India Tyre Market Size, Share, Trends and Forecast by Vehicle Type, OEM and Replacement Segment, Domestic Production and Imports, Radial and Bias Tyres, Tube and Tubeless Tyres, Tyre Size, Price Segment, and Region, 2026-2034

India Tyre Market Size, Share, Trends & Forecast (2026-2034)

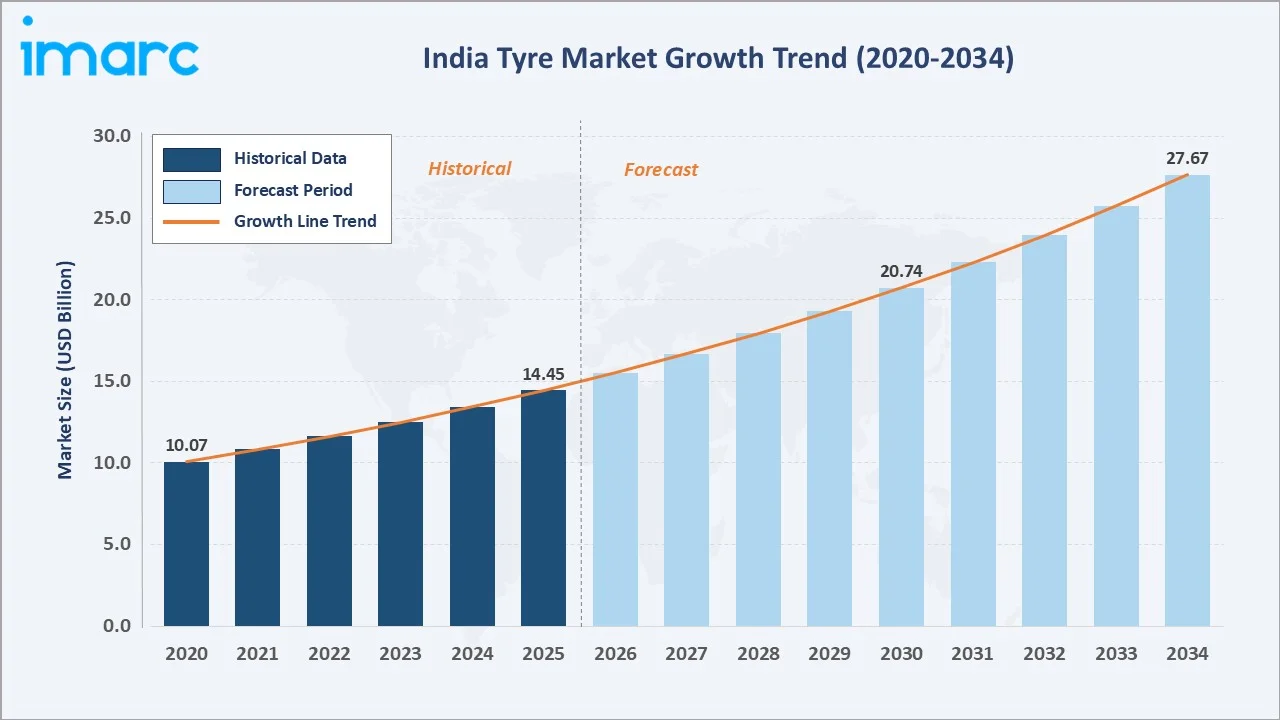

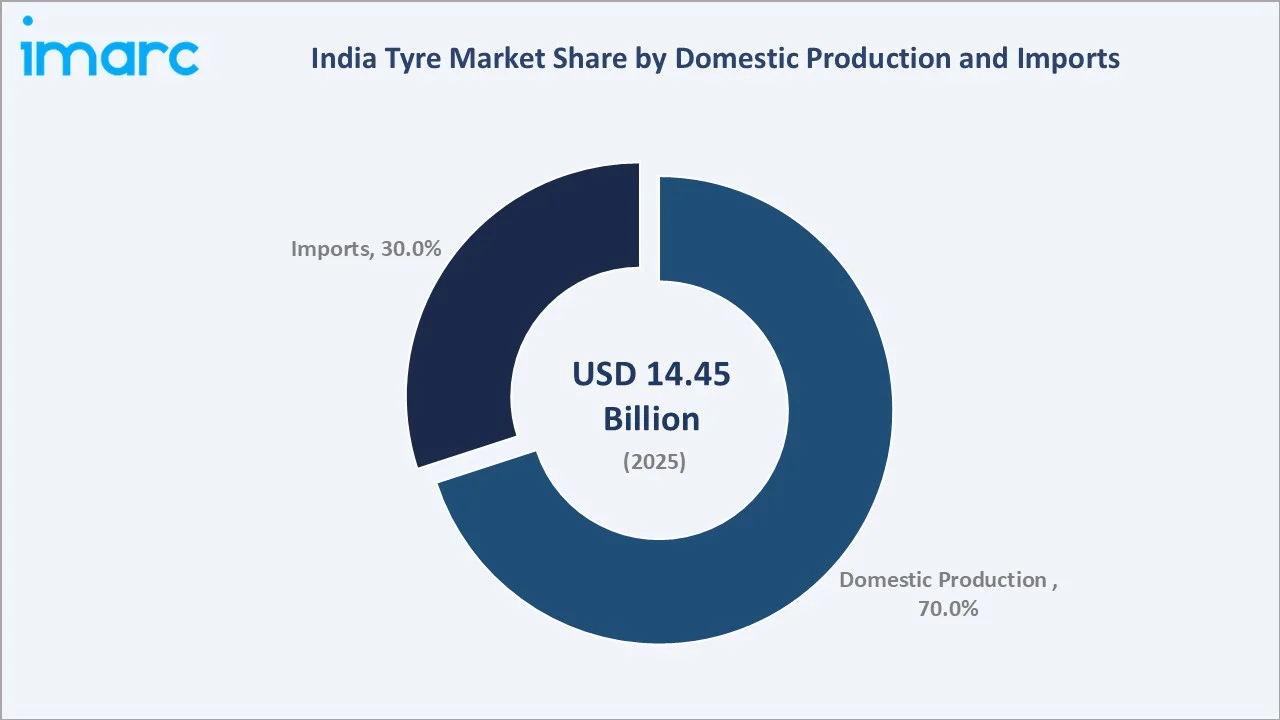

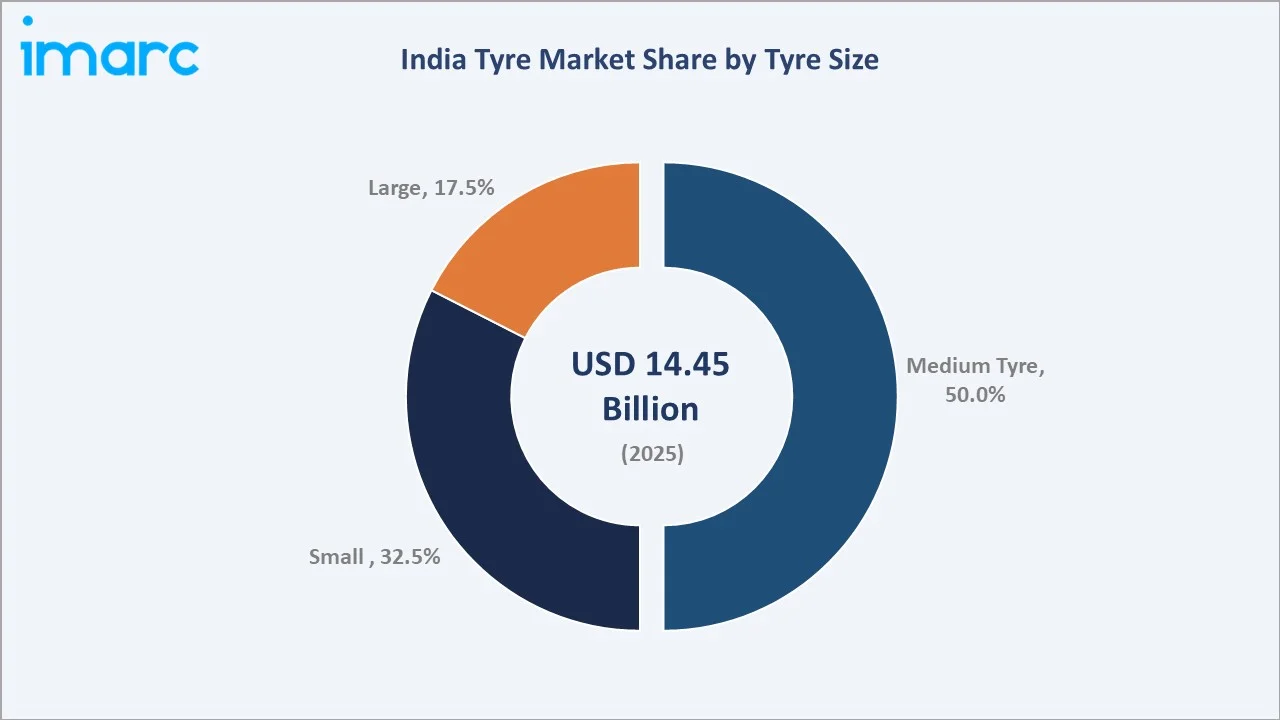

The India tyre market size reached USD 14.45 Billion in 2025 and is projected to reach USD 27.67 Billion by 2034, exhibiting a CAGR of 7.49% during 2026-2034. Rapid urbanization, rising vehicle ownership, and expanding road infrastructure continue to accelerate demand across all segments. Government PLI incentives, growing adoption of radial and tubeless technologies, and replacement tyre requirements are reinforcing India tyre market growth.

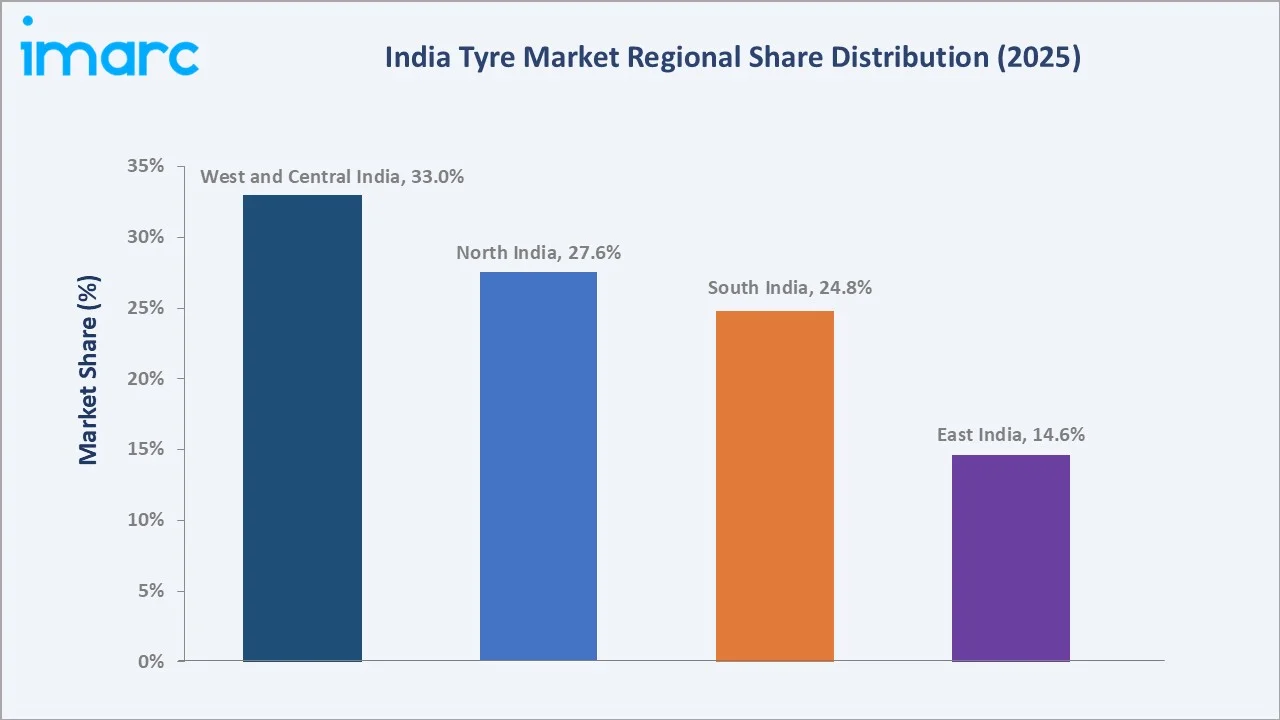

Medium tyres dominate at 50.0% share in 2025, domestic production leads at 70.0%, and West and Central India commands the largest regional share at 33.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.45 Billion |

|

Forecast Market Size (2034) |

USD 27.67 Billion |

|

CAGR (2026-2034) |

7.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (Domestic Production and Imports) |

Domestic Production (70.0%, 2025) |

|

Leading Tyre Size |

Medium (50.0%, 2025) |

|

Largest Region |

West and Central India (33.0%, 2025) |

The India tyre market growth trajectory from 2020 through 2034, with historical expansion to USD 14.45 Billion in 2025, reflects consistent vehicle-driven demand, while the forecast to USD 27.67 Billion captures accelerating EV adoption, infrastructure investment, and strengthening domestic manufacturing capabilities over the forecast period.

