India Ventral Hernia Mesh Devices Market Size, Share, Trends and Forecast by Mesh Type, Indication, Procedure, End Use, and Region, 2026-2034

India Ventral Hernia Mesh Devices Market Size, Share, Trends & Forecast (2026-2034)

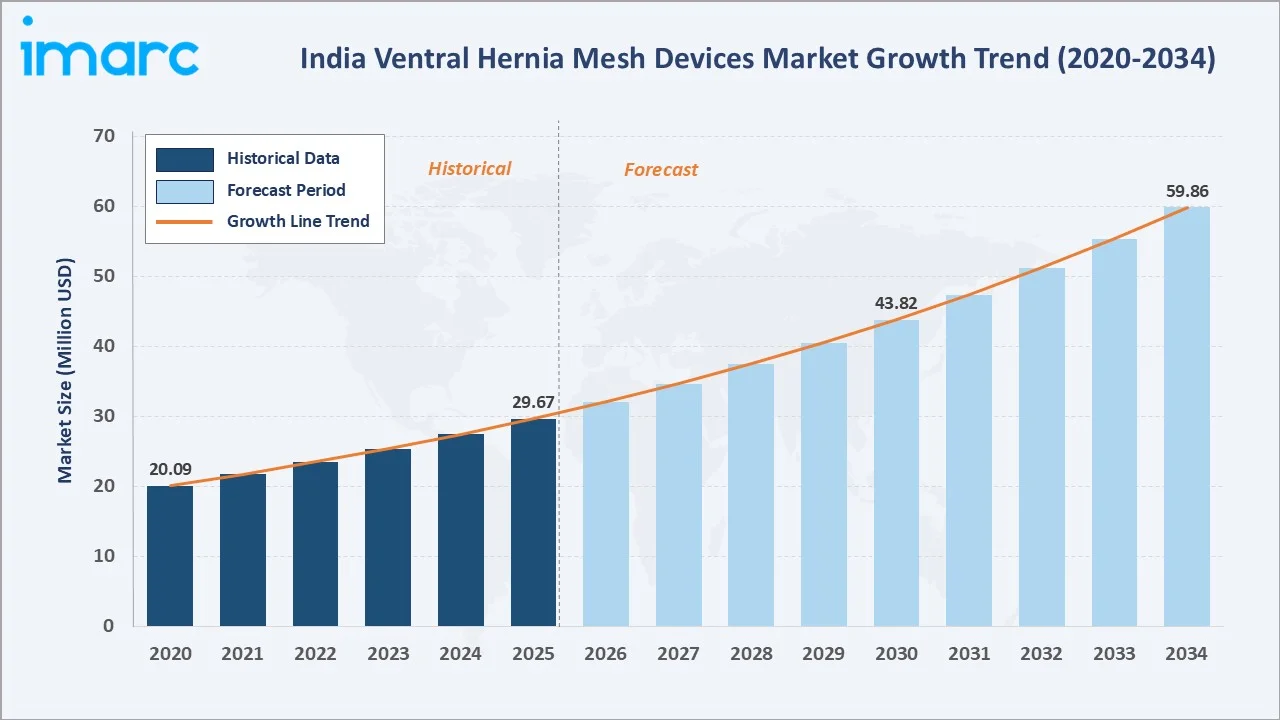

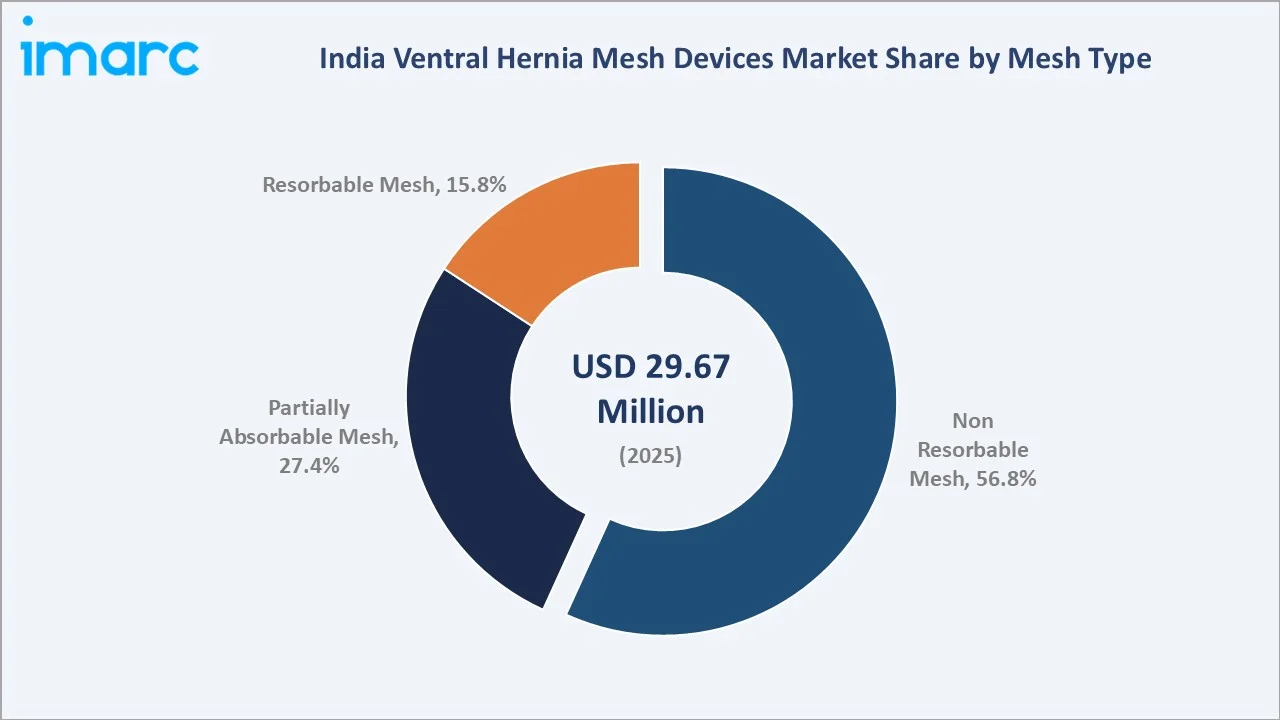

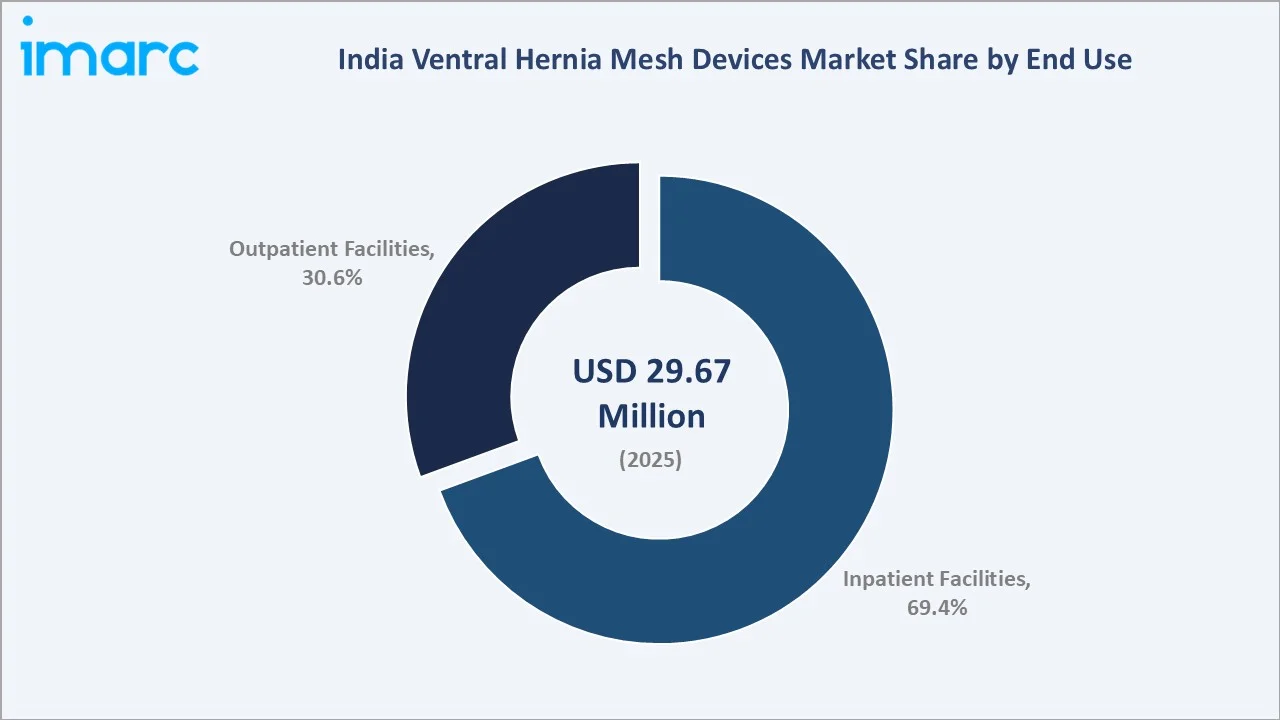

The India ventral hernia mesh devices market was valued at USD 29.67 Million in 2025 and is projected to reach USD 59.86 Million by 2034, exhibiting a CAGR of 8.11% during 2026-2034. Rising hernia surgery volumes, wider adoption of laparoscopic and robotic repair, expanding healthcare access, and a strengthening domestic manufacturing base are the primary drivers shaping the market growth.

