India Used Car Loan Market Size, Share, Trends and Forecast by Vehicle Type, Financier, Percentage of Amount Sanctioned, Tenure, and Region, 2026-2034

India Used Car Loan Market Size & Forecast 2026-2034

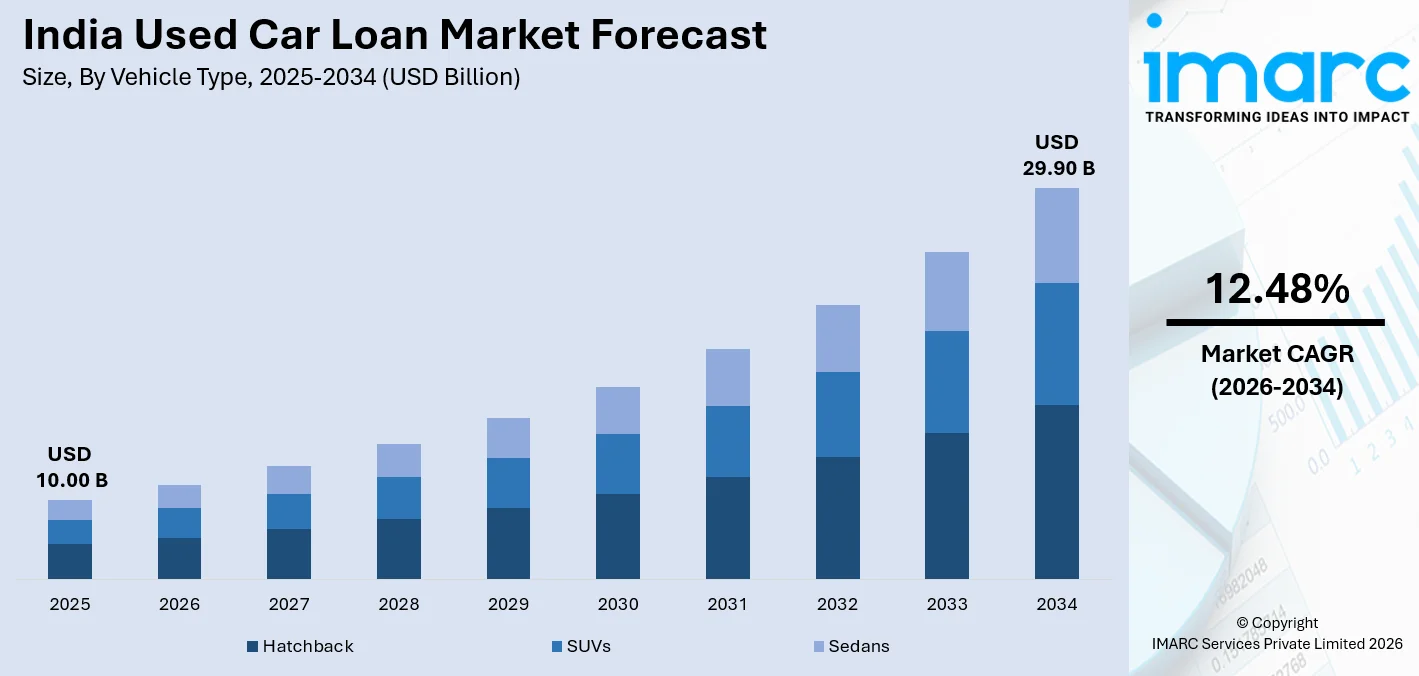

The India used car loan market size, which has reached at USD 10.00 Billion in 2025, is forecasted to reach USD 29.90 Billion by 2034, with the market growing at a CAGR of 12.48% between 2026-2034, driven by the widening affordability gap between new and used cars, the digitalization of used car loans, and the expansion of NBFCs into tier 2 and tier 3 cities. In December 2025, the RBI reduced the repo rate by 25 basis points to 5.25%, marking the fourth reduction in interest rates this year and expanding the pool of eligible auto loan borrowers to boost the India used car loan market share.

