India Warehouse Automation Market Size, Share, Trends and Forecast by Component, End User, and Region, 2026-2034

India Warehouse Automation Market Summary:

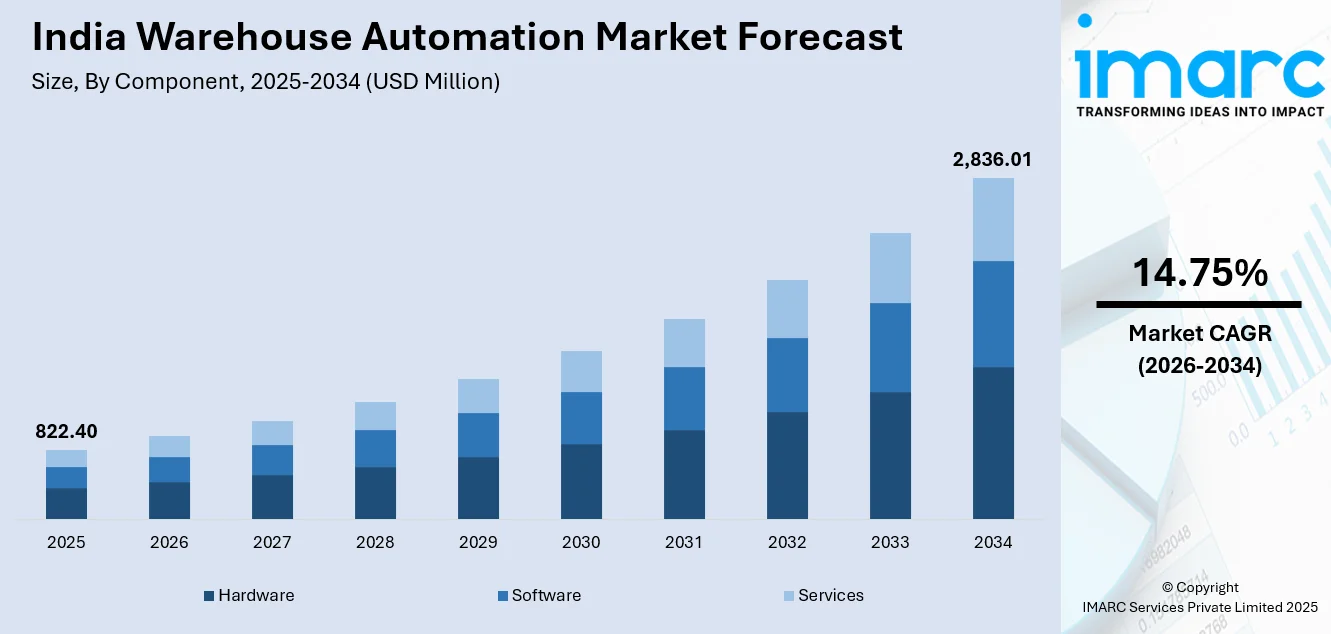

The India warehouse automation market size was valued at USD 822.40 Million in 2025 and is projected to reach USD 2,836.01 Million by 2034, growing at a compound annual growth rate of 14.75% from 2026-2034.

The India warehouse automation market is experiencing robust growth as businesses prioritize supply chain modernization and operational efficiency. Rising e-commerce penetration, increasing demand for faster order fulfillment, and the need for accurate inventory management are transforming warehousing operations. Organizations are embracing automation technologies to reduce labor dependencies, minimize errors, and enhance throughput capabilities, positioning India as a promising market for advanced logistics solutions.

Key Takeaways and Insights:

-

By Component: Hardware dominates the market with a share of 49% in 2025, driven by substantial investments in robotic systems, automated storage solutions, and conveyor technologies that form the physical backbone of modern warehouse infrastructure across India.

