India Tractor Market Size, Share, Trends and Forecast by Power Output, Drive Type, Application, and Region, 2026-2034

India Tractor Market Size, Share, Trends & Forecast (2026-2034)

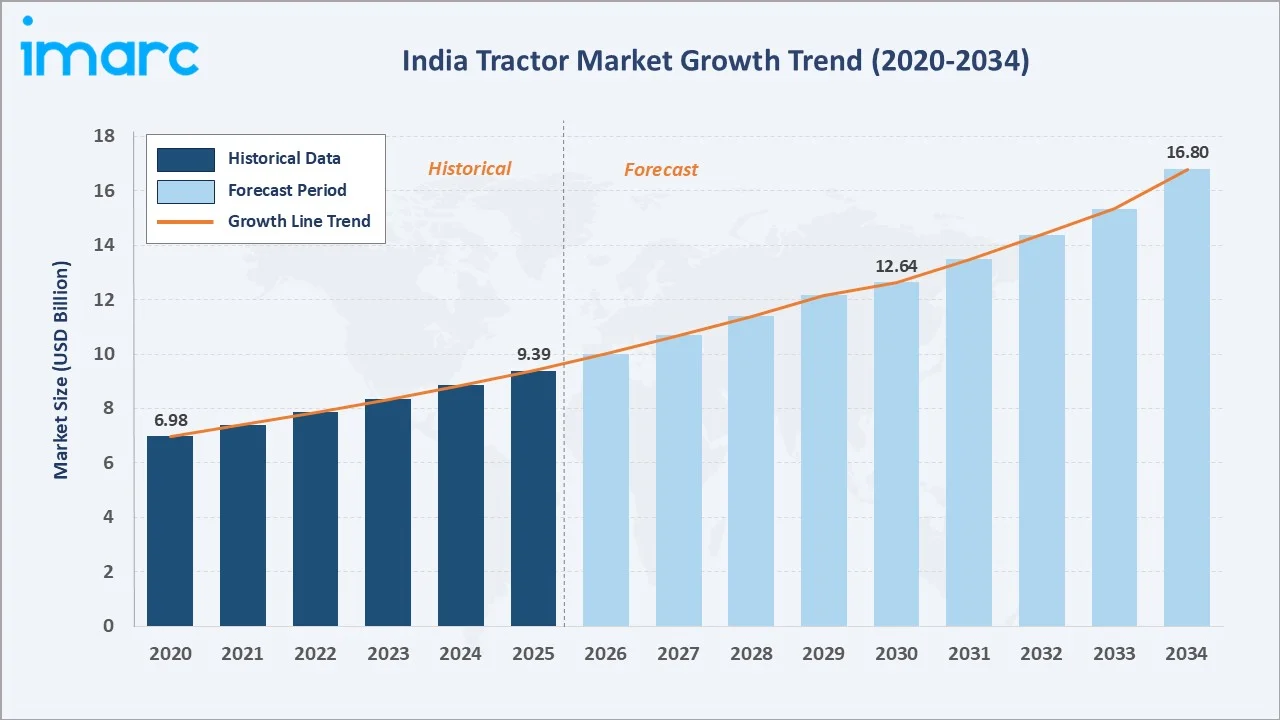

The India tractor market size reached USD 9.39 Billion in 2025 and is projected to reach USD 16.80 Billion by 2034, exhibiting a CAGR of 6.12% during 2026-2034. Rising agricultural mechanization, robust government subsidy programs, and expanding non-farm demand are the primary drivers.

