India Video Game Market Size, Share, Trends and Forecast by Device, Type, and Region, 2026-2034

India Video Game Market Size, Share, Trends & Forecast (2026-2034)

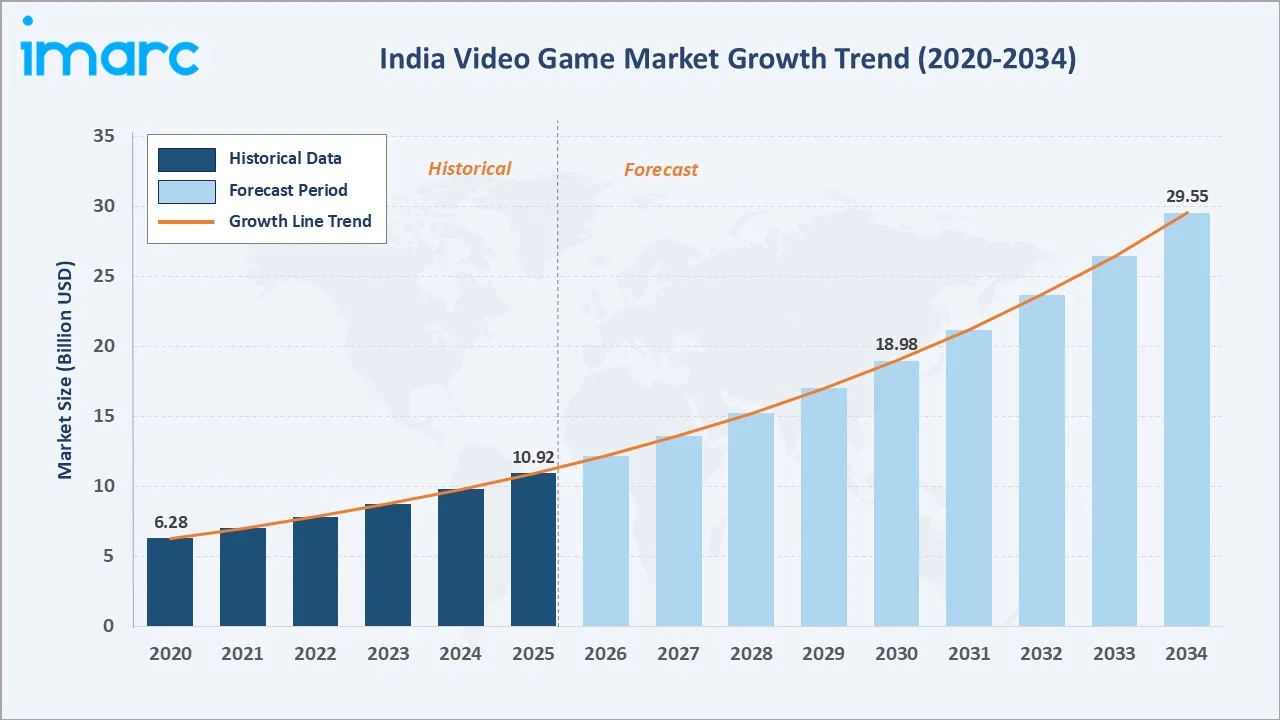

The India video game market reached USD 10.92 Billion in 2025 and is projected to reach USD 29.55 Billion by 2034, growing at a CAGR of 11.70% during 2026-2034. India has emerged as one of the world's fastest-growing gaming markets, powered by 500 million smartphone users, the world's cheapest mobile data at USD 0.09 per GB, 27% of the total population under the age of 35, and Unified Payments Interface’s (UPI) frictionless micro-payment infrastructure enabling seamless in-app purchases.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.92 Billion |