To get more information on this market, Request Sample

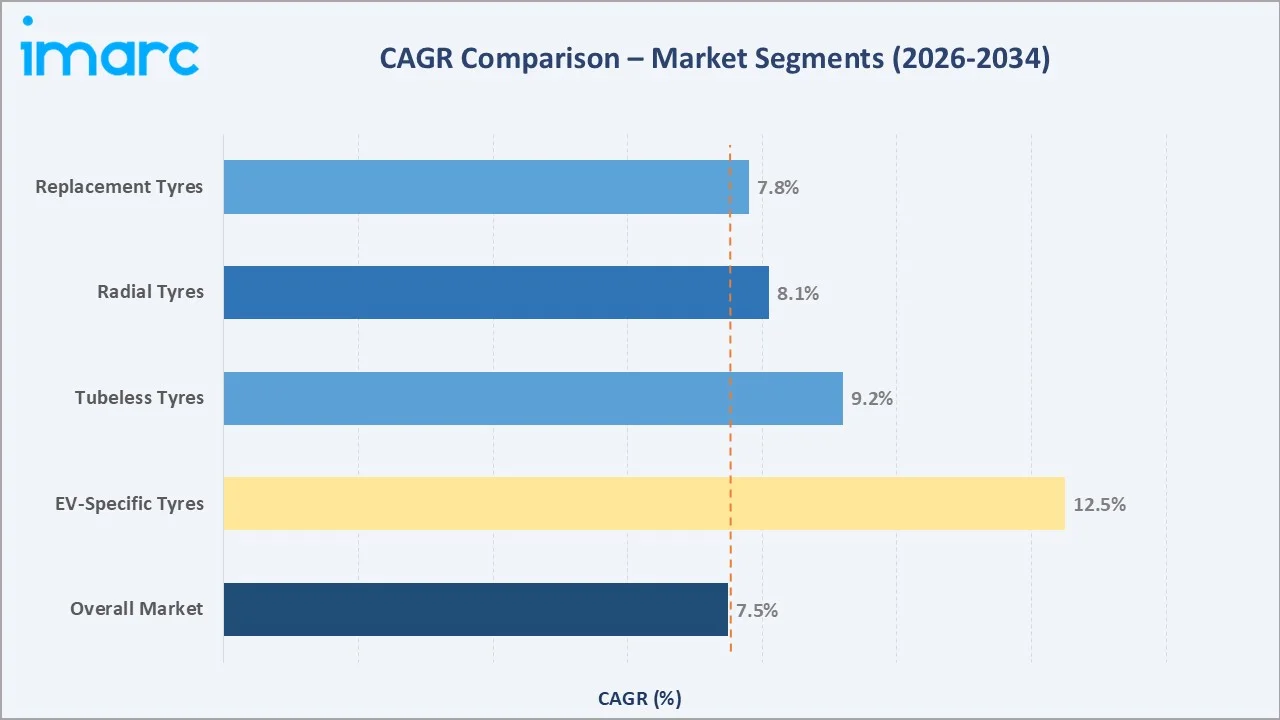

The CAGR trajectories across key tyre size, production mode, and regional sub-segments, with EV-specific tyres at ~12.5% CAGR and tubeless tyres at ~9.2% CAGR, represent the fastest-growing categories within the India tyre industry analysis through 2034. The India tyre market forecast reflects multi-dimensional demand across OEM and replacement channels.

Executive Summary

The India tyre market is on a sustained growth trajectory from USD 14.45 Billion in 2025 to USD 27.67 Billion by 2034. Tyres are an essential safety and performance component across all vehicle categories, benefiting from non-discretionary demand driven by vehicle registrations, road expansion, and mandatory replacement cycles.

Domestic production at 70.0% in 2025 reflects strong government manufacturing support, established raw material supply chains, and anti-dumping duty protection. Medium tyres at 50.0% lead the size segment, serving passenger cars, compact SUVs, and light commercial vehicles.

West and Central India dominates regionally at 33.0%, anchored by Maharashtra and Gujarat automotive production hubs. Radial tyres have established 64.0% segment leadership, while tubeless fitments account for 79.0% of total tyre market demand in 2025.

The replacement segment commands 58.0% of total market demand, sustained by an aging installed vehicle base and growing consumer awareness of safety-driven maintenance. Passenger cars lead by vehicle type at 32.0% share. The transition to EV-specific tyres, smart tyre integration, and synthetic compound adoption are defining the India tyre market trends through 2034, creating substantial product innovation and investment opportunities.

Key Market Insights

|

Insight |

Data |

|

Leading Domestic Production and Imports |

Domestic Production – 70.0% (2025) |

|

Leading Tyre Size |

Medium – 50.0% (2025) |

|

Second Tyre Size |

Small – 32.5% (2025) |

|

Third Tyre Size |

Large – 17.5% (2025) |

|

Largest Region |

West and Central India – 33.0% (2025) |

|

Top Companies |

Apollo Tyres Ltd, Bridgestone, CEAT Limited, Continental, JK Tyre & Industries Ltd., MRF Tyres, The Goodyear Tire & Rubber Company, The Yokohama Rubber Co., Ltd. |

Key Analytical Observations Expanding on the Above Data:

- Domestic production at 70.0% in 2025 dominates owing to government PLI incentives, anti-dumping duties on imported tyres, and Bureau of Indian Standards certification requirements. Indian tyre exports recorded a turnover exceeding INR 23,073 crore in FY 2024, demonstrating the sector's growing export competitiveness.

- Medium tyres at 50.0% in 2025 lead because of the high volume of passenger cars, compact SUVs, and light commercial vehicles deployed in urban logistics and personal mobility. As per IMARC Group, India's passenger car market was valued at USD 63.01 Billion in 2025, directly sustaining medium tyre demand.

- West and Central India's 33.0% dominance reflects the concentration of automobile and tyre manufacturing plants in Maharashtra and Gujarat. In October 2024, Maruti Suzuki announced EV production at its Gujarat plant from spring 2025, further stimulating regional demand.

- North India at 27.6% benefits from dense freight transportation networks, agricultural tyre demand from Punjab and Haryana, and expanding highway corridors. South India at 24.8% leverages Tamil Nadu's vehicle manufacturing base and Kerala's natural rubber cultivation.

India Tyre Market Overview

Tyres are engineered rubber compounds mounted on vehicle wheels to provide traction, support loads, absorb shocks, and enable safe vehicle operation across diverse road surfaces. Product configurations span two-wheeler tyres, three-wheeler tyres, passenger car radials, light commercial vehicle tyres, truck and bus radials, agricultural tyres, and off-road categories differentiated by size, construction, and performance specification.

India's tyre ecosystem integrates natural rubber cultivation from Kerala and northeastern states, synthetic rubber procurement, carbon black and chemical suppliers, tyre fabrication and curing facilities, hot dip galvanizing and specialized coating providers, OEM supply chains, organized retail dealerships, and end-use vehicle segments spanning personal, commercial, agricultural, and industrial categories.

