India Transformer Market Size, Share, Trends and Forecast by Power Rating, Cooling Type, Transformer Type, and Region, 2026-2034

India Transformer Market Size & Forecast 2026-2034

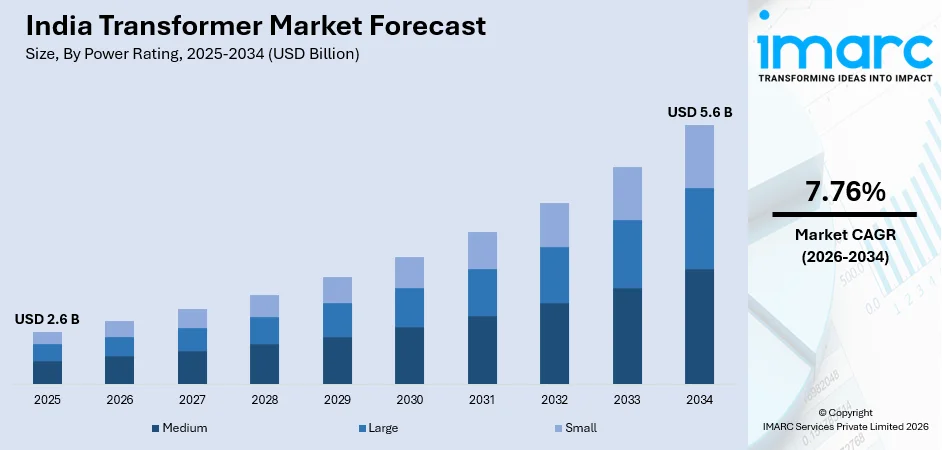

The India transformer market size, valued at USD 2.6 Billion in 2025, is projected to reach USD 5.6 Billion by 2034, growing at a CAGR of 7.76% from 2026-2034, driven by expanding power generation capacity, quick grid modernization efforts, and increasing demand for electricity in industrial and urban sectors, which support the growth. For instance, during FY 2025–26 (up to January 31, 2026), India added a record 52,537 MW of power generation capacity across sources. The expansion of large capacity systems results in increased requirements for grid infrastructure while driving up the need for transformers, which drives the development of the Indian transformer market.

To get more information on this market Request Sample

India Transformer Industry Analysis - Key Insights

- Medium commands 42.8% of power rating share in 2025 - substation upgrades and industrial grid connections between facilities demonstrate their essential function in transmitting utility-scale renewable energy throughout the nation.

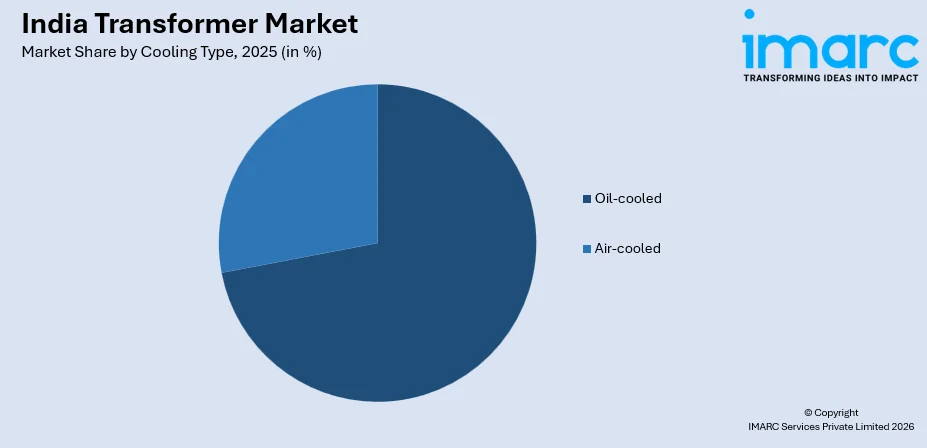

- Oil-cooled dominates cooling type at 72.3% in 2025 - triggers fierce competition from superior thermal management, long run-on life, and being the best for high power transmission at EHV levels.

- Distribution transformer leads transformer type at 48.6% in 2025 – driven by country needs large amounts of step-down equipment because the extensive last-mile grid expansion and rural electrification programs and utility modernization mandates drive their requirements.

- West India leads regionally at 29.4%in 2025 - strong industrial clusters together with renewable energy installations and extensive grid infrastructure, which exists throughout Maharashtra and Gujarat, create the need for transformers in these regions.

India Transformer Market Trends and Dynamic 2026:

Market Trends

Grid modernization and renewable integration are reshaping transformer demand.

The ongoing renewable energy transition, combined with the development of smart grid infrastructure in India, leads to an increased demand for transformer deployment across its entire transmission and distribution network system. The solar and wind energy projects need dedicated transformers that will maintain voltage stability and support their connection to the electrical grid. As of March 31, 2025, India’s total installed power generation capacity reached 475.21 GW, which increased demand for transmission equipment because of expanded grid infrastructure development. The India transformer market experienced growth because of this market development.