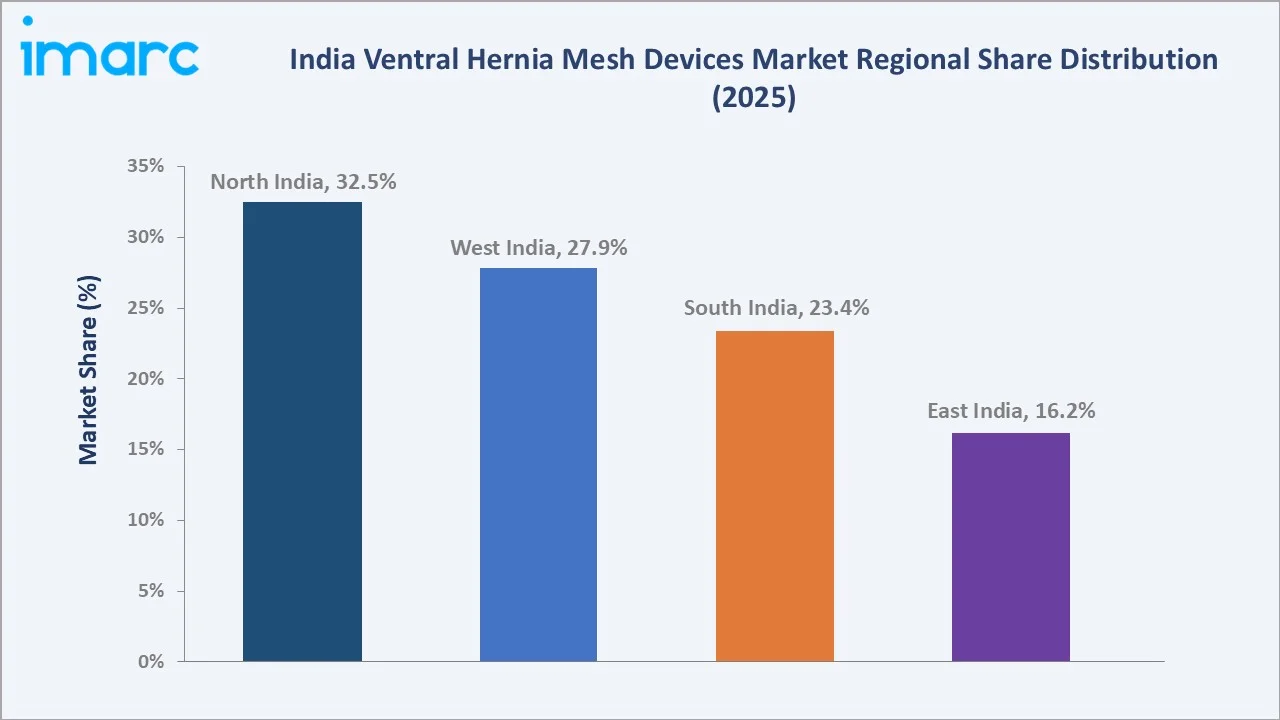

Non resorbable mesh leads the mesh type segment at 56.8%, inpatient facilities dominate the end use segment at 69.4%, and North India commands 32.5% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 29.67 Million |

|

Forecast Market Size (2034) |

USD 59.86 Million |

|

CAGR (2026-2034) |

8.11% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (32.5%, 2025) |

|

Second Largest Region |

West India (27.9%, 2025) |

|

Leading Mesh Type |

Non Resorbable Mesh (56.8%, 2025) |

|

Leading End Use |

Inpatient Facilities (69.4%, 2025) |

The India ventral hernia mesh devices market expanded from USD 20.09 Million in 2020 to USD 29.67 Million in 2025, supported by rising abdominal surgery volumes, wider mesh adoption, and improving access to specialist surgical care. Anchored at USD 43.82 Million in 2030, the forecast to USD 59.86 Million by 2034 is driven by growing laparoscopic and robotic repair, lightweight mesh uptake, and expanding day-care surgery.

To get more information on this market, Request Sample

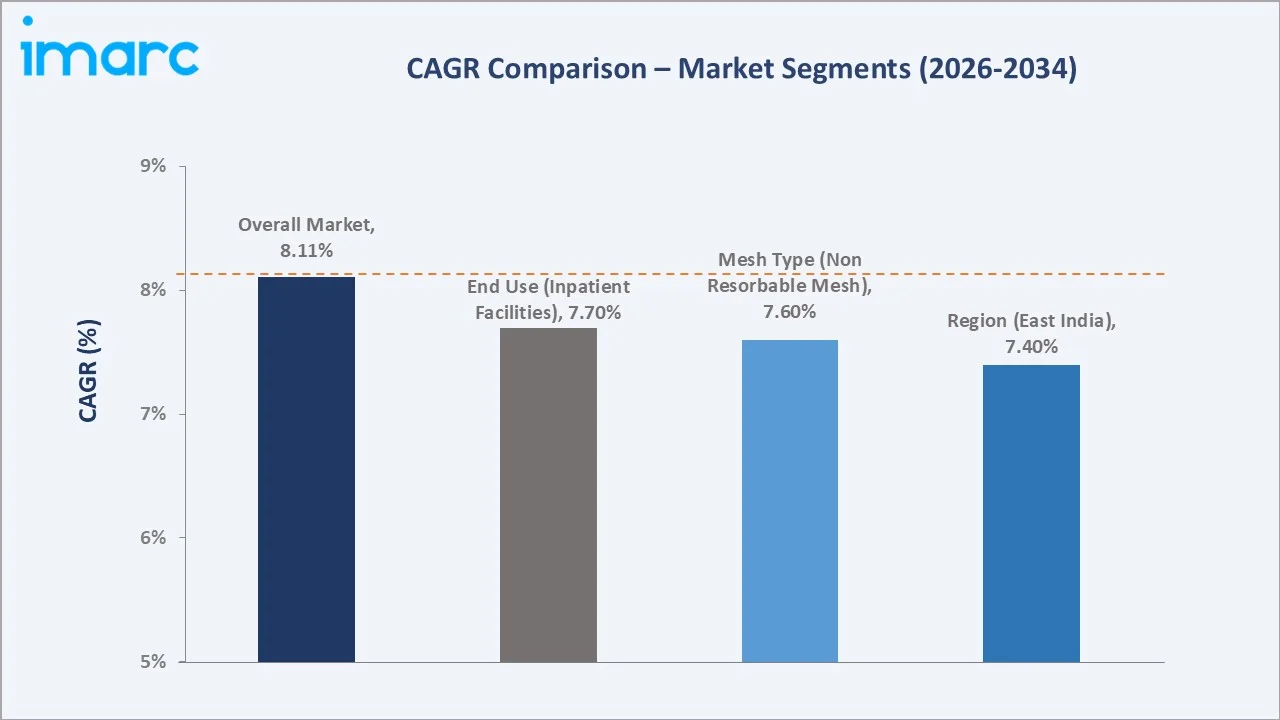

CAGR trajectories across mesh type and end use sub-segments show resorbable mesh and outpatient facilities expanding faster than the overall 8.11% market CAGR, driven by minimally invasive techniques, day-care procedures, and rising adoption of absorbable materials across surgical centres.

Executive Summary

The India ventral hernia mesh devices market is on a steady growth path from USD 20.09 Million in 2020 to USD 59.86 Million by 2034. Demand is shifting from basic open repair toward mesh-reinforced, minimally invasive procedures across primary ventral and incisional hernias. Rising obesity, an aging population, and growing surgical volumes are widening the addressable patient base. As per PIB, India's senior citizen population is projected to surge to around 230 Million by 2036, making up about 15% of the total population.

Non resorbable mesh dominates the mesh type segment at 56.8% in 2025, supported by durability, low cost, and strong tissue ingrowth. Inpatient facilities lead the end use segment at 69.4%, reflecting complex repairs that require overnight care. North India holds 32.5% of regional share, led by high surgical infrastructure density and large patient pools.