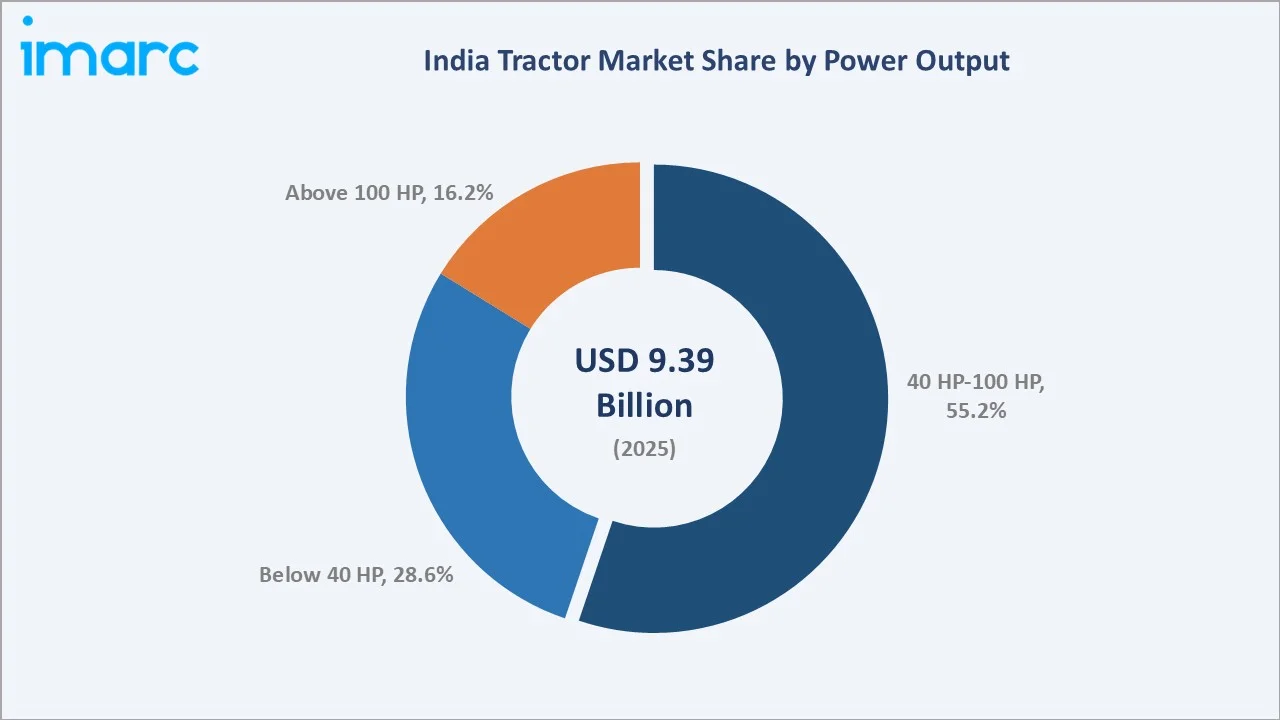

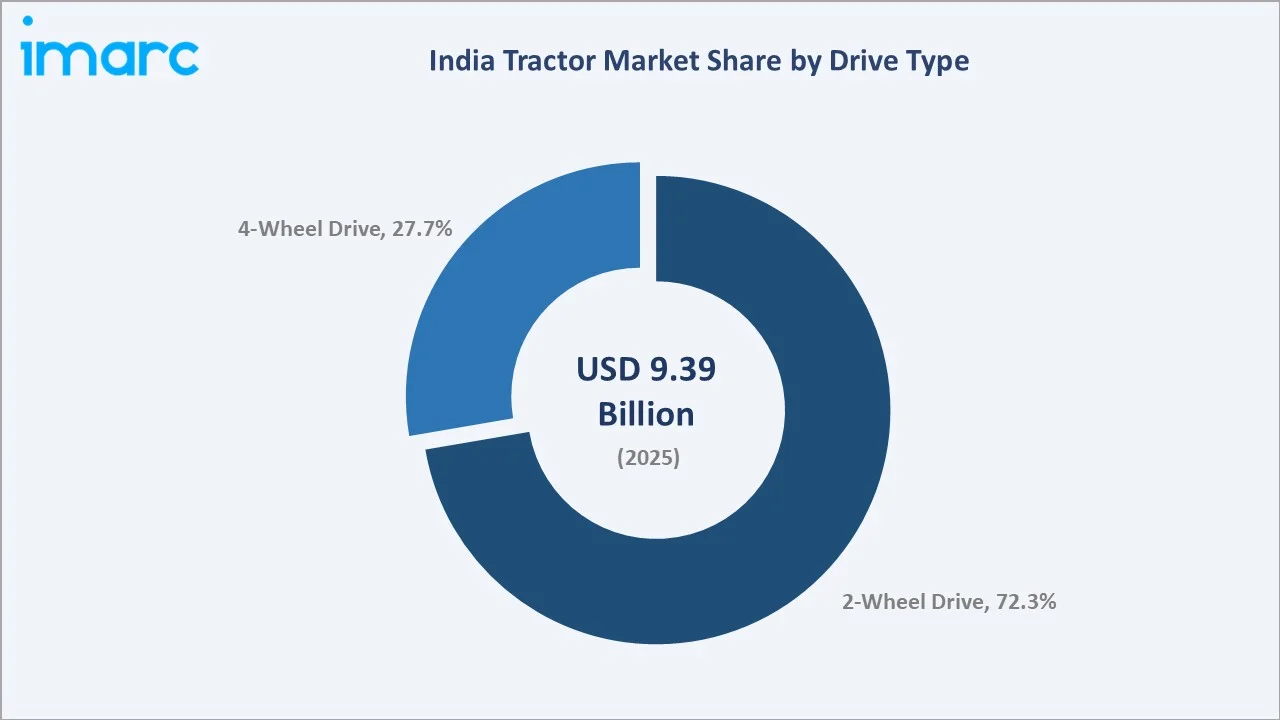

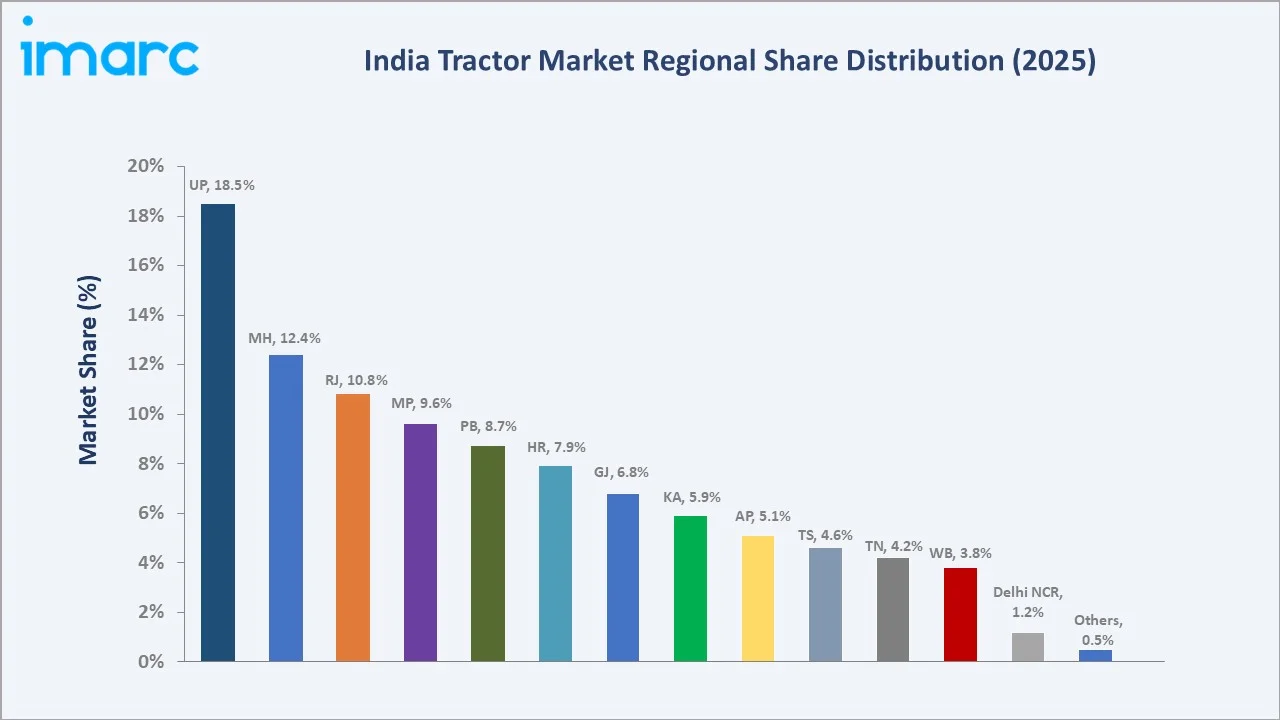

The 40 HP–100 HP segment dominates with 55.2% in 2025. 2-Wheel Drive leads drive types at 72.3%. Uttar Pradesh commands the largest regional share at 18.5%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.39 Billion |

|

Forecast Market Size (2034) |

USD 16.80 Billion |

|

CAGR (2026-2034) |

6.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Region |

Uttar Pradesh (18.5% share, 2025) |

|

Leading Power Output |

40 HP – 100 HP (55.2%, 2025) |

|

Leading Drive Type |

2-Wheel Drive (72.3%, 2025) |

The India tractor market growth trajectory from 2020 through 2034, with the historical expansion to USD 9.39 Billion in 2025, reflects agrarian-demand-driven growth, while the forecast to USD 16.80 Billion captures accelerating mechanization, policy-backed credit, and tractor penetration into construction and infrastructure applications.

