India Video Streaming Market Size, Share, Trends and Forecast by Component, Streaming Type, Revenue Model, End User, and Region, 2026-2034

India Video Streaming Market Summary:

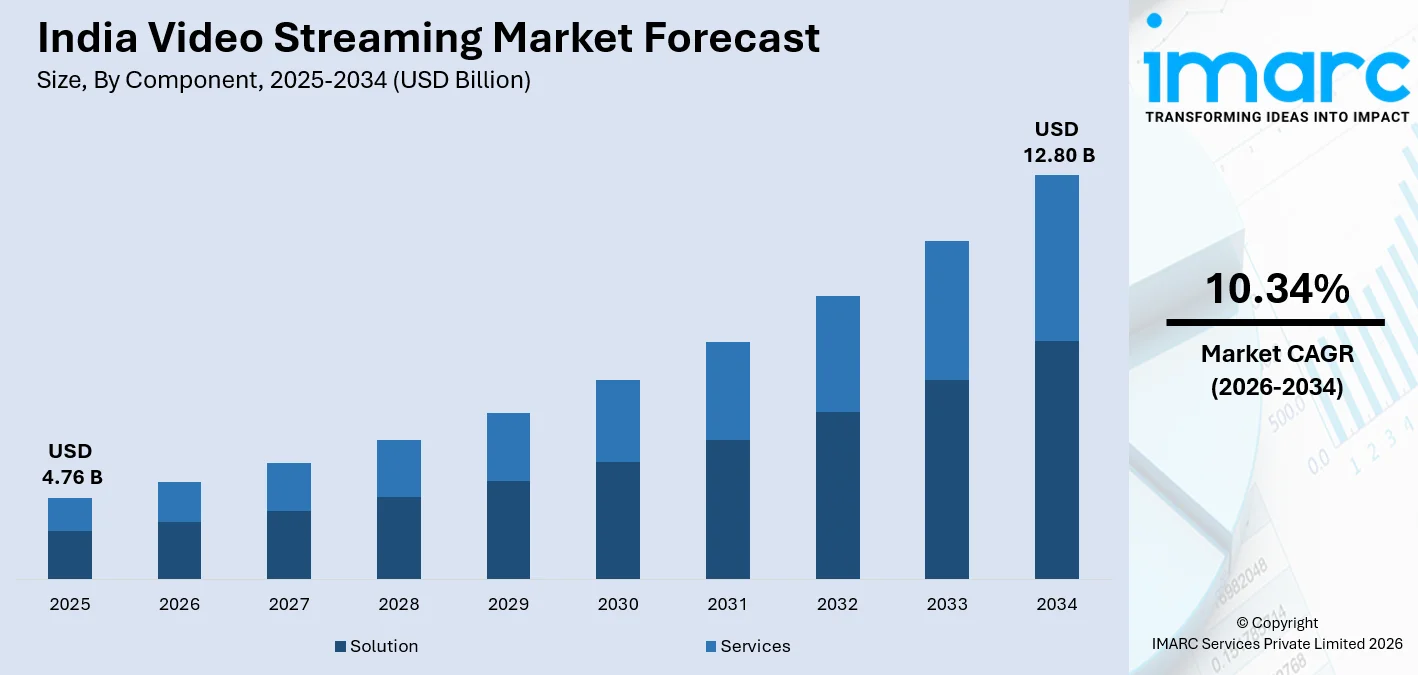

The India video streaming market size was valued at USD 4.76 Billion in 2025 and is projected to reach USD 12.80 Billion by 2034, growing at a compound annual growth rate of 10.34% from 2026-2034.

The India video streaming market is growing with a healthy rate, and the growth is driven by the increased rate of penetration of smartphones, the availability of affordable data services, and the increased willingness of people to access a variety of content through digital means. The growth of multilingual content, original content, and personalization are contributing significantly to the growth of the India video streaming market share.

Key Takeaways and Insights:

- By Component: Solution dominates the market with a share of 72.0% in 2025, driven by widespread adoption of integrated OTT platforms that deliver seamless, feature-rich content experiences.

