India Water Treatment Chemicals Market Size, Share, Trends and Forecast by Type, End User, and Region, 2026-2034

India Water Treatment Chemicals Market Size, Share, Trends & Forecast (2026-2034)

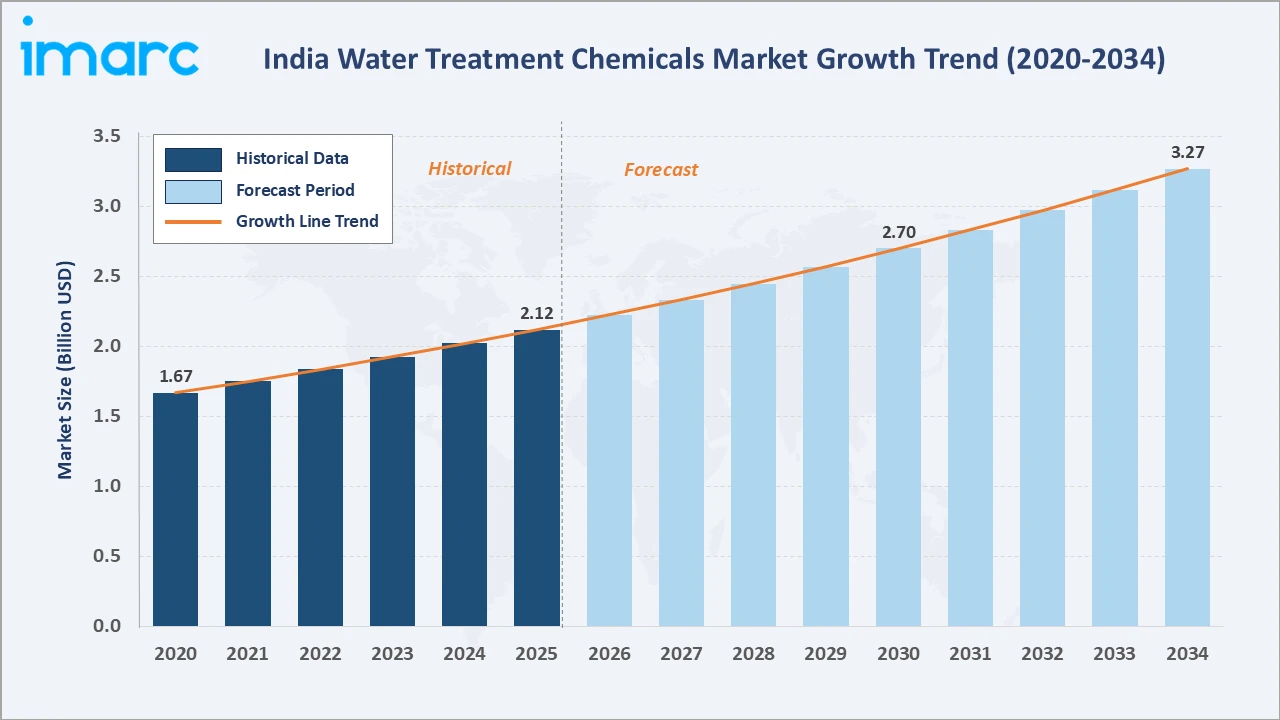

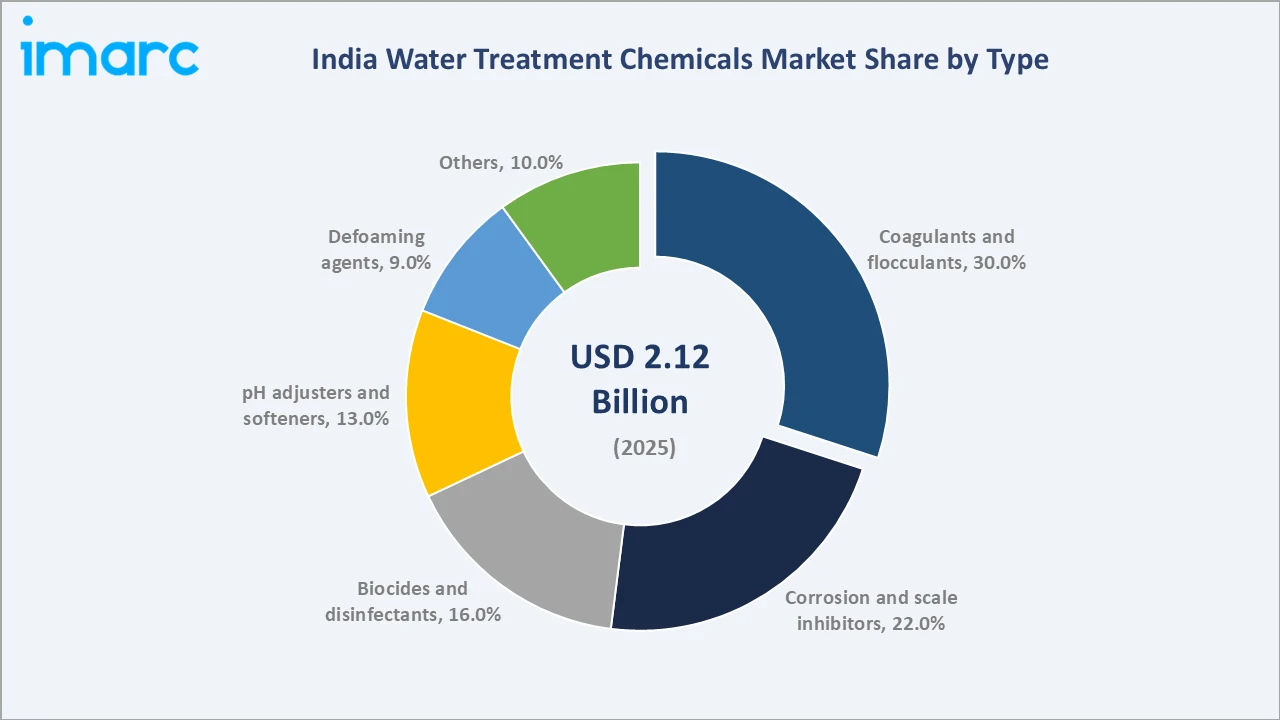

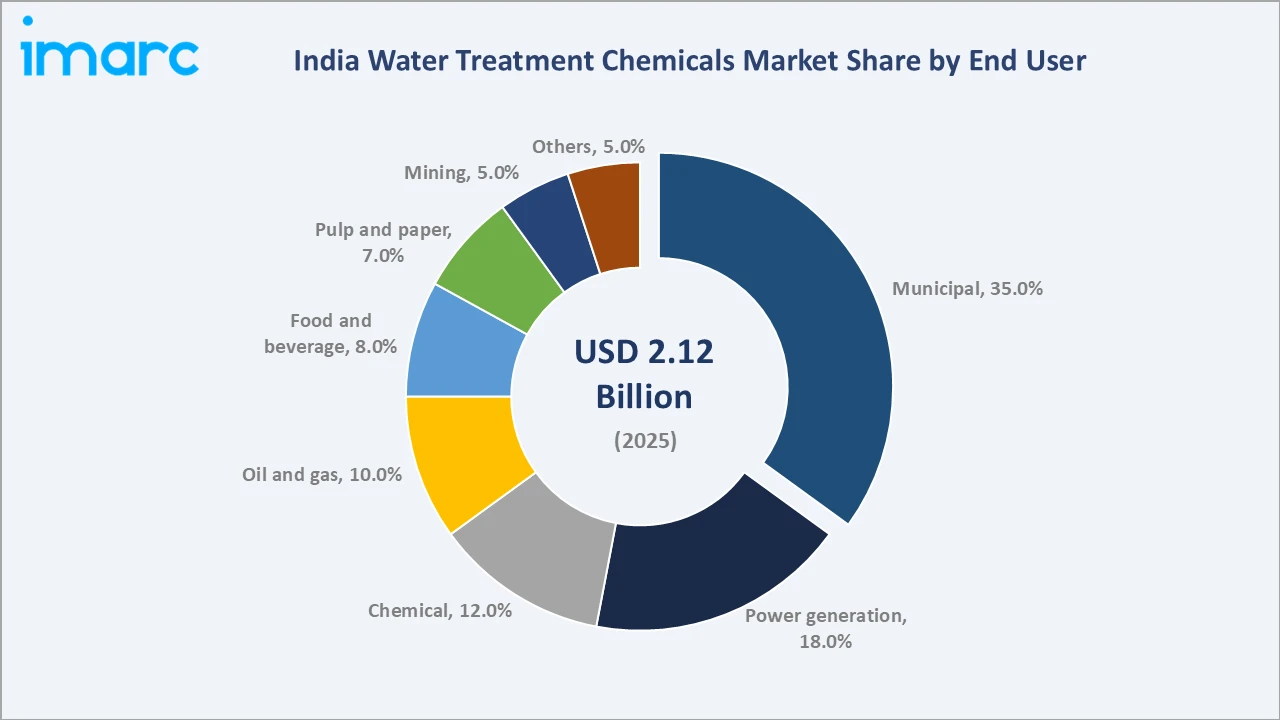

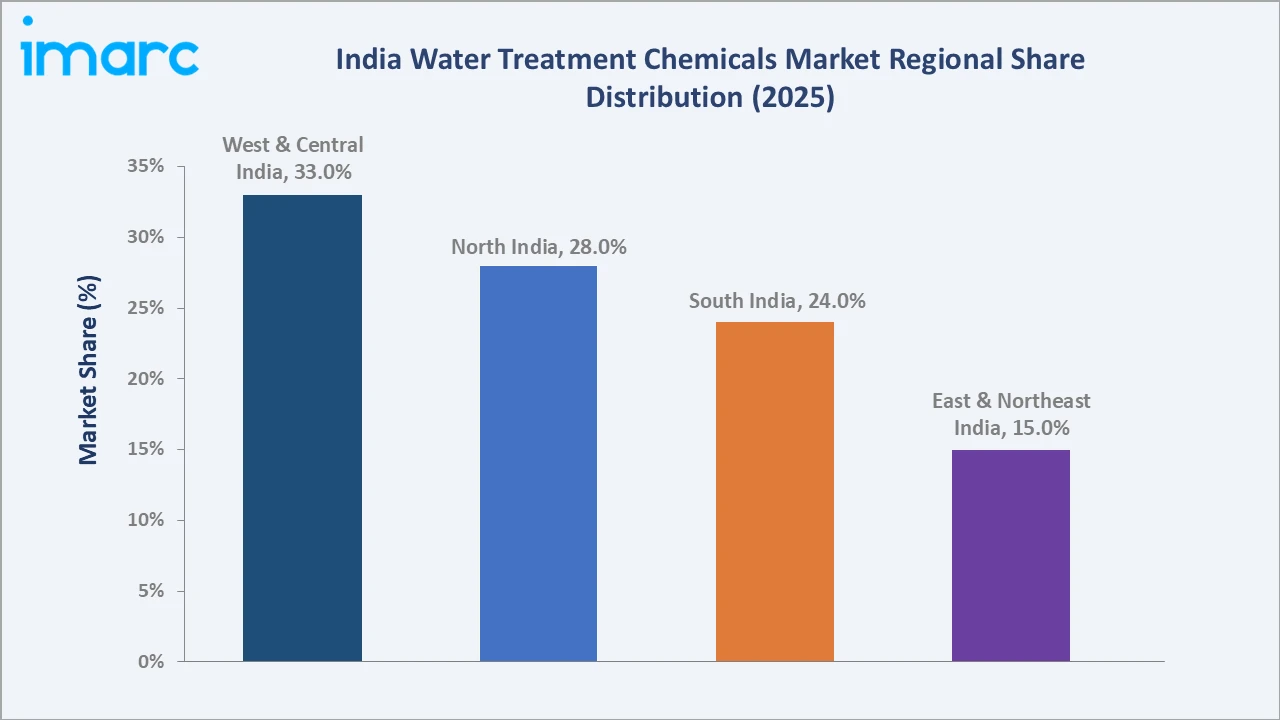

The India water treatment chemicals market reached USD 2.12 Billion in 2025 and is projected to reach USD 3.27 Billion by 2034, growing at a CAGR of 4.92% during 2026-2034. The market is driven by rapid industrialization, accelerating urbanization, and growing demand for clean water across municipal and industrial sectors. Stringent government regulations on wastewater disposal, expanding power generation capacity, and rising environmental awareness are propelling demand for advanced treatment solutions. Coagulants and Flocculants dominate with a 30.0% share. Municipal end users lead at 35.0%. West and Central India commands the largest regional share at 33.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.12 Billion |

|

Forecast Market Size (2034) |

USD 3.27 Billion |

|

CAGR (2026-2034) |

4.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Coagulants & Flocculants (30.0%, 2025) |

|

Dominant End User |

Municipal (35.0%, 2025) |

|

Leading Region |

West & Central India (33.0%, 2025) |

The India water treatment chemicals market expanded from USD 1.67 Billion in 2020 to USD 2.12 Billion in 2025, anchored at USD 2.70 Billion in 2030, and forecast to reach USD 3.27 Billion by 2034. This consistent growth trajectory reflects India's accelerating water infrastructure modernization, stringent effluent discharge norms, and industrial capacity additions across power, chemical, and food processing sectors.