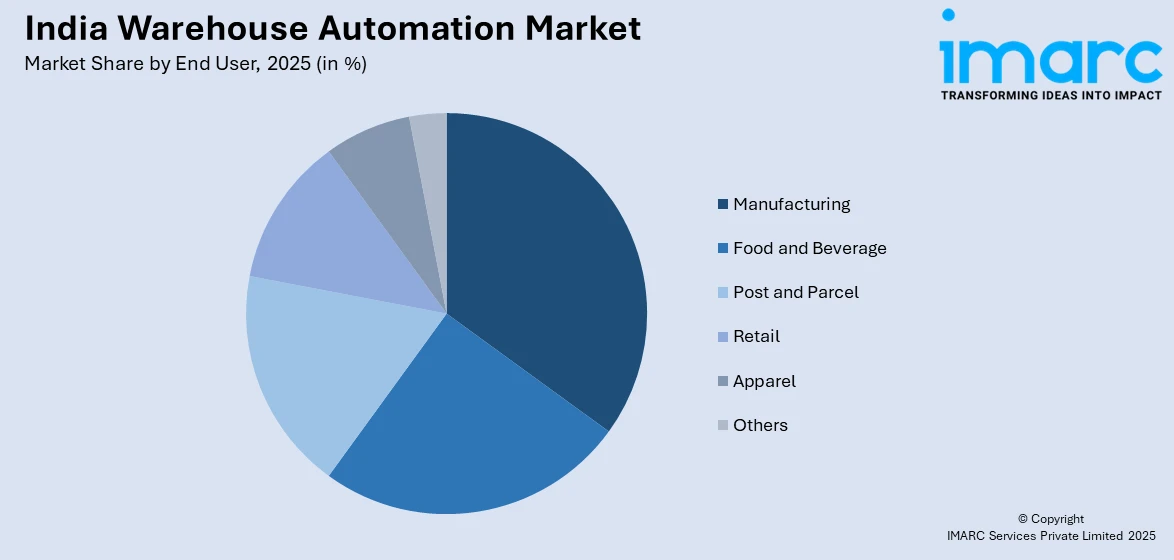

- By End User: Manufacturing leads the market with a share of 25% in 2025, reflecting the sector's growing reliance on automated material handling, just-in-time inventory practices, and streamlined production workflows to maintain competitive advantage in domestic and export markets.

- By Region: North India represents the largest segment with a market share of 30% in 2025, supported by established industrial corridors, major logistics hubs in the National Capital Region, and proximity to key consumption centers driving automation adoption.

- Key Players: The India warehouse automation market features a competitive landscape with established global technology providers competing alongside domestic integrators. Market participants are expanding their service portfolios, forming strategic partnerships, and developing customized solutions tailored to diverse industry requirements and operational scales.

To get more information on this market Request Sample

The India warehouse automation market is advancing rapidly as digital transformation reshapes logistics and supply chain operations nationwide. Growing consumer expectations for faster deliveries, expanding organized retail networks, and increasing adoption of omnichannel distribution strategies are compelling businesses to modernize their warehousing infrastructure. In September 2025, Waaree Sustainable Finance announced a strategic investment in Warehouse Now, one of India’s fastest‑growing tech‑driven warehousing and supply chain companies, highlighting rising capital flow into technologically enabled logistics platforms across the country. The integration of advanced technologies including autonomous mobile robots, automated storage and retrieval systems, and intelligent sorting solutions is enabling unprecedented levels of operational precision and scalability. Government initiatives supporting manufacturing growth and infrastructure development are creating favorable conditions for automation investments. Additionally, the rising cost of labor, emphasis on workplace safety, and need for real-time inventory visibility are accelerating the transition toward fully automated and semi-automated warehouse environments across diverse industry verticals.

India Warehouse Automation Market Trends:

Integration of Artificial Intelligence and Machine Learning

Warehouse operators across India are increasingly integrating artificial intelligence and machine learning capabilities into their automation systems. In 2025, Indian IT services firm HCLTech expanded its partnership with SAP to co‑develop “Physical AI” solutions specifically aimed at enhancing warehouse automation, including AI‑driven tools for automated picking and sorting to boost operational efficiency and accuracy. These intelligent technologies enable predictive analytics for demand forecasting, dynamic inventory optimization, and adaptive workflow management. AI-powered solutions are enhancing decision-making processes, enabling warehouses to respond proactively to demand fluctuations and optimize resource allocation.