To get more information on this market Request Sample

India Used Car Loan Industry Analysis: Key Insights

- Hatchback commands 45.3% by vehicle type in 2025- affordability and practicality anchor the segment. Models like Maruti Swift and Hyundai i20 consistently lead loan volumes across tier-1 and tier-2 cities.

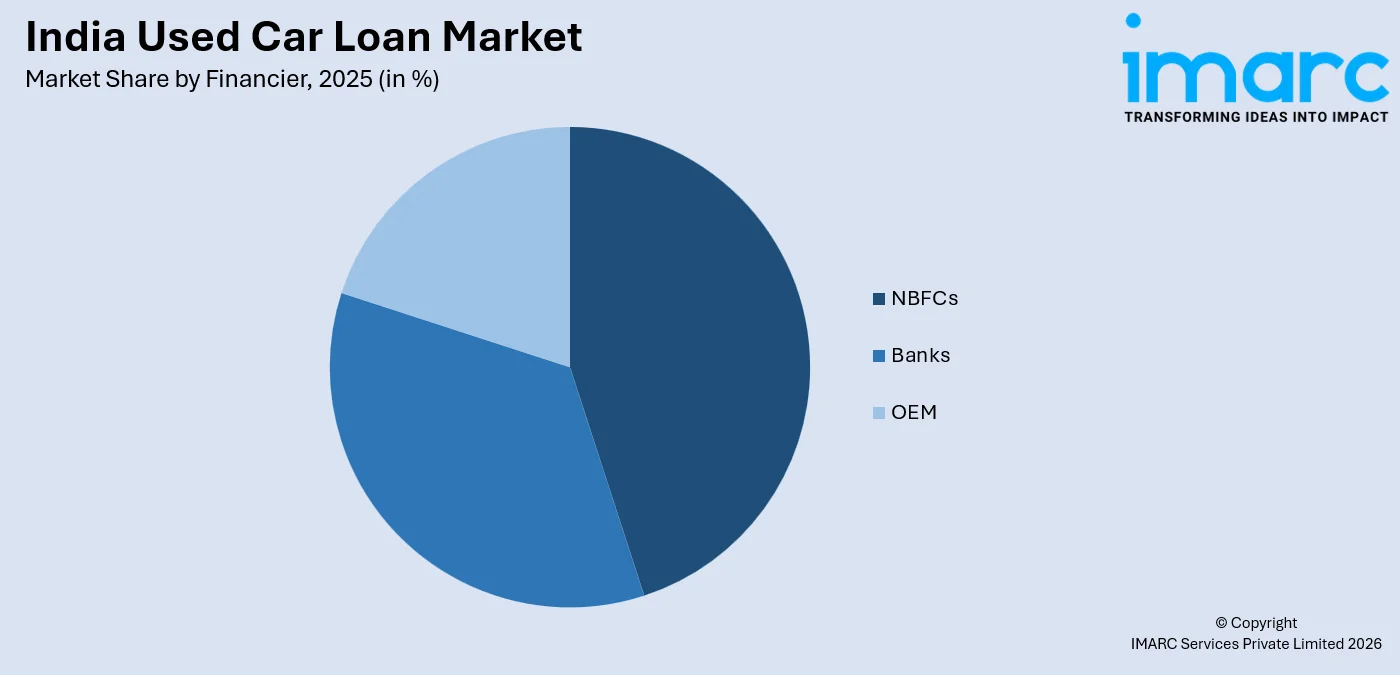

- NBFCs hold 42.7% of the financier share in 2025- the dominant single category, owing to flexible documentation, higher risk appetite, and deep penetration into rural and semi-urban markets where banks operate sparsely.

- The 51-75% leads percentage of amount sanctioned at 40.1% in 2025- conservative loan-to-value ratios dominate as lenders price in vehicle depreciation risk, keeping most borrowers anchored in the moderate-funding zone.