To get more information on this market, Request Sample

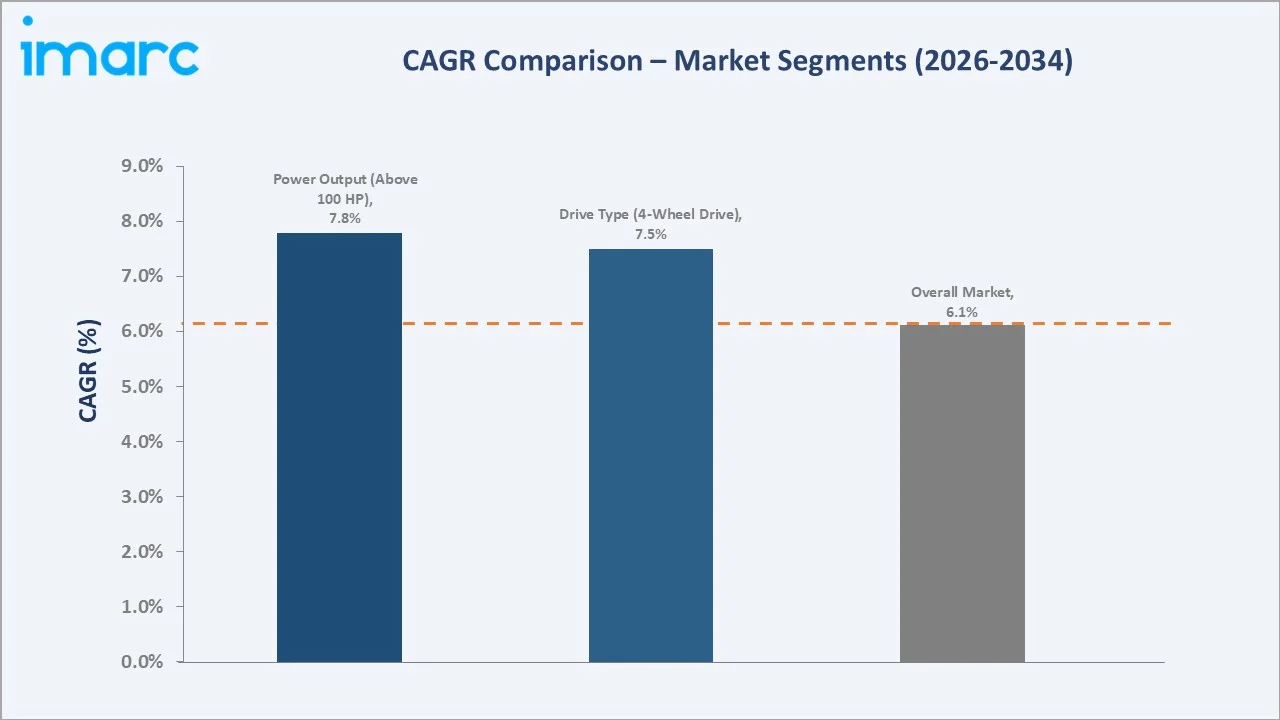

The CAGR trajectories across key sub-segments, with Above 100 HP at ~7.8% CAGR and 4-Wheel Drive at ~7.5% CAGR, represent the fastest-growing categories within the India tractor industry through 2034, driven by commercial farming consolidation, construction demand, and premium technology adoption.

Executive Summary

The India tractor market is on a sustained growth trajectory from USD 9.39 Billion in 2025 to USD 16.80 Billion by 2034. Tractors remain indispensable across India's 140-million-hectare cultivated landmass, enabling mechanized tillage, sowing, harvesting, and inter-cultural operations.

The 40 HP–100 HP segment dominates at 55.2% in 2025, favoured for its balance of power, versatility, and fuel efficiency across India's diverse cropping systems, paddy, wheat, sugarcane, and cotton.

The 2-Wheel Drive segment maintains 72.3% dominance, driven by cost affordability and suitability for flat agricultural terrain.

Uttar Pradesh anchors the regional landscape at 18.5%, followed by Maharashtra (12.4%) and Rajasthan (10.8%), reflecting large arable land bases, rising farm incomes, and PM-KISAN-linked purchasing power across northern and western India.

Key Market Insights

|

Insight |

Data |

|

Largest Power Segment |

40 HP – 100 HP – 55.2% share (2025) |

|

Dominant Drive Type |

2-Wheel Drive – 72.3% share (2025) |

|

Leading Region |

Uttar Pradesh – 18.5% share (2025) |

|

Second Largest Region |

Maharashtra – 12.4% share (2025) |

|

Key Players |

Mahindra&Mahindra Ltd., Escorts Kubota Limited, Tractors and Farm Equipment Limited, Sonalika, Deere & Company, Indo Farm Equipment Limited, Action Construction Equipment Ltd., Standard Corporation India Limited |

Key Analytical Observations Expanding on the Above Data:

- 40 HP–100 HP dominates at 55.2% in 2025 because this power band is optimally matched to India's predominant farm sizes, crop diversity, and draft load requirements for primary tillage operations across most agro-climatic zones.

- 2-Wheel Drive leads with 72.3% as entry-level and mid-segment buyers prioritize affordability, lower maintenance costs, and compatibility with India's largely flat agricultural terrain, especially in Gangetic plain states.

- Uttar Pradesh's 18.5% share reflects the state's unmatched cultivated area of 17.7 million hectares, the highest absolute number of farm households among all Indian states, and strong PM-KISAN-linked purchasing capacity.

- Punjab at 8.7% exhibits the highest per-unit mechanization intensity among Indian states, with the paddy-wheat rotation cycle driving high fleet utilization rates and sustained replacement and fleet expansion demand.