- By Streaming Type: Non-linear video streaming leads the market with a share of 65.0% in 2025, reflecting viewer preference for flexible, personalized content consumption on any device.

- By Revenue Model: Advertisement represents the largest segment with a market share of 48.0% in 2025, supported by brands targeting India's vast, digitally engaged consumer base.

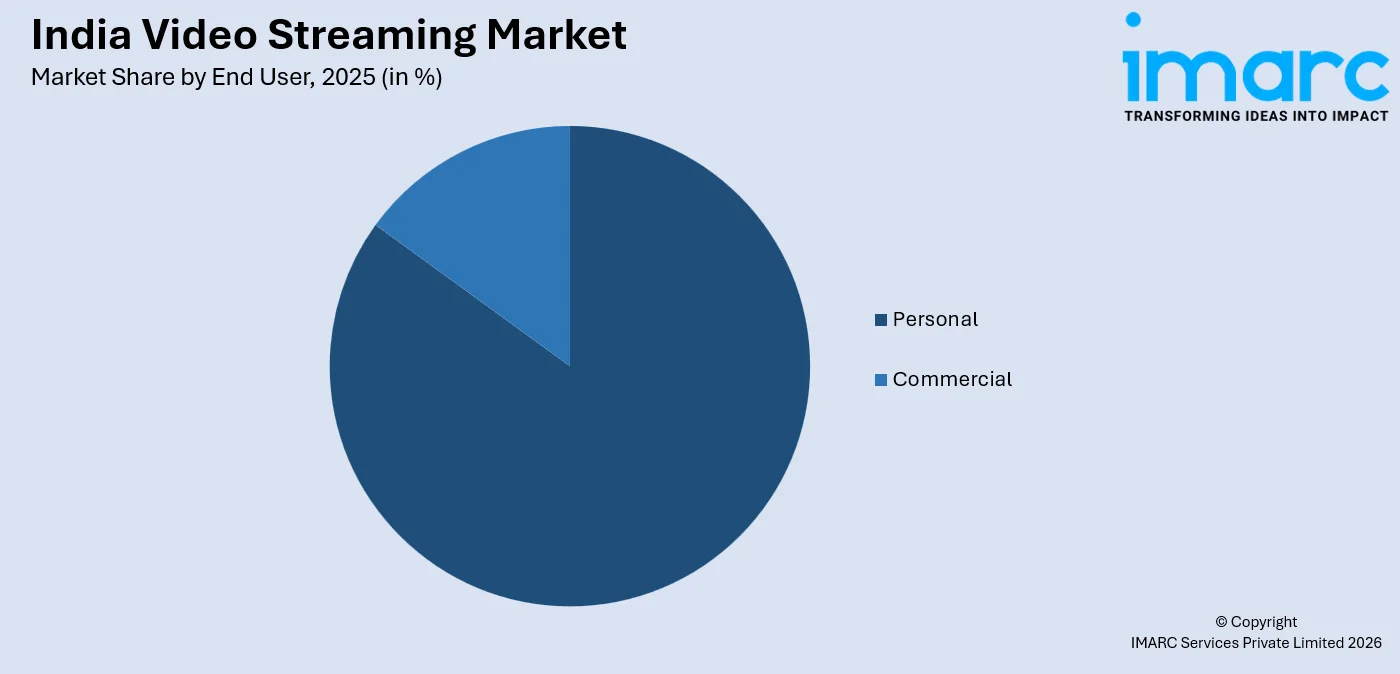

- By End User: Personal dominates the market with a share of 85.0% in 2025, as individual subscribers drive demand for entertainment, sports, and educational streaming content.

- By Region: West and Central India leads the market with a share of 32.0% in 2025, underpinned by high digital infrastructure density, urban affluence, and strong entertainment culture.

- Key Players: The India video streaming market features intense competition among domestic and international platforms, with players competing through original content investments, regional language offerings, bundled packages, and telecom partnerships.

