India Waste Management Market Size, Share, Trends and Forecast by Waste Type, Disposal Methods, and Region, 2026-2034

India Waste Management Market Summary:

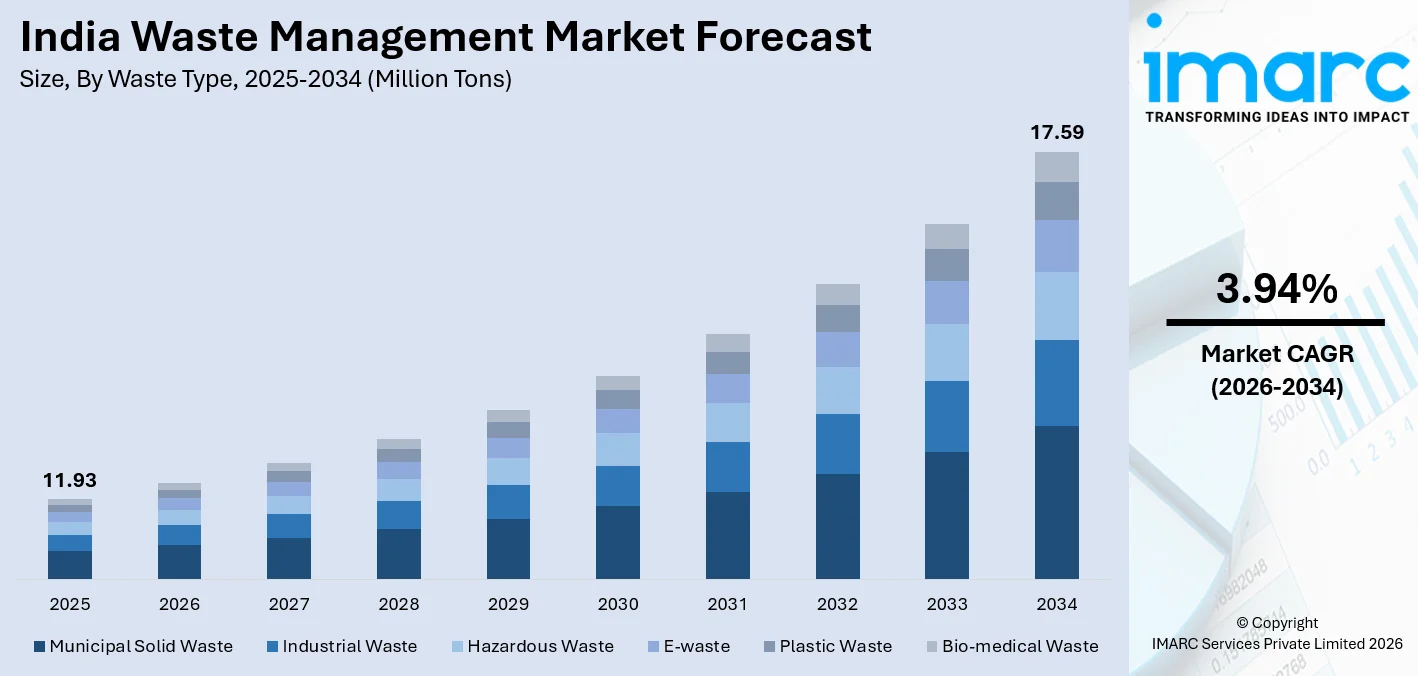

The India waste management market size reached 11.93 Million Tons in 2025 and is projected to reach 17.59 Million Tons by 2034, growing at a compound annual growth rate of 3.94% from 2026-2034.

India's waste management sector is undergoing a significant transformation, driven by rapid urbanization, expanding regulatory frameworks, and a growing emphasis on sustainable waste practices. Government-led initiatives promoting clean cities, combined with rising public awareness and growing private sector participation, are fundamentally reshaping how waste is collected, processed, and disposed of across the country. These combined forces are continuously strengthening the India waste management market share.

Key Takeaways and Insights:

- By Waste Type: Municipal solid waste dominates the market with a share of 57.3% in 2025, driven by rapid urbanization, growing urban populations, and the substantial volumes of residential and commercial waste generated daily across India's expanding metropolitan and tier-2 cities.

