India Waste Plastic Recycling Market Size, Share, Trends and Forecast by Treatment, Material, Application, Recycling Process, and Region, 2026-2034

India Waste Plastic Recycling Market Size, Share, Trends & Forecast (2026-2034)

The India waste plastic recycling market reached a volume of 11.92 Million Tons in 2025 and is projected to reach 25.88 Million Tons by 2034, exhibiting a CAGR of 9.00% during 2026-2034. Accelerating Extended Producer Responsibility (EPR) enforcement, rising circular economy mandates, expanding pyrolysis and co-processing capacities, and surging end use demand across the packaging, construction, and automotive sectors are the primary forces shaping market growth.

Pyrolysis leads the treatment segment at 26.0%, packaging commands 40.0% of the application segment, and North India accounts for 27.0% of regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

11.92 Million Tons |

|

Forecast Market Size (2034) |

25.88 Million Tons |

|

CAGR (2026-2034) |

9.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (27.0%, 2025) |

|

Second Largest Region |

West and Central India (25.6%, 2025) |

|

Leading Treatment |

Pyrolysis (26.0%, 2025) |

|

Leading Application |

Packaging (40.0%, 2025) |

The India waste plastic recycling market expanded from 7.75 Million Tons in 2020 to 11.92 Million Tons in 2025, supported by rising institutional demand for recycled materials, stricter single-use plastic bans, and growing EPR compliance by FMCG and packaging firms. Anchored at 18.34 Million Tons in 2030, the forecast to 25.88 Million Tons by 2034 reflects continued capacity scale-up in pyrolysis, co-processing, and heat compression technologies, alongside deepening collaboration between urban local bodies, informal waste pickers, and formal recyclers.

To evaluate market opportunities, Request Sample

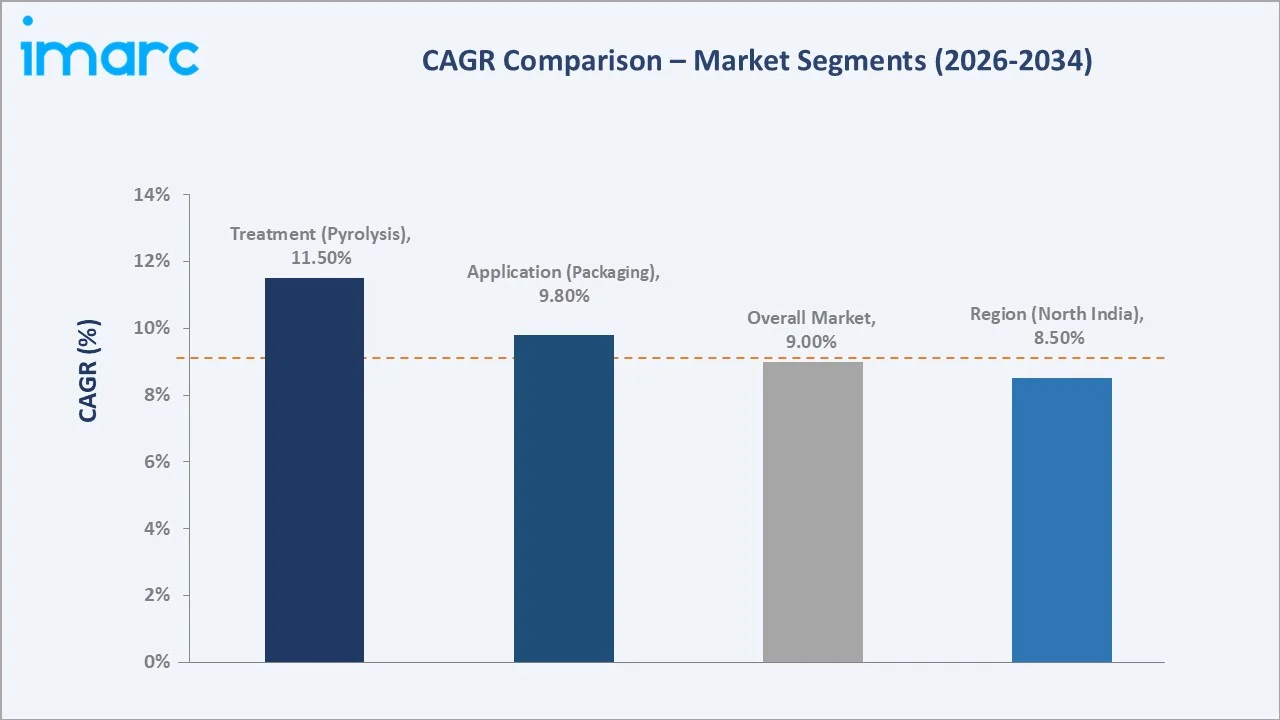

CAGR trajectories across treatment and application sub-segments reveal that pyrolysis and packaging are expanding faster than the overall 9.00% market CAGR. Packaging sector growth is driven by FMCG-led EPR targets while pyrolysis benefits from fuel oil demand and technology cost reductions.