Market Dynamics

To evaluate market opportunities, Request Sample

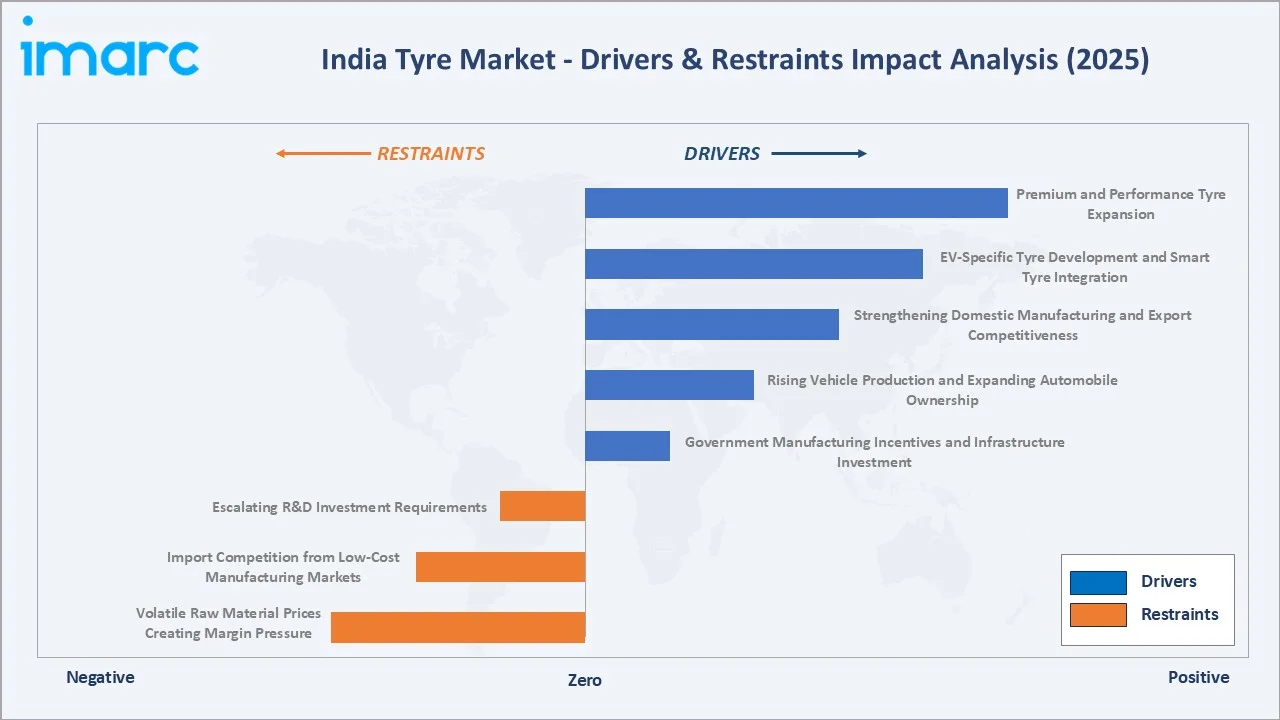

Market Drivers

- Government Manufacturing Incentives and Infrastructure Investment: The Indian government's PLI scheme incentivizes manufacturers to expand domestic production capacity and adopt advanced technologies. The national highway network expanded 60% from 91,287 km in 2014 to over 146,195 km in 2024, creating vast new road surfaces requiring consistent tyre replacement cycles. State-level policies offering land subsidies, tax concessions, and faster regulatory clearances further improve the manufacturing environment.

- Rising Vehicle Production and Expanding Automobile Ownership: Robust automobile production across all vehicle categories generates substantial OEM tyre demand while simultaneously building the installed vehicle base driving future replacement requirements. Passenger vehicle sales reached 4.3 million units in FY 2024-25 in India, as per SIAM data. In September 2024, Tata Motors commenced construction on a new greenfield manufacturing plant in Tamil Nadu to produce next-generation cars and SUVs.

- Strengthening Domestic Manufacturing and Export Competitiveness: Investments in modern production facilities, automation, and compound technologies are enabling manufacturers to scale output while meeting global quality standards. Manufacturing FDI rose 18% year-on-year in FY 2024-25, reaching USD 19.04 Billion compared to USD 16.12 Billion in FY 2023-24, reflecting heightened investor confidence in India's tyre manufacturing sector.

Market Restraints

- Volatile Raw Material Prices Creating Margin Pressure: The tyre manufacturing industry faces significant challenges from natural rubber and petroleum-derived raw material price volatility. Fluctuating input costs make long-term pricing strategies difficult, compress profit margins, and increase financial uncertainty. Cost spikes are difficult to pass on to end consumers given intense market competition, impacting profitability across the value chain.

- Import Competition from Low-Cost Manufacturing Markets: Despite anti-dumping duties and quality certification requirements, competition from low-cost tyre imports continues to exert downward pressure on domestic pricing, particularly in economy and mid-range segments. Manufacturers from neighbouring Asian countries offer products at competitive price points due to lower labour costs and raw material advantages, limiting pricing flexibility for domestic producers.

Market Opportunities

- EV-Specific Tyre Development and Smart Tyre Integration: The rapid growth of India's electric vehicle ecosystem is creating entirely new product development avenues. EV-specific low-rolling-resistance tyres, sensor-integrated smart tyre systems, and enhanced load-bearing compounds represent significant opportunity areas. India's EV market is growing substantially, with two-wheeler EV sales increasing sharply in 2024-25, driving demand for specialized tyre engineering across OEM and replacement channels.

- Premium and Performance Tyre Expansion: The growing premiumization trend in India's passenger vehicle market is reshaping tyre specifications and creating demand for larger-diameter, high-performance products. This shift is accelerating adoption of radial tyres with improved rolling resistance, wet-grip qualities, and advanced rubber formulations. SUV proliferation and the luxury vehicle segment expansion are supporting sustained premium tyre demand through 2034.

Market Challenges

- Escalating R&D Investment Requirements: Rapid evolution of tyre technology driven by EV transition, smart tyre integration, and sustainability mandates is necessitating substantial R&D expenditure. Developing specialized low-rolling-resistance tyres for EVs, integrating sensor-based monitoring systems, and formulating eco-friendly compound alternatives require sustained capital commitment that strains margins, particularly for smaller manufacturers.

- Quality and Safety Compliance Burden: Increasingly stringent BIS certification requirements, AIS (Automotive Industry Standards) mandates, and evolving tyre labelling regulations under India's Quality Control Orders impose compliance costs across the supply chain. The Bureau of Indian Standards star-labelling framework requires ongoing product testing and certification investments, creating operational complexity for smaller domestic manufacturers.