Key Market Insights

|

Insight |

Data |

|

Leading Mesh Type |

Non Resorbable Mesh - 56.8% share (2025) |

|

Second Largest Mesh Type |

Partially Absorbable Mesh - 27.4% share (2025) |

|

Leading End Use |

Inpatient Facilities - 69.4% share (2025) |

|

Second Largest End Use |

Outpatient Facilities - 30.6% share (2025) |

|

Leading Region |

North India - 32.5% share (2025) |

|

Second Largest Region |

West India - 27.9% share (2025) |

|

Top Companies |

Medtronic, Johnson & Johnson, BD, W. L. Gore & Associates, Inc. |

Key Analytical Observations Expanding On The Data Above:

- Non resorbable mesh dominance at 56.8% is supported by polypropylene durability, low recurrence in clean repairs, affordability, and long clinical familiarity among Indian surgeons.

- Partially absorbable mesh at 27.4% is gaining ground through reduced long-term foreign-body load, improved comfort, and suitability for laparoscopic intraperitoneal placement.

- Inpatient facilities at 69.4% reflect the prevalence of large, complex, and incisional hernias that need inpatient anaesthesia, monitoring, and overnight recovery.

- Outpatient facilities at 30.6% are expanding as day-care and ambulatory hernia repair grows, supported by smaller defects, lightweight mesh, and faster recovery protocols.

- North India at 32.5% leads regional demand, anchored by dense hospital networks, high surgical throughput, and strong representation of leading surgical centres.

India Ventral Hernia Mesh Devices Market Overview

Ventral hernia mesh devices are surgical implants used to reinforce the abdominal wall during repair of primary ventral, umbilical, and incisional hernias. They are placed through open, laparoscopic, or robotic techniques to reduce recurrence and support tissue healing.

The market spans non resorbable, partially absorbable, and resorbable mesh, delivered across inpatient and outpatient settings. The Indian ecosystem links polymer and biologic suppliers, mesh manufacturers, regulators such as CDSCO, distributors, hospitals, surgeons, and payers, together enabling safe and effective hernia repair across the country.

Market Dynamics

To evaluate market opportunities, Request Sample

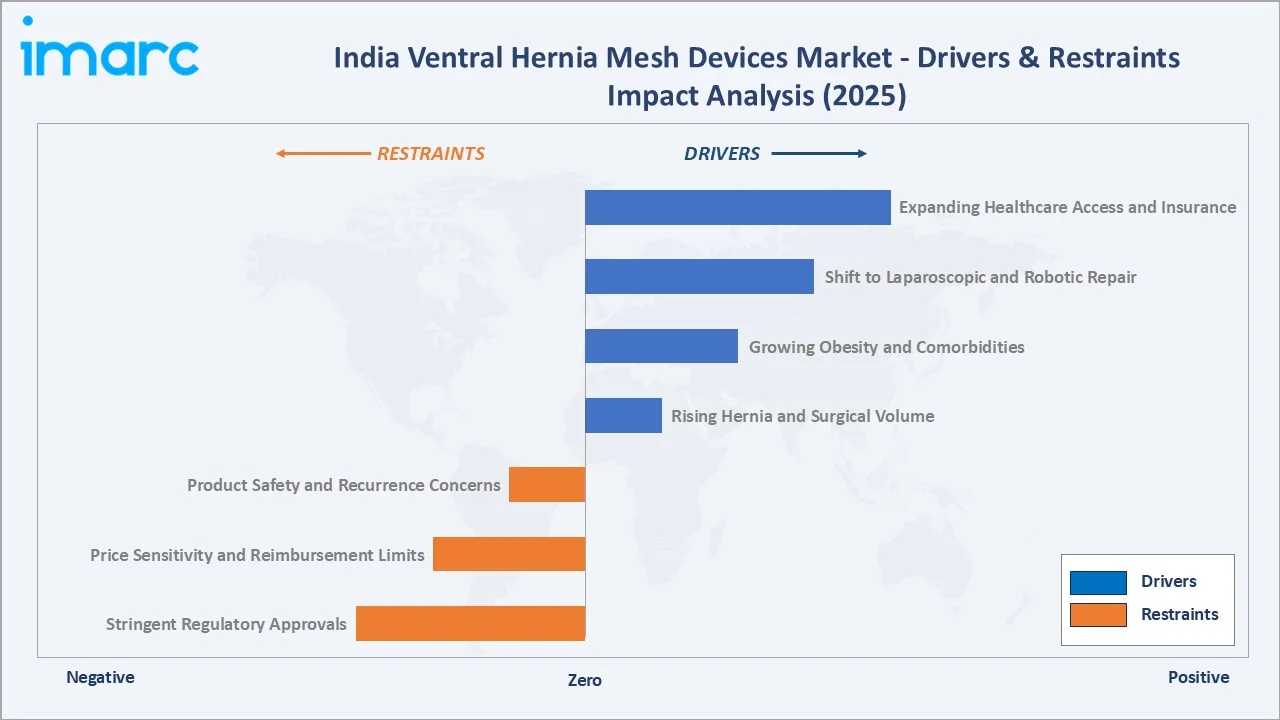

Market Drivers

- Rising Hernia and Surgical Volume: Growing numbers of abdominal and gastrointestinal surgeries are increasing primary ventral and incisional hernia cases, lifting demand for mesh-based reinforcement across hospitals.

- Growing Obesity and Comorbidities: Higher body weight raises intra-abdominal pressure and hernia risk, expanding the eligible patient pool. The rising prevalence of obesity-related conditions such as diabetes and metabolic disorders is increasing the demand for hernia repair procedures and associated treatment solutions.

- Shift to Laparoscopic and Robotic Repair: Wider adoption of minimally invasive techniques is increasing the use of composite and coated mesh designed for intraperitoneal placement and faster recovery. As per IMARC Group, the India minimally invasive surgery market size reached USD 847.7 Million in 2025.

- Expanding Healthcare Access and Insurance: Growing hospital infrastructure, government schemes, and private insurance are improving affordability and access to elective hernia repair across urban and semi-urban India.