Executive Summary

The India waste plastic recycling market is on a sustained expansion path from 7.75 Million Tons in 2020 to a projected 25.88 Million Tons by 2034. The market has moved from informally managed, open-dump-led plastic disposal toward increasingly organized, technology-enabled recycling across pyrolysis, co-processing, and mechanical processing formats. Stronger EPR regulations, urban solid waste management mandates, and rising end use demand are collectively reshaping the market's structural foundations.

Pyrolysis leads the treatment mix at 26.0% in 2025, driven by fuel-grade output demand and regulatory support for waste-to-energy pathways. Packaging commands 40.0% of the application segment as FMCG and retail brands expand use of post-consumer recycled content. North India commands 27.0% regional share, anchored by dense urban waste generation, formal collection infrastructure, and proximity to downstream manufacturing clusters. As of March 16, 2026, in Delhi, the daily production of plastic waste was approximately 1,155.7 Tons, whereas the processing capability was 939 Tons each day.

Key Market Insights

|

Insight |

Data |

|

Leading Treatment |

Pyrolysis - 26.0% share (2025) |

|

Second Largest Treatment |

Co-Processing - 20.8% share (2025) |

|

Leading Application |

Packaging - 40.0% share (2025) |

|

Second Largest Application |

Construction - 20.6% share (2025) |

|

Leading Region |

North India - 27.0% share (2025) |

|

Second Largest Region |

West and Central India - 25.6% share (2025) |

|

Top Companies |

Re Sustainability, The Shakti Plastic Industries, Gravita India Ltd., Ganesha Ecosphere Ltd. |

Key Analytical Observations Expanding on the Data Above:

- Pyrolysis leadership at 26.0% is anchored by established fuel oil offtake chains, growing investor interest in chemical recycling, and government support for waste-to-energy projects under national clean energy targets. According to the 2023-24 budget announcement, 500 new ‘Waste to Wealth’ facilities would be set up under GOBARdhan to encourage a circular economy.

- Co-processing at 20.8% benefits from cement industry adoption of refuse-derived fuel and plastic-derived fuel as coal substitutes, reducing both operational costs and carbon intensity for cement manufacturers.

- Packaging at 40.0% drives application-side demand for recycled polymers as FMCG brands and retailers pursue EPR compliance targets and sustainability commitments on post-consumer recycled content.

- Construction share at 20.6% is supported by growing use of recycled plastic in pipes, insulation materials, composite lumber, and road construction applications. Rising infrastructure development and increasing emphasis on sustainable building materials continue to expand demand for recycled polymers across the construction sector.

- North India at 27.0% leads regional share, supported by dense urban waste generation in Delhi-NCR, Uttar Pradesh, Rajasthan, and Punjab, along with well-developed informal waste collection networks.

India Waste Plastic Recycling Market Overview

Waste plastic recycling refers to the collection, sorting, processing, and conversion of discarded plastic materials into reusable raw materials or energy products. The market spans mechanical recycling, pyrolysis, co-processing with cement kilns, heat compression, incineration with energy recovery, and landfill operations, serving downstream industries including packaging, construction, textiles, and automotive.

In India, the ecosystem encompasses municipal and industrial waste generators, informal waste pickers and aggregators, material recovery facilities, EPR compliance bodies, technology providers, downstream manufacturers, and regulatory authorities at central and state levels. Together, these stakeholders constitute an evolving but increasingly formal market structure oriented around circular economy objectives.