Emerging Market Trends

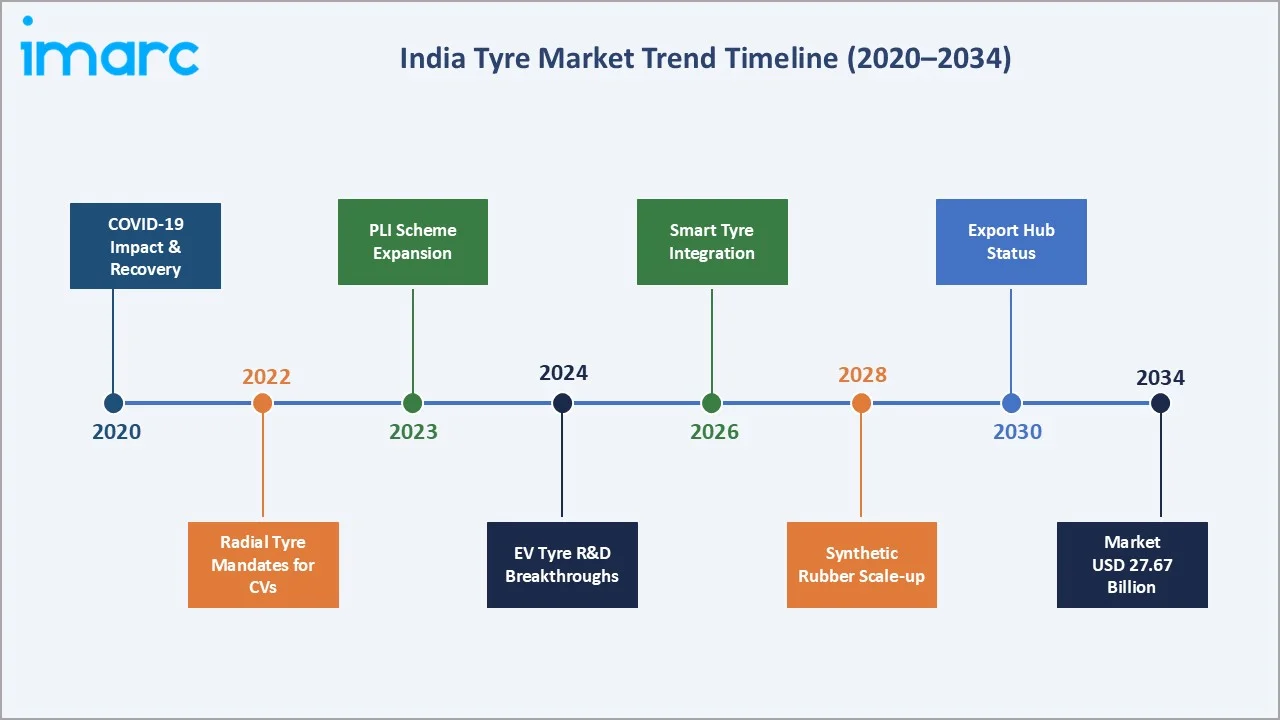

1. Growing Demand for EV-Specific Tyres

The rising adoption of electric two-wheelers and fleet-integrated electric buses is compelling tyre manufacturers to develop low-resistance, high-durability tyres tailored to EV-specific torque and load dynamics. Battery-EV fitments represent the fastest-growing propulsion segment, expanding significantly as automakers introduce new EV models with extended range and quicker charging capabilities. This shift is driving substantial investments in specialized tyre engineering, quieter tread patterns, and reinforced sidewall structures for heavier battery-pack loads. OEM and tyre producer partnerships are co-developing dedicated EV tyre platforms tailored to India's road conditions and thermal environments.

2. Expansion of Tyre-as-a-Service Business Models

Fleet operators, logistics companies, and public transport providers in India are increasingly shifting towards subscription-based and service-integrated tyre management models to optimize operating costs and improve vehicle uptime. These offerings incorporate real-time tyre pressure monitoring, predictive wear analytics, scheduled maintenance alerts, and streamlined replacement cycles under single-contract frameworks. Original equipment manufacturers and tyre producers are partnering with digital platform providers to deliver data-driven insights via telematics integration. The India tyre market outlook through 2034 indicates this model will expand significantly as large fleet aggregators and e-commerce fulfilment operators standardize fleet management practices, creating recurring revenue streams for manufacturers.

3. Adoption of Synthetic Rubber Alternatives in Manufacturing

Volatility in natural rubber prices and import dependencies from ASEAN countries are motivating Indian tyre manufacturers to accelerate adoption of synthetic rubber alternatives and advanced compound formulations. Advanced silica compounds and bio-based material integration are gaining traction as sustainability mandates intensify across the supply chain.

4. Radial Technology Mandate and Tubeless Tyre Standardization

India's regulatory drive to phase out bias tyres in commercial vehicle categories and mandate radial technology is reshaping the competitive landscape across tyre segments. Radial tyres demand is also increasing owing to superior fuel efficiency, extended tread life, and safety characteristics suited to India's expanding highway network. These India tyre market trends are expected to sustain a favourable shift toward higher-value tyre products throughout the forecast period.