India Tractor Market Overview

A tractor is a versatile agricultural and industrial prime mover designed to deliver high tractive effort at low speeds for pulling, pushing, and powering attached implements. Indian tractor configurations range from compact sub-20 HP mini tractors for horticultural applications to heavy-duty 120+ HP 4WD tractors for large-scale commercial farming and earthmoving.

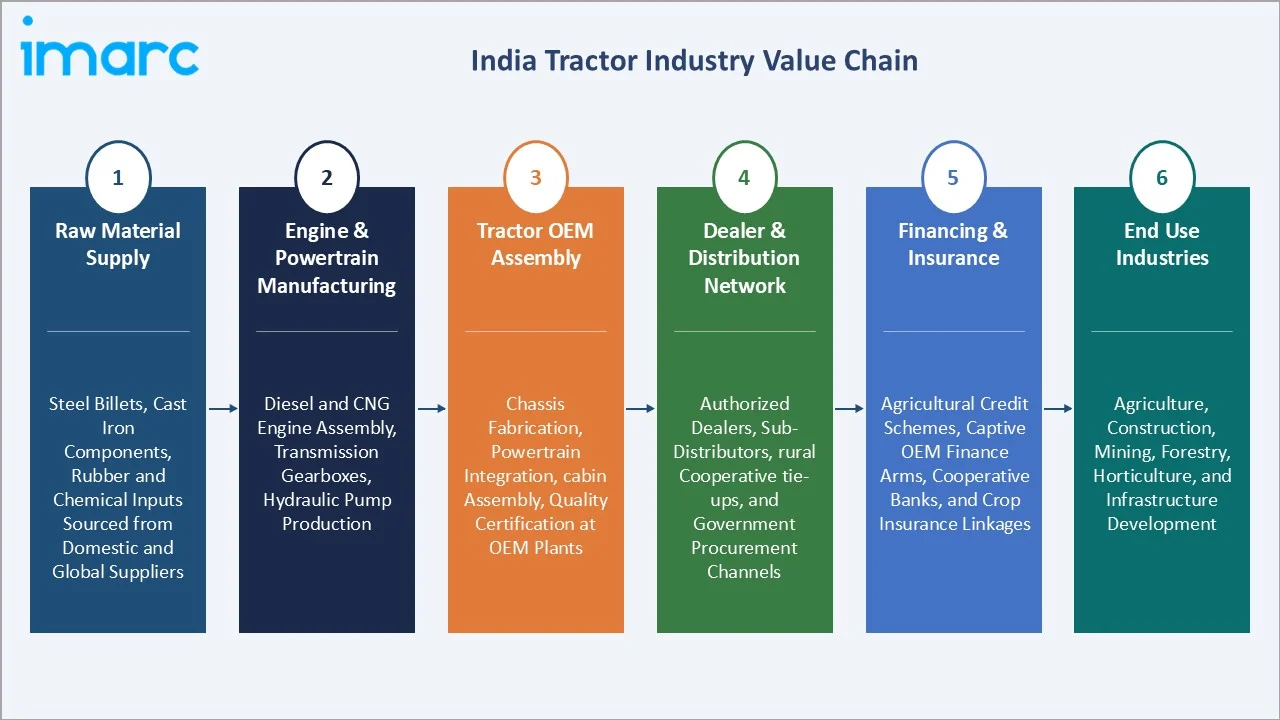

The India tractor market ecosystem integrates steel and casting raw material suppliers, engine and powertrain component manufacturers, tractor OEM assembly plants, an extensive 7,000-plus authorized dealer network, institutional financiers including NABARD and cooperative banks, and end-use buyers spanning marginal, small, and large farmer segments alongside construction contractors.

Market Dynamics

To evaluate market opportunities, Request Sample

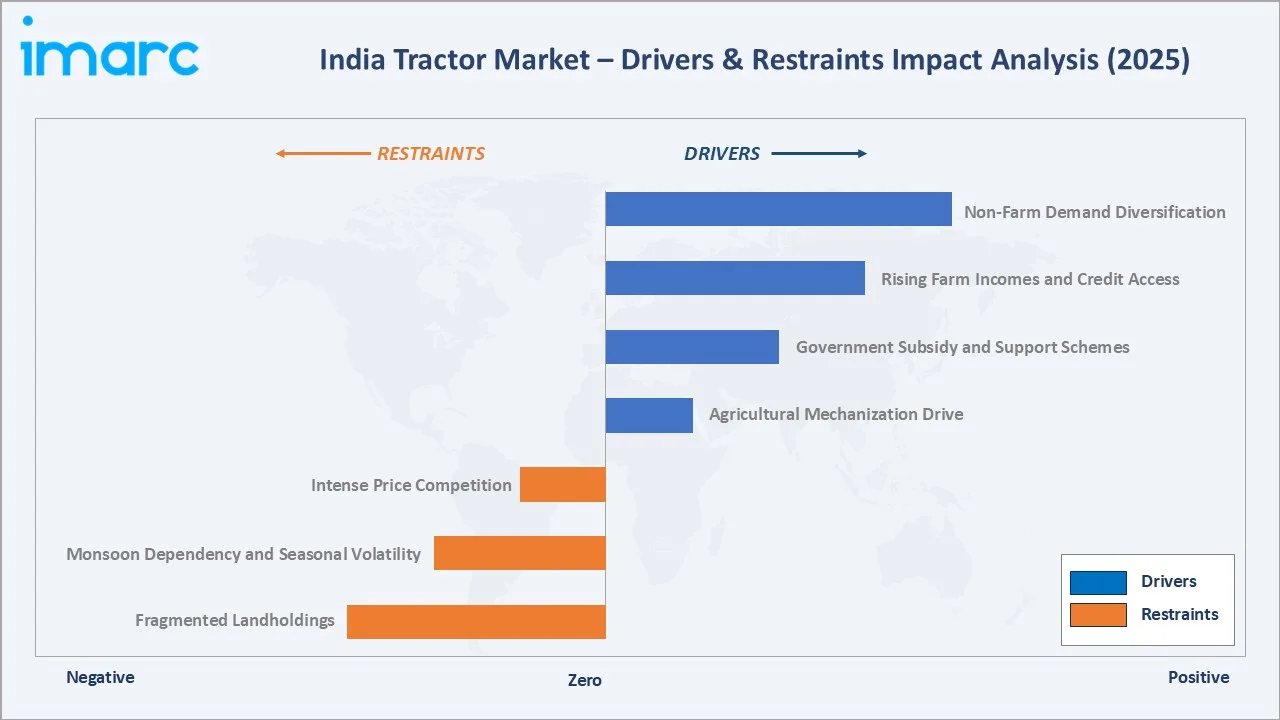

Market Drivers

- Agricultural Mechanization Drive: India's tractor density stands at approximately 16 tractors per 1,000 hectares versus 60+ in developed economies, indicating substantial headroom for penetration-driven growth as farm labour costs rise and rural wages increase across northern and central India.