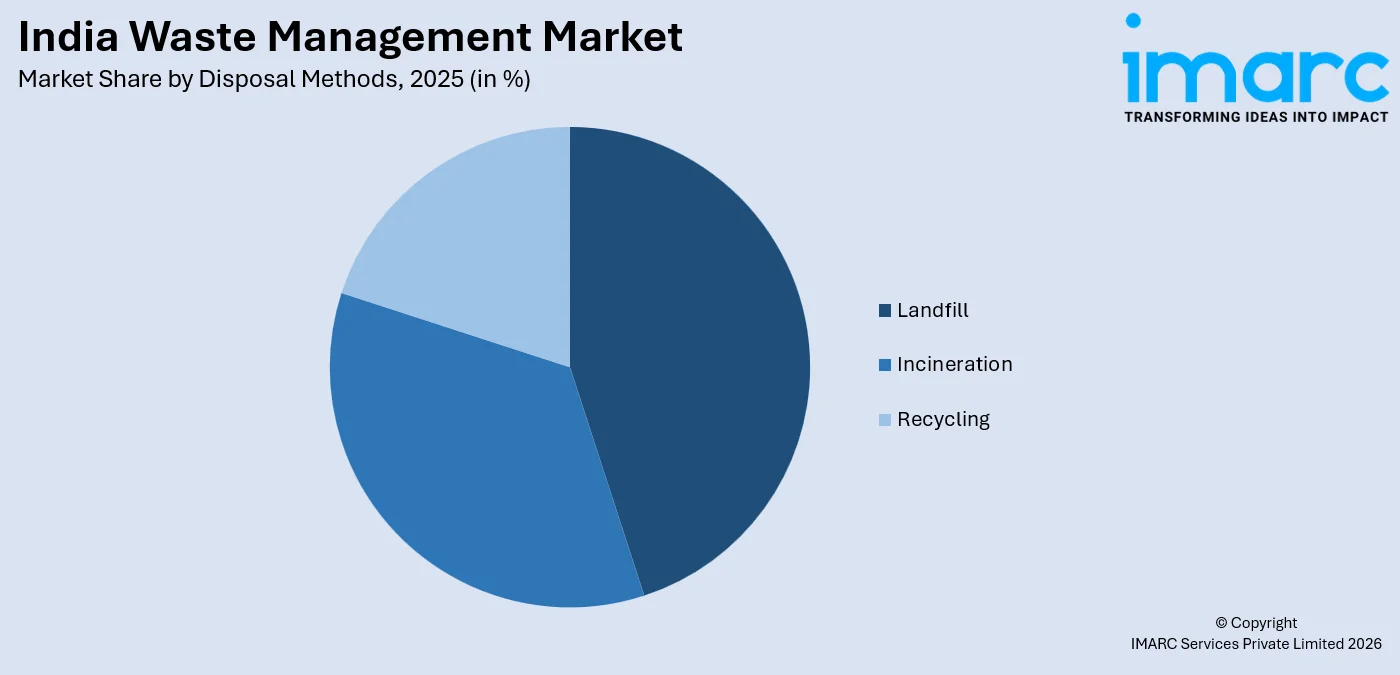

- By Disposal Methods: Landfill leads the market with a share of 44.0% in 2025, reflecting the widespread reliance on land-based disposal as the primary method for managing the large volumes of untreated and mixed waste across India's urban and semi-urban regions.

- By Region: West India represents the largest regional segment with a market share of 26.8% in 2025, supported by higher urbanization rates, stronger industrial activity, and more established waste management infrastructure across Maharashtra, Gujarat, and Madhya Pradesh.

- Key Players: The India waste management market features a moderately competitive structure, with domestic operators and international service providers competing across collection, processing, and disposal segments within an increasingly regulated environment.

To get more information on this market Request Sample

The India waste management market is characterized by a diverse waste stream composition and an evolving regulatory landscape that is progressively shifting the sector toward sustainable practices. The country generates approximately 62 million tonnes of municipal solid waste annually, with only a fraction undergoing formal treatment before disposal. Urban local bodies serve as primary service providers, though capacity and technical capabilities vary significantly across regions. Government-driven programs such as the Swachh Bharat Mission and the GOBARdhan scheme have catalyzed investment in waste processing infrastructure, while Extended Producer Responsibility regulations are compelling industry participants to adopt more structured approaches. The growing adoption of waste-to-energy technologies, particularly in metropolitan centers, is adding a new dimension to the sector. For instance, in July 2024, the Asian Development Bank signed a USD 200 million loan agreement with the Government of India to enhance solid waste management across 100 cities under the Swachh Bharat Mission 2.0, underscoring the scale of institutional commitment to strengthening India's waste management market.