- 3-5 years dominates tenure at 51.9% in 2025- a clear majority. This midrange window balances EMI affordability against total interest outgo, making it the structural default for both salaried and self-employed borrowers.

- West India leads with 30.4% regional share in 2025- driven by Maharashtra and Gujarat's organized dealer ecosystems and dense urban populations, with a moderate lead, reflecting relatively balanced multi-regional demand.

India Used Car Loan Market Trends and Dynamic 2026

Market Trends

Digital platforms redefining speed and transparency in used car loan disbursement

The used car loan market in India is witnessing significant digitalization in its finance space. In February 2025, CARS24 Financial Services announced the launch of its digital valuation-free lending platform, LOANS24, which promises instant approvals at 10.99% per annum. The company has facilitated car loans worth more than ₹4,000 crore for 80,000+ customers and is thus a significant indicator of the changing India used car loan market trends.

Organized platforms and NBFC-fintech alliances accelerating funding penetration

The convergence of organized used car platforms with digital NBFCs is creating new credit pathways. In March 2025, Spinny raised $170 million at a $1.7–1.8 billion valuations to expand its NBFC arm and link vehicle inspection with financing. Such platform-finance integration improves collateral certainty and is redefining credit structures by extending structured lending beyond India's major metropolitan areas.

Rising new vehicle costs creating sustained structural demand for pre-owned financing

Increasing prices of new vehicles are leading more and more customers into the used vehicle segment. Market data collected by CARS24 has shown that the average sell price for new vehicles increased by 32% in 2024, whereas the average sell price for second-hand vehicles has increased by a much lower 24%.

- Account Aggregator & Digital KYC Integration: RBI's Account Aggregator framework and Digital Lending Directions 2025 are enabling faster credit assessment and transparent e-KYC processes, cutting loan approval cycles.

- EV Used Car Financing Emergence: Pre-owned electric vehicles are entering used car finance portfolios, with NBFCs and fintech platforms developing specialized LTV and depreciation models for EV collateral.

- Co-Lending Model Expansion: The RBI's co-lending framework allowing 80:20 bank-NBFC risk splits, driving disbursement velocity in tier-2 and tier-3 city borrower pools.

- Subscription & Flexible Ownership Models: Emerging subscription-based vehicle ownership models are creating new categories of short-tenure used car finance, attracting younger urban consumers.

Growth Drivers

Widening price gap between new and used vehicles amplifying demand

India's Bharat Stage VI compliance has elevated new vehicle costs, widening the affordability gap with the pre-owned segment. This creates structural demand for used car loans among cost-sensitive first-time buyers. Platforms like Maruti True Value, operating 1,200+ touchpoints nationally, facilitate access to quality pre-owned vehicles, reinforcing India used car loan market growth among aspiring car buyers across Indian cities.

NBFC expansion and co-lending models deepening financial inclusion

NBFCs dominate the Indian used car loan financing market with flexibility in documentation, higher risk-taking capacity, and faster loan disbursements. Mahindra Finance has achieved AUMs of INR 1,19,673.02 crore in March 2025, growing by 17% year-on-year, which is a reflection of the dominance achieved by the NBFCs in the Indian loan market. The RBI’s co-lending mechanism that facilitates the sharing of risk between banks and NBFCs at the 80:20.

- Rising Disposable Incomes: India's expanding middle class and increasing formal payroll adoption are enlarging the creditworthy borrower pool, enabling first-time vehicle purchases through structured loan products.

- Urbanization and Mobility Demand: Rapid urbanization is driving car ownership aspirations, particularly in tier-2 and tier-3 cities where public transport infrastructure remains limited and used cars represent affordable mobility.

- Digital Lending Infrastructure: Account Aggregator frameworks, e-KYC rails, and AI-based credit scoring are cutting loan turnaround times to under 24 hours, broadening formal credit access for thin-file borrowers.