|

Forecast Market Size (2034) |

USD 29.55 Billion |

|

CAGR (2026-2034) |

11.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

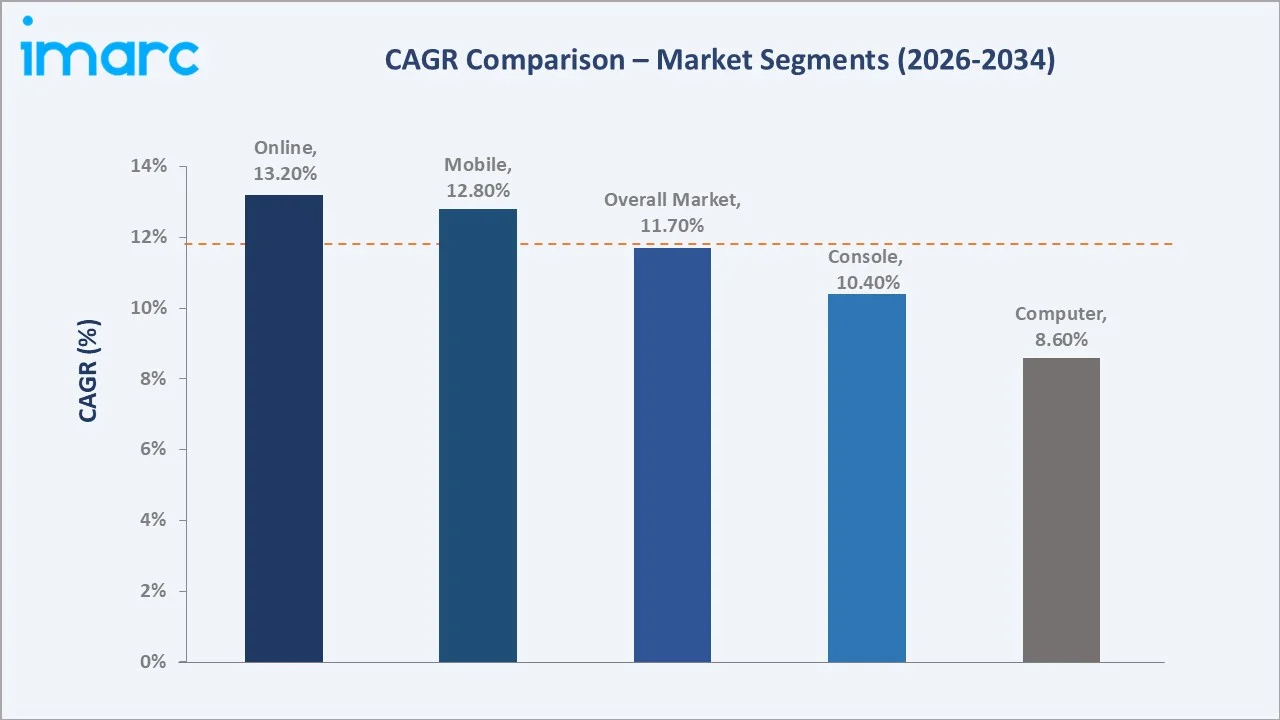

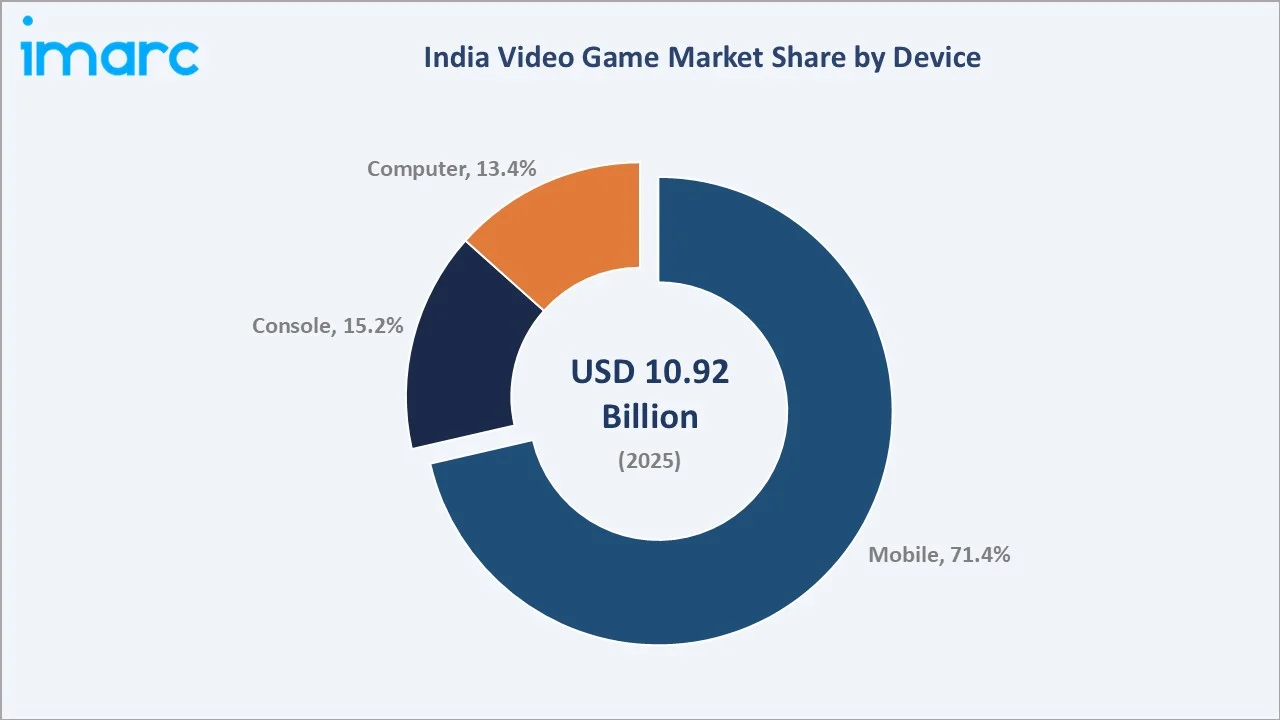

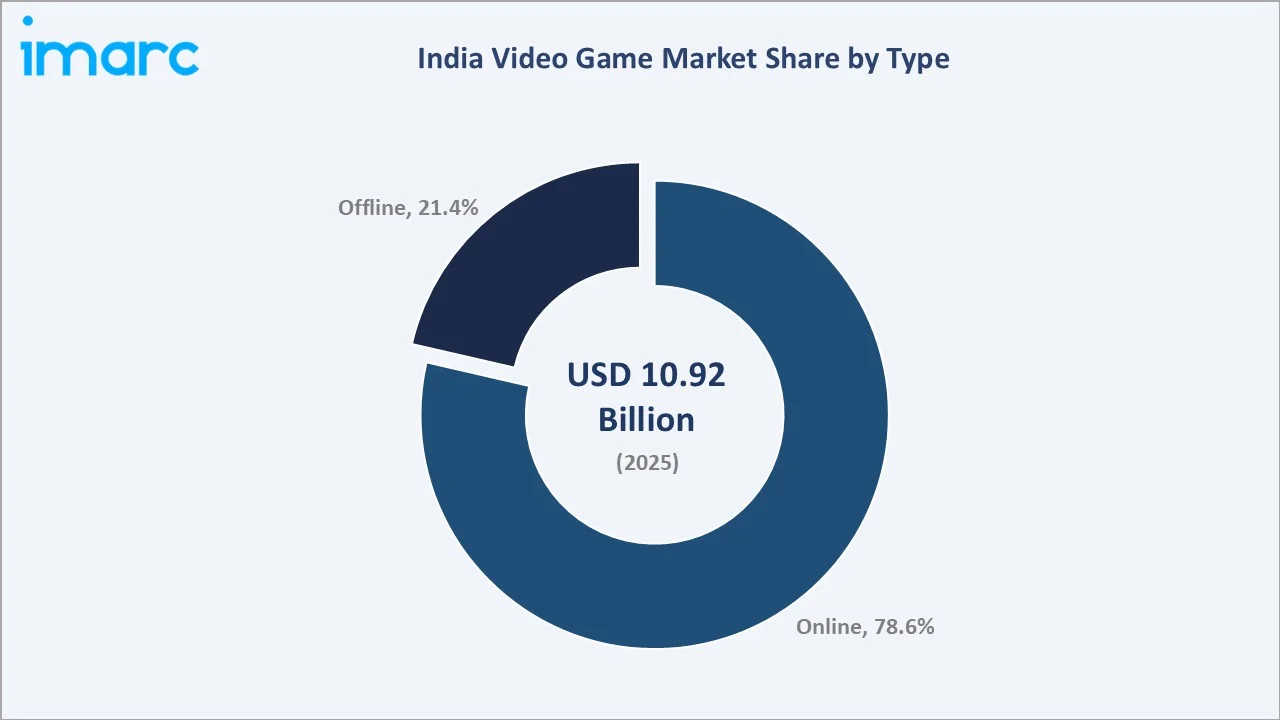

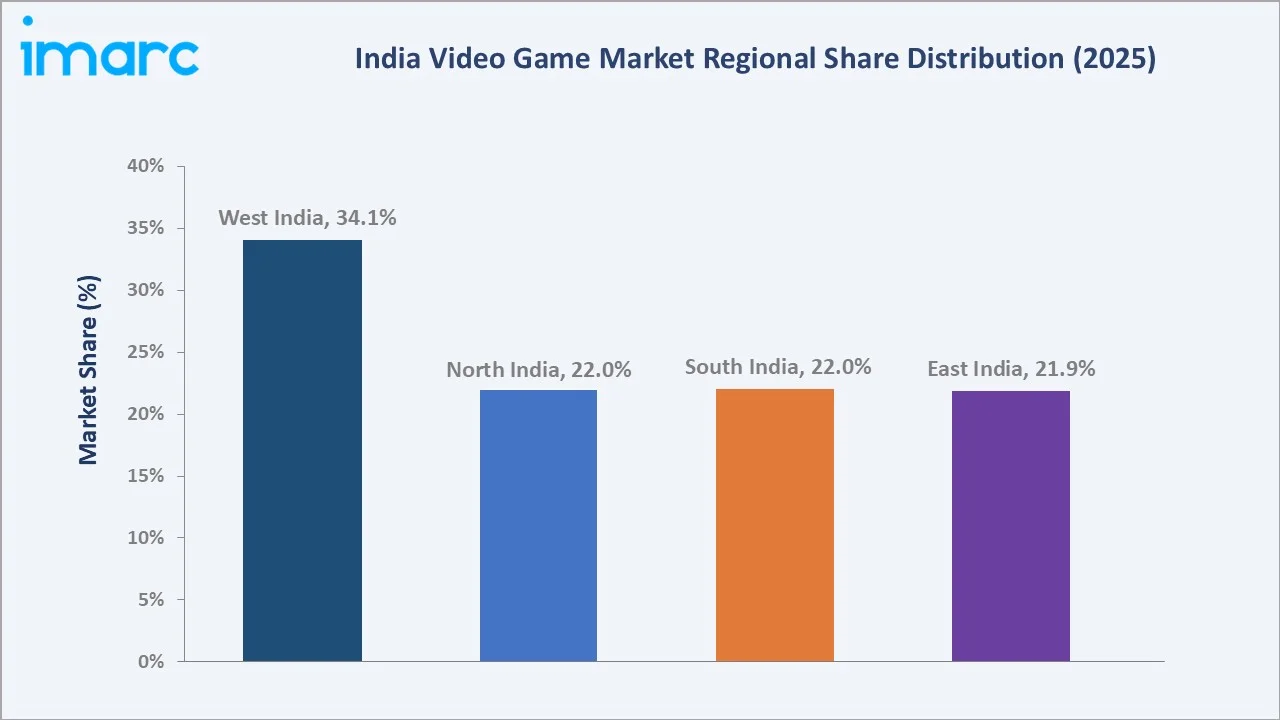

West India leads regionally with a 34.1% market share in 2025, driven by Maharashtra's game development studio concentration and Mumbai's venture capital ecosystem. Mobile gaming commands a 71.4% device share, while online gaming leads the type segment at 78.6%.

To get more information on this market, Request Sample

India's video game market is underpinned by three structural forces: the mobile-first gaming architecture that leverages India's 500 million smartphones and free-to-play monetization models accessible to price-sensitive consumers; the esports ecosystem that has institutionalized competitive gaming through major tournaments and formal government recognition, creating career pathways; and the UPI payment revolution that has reduced in-app purchase friction to a single tap.

Executive Summary

The India video game market is experiencing high-growth expansion, underpinned by the world's largest youth digital entertainment market, a rapidly scaling mobile gaming ecosystem, and the emergence of India as a significant game development hub. The market reached USD 10.92 Billion in 2025 and is forecast to reach USD 29.55 Billion by 2034, growing at a CAGR of 11.70%.

Mobile devices dominate with a 71.4% share in 2025, reflecting India's mobile-first internet infrastructure, where smartphone gaming is accessible to 500 million users at a fraction of the cost of console or PC gaming. Online gaming commands a 78.6% share, encompassing multiplayer mobile games, fantasy sports platforms, real-money skill games, cloud gaming services, and massively multiplayer online games that require internet connectivity for gameplay.

West India at 34.1% leads regionally, anchored by Maharashtra's dual advantage of game development studio concentration in Pune and venture capital in Mumbai. Leading vendors are collectively building the world's most competitive emerging market gaming ecosystem.

