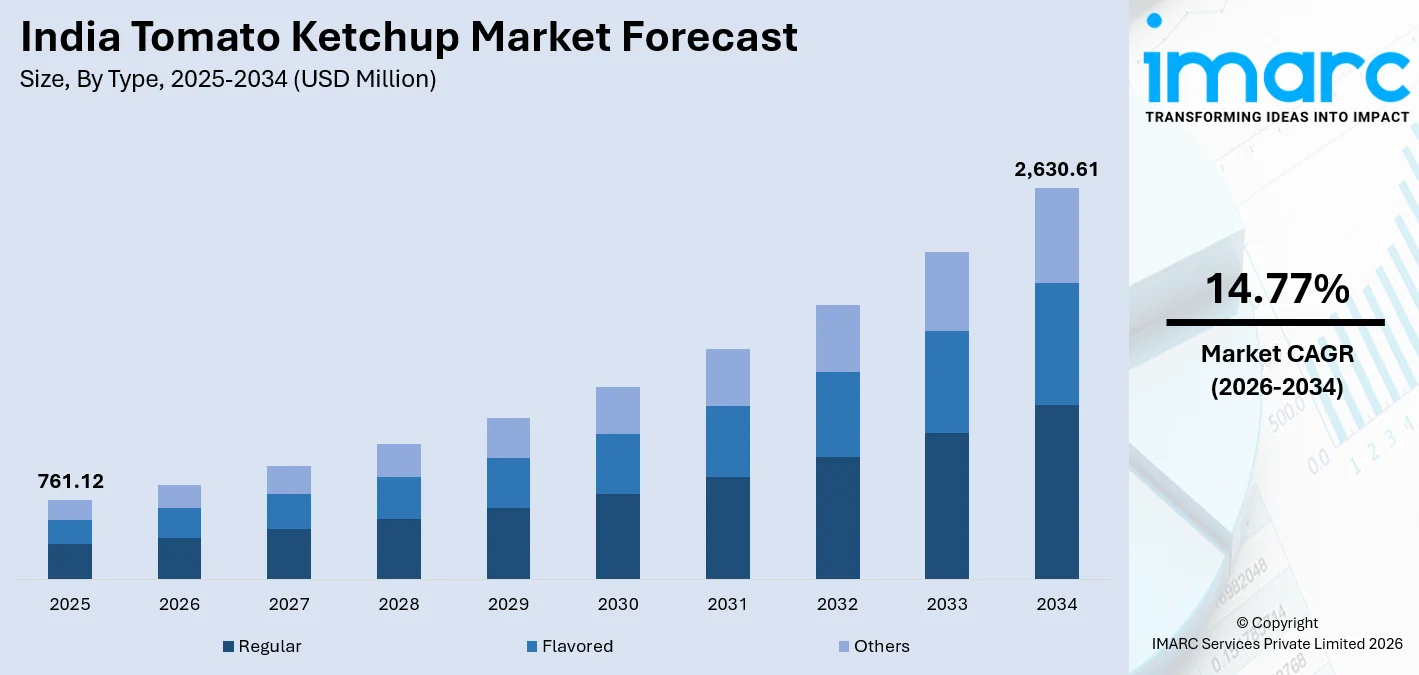

The India tomato ketchup market size was valued at USD 761.12 Million in 2025 and is projected to reach USD 2,630.61 Million by 2034, growing at a compound annual growth rate of 14.77% from 2026-2034.

The India tomato ketchup market is witnessing a steady growth due to the increasing urbanization, the rise of fast food chains and quick service restaurants, and the changing food habits of the increasing middle-class population. The rising purchasing power and the growing demand for convenience foods are increasing the consumption of tomato ketchups in households. At the same time, the industry is leveraging innovation, health, and e-commerce platforms to increase market share in the India tomato ketchup market.

Key Takeaways and Insights:

- By Type: Regular holds the largest market share of 68% in 2025, driven by widespread consumer familiarity, versatility across meal occasions, and its positioning as an affordable, everyday condiment in Indian households and foodservice establishments.