To get more information on this market, Request Sample

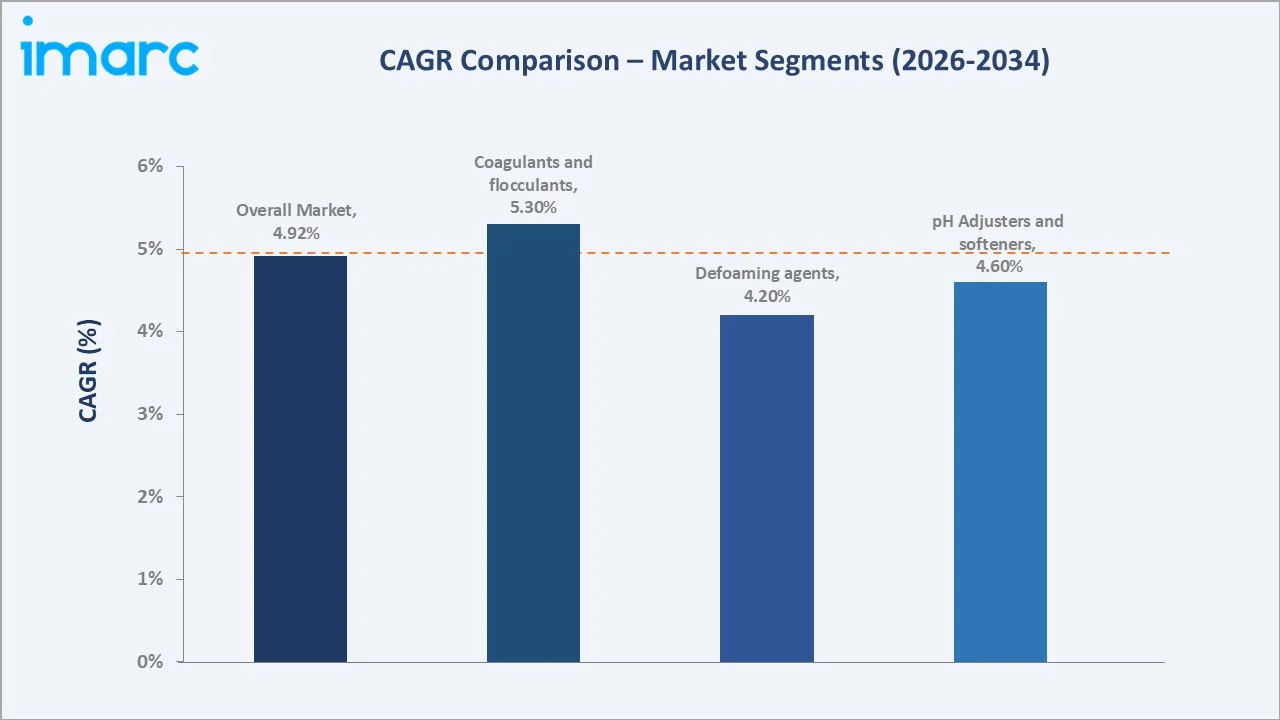

Coagulants and flocculants sustain leadership at a ~5.3% CAGR through their indispensable role in removing suspended solids and colloidal matter across municipal and industrial treatment plants. Biocides and disinfectants are the fastest-growing type segment at ~5.5% CAGR as strict microbial control norms tighten across food processing and pharmaceutical sectors.

Executive Summary

India water treatment chemicals market, valued at USD 2.12 Billion in 2025, reflects the nation's intensifying water infrastructure modernization amid rapid industrialization and urban expansion. The market is poised to reach USD 3.27 Billion by 2034, registering a CAGR of 4.92% through the forecast period. Key growth drivers include escalating water scarcity, stringent effluent discharge mandates under the Environment Protection Act, and government-led programs such as Jal Jeevan Mission and AMRUT 2.0, which are channeling significant investments into municipal water supply and sewage treatment networks.

Coagulants and flocculants represent the dominant product type at 30.0% market share in 2025, driven by their essential role in primary and secondary treatment stages across municipal and industrial applications. Corrosion and scale inhibitors account for 22.0%, supported by thermal power plant expansion. Municipal end users lead at 35.0%, reflecting government investments targeting universal potable water access. Power generation follows at 18.0%, underpinned by thermal capacity additions. The market is projected to anchor at USD 2.70 Billion in 2030 before reaching USD 3.27 Billion by 2034.

West and Central India commands 33.0% regional share in 2025, driven by heavy-industry concentration including petrochemicals, textiles, and coastal desalination projects. North India holds 28.0%, supported by manufacturing hubs and Jal Jeevan Mission investments. The competitive landscape is moderately fragmented, comprising multinational corporations alongside established domestic players competing on product innovation, sustainability, and distribution reach.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Coagulants & Flocculants - 30.0% share (2025) |

|

Largest Segment (End User) |

Municipal - 35.0% market share (2025) |

|

Leading Region |

West & Central India - 33.0% (2025) |

|

Market Opportunity |

Expansion of ZLD-compliant industrial treatment; rising desalination chemical demand; green & bio-based formulations for sustainable municipalities |

Key Analytical Observations Supporting the Above Data:

- Coagulants & Flocculants at 30.0%: These chemicals are indispensable for solid-liquid separation. Municipal authorities predominantly use iron- and aluminium-based coagulants, while polymer-based flocculants gain traction in industrial settings. Approval of new sewage treatment plants under AMRUT 2.0 reinforces segment dominance through 2034.

- Municipal at 35.0%: Government initiatives supplying piped drinking water to rural and urban households have dramatically increased chemical demand. Expansion of new sewage treatment facilities and rehabilitation of outdated plants drive large-scale coagulant, disinfectant, and pH adjuster consumption.

- West & Central India at 33.0%: Industrial density in Maharashtra and Gujarat - encompassing petrochemicals, textiles, and pharmaceuticals - generates substantial wastewater volumes. Coastal desalination projects and major industrial corridors sustain consistent demand for diverse chemical formulations.

- Power Sector at 18.0%: India's ongoing thermal and renewable energy capacity additions require rigorous boiler feed water treatment and cooling tower maintenance, creating sustained demand for corrosion inhibitors, oxygen scavengers, and scale preventatives.

- Green Chemicals Transition: Regulatory scrutiny on chemical sludge generation is accelerating transition toward bio-based coagulants, plant-derived flocculants, and non-toxic disinfection alternatives, opening a fast-growing specialty sub-segment.

India Water Treatment Chemicals Market Overview

India water treatment chemicals market encompasses a broad spectrum of chemical formulations including coagulants, flocculants, corrosion inhibitors, scale inhibitors, biocides, disinfectants, pH adjusters, defoamers, and specialty chemicals deployed across municipal and industrial water and wastewater treatment systems. The market serves diverse end-use sectors - municipal utilities, power generation, oil and gas, chemical manufacturing, food processing, pulp and paper, and mining - each with distinct treatment chemistry requirements.

The macroeconomic environment is shaped by India's accelerating industrial output, rapid urbanization adding approximately 15 million urban residents annually, and increasing pressure on freshwater resources amid declining groundwater tables. Government programs including Jal Jeevan Mission, AMRUT 2.0 (urban infrastructure modernization with an outlay exceeding INR 2.99 lakh crore, and the National River Conservation Plan collectively mandate expanded sewage treatment infrastructure and elevated treatment chemical consumption throughout the forecast period.