Rise of Goods-to-Person Fulfillment Systems

The adoption of goods-to-person fulfillment systems is gaining significant traction in Indian warehouses. This approach brings products directly to workers using autonomous mobile robots and automated storage systems, dramatically reducing travel time and improving picking accuracy. In 2025, Indian automation provider Falcon Autotech reported that its advanced goods‑to‑person (GTP) system achieved up to 650 units per station per hour in a major retailer’s distribution center, significantly boosting fulfillment speed and space utilization in real Indian operations. Organizations are implementing these solutions to address labor productivity challenges while meeting increasing throughput requirements.

Expansion of Dark Warehouse Concepts

Dark or lights-out warehouse concepts are emerging as a transformative trend in the Indian market. These fully automated facilities operate with minimal human intervention, relying entirely on robotics and automation for storage, retrieval, and order processing. In August 2024, Ola Electric announced plans to deploy portable robotic “dark stores” designed to automate warehousing and fulfilment operations within India’s quick commerce ecosystem, a move aimed at reducing human labour reliance and enhancing order processing speed. Businesses are exploring dark warehouse models to achieve continuous operations, reduce energy costs, and maximize space utilization.

Market Outlook 2026-2034:

The prospects for a warehouse automation market in India remain extremely positive with continued focus on efficiency and effective supply chain management practices in industries. The growing e-commerce sector, rising demand for cold logistics chains in distribution planning, and a greater need for environmentally savvy logistics practices are likely to fuel a rapidly increased interest in automation technologies in this sector. The coming period may also see a surge in acceptance in secondand third-tier cities with increased availability in a larger geographic spread of warehousing facilities. The market generated a revenue of USD 822.40 Million in 2025 and is projected to reach a revenue of USD 2,836.01 Million by 2034, growing at a compound annual growth rate of 14.75% from 2026-2034.

India Warehouse Automation Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Hardware |

49% |

|

End User |

Manufacturing |

25% |

|

Region |

North India |

30% |

Component Insights:

- Hardware

- Mobile Robots (AGV, AMR)

- Automated Storage and Retrieval Systems (AS/RS)

- Automated Conveyor and Sorting Systems

- De-palletizing/Palletizing Systems

- Automatic Identification and Data Collection (AIDC)

- Piece Picking Robots

- Software

- Warehouse Management Systems (WMS)

- Warehouse Execution Systems (WES)

- Services

- Value Added Services

- Maintenance

The hardware dominates with a market share of 49% of the total India warehouse automation market in 2025.

The hardware segments dominance stems from the fundamental requirement for physical automation equipment including mobile robots, automated storage and retrieval systems, conveyor networks, and robotic picking solutions. Indian businesses are making substantial capital investments in hardware infrastructure to modernize legacy warehouses and establish new automated distribution centers capable of handling increasing order volumes. For example, Addverb Technologies, one of India’s leading robotics manufacturers, operates one of the world’s largest warehouse robotics production facilities at its Greater Noida “Bot‑Verse” campus, with the capacity to manufacture autonomous robots annually to meet surging demand.

The growing emphasis on operational efficiency and accuracy is compelling organizations to deploy sophisticated hardware solutions that can operate continuously without fatigue. Automated guided vehicles and autonomous mobile robots are transforming material movement within warehouses, while advanced sorting systems are enabling rapid order processing. The expansion of e-commerce fulfillment centers and the modernization of manufacturing supply chains are primary drivers sustaining hardware investment momentum across the country.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverage

- Post and Parcel

- Retail

- Apparel

- Manufacturing

- Others

The manufacturing leads with a share of 25% of the total India warehouse automation market in 2025.