India Waste Management Market Trends:

Accelerating Adoption of Waste-to-Energy Technologies

India is rapidly expanding its waste-to-energy infrastructure, driven by the need to reduce landfill pressure and support renewable energy goals. Government initiatives are promoting the development of waste-to-electricity and biomethanation facilities across states, thereby fostering sustainable energy generation from municipal and organic waste and strengthening the country’s integrated waste management ecosystem. For instance, in March 2025, Indore launched India's first PPP-based green waste processing plant under this mission, converting green waste into sawdust and wooden pellets, demonstrating the expanding scope of renewable applications in urban waste management.

Strengthening Extended Producer Responsibility Frameworks

India's EPR regime has been significantly expanded and tightened, placing lifecycle accountability on producers across electronics, plastic, battery, and packaging waste streams. Under the E-Waste Management Rules 2022, producers must meet escalating recycling targets reaching 70% for FY 2025-26 and 2026-27. The government has updated regulations to strengthen Extended Producer Responsibility (EPR) frameworks for e-waste, plastics, and batteries by standardizing certificate pricing and improving market mechanisms. Additionally, new draft rules are expanding EPR accountability to include packaging waste, broadening formal producer responsibility across more waste streams and promoting structured, compliant waste management practices.

Digital Transformation and Smart Waste Management

Digital technologies including IoT-enabled smart bins, GPS-tracked collection fleet management, and AI-powered operational monitoring are increasingly being integrated into India's waste management operations to improve efficiency and regulatory compliance. In September 2025, international operators launched digital platforms designed specifically to optimize collection routes and enhance operational efficiency. This digital initiative aligns with India’s Smart Cities Mission, which emphasizes technology-enabled urban services. Urban local bodies are increasingly using data-driven systems to monitor and optimize waste management performance, demonstrating the growing adoption of digital governance across the sector.

Market Outlook 2026-2034:

India’s waste management sector is set for steady growth, driven by stricter regulations, rising urban waste generation, and increasing investment in formal collection and processing infrastructure. Recent legislative developments are introducing a comprehensive statutory framework for waste segregation, recycling, and disposal, marking a significant shift toward structured governance and accountability in the sector. These initiatives are encouraging greater compliance among municipalities and private operators, fostering the adoption of advanced waste processing technologies, and supporting the development of integrated waste management systems that enhance efficiency, environmental sustainability, and resource recovery across urban and semi-urban regions. The market reached a volume of 11.93 Million Tons in 2025 and is projected to reach 17.59 Million Tons by 2034, growing at a compound annual growth rate of 3.94% from 2026-2034.

India Waste Management Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Waste Type |

Municipal Solid Waste |

57.3% |

|

Disposal Methods |

Landfill |

44.0% |

|

Region |

West India |

26.8% |

Waste Type Insights:

- Industrial Waste

- Municipal Solid Waste

- Hazardous Waste

- E-waste

- Plastic Waste

- Bio-medical Waste

Municipal solid waste dominates with a market share of 57.3% of the total India waste management market in 2025.

Municipal solid waste represents the dominant category in India's waste management landscape, driven by the country's rapid urbanization and a growing urban middle class with increasing consumption levels. Urban centers in India produce substantial volumes of municipal solid waste from households, businesses, and institutions. This growing waste stream presents both challenges and opportunities for organized waste management companies, as cities invest in expanding collection networks and developing processing and recycling facilities to comply with regulations and improve efficiency across the sector. The Swachh Bharat Mission's urban component links central funding to verifiable waste processing outcomes, incentivizing urban local bodies to scale up MSW treatment capacity across tier-1 and tier-2 cities nationwide.

Municipal solid waste management in India has become increasingly sophisticated, with leading cities adopting source segregation protocols, composting infrastructure, and bio-methanation facilities. For instance, in 2024, the Government of India proposed revised Solid Waste Management Rules, effective October 1, 2025, mandating waste segregation, imposing penalties for non-compliance, and empowering sanitation workers with enforcement authority. These regulatory changes are accelerating the shift from open dumping toward formal processing systems. The entry of modern waste-to-energy plants, particularly across Maharashtra, Gujarat, and Madhya Pradesh, is adding value to MSW streams by converting non-recyclable fractions into electricity and bio-CNG, reducing the overall disposal burden on landfill infrastructure.