Market Dynamics

To evaluate market opportunities, Request Sample

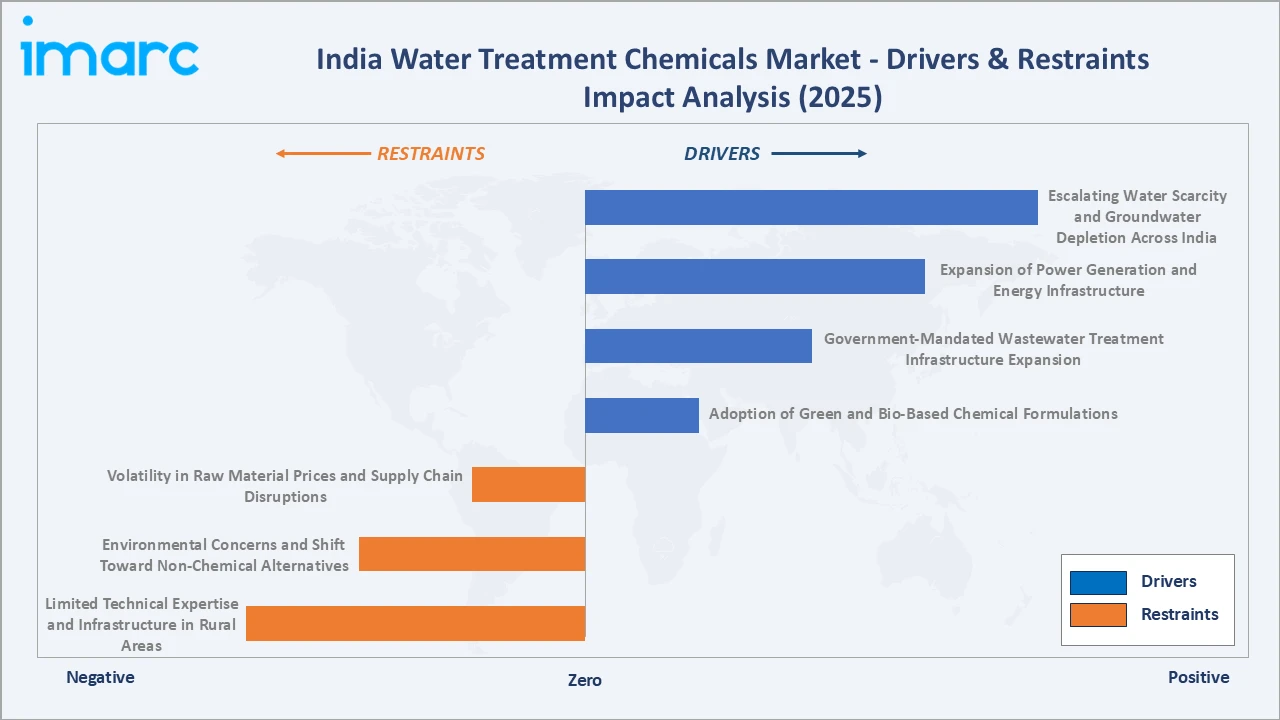

Market Drivers

- Escalating Water Scarcity and Groundwater Depletion Across India: India confronts an intensifying water crisis characterized by declining groundwater tables and diminishing freshwater reserves. According to the Central Ground Water Board (CGWB), approximately 10.8% of India's assessed groundwater blocks are classified as over-exploited. This scarcity compels industries and municipal authorities to invest heavily in wastewater recycling and reuse programs, directly increasing demand for treatment chemicals enabling effective purification of reclaimed water. In May 2025, the Bangalore Water Supply and Sewerage Board (BWSSB), in collaboration with the World Bank, launched a INR 1,323.46 crore wastewater management and reuse project, underscoring rising institutional demand for treatment solutions.

- Expansion of Power Generation and Energy Infrastructure: India's continuous power generation capacity expansion - encompassing thermal, nuclear, and renewable energy projects - is driving significant growth in water treatment chemical consumption. Thermal power plants are among the largest industrial water consumers, requiring rigorous chemical treatment for cooling systems, boiler operations, and steam generation. In July 2025, the Ministry of Environment, Forest and Climate Change cleared expansion plans for coal-fired power plants by Adani Power, NLC India, and GMR Group with combined additional capacity exceeding 2,000 MW, amplifying demand for corrosion inhibitors, oxygen scavengers, and antiscalants.

- Government-Mandated Wastewater Treatment Infrastructure Expansion: Stringent regulatory frameworks under the Environment Protection Act, 1986, Water (Prevention and Control of Pollution) Act, and zero liquid discharge (ZLD) mandates from the Central Pollution Control Board (CPCB) are accelerating adoption of treatment chemicals. AMRUT 2.0 targets construction of sewage treatment plants in 500 cities. In September 2025, Pimpri Chinchwad Municipal Corporation received approval for two new sewage treatment plants along the Indrayani River under AMRUT 2.0, reinforcing chemical demand for coagulation and flocculation in primary treatment stages.

Market Restraints

- Volatility in Raw Material Prices and Supply Chain Disruptions: The market faces significant restraint from fluctuations in prices of key raw materials including aluminium sulfate, polyacrylamide, chlorine, and specialty polymers. Price volatility impacts production costs and margins for chemical manufacturers, often resulting in unpredictable pricing for municipal and industrial buyers. Supply chain disruptions stemming from geopolitical factors and logistical bottlenecks further exacerbate procurement challenges, particularly for import-dependent specialty chemical segments.

- Environmental Concerns and Shift Toward Non-Chemical Alternatives: Growing regulatory scrutiny on chemical sludge generation, potential toxicity of residual treatment byproducts, and ecological consequences of chemical discharge is prompting some industrial operators to evaluate alternative membrane-based and UV treatment technologies. This substitution risk - albeit gradual - limits demand growth for conventional coagulant and disinfectant formulations in specific industrial segments adopting advanced physical treatment methods.

Market Opportunities

- Adoption of Green and Bio-Based Chemical Formulations: The market is witnessing a notable transition toward environmentally sustainable and biodegradable chemical formulations. In February 2026, researchers at IIT Bhilai developed an eco-friendly bio-derived hydrogel effective in absorbing toxic dyes and pollutants from contaminated water. This shift creates a premium sub-segment of green water treatment chemicals where manufacturers can differentiate through bio-based coagulants and plant-derived flocculants commanding price premiums above conventional products.

- Rising Desalination Capacity Across Coastal States: India's coastal states - particularly in Tamil Nadu, Gujarat, and Andhra Pradesh - are investing in desalination plants to augment drinking water supply. In May 2025, the Defence Research and Development Organisation (DRDO) announced development of a high-pressure polymeric membrane for seawater desalination. Each desalination facility demands specialized antiscalants, membrane cleaners, corrosion inhibitors, and biocides, creating incremental specialty chemical demand.

Market Challenges

- Limited Technical Expertise and Infrastructure in Rural Areas: A significant portion of water treatment demand originates from rural and semi-urban areas where qualified technical manpower and advanced treatment infrastructure remain limited. The absence of certified operators capable of managing chemical dosing systems constrains utilization of treatment chemicals in these regions, creating a structural gap between chemical supply availability and on-ground adoption rates.

- Rapid Technological Transition Toward Membrane and Digital Systems: The growing integration of membrane-based treatment technologies and digital precision dosing platforms is transforming treatment plant operations. While membrane systems create new demand for specialty antiscalants and cleaning agents, they simultaneously reduce consumption of conventional coagulants in facilities transitioning to direct membrane filtration. This technology substitution dynamic necessitates product portfolio adaptation for established chemical manufacturers.