The manufacturing sector holds the largest end-user share in the India warehouse automation market, driven by the sector's critical need for precise inventory control and seamless production line integration. Manufacturing facilities are deploying automation technologies to manage raw material storage, work-in-progress inventory, and finished goods distribution with enhanced accuracy and speed. The emphasis on lean manufacturing principles and just-in-time delivery requirements is accelerating automation adoption.

Indian manufacturers are increasingly recognizing automation as essential infrastructure for maintaining competitiveness in both domestic and export markets. Automated warehousing solutions enable manufacturers to optimize storage space utilization, reduce inventory carrying costs, and improve order fulfillment responsiveness. The government's manufacturing promotion initiatives and the growing presence of multinational production facilities are further stimulating demand for sophisticated warehouse automation systems within this sector.

Regional Insights:

- North India

- South India

- East India

- West India

North India exhibits a clear dominance with a 30% share of the total India warehouse automation market in 2025.

North India commands the largest regional share of the India warehouse automation market, supported by the strategic concentration of logistics infrastructure in the National Capital Region and surrounding industrial corridors. The region benefits from established connectivity networks, proximity to major consumption markets, and the presence of dedicated freight corridors enhancing supply chain efficiency. The concentration of e-commerce fulfillment operations and organized retail distribution centers drives sustained automation investments.

The development of industrial townships and logistics parks across states including Haryana, Uttar Pradesh, and Punjab is creating new opportunities for warehouse automation deployment. North India's strategic position as a gateway to central Asian markets and its well-developed road and rail networks make it an attractive location for automated distribution facilities. Continued infrastructure development and favorable state policies are expected to reinforce the region's leadership position in warehouse automation adoption.

Market Dynamics:

Growth Drivers:

Why is the India Warehouse Automation Market Growing?

Rapid Expansion of E-Commerce and Quick Commerce Sectors

The exponential growth of e-commerce and the emergence of quick commerce models are fundamentally transforming warehouse automation demand in India. The India e-commerce market was valued at USD 129.72 billion in 2025, highlighting the scale of digital retail growth that is driving demand for advanced warehousing solutions. Online retail platforms require fulfillment centers capable of processing thousands of orders daily with minimal turnaround times, necessitating sophisticated automation solutions. The proliferation of same-day and instant delivery services is compelling logistics providers to deploy high-speed sorting systems, automated picking solutions, and intelligent inventory management technologies. Consumer expectations for rapid order fulfillment are driving investments in micro-fulfillment centers positioned closer to urban populations. The continuous expansion of online shopping penetration across tier-two and tier-three cities is creating new requirements for automated warehousing infrastructure beyond metropolitan regions, extending the market's geographical footprint substantially.

Government Initiatives Supporting Logistics Infrastructure Modernization

Government programs and policy frameworks focused on logistics infrastructure development are creating favorable conditions for warehouse automation investment. National logistics policies emphasizing efficiency improvements, cost reduction, and technology adoption are encouraging businesses to modernize their warehousing operations. For example, under the National Logistics Policy and Logistics Efficiency Enhancement Programme (LEEP), the government has approved the development of 35 Multi‑Modal Logistics Parks (MMLPs) at strategic locations across the country, hubs designed to integrate modern warehousing, freight handling, and multimodal connectivity, directly supporting automated supply chain ecosystems. Initiatives promoting manufacturing competitiveness and export growth are stimulating demand for automated solutions that enhance supply chain responsiveness and accuracy. The development of dedicated freight corridors, multimodal logistics parks, and free trade warehousing zones is establishing modern infrastructure where automation technologies can be effectively deployed. Tax incentives for technology adoption and depreciation benefits for automation equipment are improving investment economics, making automated warehousing solutions more accessible to a broader range of businesses across various industry sectors.