Market Dynamics

To evaluate market opportunities, Request Sample

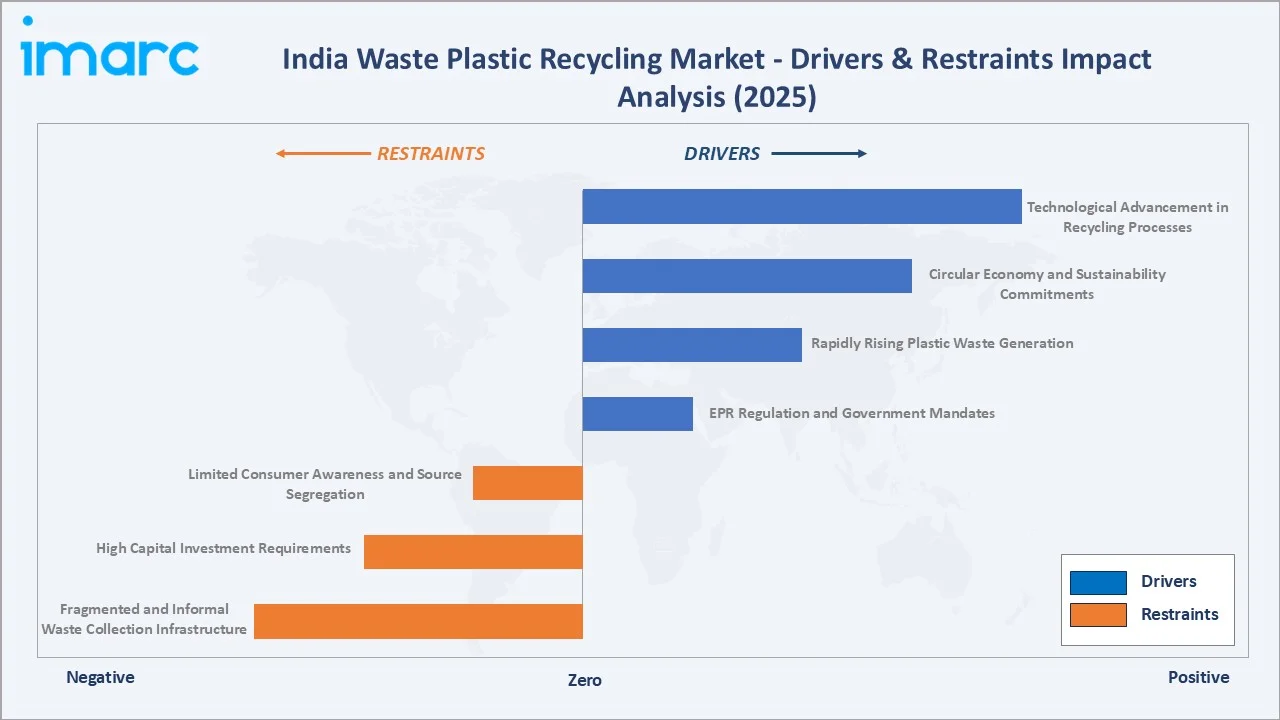

Market Drivers

- EPR Regulation and Government Mandates: Strengthening regulatory requirements for plastic waste collection, recycling, and recovery are compelling producers, importers, and brand owners to increase investment in formal recycling infrastructure. These mandates are creating sustained demand for recycled materials and improving feedstock availability across the plastic recycling value chain.

- Rapidly Rising Plastic Waste Generation: India's growing urban population, expanding FMCG consumption, and increasing use of single-use packaging are generating a steadily larger plastic waste stream, providing a durable feedstock base for recycling investments and supporting multi-year volume growth across treatment technologies. According to the Economic Survey 2023-24, it is anticipated that over 40% of India's population will inhabit urban regions by 2030.

- Circular Economy and Sustainability Commitments: Large domestic and multinational corporations operating in India are setting post-consumer recycled content targets and sustainability goals aligned with global ESG frameworks, generating stable long-term off-take commitments for recycled polymer producers and diversified recycling processors.

- Technological Advancement in Recycling Processes: Cost reductions and performance improvements in pyrolysis reactors, chemical depolymerization systems, and co-processing equipment are expanding the range of plastic types that can be economically recycled, increasing aggregate market yield and improving output quality for downstream industrial users.

Market Restraints

- Fragmented and Informal Waste Collection Infrastructure: A significant share of India's plastic waste is handled by informal waste pickers operating outside formal systems, creating inconsistency in feedstock quality, quantity, and traceability, which increases processing costs and limits the ability of formal recyclers to scale certified output.

- High Capital Investment Requirements: Advanced treatment facilities, particularly those employing pyrolysis or chemical recycling technologies, require substantial capital expenditure, which constrains entry by smaller operators and slows the pace of capacity addition relative to waste generation growth rates.

- Limited Consumer Awareness and Source Segregation: Inadequate awareness and compliance with waste segregation norms at source, particularly in tier-2 and tier-3 cities, reduces the purity and recyclability of collected plastic streams, lowering yield rates and increasing contamination management costs for formal processors.

Market Opportunities

- Waste-to-Energy and Chemical Recycling Expansion: Growing national targets for renewable energy and reduced landfill dependency are opening up investment opportunities in pyrolysis-to-fuel and plastic-to-chemical pathways, with government co-investment and private equity increasingly backing scalable chemical recycling platforms.

- Export of Recycled Polymers and Derived Products: Rising global demand for recycled-content materials in packaging, automotive, and textile applications is creating export market opportunities for Indian recyclers able to certify output quality under international standards, supporting premium pricing and improved unit economics.

Market Challenges

- Feedstock Contamination and Quality Inconsistency: Commingled plastic waste containing food residues, dyes, and multi-layer laminates reduces recycling yield, elevates sorting and washing costs, and constrains the range of end applications for recycled output, particularly in food-contact packaging.

- Policy Implementation Gaps: Uneven enforcement of EPR compliance targets and single-use plastic bans across states creates regulatory arbitrage, allowing non-compliant producers to avoid collection obligations and undermining investment confidence in formal recycling infrastructure.