Emerging Market Trends

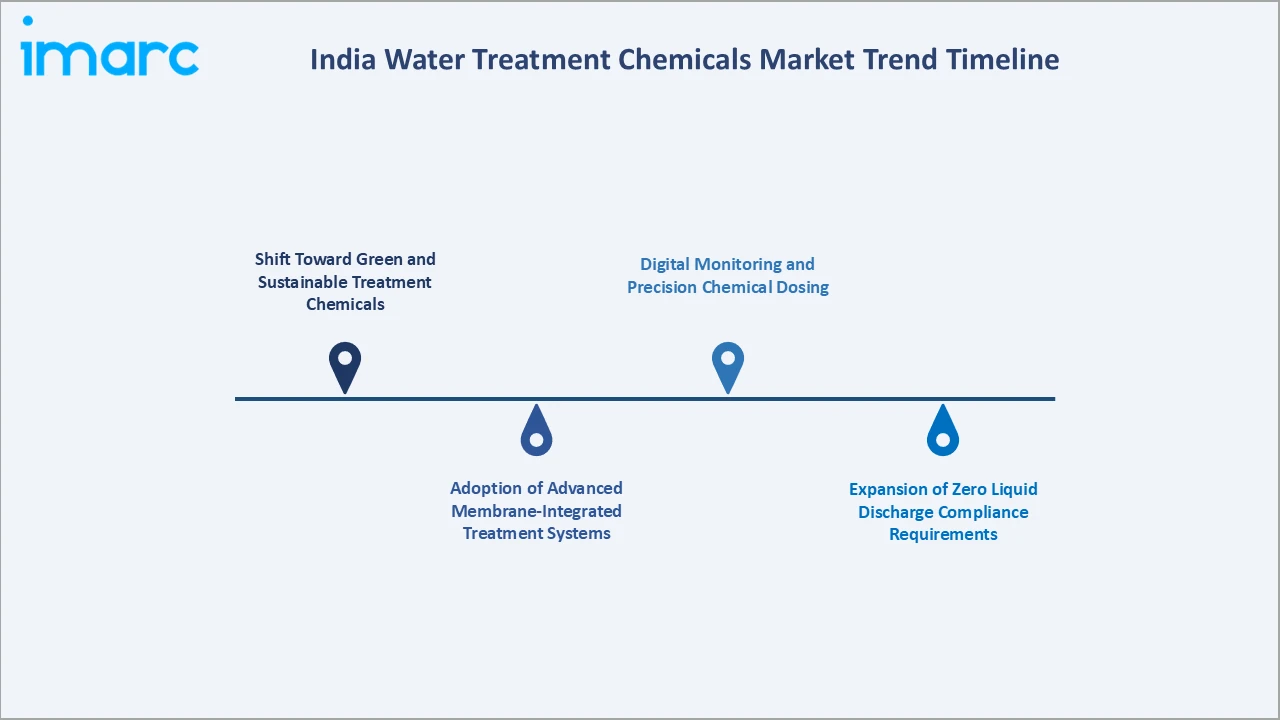

1. Shift Toward Green and Sustainable Treatment Chemicals

India's water treatment chemicals market is witnessing a notable transition toward environmentally sustainable and biodegradable formulations. Industries and municipal bodies are increasingly prioritizing bio-based coagulants, plant-derived flocculants, and non-toxic disinfection alternatives. Regulatory scrutiny on chemical discharge quality and growing corporate sustainability commitments are accelerating this shift, creating a premium segment where manufacturers can command higher margins through differentiated green product portfolios.

2. Adoption of Advanced Membrane-Integrated Treatment Systems

A significant trend is the growing integration of membrane-based treatment technologies including ultrafiltration, nanofiltration, and reverse osmosis with conventional chemical dosing systems. Industries across power generation, pharmaceuticals, and textiles are deploying these hybrid approaches to achieve higher water purity standards, demanding specialized antiscalants, membrane cleaners, and conditioning chemicals. In May 2025, DRDO announced development of a high-pressure polymeric membrane for seawater desalination, exemplifying technology advancement supporting chemical demand evolution.

3. Digital Monitoring and Precision Chemical Dosing

The incorporation of digital monitoring systems and automated precision dosing technologies is emerging as a transformative trend. Water treatment facilities are deploying sensor-based monitoring platforms, real-time water quality analytics, and SCADA systems to optimize chemical usage and reduce wastage by 15-25%. In January 2026, Noida Authority announced rollout of a cloud-based water monitoring system with real-time sensor data management, demonstrating rising institutional adoption of smart water management technologies.

4. Expansion of Zero Liquid Discharge Compliance Requirements

Stringent ZLD mandates from CPCB are compelling industries including textiles, dyes, pharmaceuticals, and distilleries to implement comprehensive wastewater treatment systems. ZLD-compliant treatment trains require advanced chemical regimens including high-performance antiscalants, membrane cleaners, and evaporator treatment chemicals, creating structurally higher chemical intensity demand per unit of industrial production.

5. Rising Private Sector Engagement in Water Infrastructure

Growing private and international investment in India's water infrastructure is driving expansion of treatment capacity and chemical adoption. In February 2026, SUEZ secured a landmark EUR 456 million concession contract to modernize the water supply system in Salem, Tamil Nadu - its largest project in India to date. Such large-scale private engagements accelerate deployment of advanced treatment solutions and expand the addressable market for premium-grade treatment formulations.

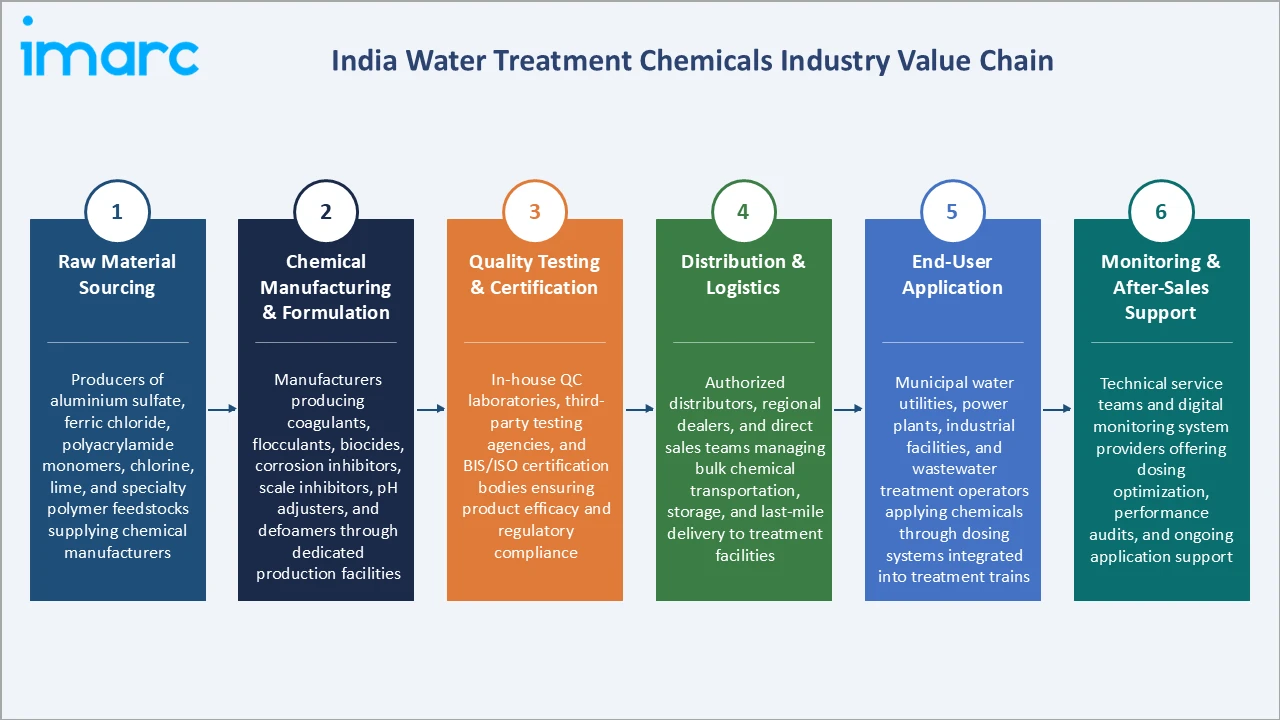

Industry Value Chain Analysis

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Producers of aluminium sulfate, ferric chloride, polyacrylamide monomers, chlorine, lime, and specialty polymer feedstocks supplying chemical manufacturers |