- Government Subsidy and Support Schemes: PM-KISAN annual income support of INR 6,000, SMAM (Sub-Mission on Agricultural Mechanization) subsidies of 40–50% on farm equipment, and NABARD refinancing lines are collectively channelling substantial funds into rural farm mechanization annually.

- Rising Farm Incomes and Credit Access: NABARD's agricultural credit target crossed INR 20 Trillion in FY2024–25, expanding tractor loan eligibility and reducing down-payment barriers for marginal and small farmers, particularly in high-productivity states.

- Non-Farm Demand Diversification: Non-agricultural demand diversification is increasingly contributing to tractor utilization, with construction, road development, and rural infrastructure activities accounting for a growing share of overall demand. Tractors equipped with boom-mounted systems and loaders are being widely deployed in government-led rural connectivity and housing initiatives across the country.

Market Restraints

- Fragmented Landholdings: Over 86% of Indian farmers hold less than 2 hectares, limiting individual ROI on full-priced tractors and constraining natural progression to higher HP segments without custom hiring centre models or group-ownership arrangements.

- Monsoon Dependency and Seasonal Demand Volatility: Monsoon dependency continues to drive seasonal demand volatility in the tractor market, with Kharif crop performance significantly influencing annual purchasing cycles. Variability in rainfall patterns, particularly in rain-fed regions, leads to fluctuations in farm income and directly impacts buying sentiment. Weak or irregular monsoons typically result in short-term demand slowdowns across key agricultural states, creating uneven sales cycles. This dependence on weather conditions introduces revenue uncertainty for manufacturers and dealers, necessitating inventory and distribution planning aligned with seasonal trends.

Market Opportunities

- Custom Hiring Centre (CHC) Expansion: The government's Farm Machinery Banks scheme supports over 25,000 CHCs, enabling pooled tractor ownership models that extend market reach to sub-2-hectare farmers and drive unit volumes without requiring individual ownership.

- Electric and Alternative Fuel Tractors: Government PLI incentives for EV agricultural equipment are catalysing R&D investment from Mahindra, Escorts Kubota, and New Holland, creating a new high-value EV tractor segment targeting initial commercial launches from 2026 onward.

Market Challenges

- Intense Price Competition and Margin Compression: The tractor market remains highly competitive, with leading players accounting for a dominant share while the entry-level segment faces aggressive pricing pressure from domestic and low-cost competitors. This intense competition continues to compress dealer margins, limiting their ability to invest in sales, service, and aftersales infrastructure. As a result, channel partners often prioritize volume over profitability, impacting long-term network sustainability. Manufacturers are increasingly focusing on product differentiation, financing schemes, and value-added services to maintain competitiveness without eroding margins further.

- Supply Chain Disruptions and Input Cost Volatility: Fluctuations in the cost of key raw materials such as steel, castings, and hydraulic components significantly impact overall tractor manufacturing costs. Periods of input cost inflation put pressure on OEM margins and constrain their ability to pass on price increases in a competitive market. Additionally, supply chain disruptions can lead to production delays and inventory mismatches, affecting market responsiveness. These challenges often result in deferred product upgrades and slower rollout of new models during volatile cost cycles.

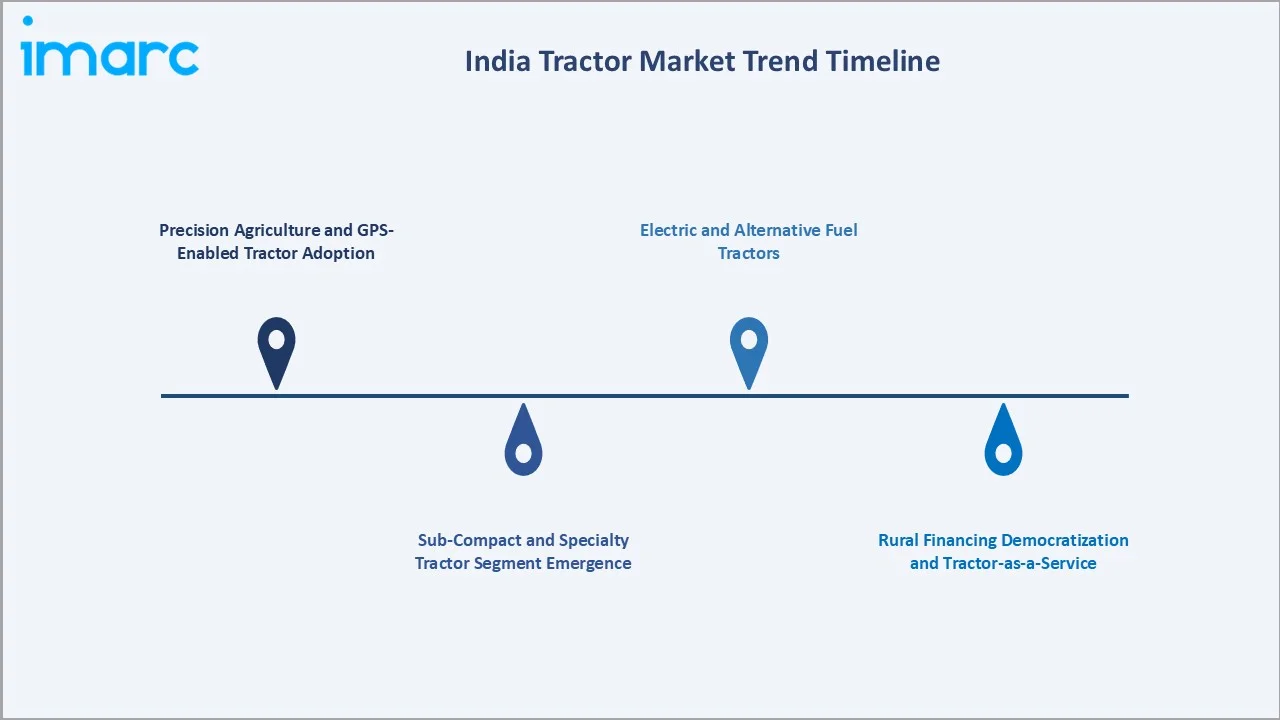

Emerging Market Trends

1. Precision Agriculture and GPS-Enabled Tractor Adoption

John Deere, Mahindra, and Escorts Kubota have integrated GPS-guided auto-steering, telematics data logging, and remote diagnostics in premium tractor platforms. Progressive farmers in Punjab, Haryana, and Maharashtra are adopting these features, targeting 5–8% input-cost savings through precision tillage path optimization and variable-rate application capabilities.