Market Restraints

- Product Safety and Recurrence Concerns: Complications such as chronic pain, adhesion, and recurrence weigh on adoption. These safety concerns can reduce patient confidence and influence clinical decision-making, limiting the uptake of certain hernia repair products.

- Price Sensitivity and Reimbursement Limits: High out-of-pocket spending and capped reimbursement push procurement toward lower-cost mesh, constraining uptake of premium composite and biologic products.

- Stringent Regulatory Approvals: Tighter device registration, quality, and import requirements under CDSCO lengthen launch timelines and raise compliance costs for manufacturers.

Market Opportunities

- Domestic Manufacturing and Cost-Competitive Mesh: Indian producers can expand share by offering affordable, quality polypropylene and composite mesh tailored to local pricing and procurement.

- Lightweight and Composite Mesh Innovation: Demand is rising for lightweight, large-pore, and tissue-separating mesh that lowers foreign-body load and supports laparoscopic and robotic repair.

Market Challenges

- Limited Specialist Access in Rural Areas: Uneven distribution of trained hernia surgeons and advanced operating facilities restricts mesh adoption beyond metropolitan and tier-1 centres.

- Fragmented Distribution and Price Competition: A crowded field of importers and local suppliers intensifies price competition, pressuring margins and complicating consistent product availability.

Emerging Market Trends

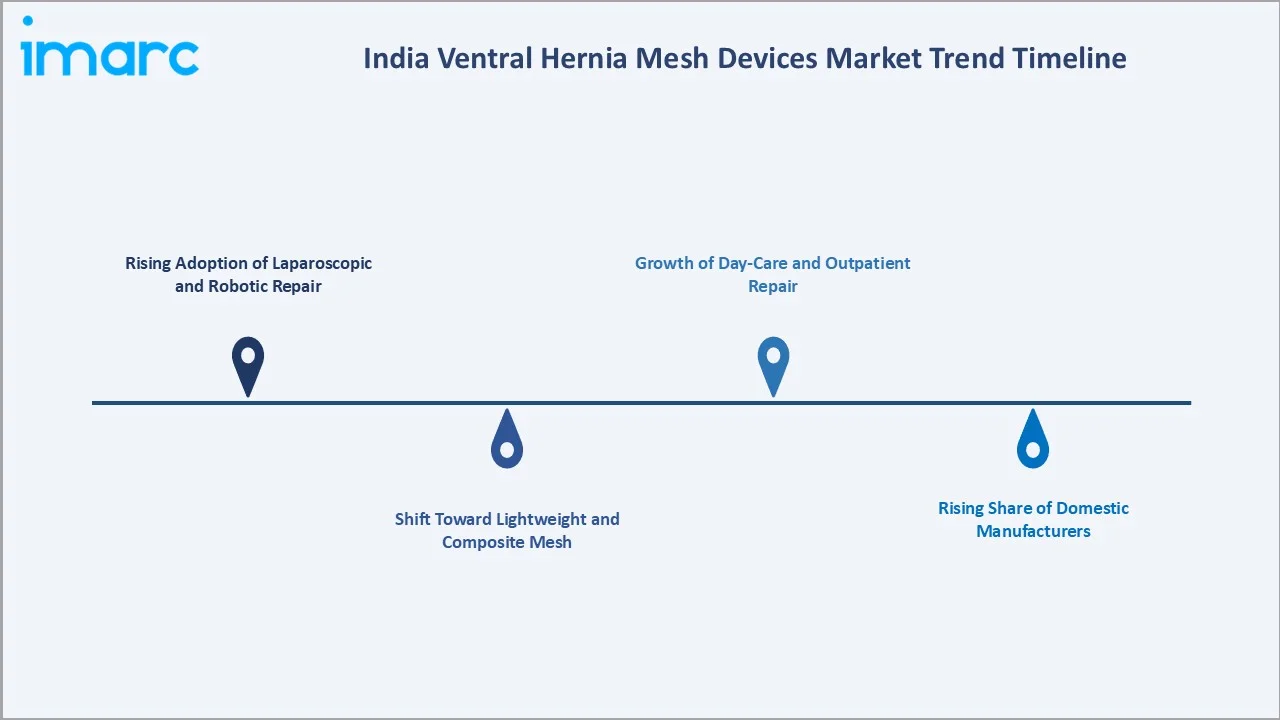

1. Rising Adoption of Laparoscopic and Robotic Repair

Minimally invasive ventral hernia repair is expanding rapidly across Indian tertiary hospitals. The growing preference for procedures that offer smaller incisions, reduced postoperative pain, and faster recovery is supporting the adoption of laparoscopic and robotic techniques.

2. Shift Toward Lightweight and Composite Mesh

Surgeons are moving from heavyweight polypropylene toward lightweight, large-pore, and tissue-separating mesh. These designs reduce chronic pain and stiffness while supporting better integration, especially in laparoscopic and robotic ventral hernia repair.

3. Growth of Day-Care and Outpatient Repair

Smaller primary ventral and umbilical hernias are increasingly managed as day-care procedures. Faster recovery, lower cost, and improved anaesthesia protocols are expanding the outpatient share of mesh-based repair across surgical centres.

4. Rising Share of Domestic Manufacturers

Indian device makers are scaling competitively priced mesh portfolios for ventral and incisional repair. Local production is improving availability, shortening supply chains, and supporting cost-sensitive procurement across public and private hospitals.