Emerging Market Trends

1. Scaling of Pyrolysis and Chemical Recycling Technologies

Pyrolysis operators are progressively transitioning from small-batch, manually operated units to continuous-feed, instrumented reactors capable of processing heterogeneous plastic waste streams with higher fuel oil yield and lower residue. Improved process automation, temperature control, and feedstock handling systems are enhancing operational efficiency and enabling more consistent product quality across commercial-scale facilities.

2. EPR Marketplace and Digital Traceability Platforms

The Central Pollution Control Board's EPR portal is being scaled to enable real-time tracking of plastic waste movement from generators to processors. Digital traceability platforms are allowing brand owners to purchase EPR certificates from certified recyclers, creating a market mechanism that is channeling formal investment into the sector and improving compliance transparency across the value chain.

3. Co-Processing in Cement and Power Sectors

Co-processing of plastic waste as alternate fuel in cement kilns is emerging as a commercially scalable pathway that simultaneously addresses waste disposal and fossil fuel substitution objectives. The cement industry's willingness to accept plastic-derived fuel at defined calorific value thresholds is creating a stable offtake channel for mixed plastic waste streams that are difficult to recycle mechanically.

4. Informal-to-Formal Sector Integration and Social Enterprises

Non-governmental organizations, social enterprises, and corporate CSR programs are bridging informal waste pickers into formal collection and aggregation networks, improving feedstock consistency while generating documented livelihoods. These integration models are attracting blended finance from development institutions and improving the overall economics of organized recycling clusters across India.

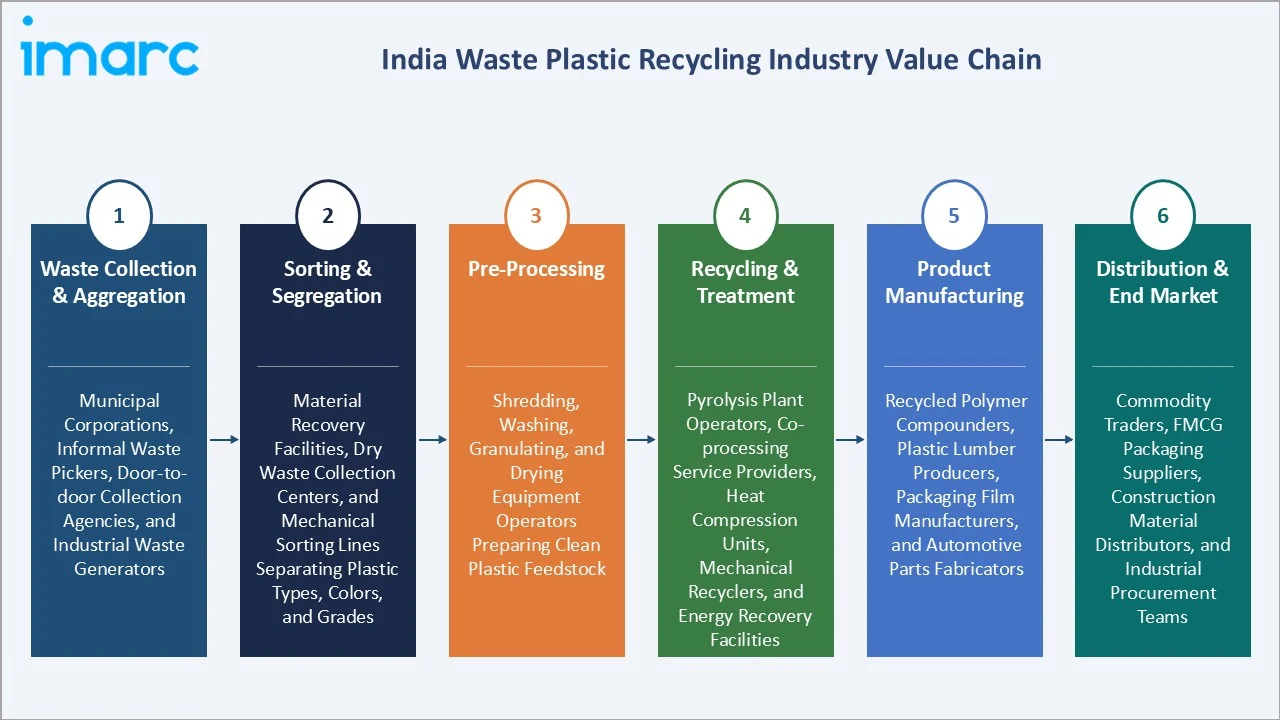

Industry Value Chain Analysis

The India waste plastic recycling value chain spans six stages from waste generation through end use product distribution. Pre-processing, recycling treatment, and product manufacturing capture the highest value-add, while collection and distribution determine the overall efficiency and inclusiveness of the market system.