Disposal Methods Insights:

Access the comprehensive market breakdown Request Sample

- Landfill

- Incineration

- Recycling

Landfill represents the largest share of 44.0% of the India waste management market in 2025.

Landfill remains the primary method of waste disposal in India due to longstanding infrastructural practices and the challenge of managing large volumes of mixed, unsegregated waste. Many disposal sites operate informally rather than as engineered sanitary facilities. Increasing regulatory oversight is pressuring urban local bodies to adopt more scientific landfill management practices. At the same time, cities are investing in waste diversion infrastructure, including collection, segregation, and recycling systems, to reduce environmental impacts and improve compliance, fostering the gradual modernization of the country’s waste management ecosystem.

Although landfill use continues to dominate, regulatory measures are increasingly encouraging waste diversion to more sustainable alternatives. Policies now promote the redirection of high-calorific, non-recyclable waste toward energy recovery, industrial co-processing, or production of refuse-derived fuels. Public-private partnerships and dedicated waste-to-energy projects are being established to reduce landfill reliance and integrate alternative disposal methods. These initiatives reflect a growing focus on formalized, environmentally responsible waste management strategies, highlighting the momentum toward modern, efficient, and sustainable approaches across India’s urban waste infrastructure.

Regional Insights:

- North India

- South India

- East India

- West India

West India leads with a market share of 26.8% of the total India waste management market in 2025.

West India's leadership in the national waste management market reflects the region's high urban density, industrialized economic base, and relatively more advanced waste management infrastructure. Maharashtra, Gujarat, and Madhya Pradesh, the major contributors within this zone, collectively account for a substantial share of India's urban waste generation and formal waste processing capacity. Maharashtra hosts some of the country's largest urban agglomerations, including Mumbai and Pune, whose municipal waste volumes necessitate extensive collection and disposal systems. In 2024, Gujarat's largest waste-to-energy plant in Ahmedabad commenced processing 1,000 metric tons of waste daily to generate 15 megawatts of electricity, developed in collaboration with Jindal Urban Waste Management.

The waste management industry in the region is supported by the aggressive state-level policies and a concentration of experienced operators. Tough segregation requirements in Maharashtra and regular high scores in the urban cleanliness surveys in Gujarat are indicators of high-level regulatory compliance. Such cities as Indore are the national examples, as they have large-scale organic waste processing plants that turn biodegradable waste into energy and compost. These initiatives are beneficial because they minimize negative environmental effects and greenhouse gases, as well as encourage sustainable farming and resource reuse, and make the region a significant leader in terms of introducing effective, integrated, and environmentally sustainable waste management.

Market Dynamics:

Growth Drivers:

Why is the India Waste Management Market Growing?

Rapid Urbanization and Rising Waste Generation Volumes

India's urban population is expanding at an exceptional pace, with projections indicating that urban areas will generate approximately 165 million tonnes of municipal solid waste annually by 2030, compared to 62 million tonnes currently. This trajectory fundamentally drives demand for organized waste collection, treatment, and disposal services. Urban areas now contribute over 60% of the country's total waste generation, concentrated in tier-1 and tier-2 cities that are simultaneously experiencing infrastructure expansion. Urban India produces substantial volumes of municipal solid waste, creating a significant gap between generation and formal treatment capacity. This gap presents a key market opportunity, driving local authorities and private operators to expand and modernize waste collection, processing, and disposal infrastructure to improve efficiency, compliance, and environmental sustainability across cities. This urbanization-driven growth in waste volumes remains the primary structural driver sustaining the expansion of India's waste management market across the forecast period.

Government Policy Initiatives and Regulatory Mandates

The waste management industry in India has been revolutionized by a sound mechanism of government programs and regulatory frameworks that have not only brought about compliance needs but also investment potential. The Swachh Bharat mission urban programs encourage the process of legacy dump site remediation and the creation of viable waste management plants. Complementary schemes, such as GOBARdhan, are converting organic and agricultural waste into renewable energy and compost, while legislative measures like the Solid Waste Management Bill reinforce formal governance and accountability. Together, these initiatives are fostering a structured, sustainable, and technologically advanced waste management ecosystem across urban and rural India.