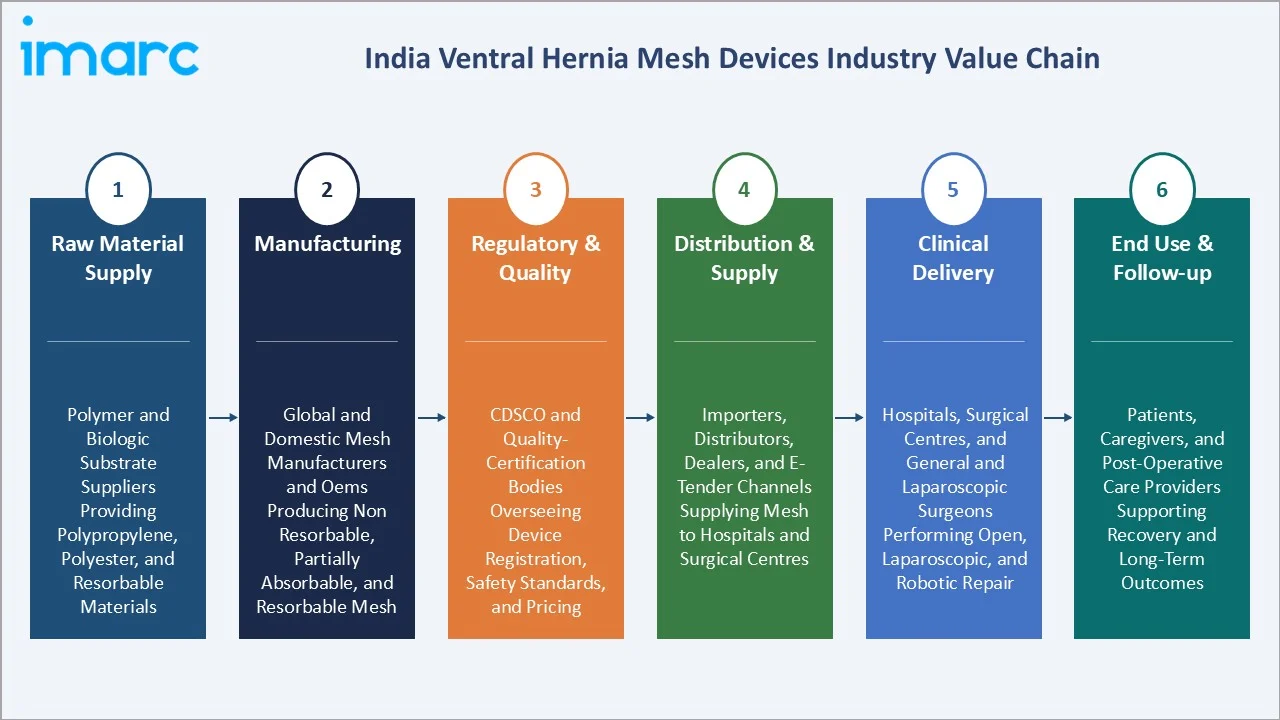

Industry Value Chain Analysis

The India ventral hernia mesh devices value chain spans six stages, from raw material supply through clinical delivery and patient follow-up. Manufacturing, regulatory quality, and clinical delivery capture the highest value, while consistent supply and surgeon training increasingly shape competitive position.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Polymer and biologic substrate suppliers providing polypropylene, polyester, and resorbable materials for mesh production |

|

Manufacturing |

Global and domestic mesh manufacturers and device OEMs producing non resorbable, partially absorbable, and resorbable mesh |

|

Regulatory & Quality |

CDSCO and quality-certification bodies overseeing device registration, safety standards, and pricing |

|

Distribution & Supply |

Importers, distributors, dealers, and e-tender channels supplying mesh to hospitals and surgical centres |

|

Clinical Delivery |

Hospitals, surgical centres, and general and laparoscopic surgeons performing open, laparoscopic, and robotic repair |

|

End Use & Follow-up |

Patients, caregivers, and post-operative care providers supporting recovery and long-term outcomes |

Vertically integrated players that own manufacturing, regulatory capability, and strong hospital relationships are positioned to capture greater value than those reliant on imports alone.

Technology Landscape in the India Ventral Hernia Mesh Devices Industry

Lightweight and Composite Mesh Materials

Manufacturers are advancing lightweight, large-pore polypropylene and composite mesh that balance strength with flexibility. These materials reduce stiffness and chronic pain while supporting durable tissue ingrowth in ventral and incisional repair.

Coatings and Tissue-Separating Designs

Coated and dual-layer mesh combine a macroporous repair surface with an absorbable anti-adhesive barrier. This design limits visceral attachment during intraperitoneal placement, improving safety in laparoscopic and robotic ventral hernia repair.

Laparoscopic and Robotic Platforms

Minimally invasive platforms are reshaping mesh selection and fixation. Robotic systems enable precise suturing and defect closure, increasing demand for composite mesh, self-fixating designs, and absorbable tack and glue fixation across centres.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Mesh Type |

Non Resorbable Mesh |

56.8% |

2025 |

|

Indication |

🔒 |

🔒 |

2025 |

|

Procedure |

🔒 |

🔒 |

2025 |

|

End Use |

Inpatient Facilities |

69.4% |

2025 |

|

Region |

North India |

32.5% |

2025 |

By Mesh Type

Non resorbable mesh commands a 56.8% majority share in 2025, driven by polypropylene durability, low recurrence in clean repairs, affordability, and broad surgeon familiarity. The segment remains the default choice across open and laparoscopic ventral hernia repair.

To access detailed market analysis, Request Sample

Partially absorbable mesh at 27.4% is gaining share through lower long-term foreign-body load and better comfort. Its ability to provide initial mechanical support while reducing the amount of permanent implanted material is driving greater acceptance among surgeons and patients.

By End Use

Inpatient facilities dominate with 69.4% share in 2025, reflecting complex, large, and incisional hernia repairs that require inpatient anaesthesia, monitoring, and overnight recovery. Tertiary hospitals remain the primary setting for advanced mesh procedures.

Outpatient facilities at 30.6% are expanding as day-care and ambulatory hernia repair grows. Smaller defects, lightweight mesh, and faster recovery protocols are shifting suitable cases toward cost-efficient outpatient settings.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

32.5% |

Dense hospital networks, high surgical volumes, strong specialist presence, and a large urban patient base |

|

West India |

27.9% |

Mature private healthcare, strong medical infrastructure, high insurance penetration, and growing day-care surgery |

|

South India |

23.4% |

Advanced tertiary care, rising medical tourism, expanding surgical capacity, and high clinical adoption |

|

East India |

16.2% |

Improving healthcare access, expanding hospital infrastructure, rising awareness, and growing tier-2 city demand |

North India at 32.5% in 2025 leads the regional landscape, anchored by dense hospital networks, high surgical throughput, and a large base of specialist surgical centres.