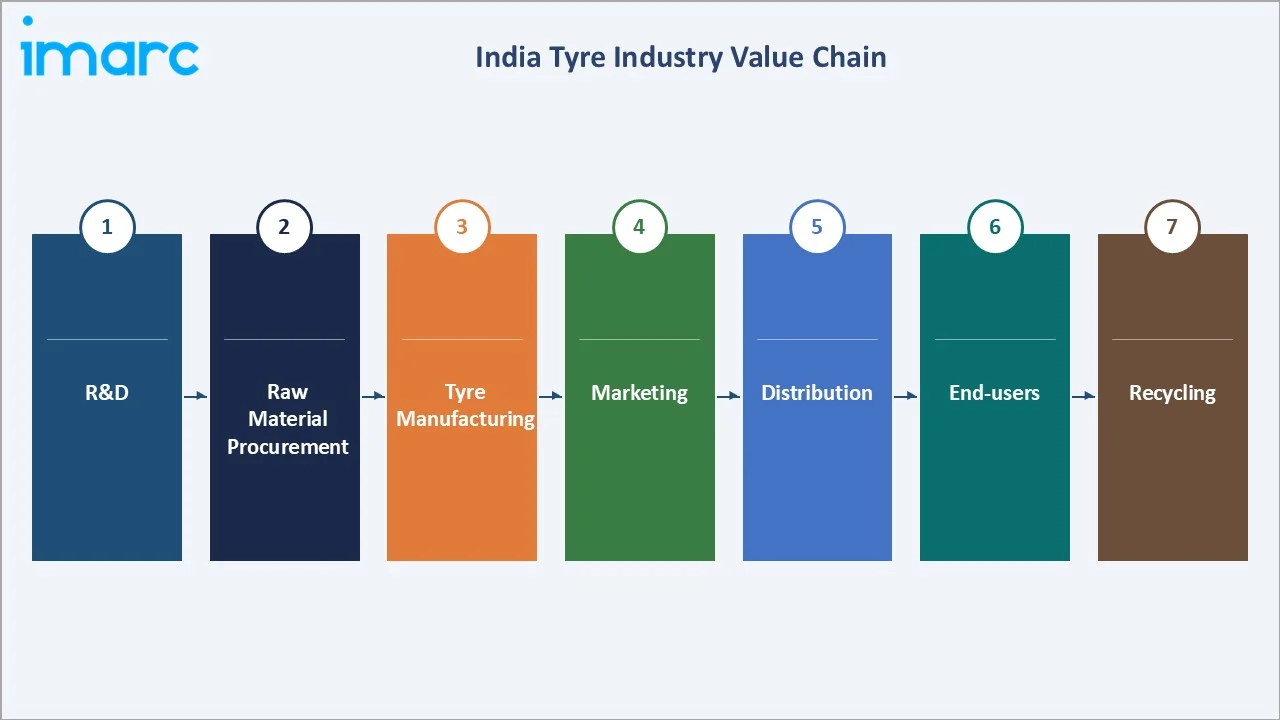

Industry Value Chain Analysis

The India tyre value chain spans eight stages from raw material procurement through recycling. Manufacturing and R&D capture the highest value-add margins, while distribution logistics and OEM supply chain management generate significant working capital requirements favouring well-capitalized mid-to-large manufacturers with diversified product portfolios.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Natural Rubber (Kerala), Synthetic Rubber, Carbon Black, Steel Cord, Chemicals |

|

R&D and Compounding |

Apollo Tyres, MRF Tyres, Bridgestone |

|

Tyre Manufacturing |

MRF Tyres, Apollo Tyres, CEAT Limited, JK Tyre & Industries Ltd., Bridgestone, Yokohama |

|

Quality Control |

BIS Certification, AIS Standards Compliance, Star-Labelling Framework |

|

Marketing and Sales |

OEM Partnerships, Retail Dealerships, Online Tyre Platforms, Fleet Sales |

|

Distribution |

Pan-India Dealer Networks, Organized Retail Chains, E-Commerce Fulfillment |

|

End-Use Segments |

Passenger Cars, 2W/3W, LCV, MHCV, Off-Road, Agricultural Machinery |

|

Recycling |

Used Tyre Collection, Pyrolysis, Crumb Rubber, Retreading |

Integrated tyre manufacturers with captive compounding facilities, in-house R&D, and pan-India distribution networks achieve lower cost structures than processors relying entirely on third-party supply chains. This vertical integration provides a meaningful competitive advantage in price-sensitive commodity segments while enabling faster response to OEM specification changes and regulatory requirements.

Technology Landscape in the India Tyre Industry

Tyre Construction and Compound Technology

Radial tyre construction dominates India's passenger and commercial tyre market, with steel belt-reinforced radials delivering superior fuel efficiency, even tread wear, and enhanced high-speed stability compared to bias-ply alternatives. Advanced silica-filled compound formulations are progressively replacing traditional carbon black compounds in premium tyre segments, delivering 20-25% rolling resistance reductions. CNC building machines and automated curing presses enable consistent dimensional accuracy and uniform vulcanization across high-volume production lines.

Smart Tyre and Sensor Integration

Tyre Pressure Monitoring System (TPMS) integration is becoming mandatory across new passenger car categories in India under evolving AIS standards, driving OEM demand for sensor-embedded tyre systems. Advanced TPMS modules measure real-time temperature, load, and pressure data, transmitting alerts to vehicle ECUs. Next-generation smart tyre platforms incorporating embedded RFID chips and strain gauges enable fleet management systems to track tyre wear, predict replacement timelines, and optimize logistics fleet uptime through predictive maintenance algorithms.

EV Tyre Engineering and Low-Rolling-Resistance Technology

Electric vehicle tyres require specialized compound formulations balancing low rolling resistance for range optimization, enhanced load-bearing capacity for battery pack weight, and reduced noise generation for the quiet EV cabin environment. Indian manufacturers are investing in silica compound optimization, tread geometry simulation using finite element analysis, and closed-cell foam inserts for acoustic comfort.

Sustainable and Bio-Based Material Innovation

Sustainability mandates and supply chain resilience requirements are driving adoption of bio-based rubber alternatives, renewable material fillers, and recycled crumb rubber integration in tyre compound formulations. Leading manufacturers are evaluating guayule-derived natural rubber and dandelion-based latex as alternatives to conventional Hevea brasiliensis rubber. These innovations align with India's circular economy goals and support tyre manufacturers seeking to demonstrate ESG credentials to global automotive OEM customers requiring supply chain sustainability certification.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Vehicle Types | Passenger Cars | 32.0% |

2025 |

| OEM and Replacement Segments | Replacement Tyres | 58.0% |

2025 |

| Domestic Productions and Imports | Domestic Production | 70.0% |

2025 |

| Radial and Bias Tyres | Radial Tyres | 64.0% |

2025 |

| Tube and Tubeless Tyres | Tubeless Tyres | 79.0% | 2025 |

| Tyre Size | Medium | 50.0% | 2025 |

| Price Segments | Medium | 55.0% | 2025 |

| Region | West and Central India | 33.0% | 2025 |

By Domestic Production and Imports

Domestic production commands a 70.0% majority share in 2025 owing to fundamental cost-competitiveness, government policy support, and a well-established supplier ecosystem. The PLI scheme for automotive components directly incentivizes manufacturers to expand domestic output and adopt advanced manufacturing technologies. Anti-dumping duties on imported tyres and BIS quality certification requirements reinforce the value proposition of locally manufactured products across price-sensitive consumer segments.

To access detailed market analysis, Request Sample

Imports at 30.0% in 2025 primarily consist of specialty tyre categories, premium passenger car fitments, and off-road tyre ranges not manufactured domestically at scale. Premium international tyre brands maintain import flows despite duty structures, targeting the growing luxury and performance vehicle segment. Ongoing policy reviews and quality certification harmonization may gradually reshape the import-domestic competitive balance over the 2026-2034 forecast period.

By Tyre Size

Medium tyres prevail with a 50.0% leading share in 2025, driven by robust demand from passenger cars, compact SUVs, and light commercial vehicles operating across India's urban and semi-urban road network. The expansion of logistics infrastructure, growing preference for mid-size passenger vehicles, and increasing SUV penetration sustain consistent medium tyre demand.

Small tyres at 32.5% in 2025 are primarily driven by India's large two-wheeler and three-wheeler fleet, which represents one of the world's largest vehicle populations in absolute terms. Large tyres at 17.5% serve medium and heavy commercial vehicles, off-road equipment, and agricultural machinery, with demand supported by construction, mining, and freight logistics expansion under national highway development programs. Manufacturers are actively developing product portfolios across all size categories to capture demand from India's diversified vehicle mix.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West and Central India |

33.0% |

Maharashtra & Gujarat auto hubs; Delhi-Mumbai Industrial Corridor; EV manufacturing ramp-up; commercial vehicle demand |

|

North India |

27.6% |

Agricultural tyre demand; highway freight networks; Amritsar-Kolkata Industrial Corridor; growing infrastructure spend |

|

South India |

24.8% |

Tamil Nadu & Karnataka vehicle manufacturing; natural rubber cultivation in Kerala; expanding port logistics |

|

East India |

14.6% |

Mining and construction tyre demand; growing e-commerce logistics fleet; infrastructure upgrades in Jharkhand and Odisha |

West and Central India's 33.0% market dominance in 2025 is driven by the concentration of major automobile and tyre manufacturing plants across Maharashtra and Gujarat. In October 2024, Maruti Suzuki announced plans to produce its first EV for Toyota at its Gujarat plant from spring 2025, further stimulating regional tyre demand. The extensive highway network, industrial corridors connecting key states, and the presence of major tyre manufacturers in Pune and Indore strengthen the regional supply chain ecosystem.