|

Chemical Manufacturing & Formulation |

Manufacturers producing coagulants, flocculants, biocides, corrosion inhibitors, scale inhibitors, pH adjusters, and defoamers through dedicated production facilities |

|

Quality Testing & Certification |

In-house QC laboratories, third-party testing agencies, and BIS/ISO certification bodies ensuring product efficacy and regulatory compliance |

|

Distribution & Logistics |

Authorized distributors, regional dealers, and direct sales teams managing bulk chemical transportation, storage, and last-mile delivery to treatment facilities |

|

End-User Application |

Municipal water utilities, power plants, industrial facilities, and wastewater treatment operators applying chemicals through dosing systems integrated into treatment trains |

|

Monitoring & After-Sales Support |

Technical service teams and digital monitoring system providers offering dosing optimization, performance audits, and ongoing application support |

The chemical manufacturing and formulation stage represents the highest value-addition point in the India water treatment chemicals value chain. Leading manufacturers are investing in R&D capabilities to develop next-generation formulations offering improved efficacy, environmental compatibility, and reduced chemical oxygen demand. Distribution and logistics constitute a critical competitive differentiator in India's geographically diverse market.

Technology Landscape in the India Water Treatment Chemicals Industry

Advanced Coagulation and Flocculation Chemistries

Next-generation coagulation technologies are transitioning from conventional inorganic salts - aluminium sulfate and ferric chloride - toward pre-polymerized coagulants including polyaluminium chloride (PAC) and polyferric sulfate (PFS). These advanced formulations deliver superior turbidity removal at lower dosing rates across a wider pH range, reducing sludge generation volumes by 20-40% compared to traditional coagulants. High-charge polyelectrolytes and dual-polymer flocculation systems are increasingly deployed in industrial wastewater applications requiring compliance with stringent effluent standards.

Membrane-Compatible Chemical Formulations

The growing adoption of ultrafiltration, nanofiltration, and reverse osmosis membranes across industrial and municipal facilities is driving specialized demand for membrane-compatible antiscalants, cleaning agents, and biocide formulations. Antiscalant technology has evolved from threshold inhibitors to crystal modification and dispersion agents offering efficacy against calcium carbonate, calcium sulfate, silica, and barium sulfate scaling at concentrations as low as 2-5 ppm. Oxidizing biocides including chlorine dioxide and peracetic acid are replacing chlorine in membrane-integrated systems.

Digital Dosing and Real-Time Water Quality Monitoring

Precision chemical dosing systems integrating sensor arrays, automated control valves, and AI-driven dosing optimization algorithms are replacing manual chemical addition practices in advanced treatment facilities. In January 2026, Noida Authority announced deployment of cloud-based water monitoring systems enabling real-time quality tracking. These digital platforms optimize chemical consumption by 15-25%, reduce operational costs, and minimize overdosing incidents, creating demand for technical-grade chemical formulations compatible with automated dosing infrastructure.

Green and Bio-Based Chemical Innovation

Bio-derived coagulants from natural sources including Moringa oleifera seeds, chitosan, and tannin-based extracts are gaining research attention as sustainable alternatives to inorganic coagulants. Enzyme-based biocidal formulations and organic peroxide disinfectants are entering industrial trial phases. In February 2026, researchers at IIT Bhilai developed a bio-derived hydrogel demonstrating effective absorption of toxic dyes and pollutants, representing the innovation pipeline entering commercial consideration across the India market.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Coagulants & Flocculants |

30.0% |

2025 |

|

End User |

Municipal |

35.0% |

2025 |

|

Region |

West & Central India |

33.0% |

2025 |

By Type

Coagulants and flocculants lead at 30.0% in 2025. This segment encompasses aluminium- and iron-based inorganic coagulants and synthetic polymer flocculants that are indispensable for solid-liquid separation across municipal sewage treatment plants, industrial effluent treatment systems, and drinking water purification facilities. Their dominance reflects the essential and non-substitutable nature of primary treatment chemistry requirements across the broadest range of end-user applications.

To access detailed market analysis, Request Sample

Corrosion and scale inhibitors command 22.0%, driven primarily by thermal power plant cooling water and boiler feed water treatment requirements. Biocides and disinfectants account for 16.0%, supported by stringent microbial control mandates in municipal drinking water treatment. pH adjusters and softeners represent 13.0%, essential for maintaining treatment chemistry effectiveness. Defoaming agents hold 9.0%, serving paper and pulp, food processing, and chemical manufacturing applications. Others including specialty membrane-compatible chemicals account for 10.0%.

By End User

Municipal applications lead at 35.0% in 2025. The municipal segment reflects government programs targeting universal potable water access, river cleaning mandates, and urban sewage treatment expansion under Jal Jeevan Mission and AMRUT 2.0 schemes. Municipalities deploy the broadest portfolio of treatment chemicals across intake water clarification, disinfection, distribution system corrosion control, and wastewater treatment stages.

Power generation accounts for 18.0%, reflecting large-volume chemical requirements for cooling tower treatment, boiler water conditioning, and condensate polishing across India's extensive thermal power infrastructure. Chemical manufacturing at 12.0% represents process water and effluent treatment requirements. Oil and gas contributes 10.0%, supported by produced water treatment applications. Food and beverage at 8.0% and pulp and paper at 7.0% represent process-critical water purity requirements. Mining at 5.0% and others contribute the remaining share.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

West & Central India |

33.0% |

Driven by heavy industries including chemicals, petrochemicals, and textiles generating large wastewater volumes; coastal desalination initiatives and major industrial corridors. |

|

North India |

28.0% |

Extensive manufacturing hubs, rapid urbanization in major metropolitan areas, and significant government investments in river cleaning and sewage treatment infrastructure. |

|

South India |

24.0% |

Strong industrial base spanning automotive, electronics, food processing, and pharmaceuticals; proactive adoption of ZLD mandates and coastal desalination expansion. |

|

East & Northeast India |

15.0% |

Emerging market fueled by expanding mining operations, thermal power generation, and rising government focus on rural water supply infrastructure. |

West and Central India's 33.0% regional dominance reflects Maharashtra and Gujarat's industrial density. The region hosts India's largest petrochemical, textile, and pharmaceutical industrial clusters that collectively generate the highest volumes of process wastewater per geographic unit, sustaining the country's most concentrated demand base for industrial water treatment chemicals.