|

Stage |

Key Players / Examples |

|

Waste Collection & Aggregation |

Municipal corporations, informal waste pickers, door-to-door collection agencies, and industrial waste generators constituting the primary feedstock sourcing layer |

|

Sorting & Segregation |

Material recovery facilities, dry waste collection centers, and mechanical sorting lines separating plastic types, colors, and grades for downstream processing |

|

Pre-Processing |

Shredding, washing, granulating, and drying equipment operators preparing clean plastic feedstock meeting quality specifications for recycling facilities |

|

Recycling & Treatment |

Pyrolysis plant operators, co-processing service providers, heat compression units, mechanical recyclers, and energy recovery facilities converting waste into usable outputs |

|

Product Manufacturing |

Recycled polymer compounders, plastic lumber producers, packaging film manufacturers, and automotive parts fabricators using recycled-content inputs |

|

Distribution & End Market |

Commodity traders, FMCG packaging suppliers, construction material distributors, and industrial procurement teams sourcing recycled-content materials |

Technology Landscape in the India Waste Plastic Recycling Industry

Pyrolysis and Thermal Depolymerization Systems

Modern pyrolysis facilities are deploying continuous-feed reactor designs with integrated gas-cleaning, oil-separation, and carbon black recovery systems. These advances are enabling operators to achieve higher fuel oil yields from mixed plastic feedstocks while meeting emission standards, improving both the economic viability and regulatory compliance profile of waste-to-energy investments.

Mechanical Recycling Automation and Quality Sorting

Artificial intelligence (AI)-enabled optical sorting systems and near-infrared spectroscopy are being deployed in material recovery facilities to improve plastic type identification accuracy, reduce manual sorting labor, and increase the purity of separated polymer streams entering downstream mechanical recycling.

Digital EPR Compliance and Traceability Platforms

Cloud-based EPR compliance platforms are integrating waste generator registrations, recycler certifications, and certificate issuance workflows into unified digital systems, improving accountability, reducing fraud, and enabling regulators to monitor compliance in real time across thousands of producers and recycling facilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Treatment |

Pyrolysis |

26.0% |

2025 |

|

Material |

High‑Density Polyethylene (HDPE) |

23.0% |

2025 |

|

Application |

Packaging |

40.0% |

2025 |

|

Recycling Process |

Mechanical |

78.0% |

2025 |

|

Region |

North India |

27.0% |

2025 |

By Treatment

Pyrolysis commands a 26.0% majority share in the treatment segment in 2025, driven by its ability to convert heterogeneous post-consumer plastic waste into fuel oil and chemical feedstocks. The technology benefits from growing offtake from refineries, industrial fuel users, and specialty chemical manufacturers, along with EPR recognition for fuel recovery outputs.

To access detailed market analysis, Request Sample

Co-processing at 20.8% in 2025 reflects its established role as a fuel and material substitute in cement production. Growing emphasis on reducing fossil fuel consumption and improving resource efficiency is further supporting its adoption across industrial facilities.

By Application

Packaging dominates with 40.0% share in 2025, reflecting the highest volume of recycled polymer consumption driven by FMCG brands meeting EPR targets and sustainability commitments on post-consumer recycled content in flexible and rigid packaging formats.

Construction at 20.6% is the second-largest application, utilizing recycled polymers in pipes, insulation boards, tiles, and structural profiles as performance and cost-competitive alternatives to virgin materials. Demand is further supported by growing infrastructure and building activity.