Smart and Digital Transformer Adoption Gaining Significant Momentum

The integration of Internet of Things sensors together with real-time monitoring systems and predictive maintenance analytics into transformer designs has become an essential requirement for Indian procurement needs. The Bureau of Energy Efficiency's updated star-label rules for transformers, implemented in 2025, have further pushed manufacturers toward higher-efficiency, technology-embedded designs that match current transformer market requirements in India.

Growth Drivers

Rising electricity demand and power infrastructure expansion

Electricity consumption in India increases due to its rising population, urban development, and industrial growth, which requires extensive development of electrical transmission and distribution systems. The population of India reached 1.46 billion people in 2025, contributing to the rising demand for electricity and the need for power systems, which resulted in the expansion of power infrastructure and transformer market growth in India.

Industrial and infrastructure development

The construction of new manufacturing clusters, metro rail systems, airports, and commercial facilities requires additional power distribution networks. The projects depend on transformer systems, which must operate reliably to deliver a constant power supply needed for essential functions.

Government initiatives supporting grid expansion

The government programs that aim to build national transmission systems and better electricity access are helping to increase transformer installation work throughout both rural and urban regions. The major programs that focus on connecting rural areas to electricity power systems and implementing smart grid technology and renewable energy solutions create ongoing demand for equipment.

Market Restraints

High capital investment requirements: Manufacturing and installing high-capacity transformers require large financial investments together with unique materials and expert engineering skills, which create a barrier to the quick expansion of production capacity.

Raw material price volatility: The manufacturing costs and profit margins of transformer manufacturers experience fluctuations because of changing prices for copper, steel, and electrical insulation materials.

Stringent environmental regulations and compliance costs: The Indian distribution networks need many legacy transformers to undergo either upgrades or complete replacements because their current state creates problems for utility companies and increases their maintenance expenses.

India Transformer Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Power Rating | Medium | 42.8% | 2025 |

| Cooling Type | Oil-cooled | 72.3% | 2025 |

| Transformer Type | Distribution Transformer | 48.6% | 2025 |

| Region | West India | 29.4% | 2025 |

Power Rating Insights

Medium - 42.8% market share (2025) | Power Rating

The energy system of India relies on medium-power transformers, which function as essential equipment for operating utility-scale renewable energy parks and 132 kV to 220 kV interstate transmission links and industrial substation upgrades that support the expansion of the country's manufacturing areas. The Central Electricity Authority's National Electricity Plan requires 123,577 circuit kilometres of new transmission lines to be constructed between 2022 and 2027, which will mainly use medium-voltage transmission systems in renewable-rich states, including Rajasthan, Gujarat, and Tamil Nadu.

|

Segment Breakdown Medium (42.8%) · Large · Small |

Cooling Type Insights

Access the comprehensive market breakdown Request Sample

Oil-cooled - 72.3% market share (2025) | Cooling Type

The Indian market for power transmission systems maintains its preference for oil-cooled transformers because these transformers demonstrate their ability to operate reliably during high-power and high-voltage transmission work that requires continuous thermal management. The development of extra-high-voltage HVDC corridors, which include the Raigarh-Pugalur link and planned Green Energy Corridor evacuation lines, will increase demand for oil-cooled transformers because these corridors require special converter and shunt reactor units that use advanced oil insulation systems.

|

Segment Breakdown Oil-cooled (72.3%) · Air-cooled |

Transformer Type Insights

Distribution Transformer - 48.6% market share (2025) | Transformer Type

The distribution transformers in India deliver essential power distribution services because they transform medium-voltage grid electricity into low-voltage power used by residential, commercial, and small industrial users throughout the nation. India launched the Revamped Distribution Sector Scheme (RDSS) in 2025 to enhance power reliability and financial efficiency. The demand for distribution transformers across India's power network is increasing because of the efforts to decrease AT&C losses and achieve the complete elimination of the ACS-ARR gap of 12-15%.

|

Segment Breakdown Distribution Transformer (48.6%) · Power Transformer |

Regional Insights

West India - 29.4% market share (2025) | Leading Region

West India's market leadership results from the combined economic power of Maharashtra and Gujarat, which together supply one-third of India's total demand for transformers. Gujarat's renewable energy capacity continues to expand because the state achieved 7449 MW of new capacity in 2024, which created a matching requirement for step-up transformers needed at solar parks, wind farms, and battery storage installations. The state petrochemical and industrial zones create a steady demand for high-capacity oil-cooled power transformers, which are used at dedicated industrial substations.

|

Regional Breakdown West India (29.4%) · North India · South India · East India |

North India:

The transformer market in North India operates at high capacity because the region has agricultural feeder networks that support its large population and developing industrial corridors that extend through Uttar Pradesh, Rajasthan, and Haryana. The companies experienced significant volume growth because of two factors: rural electrification and the development of renewable energy infrastructure.

South India:

The transformer market in South India operates through three equal components, which include renewable energy sources and electric vehicle production facilities, and commercial power needs driven by information technology. Tamil Nadu uses wind-farm evacuation systems together with port electrification projects to establish multiple power distribution transformer needs. The technology-intensive growth of the organization is driven by two main factors, which include renewable energy integration and industrial corridor development.