- By Packaging: Bottle dominates the market with a share of 60% in 2025, preferred by consumers for its convenience, reusability, and superior shelf presentation in modern retail formats across India.

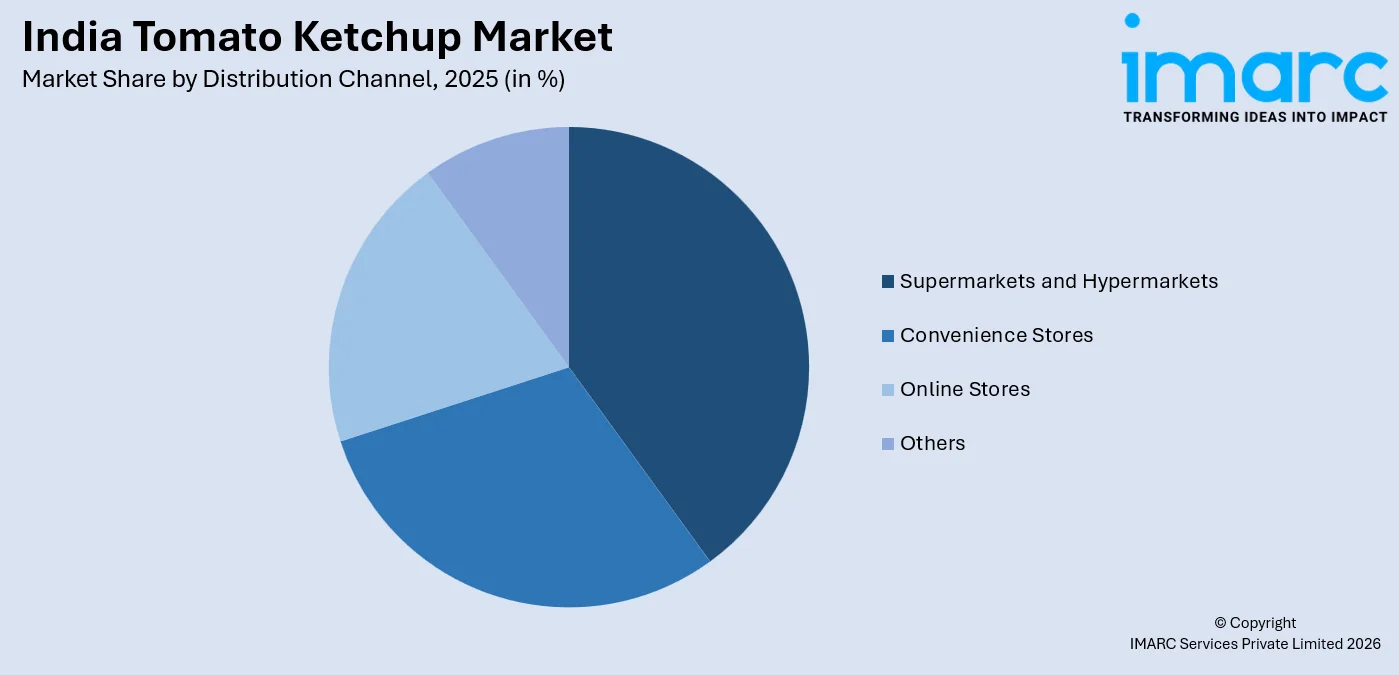

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 38% in 2025, reflecting the strong influence of organized retail in shaping consumer purchase behavior for packaged condiments in India.

- By Application: Household leads the market with a share of 77% in 2025, underscoring tomato ketchup's deep entrenchment as a daily condiment for home-cooked meals, snacks, and children's food preferences across Indian families.

- Key Players: The India tomato ketchup market is highly competitive, featuring a dynamic mix of multinational giants and established domestic FMCG players. Market participants compete intensely across flavor range diversification, packaging innovation, and distribution depth, continuously refining strategies to strengthen consumer loyalty and expand their footprint across urban and semi-urban retail channels.