Key Market Insights

|

Insight |

Data |

|

Largest Device |

Mobile – 71.4% share (2025) |

|

Fastest Growing Device |

Mobile – ~12.8% CAGR (2026-2034) |

|

Largest Type |

Online – 78.6% share (2025) |

|

Fastest Growing Type |

Online – ~13.2% CAGR (2026-2034) |

|

Leading Region |

West India – 34.1% share (2025) |

|

Top Companies |

Nazara Technologies Limited, KRAFTON, Inc., Sporta Technologies Private Limited, Sea Limited, nCore games |

Key Analytical Observations Supporting The Above Data:

- Mobile at 71.4% (2025) dominates as India's smartphone-first internet economy has made mobile the primary gaming device for gamers who own smartphones but not gaming consoles or gaming PCs.

- Online at 78.6% (2025) leads as India's gaming market is structurally oriented toward live-service, multiplayer, and real-money skill gaming formats that require continuous internet connectivity.

- West India's 34.1% (2025) share reflects Maharashtra's dominant role in India's gaming economy: Pune hosts more than 300 game development studios; Mumbai is the primary venture capital hub funding India's gaming startup ecosystem; and Maharashtra represents India's highest-spending gaming audience.

- North, South, and East India regions each hold approximately 22% share, a remarkably balanced distribution reflecting the broadening of India's gaming culture beyond its traditional West India epicenter to encompass Delhi NCR's esports culture, Bengaluru's game developer talent pool, and Kolkata's mobile gaming adoption driven by affordable Jio connectivity in eastern India.

India Video Game Market Overview

India's video game market encompasses the full spectrum of interactive entertainment: mobile casual games, mid-core mobile games, fantasy sports platforms, real-money skill games, console gaming, PC gaming, and emerging cloud gaming services. Revenue streams include in-app purchases, in-game advertising, battle pass subscriptions, real-money game entry fees, console and PC game sales, and gaming hardware.