2. Sub-Compact and Specialty Tractor Segment Emergence

The below-20 HP compact tractor segment is growing at 9–11% annually, fuelled by horticulture and polyhouse cultivation expansion in Maharashtra, Himachal Pradesh, and the North-East. VST Tillers and Captain Tractors have purpose-built models specifically targeting these smallholder and specialty farming applications.

3. Rural Financing Democratization and Tractor-as-a-Service

Fintech-backed tractor lending platforms and OEM captive finance arms are reducing loan approval cycles from weeks to days. AI-credit-scoring models are extending institutional credit to millions of marginal farmers annually, materially expanding the addressable buyer pool beyond traditional credit-eligible farm households.

4. Electric and Alternative Fuel Tractors

India's FAME-III and PLI-AgriEquipment policies are accelerating EV tractor development timelines. Commercial electric tractor prototypes have been launched by leading OEMs targeting horticulture and greenhouse applications where torque profiles match electric drivetrains and short daily range requirements suit battery capacity economics.

Industry Value Chain Analysis

The India tractor value chain spans six stages from raw material procurement through end-use deployment. OEM assembly and powertrain manufacturing capture the highest value-add, while dealer financing and aftersales services generate recurring revenue streams that favour well-capitalised, vertically integrated OEMs with strong brand and service networks.

|

Stage |

Key Activities / Examples |

|

Raw Material Supply |

Steel billets, cast iron components, rubber and chemical inputs sourced from domestic and global suppliers |

|

Engine & Powertrain Manufacturing |

Diesel and CNG engine assembly, transmission gearboxes, hydraulic pump production |

|

Tractor OEM Assembly |

Chassis fabrication, powertrain integration, cabin assembly, quality certification at OEM plants |

|

Dealer & Distribution Network |

Authorized dealers, sub-distributors, rural cooperative tie-ups, and government procurement channels |

|

Financing & Insurance |

Agricultural credit schemes, captive OEM finance arms, cooperative banks, and crop insurance linkages |

|

End Use Industries |

Agriculture, construction, mining, forestry, horticulture, and infrastructure development |

Vertically integrated OEMs with captive engine manufacturing achieve cost structures 8–12% below assemblers relying on third-party powertrain procurement, enabling more competitive pricing in volume-sensitive entry-level segments while sustaining margins in the premium technology tier.

Technology Landscape in the India Tractor Industry

Engine and Powertrain Technology: TREM IV to Electric Transition

Tractor Engine Regulation Mode (TREM) IV emission norms, aligned with European Stage IIIB standards, are driving OEMs to upgrade fuel injection systems, EGR components, and exhaust after-treatment technologies. Common-rail direct injection (CRDI) engines offering 8–12% better fuel efficiency versus conventional DI engines are progressively being adopted across the 40–75 HP mid-range by leading manufacturers including Mahindra and Escorts Kubota.

Precision Agriculture and Telematics Integration

Advanced tractor platforms now incorporate ISOBUS-compatible electronic control units (ECUs) enabling interoperability with precision implements, GPS auto-steering systems capable of sub-10cm pass-to-pass accuracy, and real-time telematics transmitting machine health data to OEM cloud platforms. John Deere Operations Center and Mahindra DigiSense are actively deployed across thousands of premium units in India.

Material Innovation: High-Strength Fabrication and Lightweighting

High-strength low-alloy (HSLA) steel grades are progressively replacing conventional mild steel in tractor chassis and axle housings, reducing structural weight by 8–12% while maintaining load-bearing specifications. Composite polymer hoods, lightweight aluminium hydraulic manifolds, and glass-fibre reinforced dashboard panels are improving tractor ergonomics and fuel economy simultaneously.

Digital Design and Simulation-Driven Product Development

Leading Indian OEMs are investing in finite element analysis (FEA) simulation platforms, virtual tractor testing environments, and digital twin models that reduce physical prototype cycles by 30–40%. Computational fluid dynamics (CFD) is being applied to engine cooling and cab ventilation design, shortening new model development timelines from 36 months to 24 months at leading OEMs.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Power Output | 40 HP - 100 HP | 55.2% | 2025 |

| Drive Type | 2-Wheel Drive | 72.3% | 2025 |

| Application | Agriculture | 82.4% | 2025 |

| Region | Uttar Pradesh | 18.5% | 2025 |

By Power Output

The 40 HP–100 HP segment commands a 55.2% majority share in 2025, owing to its versatility across India's diverse agro-climatic zones. This mid-range power band is compatible with primary tillage, paddy transplanting, sugarcane harvesting, and transportation of harvested produce across most Indian farming conditions and land sizes.

To access detailed market analysis, Request Sample

The Below 40 HP segment holds 28.6% in 2025, driven by smallholder and horticultural demand in southern and hilly states.

Above 100 HP accounts for 16.2%, with rising adoption in Punjab, Haryana, and commercial farm operations, growing at the fastest CAGR of ~7.8% through 2034 reflecting heavy-duty application expansion.

By Drive Type

2-Wheel drive tractors dominate with 72.3% in 2025, reflecting their cost advantage and operational suitability for India's predominantly flat agricultural plains across northern and central India.

4-Wheel drive tractors hold 27.7% and are growing faster at ~7.5% CAGR through 2034, driven by heavy-duty construction applications, hilly terrain mechanization in Uttarakhand and the Northeast, and superior traction advantage in waterlogged paddy fields across eastern India.