West India at 27.9% holds a significant share of the regional market, supported by advanced healthcare infrastructure, a strong presence of multispecialty hospitals, and increasing adoption of minimally invasive hernia repair procedures.

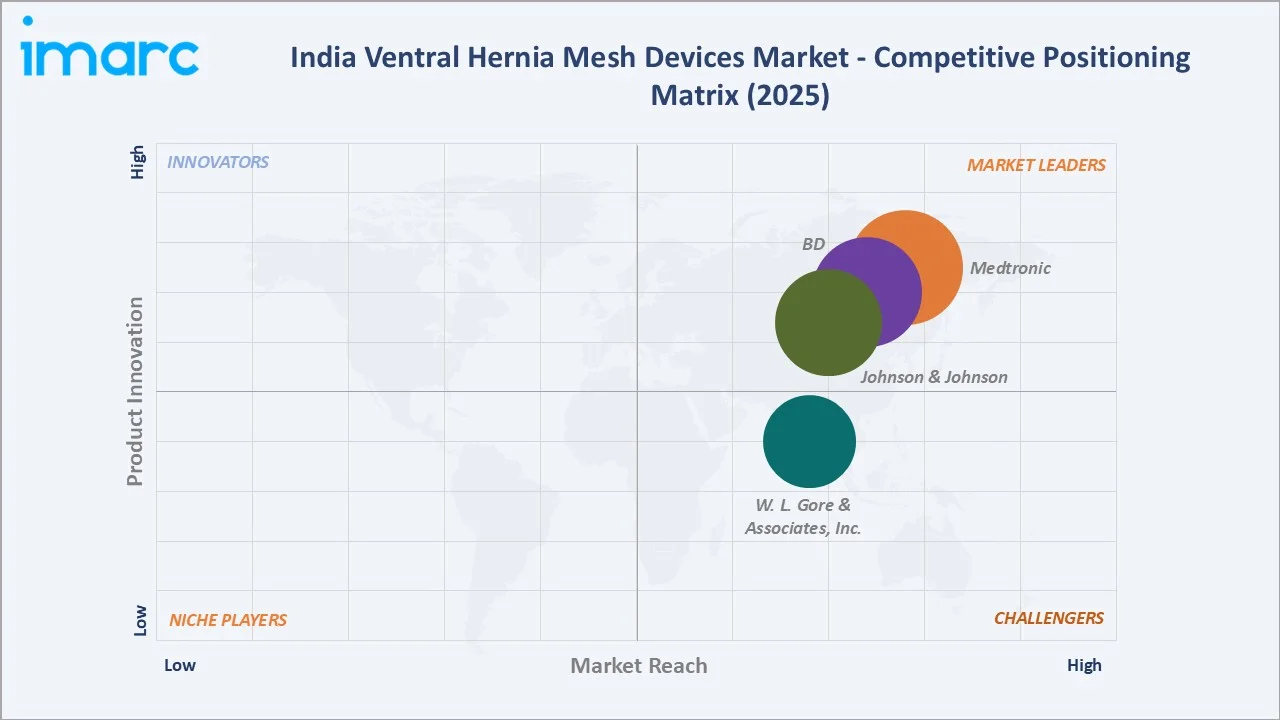

Competitive Landscape

The India ventral hernia mesh devices market is moderately consolidated, with global leaders holding strong positions in premium mesh, while domestic players compete on affordability and availability. Product breadth, clinical evidence, pricing, and surgeon relationships form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Medtronic |

Parietex, Symbotex Mesh |

Leader |

Broad mesh portfolio and minimally invasive surgery focus |

|

Johnson & Johnson |

Prolene |

Leader |

Wound closure leadership and surgical innovation focus |

|

BD |

Ventralight ST, Bard Mesh |

Leader |

Comprehensive hernia mesh range and clinical support focus |

|

W. L. Gore & Associates, Inc. |

GORE® SYNECOR Biomaterial |

Challenger |

Specialty material innovation and premium mesh focus |

Key players include Medtronic, Johnson & Johnson, BD, and W. L. Gore & Associates, Inc., among others.

Key Company Profiles

Medtronic

Medtronic is a global medical technology company headquartered in Dublin, Ireland, and one of the largest medical device manufacturers in the world. The company operates across four business segments spanning cardiovascular, neuroscience, medical surgical, and diabetes portfolios, serving healthcare systems in several countries.

- Product Portfolio: Parietex and Symbotex composite hernia mesh products spanning synthetic flat mesh, anatomical designs, composite anti-adhesion barrier meshes, and hydrophilic variants for open, laparoscopic, and robotic hernia repair procedures across inguinal, ventral, and hiatal indications.

- Recent Developments: Medtronic’s Hugo™ robotic-assisted surgery system completed the Enable Hernia Repair study in fiscal year 2025, meeting both safety and effectiveness endpoints, advancing robotic-assisted hernia repair as a key growth vector for the company’s surgical innovations portfolio.

- Strategic Focus: Expanding minimally invasive and robotic-assisted hernia repair platforms, growing the Parietex and Symbotex mesh portfolio across international markets, and integrating mesh solutions with the Hugo robotic surgery ecosystem to strengthen clinical differentiation.

Johnson & Johnson

Johnson & Johnson is a diversified global healthcare company headquartered in New Brunswick, New Jersey. The company maintains a strong presence in surgical technologies and medical devices, with a broad portfolio supporting advanced wound closure, tissue repair, and minimally invasive surgical procedures.

- Product Portfolio: Prolene polypropylene mesh for abdominal wall hernia and fascial defect repair, available in standard and soft variants.