India's gaming market macroeconomic foundation is built on three converging infrastructure platforms: Reliance Jio's low-cost 4G/5G network that made mobile data consumption economical for 500 million users; UPI's instant payment infrastructure that reduced in-app purchase friction from a multi-step card payment to a single biometric authentication; and the Google Play/App Store distribution infrastructure that delivers games to Indian consumers at zero distribution cost.

Market Dynamics

To evaluate market opportunities, Request Sample

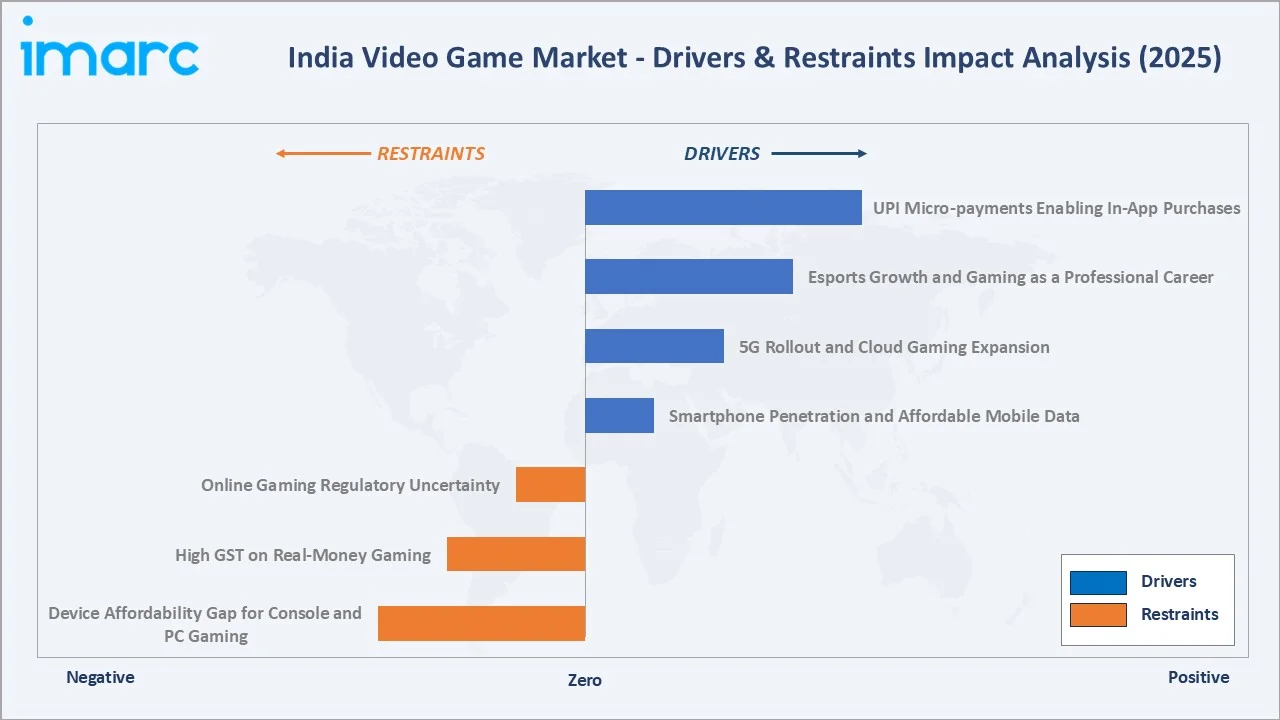

Market Drivers

- Smartphone Penetration and Affordable Mobile Data: India's 500 million smartphone user base, with entry-level gaming-capable smartphones available at INR 8,000–12,000, is enabling gaming access across all income segments. At USD 0.09 per GB, India's mobile data cost further enables Indian gamers to play data-intensive online titles without prohibitive data cost concerns.

- 5G Rollout and Cloud Gaming Expansion: India's 5G network is enabling cloud gaming services to deliver console-quality gaming experiences on mid-range smartphones without requiring expensive hardware. Xbox Cloud Gaming, NVIDIA GeForce NOW, and Jio's cloud gaming platform are collectively building India's cloud gaming infrastructure, with the India cloud gaming market size valued at USD 14.77 Million in 2025 at a 46.04% CAGR.

- Esports Growth and Gaming as a Professional Career: India's government recognition of esports as a competitive sport in 2022 was a landmark policy shift that legitimized gaming careers for India's youth. The Esports Federation of India tournaments, university esports programs, and esports-specific scholarship initiatives are creating structured career pathways for professional gamers, coaches, content creators, and tournament organizers.

- UPI Micro-payments Enabling In-App Purchases: UPI has fundamentally transformed gaming monetization in India by enabling seamless micro-payments as small as INR 10 (USD 0.12) for in-game purchases. In-app purchases now constitute 40.45% of India's gaming revenue (2025), driven by battle pass purchases, cosmetic skin bundles, and character upgrades.

Market Restraints

- Online Gaming Regulatory Uncertainty: The Online Gaming framework established by the Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Amendment Rules, 2023, while providing a welcome unified regulatory structure, has created compliance complexity for operators through KYC requirements, responsible gaming deposit limits, and self-exclusion mandates.

- High GST on Real-Money Gaming: The GST Council's October 2023 decision to impose 28% GST on the full face value of real-money gaming deposits significantly impacted the economics of India's fantasy sports and skill-gaming platforms. The effective tax burden on real-money gaming operators increases platform operating costs by 8–15 percentage points relative to pre-2023 economics.

- Device Affordability Gap for Console and PC Gaming: While mobile gaming is mass-market accessible, console gaming and gaming PCs remain aspirational purchases for India's middle class. This device affordability gap structurally limits console and PC gaming to India's top 15–20 million households, constraining the premium gaming segment's growth relative to mobile gaming's billion-user addressable market.

Market Opportunities

- India-Made Game Development and Global Export: India has 2,364 gaming startups, including Zupee, WinZO, JetSynthesys, MPL, and Nazara. The government's 'Developing Games in India' initiative, IndiaJoy gaming conference, and IndieSpark accelerator program are building the infrastructure for India to become a significant game development exporter.

- Gaming Monetization Through Brand Integration: In January 2025, KRAFTON India partnered with Mahindra to introduce the Mahindra BE 6 electric vehicle within BGMI, demonstrating the emerging brand integration monetization model where automotive, consumer goods, and entertainment companies pay game developers for branded in-game content placements.