Regional Market Insights

|

State / Region |

Share (2025) |

Key Growth Drivers |

|

Uttar Pradesh |

18.5% |

Large, cultivated area, dense rural population, strong mechanization demand |

|

Maharashtra |

12.4% |

Diverse cropping patterns, cash crop cultivation, rising mechanization intensity |

|

Rajasthan |

10.8% |

Extensive arid agricultural tracts, wheat and mustard belt expansion |

|

Madhya Pradesh |

9.6% |

Major soybean and wheat producing state, farm income growth |

|

Punjab |

8.7% |

Highest mechanization intensity, paddy-wheat cycle, fleet replacement demand |

|

Haryana |

7.9% |

High farm incomes, sugarcane and wheat cultivation, 4WD tractor adoption |

|

Gujarat |

6.8% |

Cotton and groundnut belts, strong cooperative farming network |

|

Karnataka |

5.9% |

Diverse crops including ragi, maize and sugarcane; horticulture mechanization drive |

|

Andhra Pradesh |

5.1% |

Rice and tobacco cultivation; Krishna-Godavari delta farm mechanization |

|

Telangana |

4.6% |

Cotton and paddy cultivation; rising farm incomes post-state formation |

|

Tamil Nadu |

4.2% |

Rice, banana and sugarcane; cooperative farming; small farm mechanization |

|

West Bengal |

3.8% |

Paddy cultivation dominance; mechanization push across rice bowl districts |

|

Delhi NCR |

1.2% |

Peri-urban farming; tractor demand driven by construction and infrastructure use |

|

Others |

0.5% |

North-eastern states, J&K, Himachal Pradesh; niche horticulture and hill farming demand |

Uttar Pradesh's 18.5% dominance reflects the state's 17.7 million hectares of cultivated land and dense rural economy anchored by wheat, paddy, and sugarcane.

Maharashtra (12.4%) and Rajasthan (10.8%) reflect diverse cropping patterns and large arable geographies combined with rising mechanization intensity under PM-KISAN support.

Punjab (8.7%), while geographically smaller, demonstrates the highest per-hectare tractor intensity in India. The paddy-wheat rotation cycle and early adoption of precision tillage equipment create sustained replacement and fleet expansion demand.

Competitive Landscape

The India tractor market is moderately concentrated, with the top five manufacturers, collectively commanding approximately 80% of annual domestic sales. Competitive differentiation is driven by dealer network depth, financing accessibility, product breadth, and after-sales service responsiveness.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Mahindra&Mahindra Ltd. |

Arjun, Yuvo, JIVO, OJA Series |

Leader |

Broadest portfolio; rural dealer network; EV tractor R&D |

|

Escorts Kubota Limited |

Powertrac, Farmtrac, Kubota |

Leader |

Kubota JV synergies; rice-paddy variants; global exports |

|

Tractors and Farm Equipment Limited |

Eicher Tractors, IMT Tractors, Massey Ferguson Tractors |

Leader |

MF brand strength; southern India dominance; export growth |

|

Sonalika |

Tiger DI, DI Series, Cheetah |

Leader |

High-volume, low-cost; fastest capacity expansion in India |

|

Deere & Company |

D Series, E Series |

Leader |

Premium segment; precision agri; IoT-connected tractors |

|

Indo Farm Equipment Limited |

2030 DI, 2042 DI, 3035 DI, 3055 DI HT, 4175 DI,4190 DI |

Emerging |

North India regional; cost-competitive compact tractors |

|

Action Construction Equipment Ltd. |

Veer 20, ACE Veer 3000 4WD, DI Series |

Emerging |

Construction-linked tractor segment; North India focus |

|

Standard Corporation India Limited |

DI Series |

Emerging |

Low-cost segment; rural cooperative procurement |

Key players include Mahindra&Mahindra Ltd., Escorts Kubota Limited, Tractors and Farm Equipment Limited, Sonalika, Deere & Company, Indo Farm Equipment Limited, Action Construction Equipment Ltd., Standard Corporation India Limited, and others.

Key Company Profiles

Mahindra&Mahindra Ltd.

Mahindra & Mahindra is India's largest tractor manufacturer and the world's largest tractor brand by volumes. Its Farm Equipment Sector offers the broadest Indian market portfolio from 15 HP compact tractors to 74 HP heavy-duty models across multiple product series.

- Product Portfolio: Arjun, Yuvo, JIVO, OJA Series

- Recent Developments: In October 2024, Mahindra & Mahindra introduced the Arjun 605 DI 4WD tractor in North India, targeting the growing demand for higher horsepower machines in key agricultural markets. The model is equipped with a robust 4-cylinder engine, 4WD capability, enhanced PTO power, and advanced hydraulics to support heavy-duty farming operations.

- Strategic Focus: Mahindra's strategy leverages its extensive dealer network and Mahindra Finance captive arm to maintain volume leadership across all HP segments, while investing in precision agriculture telematics, EV powertrains, and export expansion to South Asia and Africa to sustain long-term revenue and market share growth.

Escorts Kubota Limited

Escorts Kubota is India's prominent tractor OEM, formed through the 2021 strategic alliance between Escorts Limited and Japan's Kubota Corporation. Powertrac and Farmtrac brands serve mid-segment buyers, while the Steeltrac targets the utility segment.

- Product Portfolio: Powertrac, Farmtrac, Kubota

- Recent Developments: In January 2025, Indian Bank partnered with Escorts Kubota Limited to provide integrated financing solutions for both dealers and farmers, aimed at improving access to credit across the agricultural value chain. The collaboration enables dealers to avail working capital support while offering customers easy access to tractor loans at competitive rates, covering the company’s full product portfolio.

- Strategic Focus: Escorts Kubota differentiates on Kubota's Japanese engineering quality, premium product certifications for export markets, and digital connectivity features including its MyEscorts telematics suite, targeting the value-premium segment with urban and progressive-farmer buyers across India and export geographies.

Tractors and Farm Equipment Limited

TAFE is India's significant tractor manufacturer and the exclusive owner for the Massey Ferguson brand in India, operating four manufacturing facilities across southern and northern India.

- Product Portfolio: Eicher Tractors, IMT Tractors, Massey Ferguson India

- Recent Developments: In November 2025, TAFE unveiled its next-generation EVX75 electric-hybrid tractor at Agritechnica 2025, showcasing its push toward sustainable and advanced farm mechanization. The model combines a hybrid powertrain with both diesel and electric capabilities, enabling operations in zero-emission as well as high-performance hybrid modes, thereby improving efficiency and reducing operating costs.