To get more information on this market Request Sample

The India tomato ketchup market is evolving rapidly as consumer tastes diversify and the packaged food ecosystem matures. Urbanization has fundamentally altered eating habits, with a growing population gravitating toward convenient, ready-to-use condiments. Branded ketchup has successfully transitioned from a Western novelty to a household staple, particularly among younger demographics in metro and Tier I cities. In March 2025, Adani Wilmar announced the acquisition of GD Foods Manufacturing, owner of the well-known “Tops” sauces and ketchup brand, as part of its strategy to broaden its value-added foods portfolio and strengthen its position in India’s packaged foods landscape. Expanding organized retail networks and deepening e-commerce penetration are reshaping distribution dynamics, enabling both established and emerging brands to reach consumers beyond traditional retail footprints. Simultaneously, rising disposable incomes and shifting dietary preferences are fueling demand for premium, flavored, and health-oriented ketchup variants across diverse consumer segments.

India Tomato Ketchup Market Trends:

Growing Demand for Health-Oriented and Organic Ketchup Variants

A discernible shift toward health-conscious consumption is reshaping India's tomato ketchup market growth. Rising concerns over obesity, sugar intake, and preservative use are prompting manufacturers to introduce low-sugar, organic, and no-onion-no-garlic variants. In March 2024, Nestlé reformulated its Maggi tomato ketchup recipe in India to reduce sugar content by 22%, responding to growing consumer demand for healthier condiments with improved nutritional profiles. This initiative reflects the company’s focus on aligning product formulations with evolving health-conscious consumption trends in the country. Health-aware consumers increasingly seek condiments with reduced salt, sugar, and artificial additives, directly influencing reformulation strategies across the sector and compelling brands to pivot toward functional, cleaner-label product differentiation to retain relevance among evolving consumer preferences.

Flavor Localization and Portfolio Diversification

Indian manufacturers are integrating regional spice profiles and cultural flavor cues into ketchup formulations to compete with deeply embedded traditional condiments such as chutney. Spicy, chilli-infused, and chatakdaar variants have gained significant traction, particularly among younger urban consumers. According to reports, Cremica Food Industries launched a new range of sauces alongside its tomato ketchup, including globally and locally inspired flavors such as chipotle, barbeque, Thai sweet chili, and spicy variants, aimed at catering to evolving consumer demand for bold and distinctive taste profiles. This has created fertile ground for brands to launch innovative, India-specific variants that marry tomato's tanginess with local spice preferences, strengthening consumer engagement and broadening market appeal across diverse demographic and geographic segments.

E-Commerce Expansion Accelerating Digital Distribution

Online retail is emerging as a pivotal distribution channel for tomato ketchup in India, driven by surging smartphone penetration and the rapid growth of quick-commerce platforms. Artisanal and premium ketchup brands are leveraging direct-to-consumer platforms to reach urban consumers, while established players are investing heavily in digital shelf visibility and hyperlocal delivery partnerships. In December 2025, Reliance Consumer Products Limited relaunched its legacy food brand SIL, introducing a new portfolio that includes tomato ketchup, sauces, jams, and spreads as part of its comprehensive push into India’s packaged foods segment. The relaunch marked the company’s strategic expansion into everyday food categories and strengthened its presence across modern retail and online distribution channels.

Market Outlook 2026-2034:

The growth story will be driven by the proliferation of the QSR segment, the expansion of organized retail, and the penetration of e-commerce in the urban and semi-urban geography. The increasing awareness of health and wellness will drive the premiumization of the segment, with organic, low sugar, and functional variants taking a larger share of the consumer’s attention. Regional flavor innovation will also drive the segment, with flavors aligned to the regional palate preferences. Consolidation will also drive the segment, with expansion into Tier II and III markets. The market generated a revenue of USD 761.12 Million in 2025 and is projected to reach a revenue of USD 2,630.61 Million by 2034, growing at a compound annual growth rate of 14.77% from 2026-2034.

India Tomato Ketchup Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Regular |

68% |

|

Packaging |

Bottle |

60% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

38% |

|

Application |

Household |

77% |

Type Insights:

- Flavored

- Regular

- Others

The regular dominates with a market share of 68% of the total India tomato ketchup market in 2025.