Market Challenges

- Game Developer Talent Competition and Attrition: India's 18,000 game developers are in high demand from both domestic studios and international game companies opening India development centers. The talent shortage is particularly acute in specialized roles where India's game development education pipeline has not kept pace with industry demand.

- Gaming Addiction and Screen Time Concerns: Growing parental and government concern about gaming addiction is creating regulatory pressure for screen time controls, age verification mechanisms, and spending caps on minor accounts. MeitY's responsible gaming guidelines require platforms to implement parental control features, daily play time limits, and spending limit disclosures that add development cost and user friction for games with high child and adolescent user bases.

Emerging Market Trends

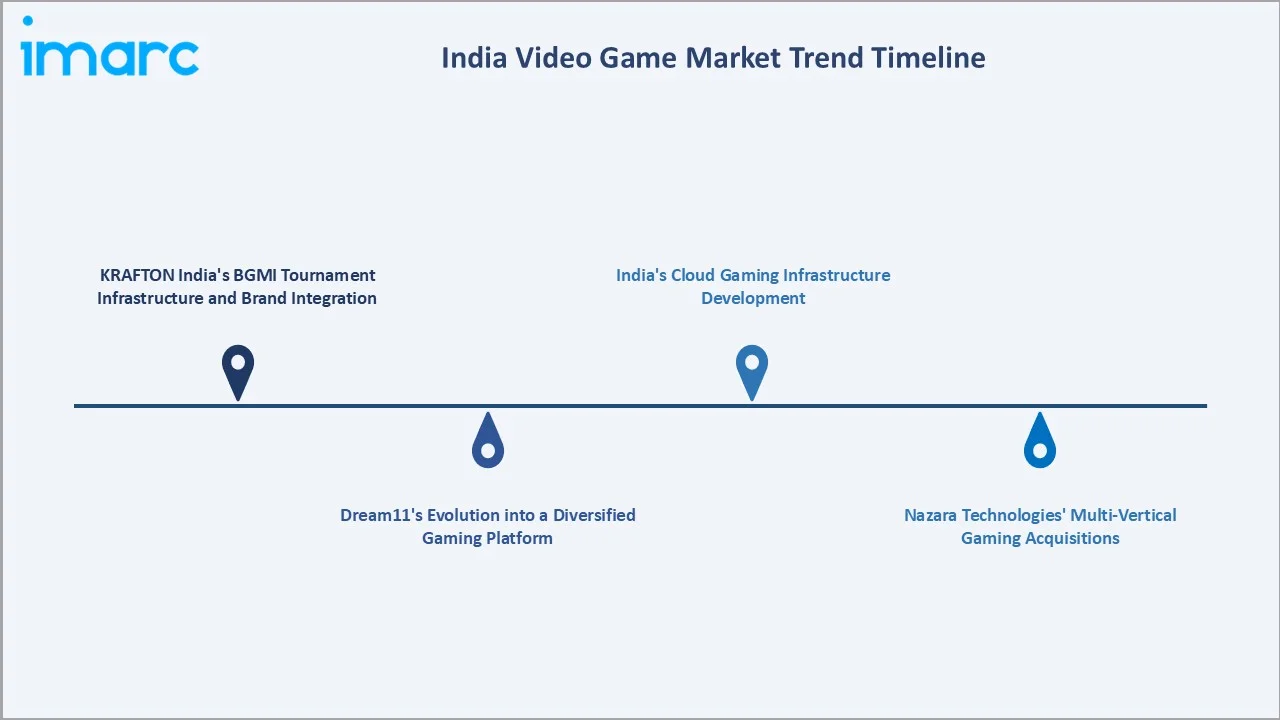

1. KRAFTON India's BGMI Tournament Infrastructure and Brand Integration

KRAFTON India's Battlegrounds Mobile India (BGMI) Series (BGIS) 2024, launched in March 2024 with a prize pool of INR 2 crore, established BGMI as India's premier esports title, sustaining the 100 million+ downloads that make it India's most popular battle royale game. In January 2025, KRAFTON India partnered with Mahindra to introduce the Mahindra BE 6 electric vehicle within BGMI's gaming universe, pioneering automotive brand integration in Indian gaming.

2. Dream11's Evolution into a Diversified Gaming Platform

Sporta Technologies' Dream11 has evolved beyond cricket fantasy to a diversified gaming ecosystem encompassing football, basketball, kabaddi, and casual game cross-selling during cricket off-seasons. Its strong brand recall, large user base, and sports-led engagement model have enabled Dream11 to deepen monetization and retain users across multiple gaming formats.

3. Nazara Technologies' Multi-Vertical Gaming Acquisitions

In August 2024, Nazara Technologies acquired Fusebox Games for USD 27.2 million to strengthen its IP-led global gaming business. The deal supports Nazara’s M&A-led expansion strategy across India and international markets. Moreover, Nazara Technologies acquired a 47.7% stake in Moonshine Technology, the parent company of PokerBaazi, for around INR 832 crore. It also planned to invest INR 150 crore in primary capital, taking the total deal value to about INR 982 crore and strengthening its real-money gaming portfolio.

4. India's Cloud Gaming Infrastructure Development

The India cloud gaming market size was valued at USD 14.77 Million in 2025 and is projected to reach USD 446.24 Million by 2034, growing at a compound annual growth rate of 46.04% from 2026 to 2034, making it the fastest-growing gaming technology segment in India. Jio's JioGames cloud platform, Airtel's Xstream gaming service, and Microsoft's Xbox Cloud Gaming expansion in India are collectively building the cloud gaming infrastructure that will democratize console-quality gaming across India's smartphone base.