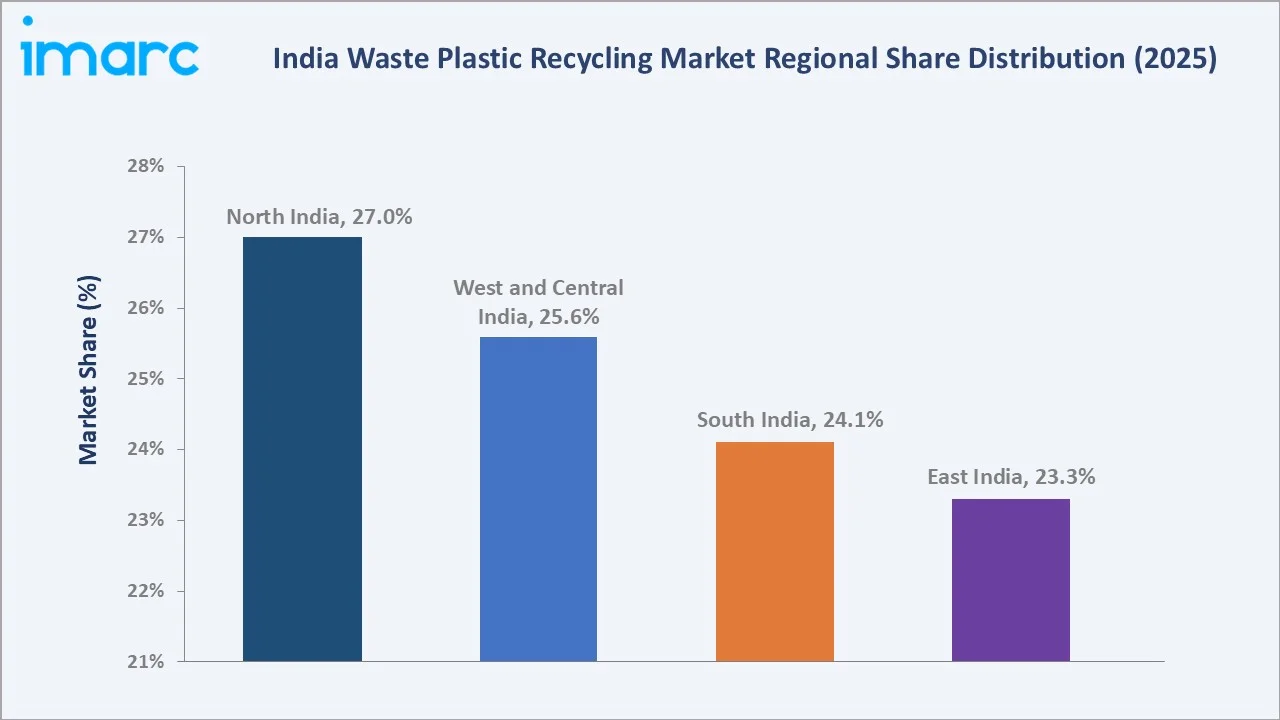

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

27.0% |

Dense urban waste generation, strong formal collection infrastructure, proximity to downstream packaging and automotive manufacturing clusters, and active EPR compliance by large brand owners |

|

West and Central India |

25.6% |

Large industrial waste streams from manufacturing hubs, established recycling clusters in Gujarat and Maharashtra, strong co-processing demand from cement sector, and high EPR activity |

|

South India |

24.1% |

Growing municipal solid waste volumes, expanding textile and packaging industry demand for recycled materials, state-level policy support for EPR, and rising investment in mechanical recycling capacity |

|

East India |

23.3% |

Emerging digital adoption in waste management, growing urban waste generation in Kolkata and Odisha corridors, expanding informal-to-formal integration, and rising demand from construction and packaging sectors |

North India at 27.0% in 2025 leads the regional landscape, driven by the high plastic waste density of Delhi-NCR, Uttar Pradesh, and Punjab, and the presence of well-structured collection networks feeding both formal and informal recyclers. Large brand owners headquartered in or operating major distribution hubs in the region are also driving EPR-linked collection investments.

West and Central India at 25.6% holds the second regional position, anchored by industrial waste streams from Gujarat and Maharashtra, active co-processing integration with cement plants, and strong EPR compliance activity by the dense FMCG and packaging manufacturing base in the region.