North India's 28.0% market share is anchored by manufacturing corridors in Uttar Pradesh, Haryana, and Punjab, alongside significant Jal Jeevan Mission investments targeting river basins through the National Mission for Clean Ganga (NMCG). South India at 24.0% reflects a strong automotive, electronics, and pharmaceutical industrial base, complemented by progressive ZLD adoption. East and Northeast India, holding 15.0%, represents the market's fastest-growing regional opportunity as expanding mining activity and thermal power development accelerate chemical adoption from a comparatively lower penetration baseline.

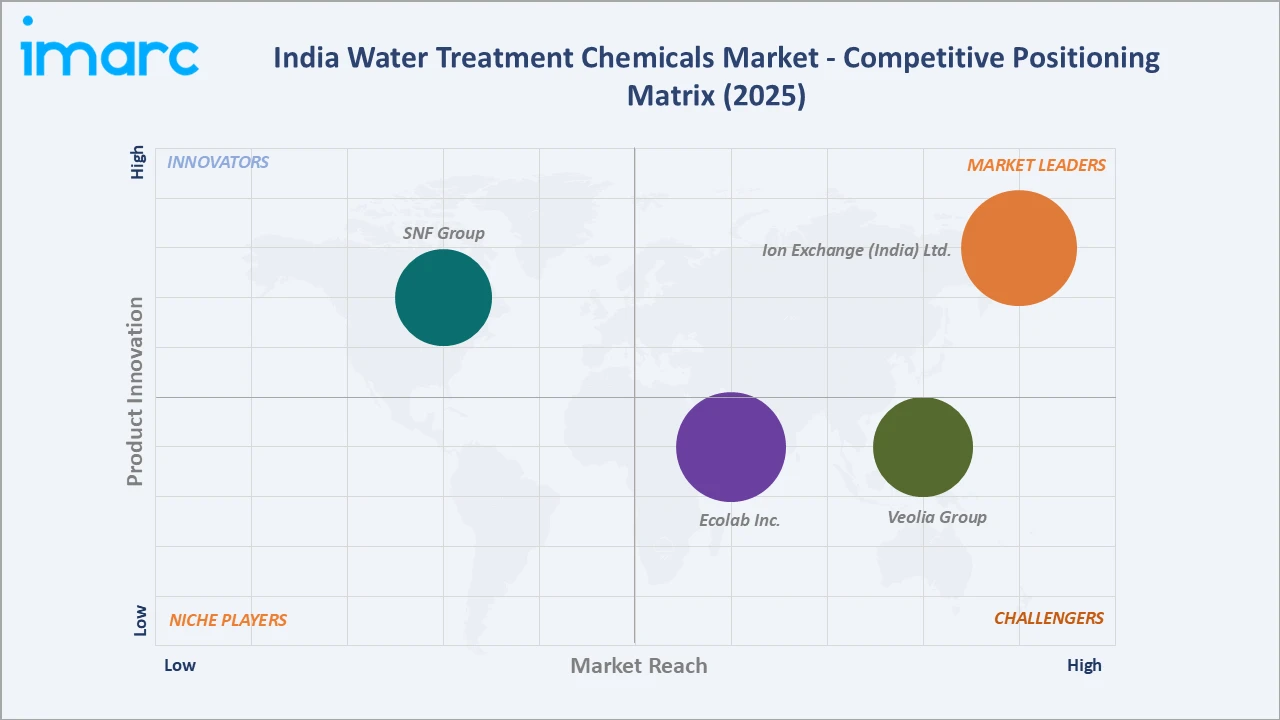

Competitive Landscape

The India water treatment chemicals market features a moderately fragmented competitive landscape comprising large multinational corporations and established domestic manufacturers. Multinational players leverage global R&D capabilities, broad product portfolios, and technical service expertise, while domestic manufacturers compete through localized production, competitive pricing, and proximity to key industrial end users.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Ion Exchange (India) Ltd. |

Ion exchange resins, RO chemicals, antiscalants |

Market Leader |

Largest domestic water treatment company with pan-India distribution and strong municipal client base |

|

Veolia Group |

Hydrex water treatment chemicals |

Strong Challenger |

Operates as Veolia Water Technologies & Solutions; integrated treatment solutions across municipal and industrial sectors with strong technical service support |

|

Ecolab Inc. |

Biocides, corrosion & scale inhibitors, specialty chemicals |

Strong Challenger |

Operates through Nalco Water; leading position in industrial water treatment for power, food & beverage, and hospitality sectors |

|

SNF Group |

Polyacrylamide flocculants, coagulants |

Innovator |

Operating locally as SNF Flopam India; a prominent polyacrylamide manufacturer serving India's expanding industrial flocculant demand |

Market participants compete on product quality, technological innovation, environmental compliance, pricing strategies, and distribution breadth. Leading players are investing in R&D to introduce next-generation formulations delivering improved efficacy, sustainability credentials, and compatibility with advanced membrane and digital treatment systems.

Key Company Profiles

Veolia Group

Veolia Group, which operates Veolia Water Technologies & Solutions, is a prominent player in water treatment, offering comprehensive chemical, equipment, and digital solutions across industrial and municipal sectors.

- Key Products: Hydrex water treatment chemicals

- Recent Developments: In February 2026, Veolia secured two 15-year O&M contracts and deploys advanced technologies for Mumbai’s largest and most critical water treatment plants, strengthening the city’s long-term water security.

- Strategic Focus: Strengthening of Hydrex portfolio, green and sustainable chemistry, integrated equipment-chemical strategy, leveraging the Hubgrade digital platform for remote diagnostics, and others.

Ecolab Inc.

Ecolab Inc., operating primarily through its industrial water and process management division, Nalco Water, has a significant presence in India's industrial water treatment chemicals market. The company serves power generation, food and beverage, hospitality, and pharmaceutical sectors with specialized corrosion and scale inhibitor programs, biocide systems, and cooling water treatment formulations.

- Key Products: Corrosion inhibitors, scale inhibitors, biocides, oxidizing disinfectants, and specialty process chemicals for industrial water and wastewater treatment.

- Strategic Focus: Leveraging digital water management and precision chemistry programs to deepen customer relationships in power, food processing, and pharmaceutical sectors; expanding geographic reach into Tier-2 industrial clusters across India.

Market Concentration Analysis

India water treatment chemicals market is moderately fragmented. No single company commands a dominant share across all product types and end-user segments. Multinational corporations including Veolia Group, Ecolab Inc., SNF Group, and Ion Exchange (India) Ltd., lead in technical sophistication and project-based municipal contracts.

The power sector sub-segment exhibits comparatively higher concentration, with the major players collectively serving the majority of India's thermal power plant chemical requirements.

Market concentration is evolving through two dynamics: multinational players pursuing large-scale municipal concession-linked chemical supply agreements creating multi-year volume commitments, and domestic players expanding product portfolios through backward integration and specialty chemical joint ventures. The entry of specialized international players in membrane-compatible and green chemistry niches is gradually increasing fragmentation in premium segments despite consolidation in the commodity chemical sub-market.