- Strategic Focus: TAFE leverages the Massey Ferguson brand's international recognition and its southern India manufacturing base to maintain dominance in Tamil Nadu, Andhra Pradesh, and Karnataka, while expanding export footprint to Africa and South Asia through the Massey Ferguson licensing network.

Market Concentration Analysis

The India tractor market is moderately concentrated at the national level, with the top five players collectively accounting for approximately 80-83% of domestic wholesale volumes in the most recent fiscal year.

Regional concentration dynamics differ materially. Punjab and Haryana show the highest brand loyalty and repeat-purchase rates, dominated by Mahindra and Sonalika. Southern states reflect stronger TAFE and Massey Ferguson penetration. The 4WD premium segment is contested primarily by Mahindra, John Deere, and New Holland, were technical differentiation and dealer service quality drive purchase decisions.

Consolidation at the national level through strategic alliances, exemplified by Escorts-Kubota, is accelerating, while smaller regional brands face margin pressure and distribution scale disadvantages that favour integration into larger OEM distribution frameworks over time.

Investment & Growth Opportunities

Fastest-Growing Segments

Above 100 HP tractors at ~7.8% CAGR through 2034 represent the highest-growth power segment, driven by commercial farming consolidation, construction demand, and export-linked mechanisation in large-scale agri-infrastructure projects. 4-Wheel Drive tractors growing at ~7.5% CAGR reflect terrain diversification and heavy-duty application penetration.

Emerging Markets

North-eastern states including Assam, Meghalaya, and Manipur are at early mechanization adoption phases with tractor penetration below 3 tractors per 1,000 hectares, representing a significant cumulative opportunity through 2034 as rural connectivity under PM Gram Sadak Yojana improves access and transport economics for farm equipment distribution.

Venture & Investment Trends

EV and smart tractor R&D investment across Indian OEMs has exceeded USD 800 Million cumulatively through 2024, supported by PLI-AgriEquipment and FAME-III incentive frameworks. Private equity interest in tractor dealership consolidation, rural fintech credit platforms, and precision agri-tech overlay services is growing, targeting the large cumulative service and aftermarket segment.

Future Market Outlook (2026-2034)

The India tractor market is forecast to expand from USD 9.39 Billion in 2025 to USD 16.80 Billion by 2034 at a CAGR of 6.12%, adding USD 7.41 Billion in incremental annual market value over the forecast period. This growth reflects the market's non-discretionary agricultural infrastructure demand characteristics.

Three structural forces will most significantly shape the trajectory. Mechanization deepening in eastern and north-eastern India—where tractor penetration remains below 10 tractors per 1,000 hectares—will generate the largest volume increments. Electric and hybrid powertrain commercialization between 2027–2030 will create a new premium-value sub-market. Smart connectivity and precision agriculture integration will progressively shift competitive differentiation from hardware specifications to data-driven yield optimisation capabilities.

Government policy continuity on PM-KISAN, SMAM subsidies, and NABARD agricultural credit disbursement will remain the single most important demand-side determinant of market growth pace, alongside monsoon performance and rural wage growth sustaining farm household purchasing power across the 2026–2034 forecast horizon.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews with India tractor industry stakeholders, including OEM product management directors, state agricultural department mechanization officers, tractor dealer principals, NABARD agricultural credit specialists, and farm equipment policy advisors at the Ministry of Agriculture & Farmers' Welfare. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include the Department of Agriculture & Farmers' Welfare Annual Report, NABARD Annual Report, Tractor and Mechanization Association (TMA) annual sales data, FAO Agricultural Mechanization Index, OECD-FAO Agricultural Outlook, Indian Council of Agricultural Research publications, and trade publications including Tractor India, Krishi Jagran, and Agriculture Today.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating India's GDP growth trajectory, agricultural output targets, farm credit expansion rates, mechanization penetration indices by state, and historical market evolution patterns. Scenario analysis was performed to account for monsoon variability and policy change risk.

India Tractor Market Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Power Outputs Covered | Below 40 HP, 40 HP - 100 HP, Above 100 HP |

| Drive Types Covered | 2-Wheel Drive, 4-Wheel Drive |

| Applications Covered | Agriculture, Construction, Mining, Forestry, Others |

| Regions Covered | Maharashtra, Tamil Nadu, Uttar Pradesh, Gujarat, Karnataka, West Bengal, Rajasthan, Andhra Pradesh, Telangana, Madhya Pradesh, Delhi NCR, Punjab, Haryana, Others |

| Companies Covered | Mahindra&Mahindra Ltd., Escorts Kubota Limited, Tractors and Farm Equipment Limited, Sonalika, Deere & Company, Indo Farm Equipment Limited, Action Construction Equipment Ltd., Standard Corporation India Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Tractor Market Report

The India tractor market reached USD 9.39 Billion in 2025, reflecting consistent demand from agricultural mechanization, government subsidy support, and growing non-farm applications in construction and infrastructure development.

The market is projected to reach USD 16.80 Billion by 2034, growing at a CAGR of 6.12% during 2026-2034, driven by deepening rural mechanization, EV tractor commercialisation, and expanding demand from non-agricultural segments including construction.

The 40 HP–100 HP segment leads with a 55.2% share in 2025, valued for its superior versatility across India's diverse cropping systems and optimal fuel efficiency for the country's predominant farm sizes and draft requirements.

2-Wheel Drive dominates at 72.3% in 2025, reflecting its cost affordability and broad suitability for India's predominantly flat agricultural plains across the Gangetic belt and central India.

Uttar Pradesh leads with 18.5% market share in 2025, driven by its 17.7 million hectares of cultivated land, the largest rural farming population in India, and strong PM-KISAN-linked purchasing power supporting mechanization investment.

Above 100 HP tractors are the fastest-growing segment at ~7.8% CAGR through 2034, driven by commercial farming consolidation, construction and infrastructure applications, and the expanding use of heavy-duty tractors in large-scale agri-operations across Punjab and Haryana.

Leading companies include Mahindra&Mahindra Ltd., Escorts Kubota Limited, Tractors and Farm Equipment Limited, Sonalika, Deere & Company, Indo Farm Equipment Limited, Action Construction Equipment Ltd., Standard Corporation India Limited, and others.

Key applications include primary and secondary tillage, crop sowing and planting, inter-cultural operations, harvesting and threshing, load transportation, and non-farm uses including road construction, building material transport, rural infrastructure development, and small-scale mining operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)