- Recent Developments: Johnson & Johnson has continued to strengthen its surgical technologies business through ongoing investments in product innovation, robotic-assisted surgery capabilities, and clinical education initiatives. The company is also expanding collaborations and training programs to support the adoption of advanced hernia repair and wound closure solutions across global healthcare markets.

- Strategic Focus: Strengthening wound closure and hernia repair leadership, advancing surgical innovation through robotic-assisted procedures, and growing mesh product adoption through clinical education and surgeon training programs across global markets.

BD

BD is a global medical technology company headquartered in Franklin Lakes, New Jersey, and listed on the New York Stock Exchange. The company operates across multiple healthcare segments, offering a broad portfolio of medical devices, diagnostic solutions, and interventional technologies for hospitals and healthcare providers worldwide.

- Product Portfolio: Ventralight ST composite mesh for laparoscopic ventral hernia repair and the Bard hernia mesh family, covering a comprehensive range of synthetic, composite, and bioabsorbable hernia repair solutions for inguinal, ventral, and incisional indications.

- Recent Developments: BD received FDA 510(k) clearance and launched the Phasix ST Umbilical Hernia Patch, the first bioabsorbable mesh designed specifically for umbilical hernia repair, in fiscal year 2025.

- Strategic Focus: Expanding the bioabsorbable mesh portfolio, maintaining comprehensive hernia mesh range leadership across synthetic and composite categories, and growing clinical support services to differentiate from competitors in the organized surgical environment.

Market Concentration Analysis

The India ventral hernia mesh devices market is moderately consolidated, with the top global players holding a significant combined share of premium mesh through broad portfolios, clinical evidence, and established hospital relationships.

Barriers to entry include device registration under CDSCO, the need for clinical validation, surgeon training, and reliable supply at competitive prices. These factors favour established multinationals and well-capitalised domestic manufacturers.

Consolidation is gradually increasing as global leaders extend composite and robotic-ready mesh, while Indian players expand affordable portfolios. Strategic investment, local manufacturing, and distribution partnerships are reinforcing competitive positioning across the market.

Investment & Growth Opportunities

Fastest-Growing Segments

Resorbable mesh expands fastest among mesh types, driven by demand for temporary reinforcement in contaminated and high-risk repair. Outpatient facilities are the next-fastest setting, supported by day-care surgery and faster recovery protocols.

Emerging Markets

South India is the fastest growing region, anchored by advancing tertiary care, rising medical tourism, and expanding surgical capacity. Tier-2 and tier-3 cities represent significant untapped opportunity for cost-competitive mesh.

Venture & Investment Trends

Investment is flowing into domestic manufacturing, lightweight and composite mesh innovation, and robotic-ready product lines. Strategic acquisitions and capacity expansion are strengthening local supply and broadening access across hospitals.

Future Market Outlook (2026-2034)

The India ventral hernia mesh devices market is forecast to expand from USD 29.67 Million in 2025 to USD 59.86 Million by 2034 at a CAGR of 8.11%, adding roughly USD 30.19 Million in market value over the forecast period.

Four forces will shape the market through 2034: rising hernia and surgical volumes; wider adoption of laparoscopic and robotic repair; continued innovation in lightweight and composite mesh; and a growing share of cost-competitive domestic manufacturers.

By 2034, ventral hernia repair in India is expected to be defined by minimally invasive, mesh-reinforced procedures, with absorbable and composite designs taking a larger share. Expanding access and insurance coverage will further accelerate adoption across surgical settings.

Research Methodology

Primary Research

Primary research included structured interviews with hernia surgeons, hospital procurement leads, mesh manufacturers, distributors, and regulatory specialists, validating market sizing, segment mix, regional demand, and mesh type evolution.

Secondary Research

Secondary sources included CDSCO publications, peer-reviewed surgical journals, hospital and surgical society data, government health surveys, and annual reports, press releases, and investor presentations from listed device manufacturers.

Forecasting Models

Market forecasts used top-down and bottom-up models combining hernia procedure volumes, mesh adoption rates, average selling prices, technique evolution, and macroeconomic variables. Scenario analysis addressed regulatory pace, pricing pressure, and adoption of minimally invasive repair.

India Ventral Hernia Mesh Devices Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Mesh Types Covered | Resorbable Mesh, Partially Absorbable Mesh, Non Resorbable Mesh |

| Indications Covered | Umbilical Hernia, Epigastric Hernia, Incisional Hernia, Others |

| Procedures Covered | Open Surgery, Laparoscopic Surgery, Robotic Surgery, Others |

| End Uses Covered | Inpatient Facilities, Outpatient Facilities |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Medtronic, Johnson & Johnson, BD, W. L. Gore & Associates Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India ventral hernia mesh devices market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India ventral hernia mesh devices market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India ventral hernia mesh devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Ventral Hernia Mesh Devices Market Report

The India ventral hernia mesh devices market was valued at USD 29.67 Million in 2025, driven by rising hernia surgery volumes, growing obesity, and wider adoption of mesh-based ventral hernia repair.

The market is projected to grow at an 8.11% CAGR from 2026 to 2034, reaching USD 59.86 Million, supported by laparoscopic and robotic repair, lightweight mesh innovation, and expanding healthcare access.

Non resorbable mesh leads at 56.8% in 2025, driven by durability, low cost, and strong tissue ingrowth.

Inpatient facilities dominate at 69.4% in 2025, reflecting complex repairs that need overnight care. Outpatient facilities at 30.6% are growing through day-care and ambulatory surgery.

North India commands 32.5% in 2025, led by dense hospital networks, high surgical volumes, and strong specialist presence.

Leading players include Medtronic, Johnson & Johnson, BD, and W. L. Gore & Associates, Inc., among others.

Growth is driven by rising surgical volumes, growing obesity, the shift to laparoscopic and robotic repair, expanding insurance coverage, and a strengthening base of cost-competitive domestic manufacturers.

Advances in lightweight, composite, and tissue-separating mesh, along with robotic and laparoscopic platforms, are improving safety and recovery, raising adoption of premium, technique-specific mesh products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)