Conventional tomato ketchup currently leads the India tomato ketchup market due to its familiarity and usage in various meal settings, besides being perceived as an affordable condiment in Indian households and establishments. Its sweet and tangy taste combination suits a variety of foods, ranging from burgers and fries to home-cooked meals. Its consistent taste, longer shelf life, and easy storage have further contributed to its popularity, making it the preferred choice of consumers in both urban and semi-urban India.

The dominance of regular ketchup is further reinforced by its deep-rooted presence in the emerging fast food culture in India and the growing quick service restaurant market. With the rising frequency of eating out among the younger generation, regular ketchup continues to be a staple condiment in the foodservice sector, institutional, and cloud kitchens. The product’s presence in a variety of pack sizes and price points ensures its strong penetration in the modern trade and general trade market.

Packaging Insights:

- Pouch

- Bottle

- Others

The bottle leads with a share of 60% of the total India tomato ketchup market in 2025.

Bottle packaging leads the India tomato ketchup market, driven by consumer preference for convenient dispensing packaging and the perception that bottles are associated with better product quality and freshness. Squeezable PET and glass bottles provide portion control, convenience, and improved retail shelf impact, which appeals to urban consumers. The format is also driven by its presence in the modern trade environment, where retail shelf impact and visibility are important factors in influencing consumer purchasing decisions at the point of sale.

The consistent preference for bottle packaging is further reinforced by its compatibility with various SKU sizes, ranging from single-serve to family packs, thus allowing manufacturers to meet the varied needs of households. The premium and flavored variants of ketchup are mainly packaged in bottles, thus aligning with the premiumization trend that is picking up pace among health- and quality-conscious consumers in urban India. Innovations in the squeezable, resealable, and ergonomic bottle designs are continuously improving convenience, thus further solidifying the leadership position of bottle packaging in the organized retail market of India.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

The supermarkets and hypermarkets dominate with a market share of 38% of the total India tomato ketchup market in 2025.

Supermarkets and hypermarkets are the most prominent distribution channel for tomato ketchup in India, as they are able to reap the benefits of growing penetration in major cities and Tier I cities, as well as the rising preference for organized shopping environments. The distribution channel provides consumers with a wide range of brands, proper shelving, and visibility that help in increasing product trials among new consumer groups. The presence of various sizes of SKUs and competitive pricing in organized retail stores helps consumers make informed purchasing decisions.

The impact of supermarkets and hypermarkets is not limited to metro cities, and modern trade formats are gradually increasing their presence in Tier II and emerging urban centers. Organized in-store promotions, loyalty programs, and bundled condiment promotions are increasingly contributing to impulse purchases in these formats. Companies are investing in shelf fixtures, point-of-sale promotions, and in-store sampling programs to maximize brand exposure. As the organized retail infrastructure continues to evolve in the rapidly urbanizing Indian landscape, supermarkets and hypermarkets are likely to maintain their leading share in the ketchup market.

Application Insights:

- Household

- Commercial

- Others

The household leads with a share of 77% of the total India tomato ketchup market in 2025.

The household segment is the leading segment in the tomato ketchup market in India, and this is because of the widespread usage of tomato ketchup in the country. Tomato ketchup is used in a variety of meals, ranging from applying it to rotis and parathas to eating it with fried foods, sandwiches, pasta, and kids' meals. The increasing number of home-cooked meals, along with the growing awareness of brands among the middle-class population, has made ketchup a staple item in every Indian household.

Household consumption is also fueled by the rising demand for convenient and ready-to-use condiments from busy working families and nuclear families. The trend of making pouch and bottle packaging options available in smaller packs has reduced the barrier to entry for new consumers, making it easier for them to try the category. At the same time, the impact of social media food content on cooking with ketchup as an ingredient in cooking, apart from being a condiment, is fueling new household consumption.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India represents the largest regional market for tomato ketchup, underpinned by high urban density, strong fast food consumption culture in cities such as Delhi, Chandigarh, and Lucknow, and well-established organized retail infrastructure. The region benefits from deep brand penetration across both modern trade and traditional general trade channels, with significant household and commercial foodservice demand driving consistent, high-volume ketchup consumption throughout the year.