To get more information on this market Request Sample

The India video streaming market is undergoing transformative growth, driven by a confluence of technological, economic, and cultural factors reshaping entertainment consumption patterns. The proliferation of affordable smartphones and cost-effective mobile internet plans has democratized access to streaming platforms across diverse demographics and income groups. In November 2025, the newly formed platform JioHotstar, created from the merger of Disney+ Hotstar and JioCinema, surpassed 1 billion downloads on the Google Play Store and amassed an estimated ~300 million subscribers, underscoring the scale of platform consolidation and user adoption in India’s OTT space. Regional language content initiatives are unlocking vast audiences in tier-2 and tier-3 cities, while original productions and live sports streaming are significantly boosting subscription acquisition and retention. The advertising-video-on-demand (AVOD) model is expanding viewer reach by offering free content to cost-sensitive consumers, complementing subscription-based tiers. Industry partnerships between telecom operators, smart TV manufacturers, and content platforms are creating bundled ecosystems that accelerate adoption, solidifying the market's trajectory across both metropolitan and emerging digital markets.

India Video Streaming Market Trends:

Expansion of Regional Language Content Libraries

The India video streaming market is witnessing substantial growth driven by the proliferation of regional language content across multiple linguistic streams. In December 2025, JioHotstar announced plans to invest ₹4,000 crore over the next five years to produce and acquire South India-focused and regional content, including originals in Tamil, Telugu, Malayalam, and Kannada, highlighting major platforms’ strategic shift toward vernacular programming to capture diverse audiences. Platforms are investing in vernacular programming spanning entertainment, drama, comedy, and documentary genres to capture audiences beyond metropolitan areas, unlocking previously underserved viewer segments in smaller cities and rural communities.

Integration of Live Sports Streaming

Live sports broadcasting is emerging as a powerful catalyst for streaming platform growth in India. In March 2026, the India–England ICC Men’s T20 World Cup semi-final on JioHotstar set a global digital sports viewership record with a peak of 65.2 million concurrent viewers, the highest ever for a live event on any streaming platform, highlighting how premium sports rights are driving massive engagement on digital services. The convergence of sports rights acquisition and digital delivery is reshaping subscription economics, drawing sports enthusiasts toward streaming platforms and reinforcing viewership retention. This trend is expanding subscriber bases while significantly increasing platform stickiness and daily active user engagement, contributing to India video streaming market growth.

Rise of Short-Form and Interactive Content Formats

Short-form video content and interactive entertainment formats are gaining significant traction on Indian streaming platforms, responding to evolving viewer preferences for quick, engaging experiences. In 2025, entertainment major Balaji Telefilms partnered with micro-drama platform Story TV, which has over million users, to create mobile-first, short-format shows tailored for digital audiences, highlighting how traditional media houses are embracing bite-sized content to capture attention on the go. Mobile-first consumption patterns are accelerating the adoption of bite-sized episodes, interactive storytelling, and gamified viewing formats, reflecting shifting content consumption habits particularly among younger demographics driving digital entertainment demand.

Market Outlook 2026-2034:

The Indian video streaming industry is on the cusp of sustained growth, with the industry’s penetration and depth being influenced by a variety of factors. As connected devices, smart TVs, and high-speed internet penetration continue to increase, the video streaming industry is likely to benefit from a widening audience base. Advertisers’ sentiment towards video streaming is also becoming increasingly favorable, and with a multi-tiered subscription model, the industry is well-placed to benefit from a range of consumption abilities. The market generated a revenue of USD 4.76 Billion in 2025 and is projected to reach a revenue of USD 12.80 Billion by 2034, growing at a compound annual growth rate of 10.34% from 2026-2034.

India Video Streaming Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Solution |

72.0% |

|

Streaming Type |

Non-Linear Video Streaming |

65.0% |

|

Revenue Model |

Advertisement |

48.0% |

|

End User |

Personal |

85.0% |

|

Region |

West and Central India |

32.0% |

Component Insights:

- Solution

- IPTV

- Over-the-top

- Pay TV

- Services

- Consulting

- Managed Services

- Training and Support

The solution dominates with a market share of 72.0% of the total India video streaming market in 2025.