Expanding Extended Producer Responsibility and Circular Economy Imperatives

The growth of Extended Producer Responsibility (EPR) by India in e-waste, plastics, batteries, and packaging is creating an intense demand for formal waste collection and recycling infrastructure. The manufacturers must comply with the increasing recycling requirements and promote the establishment of collection systems and licensed processing plants. Recent policies make packaging materials accountable and introduce the concept of traceability, which will promote a systematic cyclic economy. As the number of registered processors continues to rise and the amounts of waste being handled through EPR systems continue to increase, the organized waste management sector in India is expanding at an astute pace and empowering the recycling and recovery of resources sustainably throughout the nation.

Market Restraints:

What Challenges the India Waste Management Market is Facing?

Inadequate Infrastructure Across Urban Local Bodies

Many urban local bodies in India still lack sufficient waste processing facilities, including segregation and dedicated sorting centers. This fragmented infrastructure limits treatment capacity, resulting in ongoing reliance on informal dumpsites and open landfills. The gap in organized waste management hampers efforts to implement sustainable practices and delays the transition toward formal, environmentally responsible waste handling across municipalities.

High Capital and Operational Costs

Implementing advanced waste management systems requires substantial capital investment and specialized equipment, making large-scale adoption challenging for smaller municipalities. Operational expenses, including skilled labor and maintenance, further increase costs, limiting the deployment of modern waste collection, sorting, and processing technologies. These financial constraints hinder compliance with evolving regulatory standards and slow the modernization of the waste management ecosystem.

Enforcement Gaps and Regulatory Compliance Challenges

Despite strengthened regulations, enforcement of waste management rules remains inconsistent across urban jurisdictions. Variations in governance capacity among local bodies lead to uneven adherence to policies and hinder the monitoring of compliance. These gaps between regulatory mandates and on-ground implementation present challenges for achieving nationwide standardization and effective, verifiable enforcement of waste management practices.

Competitive Landscape:

The India waste management market features a moderately competitive structure encompassing established domestic operators, multinational service providers, and an active informal sector that continues to handle a significant share of the country's recyclable waste streams. Organized players compete based on service breadth, technology adoption, geographic reach, and public-private partnership participation. Municipal contracts remain the primary revenue avenue for large operators, while EPR compliance services, waste-to-energy project development, and digital waste monitoring solutions are emerging as differentiated growth segments. The competitive intensity is increasing as stricter regulatory requirements reward participants with broader processing capabilities and penalize informal or non-compliant operators.

Recent Developments:

- December 2025: The Solid Waste Management Bill, 2025, was introduced in the Rajya Sabha, proposing a binding statutory framework for the segregation, recycling, treatment, and disposal of municipal solid waste in India. The Bill mandates transportation of non-recyclable waste to notified landfills, regulates the use of recyclable waste in energy plants, and shifts core waste management obligations to parliamentary statute, significantly strengthening enforceability and accountability across local bodies.

- March 2025: Pune became the first city in India to implement the central government's NAMASTE scheme for waste pickers, formally recognizing waste pickers as workers and providing them with social security benefits, improved working conditions, and access to government welfare schemes. The initiative aims to integrate waste pickers into the formal solid waste management system, supporting a more inclusive and structured waste collection framework nationwide.

India Waste Management Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Waste Types Covered | Industrial Waste, Municipal Solid Waste, Hazardous Waste, E-Waste, Plastic Waste, Bio-Medical Waste |

| Disposal Methods Covered | Landfill, Incineration, Recycling |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Waste Management Market Report

The India waste management market size was valued at 11.93 Million Tons in 2025.

The India waste management market is expected to grow at a compound annual growth rate of 3.94% from 2026-2034 to reach 17.59 Million Tons by 2034.

Municipal solid waste dominated the India waste management market with a share of 57.3% in 2025, driven by rapid urbanization, high household waste generation volumes, and the expanding urban populations across India's metropolitan and tier-2 cities.

Key factors driving the India waste management market include rapid urbanization increasing waste generation volumes, government initiatives such as the Swachh Bharat Mission and GOBARdhan scheme, expanding Extended Producer Responsibility mandates, growing adoption of waste-to-energy technologies, and rising private sector investment in formal waste processing infrastructure.

Major challenges include inadequate waste processing infrastructure across urban local bodies, high capital costs for advanced waste management systems, enforcement gaps in regulatory compliance, insufficient waste segregation at source, and limited technical capacity in smaller municipalities to adopt modern waste management technologies at the pace required by evolving national mandates.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)