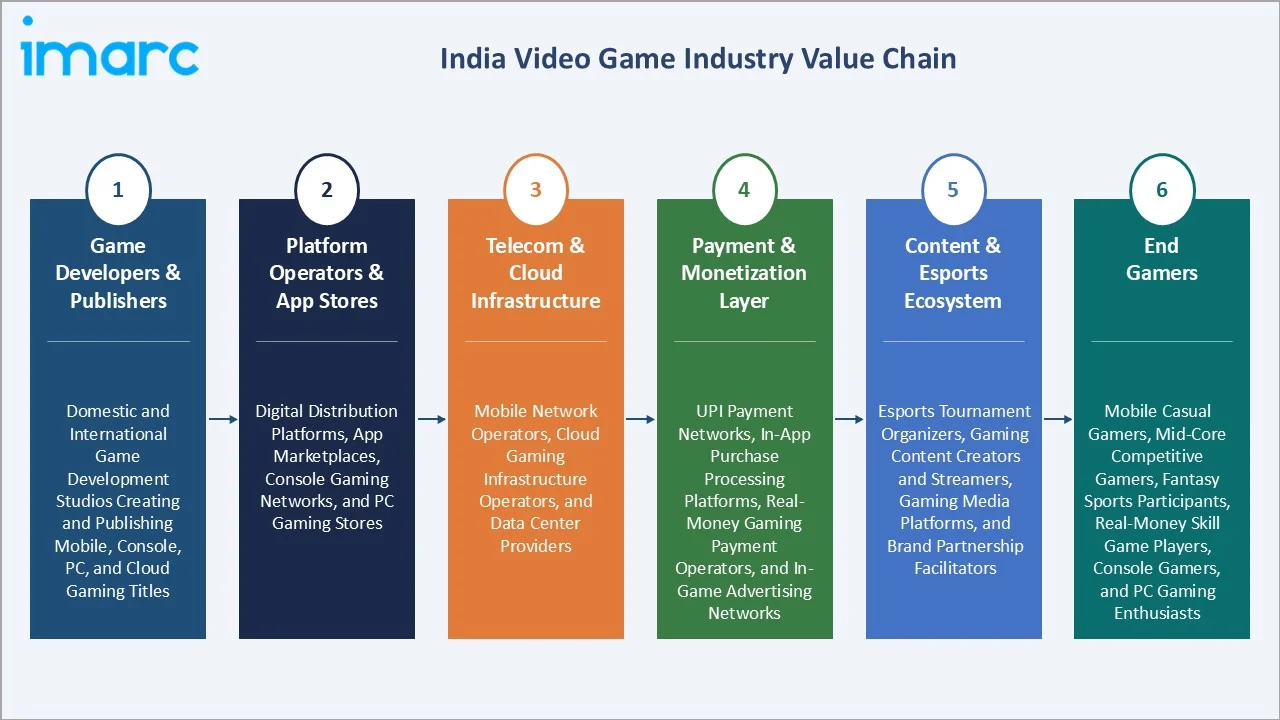

Industry Value Chain Analysis

India's video game market value chain spans game creation through player engagement, with each stage occupied by specialized developers, platform operators, infrastructure providers, payment processors, and content distribution channels whose collective performance determines game quality, accessibility, and commercial viability.

|

Stage |

Key Players / Examples |

|

Game Developers & Publishers |

Domestic and international game development studios creating and publishing mobile, console, PC, and cloud gaming titles |

|

Platform Operators & App Stores |

Digital distribution platforms, app marketplaces, console gaming networks, and PC gaming stores |

|

Telecom & Cloud Infrastructure |

Mobile network operators, cloud gaming infrastructure operators, and data center providers |

|

Payment & Monetization Layer |

UPI payment networks, in-app purchase processing platforms, real-money gaming payment operators, and in-game advertising networks |

|

Content & Esports Ecosystem |

Esports tournament organizers, gaming content creators and streamers, gaming media platforms, and brand partnership facilitators |

|

End Gamers |

Mobile casual gamers, mid-core competitive gamers, fantasy sports participants, real-money skill game players, console gamers, and PC gaming enthusiasts |

Technology Landscape in the India Video Game Industry

Mobile Gaming Technology

India's mobile gaming technology stack is defined by the Android ecosystem, with Unity and Unreal Engine powering the majority of India's mid-core and casual mobile games, respectively. Game developers are increasingly targeting Snapdragon 6-series and MediaTek Dimensity 700-series chipsets found in INR 10,000–20,000 smartphones, optimizing game graphics and performance for the devices owned by the mobile gaming audience.

Online and Real-Time Multiplayer Infrastructure

India's online gaming infrastructure has matured significantly, with AWS Mumbai, Microsoft Azure India, and Google Cloud India data centers providing low-latency game server hosting for BGMI and Free Fire. Real-time multiplayer gaming requires sub-50ms server response times, now achievable for urban and semi-urban gamers through India's expanded fiber and 5G backhaul infrastructure.

Esports Technology and Streaming Infrastructure

India's esports ecosystem is supported by dedicated gaming streaming platforms that provide real-time tournament streaming, interactive viewer features, and creator monetization tools. NODWIN Gaming's esports technology platform manages bracket management, player verification, and prize distribution for annual tournaments, while gaming content creator studios in Mumbai and Bengaluru are producing professional gaming commentary and analysis content that builds tournament viewership and brand sponsorship markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Device |

Mobile |

71.4% |

2025 |

|

Type |

Online |

78.6% |

2025 |

|

Region |

West India |

34.1% |

2025 |

By Device

Mobile gaming commands a 71.4% share in 2025, reflecting India's fundamental market reality: 500 million smartphone users versus 15–20 million console owners and 30–40 million gaming PC users create an addressable market ratio of 20:1 for mobile versus other gaming devices. Free-to-play mobile games' zero upfront cost eliminates the greatest barrier to gaming adoption for India's price-sensitive consumer base.

To access detailed market analysis, Request Sample

Console gaming represents 15.2% of the market and is projected to grow at approximately 10.4% CAGR as PlayStation 5 and Xbox Series X penetration expands among India's premium consumer segment and cloud gaming lowers the effective hardware cost barrier. Computer gaming at 13.4% serves India's esports community and PC gaming enthusiasts who invest in gaming-configured systems for competitive titles, including Valorant, Counter-Strike 2, and Dota 2.

By Type

Online gaming commands a 78.6% share in 2025, reflecting India's data consumption revolution, with average monthly mobile data consumption per user crossing 31 GB in 2025. Indian gamers have embraced internet-connected gaming experiences that were economically inaccessible pre-Jio. Online gaming also enables the live service monetization models that generate superior per-user lifetime value compared to one-time purchase games.

Offline gaming at 21.4% encompasses single-player console and PC games, downloaded mobile games playable without connectivity, and physical game media sales. Offline gaming retains meaningful market share among console and PC gamers who invest in premium single-player narrative experiences and among rural mobile gamers with inconsistent connectivity who prefer games downloadable for offline play.

Regional Market Insights

West India's market leadership (34.1%, 2025) traces directly to Maharashtra's dual advantage: a dense concentration of game development studios in Pune and the financial services ecosystem in Mumbai that funds gaming startups.