West and Central India constitutes a significant regional market, driven by Mumbai's cosmopolitan food culture, rapid retail modernization across Maharashtra and Gujarat, and growing urban-rural connectivity. The region's relatively affluent consumer base demonstrates strong openness to premium and flavored ketchup variants. Increasing FMCG penetration into semi-urban Maharashtra and Madhya Pradesh, supported by expanding modern trade infrastructure and direct-to-retail distribution strategies, is steadily broadening the regional consumer base.

South India represents a rapidly growing regional market, supported by accelerating QSR proliferation in Bengaluru, Chennai, Hyderabad, and Kochi, alongside expanding modern retail formats. Consumer preference for spicy and tangy condiment profiles in this region aligns favorably with chilli-tomato and flavored ketchup variants, offering meaningful product differentiation opportunities. Improving cold chain logistics and strengthening distributor networks are further enhancing ketchup accessibility across both metro cities and smaller southern urban centers.

East and Northeast India is an emerging regional market with considerable untapped growth potential, driven by increasing urbanization in cities such as Kolkata, Patna, and Guwahati, and rising packaged food adoption among aspirational middle-class consumers. While traditional trade channels remain dominant, gradual expansion of modern retail and e-commerce is opening new distribution avenues. Affordable pouch-format SKUs and regionally adapted flavoring strategies are helping manufacturers drive trial and penetration across price-conscious semi-urban consumers.

Market Dynamics:

Growth Drivers:

Why is the India Tomato Ketchup Market Growing?

Rapid Expansion of the Fast Food and QSR Sector

India's quick-service restaurant industry is one of the most powerful demand catalysts for the tomato ketchup market. The proliferation of domestic and international fast food chains across Tier I and II cities has dramatically elevated bulk ketchup procurement from the foodservice channel. In March 2025, Jubilant FoodWorks, operator of Domino's Pizza India, announced plans to expand Domino’s network to 3,000 stores across India, with a strong focus on entering smaller Tier II and Tier III cities. This aggressive expansion strategy reflects the rapid growth of organized quick-service restaurants and their increasing demand for standardized condiments such as tomato ketchup to support large-scale foodservice operations. The expanding cloud kitchen ecosystem adds another layer of institutional demand, creating consistent, high-volume offtake for ketchup manufacturers. Food service establishments are increasingly standardizing tomato ketchup as a default condiment, sustaining strong commercial segment growth throughout the forecast period.

Rising Urbanization and Growing Middle-Class Expenditure on Packaged Foods

India's urban population continues to expand rapidly, driving a fundamental shift in dietary patterns toward packaged and convenience foods. Rising disposable incomes among urban and semi-urban households have elevated consumer spending on branded FMCG products, including flavored and premium ketchup variants. According to a Deloitte‑FICCI report, India’s urban consumers now allocate nearly 50 % of their food budget to packaged and prepared foods, dining out, and deliveries, underscoring how food preferences are shifting toward convenience‑oriented consumption in city markets. The middle class's growing familiarity with global food formats such as burgers, sandwiches, wraps, and pasta is embedding tomato ketchup into mainstream Indian food culture, driving consistent household repeat purchases and expanding the market's overall consumer base across diverse demographic groups.

Expansion of Organized Retail and Growing Modern Trade Penetration

The steady expansion of organized retail formats, including hypermarkets, supermarkets, and modern convenience stores, across India's urban and suburban landscapes is significantly enhancing ketchup's shelf visibility and accessibility. Organized retail offers manufacturers structured promotional platforms, wide SKU listing opportunities, and superior brand discovery environments, enabling trial among new consumer segments. In July 2025, Avenue Supermarts’ online grocery sales rose 21 % to ₹3,502 crore, highlighting its expansion in e‑commerce and efforts to meet growing demand for packaged foods and condiments. Simultaneously, e-commerce platforms are providing a cost-effective complementary channel for both established and emerging ketchup brands, collectively accelerating market penetration beyond the reach of conventional trade networks.