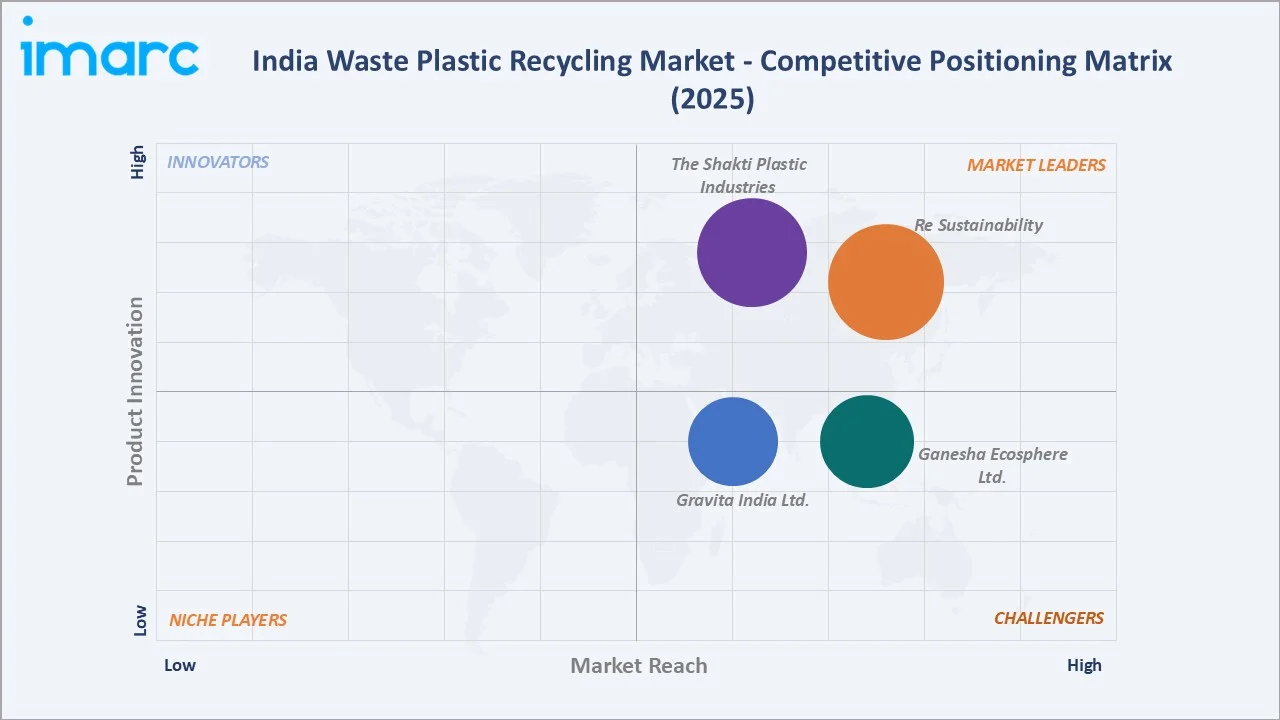

Competitive Landscape

The India waste plastic recycling market is moderately fragmented, with a mix of large integrated recyclers, specialized technology operators, and informal sector aggregators. Brand strength, technology capability, feedstock sourcing networks, and EPR certification status form the core competitive differentiators as the market transitions toward higher formalization and regulatory compliance.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Re Sustainability |

Re Sustainability |

Leader |

Integrated waste management and recycling services with broad plastic waste processing capability |

|

The Shakti Plastic Industries |

The Shakti Plastic Industries |

Leader |

Mechanical recycling and plastic granule production with established EPR compliance credentials |

|

Gravita India Ltd. |

Recycled Plastic Granules |

Challenger |

Multi-material recycling with focus on plastic granule production and circular economy solutions |

|

Ganesha Ecosphere Ltd. |

Go Rewise |

Leader |

Large-scale PET bottle recycling with diversified recycled polyester product portfolio |

Key players include Re Sustainability, The Shakti Plastic Industries, Gravita India Ltd., and Ganesha Ecosphere Ltd., among others.

Key Company Profiles

Re Sustainability

Re Sustainability is one of Asia’s leading integrated waste management and recycling companies. It provides a comprehensive range of environmental services including municipal, industrial, and biomedical waste management, plastic recycling, waste-to-energy operations, and EPR compliance solutions across India and international markets.

- Product Portfolio: Plastic waste collection, sorting, and recycling services; EPR compliance solutions for brand owners; waste-to-energy operations; hazardous and municipal solid waste management; and recycled plastic granule production.

- Recent Developments: Re Sustainability forged a strategic partnership with PolyCycl Private Limited in 2023 to develop a network of feedstock preparation facilities for chemical recycling of post-consumer flexible plastics across India, expanding its capability beyond mechanical recycling into chemical recycling pathways.

- Strategic Focus: Expanding plastic recycling capacity across India, deepening EPR compliance service offerings, and advancing strategic collaborations for chemical recycling and waste-to-energy solutions.

The Shakti Plastic Industries

The Shakti Plastic Industries is one of India's leading plastic waste recycling companies, engaged in the collection and recycling of post-consumer and industrial plastic waste into recycled granules and pellets, with operations across multiple states.

- Product Portfolio: Recycled plastic granules and pellets across various polymer grades and EPR compliance services for brand owner clients.

- Recent Developments: The company continues to invest in upgrading its recycling infrastructure and expanding its EPR compliance capabilities to serve a growing base of brand owner clients across India.

- Strategic Focus: Expanding post-consumer plastic waste collection network, improving recycled granule quality, and broadening EPR compliance service offerings.

Gravita India Ltd.

Gravita India Ltd. is a diversified recycling company engaged in the recycling of lead, aluminum, plastic, and rubber. The company operates plastic recycling facilities producing recycled polymer granules from post-consumer and industrial plastic waste, serving domestic and international customers.

- Product Portfolio: Recycled plastic granules and EPR consultancy services.

- Recent Developments: The company has been progressively expanding its plastic recycling capacity and strengthening its procurement network to support growing demand for recycled polymer products across domestic and export markets.

- Strategic Focus: Multi-material recycling with focus on plastic granule production and circular economy solutions across domestic and global markets.

Market Concentration Analysis

The India waste plastic recycling market is moderately fragmented, with the top players, including Re Sustainability, The Shakti Plastic Industries, Gravita India Ltd., and Ganesha Ecosphere Ltd., collectively accounting for a significant share of formal recycling activity through integrated collection, processing, and EPR service operations.

Barriers to entry include high capital costs for formal recycling facilities, the need for CPCB registration and EPR certification, feedstock sourcing capability across fragmented collection networks, and the ability to maintain consistent output quality for downstream industrial clients. These factors favor well-capitalized operators with established collection reach and regulatory credentials.

Consolidation is accelerating as formal EPR mandates create regulatory incentives for scale and certification, while technology costs for advanced recycling systems favor larger operators. Strategic partnerships between technology providers, waste generators, and brand owners are further concentrating market activity among organized players and reducing the share managed through fully informal channels.