North India at 22.0% is distinguished by Delhi-NCR's status as India's premier esports hub, hosting the highest concentration of esports venues, gaming cafés, and professional team training facilities in India. Moreover, the region’s large college-educated youth population creates a dense competitive gaming community.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

34.1% |

Game development studio concentration in Pune; Mumbai venture capital funding for gaming startups; Maharashtra's high-spending urban consumer base |

|

North India |

22.0% |

Delhi-NCR's dense esports event infrastructure and high UPI gaming transaction volumes, UP and Punjab's growing mobile gaming adoption, and competitive gaming culture |

|

South India |

22.0% |

Bengaluru's game developer talent hub, Karnataka's reversal of skill-gaming ban opening real-money market, and Tamil Nadu's strong mobile gaming culture |

|

East India |

21.9% |

West Bengal and Odisha's rapidly growing mobile gaming adoption, Kolkata's gaming café culture, growing BGMI and Free Fire esports community in tier 2 cities, and Northeast India's strong mobile gaming engagement |

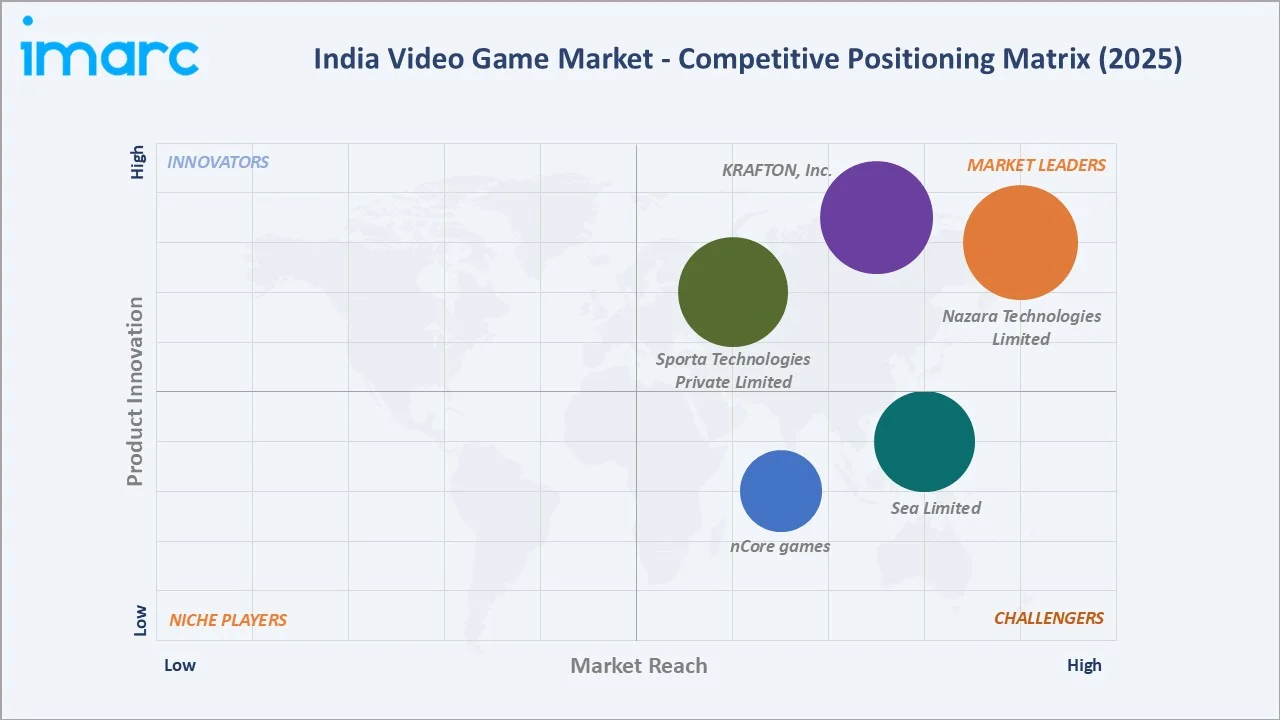

Competitive Landscape

India's video game market is moderately fragmented, with the top five players collectively accounting for an estimated 40–45% of market revenue in 2025.

|

Company Name |

Key Products / Titles |

Market Position |

Core Strength |

|

Nazara Technologies Limited |

World Cricket Championship 3 (WCC3), King of Thieves (KoT), CATS: Crash Arena Turbo Stars, Smaaash, Funky Monkeys, among others |

Market Leader |

Diversified gaming portfolio spanning multiple genres and verticals; established track record across mobile gaming, esports, edutainment, and real-money gaming segments |

|

KRAFTON, Inc. |

BATTLEGROUNDS MOBILE INDIA (BGMI), Road to Valor: Empires, Garuda Saga, Bullet Echo India, Archery King: PVP Battle, CookieRun India |

Market Leader |

Established mid-core mobile gaming presence; active esports tournament ecosystem |

|

Sporta Technologies Private Limited |

Dream11, FanCode, DreamSetGo, DreamCricket |

Market Leader |

One of India's largest fantasy sports platforms, strong UPI-integrated monetization capabilities, diversified sports-gaming ecosystem |

|

Sea Limited |

Free Fire |

Strong Challenger |

Broad mobile gaming user base across urban and Tier 2/3 city markets; well-established battle royale gaming franchise |

|

nCore games |

FAU-G, Apna Games |

Challenger |

Pioneering domestically developed mobile game IP; focused on localized hero and mythology-based gaming content |

Regional developers, independent mobile studios, and vernacular gaming platforms account for the remaining share, ensuring a diverse and competitive ecosystem where innovation from smaller players continuously challenges established market leaders.

Key Company Profiles

Nazara Technologies Limited

Nazara Technologies Limited is one of India's leading gaming and sports media companies. Nazara's multi-vertical gaming strategy is designed to capture revenue across every major segment of India's gaming economy.

- Product Portfolio: World Cricket Championship 3 (WCC3), King of Thieves (KoT), CATS: Crash Arena Turbo Stars, Smaaash, Funky Monkeys, among others.

- Recent Developments: In March 2026, Nazara Technologies announced plans to acquire a 50% stake in Spain-based Bluetile Games and BestPlay Systems for USD 100.3 million. The deal will strengthen Nazara’s casual gaming portfolio through 17 live titles, 375 million downloads, and AI-led operations.