- Favorable Macroeconomic Conditions: India's GDP expanding at 8.2% in Q2 of FY 2025-2026 is improving household incomes and employment levels, translating into greater capacity for consumer loan uptake and vehicle financing demand.

Market Restraints

Inconsistent Used Vehicle Valuation Practices: Lack of a standardized vehicle valuation system has resulted in significant uncertainty for lenders. Inconsistent regional demand patterns and vehicle condition inconsistencies make it challenging for lenders to assess loan-to-value risks, thereby increasing the risks of elevated collateral and recovery risks for lenders.

High Credit Risk of Informal Income Borrowers: Informal income borrowers of used car loans in tier-2 and tier-3 cities are a significant challenge for lenders, as a substantial percentage of these borrowers have limited income documentation and thus present a high credit risk for lenders, thereby increasing the risks of elevated non-performing assets and deterring lenders from entering this space.

Regulatory Complexity and Compliance Burden: India’s used car loan space is governed by a multi-layered regulatory framework, including the Reserve Bank of India’s digital lending guidelines, state-specific vehicle registrations, and data protection regulations. This has resulted in a significant regulatory burden for smaller NBFCs and has the potential to deter lenders from entering the space.

India Used Car Loan Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Vehicle Type |

Hatchback |

45.3% |

2025 |

|

Financier |

NBFCs |

42.7% |

2025 |

|

Percentage of Amount Sanctioned |

51-75% |

40.1% |

2025 |

|

Tenure |

3-5 Years |

51.9% |

2025 |

|

Region |

West India |

30.4% |

2025 |

Vehicle Type Insights

Hatchback- 45.3% Market Share (2025) | Leading Vehicle Type

Hatchbacks are at the top of the used car loan market in India due to their affordability, compact size, and low maintenance costs. Maruti Suzuki’s True Value program, which facilitates used car financing in India, achieved 60 lakhs in cumulative used car sales in August 2025, with Swift, Baleno, and WagonR leading the pack of financed used cars in India.

|

Segment Breakdown Hatchback (45.3%) · SUVs · Sedans |

Financier Insights

Access the Comprehensive Market Breakdown Request Sample

NBFCs- 42.7% Market Share (2025) | Leading Financier

NBFCs lead India's used car loan financier space through flexible documentation, higher risk appetite, and faster disbursements. NBFC’s AUM is rapidly expanding, reflecting scale built through used vehicle origination and deep rural penetration. Their capacity to finance borrowers with informal credit histories gives NBFCs a structural competitive advantage over traditional banking institutions in this segment.

|

Segment Breakdown NBFCs (42.7%) · Banks · OEM |

Percentage of Amount Sanctioned Insights

51-75%- 40.1% Market Share (2025) | Leading Percentage of Amount Sanctioned

The 51–75% LTV bracket leads India's used car loan sanctioning as lenders apply conservative collateral management for pre-owned assets. HDFC Bank securitized INR 9000 crore in auto loans to free capital for fresh disbursals, illustrating how moderate LTV portfolios attract investor confidence. Better recovery outcomes and reduced repossession risk entrench this as the structural default in the India used car loan market forecast.

|

Segment Breakdown 51-75% (40.1%) · Up to 25% · 25-50% · Above 75% |

Tenure Insights

3-5 Years- 51.9% Market Share (2025) | Leading Tenure

The tenure of 3-5 years is the dominant tenure in the used car loan market in India, as it strikes an optimal balance between EMI and total interest incurred. For those who are employed and self-employed, repaying the loan is in line with the growth of income for the borrower. Bank of Maharashtra lowered its car loan rates from 7.70% to 7.45%. This has eased the burden of EMI repayments for those in mid-tenure loan products.