Rising Labor Costs and Workforce Availability Challenges

Increasing labor costs and difficulties in recruiting and retaining warehouse workers are compelling businesses to accelerate automation investments. The physically demanding nature of warehouse work, combined with rising wage expectations and high attrition rates, is making automation an economically attractive alternative to labor-intensive operations. For instance, Flipkart’s deployment of over 100 autonomous guided vehicles (AGVs) at its Bengaluru sortation centre has enabled robots to sort around 5,000 parcels per hour, more than 10 times the throughput of manual sorting, significantly reducing the workload on human staff. Organizations are recognizing that automated systems can operate continuously without fatigue, maintaining consistent productivity levels regardless of shifts or seasons. Workplace safety considerations and the desire to reduce repetitive strain injuries are further motivating the transition toward automated material handling solutions. The challenge of scaling workforce capacity during peak demand periods such as festive seasons is driving adoption of flexible automation technologies that can handle volume fluctuations without proportional labor increases, improving operational resilience and cost predictability.

Market Restraints:

What Challenges the India Warehouse Automation Market is Facing?

High Initial Capital Investment Requirements

The substantial upfront capital required for implementing comprehensive warehouse automation systems presents a significant barrier for many Indian businesses. Small and medium enterprises often struggle to justify large initial investments despite potential long-term operational savings. The need for specialized infrastructure modifications, integration services, and extended implementation timelines further increases project costs, limiting adoption among budget-constrained organizations.

Technical Expertise and Skilled Workforce Shortage

The shortage of technical personnel capable of implementing, operating, and maintaining sophisticated automation systems poses challenges for market expansion. Warehouses require skilled technicians, automation engineers, and system integrators who understand both mechanical and software components. The limited availability of trained professionals increases operational risks and maintenance costs, particularly for organizations operating outside major metropolitan areas.

Integration Complexity with Legacy Systems

Integrating modern automation technologies with existing warehouse management systems and enterprise software presents technical challenges that can delay implementation and increase costs. Many Indian warehouses operate legacy systems that lack standardized interfaces for seamless automation connectivity. The complexity of achieving interoperability between diverse equipment vendors and software platforms requires extensive customization, potentially compromising system reliability and performance optimization.

Competitive Landscape:

The warehouse automation industry in the Indian market is portrayed as having a challenging competitive landscape, with established global technology suppliers competing with new Indian solution integrators. Complimentary approaches, including technological, support, and adaptability, are being adopted by market participants as a measure of differentiation. Strategic alliances between global automated solution providers and Indian system integrators are opening up avenues for efficient market entry as well as expanding the reach of customers. The strategy of providing end-to-end solutions, from design through implementation into support, is gaining prominence as a key component of competitiveness for market leaders. Infrastructure development for demonstration purposes, as well as pilot solutions, is being pursued by industry leaders as a means of showcasing automated solutions and allaying customer fears regarding implementation feasibility. Scalability, as an emerging trend, is becoming prominent with the requirement for flexible automated solutions pathways being emphasized by industry leaders.

Recent Developments:

- In January 2026, Pune-based warehouse automation startup Unbox Robotics raised $28 million in a funding round led by ICICI Venture, with participation from RedStart Labs and others. The capital will boost product development, expand engineering teams, and scale operations across India, Europe, and the U.S.

India Warehouse Automation Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| End Users Covered | Food and Beverage, Post and Parcel, Retail, Apparel, Manufacturing, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Warehouse Automation Market Report

The India warehouse automation market size was valued at USD 822.40 Million in 2025.

The India warehouse automation market is expected to grow at a compound annual growth rate of 14.75% from 2026-2034 to reach USD 2,836.01 Million by 2034.

Hardware holds the largest component share at 49%, driven by substantial investments in robotic systems, automated storage solutions, conveyor technologies, and sorting systems that form the essential infrastructure of automated warehouse operations.

Key factors driving the India warehouse automation market include rapid e-commerce expansion, government logistics infrastructure initiatives, rising labor costs, increasing emphasis on operational efficiency, growing cold chain requirements, and technological advancements in robotics and artificial intelligence.

Major challenges include high initial capital investment requirements, shortage of skilled technical personnel, integration complexity with legacy systems, infrastructure limitations in certain regions, and the need for customized solutions across diverse industry applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)