OTT solutions form the technological backbone of India's video streaming ecosystem, enabling platforms to deliver high-quality, scalable content experiences across diverse devices and network conditions. These solutions encompass content management systems, recommendation engines, digital rights management, and multi-device playback capabilities that collectively define the viewer experience. In December 2025, Yupp Video Services powered a major platform upgrade for regional OTT service Chaupal, enabling it to deliver content seamlessly across more than 25 device types with enhanced performance, AI-driven personalisation, and robust multi-device support, highlighting how advanced OTT infrastructure partnerships are fueling streaming growth beyond global players. The deep integration of cloud-based delivery infrastructures and adaptive bitrate streaming ensures consistent accessibility even in bandwidth-constrained environments, making OTT solutions fundamental to market expansion across metropolitan and emerging geographies.

The popularity of OTT solutions indicates the changing face of digital consumption in India, with consumers demanding a seamless viewing experience. Solutions based on advanced OTT technology are more likely to offer content discovery, user analytics, and monetization options that help in improving the competitive advantage of a service. Innovation in user interface, artificial intelligence-based personalization, and multi-screen support are also contributing factors in underlining the importance of the solution segment in building user loyalty.

Streaming Type Insights:

- Live/Linear Video Streaming

- Non-Linear Video Streaming

The non-linear video streaming leads with a share of 65.0% of the total India video streaming market in 2025.

Non-linear, on-demand streaming has fundamentally transformed how Indian audiences engage with entertainment and informational content. The ability to access vast content libraries at any chosen time, pause, rewind, and resume viewing across devices aligns perfectly with the dynamic lifestyles of India's growing urban and semi-urban populations. Original series, films, documentaries, and diverse genre offerings available on-demand are driving higher per-session engagement, contributing to increased subscription retention and sustained platform loyalty across demographic segments.

The dominance of on-demand content reflects a structural shift away from scheduled broadcasting toward viewer-centric consumption models. Platforms are investing heavily in original, exclusive, and licensed on-demand content to differentiate their libraries and attract diverse subscriber bases. Advanced recommendation systems powered by artificial intelligence enhance content discoverability, encouraging deeper catalog exploration. The growing catalog of multilingual, multi-genre on-demand titles continues attracting new subscribers, reinforcing the non-linear segment's commanding position within India's video streaming market.

Revenue Model Insights:

- Subscription

- Transactional

- Advertisement

- Hybrid

The advertisement dominates with a market share of 48.0% of the total India video streaming market in 2025.

The advertisement-based video-on-demand model thrives in India's price-sensitive consumer environment, offering viewers unrestricted access to extensive content libraries without subscription commitments. Brands recognize the significant reach potential of streaming platforms that attract diverse, digitally engaged audiences, making programmatic and targeted advertising highly valuable. The capacity to deliver personalized ad experiences based on viewer demographics, preferences, and behavioral patterns enhances campaign effectiveness, positioning streaming platforms as compelling alternatives to traditional television advertising channels for marketers seeking measurable outcomes.

The advertisement revenue model extends platform accessibility to audiences in tier-2 and tier-3 cities where subscription willingness remains comparatively lower, expanding total addressable reach for both platforms and advertisers simultaneously. Evolving technologies in ad insertion, viewability measurement, and fraud prevention are progressively improving advertiser confidence in digital video investments. As brands increasingly allocate budgets toward connected television and mobile streaming, the advertising revenue segment is positioned to maintain its commanding presence, supporting broader viewer acquisition and platform monetization strategies.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Personal

- Commercial

The personal leads with a share of 85.0% of the total India video streaming market in 2025.

The personal end-user segment dominates India's video streaming landscape as individual consumers constitute the primary audience for entertainment, sports, educational, and lifestyle content. Rising smartphone ownership, affordable data tariffs, and expanding streaming platform catalogues have significantly lowered barriers to personal consumption. Individual viewers increasingly access multiple streaming platforms through bundled telecom subscriptions, personal device proliferation, and family sharing plans, driving sustained subscriber growth and engagement across platforms catering to diverse personal content preferences and viewing habits.