|

Segment Breakdown 3-5 Years (51.9%) · Less Than 3 Years · More Than 5 Years |

Regional Insights

West India-30.4% Market Share (2025) | Leading Region

West India's regional lead is anchored by Maharashtra and Gujarat's large urban consumer bases, organized dealership networks, and strong formal employment ecosystems. CARS24 Financial Services, operating across the nation, identifies Maharashtra and Gujarat among its highest loan disbursement states, with Mumbai, Pune, and Ahmedabad driving used car financing volumes through platform-led and NBFC-supported lending channels.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 30.4% |

| Major States | Maharashtra, Gujarat, Rajasthan, Goa |

| Key Growth Drivers | Strong urban consumer base, organized dealer networks, high vehicle ownership rates |

| Outlook | Steady regional leader with growing digital lending expansion |

|

Regional Breakdown West India (30.4%) · North India · South India · East India |

North India:

North India is a key demand hub for used car loans, driven by Delhi-NCR's expansive consumer base of first-time buyers and upgraders. Mahindra Finance and HDFC Bank lead regional lending with flexible EMI schemes for popular hatchback and sedan models. CarTrade Tech's Q3 FY25 net profit of INR 42.69 crore reflects the commercial viability of digital used car platforms serving this high-volume market.

|

Metric

|

Details

|

|---|---|

| Major States | Delhi, Uttar Pradesh, Punjab, Haryana |

| Key Growth Drivers | Large urban population, NBFC-bank co-lending, technology-enabled credit processing |

| Outlook | Growing digital adoption driving loan volume expansion |

South India:

South India is a fast-growing hub for digitally-enabled used car loan origination. Bengaluru led online used car transactions, and platforms such as Cars24, Spinny, and CarDekho report that more than half of buyers in Hyderabad and Bengaluru now prefer online discovery and financing, reflecting the region's technology-first consumer behavior and creating fertile ground for digital NBFC lending expansion.

|

Metric

|

Details

|

|---|---|

| Major States | Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala |

| Key Growth Drivers | Digital platform adoption, two-wheeler upgrade demand, tier-3 city expansion |

| Outlook | Digital-first lending model growing rapidly across the region |

East India:

East India represents an emerging frontier for used car loan growth, driven by urbanization in Kolkata and tier-2 cities like Bhubaneswar and Patna. Many companies operate in the region nationally through a twin-hub model combining centralized credit analytics with district-level origination, enabling credit access in East India's previously underserved semi-urban and rural geographies.

|

Metric

|

Details

|

|---|---|

| Major States | West Bengal, Odisha, Bihar, Jharkhand, Assam |

| Key Growth Drivers | Digital finance penetration, urbanization, NBFC branch expansion |

| Outlook | High growth potential in under-banked areas |

Market Outlook (2026-2034)

What is the future outlook of the India used car loan market?

The India used car loan market is expected to sustain steady revenue growth through 2034.

Robust structural demand from widening price differentials between new and pre-owned vehicles, progressive monetary easing, and digital lending innovation will sustain the market's expansion. NBFCs and fintech platforms are expected to deepen tier-2 and tier-3 penetration, while organized platforms' IPO momentum and AI-led valuation investments will improve borrower trust and credit efficiency through 2034.

India Used Car Loan Market- Leading Key Players

The used car loan market in India is marked by the presence of public sector banks, private sector banks, and NBFCs, who compete on pricing, speed, and technology, thereby contributing to the formalization of the market in the country, catering to the diverse consumer segments in urban, semi-urban, and rural areas.

| Company | Leading Brands/Products | Highlights |

|---|---|---|

|

State Bank of India |

SBI Used Car Loan, SBI Smart Car Loan |

India's largest public sector lender; extensive branch network across all states and union territories; competitive used car loan rates with flexible eligibility criteria for salaried and self-employed borrowers. |

|

HDFC Bank Limited |

HDFC Used Car Loan |

Securitized INR 9000 crore in auto loans to free capital for fresh disbursals; digital and paperless approvals for pre-approved customers; strong presence in metro and tier-2 cities. |

|

ICICI Bank Limited |

ICICI Used Car Loan |

Used car loan interest rate of 11% p.a.; instant digital approvals and repo-linked floating rates; strong metro-focused used car loan portfolio with rapid turnaround times. |

Major players in the market include Mahindra & Mahindra Financial Services Limited, Shriram Finance Limited, Cholamandalam Investment and Finance Company Limited, Tata Capital Financial Services Limited, CARS24 Financial Services Private Limited, Poonawalla Fincorp Limited, Bajaj Finserv Limited, etc.