- Strategic Focus: Multi-vertical gaming expansion; WCC series franchise development for cricket gaming; international acquisition strategy targeting complementary gaming studios.

KRAFTON, Inc.

KRAFTON, Inc. operates in India through its flagship title BATTLEGROUNDS MOBILE INDIA (BGMI), the localized India version of BGMI/PUBG Mobile specifically developed to comply with India's data localization requirements.

- Product Portfolio: BATTLEGROUNDS MOBILE INDIA (BGMI), Road to Valor: Empires, Garuda Saga, Bullet Echo India, Archery King: PVP Battle, CookieRun India, and Real Cricket.

- Recent Developments: In April 2026, KRAFTON India launched the third cohort of its KRAFTON India Gaming Incubator (KIGI) and announced the upcoming release of Frontier Paladin, the first PC game developed through the program. The new cohort will support four emerging studios with funding of up to USD 150,000, mentorship, user acquisition support, and access to industry partners to help scale globally.

- Strategic Focus: BGMI India content localization (Indian maps, characters, festival events); BGIS esports ecosystem development; automotive and consumer brand integration revenue stream; India game development investment through KRAFTON India Incubator program.

Market Concentration Analysis

India's video game market exhibits moderate fragmentation, reflecting the diversity of India's gaming economy, where mobile casual gaming, fantasy sports, battle royale, and real-money gaming represent distinct sub-markets, each with its own dominant players.

Vertical-specific concentration is higher: Dream11 holds approximately 70%+ of India's fantasy sports market; BGMI holds approximately 35–40% of India's battle royale mobile gaming segment; and WCC holds approximately 40% of India's cricket mobile gaming segment.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud gaming (~46% CAGR), online gaming type (~13.2% CAGR), mobile device gaming (~12.8% CAGR), in-app purchases monetization (~44% CAGR for IAP revenue), and esports sponsorship revenue (~25% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address USD 15+ billion in incremental market opportunity within India's video game ecosystem by 2030.

Emerging Market Expansion

India's Tier 2 and Tier 3 cities represent the next frontier of India's mobile gaming market expansion. Garena's Free Fire achieved its dominant position precisely through Tier 2/3 city penetration, where lighter game file sizes and lower device requirements suited the entry-level smartphones prevalent outside metro India.

Rural India represents a long-term but structurally growing gaming market. Casual and hyper-casual mobile games requiring no investment beyond 1 GB smartphone storage and minimal data consumption are reaching India's rural youth population through feature-phone-to-smartphone upgrades that are adding 30–40 million new potential gamers annually.

Venture and Institutional Investment Trends

- The Gaming sector in India comprises 2.36K startups, including 268 funded companies having collectively raised USD 3.22 Billion in venture capital money and private equity. Out of these, 75 are Series A+ funded, and 4 have achieved unicorn status.

- Government policy support signals policy alignment between gaming industry growth and India's broader digital economy agenda. The government's recognition of esports as a competitive sport and India's inclusion in the 2022 Commonwealth Games esports exhibition are creating a policy environment that treats gaming as a legitimate economic and cultural sector.

Future Market Outlook (2026-2034)

The India video game market is positioned for high-growth, sustained expansion through 2034. From a base of USD 10.92 Billion in 2025, the market is projected to reach USD 29.55 Billion by 2034, representing total incremental value creation of USD 18.63 billion at a CAGR of 11.70%.

The growth reflects India's structural gaming fundamentals: the world's second-largest gamer population (568 million), the world's cheapest mobile data enabling gaming monetization at scale, and the compounding effect of a gaming-native generation aging into higher-income demographics that will increase average per-user gaming spending from USD 15–25 (2025) toward USD 40–60 (2034).

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants in 2024–2025, including game developers, gaming platform executives, esports tournament organizers, gaming investors, telecom gaming partnership managers, and government gaming policy officials across Mumbai, Bengaluru, Pune, Delhi, and Hyderabad.

Secondary Research

Secondary research encompassed company disclosures, FICCI-EY gaming sector reports, IndieSpark gaming startup database, NODWIN Gaming esports market data, MeitY online gaming regulation documents, and industry publications (India Game Developer Conference reports, Gaming Tech India, IGN India).

Forecasting Models

Market size estimations incorporated India gamer population growth projections, per-gamer spending trajectory modeling, device penetration forecasts, online gaming platform revenue data, and in-app purchase value chain analysis. A base-case CAGR of 11.70% reflects consensus estimates validated against platform revenue disclosures, venture transaction multiples, and gaming population growth trajectories from FY2020 to FY2025.

India Video Game Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Devices Covered |

Console, Mobile, Computer |

|

Types Covered |

Online, Offline |

|

Regions Covered |

North India, South India, East India, West India |

|

Companies Covered |

Nazara Technologies Limited, KRAFTON, Inc., Sporta Technologies Private Limited, Sea Limited, nCore games, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Video Game Market Report

The India video game market reached USD 10.92 Billion in 2025 and is projected to reach USD 29.55 Billion by 2034.

The market is expected to grow at a CAGR of 11.70% during 2026-2034, driven by smartphone penetration, 5G rollout, esports growth, and UPI-enabled in-app purchase monetization.

West India leads with a 34.1% share in 2025, anchored by Maharashtra's game development studio concentration in Pune and Mumbai's venture capital ecosystem funding gaming startups.

Mobile dominates with a 71.4% share in 2025, reflecting India's 500 million smartphone user base, the world's lowest mobile data cost, and free-to-play game accessibility at zero upfront hardware investment.

Online gaming holds the largest share at 78.6%, encompassing multiplayer mobile games, fantasy sports platforms, real-money skill games, and cloud gaming services that require internet connectivity for gameplay.

Some of the key players include Nazara Technologies Limited, KRAFTON, Inc., Sporta Technologies Private Limited, Sea Limited, and nCore games.

Online gaming is growing at ~13.2% CAGR as India's data consumption revolution has enabled live-service game monetization that generates 3–5x higher per-user lifetime value than one-time purchase offline games, incentivizing developer investment in online game formats.

Key challenges include online gaming regulatory uncertainty, 28% GST on real-money gaming deposits, device affordability gap for console and PC gaming, internet latency in rural areas, and game developer talent competition from international studios opening India offices.

Cloud gaming infrastructure, vernacular language mobile gaming, India-made game IP development, esports ecosystem investment, Tier 2/3 city gaming platform expansion, and gaming creator economy monetization represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)