North India at 27.6% benefits from dense agricultural activity generating consistent demand for farm-use tyres, a vast freight transportation network linking major consumption centers, and ongoing highway development. South India at 24.8% leverages its position as a key vehicle manufacturing hub in Tamil Nadu and Karnataka, combined with natural rubber cultivation in Kerala.

Competitive Landscape

The India tyre market is characterized by a mix of established domestic manufacturers and international players competing across diverse vehicle and price segments. Domestic companies leverage strong brand recognition, extensive distribution networks, and proximity to manufacturing bases to maintain leadership. International manufacturers focus on premium positioning and technology differentiation to capture higher-value market tiers. The competitive landscape is intensifying as manufacturers invest in capacity expansion, advanced manufacturing technologies, and product innovation.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

MRF Tyres |

Passenger Car Tyres, Two-Wheeler Tyres, OTR Tyres, 3-Wheeler Tyres |

Leader |

Largest domestic share; premium OEM supply; R&D leadership |

|

Apollo Tyres Ltd |

Car Tyres, SUV & Van Tyres, Bike & Scooter Tyres, Agricultural Tyres, Truck and Bus Tyres |

Leader |

Global expansion; EV tyre innovation; premium passenger segment |

|

CEAT Limited |

Passenger Car Tyres, Commercial Tyres, Two-Wheeler Tyres, 3-Wheeler Tyres |

Leader |

Mid-segment leadership; strong distribution network; EV portfolio |

|

Bridgestone |

Passenger Car Tyres, Truck & Bus Tyres, Off Road Tyres |

Leader |

Premium OEM partnerships; Pune and Indore manufacturing; global tech |

|

JK Tyre & Industries Ltd. |

Passenger Car Tyres, 2 & 3-Wheeler Tyres, Industrial Tyres |

Challenger |

Commercial vehicle leadership; OTR expansion; smart tyre development |

|

Continental |

Car & Van Tyres, 2-Wheeler Tyres |

Challenger |

Premium passenger; OEM supply to German automakers; EV tyre focus |

|

The Goodyear Tire & Rubber Company |

Passenger Tyres, SUV/4x4 Tyres, Farm/Agricultural Tyres |

Challenger |

Global brand strength; retail presence; performance segment strategy |

|

The Yokohama Rubber Co., Ltd. |

Passenger Tyres |

Emerging |

Premium segment; OEM supply; Japan-backed technology deployment |

Key players include MRF Tyres, Apollo Tyres Ltd, CEAT Limited, Bridgestone, JK Tyre & Industries Ltd., Continental, The Goodyear Tire & Rubber Company, The Yokohama Rubber Co., Ltd., and others.

Key Company Profiles

MRF Tyres

MRF Tyres is India's largest tyre manufacturer by revenue and market share, headquartered in Chennai, Tamil Nadu. MRF's scale, deep OEM relationships, and extensive pan-India distribution network underpin its dominant market position.

- Product Portfolio: Offers passenger car tyres, two-wheeler tyres, OTR tyres, 3-wheeler tyres, and others.

- Recent Developments: In March 2026, MRF signed a memorandum of understanding (MoU) with the Tamil Nadu government to establish a new greenfield manufacturing plant in Sivaganga district. The proposed facility, focused on producing automotive tyres and related products, will be set up at the SIPCOT Industrial Park. The project is expected to involve an investment of around ₹5,300 crore over a 12-year period and could create approximately 1,000 direct jobs..

- Strategic Focus: MRF's strategy leverages its scale, brand equity, and distribution depth to compete on total delivered value in the Indian market, while selectively pursuing premium passenger and performance tyre segments where higher margins support continued R&D investment.

Apollo Tyres Ltd

Apollo Tyres Ltd is a leading Indian multinational tyre manufacturer headquartered in Gurugram, Haryana, with manufacturing operations in India, Netherlands, and Hungary. Apollo has pursued aggressive capacity expansion and technology investment to establish a position in both domestic OEM supply and European replacement markets.

- Product Portfolio: Company offers car tyres, SUV & van tyres, bike & scooter tyres, agricultural tyres, truck and bus tyres, and others.

- Recent Developments: In January 2026, Apollo Tyres introduced a new range of truck-bus bias (TBB) tyres aimed at improving performance while reducing the overall operating costs for fleet operators. Developed through collaboration between its global R&D and manufacturing teams, the new range incorporates advanced technology to enhance durability, mileage, and on-road reliability. The company has added three new tyre models—XT 1x, XT 2x, and XR 1x—in the widely used 10.00–20 size segment, catering to various truck and bus applications.

- Strategic Focus: Apollo's strategy focuses on EV tyre innovation, premium product positioning in both domestic and European markets, and strengthening OEM partnerships with leading passenger vehicle manufacturers transitioning to electric platforms.

CEAT Limited

CEAT Limited, a flagship company of the RPG Group, is one of India's largest tyre manufacturers headquartered in Mumbai, Maharashtra. CEAT serves OEM and replacement channels across two-wheelers, passenger cars, and commercial vehicles with a broad mid-segment product portfolio.

- Product Portfolio: Offers passenger car tyres, commercial tyres, two-wheeler tyres, 3-wheeler tyres, and others.

- Recent Developments: In August 2025, CEAT launched SecuraDrive CIRCL, India’s first road-ready passenger car tyre made with up to 90% sustainable, bio-based materials. Developed at its R&D facility in Halol, the tyre is designed to combine environmental responsibility with high performance, safety, and durability.

- Strategic Focus: CEAT's strategy targets mid-market leadership through competitive pricing, strong distributor relationships, and early entry into the EV-specific tyre segment to capture first-mover advantage in this rapidly growing category.

JK Tyre & Industries Ltd.

JK Tyre & Industries Ltd. is a leading Indian tyre manufacturer headquartered in New Delhi, with plants across Rajasthan, Madhya Pradesh, Tamil Nadu, and Karnataka. JK Tyre is particularly strong in the commercial vehicle tyre segment and has been expanding its OTR tyre portfolio for construction and mining applications.

- Product Portfolio: Offers passenger car tyres, 2 & 3-wheeler tyres, industrial tyres, and others.