Latest Development & News

- In December 2025, the Reserve Bank of India reduced the repo rate by 25 basis points to 5.25%. This decision was taken in the final MPC meeting of the year and is the fourth such move in 2025. This decision would directly result in the reduction in the auto loan borrowers’ cost as well as the affordability of used car loan borrowers on floating rates.

- In April 2025, CARS24 acquired Team-BHP, a popular auto enthusiast community platform in India, and leveraged the user base and auto expertise offered through this acquisition. This acquisition is expected to improve the car-buying experience through community-driven insights and will allow the financial services arm of CARS24, known as LOANS24, to gain from the organic user base for its used car loan product offerings.

- In February 2025, CARS24 Financial Services officially launched LOANS24, extending its digital credit platform to buyers outside the CARS24 marketplace. The platform offers up to 100% on-road price financing with repayment terms of up to six years, with tier-2 cities growing their share of total disbursements to 26%, reflecting the rapid geographic expansion of digital used car financing beyond India's major metros.

India Used Car Loan Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Hatchback, SUVs, Sedan |

| Financiers Covered | Banks, NBFCs, OEM |

| Percentage of Amount Sanctioneds Covered | Up to 25%, 25-50%, 51-75%, Above 75% |

| Tenures Covered | Less than 3 Years, 3-5 Years, More than 5 Years |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India used car loan market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India used car loan market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India used car loan industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Used Car Loan Market Report

The India used car loan market was valued at USD 10.00 Billion in 2025.

The India used car loan market is anticipated to reach a value of USD 29.90 Billion by 2034.

Hatchback dominates the market with a share of 45.3%, driven by its unmatched affordability, widespread availability of popular models, low maintenance costs, and strong resale value which collectively make it the default vehicle type financed across India's organized and platform-based used car loan channels.

NBFCs command the market with a share of 42.7%, owing to their flexible loan terms, minimal documentation requirements, and proven ability to serve borrowers with informal income sources in tier-2 and tier-3 cities where traditional bank presence is limited.

Some of the major players in the India used car loan market include State Bank of India, HDFC Bank, ICICI Bank, Mahindra Finance, Shriram Finance, Cholamandalam Investment and Finance, Tata Capital Financial Services, CARS24 Financial Services, Poonawalla Fincorp, and Bajaj Finserv Limited, etc.

Key trends include the rapid adoption of AI-powered credit scoring enabling sub-24-hour loan approvals, the rise of peer-to-peer fintech platforms integrating vehicle inspection with financing, increasing participation of women borrowers in digital lending channels, and the emergence of pre-owned EV financing as a new product category being developed by NBFCs and specialized lenders.

West India currently leads the India used car loan market, accounting for a share of 30.4%. Maharashtra and Gujarat's concentrated urban populations, well-established dealership ecosystems, and high vehicle ownership rates drive the region's position, with Mumbai, Pune, and Ahmedabad serving as primary loan origination centers.

Key growth drivers include India's favourable demographic profile with a young, aspirational population entering peak earning years, the expansion of formal payroll systems bringing new borrowers into the credit system, government investments in road and highway infrastructure increasing vehicle utility, and the growing availability of curated used car inventory through certified OEM programs and organized dealer chains.

Key challenges include fragmented and inconsistent vehicle valuation practices across geographies creating LTV uncertainty, the dominance of unorganized dealers in rural markets operating outside formal documentation frameworks, elevated NPA rates among NBFCs that over-extended into thin-file borrower segments, and the lack of a centralized vehicle history database complicating collateral assessment and increasing repossession risk for lenders.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)