East India:

The transformer market in East India operates according to three main drivers, which include mining electrification, steel capacity expansion, and the provision of electricity to remote areas in West Bengal, Odisha, and Jharkhand. The industrial operations in the region require substantial power capacity because the area possesses extensive coal and mineral resources.

Market Outlook 2026-2034

What is the future outlook of the India Transformer Market?

The India transformer market is expected to sustain steady revenue growth through 2034.

The India transformer market is expected to grow continuously until 2034 since the country develops its power infrastructure and electricity usage increases in all residential, commercial, and industrial areas. The demand for transformers will remain strong because grid modernization projects, renewable energy integration, and government initiatives for better power distribution will create ongoing requirements.

India Transformer Market - Leading Key Players

The India transformer market is characterized by a competitive landscape featuring established multinational corporations and regional specialists. Key players are driving innovation through sustainable manufacturing processes, advanced fiber technologies, premium design collections, and expanded e-commerce capabilities to strengthen market positioning.

| Company | Leading Brands | Highlights |

|---|---|---|

| BHEL (Bharat Heavy Electricals Limited) | BHEL Transformers | State-owned engineering giant that manufactures power and distribution transformers; a major supplier to POWERGRID and state utilities |

| ABB India Limited | ABB Power Transformers | Global technology leader; strong presence in HV transformer segment; focus on energy efficiency and digital solutions |

| Siemens Limited (India) | Siemens Transformers | Diversified industrial conglomerate; manufactures power transformers at Kalwa and Nashik plants; innovation in smart grid integration |

Some of the other key players existing in the India transformer market include CG Power and Industrial Solutions Ltd., GE Vernova T&D India Limited, Hitachi Energy India Limited, Toshiba T&D Systems (India) Pvt. Ltd., Transformers & Rectifiers (India) Ltd, etc.

Latest Development & News

- In August 2025, Toshiba Transmission & Distribution Systems (India) Pvt. Ltd. (TTDI) launched a new automated CRGO core processing line for distribution transformers, putting its Hyderabad facility at greater production efficiency. The company opened a new surge arrester business unit, which added to its existing transformer product line. TTDI plans to increase its production capacity by 1.4 times during the upcoming one to two years to meet rising domestic and export demands.

- In May 2025, The Power Grid Corporation of India Limited (POWERGRID) selected GE Vernova Inc. to supply more than 70 extra-high-voltage transformers and shunt reactors for its major transmission projects throughout India. The 765 kV class units manufactured at GE Vernova's Vadodara facility will deliver renewable power through evacuation corridors that connect Rajasthan, Gujarat, Karnataka, Tamil Nadu, and Andhra Pradesh, with deliveries set to start in 2026.

- In April 2025, Toshiba Transmission & Distribution Systems (India) Pvt. Ltd. signed a memorandum of understanding with the Government of Telangana in Tokyo, covering capacity enhancement, job creation, and human resource development through new capital investment in its Hyderabad manufacturing campus. The MoU demonstrates Toshiba's dedication to India, which they intend to develop into a manufacturing and export center for power and distribution transformer equipment.

India Transformer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Power Ratings Covered | Large, Medium, Small |

| Cooling Types Covered | Air-cooled, Oil-cooled |

| Transformer Types Covered | Power Transformer, Distribution Transformer |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India transformer market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India transformer market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India transformer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Transformer Market Report

The India transformer market was valued at USD 2.6 Billion in 2025.

The India transformer market is anticipated to reach a value of USD 5.6 Billion by 2034.

Medium power dominates the market with a share of 42.8%, reflecting its critical role in renewable energy park connections, interstate transmission upgrades, and industrial substation infrastructure across the country.

Oil-cooled transformers command the market with a share of 72.3%, driven by their superior performance in high-voltage transmission applications, well-established maintenance ecosystems, and dominant specification status in POWERGRID and state utility procurement tenders.

Some of the major players in the India transformer market include BHEL (Bharat Heavy Electricals Limited), ABB India Limited, Siemens Limited (India), CG Power and Industrial Solutions Ltd., GE Vernova T&D India Limited, Hitachi Energy India Limited, Toshiba T&D Systems (India) Pvt. Ltd., Transformers & Rectifiers (India) Ltd, etc.

Key trends include the rapid integration of renewable energy sources driving demand for specialised inverter-duty and collector-station transformers, the growing adoption of smart and IoT-enabled digital transformers for predictive maintenance and grid optimisation, the expansion of HVDC corridors requiring converter transformer technology, and the accelerating replacement of ageing distribution transformers under BEE efficiency mandates and RDSS-funded modernisation programs.

West India currently leads the India transformer market, accounting for a share of 29.4%. The region's leadership is supported by the combined industrial and renewable energy intensity of Maharashtra and Gujarat, which together host some of India's largest solar parks, petrochemical complexes, and urban infrastructure development programs.

Key drivers include expansion of power transmission infrastructure, renewable energy integration, government programs aimed at grid modernization, and rising electricity demand across residential and industrial sectors.

The market faces challenges such as raw material price volatility, high capital investment requirements for infrastructure projects, and operational complexities associated with aging grid systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)