- Recent Developments: In January 2026, JK Tyre inaugurated Phase III of capacity expansion and modernization at its passenger car radial (PCR) tyre manufacturing facility in Banmore, Madhya Pradesh. This expansion is part of the company’s multi-phase investment plan of over ₹1,000 crore, aimed at strengthening its domestic manufacturing capabilities.

- Strategic Focus: JK Tyre focuses on commercial vehicle and OTR segment leadership, smart tyre technology development, and strengthening its distribution network to capture growing construction and logistics tyre demand across India's expanding infrastructure investment cycle.

Market Concentration Analysis

The India tyre market is moderately concentrated, with the top five domestic manufacturers holding approximately 65-70% of total market revenue by value in 2025. MRF Tyres, Apollo Tyres, CEAT, Bridgestone India, and JK Tyre collectively dominate OEM supply channels, while international players including Continental, Goodyear, and Yokohama compete in premium segments.

Consolidation pressure is building as manufacturers invest in capacity expansion, advanced tyre technologies, and digital customer engagement platforms. The shift toward EV-specific tyres, smart tyre integration, and sustainable materials is expected to widen the performance gap between well-capitalized large manufacturers and smaller regional players, potentially accelerating market consolidation over the 2026-2034 forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

EV-specific tyres at ~12.5% CAGR through 2034 represent the highest-growth sub-segment, driven by India's accelerating electric two-wheeler and electric bus adoption. Tubeless tyres growing at ~9.2% CAGR reflect regulatory standardization across new vehicle platforms. The replacement market, driven by the expanding installed vehicle base and growing consumer safety awareness, sustains broad-based volume growth across all tyre categories through 2034.

Emerging Markets

East India at the fastest regional CAGR through 2034 is driven by accelerating mining and construction activity in Jharkhand, Odisha, and West Bengal, alongside growing logistics fleet deployment. North India's agricultural tyre demand is strengthening as farm mechanization deepens. Export opportunity from India to ASEAN, Middle East, and Africa markets is growing, with Indian tyre exports already exceeding INR 23,073 crore in FY 2024.

Venture & Investment Trends

Private equity and strategic investors are increasingly attracted to India's tyre sector, driven by its high-growth domestic market, strong export potential, and government-backed manufacturing incentives under the PLI scheme. Foreign tyre manufacturers are evaluating greenfield and joint-venture investments in India as part of China-plus-one supply chain diversification strategies. Sustainability investments, including natural rubber certification, recycled material integration, and carbon footprint reduction programs, are gaining prominence as global automotive OEMs impose ESG requirements on tyre supply chains.

Future Market Outlook (2026-2034)

The India tyre market is forecast to expand from USD 14.45 Billion in 2025 to USD 27.67 Billion by 2034 at a CAGR of 7.49%, adding over USD 13 Billion in incremental annual market value. This consistent, sustained growth reflects the market's vehicle-linked, non-discretionary demand characteristics and India's structural economic growth momentum.

Three technological forces will most significantly shape the India tyre industry through 2034. EV-specific tyre engineering, with India targeting 30% EV penetration by 2030 across two-wheelers, will generate specialized low-rolling-resistance demand at premium pricing. Smart tyre integration with TPMS mandates, fleet telematics, and predictive wear analytics will create recurring digital service revenue streams. Sustainable compound innovation using synthetic rubber alternatives and bio-based materials will reshape supply chains and support export market access under increasingly stringent ESG procurement criteria of global OEMs.

Research Methodology

Primary Research

Primary research encompassed structured interviews with India tyre industry stakeholders in 2024-2025, including senior commercial managers from leading tyre manufacturers, OEM procurement specialists, fleet operators, tyre retail chain managers, Automotive Component Manufacturers Association (ACMA) representatives, and SIAM data analysts. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include SIAM automotive sales data, Automotive Tyre Manufacturers' Association (ATMA) annual reports, Ministry of Road Transport and Highways highway development data, Bureau of Indian Standards tyre certification guidelines, IMARC Group automotive and component market databases, World Bank development finance data, and trade publications including Rubber News, Tyre Asia, and Indian Automotive News.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating vehicle production data, vehicle registration statistics, tyre replacement cycle assumptions, average tyre prices by category, and import-export flow analysis. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty and raw material price volatility.

India Tyre Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Two Wheelers, Three Wheelers, Passenger Cars, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles, Off the Road |

| OEM and Replacement Segments Covered | OEM Tyres, Replacement Tyres |

| Domestic Productions and Imports Covered | Domestic Production, Imports |

| Radial and Bias Tyres Covered | Bias Tyres, Radial Tyres |

| Tube and Tubeless Tyres | Tube Tyres, Tubeless Tyres |

| Tyres Size Covered | Small, Medium, Large |

| Price Segments Covered | Low, Medium, High |

| Regions Covered | North India, East India, West and Central India, South India |

| Companies Covered | MRF Tyres, Apollo Tyres Ltd, CEAT Limited, Bridgestone, JK Tyre & Industries Ltd., Continental, The Goodyear Tire & Rubber Company, The Yokohama Rubber Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Tyre Market Report

The India tyre market size was valued at USD 14.45 Billion in 2025, reflecting consistent demand from rising vehicle ownership, infrastructure expansion, and growing replacement tyre requirements across all vehicle categories.

The market is projected to reach USD 27.67 Billion by 2034, growing at a CAGR of 7.49% during 2026-2034, driven by EV adoption, India's expanding automobile production base, growing logistics and commercial vehicle fleet demand, and strengthening export competitiveness of domestic manufacturers.

Domestic production leads with a 70.0% market share in 2025, supported by government PLI incentives, anti-dumping duties on imports, BIS quality certification requirements, and a well-established domestic raw material and component supply ecosystem.

Medium tyres lead at 50.0% in 2025, representing the most widely used tyre size across passenger cars, compact SUVs, and light commercial vehicles that constitute the largest and fastest-growing vehicle categories operating across India's expanding urban and inter-city road network.

West and Central India currently dominates the India tyre market, accounting for a share of 33.0%. The region benefits from the concentration of major automobile manufacturing hubs in Maharashtra and Gujarat, extensive industrial corridors, strong commercial vehicle demand, and an accelerating EV manufacturing ecosystem.

Key drivers include supportive government manufacturing incentives under the PLI scheme, rapidly expanding road and highway infrastructure, rising vehicle production across passenger and commercial categories, accelerating EV adoption, growing replacement tyre demand from an aging installed vehicle base, and increasing export competitiveness of domestic manufacturers.

Leading companies include MRF Tyres, Apollo Tyres Ltd, CEAT Limited, Bridgestone, JK Tyre & Industries Ltd., Continental, The Goodyear Tire & Rubber Company, The Yokohama Rubber Co., Ltd., and others.

Key applications include passenger car mobility, two-wheeler and three-wheeler transport, light and heavy commercial vehicle freight, agricultural machinery operations, and off-road and construction equipment deployment across India's diverse vehicle fleet.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)