Investment & Growth Opportunities

Fastest-Growing Segments

Pyrolysis at 26.0% share is the leading treatment pathway by volume and is growing faster than the overall market average, driven by fuel oil demand, chemical recycling investment, and EPR recognition for energy recovery outputs. Packaging at 40.0% of the application segment is the highest-volume end use, with growing EPR-driven post-consumer recycled content commitments from FMCG and retail brands accelerating demand for certified recycled polymers.

Emerging Markets

West and Central India at 25.6% and South India at 24.1% represent significant growth opportunities, with expanding industrial waste streams, growing EPR compliance activity, and increasing municipal solid waste management investment driving formal recycling capacity additions. Tier-2 and tier-3 cities across these regions represent largely untapped collection and processing opportunity for operators able to build localized infrastructure.

Venture & Investment Trends

Investment is concentrated in EPR compliance technology platforms, chemical recycling startups, and informal sector integration models that bridge waste pickers into formal supply chains. Development finance institutions and corporate sustainability funds are increasingly co-investing in recycling infrastructure projects aligned with India's Nationally Determined Contributions and circular economy policy goals.

Future Market Outlook (2026-2034)

The India waste plastic recycling market is forecast to expand from 11.92 Million Tons in 2025 to 25.88 Million Tons by 2034 at a CAGR of 9.00%, adding approximately 13.96 Million Tons in incremental annual recycling volume over the forecast period.

Four forces will shape the market through 2034: progressively tighter EPR compliance enforcement and expanding producer obligations; accelerating scale-up of pyrolysis, chemical recycling, and advanced mechanical processing technologies; deeper integration of informal waste networks into formal collection and aggregation systems; and growing industrial off-take demand for certified recycled polymers across packaging, construction, and automotive sectors.

By 2034, the India waste plastic recycling market is expected to be characterized by higher formalization, greater technology diversification across treatment pathways, and stronger alignment between EPR compliance requirements and recycling investment flows. Chemical recycling and pyrolysis are expected to collectively account for a higher combined share of treated volumes as mechanical recycling approaches practical yield limits for mixed post-consumer plastic fractions.

Research Methodology

Primary Research

Primary research included structured interviews with recycling facility operators, EPR compliance managers at brand owner companies, technology providers, urban local body officials, informal sector coordinators, and investment analysts, validating market sizing, treatment mix, regional demand patterns, and technology adoption trajectories.

Secondary Research

Secondary sources included Central Pollution Control Board publications and EPR portal reports, Ministry of Environment Forest and Climate Change notifications, Plastic Waste Management Rules and amendments, Ministry of Housing and Urban Affairs solid waste management data, and annual reports, press releases, and investor presentations from listed and private recycling operators.

Forecasting Models

Market forecasts used top-down and bottom-up models combining plastic waste generation estimates, recycling yield rates by technology, capacity utilization assumptions, policy transition scenarios, and end use demand projections. Scenario analysis addressed EPR enforcement pace, technology cost trajectories, and informal sector formalization rates.

India Waste Plastic Recycling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion, Million Tons |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Treatment Covered | Co-Processing, Heat Compression, Pyrolysis, Landfill, Incineration, Others |

| Material Covered | Poly Vinyl Chloride (PVC), Low-Density Polyethylene (LDPE), High-Density Polyethylene (HDPE), Polyethylene Terephthalate (PET), Polypropylene (PP), Acrylonitrile Butadiene Styrene (ABS), Others |

| Application Covered | Packaging, Construction, Textile, Automotive, Others |

| Recycling Process Covered | Mechanical, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Re Sustainability, The Shakti Plastic Industries, Gravita India Ltd., Ganesha Ecosphere Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Waste Plastic Recycling Market Report

The India waste plastic recycling market was volumed at 11.92 Million Tons in 2025, driven by EPR mandates, rising plastic waste generation, and growing end use demand for recycled polymers.

The market is projected to grow at a CAGR of 9.00% from 2026 to 2034, reaching 25.88 Million Tons, driven by technology scaling, EPR enforcement, and circular economy policy support.

Pyrolysis leads at 26.0% in 2025, driven by its ability to process mixed and difficult-to-recycle plastic waste while generating valuable fuel and chemical outputs.

Packaging dominates at 40.0% in 2025, driven by FMCG and retail brands' EPR compliance obligations and growing demand for post-consumer recycled content in flexible and rigid packaging formats.

North India commands 27.0% in 2025, fueled by dense urban waste generation, well-developed collection networks, and strong EPR compliance activity from large brand owners and packaging manufacturers.

Leading players include Re Sustainability, The Shakti Plastic Industries, Gravita India Ltd., and Ganesha Ecosphere Ltd.

EPR mandates producers to collect and recycle plastic packaging waste, directly driving formal recycling investment, feedstock demand, and EPR certificate market activity across India.

Key challenges include feedstock contamination from mixed waste streams, fragmented informal collection infrastructure, high capital costs for advanced recycling technologies, and uneven EPR enforcement across states.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)