The segment's dominance is reinforced by strong engagement among younger demographics, particularly millennials and Generation Z audiences who have developed digital-first entertainment habits. Personalized recommendation engines, social sharing features, and multi-device accessibility enhance the individual viewing experience, encouraging higher session durations and platform loyalty. As digital literacy continues improving across age groups and income levels, the personal end-user segment is expected to sustain its commanding market position, driving consistent revenue growth throughout the forecast period.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India exhibits a clear dominance with a 32.0% share of the total India video streaming market in 2025.

West and Central India's leadership in the video streaming market reflects the region's advanced digital infrastructure, high urban population density, and strong economic activity across key metropolitan centers. The presence of large professional workforces and a youthful, digitally engaged population creates ideal conditions for sustained streaming platform adoption. The region's diverse cultural entertainment preferences, spanning multiple languages and genres, support broad content demand across platform categories and revenue models, contributing to consistently high viewer engagement and monetization potential.

The region benefits from strong telecom infrastructure density and well-established smart device penetration that facilitates seamless, high-quality streaming experiences across households. An affluent urban consumer base demonstrates greater willingness to invest in premium subscription tiers while simultaneously generating significant advertising revenue through high-engagement viewing patterns. Entertainment industry activity concentrated in the region further contributes to local content production and consumption, strengthening platform engagement and reinforcing West and Central India's dominant position within the national video streaming landscape.

Market Dynamics:

Growth Drivers:

Why is the India Video Streaming Market Growing?

Rapid Smartphone Penetration and Affordable Data Access

India's video streaming market is fundamentally underpinned by the extraordinary proliferation of smartphones across diverse socioeconomic and geographic segments. The widespread availability of affordable mobile devices compatible with high-quality video streaming has transformed access to digital entertainment, making it accessible to consumers across metropolitan cities, tier-2 towns, and rural communities alike. In 2025, leading Indian telecom operator Reliance Jio introduced a new prepaid data plan priced at ₹195 that included 15 GB of high‑speed data along with a complimentary JioHotstar subscription, making mobile streaming more accessible and affordable for price‑sensitive users. Mobile internet plans have become substantially more accessible in terms of cost, enabling large portions of the population to consume high-definition streaming content regularly. Telecom operators offering bundled streaming service packages within their mobile data plans further accelerate the organic acquisition of new streaming audiences. As smartphone technology continues advancing while device affordability improves, mobile-first content consumption is expected to remain the dominant mode of platform engagement, sustaining strong market expansion momentum.

Growing Demand for Regional and Multilingual Content

The diversity of India's linguistic and cultural landscape presents a unique growth driver for the video streaming market, as platforms increasingly invest in developing extensive multilingual content libraries to serve audiences beyond the traditional Hindi-speaking demographic. Recently, Tata Play Binge expanded its OTT portfolio by integrating two new regional entertainment platforms, Ultra Play and Ultra Jhakaas, into its aggregation service, reinforcing its commitment to broadening regional content offerings across languages and genres. The strategic expansion of content in regional languages reflects platforms' recognition that untapped viewer populations in linguistically distinct states represent enormous growth potential. Investment in original regional productions, dubbed content, and localized user interfaces is enabling platforms to penetrate markets that were previously underserved by mainstream entertainment options. The resonance of culturally authentic storytelling with local audiences creates high viewer engagement and loyalty, encouraging sustained subscription retention and reducing churn. This content-driven inclusivity strategy is expanding the total addressable market while simultaneously enriching the diversity of the India video streaming ecosystem.

Increasing Integration with Telecom and Digital Ecosystems

Strategic partnerships between video streaming platforms and telecommunications operators represent a powerful growth driver, expanding platform reach while reducing consumer acquisition costs. In January 2026, newly launched OTT platform Times Play significantly widened its distribution footprint by integrating with major telecom-led OTT bundles and aggregator services, including JioTV+, Airtel Xstream Play, Vi Movies & TV, Tata Play Binge, and OTTplay, enabling seamless access to its content through existing digital ecosystems and subscriber bases. Bundled digital service offerings that combine mobile data plans with streaming access have substantially lowered barriers to entry, particularly for cost-sensitive consumer segments. The integration of streaming capabilities within smart television operating systems, connected streaming devices, and gaming consoles further embeds video platforms within India's expanding connected home ecosystem. Growing investment in digital payment infrastructure and the progressive rollout of broadband connectivity to previously underserved geographies are enabling platforms to reach and monetize large new user segments. These ecosystem-level dynamics collectively accelerate subscriber acquisition, enhance revenue model diversification, and strengthen the long-term structural growth of India's video streaming market.