Market Restraints:

What Challenges the India Tomato Ketchup Market is Facing?

Volatility in Raw Tomato Prices

Tomato prices in India are highly susceptible to weather-related disruptions, seasonal crop failures, and transportation bottlenecks, creating significant raw material cost volatility for ketchup manufacturers. Price surges directly elevate production costs and compress manufacturer margins, particularly for mid-sized and regional players with limited backward integration capabilities. This unpredictability hampers consistent pricing strategies and may force periodic retail price revisions that negatively impact demand elasticity among price-sensitive consumer segments across India.

Competition from Traditional Condiments and Regional Sauces

Tomato ketchup faces persistent competition from deeply embedded traditional Indian condiments, including chutneys, pickles, tamarind sauces, and regional pastes, that enjoy strong household familiarity and are often sourced inexpensively through local vendors. In rural and semi-urban markets, where ketchup brand penetration remains relatively limited, traditional condiment preferences pose a significant barrier to expansion, constraining the category's addressable consumer base and limiting manufacturers' ability to scale rapidly beyond established urban strongholds.

Health Concerns Over High Sugar and Preservative Content

Growing consumer awareness about the nutritional drawbacks of conventional tomato ketchup, particularly its high sugar, sodium, and preservative content, is creating headwinds for mainstream product lines. Health-conscious urban consumers are increasingly scrutinizing ingredient labels and shifting preferences toward natural, organic, or preservative-free alternatives. This trend pressures manufacturers to invest in reformulation, potentially increasing production costs and compelling brands to adopt transparent labeling and healthier innovation strategies to retain relevance among evolving consumer preferences.

Competitive Landscape:

The India tomato ketchup market is characterized by a moderately concentrated competitive landscape, featuring a dynamic blend of multinational FMCG leaders and strong domestic players. Leading brands compete intensely on flavor portfolio breadth, consumer engagement, packaging innovation, and distribution depth, continuously refining their strategies to strengthen market positioning. Established multinationals leverage global expertise and extensive supply chain capabilities, while domestic players differentiate through regional flavor adaptation and affordability. The next tier of competitors focuses on premium positioning, ingredient quality, and e-commerce-first strategies to capture digitally active urban consumers. Ongoing consolidation through mergers and acquisitions is reshaping the competitive landscape, with larger conglomerates acquiring established regional brands to rapidly scale their packaged food portfolios and broaden national distribution reach.

Recent Developments:

- In December 2025, Reliance Consumer Products relaunched its legacy food brand SIL, expanding into everyday staples including tomato ketchup. The company introduced highly affordable packs, such as ₹1 sachets, signaling its strategic push into India’s organized ketchup and sauces segment.

India Tomato Ketchup Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Flavored, Regular, Others |

| Packagings Covered | Pouch, Bottle, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Applications Covered | Household, Commercial, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Tomato Ketchup Market Research Report and Industry Forecast Report

The India tomato ketchup market size was valued at USD 761.12 Million in 2025.

The India tomato ketchup market is expected to grow at a compound annual growth rate of 14.77% from 2026-2034 to reach USD 2,630.61 Million by 2034.

Regular ketchup, holding the largest revenue share of 68%, remains the most consumed type in India, valued for its universal taste compatibility, affordability, and widespread availability across household and commercial foodservice segments.

Key factors driving the India tomato ketchup market include the rapid expansion of the QSR and fast food sector, rising urbanization and growing middle-class expenditure on branded packaged foods, expanding organized retail and e-commerce distribution, flavor innovation aligned with India-specific palate preferences, and ongoing M&A activity consolidating the competitive landscape.

Major challenges include raw tomato price volatility impacting production costs, intense competition from deeply embedded traditional condiments such as chutney in rural and semi-urban markets, and rising health concerns over high sugar and preservative content in conventional ketchup formulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)