Investment & Growth Opportunities

Highest Growth Segments

The biocides and disinfectants segment exhibits the highest growth trajectory at ~5.5% CAGR through tightening microbial control standards across food processing and pharmaceutical water systems. Membrane-compatible specialty chemicals - including antiscalants and membrane cleaners - are the fastest-growing specialty sub-segment as India's RO-based treatment capacity expands across industrial and municipal applications. Green and bio-based coagulant formulations represent an emerging premium sub-category growing significantly faster than the overall market, supported by corporate ESG commitments and regulatory pressure on chemical discharge quality.

Emerging Investment Opportunities

India's desalination capacity expansion along coastal Tamil Nadu, Gujarat, and Andhra Pradesh creates a high-value specialty chemical opportunity. Desalination facilities require precision antiscalants, biocides, and membrane cleaners in technically demanding specifications, creating recurring high-margin chemical supply relationships. The ZLD compliance chemical market - serving textile, dyeing, distillery, and pharmaceutical industrial clusters mandated by CPCB - represents a structurally higher chemical intensity segment where per-unit treatment chemical consumption exceeds conventional programs by a factor of 2-3x.

Investment Themes

- Green chemistry R&D and bio-based formulation development for premium differentiation in municipal and ESG-committed industrial clients seeking sustainable treatment solutions compliant with India's evolving discharge quality norms.

- Strategic manufacturing facility establishment in West and Central India's industrial corridor to serve the highest-concentration industrial chemical demand geography at reduced logistics cost and with supply reliability advantages.

- Digital water management platform integration with chemical supply programs, following the Ecolab ECOLAB3D model, to create differentiated service relationships with large industrial clients adopting Industry 4.0 water management frameworks.

- Municipal treatment concession partnerships, following the SUEZ-Salem model, to secure long-term chemical supply commitments linked to treatment plant capacity expansions under Jal Jeevan Mission and AMRUT 2.0 investments.

Future Market Outlook (2026-2034)

India water treatment chemicals market is projected to grow from USD 2.12 Billion in 2025 to USD 3.27 Billion by 2034, delivering a 4.92% CAGR over the forecast period. The market's anchor value of USD 2.70 Billion in 2030 represents a structural milestone reflecting the combined impact of government-mandated infrastructure expansion, industrial capacity additions, and adoption of advanced treatment chemistries across established end-user segments.

Three structural forces define market growth through 2034. First, India's continued industrial expansion - particularly in power generation, chemical manufacturing, food processing, and pharmaceuticals - sustains rising per-unit water treatment chemical consumption as production scale increases and discharge standards tighten. Second, government infrastructure investment through Jal Jeevan Mission, AMRUT 2.0, and the National Mission for Clean Ganga collectively create mandatory demand for expanded treatment capacity and associated chemical procurement across hundreds of new and upgraded treatment facilities.

Third, technological transition toward membrane-based treatment, ZLD-compliant systems, and precision dosing platforms is reshaping the chemical demand mix - reducing conventional coagulant consumption in advanced facilities while creating higher-value specialty chemical demand for antiscalants, membrane cleaners, and biocides. This portfolio premiumization trend is expected to sustain revenue growth above volume growth rates, supporting market value expansion through the 2026-2034 forecast horizon.

Research Methodology

Primary Research

Primary research comprised structured interviews with India water treatment chemicals industry stakeholders, including Technical Directors, Business Development Heads, Plant Managers at major treatment facilities, procurement managers at municipal utilities and industrial end users, and independent industry consultants. Interviews covered product demand trends, pricing dynamics, regulatory impact, and technology adoption patterns across end-user segments and geographies.

Secondary Research

Secondary research encompassed India water treatment chemical import-export statistics from the Directorate General of Commercial Intelligence and Statistics (DGCIS), Central Pollution Control Board (CPCB) compliance reports, Central Ground Water Board (CGWB) groundwater assessment data, company annual reports and investor presentations, Ministry of Jal Shakti program documentation, AMRUT 2.0 project data, and peer-reviewed journals. Over 60 secondary sources were reviewed and cross-validated.

Forecasting Models

Market revenue forecasts were developed through a bottom-up segmentation model: individual end-user sector water treatment chemical consumption per unit of industrial output multiplied by sector-specific output growth projections, summed across Type categories to produce total market revenue by year. Historical (2020-2025) data was validated against import-export statistics and company revenue disclosures. Forecast values reflect regulatory scenario analysis incorporating CPCB discharge standard tightening trajectories and government infrastructure investment schedules.

India Water Treatment Chemicals Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, Ph Adjusters and Softeners, Defoaming Agents, Others |

| End Users Covered | Municipal, Power, Oil and Gas, Mining, Chemical, Food and Beverage, Pulp and Paper, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Ion Exchange (India) Ltd., Veolia Group, Ecolab Inc., SNF Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Water Treatment Chemicals Market Report

The India water treatment chemicals market reached USD 2.12 Billion in 2025, driven by industrial expansion, government water infrastructure investments, stringent effluent discharge regulations, and rising demand for advanced treatment solutions across municipal and industrial end-user sectors.

The India water treatment chemicals market is projected to grow at a CAGR of 4.92% during 2026-2034, reaching USD 3.27 Billion by 2034, supported by continued industrial expansion, ZLD compliance mandates, and government-led municipal treatment infrastructure modernization programs.

Coagulants and flocculants lead at 30.0% market share in 2025, reflecting their essential role in primary treatment across municipal sewage treatment plants and industrial effluent systems requiring solid-liquid separation and suspended solids removal.

The municipal segment leads at 35.0% market share in 2025, driven by government investments in piped water supply, sewage treatment plant expansion under AMRUT 2.0, and water quality compliance requirements under Jal Jeevan Mission infrastructure programs.

West and Central India leads with 33.0% market share in 2025, supported by the highest concentration of heavy industries including petrochemicals, textiles, and pharmaceuticals in Maharashtra and Gujarat, and coastal desalination expansion initiatives.

The India water treatment chemicals market is projected to reach USD 2.70 Billion in 2030, reflecting steady expansion through industrial growth, government infrastructure investments, and rising ZLD compliance requirements across textile, chemical, and power generation sectors.

Key drivers include escalating water scarcity and groundwater depletion, expansion of India's power generation capacity, Jal Jeevan Mission and AMRUT 2.0 government infrastructure investments, and mandatory ZLD compliance for industrial facilities under CPCB mandates.

Key challenges include raw material price volatility for aluminium sulfate and polyacrylamide feedstocks, limited technical expertise in rural treatment facilities constraining chemical adoption, and growing competition from non-chemical membrane treatment alternatives.

Emerging trends include a shift toward green and bio-based chemical formulations, adoption of membrane-integrated treatment requiring specialty antiscalants and biocides, digital precision dosing systems optimizing chemical consumption by 15-25%, and rising private sector engagement through large concession contracts.

Leading companies include Ion Exchange (India) Ltd., Veolia Group, Ecolab Inc., and SNF Group, among other domestic and multinational participants.

The India water treatment chemicals market was valued at USD 1.67 Billion in 2020, growing to USD 2.12 Billion in 2025 at approximately 4.9% CAGR during 2020-2025, driven by industrial expansion and government water infrastructure investments.

Key growth opportunities include desalination chemical specialties for India's expanding coastal desalination plants, ZLD-compliant treatment chemical programs for mandated industrial sectors, green and bio-based formulation premiumization, and municipal concession-linked long-term chemical supply contracts under Jal Jeevan Mission and AMRUT 2.0 programs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)