Market Restraints:

What Challenges the India Video Streaming Market is Facing?

Content Licensing and Rights Fragmentation

The complexity of content licensing and intellectual property rights in India's video streaming market presents a significant operational challenge for platforms. Fragmented rights ownership, regional licensing restrictions, and evolving regulatory frameworks around digital content distribution create barriers to assembling comprehensive content libraries. Negotiating licensing agreements across multiple rights holders for diverse content categories demands significant financial and administrative resources, constraining smaller platforms and complicating content strategy planning for established players.

Digital Infrastructure Disparities Across Regions

Despite significant progress in national digital infrastructure development, meaningful connectivity disparities persist between urban centers and rural or semi-urban areas across India. Inconsistent broadband speeds, limited network coverage in remote regions, and unreliable power supply in certain geographies impede streaming quality and limit platform accessibility for large population segments. These infrastructure gaps restrict market penetration in potentially high-volume underserved markets, moderating the overall pace of streaming adoption.

Intense Competition and Subscriber Retention Challenges

India's video streaming landscape is characterized by exceptionally intense competition among numerous domestic and international platforms competing for a shared subscriber base. The proliferation of available platforms creates content fragmentation, where audiences distribute attention and subscription budgets across multiple services simultaneously. High churn rates driven by subscription fatigue, price sensitivity, and the seasonal consumption of specific content releases challenge platforms in sustaining consistent subscriber growth and monetizing user bases effectively over the long term.

Competitive Landscape:

The India video streaming market is characterized by dynamic and intensifying competition as both domestic and international platforms actively expand their footprints across content categories, regional languages, and distribution channels. Market participants are differentiating through substantial investments in original content production, exclusive sports broadcasting rights, and innovative technology deployment including artificial intelligence-driven recommendations and interactive viewing features. The competitive environment is further shaped by the strategic evolution of distribution models, with platforms experimenting across subscription, advertising, and hybrid monetization approaches to optimize revenue capture and audience penetration. Partnerships with telecommunications operators, device manufacturers, and content creators are emerging as critical competitive tools, enabling platforms to broaden distribution reach while reducing subscriber acquisition costs. As the market matures, competitive dynamics increasingly favor platforms with the deepest content libraries, strongest brand recognition, and most sophisticated user experience capabilities.

Recent Developments:

- In March 2026, Tata Play Binge expanded to VIDAA‑powered smart TVs in India, broadening access beyond mobile devices. The platform also launched “Shots”, a hub for short-form vertical dramas. Meanwhile, Stingray entered India via JioTV, introducing 13 FAST (ad-supported) video and music channels for wider international content reach.

India Video Streaming Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Streaming Types Covered | Live/Linear Video Streaming, Non-Linear Video Streaming |

| Revenue Models Covered | Subscription, Transactional, Advertisement, Hybrid |

| End Users Covered | Personal, Commercial |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Video Streaming Market Report

The India video streaming market size was valued at USD 4.76 Billion in 2025.

The India video streaming market is expected to grow at a compound annual growth rate of 10.34% from 2026-2034 to reach USD 12.80 Billion by 2034.

Solution holds the largest component share of 72.0%, enabling seamless content delivery, platform personalization, and scalable streaming operations that define competitive positioning across India's digital entertainment landscape.

Key factors driving the India video streaming market include rising smartphone adoption, affordable mobile data access, growing regional language content demand, telecom bundling strategies, and expanding digital payment infrastructure enabling diverse monetization models.

Major challenges include content licensing fragmentation, digital infrastructure disparities across regions, intense platform competition driving high subscriber churn, price sensitivity among cost-conscious consumer segments, and regulatory complexities around digital content distribution.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)